Last Updated: 05/05/2026

Table of Contents

Protect your business with reliable and effective AML strategies with AML UAE.

Contact Us Now

Key Highlights

In-scope status: Commercial gaming operators brought into the AML perimeter as a DNFBP activity under Cabinet Resolution No. (134) of 2025, Article (3) Item 1.

Activity trigger: Single or linked financial transactions equal to or above AED 11,000. Pure gaming chips or gaming instruments do not count as a financial transaction.

Supervisory authority: General Commercial Gaming Regulatory Authority (GCGRA), the sole AML/CFT supervisor for the sector.

Primary federal law: Federal Decree-Law No. (10) of 2025 on Combating Money Laundering, Terrorist Financing and Proliferation Financing.

Cross-sector baseline: Beneficial owner regime under Cabinet Decision No. (109) of 2023 and terrorist/PF sanctions regime under Cabinet Decision No. (74) of 2020.

Administrative penalties: AED 10,000 to AED 5,000,000 per violation under Federal Decree-Law No. (10) of 2025, Article (17), plus warning, suspension, prohibition and licence revocation.

Record-keeping period: At least five years for transactions, identification documents, correspondence and analyses under Cabinet Resolution No. (134) of 2025, Article (25).

Sector policy reference: Policy Paper on Commercial Gaming (2025) issued by the General Secretariat of the National AML/CFT Policies Committee.

Regulatory posture: Emerging niche sector; UAE ML/TF National Risk Assessment 2024 notes it was not separately evaluated as no entities were licensed at the time of assessment.

Definition

A commercial gaming operator in the UAE is a licensee of the General Commercial Gaming Regulatory Authority authorised to offer commercial games for value, and is subject to AML obligations once a single transaction, or linked transactions, equal or exceed AED 11,000.

Scope Note

This page is a forward-looking, sector-specific guide to AML regulations for commercial gaming operators in UAE. It focuses on how the federal AML framework, the overarching sanctions and proliferation financing guidance, the National Risk Assessment and the 2025 Commercial Gaming Policy Paper combine to shape compliance expectations for licensees of the General Commercial Gaming Regulatory Authority.

The AML regulations for commercial gaming operators in UAE sit at the intersection of a well-established federal AML framework and a brand-new sector. Cabinet Resolution No. (134) of 2025 expanded the list of Designated Non-Financial Businesses and Professions (DNFBPs) to explicitly include commercial gaming operators, and the General Commercial Gaming Regulatory Authority (GCGRA) has been set up as the sole sector supervisor for AML and counter-financing of terrorism purposes. Licensees therefore have to implement the full suite of DNFBP obligations from day one, even though the sector has no operational history to draw on within the UAE.

This guide explains how AML regulations for commercial gaming operators in UAE are structured, who the supervisory authority is, and which federal laws, cross-sector guidance documents, risk assessments and sector-specific policy papers apply. It is the commercial gaming spoke of our DNFBPs pillar and sits within the broader AML Laws in UAE hub. Read it alongside our Federal AML laws and executive regulations page for the baseline legal text.

Who Counts as a Commercial Gaming Operator for AML Purposes in UAE?

AML regulations for commercial gaming operators in UAE apply to any operator of commercial games whose activity crosses the AED 11,000 trigger set out in Cabinet Resolution No. (134) of 2025. Article (3) Item (1) of the Executive Regulations lists, among the categories of DNFBPs, “Commercial Gaming Operators, including Commercial Gaming conducted on board vessels or marine craft, when conducting a single financial transaction or several transactions that appear to be linked and whose value equals or exceeds eleven thousand dirhams (AED 11,000). A financial transaction shall not include a transaction that solely involves gaming chips or gaming instruments”.

Three features of this definition matter for the AML perimeter. First, it is activity-based; the obligation is triggered by transaction value. Second, it covers on-board operations on vessels or marine craft, keeping offshore setups inside the DNFBP perimeter. Third, it carves out pure chip or gaming-instrument transactions; those are treated as internal gaming mechanics rather than financial transactions for AML purposes. Every AED 11,000 equivalent cash-in, cash-out, wire transfer, e-wallet load or redemption does trigger customer due diligence, record-keeping and reporting obligations.

Who is in scope

Four tests every commercial gaming operator in the UAE has to apply before onboarding a patron.

1. Activity test: operator of commercial games

2. Location test: mainland UAE or UAE-flagged vessel

3. Threshold test: single or linked transactions at or above AED 11,000

4. Carve-out: pure chip or gaming instrument movements

1. Licensed commercial gaming operators

Entities licensed by the General Commercial Gaming Regulatory Authority to conduct commercial games in mainland UAE. Article (3) Item (1) of Cabinet Resolution No. (134) of 2025 places them squarely within the DNFBP perimeter.

2. On-board commercial gaming on vessels and marine craft

The DNFBP definition specifically extends to commercial gaming conducted on board vessels or marine craft. Operators cannot avoid AML obligations by moving activity offshore while remaining within UAE jurisdiction.

3. Activity that hits AED 11,000 single or linked transactions

The AED 11,000 trigger is applied on a single transaction, or several transactions that appear to be linked. Operators must have rules to aggregate same-patron activity across sessions, accounts, payment methods and time windows.

4. Transactions outside the AML perimeter

Transactions that solely involve gaming chips or gaming instruments are not financial transactions for AML purposes under Article (3) Item (1). Internal chip movements remain a risk indicator but do not by themselves trigger CDD.

Key legal hook

The DNFBP definition in Cabinet Resolution No. (134) of 2025 is the single legal hook that makes AML regulations for commercial gaming operators in UAE mandatory. Every downstream control, from CDD to reporting, flows from that designation.

Need a DNFBP gap assessment built for commercial gaming?

AML UAE supports GCGRA licensees with DNFBP scope reviews, enterprise risk assessments and AML programme design tailored to commercial gaming models.

Explore our DNFBP AML compliance services →

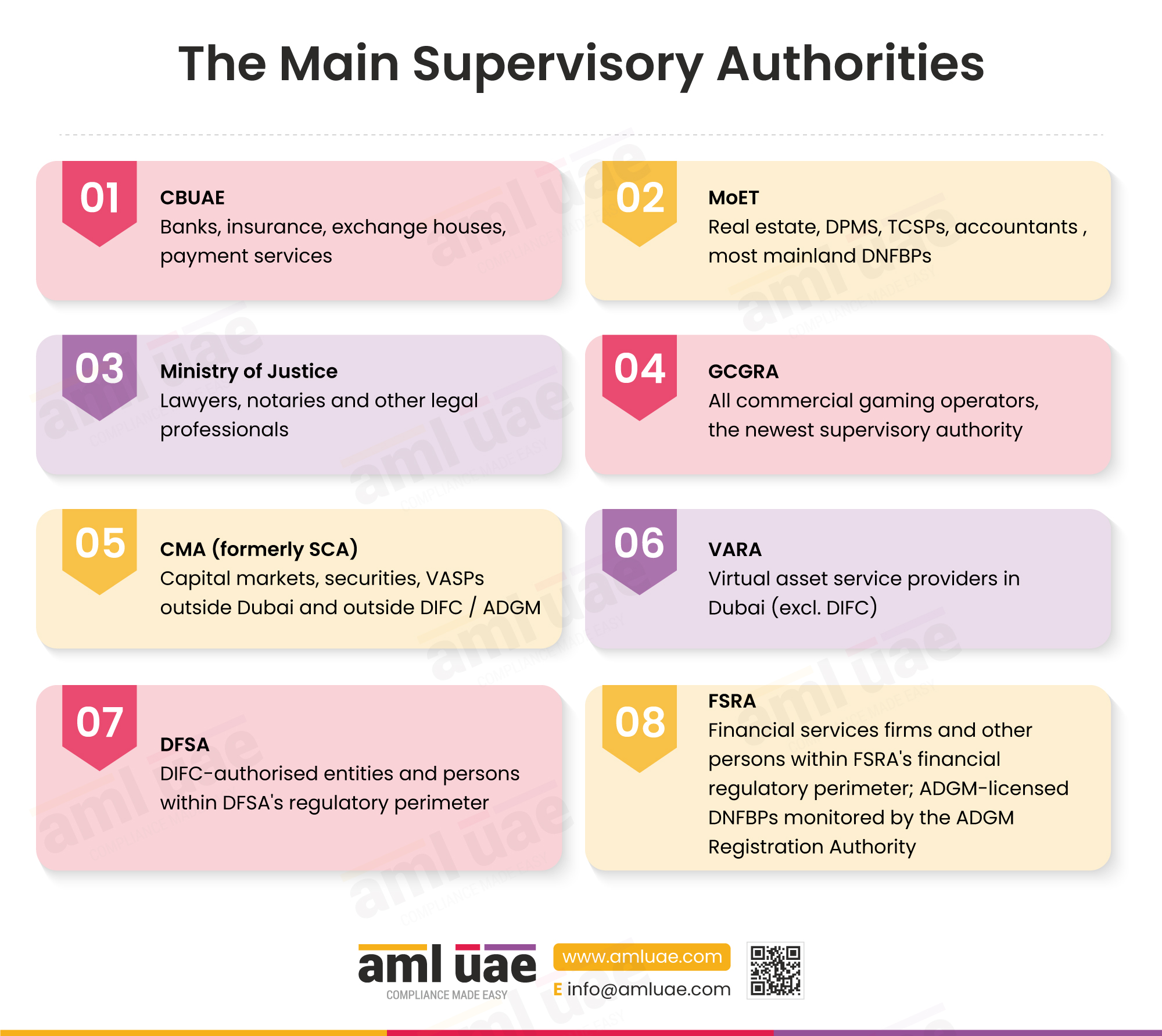

AML Supervisory Authority for Commercial Gaming Operators in UAE

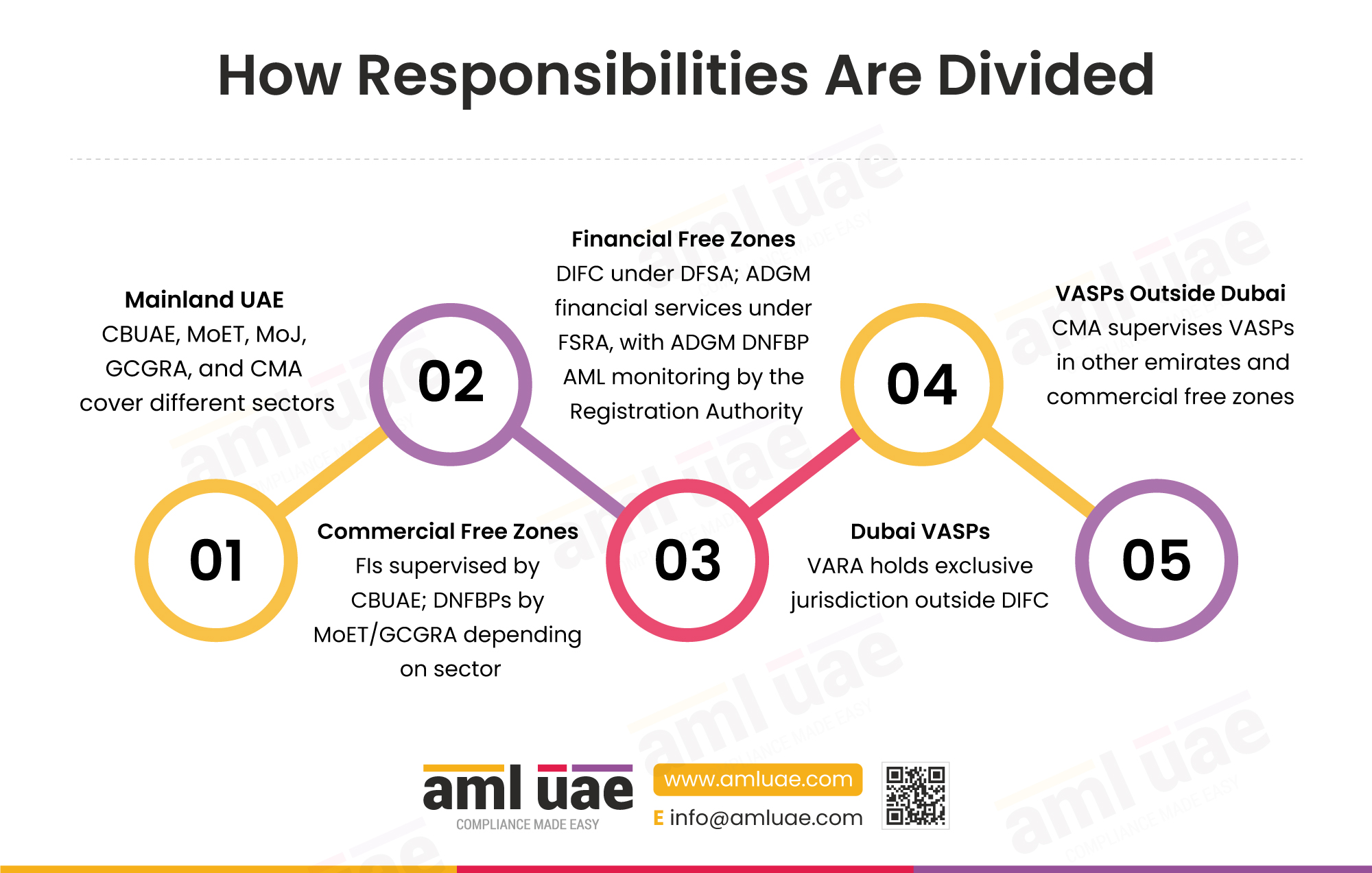

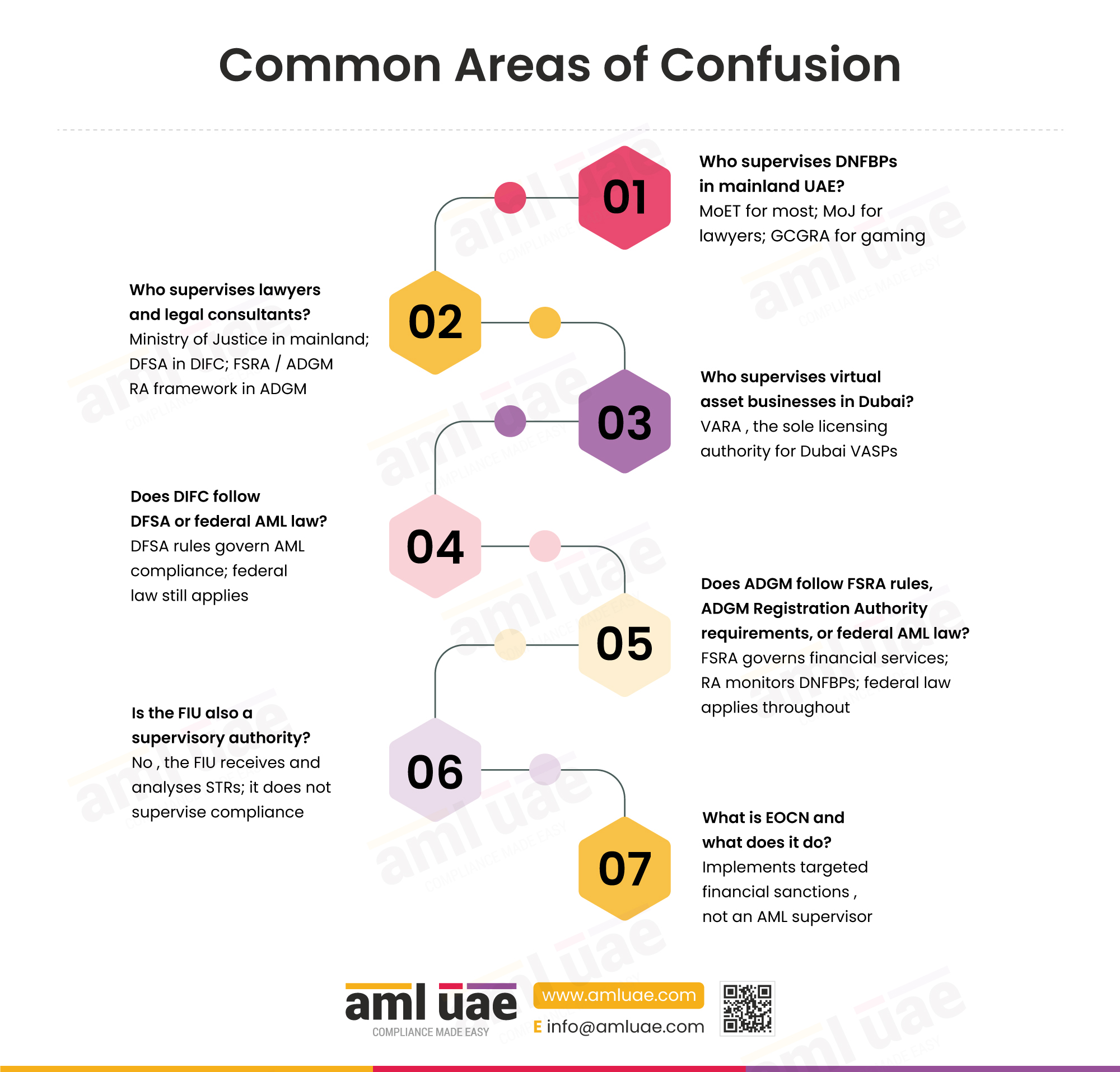

The AML supervisory authority for commercial gaming operators in UAE is the General Commercial Gaming Regulatory Authority. Paragraph 234 of the UAE ML/TF National Risk Assessment 2024 records that the authority was established in September 2023, and paragraph 241 treats its creation as a prudent step in anticipating commercial gaming activity. Because there were no licensed entities at the time of the National Risk Assessment, paragraph 234 also notes that the sector was not separately evaluated. GCGRA is therefore the first and only AML/CFT supervisor for commercial gaming in the UAE, with no overlap with the Ministry of Economy DNFBP supervision covered elsewhere in the DNFBPs cluster.

GCGRA’s role in AML supervision draws on the general competencies of a Supervisory Authority set out in Federal Decree-Law No. (10) of 2025. Article (16) of the Decree-Law requires each Supervisory Authority to assess ML/TF risks in its sector, supervise financial institutions and DNFBPs under its jurisdiction, provide guidance, impose administrative penalties and maintain statistics. For commercial gaming the authority has expressed those competencies through the 2025 Commercial Gaming Policy Paper and ongoing licensing conditions.

What GCGRA does as AML/CFT supervisor

The General Commercial Gaming Regulatory Authority exercises the standard Supervisory Authority powers under Federal Decree-Law No. (10) of 2025, applied to a sector-specific risk profile.

1. Sector risk assessment

2. Licensing and fit-and-proper controls

3. AML/CFT supervision and inspection

4. Policy, guidance and typologies

5. Administrative penalties

6. Coordination with FIU and EOCN

1. Sole AML supervisor for commercial gaming

GCGRA is the only federal body designated to supervise commercial gaming operators for AML/CFT in the UAE. This avoids the overlap seen in other DNFBP sectors where Ministry of Economy supervision runs alongside free zone regulators.

2. Supervisory competencies under Federal Decree-Law No. (10) of 2025

Article (16) of Federal Decree-Law No. (10) of 2025 sets out the competencies of a Supervisory Authority, including assessing ML/TF risks, conducting AML/CFT supervision, issuing guidance, imposing administrative penalties and maintaining statistics. GCGRA exercises these powers for commercial gaming.

3. Coordination with the FIU

The Financial Intelligence Unit within the Central Bank, established under Article (11) of Federal Decree-Law No. (10) of 2025, remains the sole recipient of suspicious transaction reports via the goAML system. GCGRA supervises the reporting culture; it does not receive STRs directly.

4. Coordination with EOCN on sanctions

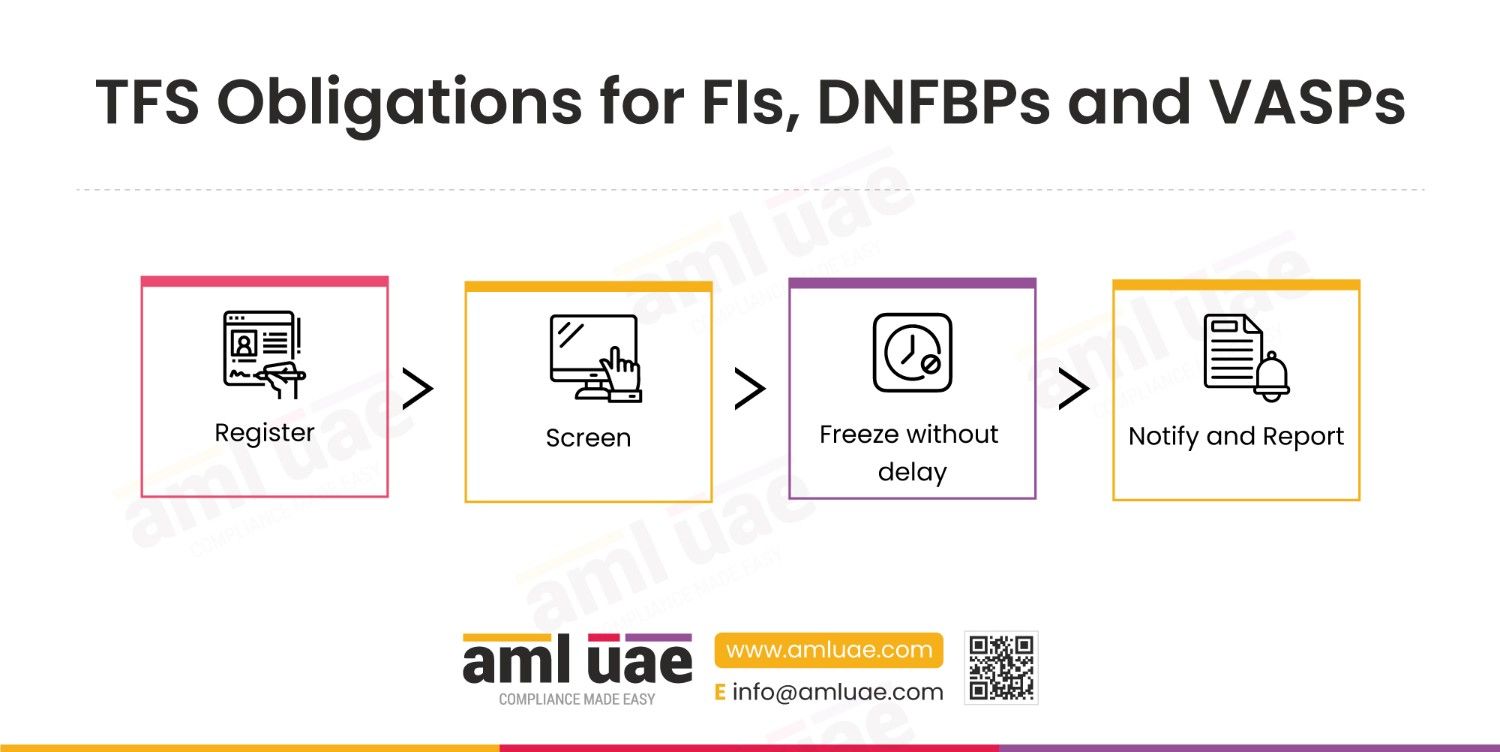

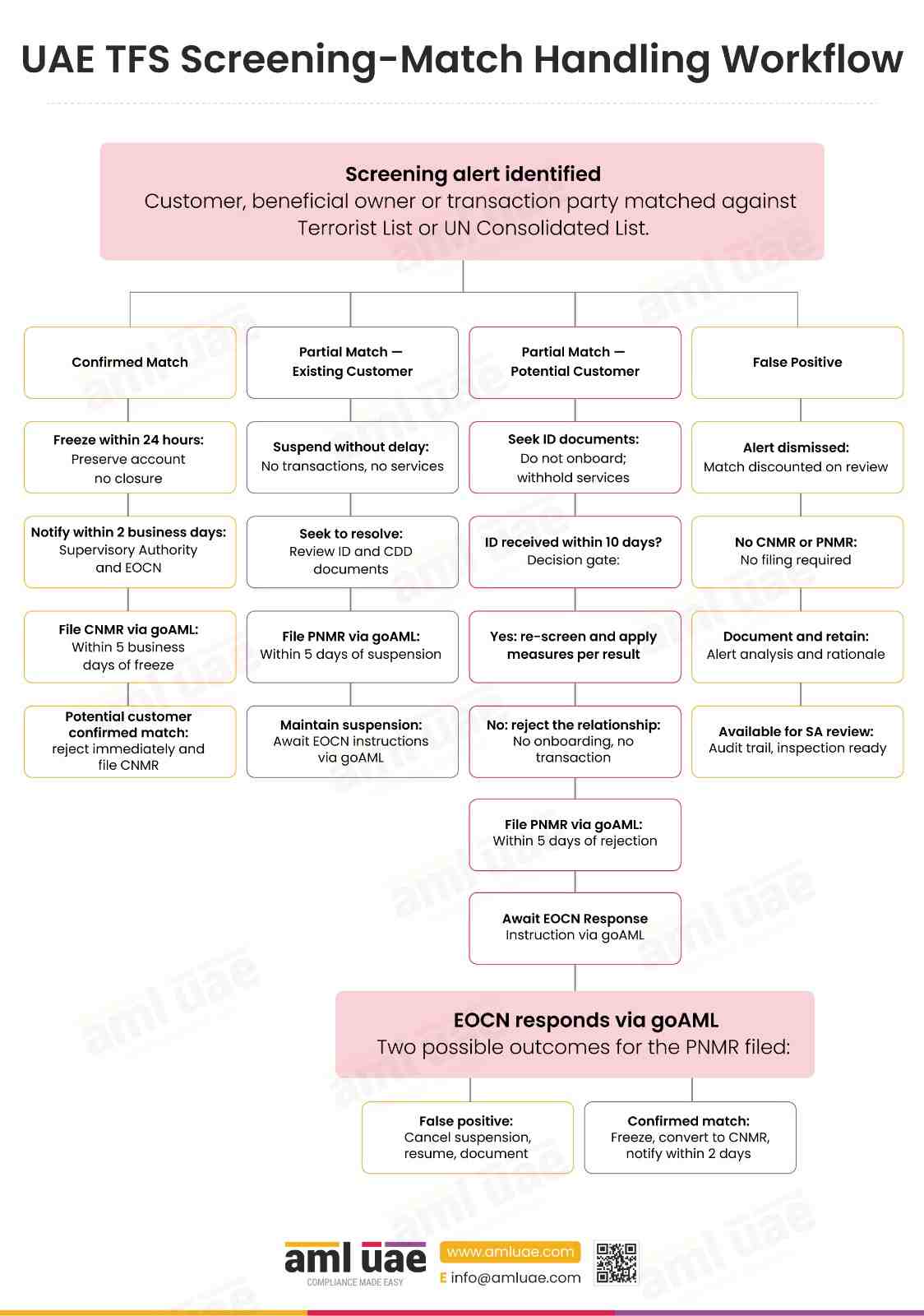

The Executive Office for Control and Non-Proliferation issues and updates the Targeted Financial Sanctions regime. GCGRA expects commercial gaming operators to screen against the UAE Local Terrorist List and UN Security Council Consolidated List in accordance with Cabinet Decision No. (74) of 2020.

Supervisory context

Because commercial gaming has no UAE operating history and no licensed population at the time of the 2024 National Risk Assessment, GCGRA’s early supervisory approach relies heavily on the 2025 Commercial Gaming Policy Paper and cross-sector overarching guidance rather than sector-specific typologies.

Planning your GCGRA AML programme?

Our team helps commercial gaming licensees stand up AML governance, ERA, CDD workflows, sanctions screening and MLRO frameworks that map to GCGRA expectations.

Talk to AML UAE about commercial gaming compliance →

AML Regulations Applicable to Commercial Gaming Operators in UAE

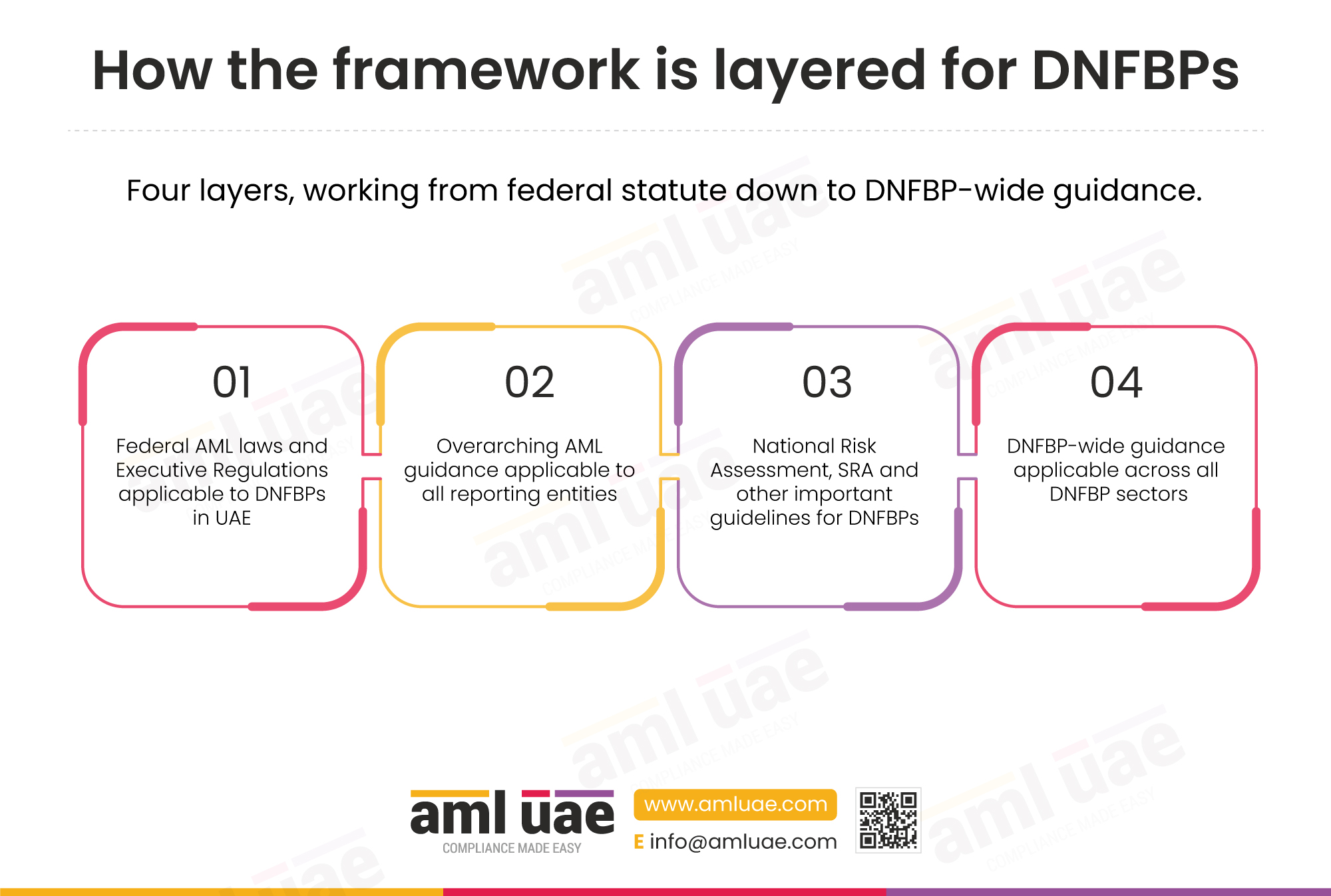

AML regulations for commercial gaming operators in UAE combine four layers of source material. Federal laws and executive regulations form the mandatory baseline; overarching sanctions, proliferation financing and typology guidance add cross-sector expectations; the UAE National Risk Assessment sets country-level context; and the 2025 Commercial Gaming Policy Paper provides sector-specific direction. This page captures all four layers so that GCGRA licensees can see the full compliance perimeter in one place.

The four layers of AML rules that apply to commercial gaming

Read them as a stack: federal laws create the obligation, overarching guidance fills in the sanctions and proliferation financing detail, and sector documents translate them into gaming-specific controls.

1. Federal AML laws and executive regulations

2. Overarching AML, TFS and PF guidance

3. National Risk Assessment 2024

4. Sector-specific Commercial Gaming Policy Paper 2025

Federal AML Laws and Executive Regulations Applicable to Commercial Gaming Operators

Federal laws and executive regulations are the mandatory AML baseline for commercial gaming operators in the UAE. The Decree-Law and its Executive Regulations establish obligations on customer due diligence, beneficial owner identification, suspicious transaction reporting, record-keeping, sanctions compliance and administrative penalties. The terrorism, beneficial owner and penalty frameworks complete the picture.

Federal AML laws and executive regulations at a glance

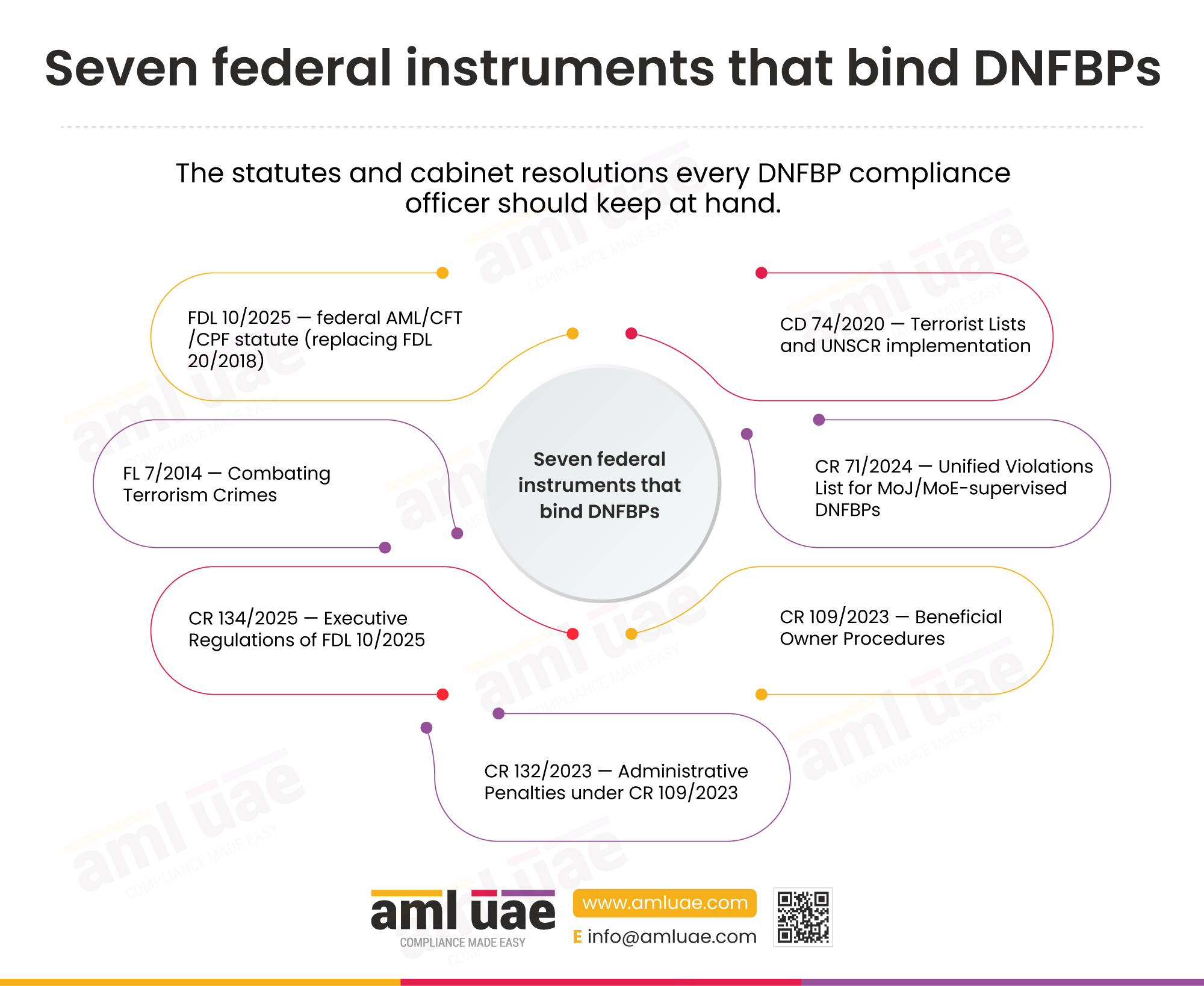

Seven mandatory federal instruments underpin AML regulations for commercial gaming operators in UAE.

01 Federal Decree-Law No. (10) of 2025

02 Federal Law No. (7) of 2014

03 Cabinet Resolution No. (134) of 2025

04 Cabinet Decision No. (74) of 2020

05 Cabinet Decision No. (109) of 2023

06 Cabinet Resolution No. (132) of 2023

Federal Decree by Law No. (10) of 2025 Regarding Anti-Money Laundering, and Combating the Financing of Terrorism and Proliferation Financing

2025

Federal Decree-Law No. (10) of 2025 on Combating Money Laundering, Terrorist Financing and Proliferation Financing

Issued by: UAE Federal Government

The primary federal AML law. It defines the money laundering, terrorist financing and proliferation financing offences; establishes the Financial Intelligence Unit at the Central Bank under Article (11); sets out Supervisory Authority competencies under Article (16); requires reporting of suspicious transactions under Article (18); and imposes criminal and administrative penalties, with administrative fines ranging from AED 10,000 to AED 5,000,000 per violation under Article (17).

Key citation: Articles (11), (16), (17), (18) and (28) to (35).

Federal Law No. (7) of 2014 Combating Terrorism Crimes

2014

Federal Law No. (7) of 2014 Combating Terrorism Crimes

Issued by: UAE Federal Government

Sets the substantive terrorism offences that sit behind the terrorist financing offence in Federal Decree-Law No. (10) of 2025. For gaming operators it matters because CDD, sanctions screening and STR obligations all anchor in whether a patron or counterparty is connected to terrorism offences defined in this law.

Key citation: Definitions of terrorist act, terrorist offence and terrorist organisation.

Cabinet Resolution No. (134) of 2025 Concerning the Executive Regulations of Federal Decree-Law No. (10) of 2025

2025

Cabinet Resolution No. (134) of 2025 (Executive Regulations of the AML Decree-Law)

Issued by: UAE Cabinet

The operational rulebook for the AML Decree-Law. It lists the DNFBPs (including commercial gaming operators with the AED 11,000 trigger) under Article (3); sets the risk assessment obligation in Article (5); details CDD and beneficial owner identification in Articles (6) to (10); requires PEP handling in Article (16); mandates STR reporting and non-disclosure in Articles (17) to (19); governs third-party reliance in Article (20); demands internal policies and training in Article (21); requires appointment of a Compliance Officer in Article (22); addresses high-risk countries in Article (23); covers new technologies in Article (24); and sets the minimum five-year record-keeping period in Article (25).

Key citation: Article (3) Item (1) is the DNFBP entry for commercial gaming; AED 11,000 threshold and chip carve-out.

Cabinet Decision No. (74) of 2020 Regarding Terrorism Lists Regulation and Implementation of UN Security Council Resolutions on the Suppression and Combating of Terrorism, Terrorist Financing, Countering the Proliferation of Weapons of Mass Destruction and related resolutions

2020

Cabinet Decision No. (74) of 2020 on Terrorism Lists and UN Sanctions

Issued by: UAE Cabinet

The core targeted financial sanctions instrument. It governs the UAE Local Terrorist List and the implementation of UN Security Council Consolidated Lists on terrorism, terrorist financing and proliferation financing. Commercial gaming operators must screen patrons and counterparties against these lists, freeze assets without delay and report matches to the Executive Office for Control and Non-Proliferation.

Key citation: Freezing without delay, reporting to the Executive Office, and implementation of UN resolutions.

Cabinet Decision No. (109) of 2023 on Regulating the Beneficial Owner Procedures

2023

Cabinet Decision No. (109) of 2023 on Regulating the Beneficial Owner Procedures

Issued by: UAE Cabinet

The beneficial owner regime applicable to legal persons in the UAE. Commercial gaming operators that are legal persons must maintain and file beneficial owner and real beneficiary registers in line with this decision, update them on change, and provide the data to the Registrar and competent authorities as required.

Key citation: Obligation to maintain and disclose Real Beneficiary and Shareholder registers; 25 per cent ownership/control test.

Cabinet Resolution No. (132) of 2023 Concerning Administrative Penalties for Violations of Cabinet Resolution No. (109) of 2023 on the Regulation of Beneficial Owner Procedures

2023

Cabinet Resolution No. (132) of 2023 on Administrative Penalties for Beneficial Owner Violations

Issued by: UAE Cabinet

Sets graduated administrative penalties for failures to maintain and disclose beneficial owner information under Cabinet Decision No. (109) of 2023. Commercial gaming operators should treat beneficial owner breaches as material, not procedural, given the penalty structure.

Key citation: Written warning, financial penalty and suspension of activities for repeated or serious breaches.

Decoding the federal AML stack for your gaming licence?

We translate Federal Decree-Law No. (10) of 2025 and Cabinet Resolution No. (134) of 2025 into practical policies, risk matrices and monitoring rules calibrated to commercial gaming.

See our AML compliance services →

Overarching AML Guidance Applicable to Commercial Gaming Operators in the UAE

Overarching guidance extends the federal baseline with cross-sector expectations on targeted financial sanctions, proliferation financing, terrorist financing red flags, virtual asset provider risks and practical supervisory conduct. Each document is valid until specifically repealed; where it was issued under the prior AML law, it continues to apply to the extent consistent with Federal Decree-Law No. (10) of 2025 and Cabinet Resolution No. (134) of 2025.

Overarching AML guidance at a glance

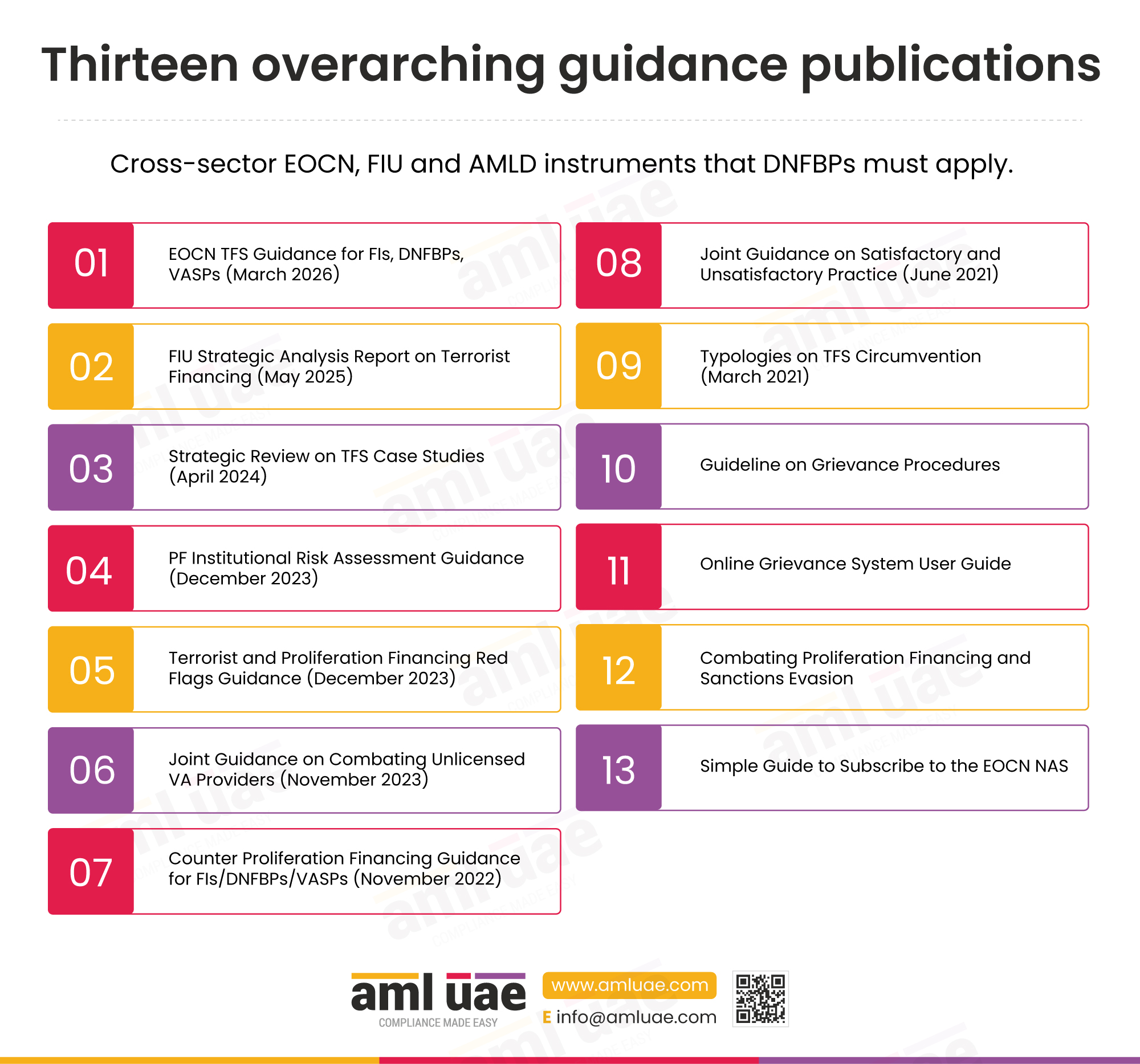

Thirteen cross-sector guidance documents that commercial gaming operators must read into their own AML programme.

01 EOCN TFS Guidance (2026)

02 FIU TF Strategic Analysis (2025)

03 TFS Case Studies Review (2024)

04 PF Institutional Risk Assessment Guidance (2023)

05 Terrorist and PF Red Flags (2023)

06 Unlicensed VASP Joint Guidance (2023)

07 Counter Proliferation Financing Guidance (2022)

08 Satisfactory and Unsatisfactory Practice (2021)

09 TFS Typology Paper (2021)

10 Guideline on Grievance Procedures

11 Online Grievance System User Guide

12 Combating PF and Sanctions Evasion

13 NAS Subscription Simple Guide

Guidance on Targeted Financial Sanctions for Financial Institutions, DNFBPs and VASPs – March 2026

March 2026

Guidance on Targeted Financial Sanctions for FIs, DNFBPs and VASPs

Issued by: Executive Office for Control and Non-Proliferation (EOCN)

The consolidated EOCN guidance on implementing targeted financial sanctions. It explains freezing without delay, rejection and reporting obligations, the role of the UAE Local Terrorist List and UN Consolidated List, registration for the Notification Alert System, and expectations on screening, governance and testing. Commercial gaming operators must build their sanctions programme to this document.

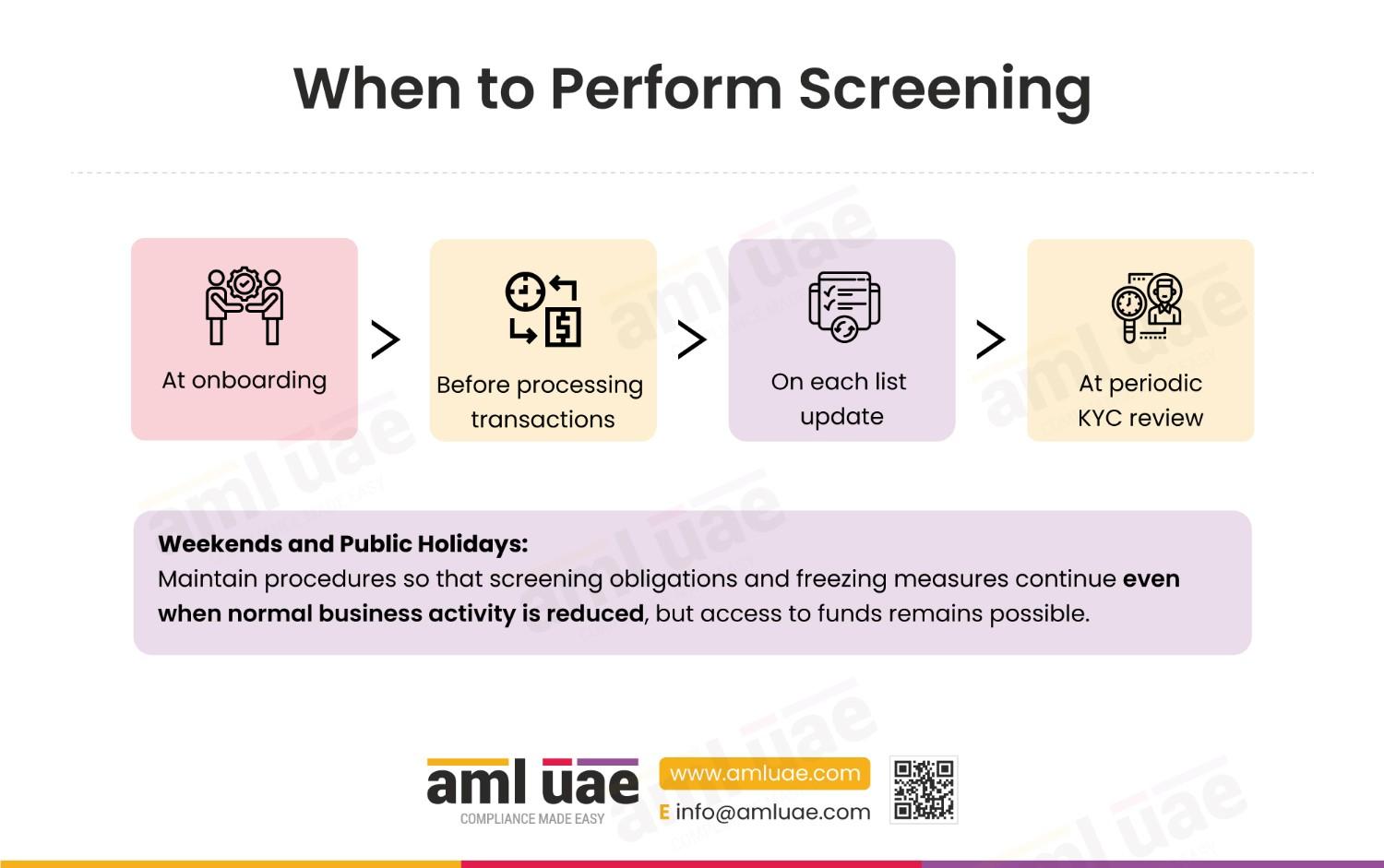

Key citation: Freezing without delay; NAS registration; screening at onboarding and on list updates.

FIU’s Strategic Analysis Report on Terrorist Financing – May 2025

May 2025

FIU Strategic Analysis Report on Terrorist Financing

Issued by: UAE Financial Intelligence Unit

Sets out the FIU’s strategic view of terrorist financing typologies, red flags and reporting patterns in the UAE. Gaming operators should feed this into transaction monitoring rules, EDD triggers and training, particularly for high-risk jurisdiction patronage and cash-heavy activity.

Key citation: Strategic TF typologies and red flags relevant to patron profiling.

Strategic Review on Targeted Financial Sanctions Case Studies – April 2024

April 2024 (IEC-SR.01.22 series)

Strategic Review on Targeted Financial Sanctions Case Studies

Issued by: Executive Office for Control and Non-Proliferation (EOCN)

Case-study based review of TFS implementation practice, covering asset-freezing failures, partial matches, false positives and typologies of evasion. Useful for gaming operators when calibrating screening thresholds and name-matching logic.

Key citation: Sanctions evasion typologies and screening quality expectations.

Proliferation Finance Institutional Risk Assessment Guidance for FIs, DNFBPs and VASPs – December 2023

December 2023

Proliferation Finance Institutional Risk Assessment Guidance

Issued by: Executive Office for Control and Non-Proliferation (EOCN)

Walks firms through conducting a proliferation financing institutional risk assessment. Commercial gaming operators should use it to build their own PF IRA, covering country, customer, product, channel and transaction risks, and linking conclusions to controls.

Key citation: Five-factor PF IRA framework and control linkage.

Terrorist and Proliferation Financing Red Flags Guidance – December 2023

December 2023

Terrorist and Proliferation Financing Red Flags Guidance

Issued by: Supervisory Authority Sub-Committee

A practical catalogue of red flag indicators for terrorist financing and proliferation financing, covering customer behaviour, transaction patterns, geographies and document anomalies. Directly usable as monitoring rule inputs for commercial gaming.

Key citation: Red flag catalogue for TF and PF.

Joint Guidance on Combating the Use of Unlicensed Virtual Asset Providers in the UAE – November 2023

March 2022, updated 2023

Joint Guidance on Combating the Use of Unlicensed Virtual Asset Providers

Issued by: Joint issuance by UAE supervisory authorities

Warns supervised firms against dealing with or enabling unlicensed virtual asset service providers. Relevant for gaming operators that consider VA payment rails, token integrations or patrons whose source of funds includes virtual assets.

Key citation: No dealings with unlicensed VASPs; risk-based screening of VA payment flows.

Guidance on Counter Proliferation Financing for FIs, DNFBPs and VASPs – November 2022

March 2022

Guidance on Counter Proliferation Financing

Issued by: Executive Office for Control and Non-Proliferation (EOCN)

Core PF typology and controls guidance, covering dual-use goods, front companies, trade-based PF and sanctions evasion. Commercial gaming operators use it primarily for PF EDD scenarios and to support their PF IRA.

Key citation: PF typologies and control expectations for DNFBPs.

Joint Guidance – Satisfactory/Unsatisfactory Practice – June 2021

June 2021

Joint Guidance on Satisfactory and Unsatisfactory Practice

Issued by: Joint issuance by UAE supervisory authorities

Contrasts satisfactory versus unsatisfactory AML practice across governance, CDD, EDD, monitoring, reporting, sanctions and training. Provides a useful supervisory lens for gaming operators benchmarking their controls during mobilisation.

Key citation: Satisfactory vs unsatisfactory AML practice examples.

Typologies on the Circumvention of Targeted Sanctions against Terrorism and the Proliferation of Weapons of Mass Destruction – March 2021

March 2021

TFS Typology Paper

Issued by: Executive Office for Control and Non-Proliferation (EOCN)

Typology paper on how designated persons and entities attempt to circumvent targeted financial sanctions. Gaming operators use it to shape red flag scenarios, EDD questionnaires and internal training.

Key citation: Sanctions evasion typologies.

Guideline on Grievance Procedures

Updated periodically

Guideline on Grievance Procedures

Issued by: Executive Office for Control and Non-Proliferation (EOCN)

Explains the delisting and grievance process for persons subject to targeted financial sanctions. Relevant when a patron contests a listing or a freeze; operators must route such grievances through the prescribed procedure rather than adjusting controls unilaterally.

Key citation: Formal grievance and delisting workflow.

Online Grievance System User Guide

Updated periodically

Online Grievance System User Guide

Issued by: Executive Office for Control and Non-Proliferation (EOCN)

Practical user guide to the EOCN online grievance platform. Supports the formal delisting procedure with step-by-step instructions that compliance teams can reference when handling patron grievances.

Key citation: Online grievance submission flow.

Combating Proliferation Financing and Sanctions Evasion

Updated periodically

Combating Proliferation Financing and Sanctions Evasion

Issued by: Executive Office for Control and Non-Proliferation (EOCN)

Companion document to the PF guidance that deepens the discussion of sanctions evasion tactics and the regulatory expectation that DNFBPs integrate PF controls into their AML programmes.

Key citation: Sanctions evasion detection and PF programme integration.

Simple Guide to Subscribe to the EOCN Notification Alert System (NAS)

Updated periodically

NAS Subscription Simple Guide

Issued by: Executive Office for Control and Non-Proliferation (EOCN)

Step-by-step guide for DNFBPs to register for the EOCN Notification Alert System so that they receive list updates without delay. Subscription to NAS is the operational foundation of freezing without delay under Cabinet Decision No. (74) of 2020.

Key citation: NAS registration underpins the freezing without delay obligation.

Bring the overarching guidance into your sanctions and PF playbooks

We turn EOCN TFS, PF and typology guidance into concrete screening rules, PF IRAs and freezing playbooks that survive supervisory inspection.

Contact us now →

NRA, SRA and Other Important Guidelines Applicable to Commercial Gaming Operators

The UAE’s National Risk Assessment is the country-level evidence base that supervisors, DNFBPs and financial institutions draw on for their enterprise risk assessments. For commercial gaming operators, it is also the document that explicitly acknowledges that their sector had no licensed population at the point of assessment, and that GCGRA was only recently formed.

UAE ML/TF National Risk Assessment – 2024

2024

UAE ML/TF National Risk Assessment

Issued by: Executive Office of Anti-Money Laundering and Countering the Financing of Terrorism

Country-level assessment of money laundering and terrorist financing risks, threats, vulnerabilities and controls across sectors. Paragraph 234 records that GCGRA was introduced in September 2023 and that the commercial gaming sector was not evaluated because there were no licensed entities at the time. Paragraph 235 flags the need to develop a robust regulatory and supervisory framework aligned with FATF expectations. Paragraph 241 treats GCGRA’s establishment as a prudent step.

Key citation: Paragraphs 234, 235 and 241 on commercial gaming and GCGRA.

Sector-Specific Guidelines Applicable to Commercial Gaming Operators in UAE

The sector-specific guidance for commercial gaming operators in UAE is the 2025 Commercial Gaming Policy Paper. It sits below the federal law and the overarching guidance, and translates them into controls that match the ML/TF risk profile of commercial gaming.

Policy Paper – Commercial Gaming Policy (2025)

2025

Policy Paper on Commercial Gaming

Issued by: General Secretariat of the National AML/CFT Policies Committee (GSNAMLCFTPC)

The founding sector paper for commercial gaming AML/CFT in the UAE. It identifies the key ML/TF risks for the sector (anonymous transactions, exploitation of player accounts, use of third-party payments, foreign jurisdiction patronage, multiple payment methods, casino value instruments, VIP programmes, employee complicity and cash usage); designates GCGRA as the sole AML/CFT supervisor; and sets out a requirements table covering governance, institutional risk assessment, patron risk classification, PDD at the AED 11,000 threshold, EDD for high-risk categories, record-keeping of at least five years, MLRO appointment, suspicious activity reporting, sanctions screening and technical controls including ISO 27001 alignment and vulnerability assessment and penetration testing.

Key citation: Nine ML/TF sector risks; AML requirements table across governance, CDD, EDD, reporting and technical controls.

Operationalise the 2025 Commercial Gaming Policy Paper

AML UAE helps GCGRA licensees convert the sector paper into a documented AML programme, sanctions framework, PDD/EDD workflows and technical control baseline.

Speak to our commercial gaming compliance team →

Conclusion

The AML regulations for commercial gaming operators in UAE are mature on paper and new in practice. The perimeter is set by Cabinet Resolution No. (134) of 2025, the controls are anchored in Federal Decree-Law No. (10) of 2025, the sanctions and proliferation financing backbone is provided by Cabinet Decision No. (74) of 2020 and the EOCN guidance suite, and the sector-specific translation is delivered by the 2025 Commercial Gaming Policy Paper. GCGRA is the sole AML/CFT supervisor for the sector and is expected to adopt a risk-based supervisory approach as licensees go live.

For the first wave of GCGRA licensees, the practical compliance priorities are clear: build an enterprise risk assessment that takes the nine sector risks in the 2025 Policy Paper; stand up a DNFBP-grade CDD programme keyed to the AED 11,000 trigger; hard-wire sanctions screening and freezing without delay using NAS; integrate PF controls from the outset; appoint a Compliance Officer and MLRO under Article (22) of Cabinet Resolution No. (134) of 2025; and maintain records for at least five years under Article (25). Getting these right from day one will matter more than any retrospective remediation once supervision intensifies.

FAQs on AML Regulations for Commercial Gaming Operators in UAE

Are commercial gaming operators covered by UAE AML law?

Yes. Commercial gaming operators are covered under UAE AML law. Cabinet Resolution No. (134) of 2025, Article (3) Item (1) places them within the DNFBP perimeter once a single transaction or linked transactions reach AED 11,000. Transactions that involve only gaming chips or gaming instruments are not treated as financial transactions for this purpose.

Licensed commercial gaming operators must comply with the full DNFBP obligation set under Federal Decree-Law No. (10) of 2025 and Cabinet Resolution No. (134) of 2025, including CDD, EDD, sanctions screening, STR reporting and five-year record-keeping.

Which regulator is relevant for commercial gaming and AML in the UAE?

The General Commercial Gaming Regulatory Authority (GCGRA) is the sole AML/CFT supervisor for commercial gaming operators in the UAE. The UAE ML/TF National Risk Assessment 2024 (paragraph 234) confirms that the authority was established in September 2023.

GCGRA exercises the Supervisory Authority competencies set out in Article 16 of Federal Decree-Law No. (10) of 2025, coordinates with the FIU at the Central Bank for STRs and with the Executive Office for Control and Non-Proliferation on targeted financial sanctions.

What AML controls should a gaming operator build first?

A commercial gaming operator should start with six controls, all traceable to Cabinet Resolution No. (134) of 2025 and the 2025 Commercial Gaming Policy Paper: an enterprise risk assessment under Article (5); CDD and beneficial owner identification under Articles (6) to (10); PEP handling under Article (16); sanctions screening under Cabinet Decision No. (74) of 2020; STR filing via goAML under Articles (17) to (19); and record-keeping under Article (25).

These should be supported by the appointment of a Compliance Officer under Article (22), written internal policies under Article (21), training, and technical controls aligned with the 2025 Commercial Gaming Policy Paper’s ISO 27001 and VAPT expectations.

How should gaming firms approach source of funds checks?

Source of funds and source of wealth checks flow from Articles (6) to (10) and Article (16) of Cabinet Resolution No. (134) of 2025, supported by the 2025 Commercial Gaming Policy Paper’s treatment of patron risk and EDD. At onboarding, the operator collects and verifies funding information proportionate to patron risk; for higher-risk patrons, PEPs or those from higher-risk jurisdictions, enhanced evidence is required.

Ongoing source of funds review should be triggered by threshold breaches, unusual patterns, matches against EOCN and UN lists, and red flags drawn from the Terrorist and PF Red Flags Guidance of December 2023 and the FIU’s May 2025 Strategic Analysis Report on Terrorist Financing.

Was this guide useful?

If this article helped you map AML expectations for commercial gaming in the UAE, a short Google review means a great deal.

Leave a review for AML UAE.

Share via :