AML Laws in UAE: Complete Guide to AML/CFT Legislation 2026

Published On: 03/17/2026

Protect your business with reliable and effective AML strategies with AML UAE.

Last Reviewed On: 07/20/2026 | Last Updated On: 07/20/2026

Key Highlights:

- Federal Decree Law No. (10) of 2025 is the principal regulation dealing with AML/CFT/CPF in the UAE

- Cabinet Resolution No. (134) of 2025 is the implementing regulation of the Federal Decree Law No. (10) of 2025

- The respective supervisory authorities issue sector-specific guidelines

- ADGM and DIFC have their Own Rulebooks, and regulated entities operating from financial free zones must follow Federal Law in addition to these rulebooks

A guide to Anti Money Laundering AML Laws in UAE | 2026

The UAE’s AML framework requires regulated entities to identify customers, assess risk, monitor transactions, screen for sanctions and terrorism financing, and report suspicious activity to the UAE FIU through goAML, supported by strong governance, training, and audit controls.

It is critical to combat money laundering and terrorism financing and safeguard the economy. In these efforts to identify and mitigate the financial crime risks, here is the comprehensive guide to Anti-Money Laundering (AML) Laws in the UAE for various regulated entities.

AML/CFT/CPF Legal Framework in the UAE

As part of the UAE government’s efforts to fight these financial crimes, AML/CFT regulations have been issued, supported by detailed guidelines from various supervisory authorities that lay down the principles and best practices for identifying financial crime instances and mitigating the risks, in accordance with the federal AML regulations.

Federal AML/CFT/CPF Laws and Executive Regulations

The Federal AML/CFT/CPF laws and executive regulations apply to banks, financial institutions, DNFBPs, and VASPs operating in the mainland and free zones (commercial as well as financial free zones).

The following are the key AML regulations setting the foundation for the regulated entities to detect and mitigate the ML/FT and PF risks:

- Federal Decree by Law No. (10) of 2025 Regarding Anti-Money Laundering, and Combating the Financing of Terrorism and Proliferation Financing

The federal decree law lays down the foundation for the Financial Intelligence Unit (FIU), AML supervisory authorities, and the regulated entities. It also defines the financial crime offences subject to conviction in the UAE, the expectations from regulated entities regarding combating financial crime, and the measures that the FIU and supervisory authorities can/must undertake to ensure effective enforcement of the AML regulations, including the powers entrusted to the authorities. - Cabinet Resolution No. (134) of 2025 Concerning the Executive Regulations of Federal Decree-Law No. (10) of 2025 Concerning Combating Money Laundering, Terrorist Financing, and the Financing of the Proliferation of Weapons

The cabinet decision prescribes the regulations governing how the provisions of the federal decree law are to be implemented by regulated entities to identify and manage financial crime risk. This set of regulations covers the procedures and controls entities must adopt for AML/CFT and CPF. - Federal Law No. (7) of 2014 Combating Terrorism Crimes

The law defines the activities that shall be construed as a terrorism crime and the corresponding penalties. - Cabinet Decision No. 74 of 2020 Regarding Terrorism Lists Regulation and Implementation of UN Security Council Resolutions on the Suppression and Combating of Terrorism, Terrorist Financing, Countering the Proliferation of Weapons of Mass Destruction and related resolutions

This cabinet decision discusses the processes, procedures, and controls for the effective implementation of the targeted financial sanctions program by regulated entities in the UAE. Moreover, it provides for the functions and powers of the relevant authorities in the UAE to issue the Local Terrorist List and enforce it, as well as to effectively administer the UNSC sanctions directives. - Cabinet Resolution No. (71) of 2024 Regulating Violations, Administrative Penalties Imposed on Violators of Measures for Confronting Money Laundering and Combating Financing of Terrorism Subject to the Control of the Ministry of Justice and the Ministry of Economy

The cabinet resolution sets out the penalties that regulated entities would be subject to for non-compliance with federal AML regulations. This applies only to entities subject to supervision by the Ministry of Economy and Tourism (MoET) and the Ministry of Justice (MoJ), i.e., the Designated Non-Financial Businesses and Professions, except for commercial gaming operators. - Cabinet Decision No. (109) of 2023 On Regulating the Beneficial Owner Procedures

Though not directly affecting the AML function, this cabinet decision requires all legal entities in the UAE to adequately disclose, document, and maintain data on their ultimate beneficial owners (UBOs). - Cabinet Resolution No. (132) of 2023 Concerning the Administrative Penalties against Violators of The Provisions of the Cabinet Resolution No. (109) of 2023 Concerning the Regulation of Beneficial Owner Procedures

The administrative fines and penalties for violations of the UBO disclosure and transparency requirements (as required under Cabinet Decision No. (109) of 2023) are set out in this cabinet resolution.

NRA, SRA, and Other Important Guidelines

UAE ML/FT National Risk Assessment

UAE PF National Risk Assessment

The above-referred-to NRAs outline the outcomes of the UAE’s national assessment of financial crime vulnerabilities, threats, and risks across various sectors. It also evaluates the quality of the controls deployed by these regulated sectors to manage the risks.

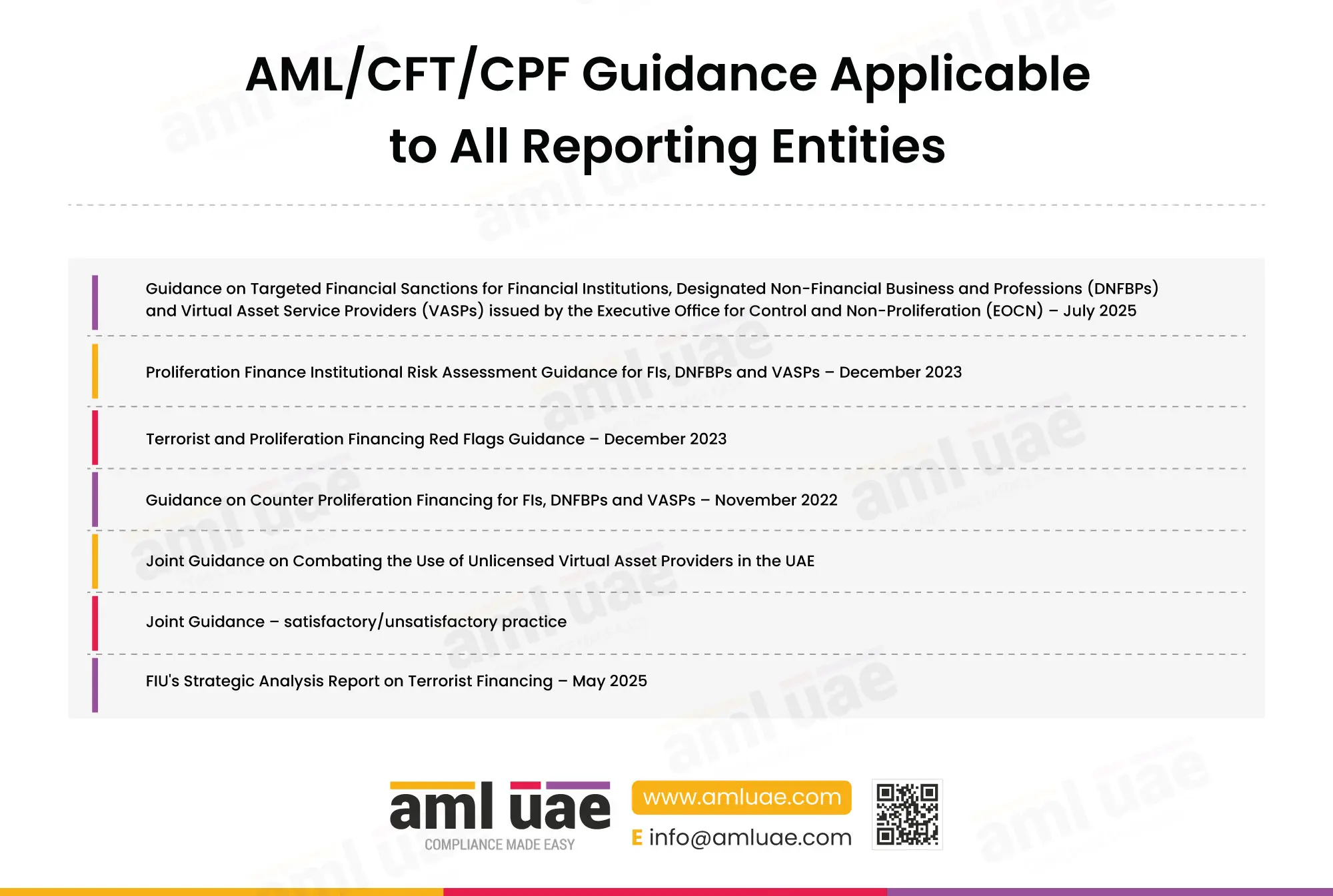

AML/CFT/CPF Guidance Applicable to All Reporting Entities

The following are the key AML/CFT/CPF and TFS-related guidance and guidelines issued by the concerned authorities, which are relevant to all the regulated entities and guide them in the effective implementation of the federal regulations:

- Guidance on Targeted Financial Sanctions for Financial Institutions, Designated Non-Financial Business and Professions (DNFBPs) and Virtual Asset Service Providers (VASPs) issued by the Executive Office for Control and Non-Proliferation (EOCN) – July 2025

This guideline aims to clarify the TFS obligations of the regulated entities and seeks to define the scope of the TFS measures, including the specific obligations of subscribing to the EOCN’s Notification Alert System, screening against the local and UNSC lists, applying the freezing measures and reporting the designated person. - Proliferation Finance Institutional Risk Assessment Guidance for FIs, DNFBPs and VASPs – December 2023

The guidance aims to provide focused assistance to regulated entities in identifying, assessing, and managing profiling financing risk. - Terrorist and Proliferation Financing Red Flags Guidance – December 2023

The guidance document lists the TF and PF red flags intended to assist regulated entities in identifying and detecting suspicious TF and PF activities. - Guidance on Counter Proliferation Financing for FIs, DNFBPs and VASPs – November 2022

Guidance is issued by EOCN to help regulated entities understand the threats, risks, and vulnerabilities of PF and to identify, assess, and mitigate PF risks. - Joint Guidance on Combating the Use of Unlicensed Virtual Asset Providers in the UAE – November 2023

This joint guidance document has been issued by NAMLCFTC to educate financial institutions, DNFBPs, VASPs, and the public at large about the risks associated with unlicensed virtual asset service providers. The joint guidance expects the regulated entities and the public to report unlicensed virtual asset activities through the whistleblowing mechanism. - Joint Guidance – satisfactory/unsatisfactory practice – June 2021

Various supervisory authorities observed common themes during inspections from January 2020 to May 2021. Common themes regarding “Satisfactory/Unsatisfactory” practices observed during inspections are outlined in the Joint Guidance, relevant for financial institutions and DNFBPs. - FIU’s Strategic Analysis Report on Terrorist Financing – May 2025

The report has been drawn by the FIU based on the SARs and STRs received over 4 4-year period (from 2021 to 2024). It covers TF-related trends and typologies and aims to guide regulated entities in identifying TF-related activities.

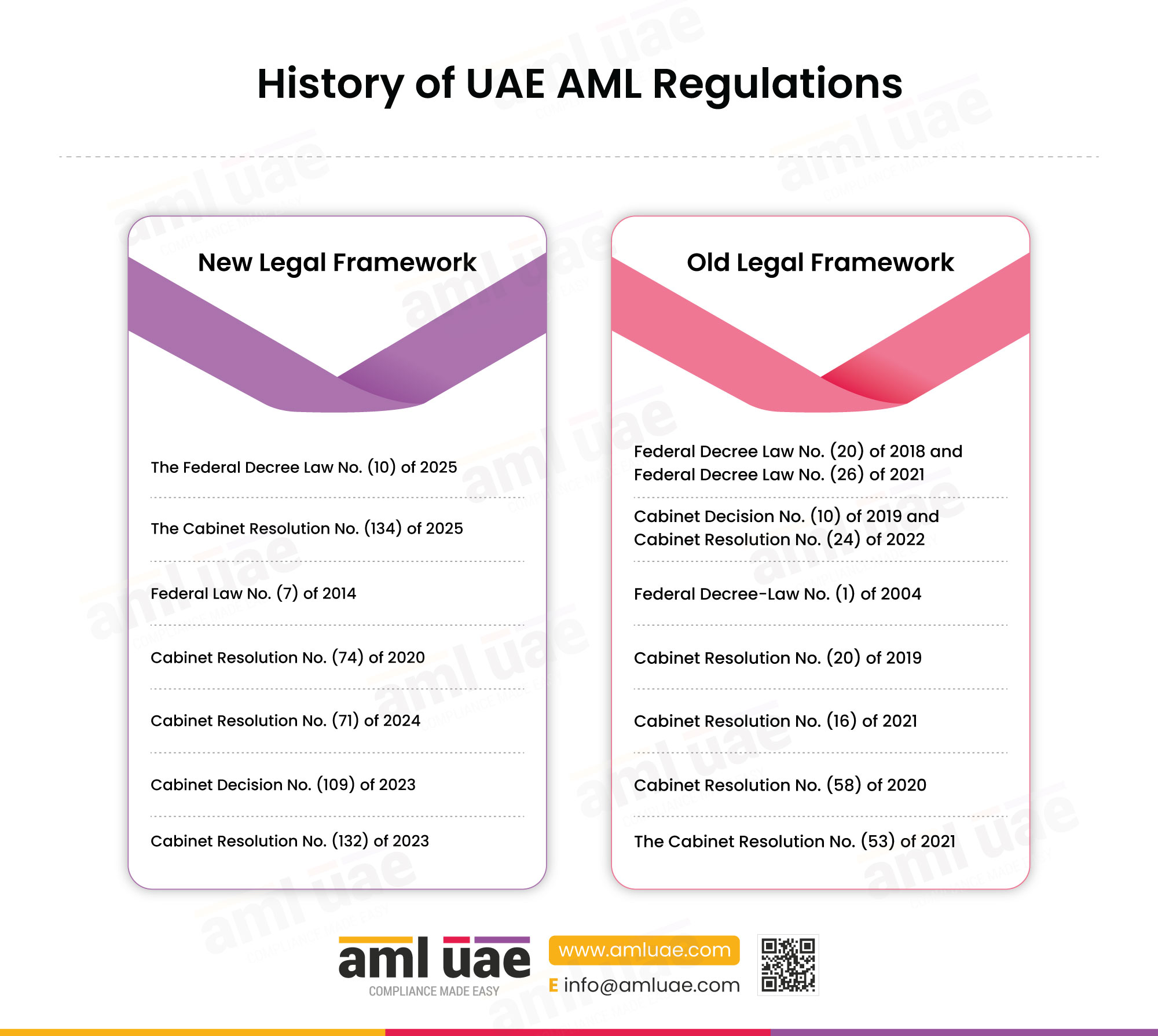

History of UAE AML Regulations

- The Federal Decree Law No. (10) of 2025 came into effect from October 14, 2025, and it repealed Federal Decree Law No. (20) of 2018 and Federal Decree Law No. (26) of 2021 (amendments to the 2018 AML law).

- The Cabinet Resolution No. (134) of 2025 came into effect from December 14, 2025, and it repealed Cabinet Decision No. (10) of 2019 and Cabinet Resolution No. (24) of 2022 (amendments to the 2019 Executive Regulation).

- Federal Law No. (7) of 2014 Combating Terrorism Crimes came into effect from 1st September 2024, and it repealed Federal Decree-Law No. (1) of 2004 on Combating Terrorist Crimes.

- Cabinet Resolution No. (74) of 2020 Regulating the Terrorist Lists and Implementing the Security Council’s Resolutions Regarding the Prevention and Suppression of Terrorism and its Financing and Proliferation of Armaments and the related Resolutions came into force with effect from 29th October 2020, and it repealed Cabinet Resolution No. (20) of 2019 Concerning the Regulation of Terrorism lists and the application of the Security Council resolutions and the relevant resolutions on the prevention, suppression of terrorism and its financing and the cessation of weapon proliferation and its financing & the Relevant Resolutions.

- Cabinet Resolution No. (71) of 2024 Regulating Violations, Administrative Penalties Imposed on Violators of Measures for Confronting Money Laundering and Combating Financing of Terrorism Subject to the Control of Ministry of Justice and Ministry of Economy came into force with effect from 8th July 2024, and it repealed the Cabinet Resolution No. (16) of 2021 Concerning the Unified List of Violations and Administrative Fines Imposed on Violators of Measures for Confronting Money Laundering and Combating the Financing of Terrorism Who are Under the Control of the Ministry of Justice and Ministry of Economy.

- Cabinet Decision No. (109) of 2023 On Regulating the Beneficial Owner Procedures came into force on 6th November 2023, and it repealed the Cabinet Resolution No. (58) of 2020 regulating Real Beneficiary Procedures.

- Cabinet Resolution No. (132) of 2023 Concerning the Administrative Penalties against Violators of The Provisions of the Cabinet Resolution No. (109) of 2023 Concerning the Regulation of Beneficial Owner Procedures came into force with effect from 30th December 2023, and it repealed The Cabinet Resolution No. (53) of 2021 concerning Administrative Penalties imposed on Violators of the provisions of Cabinet Resolution No. (58) of 2020 concerning Regulating Real Beneficiary procedures.

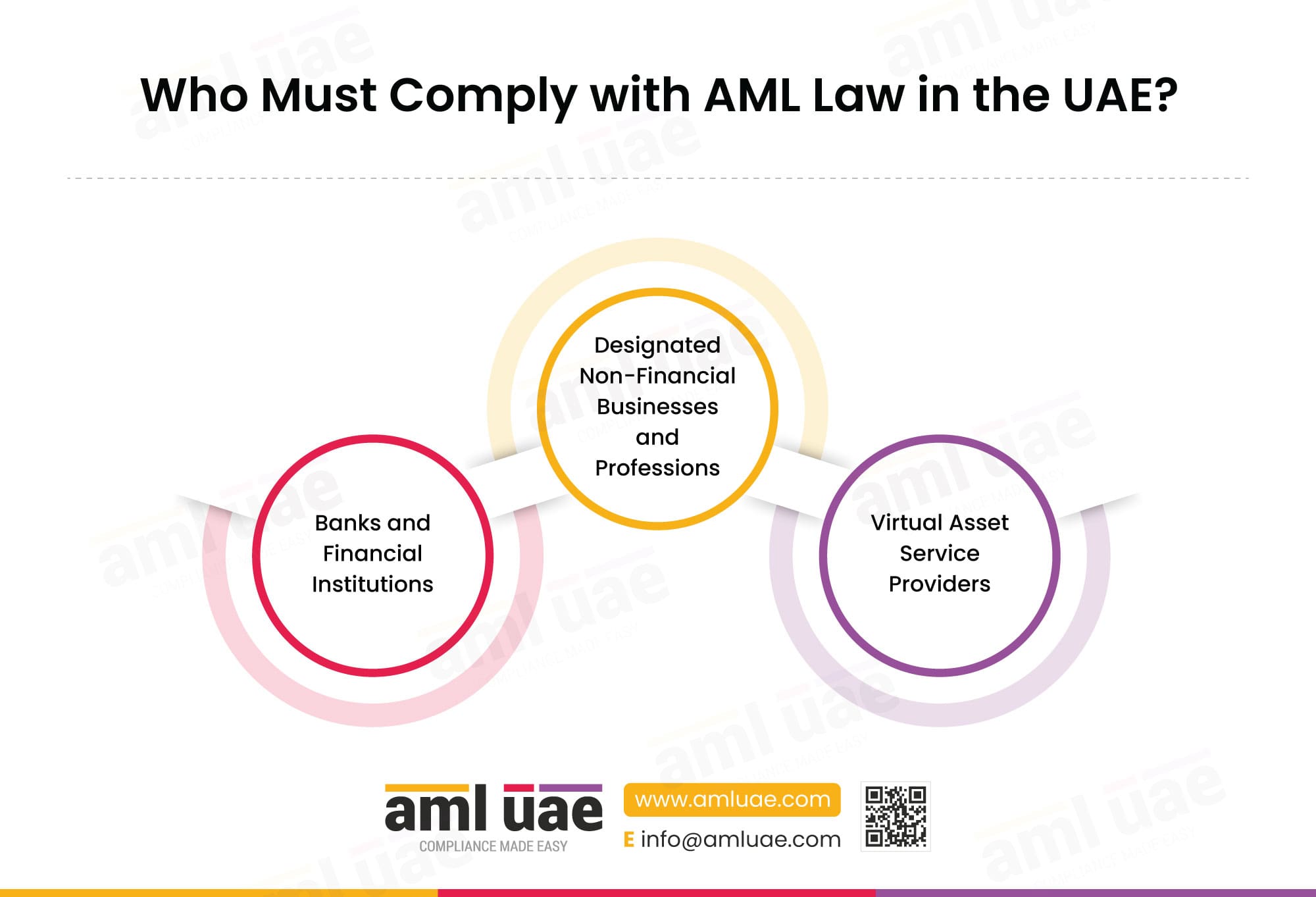

Who Must Comply with AML Law in the UAE?

The AML Law in the UAE applies to Financial Institutions, Designated Non-Financial Businesses and Professions (DNFBPs), and Virtual Asset Services Providers (VASPs).

AML/CFT Covered Activities for Banks and Financial Institutions

The Financial Institutions undertaking the following activities would be subject to AML compliance:

- Accepting deposits and other repayable funds from the public.

- Lending, including consumer credit and mortgage lending and financing commercial transactions, including the purchase of export bills and debts.

- Financial leasing, excluding financial leasing related to consumer products.

- Money or value transfer services.

- Issuing and managing means of payment, such as debit cards, credit cards, cheques, payment orders, banker’s drafts, and electronic money.

- Financial guarantees and commitments.

- Trading in money market instruments such as cheques, bills of exchange, certificates of deposit, derivatives and related instruments; or foreign exchange; or currency, interest rate and index instruments; or other financial derivatives; or negotiable financial instruments; and trading in commodity futures contracts.

- Participating in securities issuance and providing financial services related to such issuances.

- Managing funds and portfolios of all types.

- Safekeeping and administration of cash or liquid securities on behalf of others.

- Other operations involving investment, management, or administration of funds or money on behalf of others.

- Underwriting or subscribing to life insurance policies and other investment-related insurance products, including those provided by insurance agents and brokers.

- Currency exchange.

AML/CFT Covered Activities for Designated Non-Financial Businesses and Professions (DNFBPs)

The Designated Non-Financial Businesses and Professions include:

- Real estate brokers and agents conduct transactions related to the purchase or sale of real estate on behalf of their customers.

- Dealers in precious metals and stones.

- Lawyers, notaries, other independent legal professionals, and independent accountants, when preparing, conducting, or executing financial transactions:

- Purchase and sale of real estate.

- Management of funds owned by the Customer.

- Management of bank accounts, savings accounts, or securities accounts.

- Organising contributions for the creation, operation, or management of companies.

- Creating, operating, or managing juristic persons or Legal Arrangements, or the sale or purchase of business entities.

- Company and trust service providers, when carrying out a transaction in relation to the following activities:

- Acting as an agent in the incorporation or creation of legal persons.

- Acting, or arranging for another person to act, as a director or secretary of a company, or as a partner or in an equivalent position in another legal person.

- Providing a registered office, business address, residence, correspondence address, or administrative address for a company, another legal person, or a legal arrangement.

- Acting, or arranging for another person to act, as a Trustee of an express trust or performing an equivalent function for another form of legal arrangement.

- Acting, or arranging for another person to act, as a nominee shareholder for another person.

- Operators of Commercial Games (included in the definition of the DNFBP vide Cabinet Decision No. (134) of 2025, effective December 14, 2025.)

AML/CFT Covered Activities for Virtual Asset Service Providers (VASPs) in UAE

Virtual Asset Service Providers shall be subject to AML compliance when undertaking the following activities:

- Exchange between Virtual Assets and fiat currencies.

- Exchange between one or more types of virtual assets.

- Transfer of virtual assets.

- Safekeeping or administration of virtual assets or instruments enabling control over virtual assets.

- Providing financial services or activities related to the issuer’s offering, sale, or participation in virtual assets.

AML/CFT Supervisory Authorities in the UAE

For overseeing the enforcement of the above-mentioned federal AML regulations and also to issue the relevant guidance to the supervised entities under their respective purview in line with the powers granted under the federal AML regulations, the following authorities have been designated as the AML Supervisory Authorities:

Supervised Entities | Supervisory Authority | Jurisdictions |

Financial Institutions | Central Bank of the UAE | Entire UAE (except financial freezones) |

Trusts and Company Service Providers | Ministry of Economy and Tourism | Entire UAE (except financial freezones) |

Dealers in Precious Metals and Stones | Ministry of Economy and Tourism | Entire UAE (except financial freezones) |

Independent Auditors and Accountants | Ministry of Economy and Tourism | Entire UAE (except financial freezones) |

Real Estate Brokers and Agents | Ministry of Economy and Tourism | Entire UAE (except financial freezones) |

Lawyers, Notaries and Legal Consultants | Ministry of Justice | Entire UAE (except financial freezones) |

Capital Market | Capital Market Authority | Entire UAE (except DIFC and ADGM) |

Virtual Asset Service Providers | Capital Market Authority | Entire UAE (except Dubai) |

Virtual Assets Regulatory Authority | Emirate of Dubai (except DIFC) | |

All regulated entities in DIFC | Dubai Financial Services Authority | DIFC |

All regulated entities in ADGM | Financial Services Regulatory Authority | ADGM |

Operators of Commercial Games | General Commercial Gaming Regulatory Authority | Entire UAE (except financial freezones) |

Financial Intelligence Unit (FIU): While the above-mentioned authorities supervise AML implementation by regulated entities, the Financial Intelligence Unit (FIU) remains the central reporting authority from an AML perspective, irrespective of the nature of the business or the location of operations in the UAE.

Executive Office for Control and Non-Proliferation (EOCN): The authority enforcing the targeted financial sanctions regime in the UAE is the EOCN, which is also receiving, reviewing and guiding the regulated entities on implementing the TFS and evaluating the reports made by the regulated entities related to sanctions match (reporting is done through the goAML Portal only).

Sector-Specific AML/CFT/CPF Legal Framework in the UAE

The regulatory framework for AML/CFT/CFP in the UAE is structured across multiple sectors, each governed by dedicated laws, executive regulations, supervisory authorities, and guidance frameworks.

The UAE’s AML/CFT framework imposes comprehensive obligations on a wide spectrum of entities. While all regulated sectors must adhere to the core federal legislation, i.e., Federal Decree-Law No. (10) of 2025 and Cabinet Resolution No. (134) of 2025, they are also subject to detailed sector-specific laws, regulations, and guidance from their respective authorities.

To simplify navigation of this landscape, the following consolidates the primary legislation, rulebooks, circulars, guidelines, compliance publications, and regulatory bodies across all sectors.

AML/CFT/CPF Legal Framework for Designated Non-Financial Businesses and Professions (DNFBPS)

DNFBPs encompass a range of non-financial businesses and professions that are particularly vulnerable to money laundering, terrorism financing, and proliferation financing due to the nature of the products or services they offer. These entities, which include dealers in precious metals, real estate agents, legal professionals, corporate service providers, independent accountants and auditors, and operators of commercial games must comply with federal AML/CFT laws, as well as the sector-specific regulations issued by their respective supervisory authorities.

All DNFBPs have to adhere to:

- Federal AML/CFT/CPF Laws and Executive Regulations

- AML/CFT/CPF Guidance Applicable to All Reporting Entities

- NRA, SRA, and Other Important Guidelines

- AML/CFT Guidelines for Designated Non-Financial Businesses and Professions – September 2025

The MoET has issued this detailed guideline to provide DNFBPs with an organised methodology and procedures to identify risks, implement measures to mitigate them, streamline the AML governance framework, and enhance the quality of AML reporting.

- Implementation Guide For DNFBPs on Customer Risk Assessment (CRA) – November 2024

The guide focuses on the customer risk assessment process that DNFBPs must perform as part of customer onboarding. It elaborates on the CRA methodology and the risk factors that different DNFBPs must consider.

- Implementation Guide For DNFBPs on Customer Due Diligence (CDD) – November 2024

This guide provides practical insights into the CDD process that DNFBPs follow. It aims to assist entities with their day-to-day challenges related to CDD and to guide them on international best practices for CDD.

- Circular No. (2) of 2022 regarding Implementation of Targeted Financial Sanctions (TFS) on UNSCRs 1718 (2006) and 2231 (2015)

To ensure compliance with obligations under Cabinet Decision No. 74 of 2020.

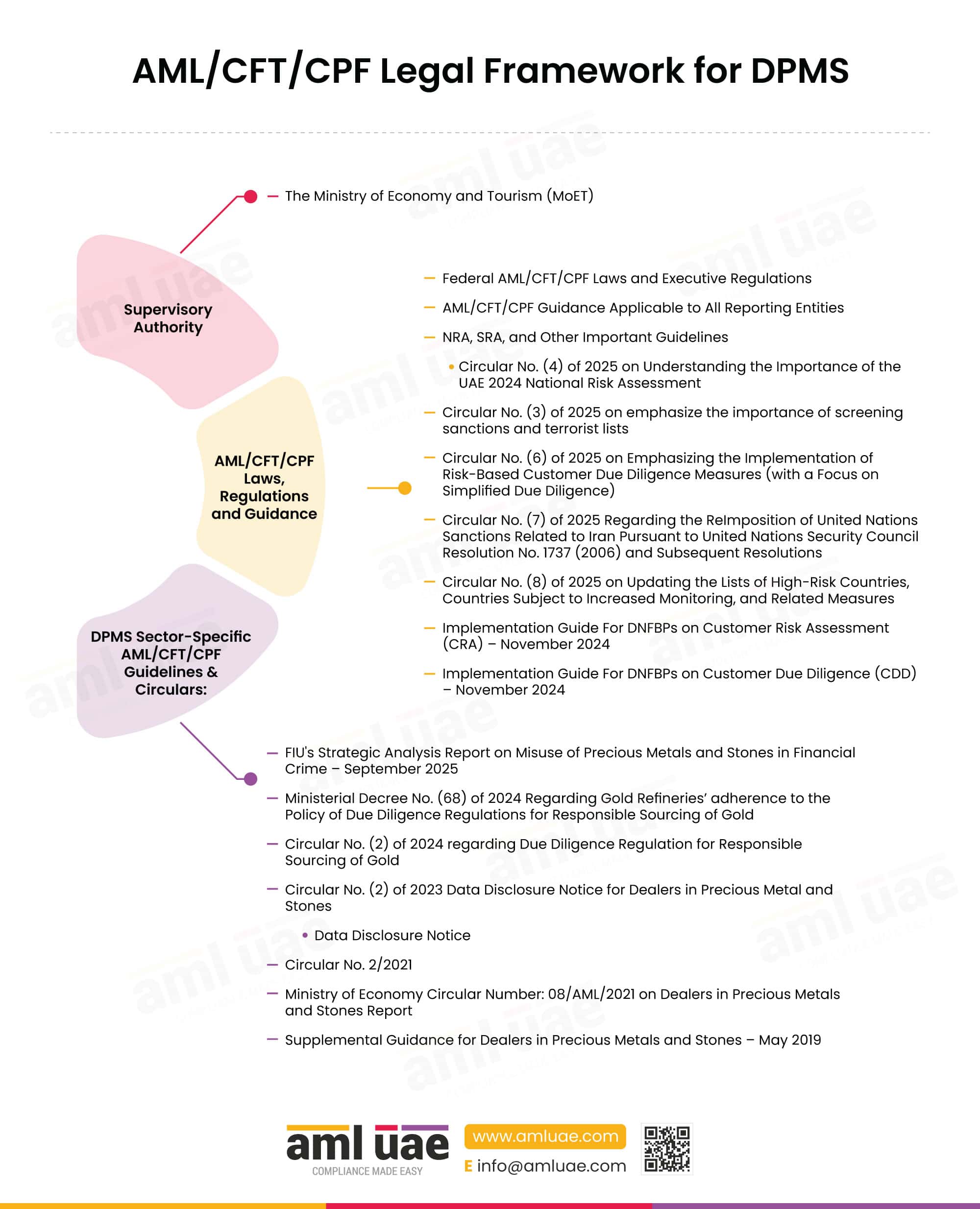

AML/CFT/CPF Legal Framework for Dealers in Precious Metals & Stones (DPMS)

Supervisory Authority for Dealers in Precious Metals and Stones Sector:

The Ministry of Economy and Tourism (MoET) is the AML supervisory authority for the dealers in the precious metals and stones sector operating in and from the UAE Mainland and the commercial free zones.

AML/CFT/CPF Laws, Regulations and Guidance Applicable to DPMS Sector:

- Federal AML/CFT/CPF Laws and Executive Regulations

- AML/CFT/CPF Guidance Applicable to All Reporting Entities

- NRA, SRA, and Other Important Guidelines In the context of the NRA, DPMS are required to adhere to Circular No. (4) of 2025 on Understanding the Importance of the UAE 2024 National Risk Assessment to meet the expectations set out applicable to their sector.

- AML/CFT Guidelines for Designated Non-Financial Businesses and Professions – September 2025

- Circular No. (3) of 2025 on emphasize the importance of screening sanctions and terrorist lists

- Circular No. (6) of 2025 on Emphasizing the Implementation of Risk-Based Customer Due Diligence Measures (with a Focus on Simplified Due Diligence)This circular provides reference to the Implementation Guide for DNFBPs on CDD and CRA (November 2024).

- Circular No. (7) of 2025 Regarding the ReImposition of United Nations Sanctions Related to Iran Pursuant to United Nations Security Council Resolution No. 1737 (2006) and Subsequent Resolutions

- Circular No. (8) of 2025 on Updating the Lists of High-Risk Countries, Countries Subject to Increased Monitoring, and Related Measures.

- Implementation Guide For DNFBPs on Customer Risk Assessment (CRA) – November 2024

- Implementation Guide For DNFBPs on Customer Due Diligence (CDD) – November 2024

DPMS Sector-Specific AML/CFT/CPF Guidelines & Circulars:

Along with the above-referred federal decree laws and implementing regulations, and cabinet decisions, the DPMS is required to adhere to the following guidance documents and relevant ministerial decrees:

- FIU’s Strategic Analysis Report on Misuse of Precious Metals and Stones in Financial Crime – September 2025

This report by FIU discusses the typologies relevant to the exploitation of dealers in precious metals and stones for financial crimes.

- Ministerial Decree No. (68) of 2024 Regarding Gold Refineries’ adherence to the Policy of Due Diligence Regulations for Responsible Sourcing of Gold

Calls on businesses engaged in activities pertaining to refining gold or recycling the same, and stakeholders in the supply chain, to put in place strong company management systems and adopt a customised policy to ensure due diligence on gold supply chains. Identify and assess risks within gold supply chains, design and implement management strategies to mitigate risks in the gold supply chains. DPMS must also ensure the appointment of an independent third-party auditor to conduct due diligence of the gold supply chain and submit the report on the same.

- Circular No. (2) of 2024 regarding Due Diligence Regulation for Responsible Sourcing of Gold

The circular calls for all Gold Refineries licensed in the UAE to follow the 5-step framework of the Due Diligence Regulation for Responsible Sourcing of Gold.

- Circular No. (2) of 2023 Data Disclosure Notice FOR Dealers in precious metals and stones

- Ministry of Economy Circular Number: 08/AML/2021 on Dealers in Precious Metals and Stones Report

The DPMS are required to mandatorily report precious metals and stones transactions involving cash or international wire transfer that exceed the specified amount on the goAML Portal.

- Circular No. 2/2021 Calls for the implementation of AML/CFT obligations by DPMS and explains the supervisory authority’s procedures for onsite and offsite inspection for the compliance of the same.

- Supplemental Guidance for Dealers in Precious Metals and Stones – May 2019

The supplemental guidance document is to be read with the above-mentioned DNFBP guidelines. This supplemental guidance details the DPMS activities that shall be subject to AML compliance. It also includes certain illustrations of the sectoral abuse for money laundering and terrorism financing.

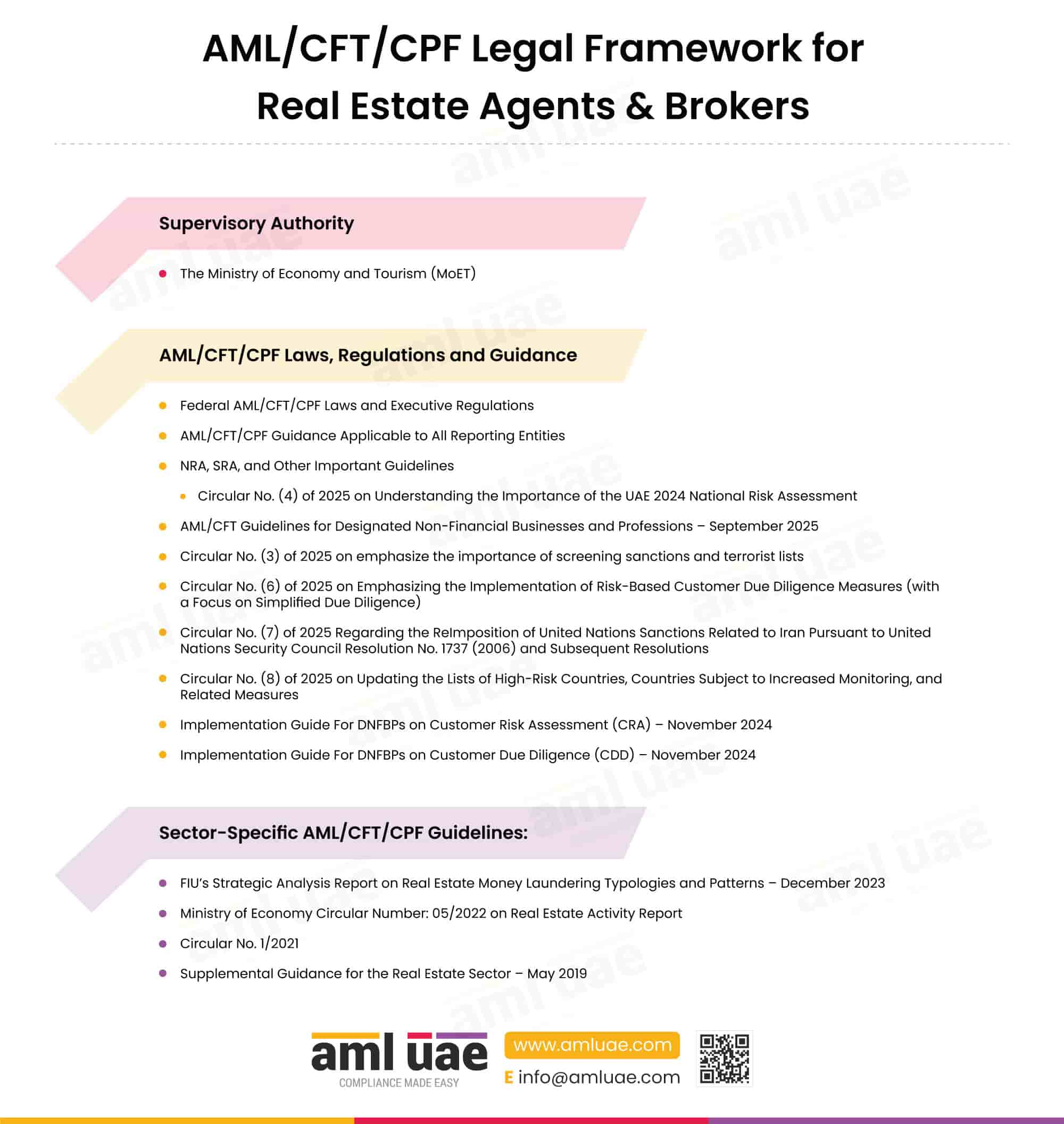

AML/CFT/CPF Legal Framework for Real Estate Agents & Brokers

Supervisory Authority for Real Estate Brokers and Agents:

The Ministry of Economy and Tourism (MoET) is the AML supervisory authority for real estate agents and brokers operating in the UAE (except those licensed and operating from DIFC and ADGM).

AML/CFT/CPF Laws, Regulations and Guidance Applicable to Real Estate Sector:

- Federal AML/CFT/CPF Laws and Executive Regulations

- AML/CFT/CPF Guidance Applicable to All Reporting Entities

- NRA, SRA, and Other Important Guidelines In the context of the NRA, Real Estate Agents and Brokers are required to adhere to Circular No. (4) of 2025 on Understanding the Importance of the UAE 2024 National Risk Assessment to meet the expectations set out applicable to their sector.

- AML/CFT Guidelines for Designated Non-Financial Businesses and Professions – September 2025

- Circular No. (3) of 2025 on emphasize the importance of screening sanctions and terrorist lists

- Circular No. (6) of 2025 on Emphasizing the Implementation of Risk-Based Customer Due Diligence Measures (with a Focus on Simplified Due Diligence) This circular provides reference to the Implementation Guide for DNFBPs on CDD and CRA (November 2024)

- Circular No. (7) of 2025 Regarding the ReImposition of United Nations Sanctions Related to Iran Pursuant to United Nations Security Council Resolution No. 1737 (2006) and Subsequent Resolutions

- Circular No. (8) of 2025 on Updating the Lists of High-Risk Countries, Countries Subject to Increased Monitoring, and Related Measures.

- Implementation Guide For DNFBPs on Customer Risk Assessment (CRA) – November 2024

- Implementation Guide For DNFBPs on Customer Due Diligence (CDD) – November 2024.

Real Estate Sector-Specific AML/CFT/CPF Guidelines & Circulars

Real estate agents and brokers are required to comply with the additional guidance documents, in addition to the above-referred federal decree laws, implementing regulations, and cabinet decisions.

- FIU’s Strategic Analysis Report on Real Estate Money Laundering Typologies and Patterns – December 2023

This strategic report by FIU discusses the common typologies and trends used in exploiting the real estate sector.

- Ministry of Economy Circular Number: 05/2022 on Real Estate Activity Report

By way of this circular, real estate agents and brokers are obligated to an additional reporting requirement when a freehold property transaction is settled in cash or a virtual asset above the specified threshold.

- Circular No. 1/2021 Calls for the implementation of AML/CFT obligations by real estate agents and brokers and explains the supervisory authority’s procedures for onsite and offsite inspection for the compliance of the same.

- Supplemental Guidance for the Real Estate Sector – May 2019

The supplemental guidance document is to be read in conjunction with the DNFBP guidelines. This guidance documents the various real estate-related activities which are vulnerable to financial crime. Various examples of the exploitation of the real estate sector for money laundering and terrorism financing are provided, along with the sectoral ML/FT red flags.

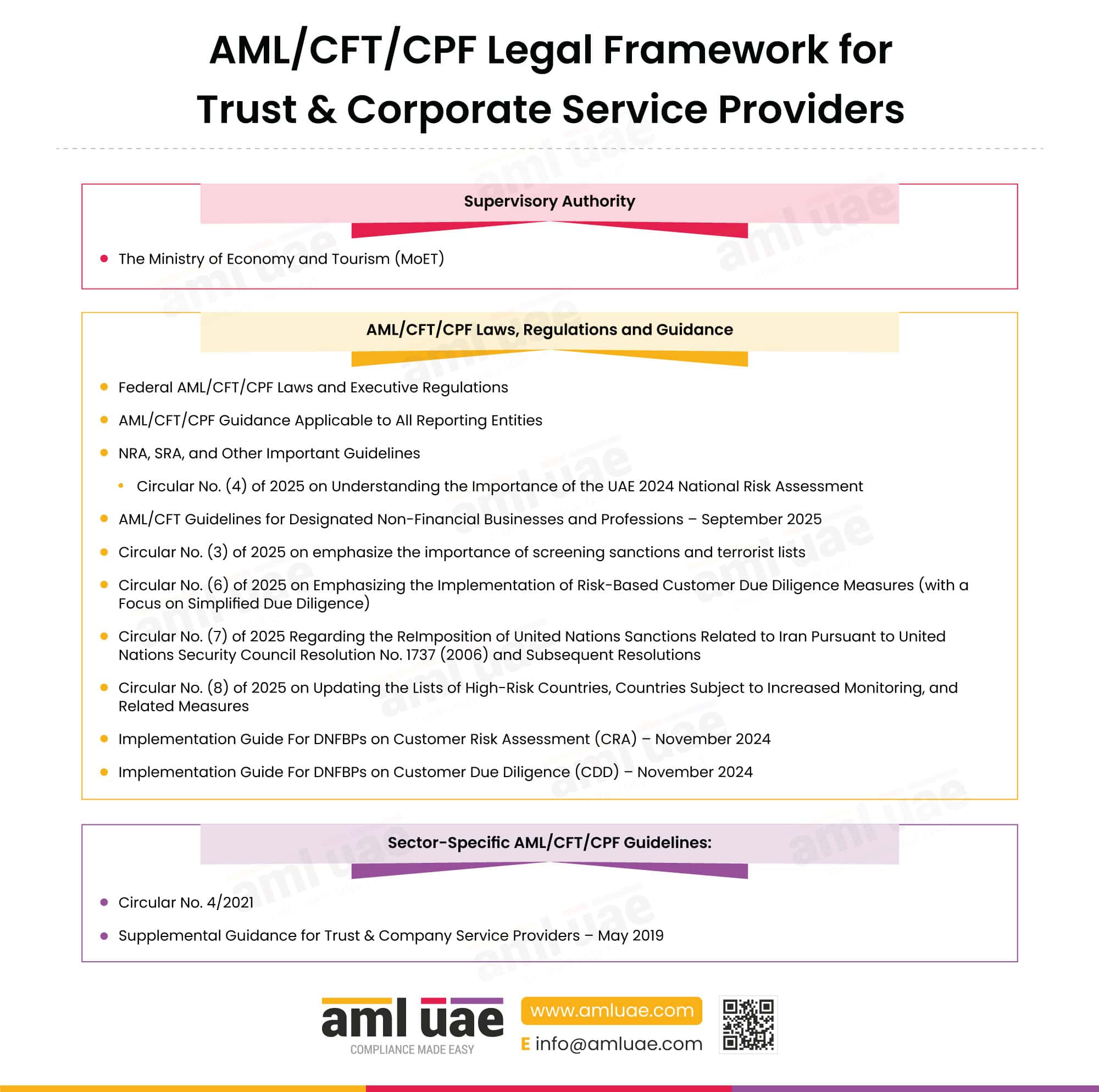

AML/CFT/CPF Legal Framework for Trust & Corporate Service Providers (TCSPs)

Supervisory Authority for Trust & Corporate Service Providers:

The Ministry of Economy and Tourism is the AML supervisory authority for trust and corporate service providers licensed in the UAE Mainland and the commercial free zones.

AML/CFT/CPF Laws, Regulations and Guidance Applicable to TCSPs:

- Federal AML/CFT/CPF Laws and Executive Regulations

- AML/CFT/CPF Guidance Applicable to All Reporting Entities

- NRA, SRA, and Other Important GuidelinesIn the context of the NRA, TCSPs are required to adhere to Circular No. (4) of 2025 on Understanding the Importance of the UAE 2024 National Risk Assessment to meet the expectations set out within applicable to their sector.

- AML/CFT Guidelines for Designated Non-Financial Businesses and Professions – September 2025

- Circular No. (3) of 2025 on emphasize the importance of screening sanctions and terrorist lists

- Circular No. (6) of 2025 on Emphasizing the Implementation of Risk-Based Customer Due Diligence Measures (with a Focus on Simplified Due Diligence) This circular provides reference to the Implementation Guide for DNFBPs on CDD and CRA (November 2024)

- Circular No. (7) of 2025 Regarding the ReImposition of United Nations Sanctions Related to Iran Pursuant to United Nations Security Council Resolution No. 1737 (2006) and Subsequent Resolutions

- Circular No. (8) of 2025 on Updating the Lists of High-Risk Countries, Countries Subject to Increased Monitoring, and Related Measures

- Implementation Guide For DNFBPs on Customer Risk Assessment (CRA) – November 2024

- Implementation Guide For DNFBPs on Customer Due Diligence (CDD) – November 2024.

TCSP Sector-Specific AML/CFT/CPF Guidelines

TCSPs are mandated to adhere to the guidance documents, in addition to the federal AML regulations mentioned above.

- Circular No. 4/2021 Calls for the implementation of AML/CFT obligations by TCSPs and explains the supervisory authority’s procedures for onsite and offsite inspection for the compliance of the same.

- Supplemental Guidance for Trust & Company Service Providers – May 2019

The supplemental guidance must be read in parallel with the DNFBP guidelines referenced above. This guidance lists various activities performed by the TCSP that shall be subject to AML measures, and others that are low risk and do not require risk mitigation measures. It also captures the sectoral red flag indicators that the TCSP must be mindful of.

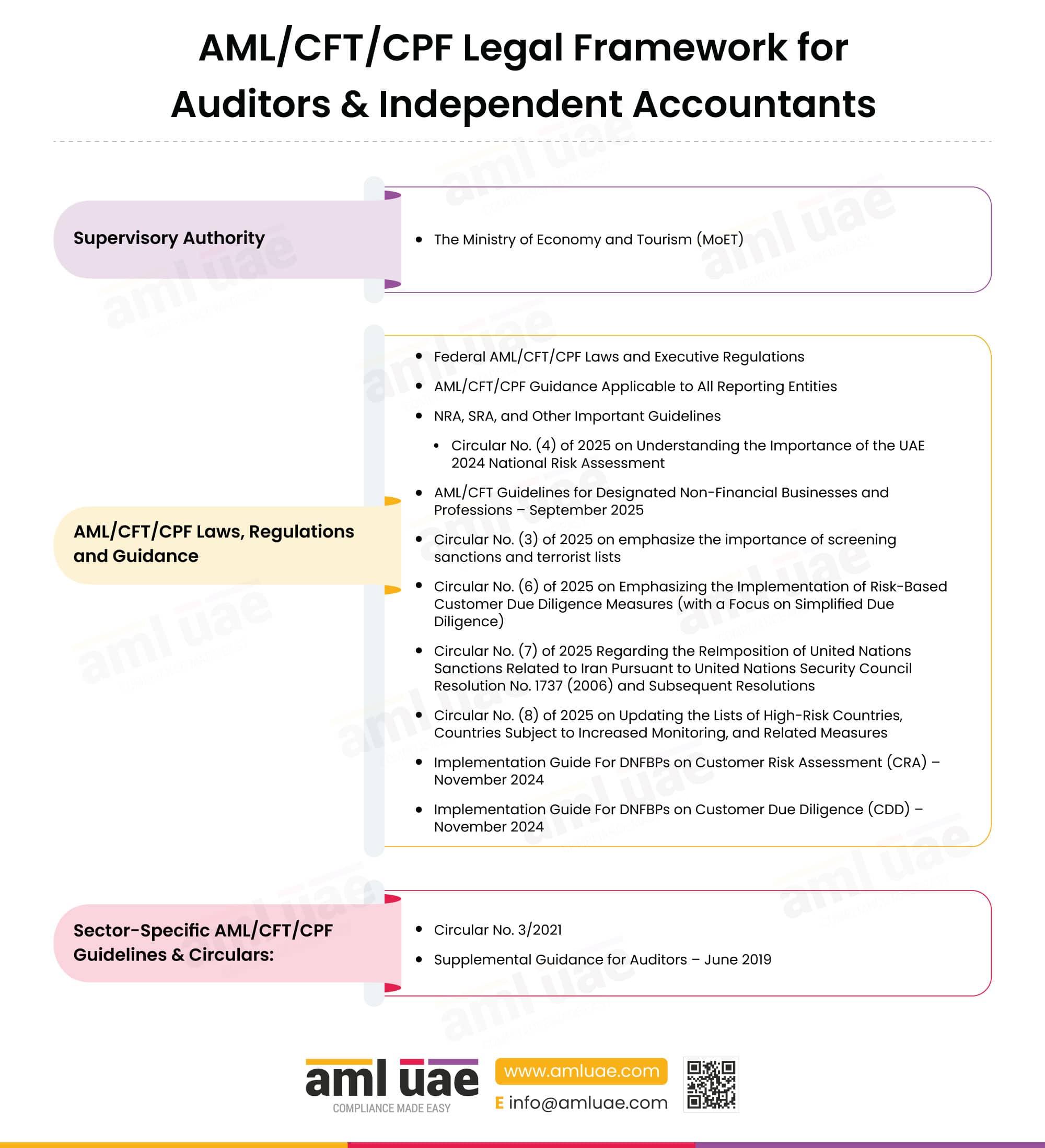

AML/CFT/CPF Legal Framework for Auditors & Independent Accountants

Supervisory Authority for Auditors and Independent Accountants:

The independent auditors and accountants (licensed in the UAE, except those licensed by the FSRA and DFSA) are subject to AML supervision by the Ministry of Economy and Tourism.

AML/CFT/CPF Laws, Regulations, and Guidance Applicable to Auditors and Independent Accountants:

- Federal AML/CFT/CPF Laws and Executive Regulations

- AML/CFT/CPF Guidance Applicable to All Reporting Entities

- NRA, SRA, and Other Important Guidelines In the context of the NRA, Auditors and Accountants are required to adhere to Circular No. (4) of 2025 on Understanding the Importance of the UAE 2024 National Risk Assessment to meet the expectations set out within applicable to their sector.

- AML/CFT Guidelines for Designated Non-Financial Businesses and Professions – September 2025

- Circular No. (3) of 2025 on emphasize the importance of screening sanctions and terrorist lists

- Circular No. (6) of 2025 on Emphasizing the Implementation of Risk-Based Customer Due Diligence Measures (with a Focus on Simplified Due Diligence) This circular provides reference to the Implementation Guide for DNFBPs on CDD and CRA (November 2024)

- Circular No. (7) of 2025 Regarding the ReImposition of United Nations Sanctions Related to Iran Pursuant to United Nations Security Council Resolution No. 1737 (2006) and Subsequent Resolutions

- Circular No. (8) of 2025 on Updating the Lists of High-Risk Countries, Countries Subject to Increased Monitoring, and Related Measures

- Implementation Guide For DNFBPs on Customer Risk Assessment (CRA) – November 2024

- Implementation Guide For DNFBPs on Customer Due Diligence (CDD) – November 2024.

Auditors & Independent Accountants Sector-Specific AML/CFT/CPF Guidelines & Circulars

Independent accountants and auditors are required to develop the AML program in accordance with the guidance documents listed below, as well as the federal decree law, the cabinet decision, and general AML publications at the federal level.

- Circular No. 3/2021 Calls for the implementation of AML/CFT obligations by Accountants and Auditors and explains the supervisory authority’s procedures for onsite and offsite inspection for the compliance of the same.

- Supplemental Guidance for Auditors – June 2019

The supplemental guidance for auditors is to be considered as a follow-up document to the above-mentioned DNFBP guidelines. This guidance lists various risks that the independent auditors may encounter while discharging their professional duties. The guidance also documents examples of abuse of auditor services, certain known typologies, and sectoral red flag indicators that the auditor should be mindful of.

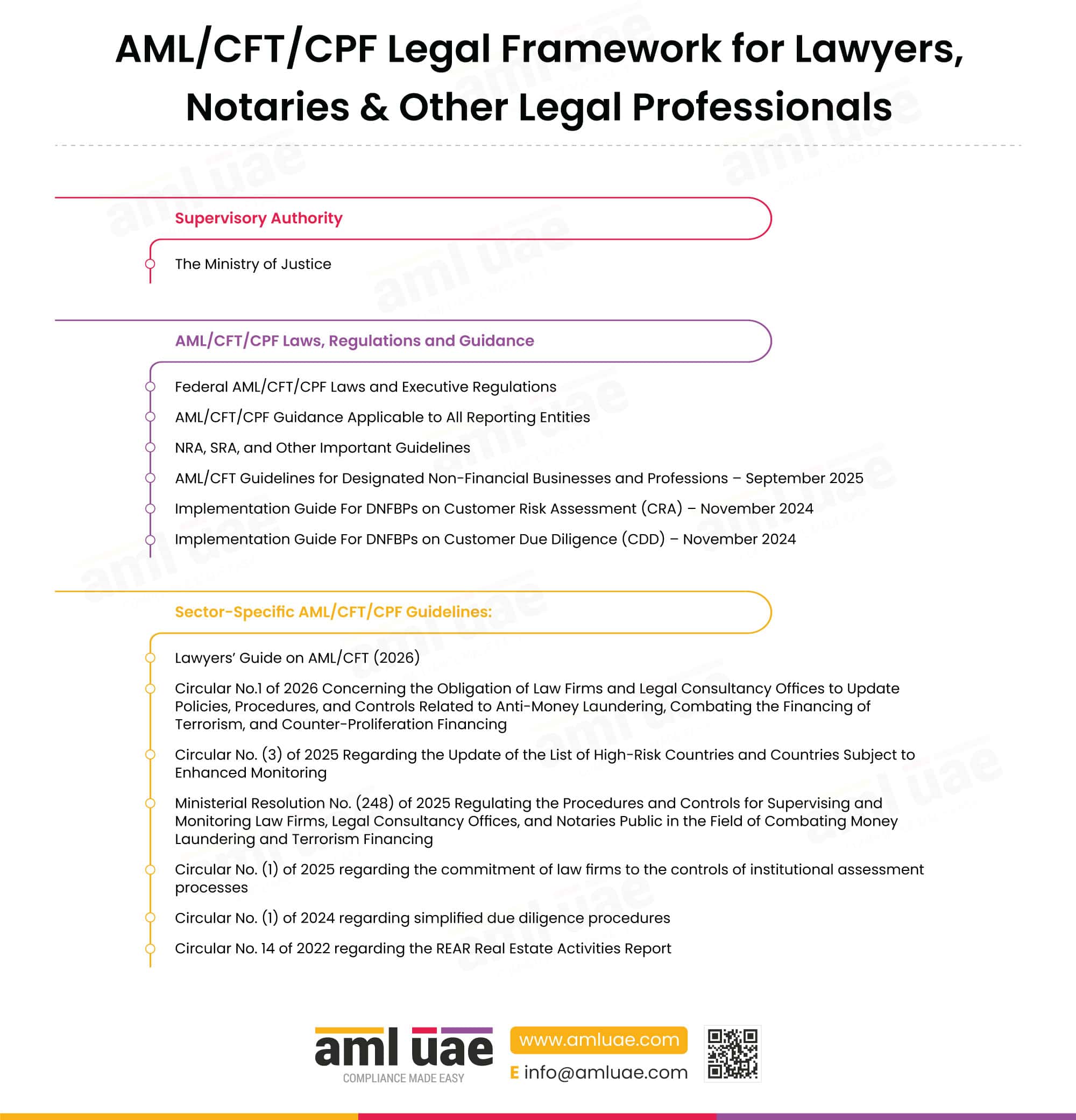

AML/CFT/CPF Legal Framework for Lawyers, Notaries & Other Legal Professionals

Supervisory Authority for Lawyers, Notaries, and Other Legal Professionals:

The Ministry of Justice (MoJ) is the AML supervisory authority for lawyers, notaries and independent legal professionals operating in the UAE (except the financial free zones).

AML/CFT/CPF Laws, Regulations and Guidance Applicable to Lawyers, Notaries, and Other Legal Professionals

- Federal AML/CFT/CPF Laws and Executive Regulations

- AML/CFT/CPF Guidance Applicable to All Reporting Entities

- NRA, SRA, and Other Important Guidelines

- AML/CFT Guidelines for Designated Non-Financial Businesses and Professions – September 2025

- Implementation Guide For DNFBPs on Customer Risk Assessment (CRA) – November 2024

- Implementation Guide For DNFBPs on Customer Due Diligence (CDD) – November 2024

Legal Sector-Specific AML/CFT/CPF Guidelines

Legal professionals, lawyers, and law firms are required to implement an AML program in accordance with regulatory documents issued by the MoJ, as well as the federal AML regulations mentioned above.

- Lawyers’ Guide on AML/CFT (2026) The guide illustrates the best practices that lawyers and legal professionals should adopt to comply with AML obligations regarding the identification, assessment, and mitigation of ML/FT risks they may face. It places emphasis on firm-level accountability, firm-wide risk assessment processes aligned with FATF standards, integration of CPF controls alongside AML/CFT controls, reliance on data analytics and client behaviour patterns beyond traditional ID checks.

- Circular No.1 of 2026 Concerning the Obligation of Law Firms and Legal Consultancy Offices to Update Policies, Procedures, and Controls Related to Anti-Money Laundering, Combating the Financing of Terrorism, and Counter-Proliferation Financing (Available only in Arabic) Requires law firms and legal consultancies to update their AML/CTF and CPF Policies, Procedures, and Controls whenever relevant risk factors change or regulatory requirements arise. It mandates that changes to the AML Framework must be triggered by changes in the National Risk Assessments, internal risk levels, client base, services offered, or legal obligations to ensure that AML Compliance Program stays current and effective to mitigate evolving ML/TF and PF risks.

- Circular No. (3) of 2025 Regarding the Update of the List of High-Risk Countries and Countries Subject to Enhanced Monitoring (Available only in Arabic) Calls for legal professionals to review the updated FATF Grey Lists and Blacklists and update their firm’s AML/CFT Policies and Procedures accordingly, and implement the necessary diligence measures when dealing with clients belonging to those countries.

- Ministerial Resolution No. (248) of 2025 Regulating the Procedures and Controls for Supervising and Monitoring Law Firms, Legal Consultancy Offices, and Notaries Public in the Field of Combating Money Laundering and Terrorism Financing (Available only in Arabic)

Repealing the Ministerial Decision No. (533) of 2019 On AML/CFT related to Lawyers, Notaries and Legal Independent ProfessionalsThis MoJ Decision aligns with Cabinet Resolution 71 of 2024 containing the penalty framework while embedding risk-based inspection planning formally and strengthens escalation triggers. It further confirms applicability to Financial Free Zones and Non-Financial Free Zones.

It provides for temporary practice ban, suspension of partners and directors, and license revocation other than fines and penalties for violation of AML/CFT obligations. It also requires Legal Professionals engaged in covered activities to have a written methodology for Client Risk Assessment, documented EDD triggers, PEP Screening protocols, and Sanctions Screening logs and database and further obligates them to perform transaction level risk assessment, obtain source of funds documentation, maintain ongoing monitoring records and ensure beneficial ownership verification.

The major obligation it imposes on lawyers and legal professionals engaged in covered activities under AML purview is to ensure inspection readiness by appointing a designated inspection response officer, maintaining a corrective action tracking register and a readily available document repository that assists with partner oversight of AML reports, periodic AML internal audit and maintaining a robust internal breach reporting mechanism. In simple words the resolution aims to lay down the AML obligations of lawyers and legal professionals in line with the federal AML regulations and guide them on the procedures to be adopted to ensure compliance.

- Circular No. (1) of 2025 regarding the commitment of law firms to the controls of institutional assessment processes (Available only in Arabic) Requires legal professionals and lawyers to conduct and document institutional risk assessments specifically addressing proliferation financing risks and requires them to update their internal AML/CFT controls to align with FATF recommendations and UAE non-proliferation laws, particularly Federal Decree-Law No. 43 of 2021 on the Goods Subject to Non-Proliferation. It further mandates the Compliance Officers to follow guidance issued by the MoJ and the EOCN to prevent involvement of legal professionals and practitioners in transactions linked to weapons proliferation

- Circular No. (1) of 2024 regarding simplified due diligence procedures. (Available only in Arabic)

The circular elaborates on the simplified due diligence measures that the law firms and legal professionals may apply to the customers identified as posing low ML/FT risks.

- Circular No. 14 of 2022 regarding the REAR Real Estate Activities Report (Available only in Arabic). The circular imposes additional obligations on lawyers to report real estate transactions they facilitate in which the property value is settled in cash or virtual assets, above a specified threshold.

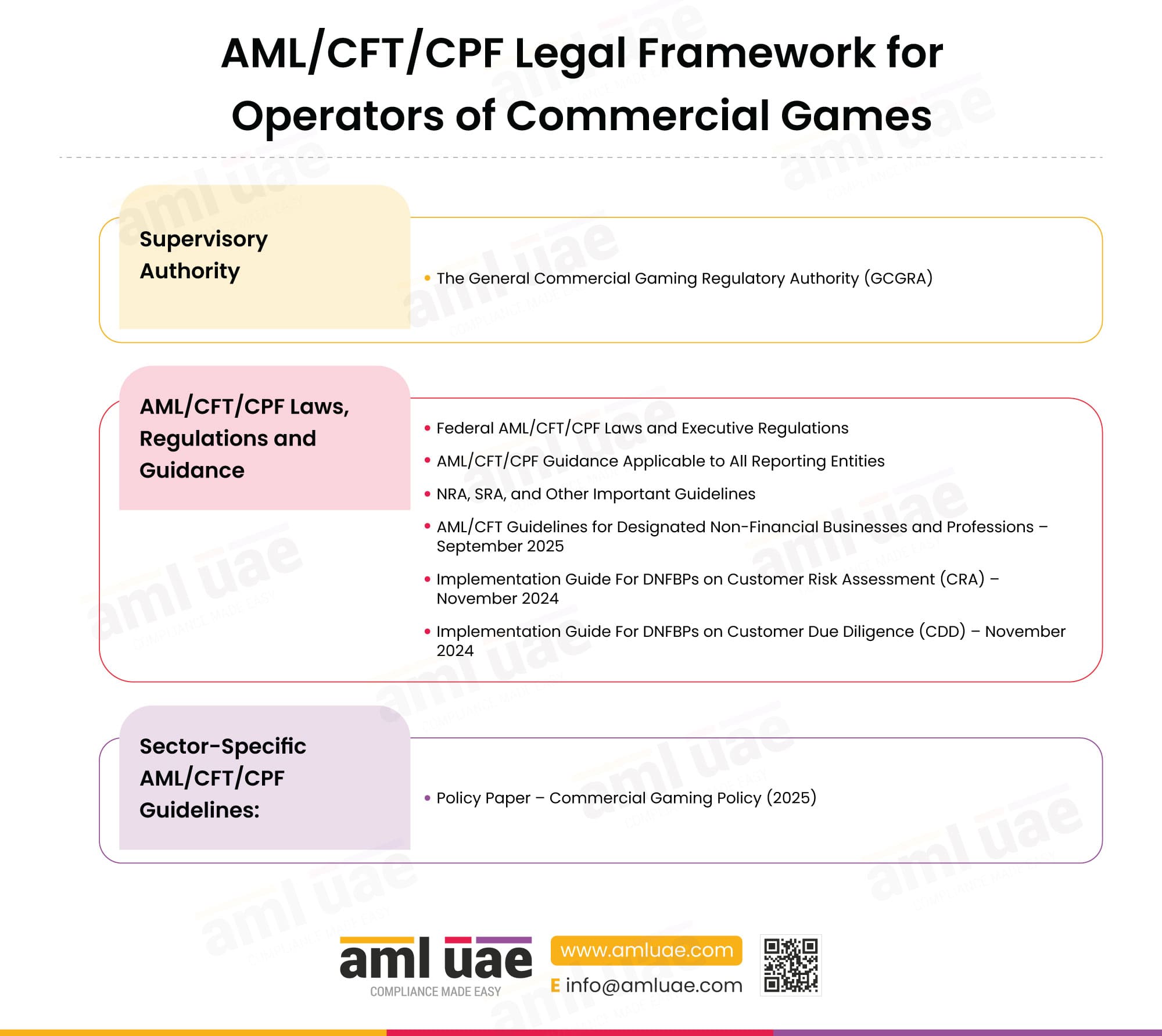

AML/CFT/CPF Legal Framework for Operators of Commercial Games (New Sector)

Supervisory Authority for Operators of Commercial Games:

The General Commercial Gaming Regulatory Authority (GCGRA) is the AML supervisory authority for the newly brought commercial gaming operators under the AML regime.

AML/CFT/CPF Laws, Regulations and Guidance Applicable to Operators of Commercial Games:

- Federal AML/CFT/CPF Laws and Executive Regulations

- AML/CFT/CPF Guidance Applicable to All Reporting Entities

- NRA, SRA, and Other Important Guidelines

- AML/CFT Guidelines for Designated Non-Financial Businesses and Professions – September 2025

- Implementation Guide For DNFBPs on Customer Risk Assessment (CRA) – November 2024

- Implementation Guide For DNFBPs on Customer Due Diligence (CDD) – November 2024

Sector-Specific AML/CFT/CPF Guidelines for Commercial Game Operators:

For now, the gaming operators are required to comply with the above-referred federal decree laws and implementing regulations, as well as cabinet decisions, while the sector-specific AML/CFT guidelines are yet to be issued by the GCGRA.

Additionally, it is recommended to consider the following:

- Policy Paper – Commercial Gaming Policy (2025)

This policy paper has been issued jointly by the NAMLCFTC and GCGRA. The policy paper documents the key ML/FT and PF risks associated with the gaming industry and provides the targeted recommended strategies that can be adopted to mitigate the risks.

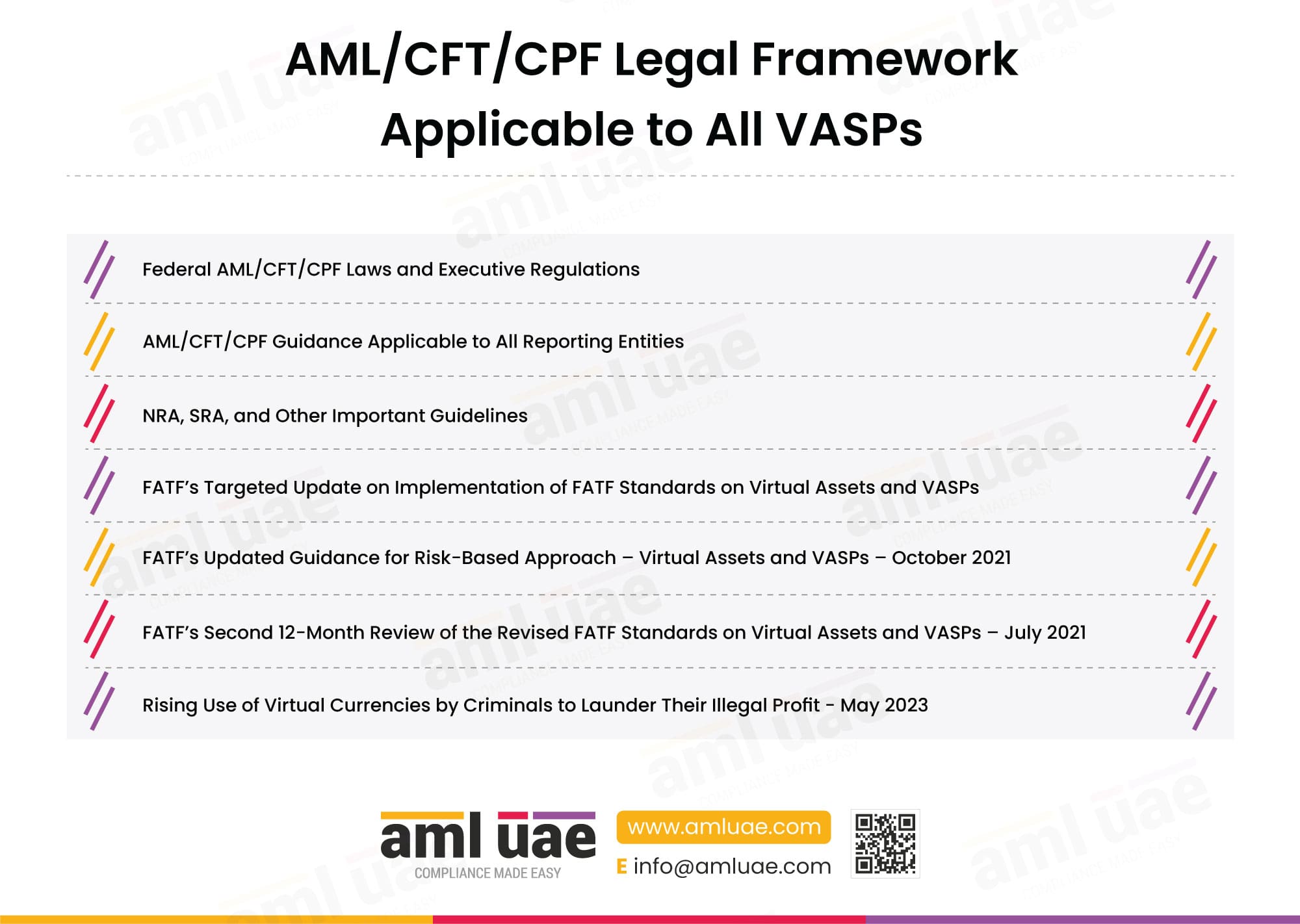

AML/CFT/CPF Legal Framework for Virtual Asset Service Providers (VASPs)

All Virtual Asset Service Providers have to adhere to:

- Federal AML/CFT/CPF Laws and Executive Regulations

- AML/CFT/CPF Guidance Applicable to All Reporting Entities

- NRA, SRA, and Other Important Guidelines

VASPs are subject to different authorities depending on the jurisdiction in which they operate. Accordingly, VASPs are expected to comply with the AML guidelines and rulebooks issued by the relevant AML supervisory authority.

In addition to this, the VASPs are required to refer to the following FATF publications when developing their ML/FT risk mitigation framework (mandated by the supervisory authorities):

- FATF’s Targeted Update on Implementation of FATF Standards on Virtual Assets and VASPs

The report highlights the FATF’s observations and feedback on the implementation of the FATF standards in the virtual asset sector across various countries. It also discusses the evolving risks and the exploitation of virtual assets for proliferation and terrorism financing. The last section of the report documents the FATF’s recommendations to VASPs and regulatory authorities.

- FATF’s Updated Guidance for Risk-Based Approach – Virtual Assets and VASPs – October 2021

This guidance by FATF focuses on helping VASPs understand the key ML/FT risks associated with the sector and describes the key obligations of VASPs to mitigate these risks (in line with the FATF recommendations).

- FATF’s Second 12-Month Review of the Revised FATF Standards on Virtual Assets and VASPs – July 2021

The FATF report describes the evolution of the global virtual asset market, including the ML/FT risks associated with the sector. It also documents the main concerns regarding the VASP’s implementation of the global AML/CFT best practices, as identified by the FATF.

The VASPs are also expected to refer to this report issued by Public Private Partnership Sub Committee and NAMLCFTC – Rising Use of Virtual Currencies by Criminals to Launder Their Illegal Profit.” The report documents how virtual currencies are misused for laundering and terrorism financing, lists certain red flag indicators, and includes key recommendations for regulated entities.

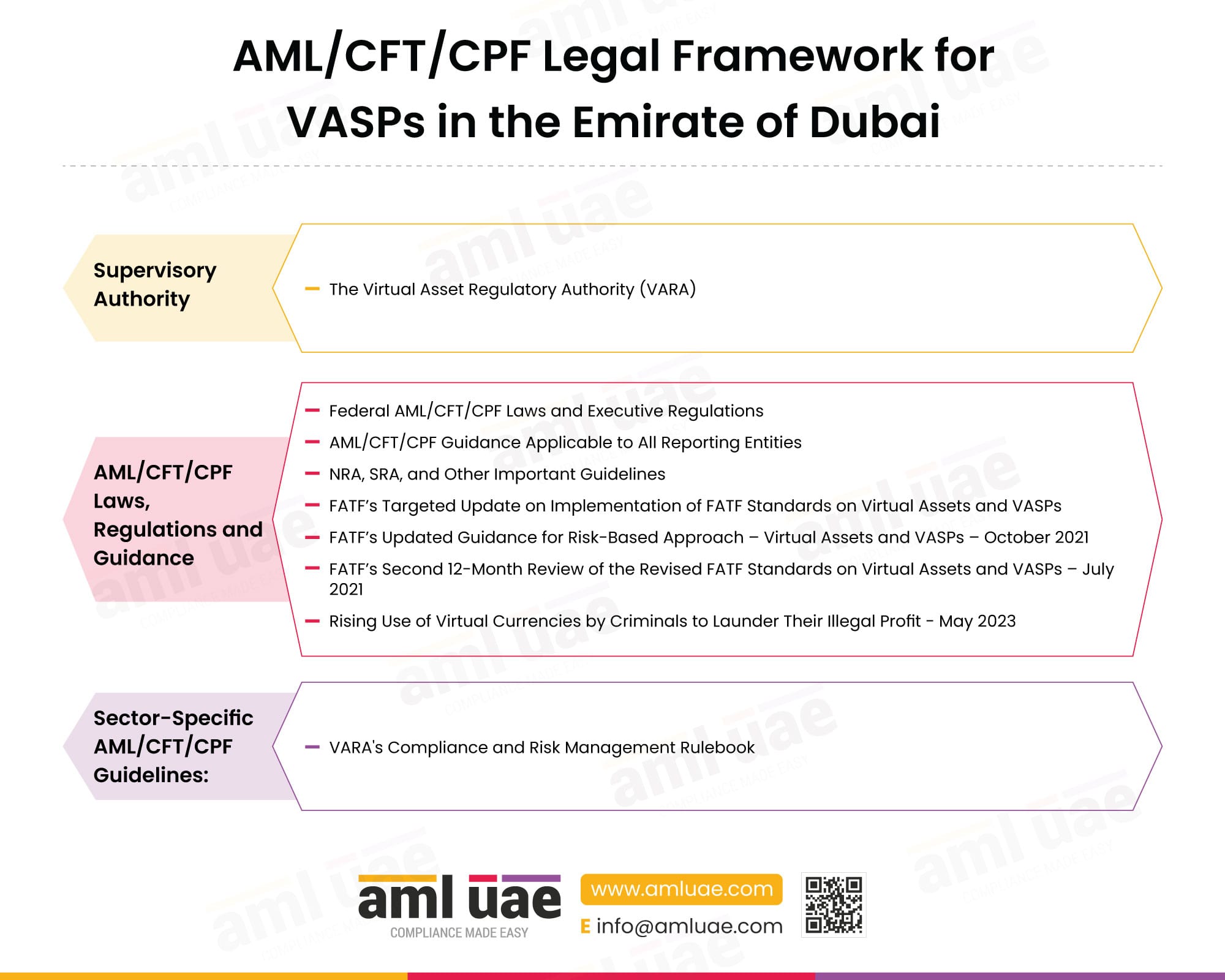

AML/CFT/CPF Legal Framework for VASPs in the Emirate of Dubai

Supervisory Authority for Virtual Asset Service Providers in the Emirate of Dubai

The Virtual Asset Regulatory Authority (VARA) is the AML supervisory authority for the VASPs licensed and operating in or from Dubai.

AML/CFT/CPF Laws, Regulations and Guidance Applicable to VASPs in the Emirate of Dubai:

- Federal AML/CFT/CPF Laws and Executive Regulations

- AML/CFT/CPF Guidance Applicable to All Reporting Entities

- NRA, SRA, and Other Important Guidelines

- FATF’s Targeted Update on Implementation of FATF Standards on Virtual Assets and VASPs

- FATF’s Updated Guidance for Risk-Based Approach – Virtual Assets and VASPs – October 2021

- FATF’s Second 12-Month Review of the Revised FATF Standards on Virtual Assets and VASPs – July 2021

- Rising Use of Virtual Currencies by Criminals to Launder Their Illegal Profit – May 2023

Sector-Specific AML/CFT/CPF Guidelines for VASPs in the Emirate of Dubai

Along with the above-referred federal decree laws and implementing regulations, and cabinet decisions, the VASPs subject to VARA supervision are required to comply with the following:

- VARA’s Compliance and Risk Management Rulebook

Part III of the rulebook provides detailed guidance to the VARA-licensed VASPs on the AML/CFT obligations, including the mandate to adequately assess the business risks arising from virtual asset operations. The rulebook requires VASPs to develop an AML program, led by a fit-and-proper person (Compliance Officer), that assists VASPs with customer onboarding, transaction monitoring, record maintenance, etc.

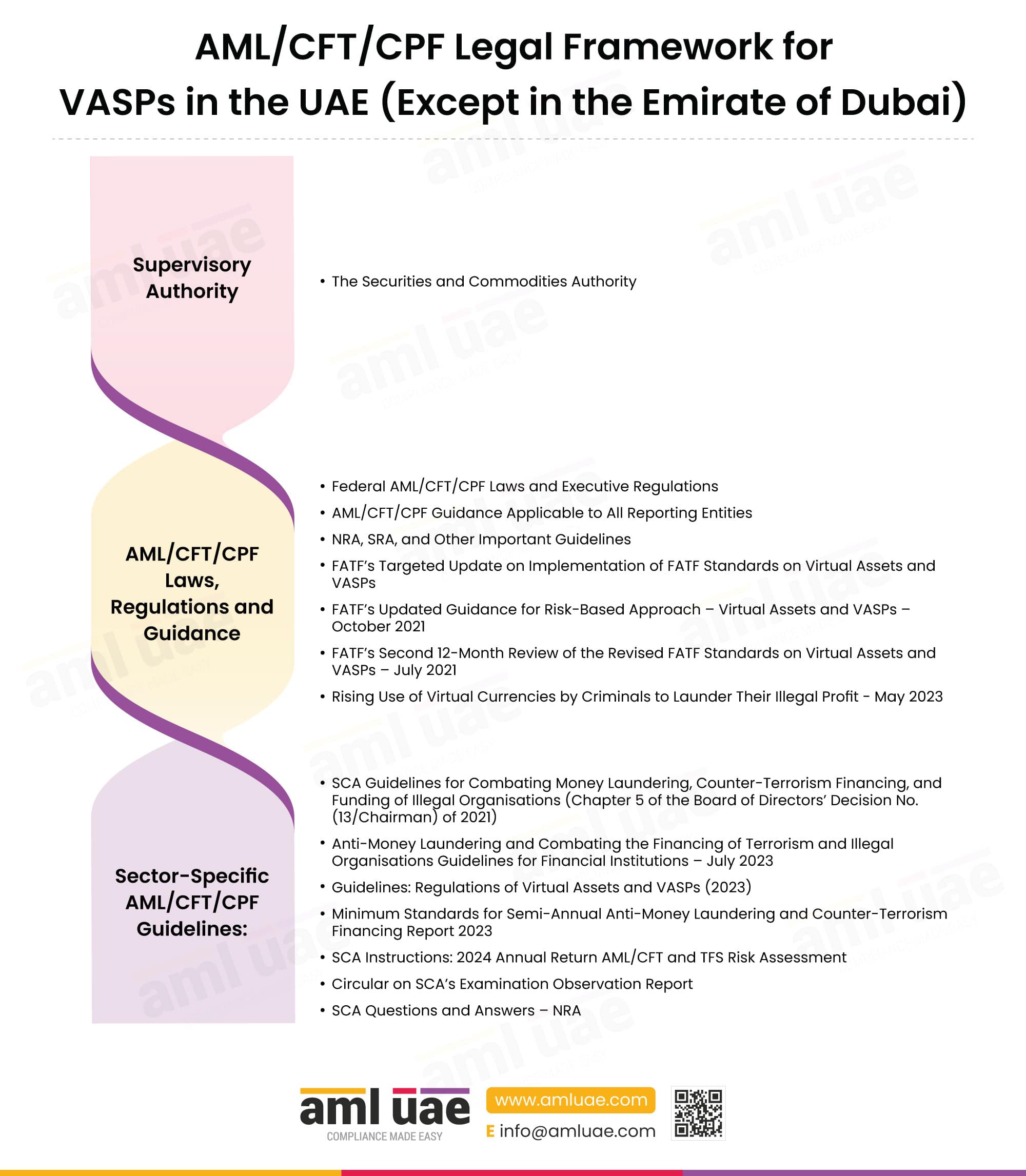

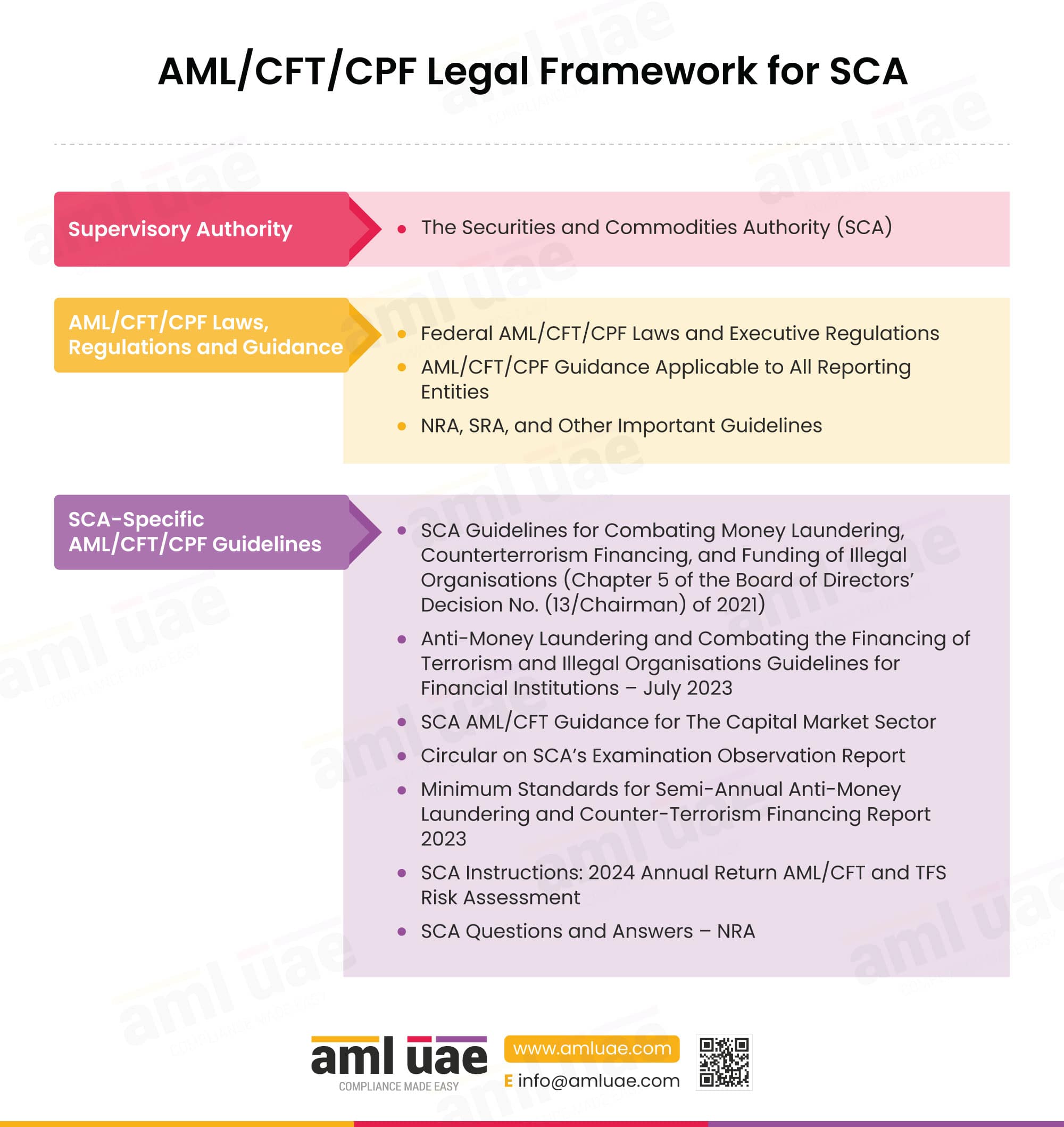

AML/CFT Legal Framework for VASPs in the UAE (Except in the Emirate of Dubai)

Supervisory Authority for Virtual Asset Service Providers in the UAE (Except in the Emirate of Dubai)

The VASPs, operating in or from anywhere in the UAE, except Dubai and the financial free zones, are subject to AML supervision by the Capital Market Authority of the UAE.

AML/CFT/CPF Laws, Regulations and Guidance Applicable to VASPs in the UAE (Except in the Emirate of Dubai) :

- Federal AML/CFT/CPF Laws and Executive Regulations

- AML/CFT/CPF Guidance Applicable to All Reporting Entities

- NRA, SRA, and Other Important Guidelines

- FATF’s Targeted Update on Implementation of FATF Standards on Virtual Assets and VASPs

- FATF’s Updated Guidance for Risk-Based Approach – Virtual Assets and VASPs – October 2021

- FATF’s Second 12-Month Review of the Revised FATF Standards on Virtual Assets and VASPs – July 2021

- Rising Use of Virtual Currencies by Criminals to Launder Their Illegal Profit

Sector-Specific AML/CFT/CPF Guidelines for VASPs in UAE (Except in the Emirate of Dubai)

- CMA Guidelines for Combating Money Laundering, Counter-Terrorism Financing, and Funding of Illegal Organisations (Chapter 5 of the Board of Directors’ Decision No. (13/Chairman) of 2021)

Chapter 5 of this CMA Board Decision provides detailed procedures and measures that the CMA-regulated VASPs are expected to establish to identify and manage the financial crime risks.

- Anti-Money Laundering and Combating the Financing of Terrorism and Illegal Organisations Guidelines for Financial Institutions – July 2023

As per the Observations Appendix issued by the CMA, the CMA–licensed VASPs are required to adhere to the CBUAE’s AML/CFT guidelines for the financial institutions, which provide guidance on effective implementation of the provisions of the federal AML regulations and ensure compliance with the statutory obligations.

- Guidelines: Regulations of Virtual Assets and VASPs (2023)

This CMA issued guidelines mandate that VASPs develop and implement a robust AML/CFT and sanctions compliance program, including the appointment of a Compliance Officer, documenting a comprehensive AML/CFT policy and procedures, assessing business and customer risks, applying adequate CDD measures, etc.

- Circular on CMA’s Examination Observation Report

The report highlights shortcomings across the sector related to ML/FT and defines expectations for regulated entities to take robust measures to ensure that the developed AML/CFT and sanctions compliance program is aligned with the business risk.

- Minimum Standards for Semi-Annual Anti-Money Laundering and Counter-Terrorism Financing Report 2023

The document establishes the minimum standard that helps the compliance officer develop a detailed and effective report, which serves as an effective tool for communicating with management and the CMA.

- CMA Instructions: 2024 Annual Return AML/CFT and TFS Risk Assessment

The instruction defines the terms used in the Annual Risk Assessment Return and provides the directives to assist the regulated entities in completing the AML/CFT and TFS Risk Assessment Information Return.

- CMA Questions and Answers – NRA

The CMA issued the FAQs in line with the latest NRA, setting out the CMA’s expectations of regulated entities to update their EWRA and align it with the outcome of the latest ML/FT NRA

AML/CFT Legal Framework for Financial Free Zones

The financial free zones in the UAE, i.e. DIFC and ADGM, operate under their own legal and regulatory frameworks that are aligned with federal AML/CFT requirements. These jurisdictions have enacted specific laws and rulebooks to govern business activities within their territories while ensuring consistency with the national AML/CFT strategy.

AML/CFT/CPF Laws, Regulations, and Guidance Applicable to Financial Free Zones

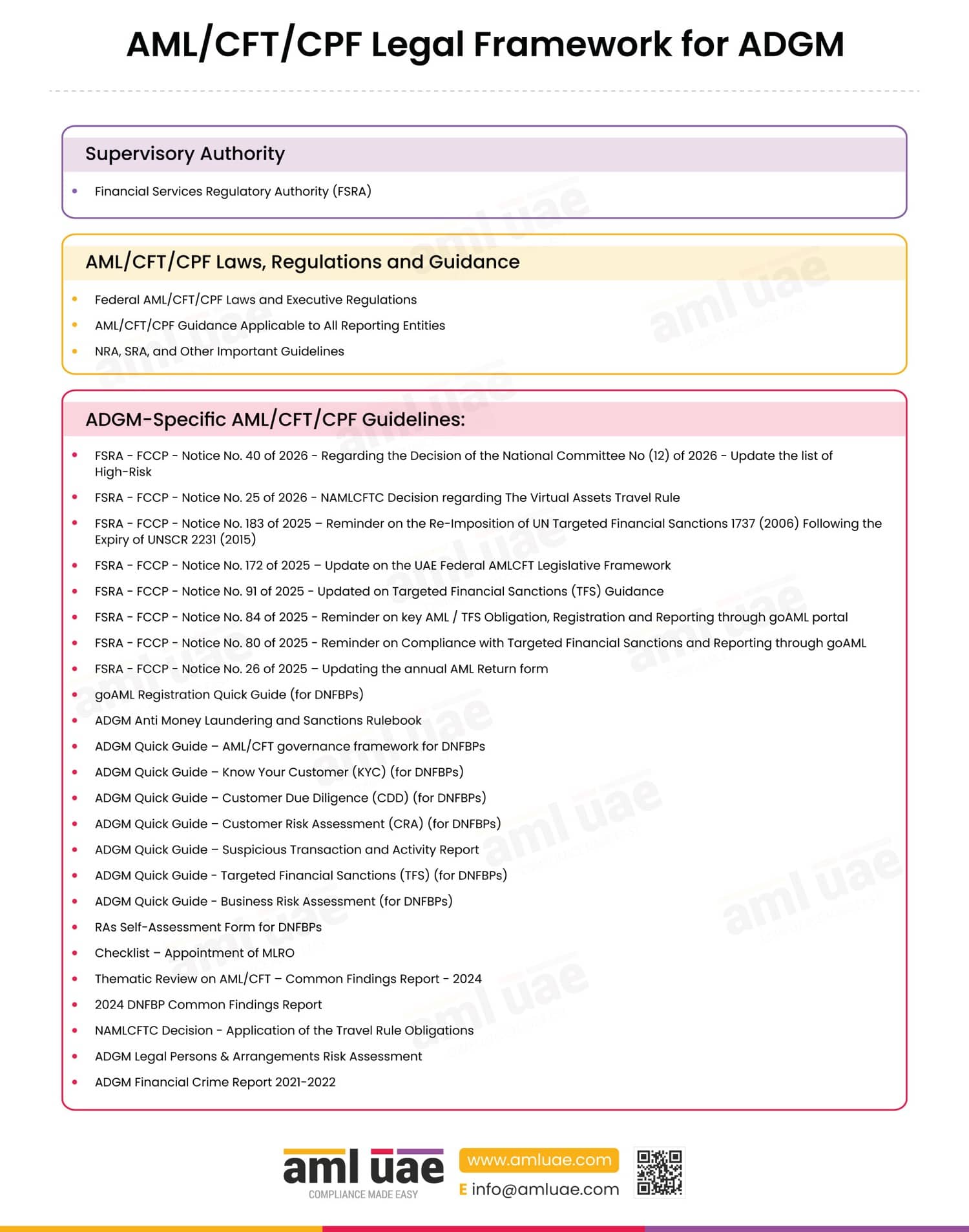

AML/CFT/CPF Legal Framework for Abu Dhabi Global Market (ADGM)

Supervisory Authority for Abu Dhabi Global Market:

All the entities operating in or from ADGM are subject to oversight and supervision of the Financial Services Regulatory Authority (FSRA).

AML/CFT/CPF Laws, Regulations and Guidance Applicable to ADGM

- Federal AML/CFT/CPF Laws and Executive Regulations

- AML/CFT/CPF Guidance Applicable to All Reporting Entities

- NRA, SRA, and Other Important Guidelines

ADGM AML/CFT/CPF Legal Framework and Key Deviations from the Federal AML/CFT/CPF Law:

Compared to the federal AML regulations, the scope of DNFBP is wide, covering a larger number of entities within the AML ambit, where the possibility of abusing the sector for ML/FT is high. In ADGM, DNFBP includes the following:

- a real estate agency which carries out transactions with other persons that involve the acquiring or disposing of real property,

- a dealer in precious metals or precious stones,

- a dealer in any saleable item of a price equal to or greater than USD 15,000,

- an accounting firm, audit firm, insolvency firm or taxation consulting firm,

- law firm, notary firm or other independent legal business, and

- Company Service Provider.

ADGM-Specific AML/CFT/CPF Laws, Regulations and Guidance

The FSRA-regulated entities are required to adhere to the following additional regulatory rulebook and guidance documents, along with federal decree laws and implementing regulations, as well as cabinet decisions.

- FSRA – FCCP – Notice No. 40 of 2026 – Regarding the Decision of the National Committee No (12) of 2026 – Update the list of High-Risk The notice is published to ensure alignment with the latest changes to the FATF Grey List and Blacklist, requiring FIs, DNFBPs, VASPs, and NPOs in the UAE to take appropriate due diligence measures as elaborated in the notice.

- FSRA – FCCP – Notice No. 25 of 2026 – NAMLCFTC Decision regarding The Virtual Assets Travel Rule Conveys the NAMLCFTC decision regarding the UAE’s Virtual Assets Travel Rule and states that in the event of conflict between the AML Rulebook and the Virtual Assets Travel Rule, FIs, DNFBPs and VASPs are required to uphold the measures and obligations set forth in the AML Rulebook.

- FSRA – FCCP – Notice No. 183 of 2025 – Reminder on the Re-Imposition of UN Targeted Financial Sanctions 1737 (2006) Following the Expiry of UNSCR 2231 (2015) This notice reminds regulated entities operating in ADGM regarding the expiry and reimposition of relevant UNSCRs to ensure alignment with Cabinet Resolution No. (74) of 2020, AML Rulebook, and FATF Recommendation No. 7.

- FSRA – FCCP – Notice No. 172 of 2025 – Update on the UAE Federal AMLCFT Legislative Framework Informs regulated entities regarding updates on UAE Federal AML/CFT laws by the introduction of Federal Decree by Law No. (10) of 2025 and the UAE Cabinet Resolution No. (134) of 2025, repealing previous legislation. It calls for FIs, DNFBPs, and VASPs in ADGM to:

- Review the new laws in detail

- Analyse the impact of the new law on their AML/CFT and TFS compliance framework

- Update their AML/CFT and TFS policies, procedures, manuals, and tools to ensure complete alignment with the new laws.

- FSRA – FCCP – Notice No. 91 of 2025 – Updated on Targeted Financial Sanctions (TFS) Guidance Requires all relevant persons to refer to updated TFS guidance to ensure compliance with screening and ongoing enforcement procedures.

- FSRA – FCCP – Notice No. 84 of 2025 – Reminder on key AML / TFS Obligation, Registration and Reporting through goAML portal Reminds relevant persons to ensure compliance with their obligations as stated in the AML Rulebook.

- FSRA – FCCP – Notice No. 80 of 2025 – Reminder on Compliance with Targeted Financial Sanctions and Reporting through goAML Reminds relevant persons to ensure TFS compliance in alignment with the latest TFS Guidance.

- FSRA – FCCP – Notice No. 26 of 2025 – Updating the annual AML Return form Provides general guidance to be followed while completing the AML Return form at the end of April each year through the FSRA Connect Portal.

- goAML Registration Quick Guide (for DNFBPs) This quick guide is aimed at assisting DNFBPs with registering on the goAML system to enable filing mandatory reports with UAEFIU and ensure compliance with ADGM AML requirements.

- ADGM Anti Money Laundering and Sanctions Rulebook The rulebook sets out the detailed procedures and controls that FSRA-regulated entities must develop and implement to identify and mitigate ML, FT, and PF risks.

- ADGM Quick Guide – AML/CFT governance framework for DNFBPs This short guide from FSRA outlines the key components of an effective AML/CFT governance framework that regulated entities are expected to adopt.

- ADGM Quick Guide – Know Your Customer (KYC) (for DNFBPs) The quick guide on KYC helps regulated DNFBPs understand the key elements of the KYC process for onboarding individual and corporate customers. It also includes certain examples of the KYC measures to be followed under different scenarios.

- ADGM Quick Guide – Customer Due Diligence (CDD) (for DNFBPs) The guide helps DNFBPs understand the types of CDD that may be adopted and their core elements.

- ADGM Quick Guide – Customer Risk Assessment (CRA) (for DNFBPs) This quick guide discusses the customer risk assessment process and provides an illustrative list of risk factors that DNFBPs can consider (depending on their business activities) when evaluating customers’ risk.

- ADGM Quick Guide – Suspicious Transaction and Activity Report The key requirements for reporting suspicion, the differences between SAR and STR filings, and the best reporting practices are captured in this guide.

- ADGM Quick Guide – Targeted Financial Sanctions (TFS) (for DNFBPs) This guide elaborates on the TFS process and helps the ADGM-based entities understand the TFS obligations, as imposed under Cabinet Decision No. (74) of 2020.

- ADGM Quick Guide – Business Risk Assessment (for DNFBPs) This guide discusses the business risk assessment factors and process so that DNFBPs can identify inherent risks and implement control measures effectively.

- RAs Self-Assessment Form for DNFBPs Regulator’s Self-Assessment Form is provided to serve as supplementary information to the ADGM Registration Authority (ADGM RA) as evidence to showcase that DNFBPs have implemented AML/CFT Policies and Procedures in alignment with ADGM AML Rules.

- Checklist – Appointment of MLRO ADGM RA has published MLRO appointment checklist to enable regulated entities to ensure that they appoint a suitable MLRO by verifying the qualifications, experience, eligibility and independence of the candidate. It also helps ensure that all required documents and information are collected and submitted to the FSRA for approval of the MLRO appointment. Lastly, the checklist helps regulated entities demonstrate that they have conducted adequate due diligence and governance checks prior to the appointment of an MLRO.

- Thematic Review on AML/CFT – Common Findings Report – 2024 The report is a summary of observations made during the review/inspection of the AML function of the DNFBPs. The report documents recommended best practices and areas for improvement for ADGM-based DNFBPs.

- 2024 DNFBP Common Findings Report The report gives out common findings identified by the RA during onsite assessments of DNFBPs, especially recurring observations across the majority of the firms.

- NAMLCFTC Decision – Application of the Travel Rule Obligations

- ADGM Legal Persons & Arrangements Risk Assessment Discusses ML risk posed by ADGM Legal Persons and Legal Arrangements.

- ADGM Financial Crime Report 2021-2022 Elaborates how FSRA supports its objectives of prevention of financial crime and aligns with UAE’s national AML/TFS agenda through RA and the Financial and Cyber-Crime Prevention unit (FCCP).

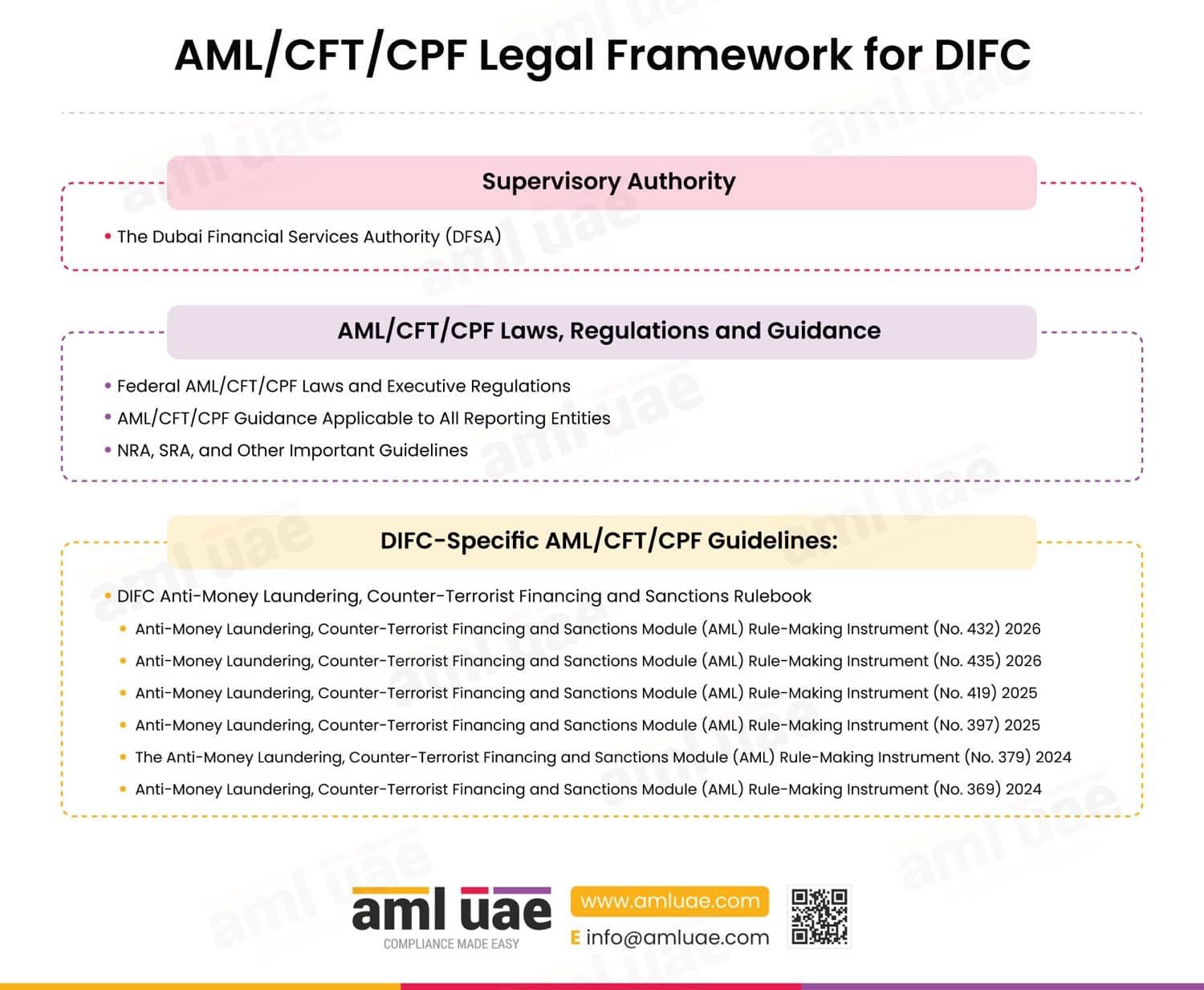

AML/CFT/CPF Legal Framework for Dubai International Financial Centre (DIFC)

Supervisory Authority:

The Dubai Financial Services Authority (DFSA) is the licensing and AML supervisory authority for entities operating in or from DIFC, regardless of their nature of activities, whether as a DNFBP, VASP, or a company carrying out financial activities.

AML/CFT/CPF Laws, Regulations and Guidance Applicable to DIFC

- Federal AML/CFT/CPF Laws and Executive Regulations

- AML/CFT/CPF Guidance Applicable to All Reporting Entities

- NRA, SRA, and Other Important Guidelines

DIFC AML/CFT/CPF Legal Framework and Key Deviations from the Federal AML Law:

The definition of DNFBP is different from what is provided under the federal AML law, bringing in more non-financial activities under the AML regime. The entities conducting the following activities are considered DNFBP in DIFC:

- a real-estate developer or agency which carries out transactions with a customer involving the buying or selling of real property,

- a dealer in precious metals or precious stones which carries out any single cash transaction or several transactions that appear to be connected and the value of which is equal to or greater than USD 15,000,

- a person who issues, or provides services relating to Non-Fungible Tokens or Utility Tokens (with certain exceptions),

- a law firm, notary firm, or other independent legal business,

- an accounting firm, audit firm or insolvency firm, and

- a company service provider.

DIFC-Specific AML/CFT/CPF Laws, Regulations and Guidance

Compliance with the rulebook below is mandatory for DFSA-regulated entities, in addition to federal decree laws, implementing regulations, and cabinet decisions.

- DIFC Anti-Money Laundering, Counter-Terrorist Financing and Sanctions Rulebook The rulebook provides for the key AML/CFT obligations of a regulated entity operating in or from DIFC, guiding them in adequately identifying and mitigating the financial crime risks. The Dubai Financial Services Authority (DFSA) systematically updates its Anti-Money Laundering, Counter-Terrorist Financing and Sanctions (AML) Module to respond to emerging ML/FT and PF risks, technological advancements and shifts in UAE legislation by publishing Rule-Making Instruments (RMIs). The RMIs published from 2024 to date (March 2026) are intended to showcase the trajectory of the DFSA AML regime.

- Anti-Money Laundering, Counter-Terrorist Financing and Sanctions Module (AML) Rule-Making Instrument (No. 432) 2026 amends the Registration and notification provisions contained in the DIFC AML, CFT and Sanctions Rulebook with effect from 1st April 2026.

- Anti-Money Laundering, Counter-Terrorist Financing and Sanctions Module (AML) Rule-Making Instrument (No. 435) 2026 amends the DFSA AML, CFT and Sanctions Rulebook to align it with new Federal AML/CFT legislation, particularly the Federal Law No. 10 of 2025 and Cabinet Resolution No. 134 of 2025, effective 2nd March 2026. The compliance impact of such alignment would require regulated entities to update their internal controls, reporting protocols, and asset-freezing measures.

- Anti-Money Laundering, Counter-Terrorist Financing and Sanctions Module (AML) Rule-Making Instrument (No. 419) 2025 Implements various minor and consequential amendments to the AML module, such as deleting the definition of “Domestic Fund” and explicitly adding the “Office of Financial Sanctions Implementation” (OFSI) when referring to U.K. HM Treasury sanctions, expecting proactive compliance steps from entities regulated by DFSA.

- Anti-Money Laundering, Counter-Terrorist Financing and Sanctions Module (AML) Rule-Making Instrument (No. 397) 2025 The definition of CSPs was updated, Simplified CDD measures were edited, and the annual AML reporting portal details were updated, with effective date from 3rd March 2025.

- The Anti-Money Laundering, Counter-Terrorist Financing and Sanctions Module (AML) Rule-Making Instrument (No. 379) 2024 came into force on 3rd June 2024, introducing the updated version of the AML/CFT Rulebook and repealing the previous one.

- Anti-Money Laundering, Counter-Terrorist Financing and Sanctions Module (AML) Rule-Making Instrument (No. 369) 2024 came into force on 1st May 2024, introducing the updated version of the AML/CFT Rulebook, repealing the previous version.

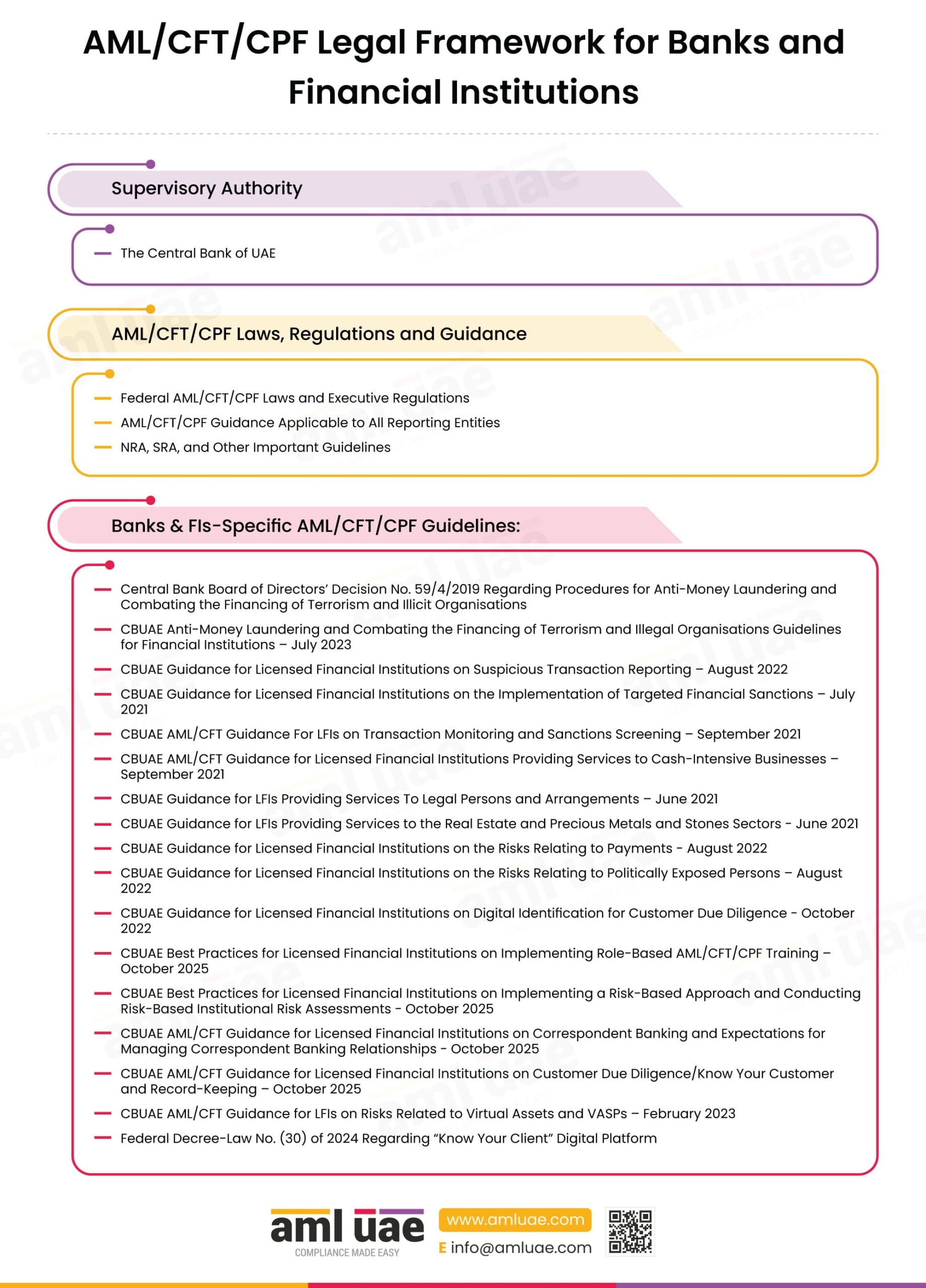

AML/CFT/CPF Legal Framework for Banks and Financial Institutions Supervised by CBUAE

Entities within the UAE’s financial sector operate under a stringent AML/CFT regime supervised primarily by the Central Bank of the UAE (CBUAE) and other specialised authorities like the Capital Market Authority (CMA). Compliance obligations extend across banking, insurance, capital markets, and payment services, and other financial activities, with sector-specific regulations supplementing the federal AML/CFT framework.

All banks and financial institutions have to adhere to:

- Federal AML/CFT/CPF Laws and Executive Regulations

- AML/CFT/CPF Guidance Applicable to All Reporting Entities

- NRA, SRA, and Other Important Guidelines

- Central Bank Board of Directors’ Decision No. 59/4/2019 Regarding Procedures for Anti-Money Laundering and Combating the Financing of Terrorism and Illicit Organisations

This decision of the CBUAE mandates the licensed financial institutions to comply with the federal AML regulations and grants power to the CBUAE to supervise and inspect the financial institutions for such compliance.

- CBUAE Anti-Money Laundering and Combating the Financing of Terrorism and Illegal Organisations Guidelines for Financial Institutions – July 2023

These guidelines, issued by the CBUAE, provide guidance and assistance to the FIs in their efforts to effectively implement the provisions of the federal AML regulations and ensure compliance with the statutory obligations.

- CBUAE Guidance for Licensed Financial Institutions on Suspicious Transaction Reporting – August 2022

This guidance document has been issued by the CBUAE to help its regulated entities identify and report suspicious transactions. It includes the illustrative list of ML/FT red flags, guides on the timing and effective process of internal and external reporting of the observed suspicion.

- CBUAE Guidance for Licensed Financial Institutions on the Implementation of Targeted Financial Sanctions – July 2021

In conjunction with the TFS guidelines issued by the EOCN, the CBUAE also issued guidance for its supervised entities, mandating that they define their sanctions risk appetite, document their TFS policy, and deploy the required internal controls. Additionally, the guidance provides a detailed methodology for conducting sanctions screening and for reviewing screening results.

- CBUAE AML/CFT Guidance For LFIs on Transaction Monitoring and Sanctions Screening – September 2021

This guidance, issued by the CBUAE, mandates that regulated entities design, implement, and maintain an effective transaction monitoring and sanctions screening program. This includes guidance on defining monitoring rules, alert scoring and prioritisation, testing and validating transaction monitoring rules, etc.

- CBUAE AML/CFT Guidance for Licensed Financial Institutions Providing Services to Cash-Intensive Businesses – September 2021

The CBUAE has issued this guidance to assist licensed entities in understanding and mitigating risks when providing financial services to customers engaged in cash-intensive operations, and to guide them in complying with their AML/CFT obligations. It discusses the risk-based approach and the corresponding risk mitigation measures to be implemented.

- CBUAE Guidance for LFIs Providing Services To Legal Persons and Arrangements – June 2021

By way of this guidance, CBUAE requires the regulated entities to identify and adequately manage the ML/FT risks when engaging with legal persons and legal arrangements. It also requires entities to identify beneficial owners and provides detailed measures for this.

- CBUAE Guidance for LFIs Providing Services to the Real Estate and Precious Metals and Stones Sectors – June 2021

This guidance has been issued by the CBUAE to help regulated entities understand and mitigate risks they may face when providing financial services to the real estate, precious metals and stones sectors, given these sectors’ vulnerabilities to financial crime. It discusses the risk-based approach and the corresponding risk mitigation measures to be implemented.

- CBUAE Guidance for Licensed Financial Institutions on the Risks Relating to Payments – August 2022

This guidance helps the regulated entities in understanding the financial crime risk associated with different types of payments and the corresponding risk mitigation measures that can be deployed to manage such ML/FT risks.

- CBUAE Guidance for Licensed Financial Institutions on the Risks Relating to Politically Exposed Persons – August 2022

The guidance has been issued to help regulated entities identify and manage risks when engaging with politically exposed persons. It provides detailed guidance on identifying PEPs, understanding the potential risks involved, and the risk mitigation measures to be adopted when serving PEPs.

- CBUAE Guidance for Licensed Financial Institutions on Digital Identification for Customer Due Diligence – October 2022

The guidance helps regulated entities effectively implement technology to support the digital identification of customers as part of the CDD process. It also discusses the risks and challenges associated with digital identification, as well as the reliability and independence of the digital identification system for CDD.

- CBUAE Best Practices for Licensed Financial Institutions on Implementing Role-Based AML/CFT/CPF Training – October 2025

The CBUAE’s best practice document guides regulated entities in developing a role-based AML/CFT/CPF training program, focusing on the different levels of the team hierarchy, such as senior management, the first line of defence, etc. It also helps the entities understand effective methods for imparting training and maintaining training logs and other records.

- CBUAE Best Practices for Licensed Financial Institutions on Implementing a Risk-Based Approach and Conducting Risk-Based Institutional Risk Assessments – October 2025

This best practice document guides the regulated entities on developing a risk assessment methodology, conducting a risk-based business risk assessment, and implementing the risk-based approach. It also describes the principles and the best practices for ML/FT/PF risk assessment.

- CBUAE AML/CFT Guidance for Licensed Financial Institutions on Correspondent Banking and Expectations for Managing Correspondent Banking Relationships – October 2025

This guidance applies to all regulated entities that form part of the correspondent banking chain. Through this guidance, the CBUAE helps entities understand the various risk factors affecting correspondent banking and the risk mitigation controls that should be adopted.

- CBUAE AML/CFT Guidance for Licensed Financial Institutions on Customer Due Diligence/Know Your Customer and Record-Keeping – October 2025

The guidance aims to assist regulated entities in identifying customers, developing their risk profiles, and implementing the overall AML record-keeping policy, specifically from a CDD perspective.

- CBUAE AML/CFT Guidance for LFIs on Risks Related to Virtual Assets and VASPs – February 2023

The guidance helps regulated entities understand the risks associated with virtual assets and virtual asset service providers. It mandates regulated entities to adopt certain mitigation measures when engaging with VASPs or handling customers’ virtual asset-related transactions, including obtaining the CBUAE’s Non-Objection to opening any new account for VASPs.

- Federal Decree-Law No. (30) of 2024 Regarding “Know Your Client” Digital Platform

Through this decree law, the authorities empower the establishment of a designated company to create and manage a platform for collecting, analysing, utilising, exchanging, and trading KYC data, as well as issuing KYC reports.

Along with the above-referred federal decree laws and implementing regulations, and cabinet decisions, the financial institutions shall be subject to the following guiding publications by the relevant supervisory authorities:

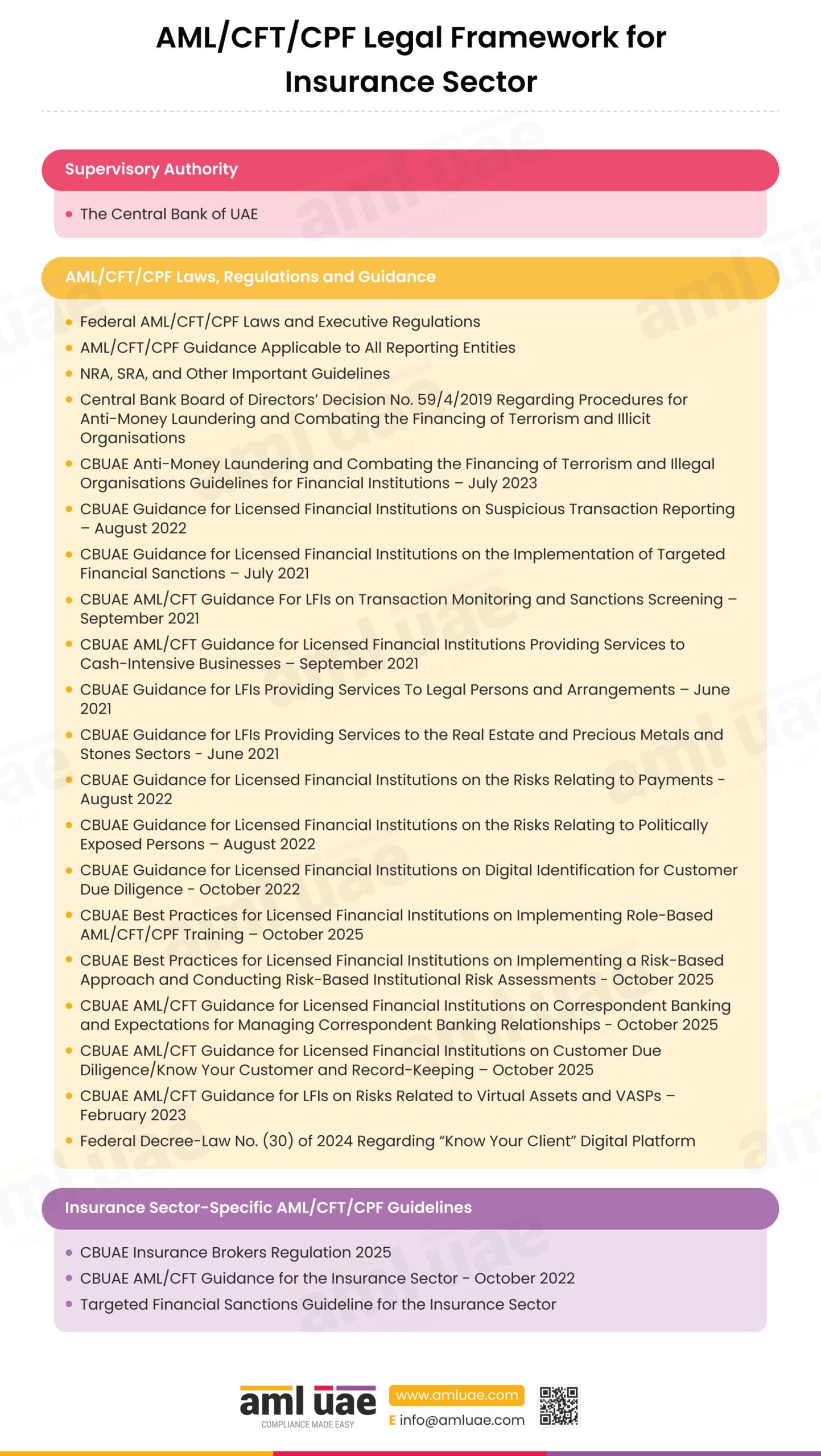

AML/CFT/CPF Legal Framework for Insurance Sector (Insurance companies, insurance agents/brokers)

Supervisory Authority:

CBUAE is the supervisory authority overseeing the effective implementation of AML/CFT regulations by insurance and reinsurance companies, as well as insurance brokers/agents.

AML/CFT/CPF Laws, Regulations and Guidance Applicable to the Insurance Sector

- Federal AML/CFT/CPF Laws and Executive Regulations

- AML/CFT/CPF Guidance Applicable to All Reporting Entities

- NRA, SRA, and Other Important Guidelines

- Central Bank Board of Directors’ Decision No. 59/4/2019 Regarding Procedures for Anti-Money Laundering and Combating the Financing of Terrorism and Illicit Organisations

- CBUAE Anti-Money Laundering and Combating the Financing of Terrorism and Illegal Organisations Guidelines for Financial Institutions – July 2023

- CBUAE Guidance for Licensed Financial Institutions on Suspicious Transaction Reporting – August 2022

- CBUAE Guidance for Licensed Financial Institutions on the Implementation of Targeted Financial Sanctions – July 2021

- CBUAE AML/CFT Guidance For LFIs on Transaction Monitoring and Sanctions Screening – September 2021

- CBUAE AML/CFT Guidance for Licensed Financial Institutions Providing Services to Cash-Intensive Businesses – September 2021

- CBUAE Guidance for LFIs Providing Services To Legal Persons and Arrangements – June 2021

- CBUAE Guidance for LFIs Providing Services to the Real Estate and Precious Metals and Stones Sectors – June 2021

- CBUAE Guidance for Licensed Financial Institutions on the Risks Relating to Payments – August 2022

- CBUAE Guidance for Licensed Financial Institutions on the Risks Relating to Politically Exposed Persons – August 2022

- CBUAE Guidance for Licensed Financial Institutions on Digital Identification for Customer Due Diligence – October 2022

- CBUAE Best Practices for Licensed Financial Institutions on Implementing Role-Based AML/CFT/CPF Training – October 2025

- CBUAE Best Practices for Licensed Financial Institutions on Implementing a Risk-Based Approach and Conducting Risk-Based Institutional Risk Assessments – October 2025

- CBUAE AML/CFT Guidance for Licensed Financial Institutions on Correspondent Banking and Expectations for Managing Correspondent Banking Relationships – October 2025

- CBUAE AML/CFT Guidance for Licensed Financial Institutions on Customer Due Diligence/Know Your Customer and Record-Keeping – October 2025

- CBUAE AML/CFT Guidance for LFIs on Risks Related to Virtual Assets and VASPs – February 2023

- Federal Decree-Law No. (30) of 2024 Regarding “Know Your Client” Digital Platform

Insurance Sector-Specific AML/CFT/CPF Guidance

Additionally, the adherence to the following regulatory documents is also mandatory:

- CBUAE Insurance Brokers Regulation 2025

The regulations mandate the licensed insurance companies to comply with the federal AML/CFT regulations.

- CBUAE AML/CFT Guidance for the Insurance Sector – October 2022

The guidance focuses on the AML/CFT obligations of the entities engaged in insurance activities. It helps entities understand the potential exposure to financial crime and the mitigation measures required to safeguard the insurance sector and remain compliant with the regulatory regime.

- Targeted Financial Sanctions Guideline for the Insurance Sector

The EOCN has issued a specific guideline for the issuance sector, laying down the authorities’ expectations regarding customer screening, timelines, screening procedures, and reporting requirements.

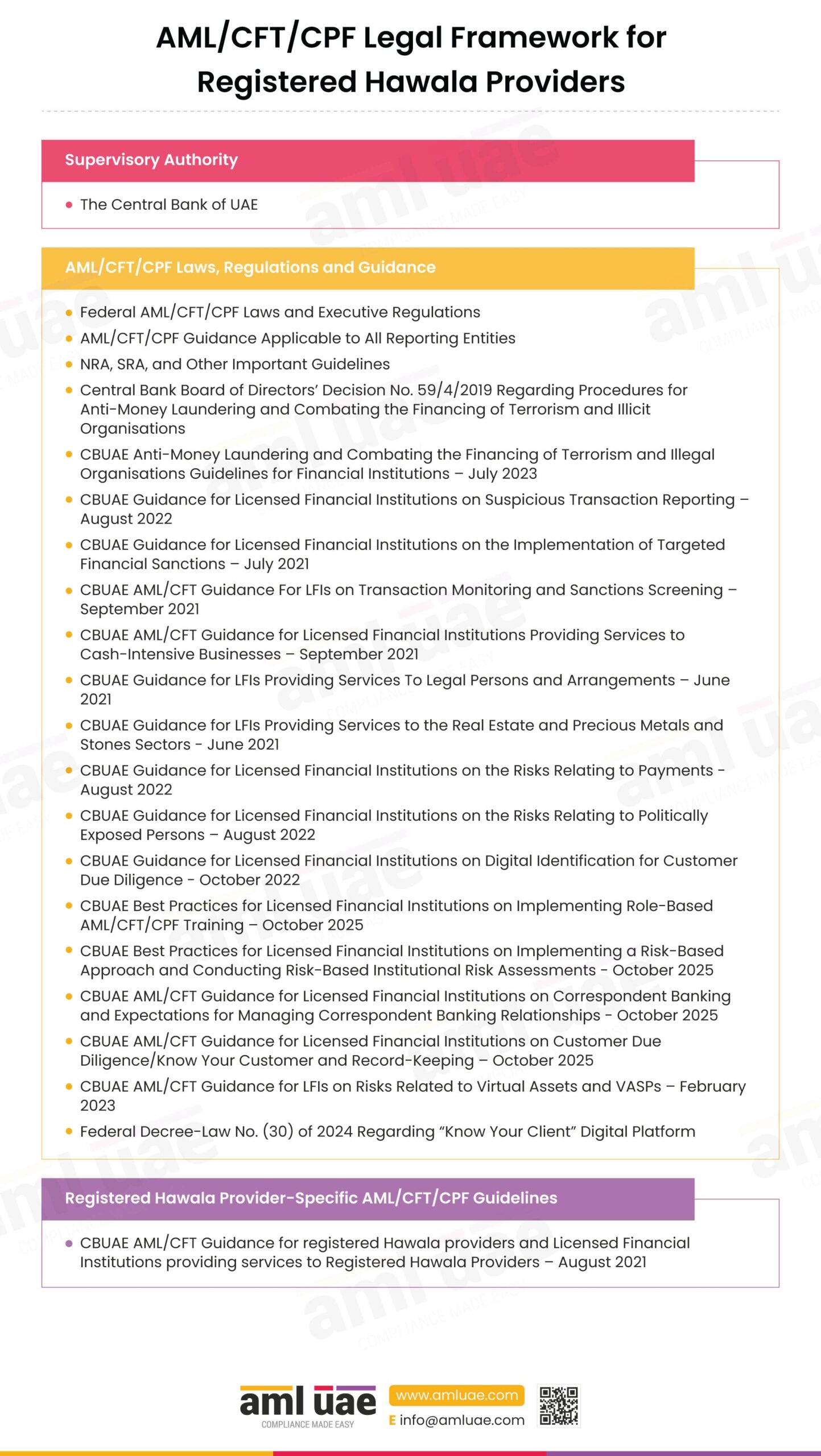

AML/CFT/CPF Legal Framework for Registered Hawala Providers

Supervisory Authority:

CBUAE is the supervisory authority overseeing the effective implementation of AML/CFT regulations by registered hawala providers.

AML/CFT/CPF Laws, Regulations and Guidance Applicable to the Registered Hawala Providers

- Federal AML/CFT/CPF Laws and Executive Regulations

- AML/CFT/CPF Guidance Applicable to All Reporting Entities

- NRA, SRA, and Other Important Guidelines

- Central Bank Board of Directors’ Decision No. 59/4/2019 Regarding Procedures for Anti-Money Laundering and Combating the Financing of Terrorism and Illicit Organisations

- CBUAE Anti-Money Laundering and Combating the Financing of Terrorism and Illegal Organisations Guidelines for Financial Institutions – July 2023

- CBUAE Guidance for Licensed Financial Institutions on Suspicious Transaction Reporting – August 2022

- CBUAE Guidance for Licensed Financial Institutions on the Implementation of Targeted Financial Sanctions – July 2021

- CBUAE AML/CFT Guidance For LFIs on Transaction Monitoring and Sanctions Screening – September 2021

- CBUAE AML/CFT Guidance for Licensed Financial Institutions Providing Services to Cash-Intensive Businesses – September 2021

- CBUAE Guidance for LFIs Providing Services To Legal Persons and Arrangements – June 2021

- CBUAE Guidance for LFIs Providing Services to the Real Estate and Precious Metals and Stones Sectors – June 2021

- CBUAE Guidance for Licensed Financial Institutions on the Risks Relating to Payments – August 2022

- CBUAE Guidance for Licensed Financial Institutions on the Risks Relating to Politically Exposed Persons – August 2022

- CBUAE Guidance for Licensed Financial Institutions on Digital Identification for Customer Due Diligence – October 2022

- CBUAE Best Practices for Licensed Financial Institutions on Implementing Role-Based AML/CFT/CPF Training – October 2025

- CBUAE Best Practices for Licensed Financial Institutions on Implementing a Risk-Based Approach and Conducting Risk-Based Institutional Risk Assessments – October 2025

- CBUAE AML/CFT Guidance for Licensed Financial Institutions on Correspondent Banking and Expectations for Managing Correspondent Banking Relationships – October 2025

- CBUAE AML/CFT Guidance for Licensed Financial Institutions on Customer Due Diligence/Know Your Customer and Record-Keeping – October 2025

- CBUAE AML/CFT Guidance for LFIs on Risks Related to Virtual Assets and VASPs – February 2023

- Federal Decree-Law No. (30) of 2024 Regarding “Know Your Client” Digital Platform

Registered Hawala Providers Sector-Specific AML/CFT/CPF Guidance

Additionally, the adherence to the following is also mandatory for the registered hawala providers:

The guidance focuses on registered hawala providers’ AML/CFT obligations, including registration requirements, developing their AML/CFT program, and the AML reporting mandate.

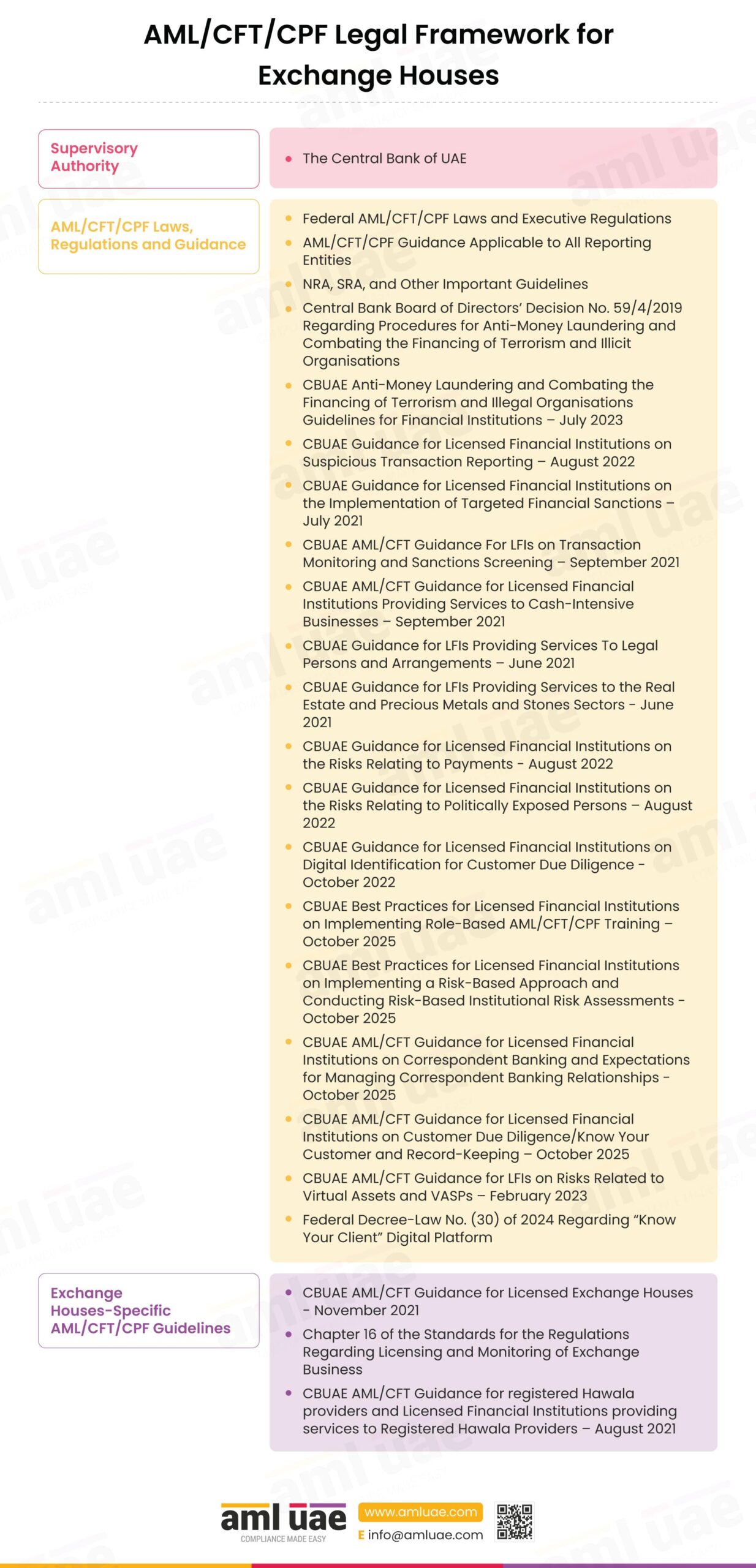

AML/CFT/CPF Legal Framework for Exchange Houses

Supervisory Authority:

CBUAE is the AML supervisory authority for the exchange houses operating in the UAE.

AML/CFT/CPF Laws, Regulations and Guidance Applicable to the Exchange Houses

- Federal AML/CFT/CPF Laws and Executive Regulations

- AML/CFT/CPF Guidance Applicable to All Reporting Entities

- NRA, SRA, and Other Important Guidelines

- Central Bank Board of Directors’ Decision No. 59/4/2019 Regarding Procedures for Anti-Money Laundering and Combating the Financing of Terrorism and Illicit Organisations

- CBUAE Anti-Money Laundering and Combating the Financing of Terrorism and Illegal Organisations Guidelines for Financial Institutions – July 2023

- CBUAE Guidance for Licensed Financial Institutions on Suspicious Transaction Reporting – August 2022

- CBUAE Guidance for Licensed Financial Institutions on the Implementation of Targeted Financial Sanctions – July 2021

- CBUAE AML/CFT Guidance For LFIs on Transaction Monitoring and Sanctions Screening – September 2021

- CBUAE AML/CFT Guidance for Licensed Financial Institutions Providing Services to Cash-Intensive Businesses – September 2021

- CBUAE Guidance for LFIs Providing Services To Legal Persons and Arrangements – June 2021

- CBUAE Guidance for LFIs Providing Services to the Real Estate and Precious Metals and Stones Sectors – June 2021

- CBUAE Guidance for Licensed Financial Institutions on the Risks Relating to Payments – August 2022

- CBUAE Guidance for Licensed Financial Institutions on the Risks Relating to Politically Exposed Persons – August 2022

- CBUAE Guidance for Licensed Financial Institutions on Digital Identification for Customer Due Diligence – October 2022

- CBUAE Best Practices for Licensed Financial Institutions on Implementing Role-Based AML/CFT/CPF Training – October 2025

- CBUAE Best Practices for Licensed Financial Institutions on Implementing a Risk-Based Approach and Conducting Risk-Based Institutional Risk Assessments – October 2025

- CBUAE AML/CFT Guidance for Licensed Financial Institutions on Correspondent Banking and Expectations for Managing Correspondent Banking Relationships – October 2025

- CBUAE AML/CFT Guidance for Licensed Financial Institutions on Customer Due Diligence/Know Your Customer and Record-Keeping – October 2025

- CBUAE AML/CFT Guidance for LFIs on Risks Related to Virtual Assets and VASPs – February 2023

- Federal Decree-Law No. (30) of 2024 Regarding “Know Your Client” Digital Platform

Exchange Houses Sector-Specific AML/CFT/CPF Guidance

Additionally, the exchange houses must comply with the following: