Pathik Shah

Last Updated: 04/17/2026

Protect your business with reliable and effective AML strategies with AML UAE.

Key Highlights

- Accountants and auditors become DNFBPs when they carry out covered activities under Article 3 of Cabinet Decision No. 134 of 2025, such as real estate transactions, managing client funds or securities, managing bank, savings or securities accounts, organising contributions for the creation or management of companies, and creating, operating or managing legal persons or arrangements.

- The Ministry of Economy and Tourism (MoET) is the designated AML/CFT supervisory authority for accountants and auditors operating in the UAE mainland and commercial free zones.

- Federal Decree-Law No. 10 of 2025 (replacing Federal Decree-Law No. 20 of 2018) and Cabinet Resolution No. 134 of 2025 set the baseline AML/CFT obligations; MoET has issued the DNFBP Guidelines of September 2025 and the Supplemental Guidance for Auditors of June 2019 to explain sector expectations.

- The 2024 UAE National Risk Assessment flags audit and accountancy services as exposed to trade-based money laundering, shell company abuse and sanctions evasion risks.

Independent accountants and auditors in the UAE become subject to anti-money laundering (AML) obligations when they prepare for or carry out specified financial transactions for clients. They are designated non-financial businesses and professions (DNFBPs) supervised by the Ministry of Economy and Tourism (MoET). This guide covers the AML regulations for accountants in UAE mainland and commercial free zones, including the Federal Decree-Law No. (10) of 2025 framework, sector-specific MoET guidance, and practical compliance expectations.

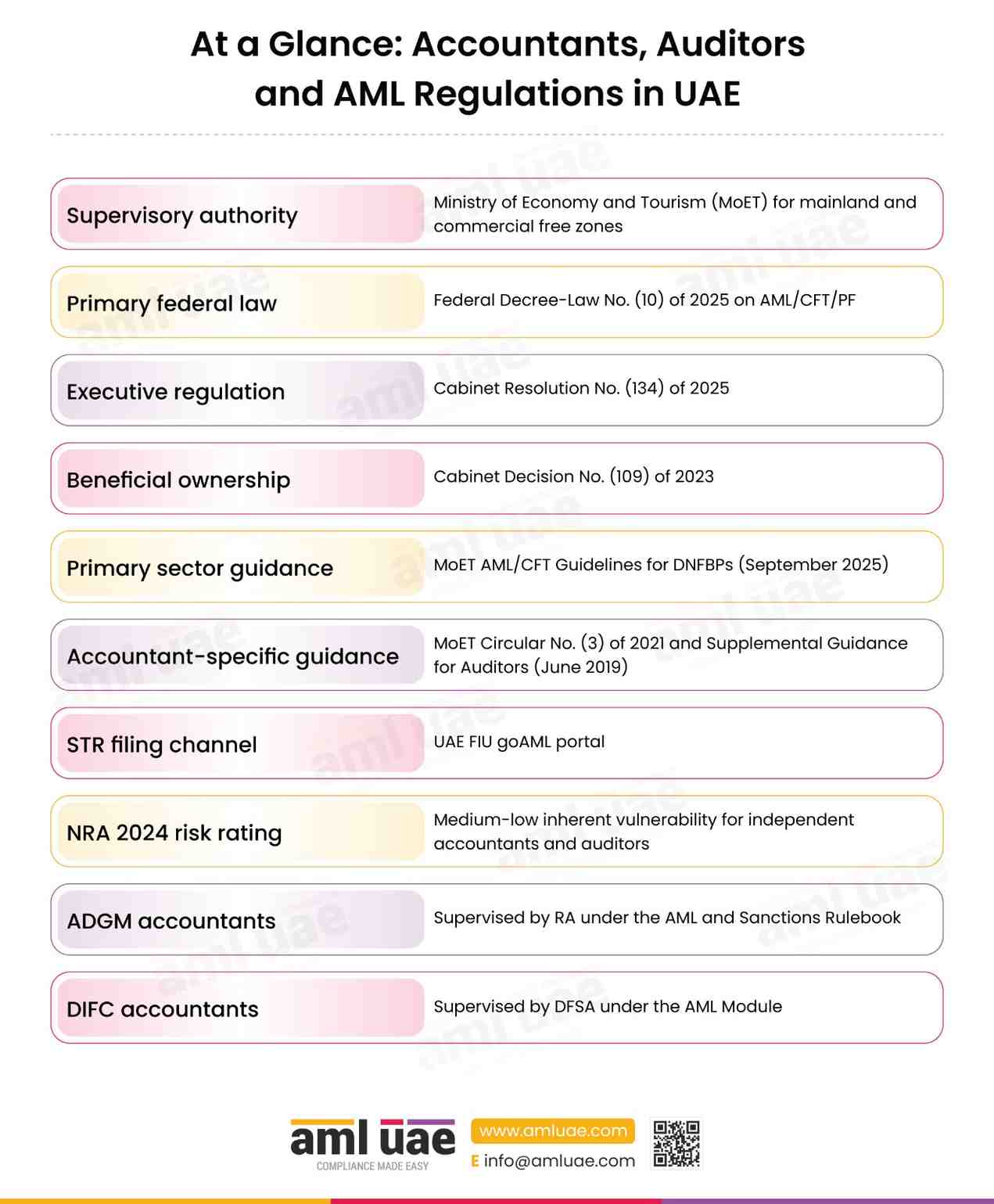

At a Glance: Accountants, Auditors and AML Regulations in UAE

Supervisory authority | Ministry of Economy and Tourism (MoET) for mainland and commercial free zones |

Primary federal law | Federal Decree-Law No. (10) of 2025 on AML/CFT/PF |

Executive regulation | Cabinet Resolution No. (134) of 2025 |

Beneficial ownership | Cabinet Decision No. (109) of 2023 |

Primary sector guidance | MoET AML/CFT Guidelines for DNFBPs (September 2025) |

Accountant-specific guidance | MoET Circular No. (3) of 2021 and Supplemental Guidance for Auditors (June 2019) |

STR filing channel | UAE FIU goAML portal |

NRA 2024 risk rating | Medium-low inherent vulnerability for independent accountants and auditors |

ADGM accountants | Supervised by RA under the AML and Sanctions Rulebook |

DIFC accountants | Supervised by DFSA under the AML Module |

When is an accountant or auditor a DNFBP?

An accountant or auditor becomes a designated non-financial business or profession (DNFBP) under UAE law when they prepare for or carry out financial transactions on behalf of clients, such as buying or selling real estate, managing client money or securities, managing bank accounts, organising contributions for the creation of companies, or creating and managing legal persons or arrangements.

Independent accountants and auditors occupy a critical gatekeeper position in the UAE anti-money laundering (AML) and counter-financing of terrorism (CFT) framework. The moment an accountant or auditor prepares for or carries out specified financial transactions on behalf of a client, the firm becomes a reporting entity for AML compliance for audit firms UAE purposes.

The UAE has placed independent accountants and auditors within the DNFBP category under Federal Decree-Law No. (10) of 2025, Cabinet Resolution No. (134) of 2025, and a layered suite of sector-specific guidance and circulars. The 2024 National Risk Assessment rates accountants and auditors as a medium-low risk DNFBP sector while acknowledging specific vulnerabilities tied to the profession’s gatekeeper role in financial transactions. DNFBP-wide rules set the baseline; sector-specific guidance layers on top.

This article covers the AML/CFT framework applicable to accountants and auditors operating in the UAE mainland and commercial free zones supervised by the MoET. For the broader DNFBP pillar, see our AML Regulations for DNFBPs in UAE guide. For the primary federal legislation, visit our guide to AML laws in UAE and the dedicated federal AML laws and executive regulations page. If your firm operates in a financial free zone, refer to AML Regulations in ADGM or AML Regulations in DIFC respectively.

Scope of this page

This page covers accountants and auditors supervised by MoET in UAE mainland and commercial free zones. For accountants in ADGM and DIFC, refer to the dedicated jurisdiction pages. Lawyers, notaries, trust and corporate service providers have their own sector pages and are only referenced here where covered activities overlap.

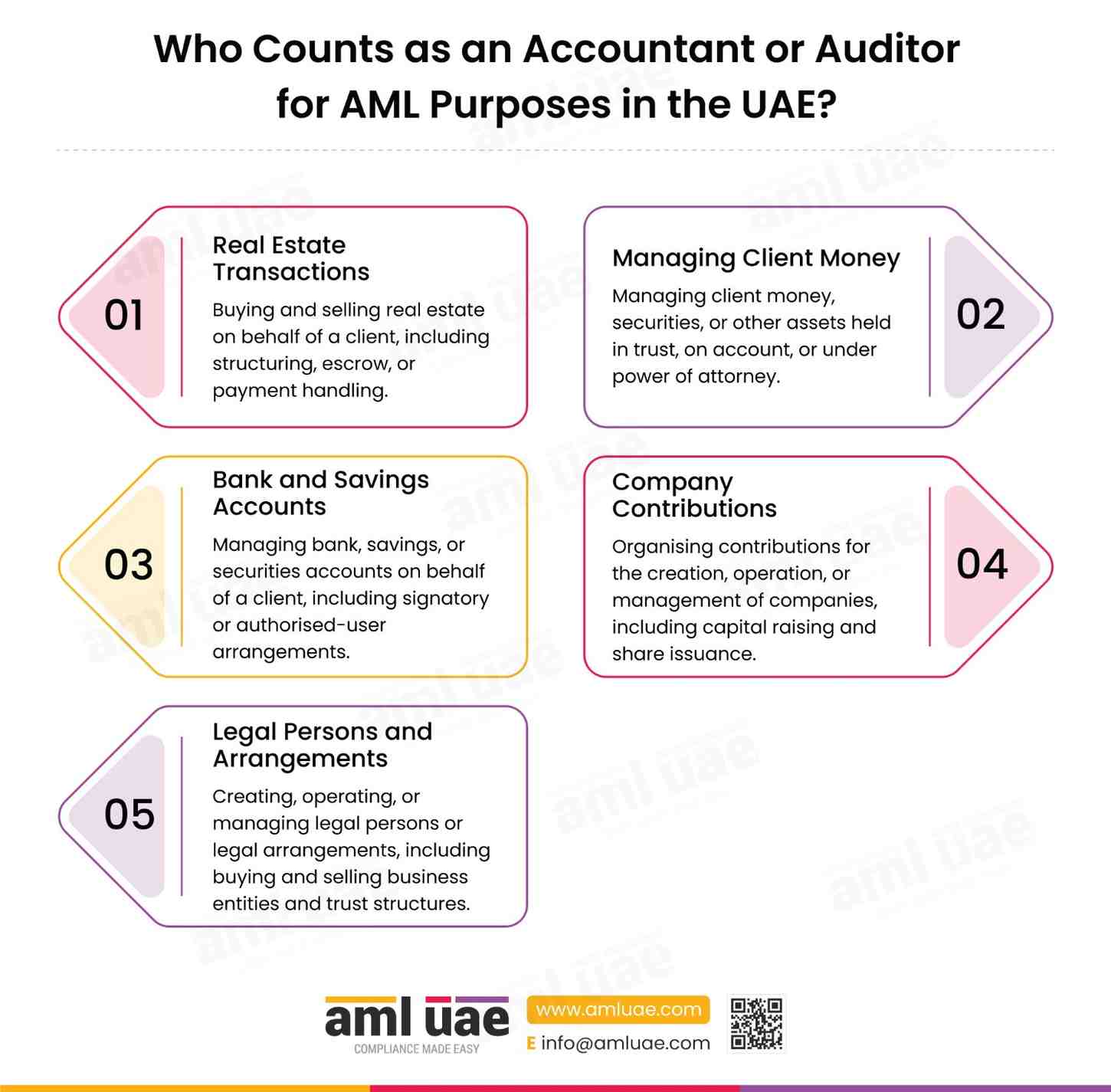

Who Counts as an Accountant or Auditor for AML Purposes in the UAE?

Not every accounting professional is a DNFBP. Under Federal Decree-Law No. (10) of 2025 and its Executive Regulations (Cabinet Resolution No. (134) of 2025), accountants and auditors are classified as DNFBPs only when they prepare for or carry out specific financial transactions for their clients.

The covered activities that bring an accountant or auditor into the AML perimeter are the following five transactions, mirrored from the Financial Action Task Force (FATF) definition:

1. Real Estate Transactions

Buying and selling real estate on behalf of a client, including structuring, escrow, or payment handling.

2. Managing Client Money

Managing client money, securities, or other assets held in trust, on account, or under power of attorney.

3. Bank and Savings Accounts

Managing bank, savings, or securities accounts on behalf of a client, including signatory or authorised-user arrangements.

4. Company Contributions

Organising contributions for the creation, operation, or management of companies, including capital raising and share issuance.

5. Legal Persons and Arrangements

Creating, operating, or managing legal persons or legal arrangements, including buying and selling business entities and trust structures.

Key legal test:

If an independent accountant, external auditor or audit firm performs one or more of these covered activities for a client in the ordinary course of business, the full AML/CFT compliance regime under Federal Decree-Law No. 10 of 2025 and its Executive Regulations applies.

These covered activities are specified in Federal Decree-Law No. (10) of 2025 and Cabinet Resolution No. (134) of 2025, as reflected in the AML/CFT Guidelines for DNFBPs (September 2025) published by the Ministry of Economy and Tourism (MoET), and align with FATF Recommendation 22. It is the nature of the financial transaction being prepared or carried out that determines whether AML obligations apply for a given engagement.

The Supplemental Guidance for Auditors (June 2019) further clarifies the scope by explaining how the auditing function intersects with AML obligations. Auditors who, in the course of their professional work, encounter indicators of money laundering, terrorist financing, or other financial crimes are expected to take appropriate action, including filing suspicious transaction reports (STRs) via the goAML portal operated by the UAE Financial Intelligence Unit. This is an overlay obligation: even where a routine audit engagement places the firm inside the DNFBP perimeter and the statutory reporting duty under Federal Decree-Law No. (10) of 2025 is triggered.

Engagement-level analysis is therefore essential. Firms should map each client relationship and engagement type to the covered-activity list, document the reasoning, and refresh the assessment whenever the scope of work changes. Cross-link this analysis with the lawyers, notaries and legal professionals page where accountant-lawyer joint engagements on corporate structuring or real estate are common.

AML Supervisory Authority for Accountants and Auditors in UAE

The Ministry of Economy and Tourism (MoET) is the designated AML/CFT supervisory authority for independent accountants and auditors operating in the mainland UAE and in commercial free zones (excluding ADGM and DIFC). MoET is responsible for day-to-day supervision, desk-based reviews, on-site inspections, thematic reviews, and enforcement action.

MoET supervises four DNFBP categories: real estate agents and brokers, dealers in precious metals and stones (DPMS), independent accountants and auditors, and trust and corporate service providers (TCSPs). For a consolidated view of all supervisors, see our AML supervisory authorities in UAE page.

During inspections, MoET follows a structured process. It sends a formal notification letter; conducts the on-site visit; completes structured inspection checklists covering governance, business-wide risk assessment, CRA, CDD, sanctions screening, STR filing, record keeping, and training; and issues a findings report. Firms are expected to remediate any identified deficiencies within the timelines set by the Ministry. Failure to do so may result in administrative sanctions under Cabinet Resolution No. (71) of 2024, which can include written warnings, fines up to AED 5 million, licence suspension, or licence revocation.

Jurisdictional comparison at a glance

Federal Decree-Law No. (10) of 2025 applies across the entire UAE. The operational supervisor, rulebook, and penalty regime differ by jurisdiction.

| Dimension | Mainland & Commercial Free Zone | ADGM | DIFC |

|---|---|---|---|

| Federal Decree-Law No. (10) of 2025 applies | Yes | Yes | Yes |

| Primary supervisor | Ministry of Economy and Tourism (MoET) | Registration Authority (RA) | Dubai Financial Services Authority (DFSA) |

| Operational rulebook | MoET AML/CFT Guidelines for DNFBPs (September 2025) and MoET circulars | FSRA AML and Sanctions Rulebook (AML) | DFSA AML, CTF and Sanctions Module |

| Reporting channel | goAML operated by the UAE Financial Intelligence Unit | goAML operated by the UAE Financial Intelligence Unit | goAML operated by the UAE Financial Intelligence Unit |

| Scope of this guide | Covered in full on this page | Refer to AML Regulations in ADGM | Refer to AML Regulations in DIFC |

Unsure whether an engagement makes your firm a DNFBP?

AML UAE helps accounting and audit firms triage engagements, scope covered-activity exposure, and build a proportionate AML/CFT compliance programme aligned with MoET expectations.

AML Regulations Applicable to Accountants and Auditors in UAE

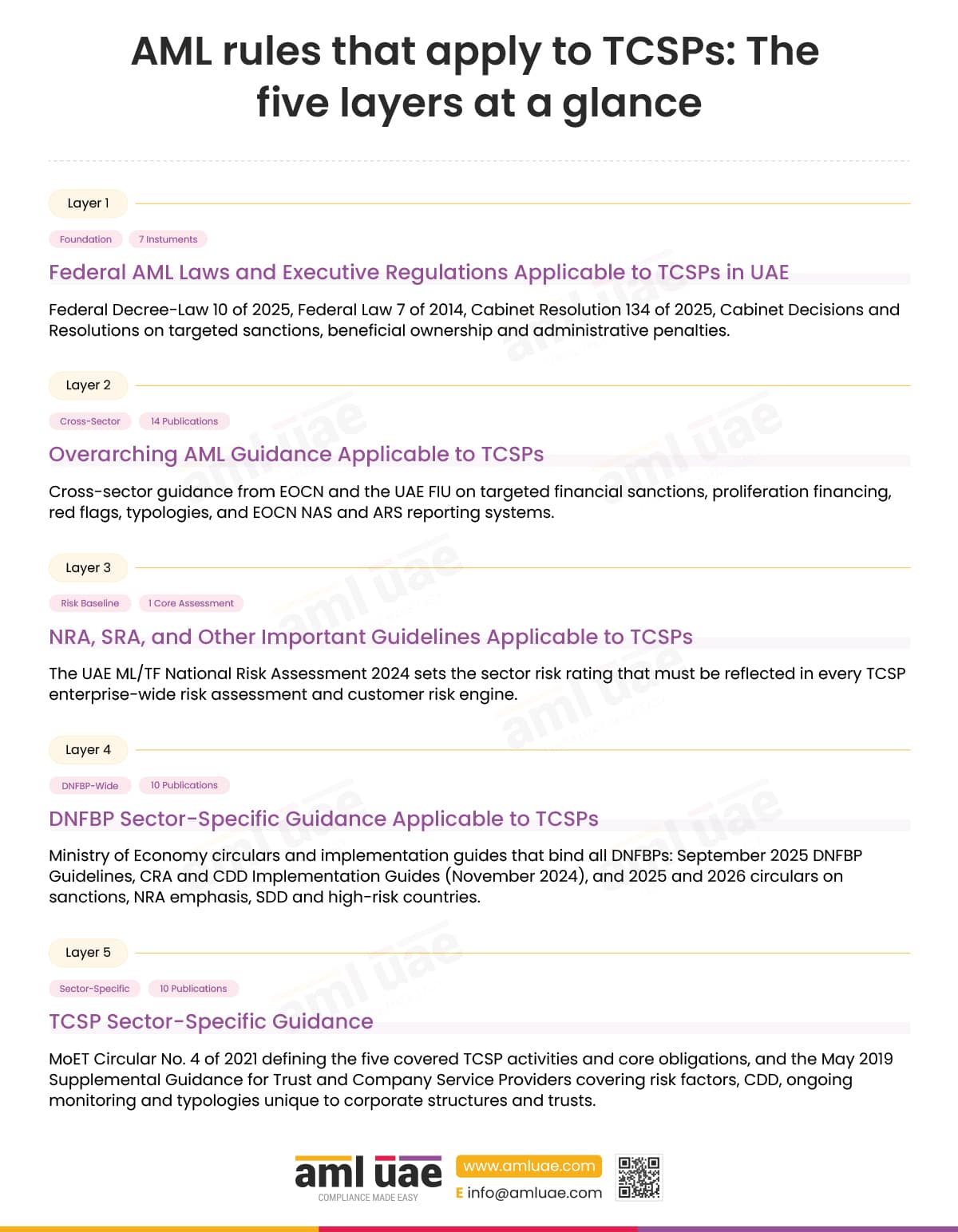

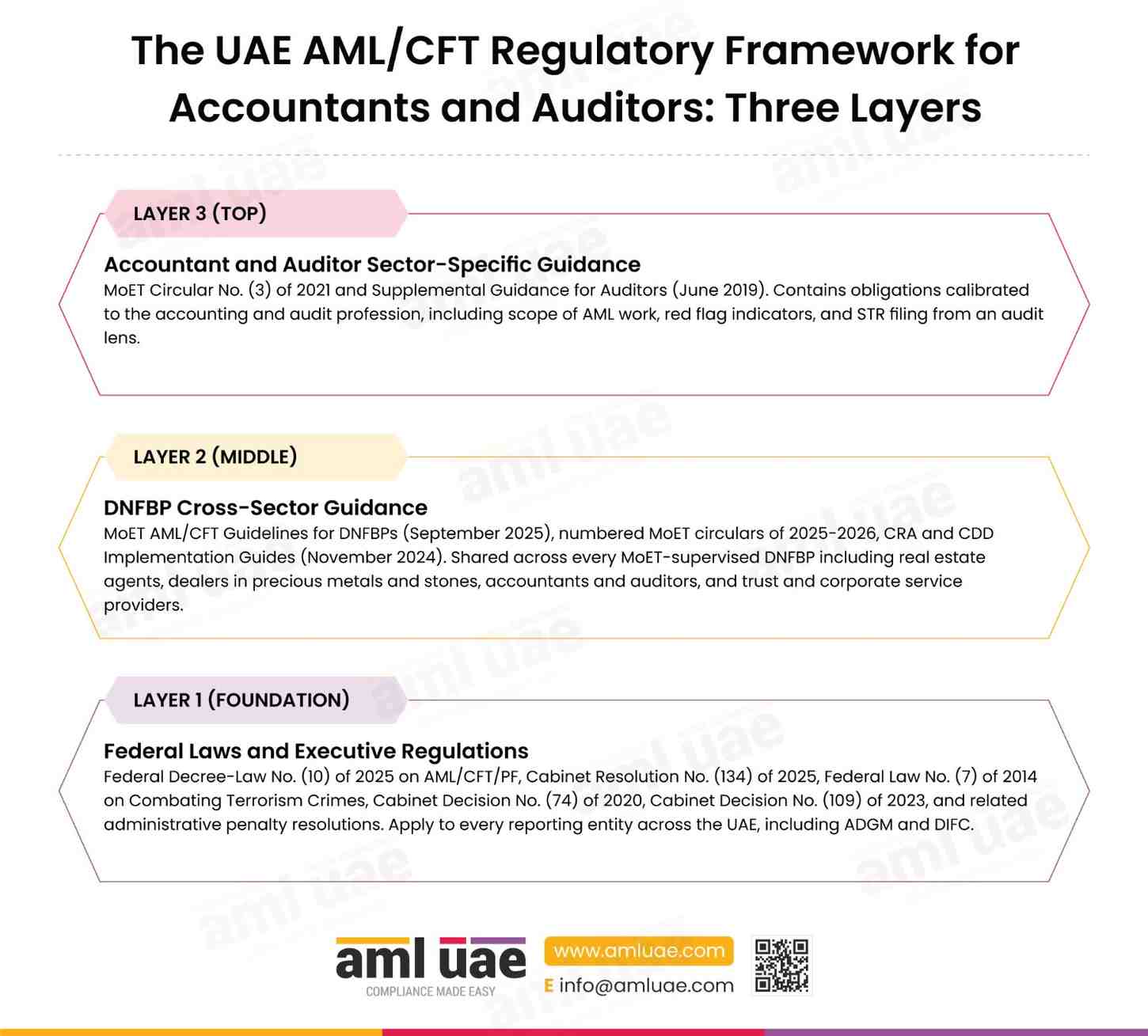

The AML/CFT regulatory framework applicable to accountants and auditors in the UAE is layered. At its foundation sits a suite of federal laws and executive regulations that apply to all reporting entities. Above that foundation sit cross-sector guidance instruments applicable to all DNFBPs, and finally sector-specific guidance directed at the accounting and auditing profession.

The UAE AML/CFT Regulatory Framework for Accountants and Auditors: Three Layers

Each layer builds on the one below it. All three apply simultaneously to accountants and auditors in UAE mainland and commercial free zones.

LAYER 3 (TOP)

Accountant and Auditor Sector-Specific Guidance

MoET Circular No. (3) of 2021 and Supplemental Guidance for Auditors (June 2019). Contains obligations calibrated to the accounting and audit profession, including scope of AML work, red flag indicators, and STR filing from an audit lens.

LAYER 2 (MIDDLE)

DNFBP Cross-Sector Guidance

MoET AML/CFT Guidelines for DNFBPs (September 2025), numbered MoET circulars of 2025-2026, CRA and CDD Implementation Guides (November 2024). Shared across every MoET-supervised DNFBP including real estate agents, dealers in precious metals and stones, accountants and auditors, and trust and corporate service providers.

LAYER 1 (FOUNDATION)

Federal Laws and Executive Regulations

Federal Decree-Law No. (10) of 2025 on AML/CFT/PF, Cabinet Resolution No. (134) of 2025, Federal Law No. (7) of 2014 on Combating Terrorism Crimes, Cabinet Decision No. (74) of 2020, Cabinet Decision No. (109) of 2023, and related administrative penalty resolutions. Apply to every reporting entity across the UAE, including ADGM and DIFC.

Federal AML Laws and Executive Regulations Applicable to Accountants and Auditors

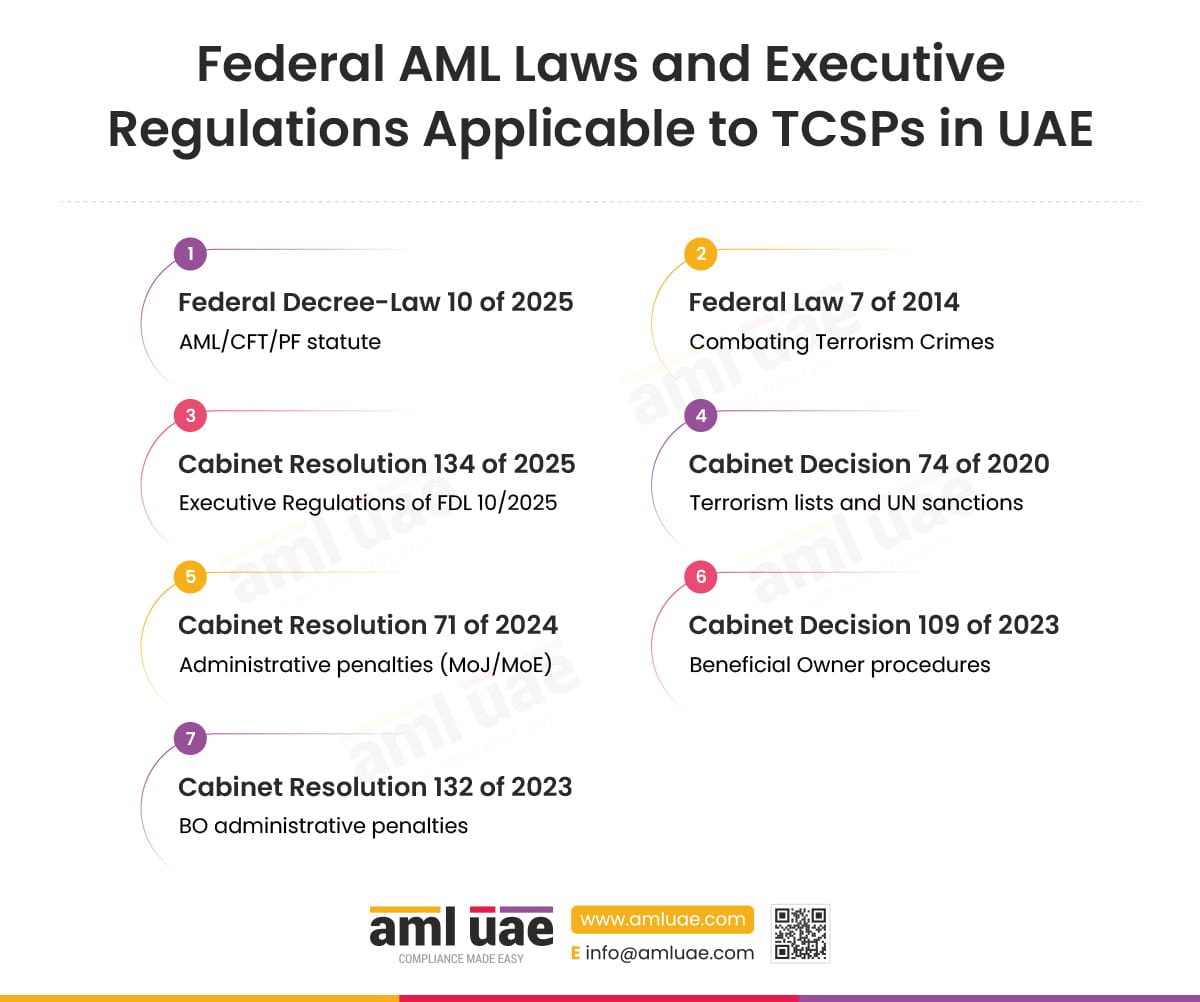

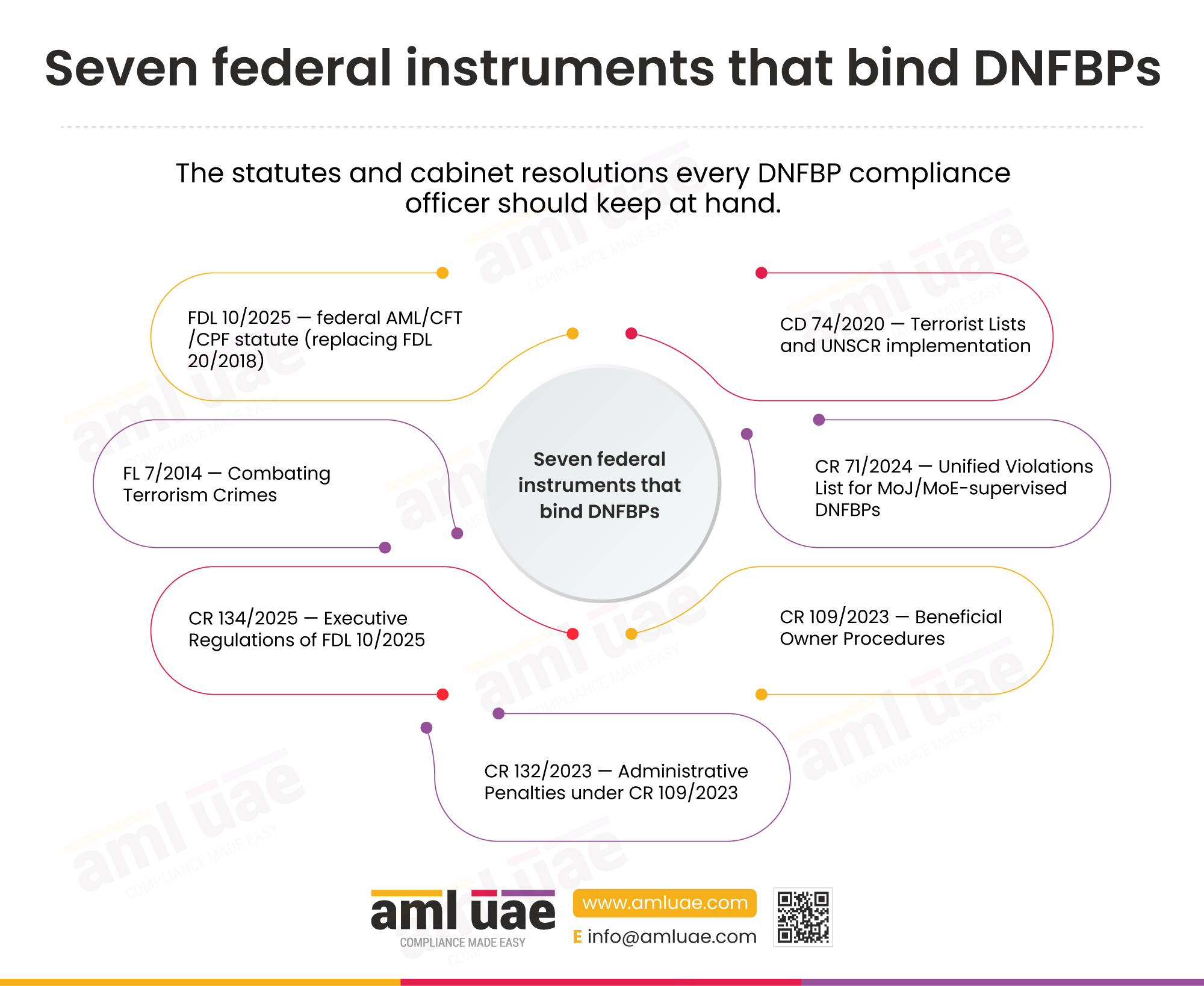

Seven federal legislative instruments form the backbone of every accountant’s and auditor’s compliance programme. Non-compliance with any of these can trigger criminal prosecution, administrative fines, licence suspension, or deregistration. These instruments are deliberately broad: they apply to every natural and legal person that is a reporting entity, including MoET-supervised accountants and auditors.

Federal AML/CFT Laws Applicable to Accountants and Auditors

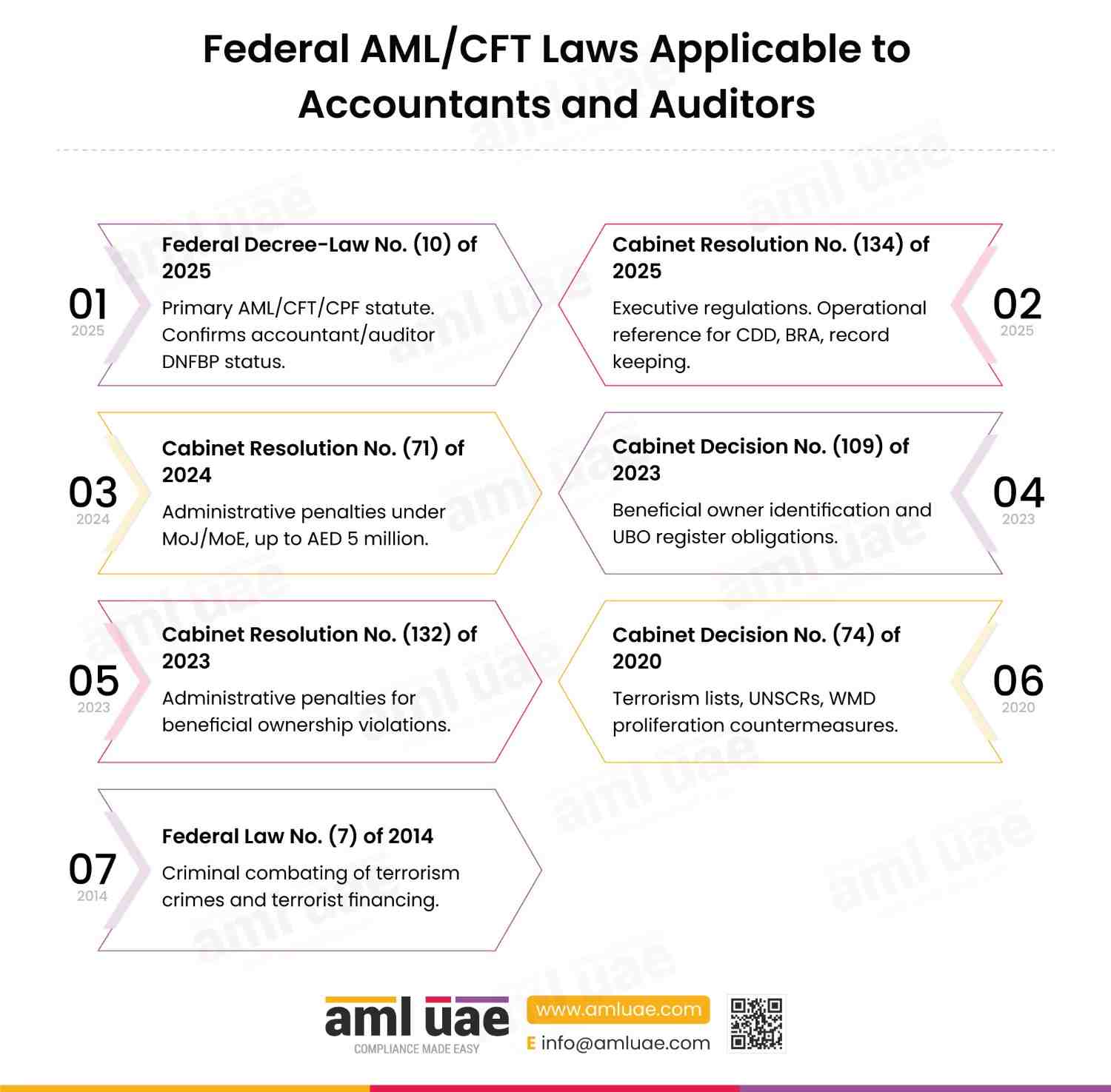

1. Federal Decree-Law No. (10) of 2025

Primary AML/CFT/CPF statute. Confirms accountant/auditor DNFBP status.

2. Cabinet Resolution No. (134) of 2025

Executive regulations. Operational reference for CDD, BRA, record keeping.

3. Cabinet Resolution No. (71) of 2024

Administrative penalties under MoJ/MoE, up to AED 5 million.

4. Cabinet Decision No. (109) of 2023

Beneficial owner identification and UBO register obligations.

5. Cabinet Resolution No. (132) of 2023

Administrative penalties for beneficial ownership violations.

6. Cabinet Decision No. (74) of 2020

Terrorism lists, UNSCRs, WMD proliferation countermeasures.

7. Federal Law No. (7) of 2014

Criminal combating of terrorism crimes and terrorist financing.

Federal Decree-Law No. (10) of 2025 Regarding Anti-Money Laundering, and Combating the Financing of Terrorism and Proliferation Financing

Federal Decree-Law No. (10) of 2025 is the primary AML/CFT/CPF statute in the UAE. It replaced and consolidated the earlier Federal Decree-Law No. 20 of 2018 and its amendments. The law defines predicate offences for money laundering, classifies accountants and auditors among the DNFBPs subject to AML/CFT obligations, and establishes the core compliance duties: customer due diligence (CDD), record keeping, suspicious transaction reporting, internal controls, staff training, and the appointment of an anti-money laundering compliance officer (MLCO). The law requires every accountant and auditor performing covered activities to verify the identity of customers and beneficial owners before establishing a business relationship or carrying out an occasional transaction above the prescribed threshold.

Federal Law No. (7) of 2014 Combating Terrorism Crimes

The Federal Law No. (7) of 2014 criminalises terrorism-related offences and defines terrorism crimes, terrorist organisations, and associated penalties. Knowingly providing accounting, tax, or corporate services to a designated terrorist or a terrorist organisation can constitute a criminal offence, independent of the firm’s AML reporting obligations.

Cabinet Resolution No. (134) of 2025 Concerning the Executive Regulations of Federal Decree-Law No. (10) of 2025

Cabinet Resolution No. (134) of 2025 is the executive regulation that operationalises the primary AML/CFT law. It sets out the practical requirements for CDD, including the specific documents that must be collected for natural persons, legal persons, and legal arrangements. It defines the triggers for enhanced due diligence (EDD) and the conditions under which simplified due diligence (SDD) may be applied. For accountants and auditors, the resolution prescribes the requirements of a business-wide risk assessment, the frequency of customer file reviews, the qualifications and reporting line of the compliance officer, and the training requirements for staff performing covered activities. It also requires that all CDD documentation, transaction records, and risk assessments be retained for a minimum of five years after the end of the business relationship.

Cabinet Decision No. (74) of 2020 Regarding Terrorism Lists Regulation and Implementation of UN Security Council Resolutions

Cabinet Decision No. (74) of 2020 implements the UN Security Council resolutions on the suppression and combating of terrorism, terrorism financing, and proliferation of armaments. Under Article 15, any person who holds funds on the UN Consolidated Sanctions List or the UAE Local Terrorist List must freeze those funds without prior notice and without delay, and notify the Executive Office for Control and Non-Proliferation (EOCN) within five working days. The operational mechanics for DNFBPs, including subscription to the EOCN Notification Alert System (NAS), filing of Confirmed Name Match Reports (CNMRs) and Partial Name Match Reports (PNMRs), and ongoing sanctions-list screening, are set out in the EOCN Targeted Financial Sanctions Guidance and are supervisory expectations for every accountant and auditor.

Cabinet Resolution No. (71) of 2024 Regulating Violations, Administrative Penalties Imposed on Violators of Measures for Confronting Money Laundering and Combating Financing of Terrorism Subject to the Control of the Ministry of Justice and the Ministry of Economy

Cabinet Resolution No. (71) of 2024 sets out the graduated administrative penalty regime applicable to entities supervised by the MoET and the Ministry of Justice, including accountants and auditors. Its annexed schedule starts at AED 50,000 for lower-severity breaches and rises to AED 1,000,000 for the most serious scheduled violations, with Article 5(2) permitting the Ministry to double the fine on repeat offences, while Article 3(1) preserves the Ministry’s power to stack any of the Article 14 sanctions under Federal Decree-Law No. (10) of 2025, namely written warnings, fines of up to AED 5,000,000 per violation, business restrictions, removal of senior management, and suspension or revocation of the professional licence.

Cabinet Decision No. (109) of 2023 on Regulating the Beneficial Owner Procedures

Beneficial ownership transparency is a core element of the UAE AML/CFT framework. This cabinet decision requires company registrars and corporate entities to identify and verify the identity of their beneficial owners, defined as any natural person who ultimately owns or controls 25 per cent or more of the shares or voting rights, or who exercises effective control through other means. Accountants and auditors who assist clients with company formation, corporate secretarial work, or ongoing management must ensure that beneficial ownership information held by the client is accurate, current, and available to competent authorities upon request, and that the UBO register is maintained at the client’s registered office.

Cabinet Resolution No. (132) of 2023 Concerning the Administrative Penalties against Violators of Cabinet Decision No. (109) of 2023 on Beneficial Owner Procedures

This companion resolution prescribes the specific fines and administrative measures that apply to entities and individuals that fail to comply with beneficial ownership requirements. Penalties include fines, suspension of activity, public warnings, and referral to criminal prosecution in cases of deliberate concealment of beneficial ownership information. Accountants who advise on corporate structuring should treat the BO regime and its penalty schedule as part of the first-line client-risk assessment.

Ready to map your obligations under Federal Decree-Law No. (10) of 2025?

AML UAE builds policies, business-wide risk assessments, and inspection-ready files aligned with the 2025 federal framework and MoET guidance.

Overarching AML Guidance Applicable to Accountants and Auditors

In addition to the federal legislative framework, accountants and auditors must follow a set of overarching guidance documents issued by national-level bodies including the Executive Office for Control and Non-Proliferation (EOCN) and the UAE Financial Intelligence Unit (FIU). While these are not primary legislation, they represent binding supervisory expectations and are treated as standards during MoET inspections.

Overarching EOCN and FIU Guidance for DNFBPs including Accountants and Auditors

1. TFS Guidance for FIs, DNFBPs and VASPs

EOCN. Most current TFS implementation guidance.

2. FIU Strategic Analysis on TF

Terrorist financing trends and red flags.

3. Strategic Review on TFS Case Studies

Real-world TFS implementation and evasion cases.

4. PF Institutional Risk Assessment

PF-IRA methodology for FIs, DNFBPs, VASPs.

5. TF and PF Red Flags Guidance

Indicators for monitoring and staff training.

6. Joint Guidance on Unlicensed VASPs

Identifying and mitigating unlicensed VASP risks.

7. Counter PF Guidance

Dual-use goods screening, trade monitoring, EDD.

8. Satisfactory/Unsatisfactory Practice

Joint good-practice benchmarks for inspections.

9. Typologies on TFS Circumvention

Front companies, nominee structures, layering.

10. Guideline on Grievance Procedures

How designated persons or entities may seek review.

11. Online Grievance System User Guide

Step-by-step instructions for the grievance portal.

12. Combating PF and Sanctions Evasion

Practical controls against sanctions evasion.

13. NAS Subscription Simple Guide

How to subscribe to the EOCN alert system.

Guidance on Targeted Financial Sanctions for Financial Institutions, DNFBPs and VASPs (EOCN, March 2026)

The most current TFS guidance from the EOCN. It details the procedures for screening, freezing, unfreezing, and reporting in relation to UN and local sanctions lists. Accountants and auditors must implement screening procedures covering all customers, beneficial owners, authorised signatories, and transaction counterparties. Confirmed matches must be reported via a Confirmed Name Match Report (CNMR) and partial matches via a Partial Name Match Report (PNMR), both submitted through the goAML system. Freezing measures must be implemented without delay upon a confirmed match, which the EOCN interprets as same-business-day at the latest.

FIU Strategic Analysis Report on Terrorist Financing — May 2025

The FIU’s strategic analysis report provides insight into current terrorist financing trends, methods, and red-flag indicators in the UAE. Accountants and auditors should use this report to inform their internal risk assessments and to train staff on emerging TF typologies, including small-value transfers layered through professional services, misuse of charitable structures, and abuse of corporate service vehicles.

Strategic Review on Targeted Financial Sanctions Case Studies — November 2021 (covering 2019-2021, EOCN reference IEC-SR.01.22)

This strategic review presents anonymised case studies illustrating how targeted financial sanctions have been applied and, in some cases, evaded. It serves as a practical reference for understanding sanctions evasion schemes and how compliance teams should respond, with examples that include the use of nominee directors, complex trust structures, and indirect ownership chains that frustrate first-layer screening.

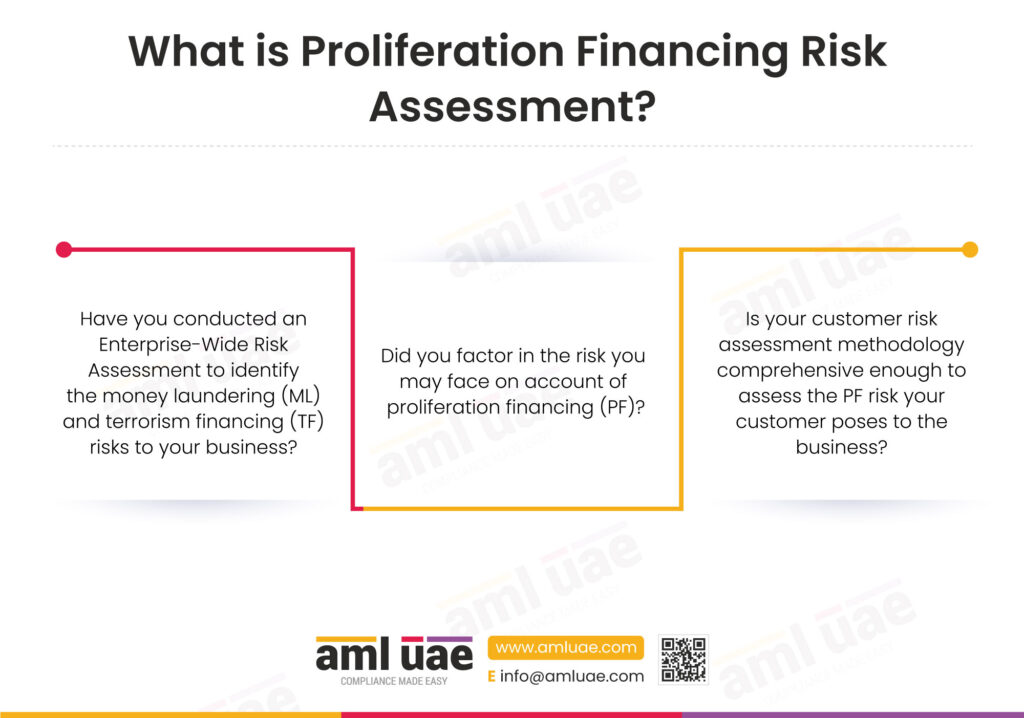

Proliferation Finance Institutional Risk Assessment Guidance for FIs, DNFBPs and VASPs — December 2023

Accountants and auditors are required to incorporate proliferation financing (PF) risks into their business-wide risk assessments. This guidance explains the methodology for conducting a PF Institutional Risk Assessment (PF-IRA), including the identification of PF risk factors, the assessment of existing controls, and the documentation of findings. The PF-IRA is a stand-alone exercise distinct from the AML business-wide risk assessment and must be reviewed at least annually.

Terrorist and Proliferation Financing Red Flags Guidance — December 2023

This document sets out the red-flag indicators that may suggest terrorist or proliferation financing activity. Accountants and auditors should embed these indicators into their transaction monitoring processes, CDD escalation triggers, and staff training programmes. Typical red flags include unexplained wire transfers to high-risk jurisdictions, layered corporate structures with no clear commercial rationale, and clients reluctant to disclose the source of wealth.

Joint Guidance on Combating the Use of Unlicensed Virtual Asset Providers in the UAE — 1 March 2022

Relevant to accountants and auditors who encounter clients using virtual assets or dealing with virtual asset service providers. It highlights the risks associated with unlicensed VASPs and the steps that DNFBPs should take to identify and mitigate those risks, including refusing to process payments to suspected unlicensed VASPs and filing STRs where appropriate.

Guidance on Counter Proliferation Financing for FIs, DNFBPs and VASPs — 1 March 2022 (EOCN reference EOCN-PF.01.22)

This guidance supplements the PF risk assessment guidance by explaining the practical counter-proliferation financing controls, including dual-use goods screening, trade-related transaction monitoring, and enhanced due diligence for clients with links to sanctioned jurisdictions such as the DPRK and Iran.

Joint Guidance on Satisfactory and Unsatisfactory Practice — June 2021

Issued jointly by UAE supervisory authorities, this guidance provides examples of good and poor compliance practice observed during inspections. Accountants and auditors should review the examples to benchmark their own compliance programmes and to calibrate remediation plans where MoET has identified a weakness.

Typologies on the Circumvention of Targeted Sanctions against Terrorism and the Proliferation of Weapons of Mass Destruction — March 2021

This document examines the techniques used to evade targeted financial sanctions, including the use of front companies, nominee structures, identity concealment, and complex layering schemes. Valuable for training compliance staff and calibrating EDD triggers.

Guideline on Grievance Procedures

Sets out how designated persons or entities may seek review of listing decisions and how supervisory authorities and DNFBPs should handle grievance requests. Accountants acting as registered agents or in nominee roles should be familiar with the process so they can respond appropriately where a client is listed.

Online Grievance System User Guide

Step-by-step instructions for using the EOCN online grievance portal, including the information required, supporting documents, and processing timelines.

Combating Proliferation Financing and Sanctions Evasion

Practical guidance for implementing counter-proliferation and sanctions-evasion controls. Useful when designing transaction monitoring scenarios and calibrating escalation triggers in higher-risk trade corridors.

Simple Guide to Subscribe to the EOCN Notification Alert System (NAS)

Explains how accountants and auditors should register for the EOCN NAS to receive real-time alerts when sanctions lists are updated. Subscription to NAS is a mandatory supervisory expectation for DNFBPs and is commonly checked during MoET inspections.

Need a PF-IRA template, TFS screening procedure, or training deck?

AML UAE delivers EOCN-aligned templates and train-the-trainer sessions calibrated to the size and risk profile of accounting and audit firms.

NRA, SRA, and Other Important Guidelines Applicable to Accountants and Auditors

The UAE National Risk Assessment (NRA) is the single most important national-level risk document for every DNFBP. It synthesises risk findings across the UAE economy and prescribes calibration of supervisory and firm-level controls. Accountants and auditors must treat the NRA as a live input into their business-wide risk assessment, not a background reference.

UAE ML/TF National Risk Assessment — 2024

The 2024 National Risk Assessment describes the audit and accounting sector as small, with medium inherent vulnerability and medium-low residual risk. The NRA acknowledges specific vulnerabilities, including the gatekeeper role that accountants play in financial transactions, the potential for professional services to be misused to obscure beneficial ownership, and identified gaps in screening and monitoring practices across parts of the profession.

Accountants and auditors are required to review the NRA findings, conduct a gap analysis between their current compliance programme and the NRA expectations, incorporate the findings into their business-wide risk assessments, and update their internal controls, CRA weighting, and training materials accordingly. MoET has confirmed that inspection teams will probe whether NRA findings are reflected in BRAs and in the calibration of the CRA.

DNFBP Sector-Specific Guidance Applicable to Accountants and Auditors

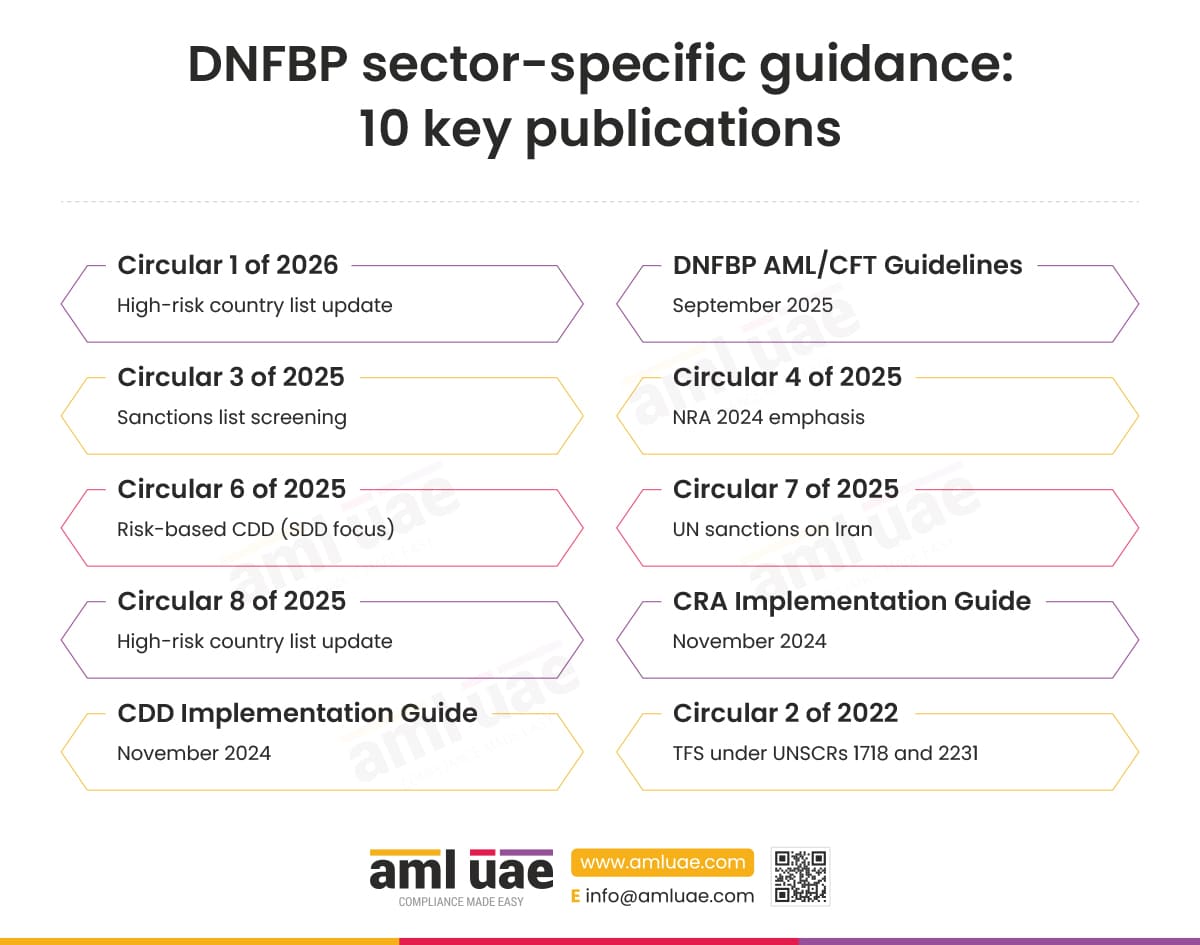

These guidance and circular instruments are issued by MoET and apply across its DNFBP perimeter. They are not accountant or auditor-specific but form the operational backbone against which inspections are conducted, and they must be read in conjunction with the federal laws above.

DNFBP Sector-Specific MoET Guidance: 10 Key Instruments

1. Circular No. (1) of 2026

Updated high-risk country list and related measures.

2. AML/CFT Guidelines for DNFBPs

Primary compliance manual covering governance, CDD, EDD, STRs.

3. Circular No. (3) of 2025

Sanctions and terrorist list screening at onboarding and continuously.

4. Circular No. (4) of 2025

NRA 2024 is a live input to BRAs.

5. Circular No. (6) of 2025

Risk-based CDD with focus on simplified due diligence.

6. Circular No. (7) of 2025

Reimposition of UN sanctions relating to Iran under UNSCR 1737.

7. Counter PF Guidance

Dual-use goods screening, trade monitoring, EDD.

8. Satisfactory/Unsatisfactory Practice

Joint good-practice benchmarks for inspections.

9. Typologies on TFS Circumvention

Front companies, nominee structures, layering.

10. Guideline on Grievance Procedures

How designated persons or entities may seek review.

Circular No. (1) of 2026 on Updating the Lists of High-Risk Countries, Countries Subject to Increased Monitoring, and Related Measures

This circular updates the lists of jurisdictions classified as high-risk (FATF black list) or subject to increased monitoring (FATF grey list) and directs accountants and auditors to apply enhanced due diligence to all relationships and transactions involving those jurisdictions. It also prohibits establishing branches or subsidiaries in high-risk jurisdictions and reliance on third parties in those countries for CDD performance.

AML/CFT Guidelines for Designated Non-Financial Businesses and Professions — September 2025

Published by MoET in September 2025, these comprehensive guidelines replace earlier DNFBP guidance and provide the definitive regulatory expectations for all MoET-supervised DNFBPs, including accountants and auditors. They cover the full compliance lifecycle: governance and the MLCO role, business-wide risk assessment, customer risk assessment, CDD (including SDD and EDD), ongoing monitoring, STR filing through goAML, record keeping, staff training, and sanctions screening. This is the single most important reference document for building an AML/CFT compliance programme for accounting and audit firms.

Circular No. (3) of 2025 on Emphasising the Importance of Screening Sanctions and Terrorist Lists (MOEC/AML/003/2025, dated 19 March 2025)

This circular reiterates the obligation to screen customer databases against the latest sanctions and terrorism lists without delay. Screening must cover not only the customer but also all beneficial owners, authorised signatories, and transaction counterparties. MoET inspection teams treat sanctions screening evidence as a priority test area.

Understanding the Importance of the UAE 2024 National Risk Assessment — A Practical Guide for DNFBPs (Ministry of Economy)

This practical guide directs all MoET-supervised DNFBPs to study the 2024 NRA, incorporate its findings into internal risk assessments, and allocate resources to address identified gaps. The NRA is a binding input to the firm’s compliance programme, not merely a reference document.

Circular No. (6) of 2025 on Emphasising the Implementation of Risk-Based Customer Due Diligence Measures (with a Focus on Simplified Due Diligence)

This circular provides practical direction on when and how SDD may be applied. SDD may never be applied where there is any suspicion of money laundering or terrorist financing. Firms must apply EDD for high-risk customers, standard CDD for medium-risk customers, and SDD only for genuinely low-risk customers where the firm has documented its risk rationale and there is no suspicion.

Circular No. (7) of 2025 Regarding the Reimposition of United Nations Sanctions Related to Iran pursuant to UNSCR 1737 (2006) and Subsequent Resolutions

This circular requires accountants and auditors to update screening systems with the latest UN Consolidated Sanctions List, re-screen all existing customers and beneficial owners for exposure to Iran sanctions, apply freezing measures without delay upon a confirmed match, and report confirmed matches (via CNMR) and partial matches (via PNMR) through the goAML system.

Circular No. (8) of 2025 on Updating the Lists of High-Risk Countries, Countries Subject to Increased Monitoring, and Related Measures

A subsequent update to the high-risk country list published within 2025. The updated lists must be reflected in the firm’s jurisdictional risk assessment, CRA, and CDD policies, and all existing relationships with nexus to the updated jurisdictions must be reviewed for potential EDD.

Implementation Guide for DNFBPs on Customer Risk Assessment (CRA) — November 2024

The Ministry of Economy’s Implementation Guide for DNFBPs on Customer Risk Assessment sets out a ten-step methodology for scoring customers across five risk-factor categories, Customer, Geographic, Product/Service/Transaction, Delivery Channel, and Other, using a one-to-five scale from Low to High. The guide requires accountants and auditors to apply the CRA at onboarding, at periodic reviews, and whenever there is a change in risk factors such as a shift in ownership, a new product, adverse media, a sanctions listing, or an update to the National or Sectoral Risk Assessment. It indicates example review cadences of every six months for high-risk clients, every one year for medium and medium-high risk clients, every eighteen months for low-medium risk clients, and every two years for low-risk clients, and it requires DNFBPs to maintain a comprehensive audit trail of all due diligence steps, risk scores, and justifications, available upon request by the competent supervisory authority.

Implementation Guide for DNFBPs on Customer Due Diligence (CDD) — November 2024

This companion guide details practical CDD steps, including identity verification for natural and legal persons, beneficial ownership identification using the 25 per cent threshold, SDD and EDD conditions, ongoing monitoring, and procedures when CDD cannot be completed. It also addresses the tipping-off prohibition: once a suspicious transaction is contemplated or reported, the firm must not disclose that fact to the client or to any third party who is not authorised to receive it.

Circular No. (2) of 2022 Regarding Implementation of Targeted Financial Sanctions on UNSCRs 1718 (2006) and 2231 (2015)

This circular provides implementation instructions for TFS related to DPRK and Iran proliferation sanctions. EDD is required for all transactions with a nexus to North Korea and Iran, including verification of cross-border transactions for potential dual-use goods, shipment documents, and end-user declarations.

Sector-Specific Guidelines Applicable to Accountants and Auditors

Beyond the DNFBP-wide instruments, the following documents are addressed specifically to the accounting and auditing profession and reflect the sector’s particular risk exposures and operational realities.

Ministry of Economy Circular No. (3) of 2021 (dated 4 February 2021)

Issued by the then Ministry of Economy Anti-Money Laundering Department (prior to the ministry’s rebranding as the Ministry of Economy and Tourism), this circular is addressed directly to independent accountants and auditors. It outlines core AML/CFT obligations, including the requirement to register with the Ministry, appoint a compliance officer, conduct customer due diligence, and file suspicious transaction reports via the goAML system.

Supplemental Guidance for Auditors — June 2019

Published by the Ministry of Economy, this is the most detailed auditor-specific compliance document available. It covers the scope of AML obligations for auditors (explaining which audit activities fall within the AML perimeter and which do not), risk factors specific to the audit profession (nature of the audit engagement, client type, geographic exposure, and transaction complexity), customer due diligence guidance for auditors (including verification of corporate clients, identification of beneficial owners in complex group structures, and managing CDD for long-standing audit relationships), red-flag indicators for auditors (unexplained cash transactions, complex multi-jurisdictional structures, inconsistencies between reported revenue and business activity, and clients with links to sanctioned jurisdictions), STR reporting obligations (identifying reportable suspicion, the goAML filing process, and the tipping-off prohibition), and common ML/TF typologies encountered in audit engagements.

Taken together, MoET Circular No. (3) of 2021 and the Supplemental Guidance for Auditors operate as the accountant-specific overlay on the DNFBP framework. They calibrate the scope of AML obligations to the practical reality of audit, assurance, and related advisory engagements, and they should be reviewed in full at least annually by the MLCO and the engagement partners.

Are you an accountant or auditor in ADGM or DIFC?

Accountants and auditors operating in the Abu Dhabi Global Market are supervised by the ADGM Registration Authority (RA) and must comply with the ADGM AML and Sanctions Rulebook. Those in the DIFC are supervised by the DFSA and must comply with the DFSA AML, CTF and Sanctions Module. The overarching federal laws and cabinet resolutions apply across the entire UAE, including ADGM and DIFC. See our ADGM and DIFC pages for the operational rulebook that applies to your firm.

Conclusion

The AML/CFT regulatory framework for accountants and auditors in the UAE is both comprehensive and continuously evolving. From the primary Federal Decree-Law No. (10) of 2025 through the detailed implementing regulations, overarching EOCN and FIU guidance, DNFBP-wide MoET circulars, and sector-specific MoET guidance, the obligations are clear and enforceable. The common thread is risk-based thinking: firms must identify where they sit in the ML/TF/PF risk landscape, calibrate controls accordingly, and be able to evidence the judgement at inspection.

For accountants and auditors operating in mainland UAE and commercial free zones, the practical priorities are as follows. Firms that invest in the controls below now will be best placed to adapt to future updates to the UAE AML/CFT/CPF framework and to avoid the significant penalties that attach to non-compliance.

1. Conduct and document a business-wide risk assessment (BRA) informed by the 2024 NRA and the September 2025 DNFBP Guidelines. Review at least annually and on trigger events such as new product lines, new jurisdictions, or new circulars.

2. Maintain a proliferation financing institutional risk assessment (PF-IRA) calibrated to client and transaction exposure to DPRK, Iran, and other proliferation-sensitive jurisdictions.

3. Apply a documented customer risk assessment to every client before providing covered services. Verify identity using reliable independent documents. Identify beneficial owners at the 25 per cent ownership or effective-control threshold. Apply EDD for high-risk clients, standard CDD for medium-risk, and SDD only where documented low-risk rationale exists and no suspicion is present.

4. Monitor client relationships continuously for changes in ownership, business activity, transaction patterns, and risk profile. Review frequencies should follow the CRA Implementation Guide: high-risk every 6 months, medium-high every 12 months, medium every 12 months, low-medium every 18 months, and low-risk every 24 months.

5. Screen all clients, beneficial owners, authorised signatories, and transaction counterparties at onboarding and continuously against the UAE Local Terrorist List, UNSC consolidated lists, and FATF-designated jurisdictions. Subscribe to the EOCN NAS for real-time alerts and register with the ARS.

6. File STRs via goAML whenever the firm knows, suspects, or has reasonable grounds to suspect that a transaction relates to ML, TF, or PF. File FFRs for confirmed matches and PNMRs for partial matches. Respect the tipping-off prohibition at all times.

7. Appoint an MLCO with adequate seniority, independence, and direct reporting to senior management. Deliver periodic AML/CFT training covering CDD, red flags, STR filing, sanctions screening, and the tipping-off prohibition to all staff performing covered activities.

8. Retain CDD documentation, transaction records, STR filings, sanctions hits, risk assessments, and training logs for a minimum of five years after the end of the business relationship or the date of the occasional transaction.

Build your accountant or auditor AML programme with AML UAE

We design, document, and stress-test AML/CFT compliance programmes for accounting and audit firms across UAE mainland and commercial free zones, including BRA/PF-IRA, CRA, CDD, screening, STR filing workflows, training, and inspection readiness.

Frequently Asked Questions

When are accountants treated as DNFBPs in the UAE?

Accountants and auditors are treated as DNFBPs when they prepare for or carry out specified financial transactions on behalf of clients. The five covered activities are buying and selling real estate, managing client money or securities, managing bank or savings accounts, organising contributions for the creation or management of companies, and creating or managing legal persons or arrangements.

Which regulator supervises accountants and auditors for AML in the UAE?

The Ministry of Economy and Tourism (MoET) is the designated AML/CFT supervisory authority for independent accountants and auditors operating in mainland UAE and in commercial free zones. Accountants and auditors licensed in the ADGM are supervised by the FSRA, and those in the DIFC are supervised by the DFSA. Federal AML laws apply in all three jurisdictions; the difference is the operational rulebook and the supervisory interface.

What due diligence is expected from accountants and auditors?

Risk-based customer due diligence is expected. This includes verifying the identity of the customer and all beneficial owners at the 25 per cent ownership or effective-control threshold, understanding the purpose and intended nature of the business relationship, conducting ongoing monitoring of transactions and customer information, and keeping records for at least five years. Enhanced due diligence is required for high-risk customers; simplified due diligence may be applied only to genuinely low-risk relationships where no suspicion of ML or TF exists.

What are common AML red flags for accountants?

Common red flags for accountants include unexplained large cash transactions or payments in rounded amounts, complex multi-jurisdictional structures with no clear business rationale, clients reluctant to provide identification or beneficial ownership information, inconsistencies between reported revenue and observable business activity, transactions involving high-risk or sanctioned jurisdictions, use of nominee directors or shell companies with no substantive operations, and sudden changes in transaction patterns or payment flows without a clear commercial reason.

Do audit firms in ADGM and DIFC follow separate rules?

Yes. ADGM and DIFC are financial free zones with their own regulatory authorities, the ADGM Registration Authority (RA) and the DFSA respectively. Audit firms licensed in those jurisdictions follow the AML/CFT rulebook issued by their regulator. However, the overarching federal laws and cabinet resolutions, including Federal Decree-Law No. (10) of 2025 and Cabinet Decision No. (134) of 2025, apply across the entire UAE, including ADGM and DIFC. The supervisor and the operational rulebook differ by jurisdiction, not the federal statute.

Enjoying this guide?

Leave us a review on Google. It helps other compliance professionals discover AML UAE and supports our ongoing research into UAE AML regulations.

Disclaimer : This article is published by AML UAE (amluae.com) for informational and educational purposes only. It does not constitute legal, regulatory, or compliance advice. The UAE AML/CFT regulatory framework is subject to change, and references to named laws, circulars, and guidance documents reflect the position known at the time of publication. For advice specific to your firm, consult a qualified AML compliance professional or licensed legal advisor. AML UAE accepts no responsibility for decisions taken in reliance on this article alone.

Share via :

About the Author

Pathik Shah

FCA, CAMS, CISA, CS, DISA (ICAI), FAFP (ICAI)

Pathik is an ACAMS-certified AML consultant specialising in governance, risk, and compliance for regulated entities in the UAE. He brings over 28 years of experience, with 1,000+ hours of AML training and 200+ advisory engagements across DNFBPs, VASPs, and FIs. He supports businesses in aligning with AML/CFT requirements from the CBUAE, DFSA, MoET, MoJ, VARA, CMA, FSRA, and FATF. Known for translating complex regulations into audit-ready procedures, Pathik enables operational clarity and compliance readiness.

Reach Out to Pathik