Pathik Shah

Last Updated: 03/30/2026

Protect your business with reliable and effective AML strategies with AML UAE.

AML Requirements for Lawyers in the UAE: Key Takeaways

- Lawyers, notaries, and legal professionals in the UAE, classified as DNFBPs, are subject to the prevailing AML/CFT/CPF framework, which includes:

- Federal Decree-Law No. (10) of 2025 and Cabinet Resolution No. (134) of 2025

- Lawyers, notaries, and legal professionals in the UAE are supervised by the Ministry of Justice (MoJ), which includes:

- Regulatory oversight and inspections

- AML obligations only apply when legal professionals engage in “covered activities, such as managing client funds, real estate transactions, or company formation, making scope identification a critical first step in compliance.

- Legal professionals must implement a risk-based AML program, including:

- Client and firm-level risk assessments

- Customer Due Diligence (CDD) and Enhanced Due Diligence (EDD)

- Beneficial ownership identification

- Ongoing transaction monitoring

- Suspicious Transaction Reporting (STR) to the FIU

- Sanctions and PEP screening

- 2025 and 2026 regulatory updates provide emphasis on ensuring:

- Inspection readiness and audit trails

- Documented risk assessment methodologies

- Alignment with FATF high-risk jurisdiction updates

- Integration of counter-proliferation financing (CPF) controls

- Lawyers and legal professionals found noncompliant can face severe regulatory action, including:

- Financial penalties

- License suspension

- Practice ban

- License revocation

When do AML/CFT and CPF Regulations Apply to lawyers, notaries, and legal professionals in the UAE?

AML obligations apply to legal professionals in UAE only when they engage in “covered activities”, including:

- Purchase and sale of real estate

- Managing customers’ bank accounts, savings, or securities accounts, creating, operating, or managing legal persons

- Management of customer’s funds

- Organising contributions for the establishment, operation, or management of the company

- Selling and buying commercial entities

In simple words, not all legal services and advisory falls within the ambit of AML/ obligations, AML compliance is only triggered when lawyers engage in specific financial or transactional activities defined under UAE AML/CFT and CPF regulations.

Lawyers, notaries, and legal professionals come under the purview of AML obligations only when they carry out certain “covered activities” or services. It is therefore important to know when AML/CFT and CPF regulations apply to lawyers and legal professionals, i.e., so that they can ensure adequate AML/CFT and CPF compliance.

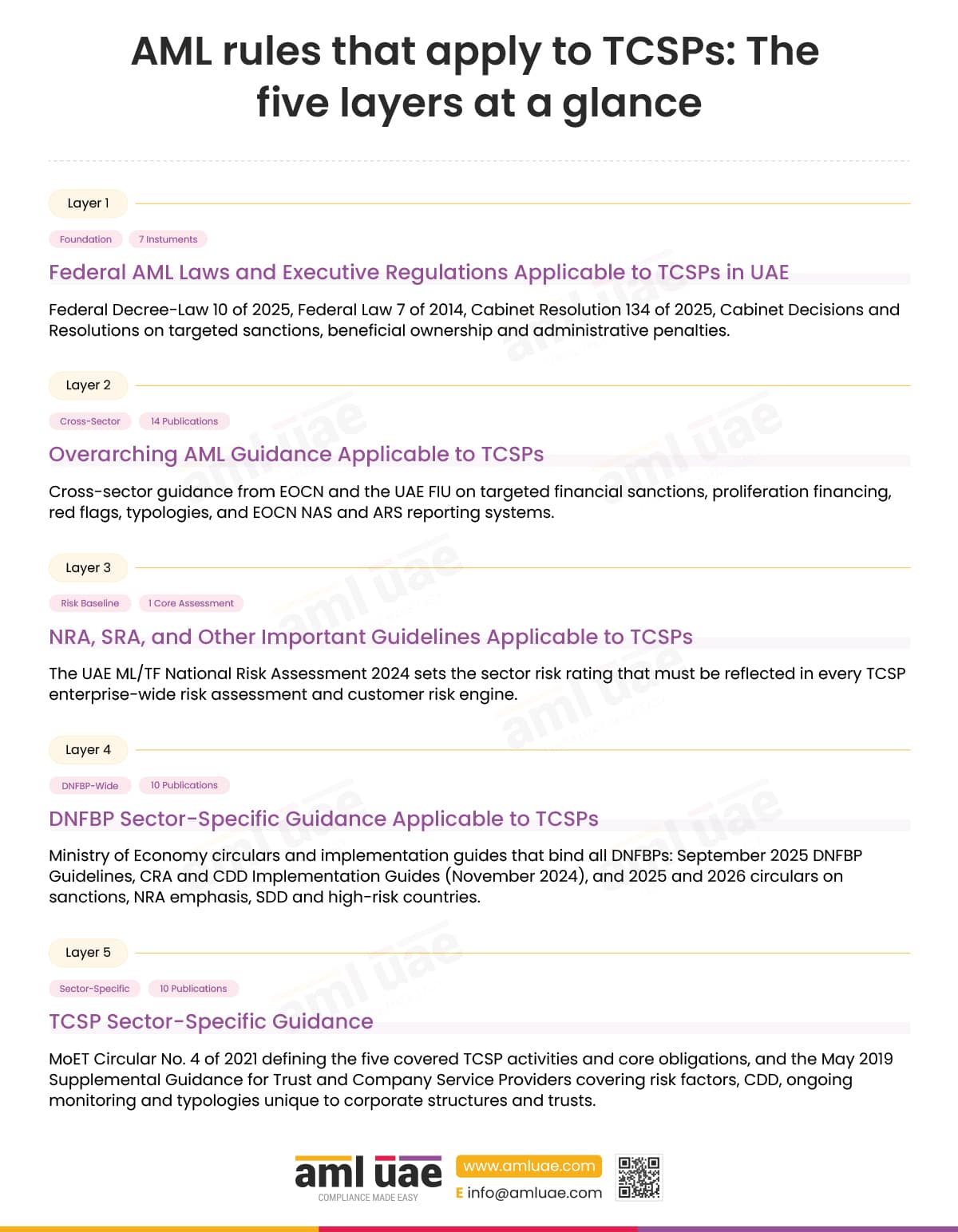

AML Legal Framework for lawyers, notaries, and legal professionals in the UAE

Core AML Legislation

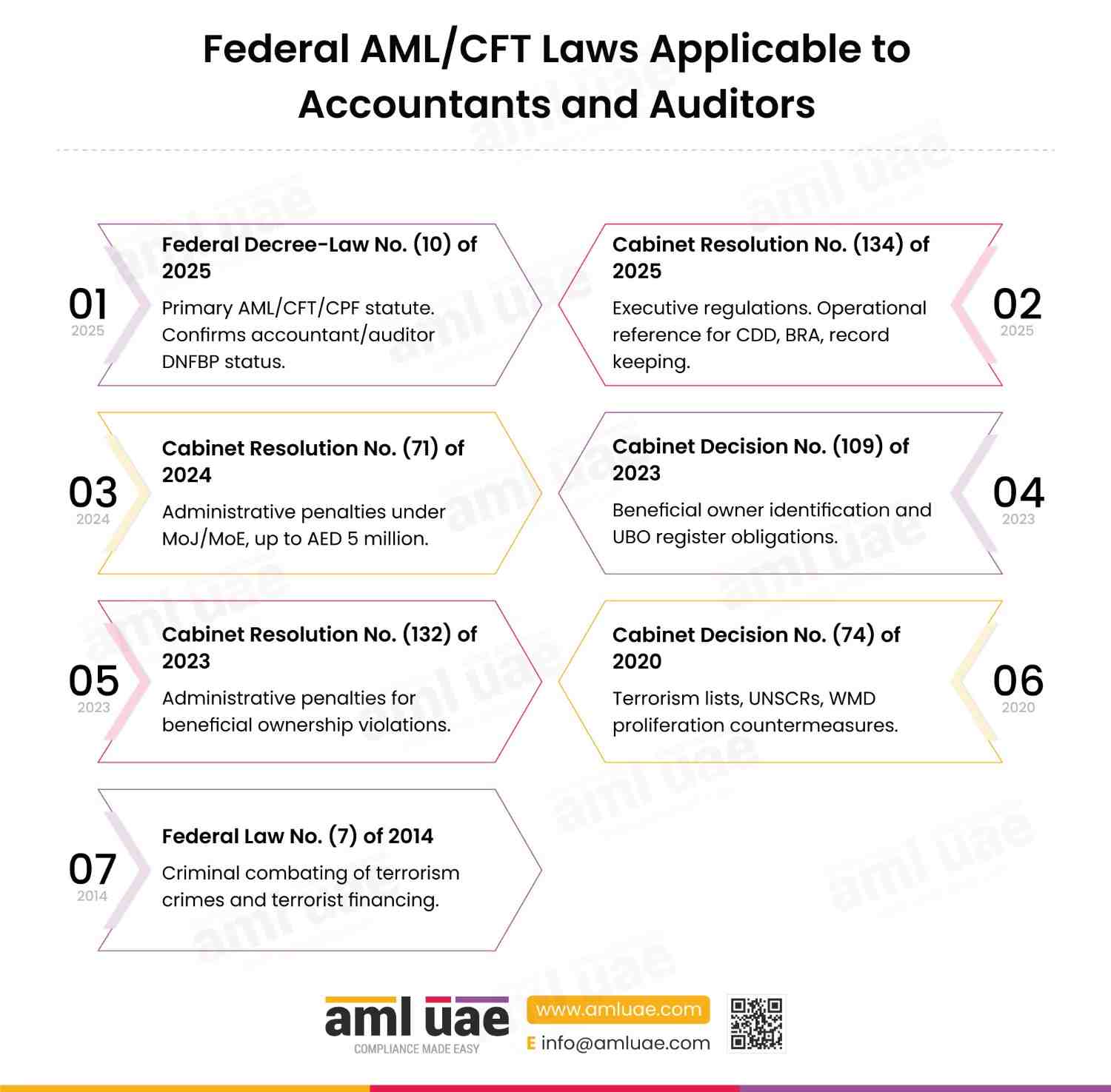

- Federal Decree by Law No. (10) of 2025 Regarding Anti-Money Laundering, and Combating the Financing of Terrorism and Proliferation Financing

- Cabinet Resolution No. (134) of 2025 Concerning the Executive Regulations of Federal Decree-Law No. (10) of 2025 Concerning Combating Money Laundering, Terrorist Financing, and the Financing of the Proliferation of Weapons

- For a detailed understanding of core AML, CFT and CPF laws, and regulations applicable to lawyers, notaries, and legal professionals, refer to: Federal AML/CFT/CPF Laws and Executive Regulations

Regulatory Updates (2022-2026)

- Lawyers’ Guide on AML/CFT (2026): Guidance issued by the Ministry of Justice.

- Circular No.1 of 2026 Concerning the Obligation of Law Firms and Legal Consultancy Offices to Update Policies, Procedures, and Controls Related to Anti-Money Laundering, Combating the Financing of Terrorism, and Counter-Proliferation Financing (Available only in Arabic): calls for lawyers, notaries and legal professionals to update their policies and procedures whenever risk factors change, or regulatory requirements arise.

- Circular No. (3) of 2025 Regarding the Update of the List of High-Risk Countries and Countries Subject to Enhanced Monitoring: requires lawyers, notaries, and legal professionals to ensure that their policies and procedures are aligned with latest changes to the FATF Grey List and Blacklist.

- Ministerial Resolution No. (248) of 2025 Regulating the Procedures and Controls for Supervising and Monitoring Law Firms, Legal Consultancy Offices, and Notaries Public in the Field of Combating Money Laundering and Terrorism Financing (Available only in Arabic): which repeals Ministerial Decision No. (533) of 2019 On AML/CFT related to Lawyers, Notaries and Legal Independent Professionals. It addresses the following:

- Alignment with Cabinet Resolution 71 of 2024 containing the penalty framework and is applicable to lawyers and legal professionals practicing in Financial Free Zones and Non-Financial Free Zones.

- Imposes a temporary practice ban, suspension of partners and directors, and license revocation in the event of non-compliance

- Requires lawyers, notaries, and legal professionals to have in place written documentation for conducting due diligence requirements, such as customer risk assessment, PEP and adverse media screening, conducting and maintaining sanctions screening logs, maintaining ongoing monitoring and UBO verification records

- Requires lawyers, notaries, and legal professionals to exhibit inspection readiness, appoint a designated inspection response officer, and maintain a corrective action tracking register.

- Circular No. (1) of 2025 regarding the commitment of law firms to the controls of institutional assessment processes (Available only in Arabic): requires lawyers, notaries, and legal professionals to conduct institutional risk assessments that address proliferation financing risks.

- Circular No. (1) of 2024 regarding simplified due diligence procedures. (Available only in Arabic): Explains simplified due diligence measures that can be applied to customers posing low ML/TF risks.

- Circular No. 14 of 2022 regarding the REAR Real Estate Activities Report (Available only in Arabic): Imposes obligations on lawyers, notaries and legal professionals engaged in real estate transactions to file REAR when transaction is settled in cash or cryptocurrencies above a specified threshold.

These regulatory developments in the legal sector reflect a shift towards stringent enforcement, increased supervisory oversight, and a significant emphasis on proactive risk management.

Supervisory Authority

In the context of lawyers, notaries, and legal professionals or law firms licensed in UAE, other than Abu Dhabi Global Market (ADGM) and Dubai International Financial Centre (DIFC), the Ministry of Justice is the AML supervisory authority.

AML Requirements for Lawyers in UAE

Lawyers operating in the UAE must comply with AML/CFT and CPF obligations, such as:

- Appointment of an AML/CFT Compliance Officer

- goAML Registration

- ML/TF Risk Assessment

- AML/CFT & CPF Policy and Procedures Documentation

- AML/CFT Training and Awareness

- Customer Due Diligence (CDD)

- Know Your Customer (KYC)

- Name Screening

- Customer Risk Assessment

- Ongoing Monitoring

- Regulatory Reporting

- Record-Keeping

- Independent Audit

What Lawyers Must Do to Comply with AML Obligations

In order to ensure AML compliance, lawyers, notaries, and legal professionals in the UAE must formulate and implement a structured methodology based on a risk-based approach that requires continuous risk assessment, verification, monitoring, and reporting across the practice and client lifecycle.

- Conducting Risk Assessment at the Firm Level: Identifying, evaluating and understanding the inherent ML/TF and PF risks associated with the business is a must for lawyers, notaries, and legal professionals, assessing ML/TF and PF risks on a practice/business level.

Lawyers must be specifically aware of the ways illicit money can enter their ordinary course of business. The entry or placement of illegal funds may be from the client’s side, transaction type, or geography. This understanding will enable the legal practitioner to be careful before taking up any work.

- Performing Customer Due Diligence (CDD/EDD): Lawyers and notaries must implement simplified or enhanced due diligence measures based on customers’ low or high risks, respectively.

The client’s risk may also vary based on the type of transaction, which may require an update on the due diligence measures.

With all this information about the client, lawyers can prepare a risk profile and allocate a risk rating. At timely intervals, review and update this information in proportion to their risk rating.

- Monitoring Client Activity and Transactions: Another essential consideration is monitoring the transactions and relationships with clients. This monitoring ensures consistency and alignment between the information lawyers have about the client and the type of transactions. Any unusual nature of inconsistency will alert lawyers at the right time to take relevant actions.

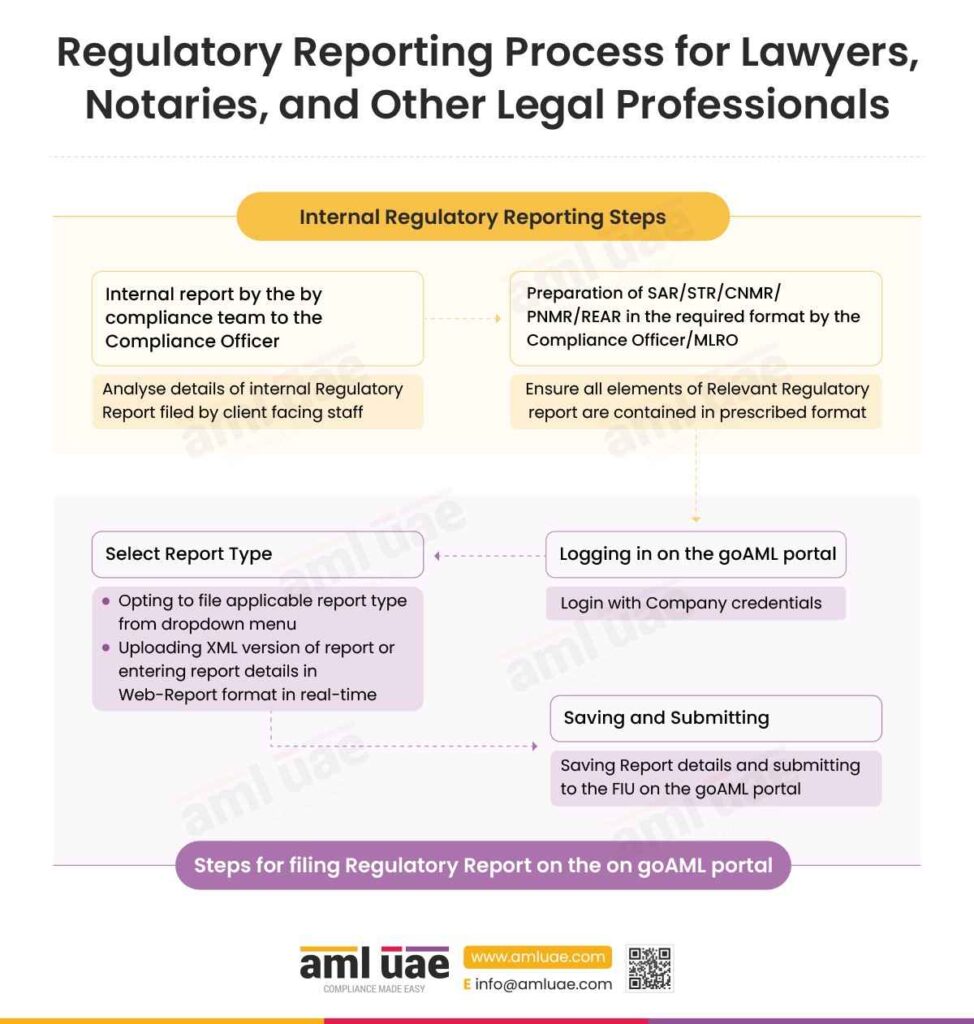

- Ensuring Regulatory Reporting: Lawyers, notaries, and all legal professionals and practitioners must report any suspicious transaction or activity indicating potential ML/TF or PF risks to FIU. They must provide all relevant supporting information to the authority for further investigation. Adequate internal policies related to this best practice help legal professionals to comply with it.

- Maintaining Adequate AML Records: Legal professionals must document and save all the compliance measures taken and activities performed for future reference and inspection readiness.

Where Lawyers Face ML/TF and PF Risks

Due to the inherent nature of legal services, certain activities and client behaviours present higher exposure to ML/TF and PF risks. The UAE’s National Risk Assessment (NRA) identifies Professional Money Laundering (PML) as one of the highest threats where criminals target legal professionals to create complex structures and legal arrangements to gain a veneer of respectability while laundering illicit funds.

High Risk Legal Activities

Lawyers, notaries and legal professionals are exposed to high ML/TF and PF risks, and are subject to AML obligations when they step beyond general legal advisory and prepare, conduct, or execute financial transactions on behalf of their clients relating to the following “covered activities” referred to above.

Types of Money Laundering Red Flags

- Client Behaviour Red Flags

- Concealing identity: The client actively avoids personal contact without sufficient cause, insists on using intermediaries for all transactions, or uses informal representation such as family or close associates acting as nominee shareholders with the intent to obscure the identities of true Ultimate Beneficial Owner (UBO) without justifiable reason.

- Refusing Documents: Clients showcasing reluctance or inability to provide personal information, refusal to clarify their sources of wealth or supply the standard documentation required to facilitate and conclude transactions. This also includes instances of customers resorting to providing falsified, forged, or counterfeit documents.

- Transaction Red Flags

- Unusual Funding: The transaction involves an unexplained influx of large sums of cash, especially when used as collateral rather than direct payment, third-party funding with no apparent nexus or legitimate explanation, or private loans lacking supporting documents or regular interest repayments

- No Business Rationale: The prospective transaction or proposal for the same appears entirely incompatible with the client’s socio-economic, educational, or professional profile. It may also include the client insisting on shortcuts or loopholes or exceptionally expedited processing, while offering to pay substantially higher fees than usual without a legitimate reason.

- Structural Red Flags

- Complex ownership changes: The business relationship shows frequent or inexplicable changes to the ownership, management, or beneficiaries of the client, especially when the lawyer is not notified in a timely manner or when last-minute changes are made to the identity of the parties before a transaction is completed.

- Multiple jurisdictions: The client insists upon creation of a complex web of legal persons or arrangements spanning multiple countries, often involving offshore entities, tax havens, or jurisdictions with strict secrecy laws specifically designed to divert financial flows, obscure the money trail, and disguise beneficial ownership.

Beyond establishing and implementing operational control measures, AML regulations in the UAE require lawyers, notaries, and legal professionals to also establish a structured governance framework that ensures ongoing compliance and inspection readiness.

Save yourself from non-compliance penalties

By hiring AMLUAE for AML/CFT compliance

AML Governance and Internal Controls

- Compliance Officer: Lawyers, notaries, and legal professionals, when engaging in covered activities, are required to appoint an independent, management-level officer to oversee AML controls and serve as the firm’s primary liaison with the Ministry of Justice and the Financial Intelligence Unit (FIU)

- Documented AML Framework: Legal professionals are required to maintain and continuously update risk-based AML/CFT, and CPF policies, procedures, systems and controls to mitigate ML/TF and PF risks specifically arising from the firm’s covered busine

Download Free AML Policy Template for lawyers, notaries, and legal professionals and practitioners

- Management Oversight: Senior Management within the law firms or lawyers or notaries working independently, without a firm structure, must approve AML/CFT and CPF policies, establish their practice’s risk appetite, allocate adequate resources and assign clear accountability and delegation.

- Independent Audit & Review: Legal professionals are required to conduct periodic, independent evaluations that are internal as well as external, to test the effectiveness of the firm’s AML framework and remediate control gaps identified.

- Regulatory Inspection Readiness: Lawyers are required to securely retain all risk assessment methodologies, outcomes, Customer Due Diligence (CDD) files and transaction records for a minimum of five years to ensure prompt responses during supervisory inspections.

Penalties on Lawyers for AML Non-Compliance

Supervisory Authorities may issue warnings, mandate submission of periodic remediation reports, or appoint a temporary supervisor to oversee the legal professional’s compliance.

Administrative Penalties

- Financial penalties: Fines of not less than AED 10,000 and up to AED 5,000,000 for each individual violation, and these fines can be applied incrementally if the legal professional repeats the same violation within a year.

- License suspension: The supervisory authorities, upon coming across violation, can suspend or restrict the activity or profession for a specific period determined.

- Practice ban: Lawyers, Notaries, and legal professionals may also be subject to a practice ban, preventing them from engaging in the legal sector for a specified period. Authorities may also suspend or restrict the powers of specific directors, partners, or executive personnel proven responsible for the compliance failure

- License revocation: In the event of systemic non-compliance, complete revocation of legal license may also be directed.

Criminal Sanctions

- Failure to Report: If lawyers, notaries, and legal professionals intentionally or through negligence fails to report a suspicious transaction to the FIU (in cases where the statutory professional secrecy exemption does not apply) then they are liable to imprisonment and a fine ranging from AED 100,000 to AED 1,000,000.

- Tipping Off: If a lawyers, notaries, and legal professionals intentionally or unintentionally warns their client that an SAR/STR is underway, they can face a minimum of six months in prison and a fine between AED 100,000 and AED 500,000.

- General Violations: Violation of any other provisions of AML/CFT and CPR Decree-law can lead to imprisonment or a fine of between ED 10,000 and AED 100,000

How Lawyers Can Implement AML Compliance Effectively

- Risk Assessment Execution: lawyers, notaries, and legal professionals must adopt a risk-based approach to understand their ML/FT risks and implement relevant measures. These risks will be different and unique for each firm or individual. The chances depend on the type of services, geographies of operation, and client base of the legal practitioner.Before commencing any business relationship, lawyers are required to conduct a risk assessment of the client. For this, they may consider national reports or sectoral reports undertaken by supervisory authorities. For instance:

- Policy Implementation: Lawyers, notaries, and legal professionals need to focus on developing and implementing policies and procedures for the company’s operations. These policies, procedures, and internal controls must manage the risks that the business faces. These controls, policies, and procedures must be:

- Applicable to all branches, subsidiaries, departments, and functions of the company

- Reviewed and approved by the management

- Reasonable, effective for the identified risks, and consistent with the results of their risk assessments.

- Training programs: Lawyers, notaries, and legal professionals in the UAE, in order to ensure the effectiveness of ML/TF and PF risk assessment and mitigation measures deployed, must ensure that their employees have adequate knowledge and understanding of risks and awareness of the internal procedures to mitigate such risks.

Conclusion

lawyers, notaries, and legal professionals Legal professionals carry out certain activities that have higher vulnerability to ML/FT risks. They are at increased risk, whether they give tax advice, facilitate property transactions, represent clients in disputes and mediations, or act as intermediaries. Financial criminals take advantage of this vast range of services to engage in money laundering and terrorism financing.

So, they need to be careful about their entity’s risk exposure and employ the above requirements. UAE has categorized them in the DNFBPs list and expects regular compliance with the AML/CFT law provisions. Such compliance with the national AML/CFT requirements will enable them to keep themselves safe from money laundering risks.

To plan and implement any of these measures, you can also take the support of AML consultants in the UAE. A professional AML consultant will be better equipped to help lawyers, notaries, and legal professionals legal professionals and practitioners with suitable, relevant measures against money laundering. The consultant will ensure that industry-specific steps are taken in the fight against money laundering and terrorism financing.

Role of AML UAE

AML UAE is a leading AML compliance services provider in UAE. We help lawyers, notaries, and legal professionals you with fulfilling all the requirements for AML and CFT in UAE. Our spectrum of AML compliance services is not restricted to national boundaries, but we also make sure that lawyers, notaries, and legal professionals you comply with the global regulations of AML.

We can help you with:

- Creating firm-specific AML policies, procedures, internal controls, best practices, and guidelines for lawyers, notaries, and legal professionals your smooth business operations

- Setting up an expert AML compliance department for your firm that can handle all AML-related activities

- Selecting the most effective and appropriate AML software for lawyers, notaries, and legal professionals your business needs to ensure AML compliance

- Helping you in filing and submitting annual AML/CFT risk assessment reports with the UAE government

- Conducting training for lawyers, notaries, and legal professionals your employees in handling KYC, screening, risk profiling, CDD, EDD, and filing of STRs

Frequently Asked Questions (FAQs)

Here are a few frequently asked questions when it comes to the need and importance of sanction and PEP screening in the customer onboarding process.

It is a good practice to appoint an AML compliance team in your company that will take care of the compliance. The team will assess the risks, implement an AML/CFT compliance program, and execute CDD measures. If you do not wish to appoint an AML team internally, you can take the services of AML consultants who will help you manage all these activities.

Legal professionals are required for the transfer of property by law or by market practice. Money launderers and financial criminals invest their illicit money in property. They do this by concealing the identity of the source of funds. They may also hide the identity of owners by using false identities. So, legal professionals must be careful when engaging in such real estate transactions. They must carry out due diligence measures for the party they are representing and the transaction.

Add a comment

Share via :

About the Author

Pathik Shah

FCA, CAMS, CISA, CS, DISA (ICAI), FAFP (ICAI)

Pathik is an ACAMS-certified AML consultant specialising in governance, risk, and compliance for regulated entities in the UAE. He brings over 28 years of experience, with 1,000+ hours of AML training and 200+ advisory engagements across DNFBPs, VASPs, and FIs. He supports businesses in aligning with AML/CFT requirements from the CBUAE, DFSA, MoET, MoJ, VARA, CMA, FSRA, and FATF. Known for translating complex regulations into audit-ready procedures, Pathik enables operational clarity and compliance readiness.

Reach Out to Pathik

")