FRAML Software

This page talks about how Regulated Entities in the UAE can strengthen their compliance programs by using FRAML Software, an integrated solution that combines Fraud Detection and Anti-Money Laundering (AML) capabilities into one unified platform. Built to align with UAE laws, FATF standards, and goAML reporting requirements, this solution is tailored to help Regulated Entities reduce risk, enhance operational control, and stay ahead of emerging threats.

What is FRAML Software

Fraud and Anti-Money Laundering Software (FRAML Software) is an integrated platform which helps in detecting, preventing, and managing both Fraud and Money Laundering (ML) activities within the Regulated Entity in UAE.

Fraud is not just a financial threat; it is often tied to Money Laundering.

Fraud and Anti-Money Laundering Tool tackles both by unifying data, workflows, and analytics into a single system. Through the use of advanced technologies such as machine learning, behavioural analytics, and dynamic risk scoring, the software significantly enhances operational efficiency while ensuring compliance with stringent regulatory expectations.

By adopting FRAML Software, Regulated Entities including Financial Institutions (FIs), Designated Non-Financial Businesses and Professions (DNFBPs), Virtual Asset Service Providers (VASPs) can proactively manage risk, align with UAE Ministry of Economy and FATF recommendations, and safeguard their operations and reputation in a fast-evolving compliance landscape.

Legal and Regulatory Requirements of FRAML in UAE

There is always a possibility that both natural and legal persons might be involved in fraud or predicate offences leading to ML activities. Individuals often exploit digital platforms and mule accounts to facilitate illicit transactions. Among legal entities, fraudulent activity is frequently linked to newly established companies either on the mainland or within commercial free zones.

To effectively combat these risks, Regulated Entities must have Fraud and Anti-Money Laundering Solution that comply with a robust framework of national and international AML/CFT regulations. These include:

Federal Decree by Law No. (10) of 2025:

Framework on Anti-Money Laundering and Combating the Financing of Terrorism and Illegal Organizations.

Cabinet Resolution No. (134) of 2025:

Framework for the implementation of the AML and CFT regulations.

Cabinet Decision No (109) of 2023 On Regulating the Beneficial Owner Procedures:

Framework for Ultimate Beneficial Ownership (UBO) related requirements.

FIU STR/SAR Reporting Guidelines:

Procedures for filing Suspicious Transaction Reports (STRs) and Suspicious Activity Reports (SARs) with the UAE Financial Intelligence Unit (FIU).

FATF Recommendations:

The FATF sets international standards for AML and CFT. FATF provides a list of 21 predicate offenses that constitute money laundering crimes under international law. Fraud is recognized as one of these predicate offenses. The UAE, as a FATF member, is committed to aligning its laws and practices with these global standards.

Federal Decree-Law No. (31) of 2021 Promulgating the Crimes and Penalties Law:

Article 451 provides, outlines the criminal offense of fraud and associated penalties.

Stop switching between fraud and AML tools

Detect fraud and Money Laundering in one intelligent platform built for UAE regulations.

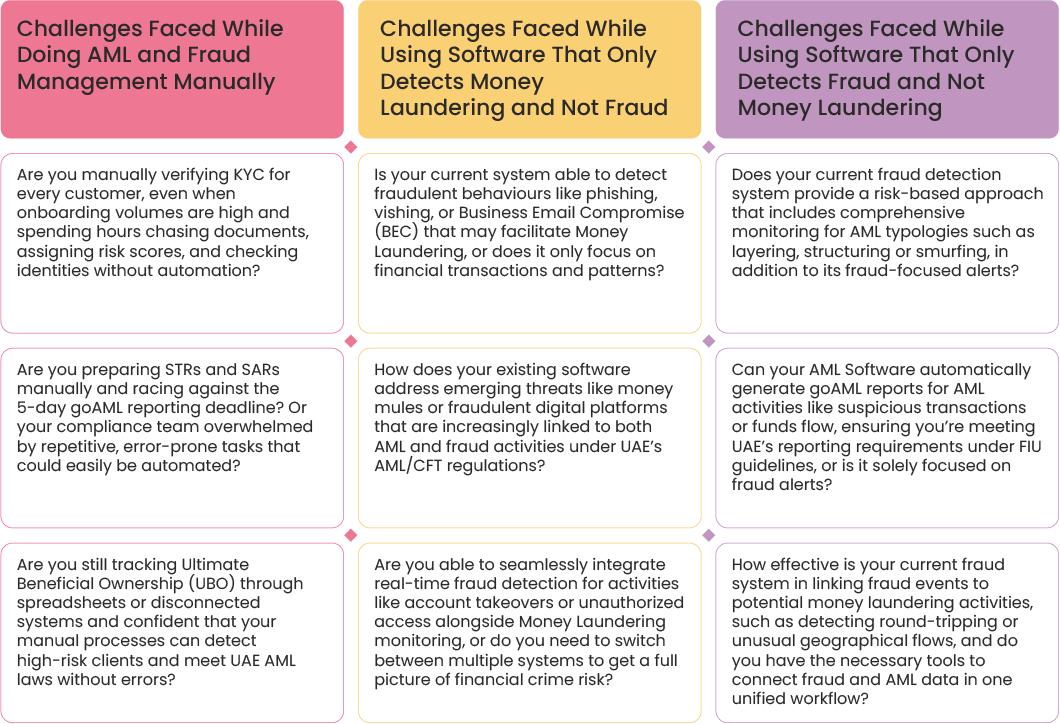

Recurring Gaps in FRAML Compliance: Which One Are You Facing?

Gaps in FRAML Compliance affect Regulated Entities with exposure to financial crime and regulatory penalties, as manual processes are time-consuming and prone to errors. Further, ML detection software misses fraud typologies like money mules and phishing; on the other hand, fraud detection system misses ML/TF risks and reporting requirements. These gaps in FRAML Compliance are identified in the infographic below:

Struggling with Manual Compliance? Let’s Automate It.

Say goodbye to spreadsheets and deadlines. Discover how fraud and AML softwae simplifies AML and Fraud Prevention workflows.

Why FRAML Software Is the Ultimate Compliance Solution in the UAE: Two Fights, One Tool

FRAML Software provides a unified risk scoring approach that detects fraud as well as Money Laundering typologies, performs Transaction Monitoring, PEP/Sanctions Screening, maps UBOs, and auto-generates reporting with machine learning & behavioural analytics capabilities.

This side-by-side comparison shows how FRAML brings it all together cutting costs, closing gaps, and keeping your compliance team one step ahead.

Fraud Detection, AML/CFT Compliance Requirements & Software Capabilities | AML/CFT Software Capabilities | Fraud Management Software Capabilities | Capabilities That Set FRAML Software Apart |

Risk Assessment | AML Centric | Fraud Centric | Unified Risk Scoring |

Fraud Typology Detection | No | Yes | Yes |

Money Laundering Typology Detection | Yes | No | Yes |

Transaction Monitoring | Suspicious patterns | Account takeovers | Both in real-time |

PEP/Sanctions Screening | Yes | No | Yes, continuous |

Ultimate Beneficial Ownership (UBO) Mapping | Yes | No | Yes |

Machine Learning & Behavioural Analytics For Fraud Detection and Ongoing Monitoring | Limited | Limited | Yes |

goAML Reporting Assistance | Limited | Limited | Yes, auto generated |

“With Money Laundering and Terrorist Financing, other fraud activities such as money mules and phishing are also prevalent. This makes it necessary to manage both fraud and money laundering. In my belief, working with an integrated compliance platform – FRAML Software- can ease the detection and prevention of financial crimes.”

How FRAML Solution Helps

Regulated Entities Fight Fraud & ML Risks

In the UAE, Fraud has become a critical driver of Money Laundering. The rising number of Fraud-related Suspicious Transaction Reports (STRs) and Suspicious Activity Reports (SARs) highlights the urgency for advanced detection Software. Fraud schemes such as phishing, vishing, Business Email Compromise (BEC ), and investment scams continue to exploit digital vulnerabilities often enabled by money mules, social engineering, and fake platforms.

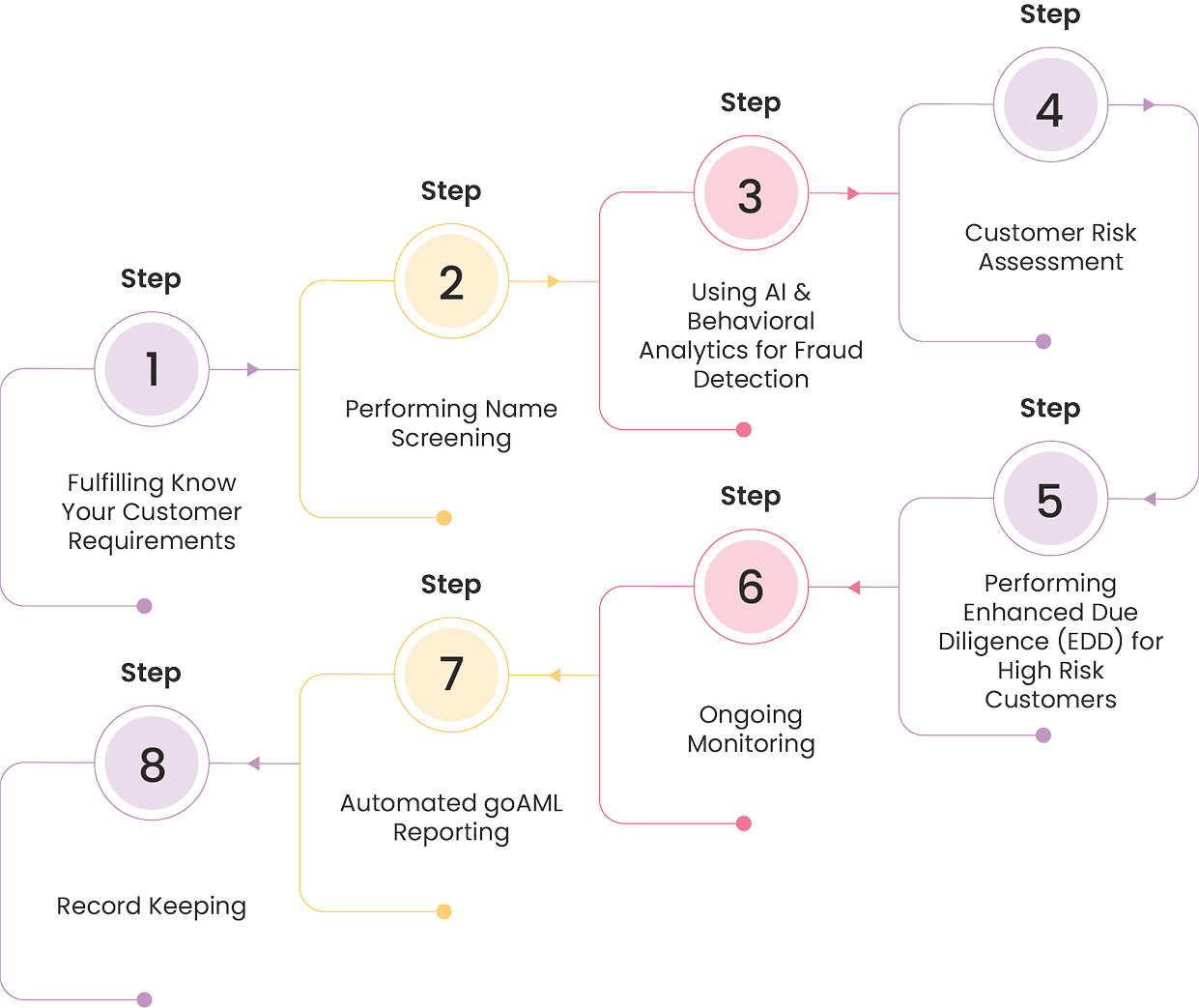

FRAML Software integrates the following best practices into a unified compliance platform, specifically designed to support Regulated Entities in the UAE in meeting the stringent Anti-Money Laundering (AML) and Counter-Terrorism Financing (CTF) obligations mandated by local and international regulatory frameworks. The solution guides Regulated Entities through the following essential compliance processes:

1. Fulfilling Know Your Customer Requirements

FRAML Software automates KYC during onboarding. It also maps ownership structures to uncover hidden Ultimate Beneficial Ownership (UBO) using integrated databases. The FRAML Software prevents ML & Fraud by:

- Detecting fake identities via biometric and ID Verification

- Verifying the source of funds and wealth

- Exposing layered or proxy ownerships used to hide illicit assets.

2. Performing Name Screening

A unified FRAML Software continuously screens customers and transactions against UN, UAE Cabinet, FATF, and other watchlists to curb fraudulent transactions and mitigate the risk of ML. The software:

- Identifies Customers and business associates against UAE Local Terrorist Lists, UN Terrorist Lists, and other international lists

- Verifies the name against various databases for PEP Screening

- Search the customers against the Adverse Media sources.

3. Using AI & Behavioural Analytics for Fraud Detection

FRAML Software tracks customer behaviour across channels, login patterns, devices, geolocations and compares it against normal profiles using machine learning. It helps the Regulated Entities to:

- Identify account takeovers, credential stuffing, and bot-driven fraud

- Detect unauthorised payments, stolen card usage, and impossible travel patterns.

4. Customer Risk Assessment

FRAML Software dynamically evaluates risk by assigning real-time risk scores to clients, transactions, and entities based on behaviour, activity, and rule-based triggers. It also considers built-in anti-fraud controls and product-level safeguards to mitigate ML/TF risks supporting both compliance and financial inclusion goals.

It helps Regulated Entities:

- Separate low-risk and high-risk cases for focused AML review

- Reduce false positives by tailoring rules to specific risk categories.

5. Initiating Enhanced Due Diligence for High-Risk Customers

FRAML Software initiate Enhanced Due Diligence (EDD) protocols for red-flag clients like foreign PEPs, crypto investors, or individuals with links to high-risk countries. It helps the Regulated Entities in:

- Collecting additional documents, such as income statements and beneficial ownership declarations

- Performing geopolitical risk scoring for cross-border clients

- Identifying shell companies and front businesses to mitigate the risk of Fraud.

6. Ongoing Monitoring

The FRAML Software continuously monitors all transactions, individuals, and entities in real time , comparing them against known Money Laundering patterns and fraud typologies to detect and flag suspicious activity instantly by:

- Detecting the structuring/smurfing transactions (breaking up large transfers into small ones)

- Flagging round-tripping, rapid movement of funds, and unusual geographic flows

- Catching account takeovers, unauthorised access, and unusual device or location usage.

7. Automated Reporting on goAML

When any fraudulent or Money Laundering activity is detected, FRAML Software generates a complete report ready for submission to goAML within the stipulated time period. The FRAML Software:

- Ensures early escalation of potential ML or Fraudulent Activity

- Aligns with UAE FIU requirements for standardised reporting

- Includes attachments like UBO charts, KYC profiles, and transaction histories.

8. Record Keeping

FRAML Software helps to mitigate fraud and ML activities by maintaining the record of all alerts, investigations, approvals, and STR filings for 5 years as per UAE AML laws. It helps the Regulated Entities as it:

- Enables quick forensic investigations

- Proves regulatory compliance during inspections

- Reduces manual documentation errors

Is Your AML Strategy Ready for UAE’s Digital Fraud Surge?

Protect your operations with AI-driven detection and goAML ready reporting.

Must-Have Features and Functionalities in Fraud and AML Software

FRAML Software must be equipped with advanced behavioural analytics, AI-driven analytics & blockchain-backed transparency, multi-factor authentication, telecom inclusion, fraud registry and fraud taskforce integration.

These advanced and essential features will enable a Regulated Entity’s AML program to be robust, efficient, and adaptable to the evolving complexities of modern Fraud and Money Laundering activities.

AI-Driven Analytics & Blockchain-Backed Transparency

AI enables the FRAML Software to detect complex fraud and ML patterns by learning from large datasets and adapting to emerging threats. Meanwhile, blockchain technology ensures transparent, tamper-proof records, especially useful in areas like Digital Identity Verification. Together, they significantly enhance a Regulated Entity’s ability to detect, prevent, and respond to financial crime efficiently and in real time.

Advanced Behavioural Analytics

The FRAML Software should be equipped with advanced behaviour analytics to identify irregular transaction patterns related to fraud. This includes features such as account behaviour profiling, detection of social engineering tactics, and automated cross-checking across digital platforms.

Multi-Factor Authentication

Multi-Factor Authentication (MFA) is a critical feature that FRAML software must include, ensuring secure access to financial platforms. MFA mitigates the risk of unauthorized access by requiring multiple forms of verification such as one-time passwords (OTPs) and biometrics. This adds an extra layer of security and helps Regulated Entities prevent fraud, ensuring compliance with AML controls to minimise financial crime risks.

Integrated Fraud Registry

FRAML Software should include an integrated fraud registry to allow Regulated Entities to quickly cross-check transactions and customer data against a centralised database of high-risk entities, mule accounts, and known fraudsters. This feature enhances AML compliance by ensuring that suspicious individuals or accounts are promptly flagged, reducing the risk of financial crimes.

Fraud Taskforce Integration

FRAML Software must facilitate seamless integration with a fraud task force or unit. This feature enables Regulated Entities to escalate fraud cases for further investigation, helping ensure that suspicious activities are promptly reported to the UAE FIU or other regulatory authorities, in compliance with AML obligations.

Telecom Inclusion for Fraud Detection

FRAML Software should integrate telecom data for enhanced fraud detection, especially related to mobile banking. By analysing data such as SIM swaps or suspicious call/SMS patterns, Regulated Entities can better identify fraud schemes ensuring robust AML safeguards in line with UAE federal decrees.

Experience UAE-specific FRAML Software

Combine ML & Fraud Detection in a single dashboard.

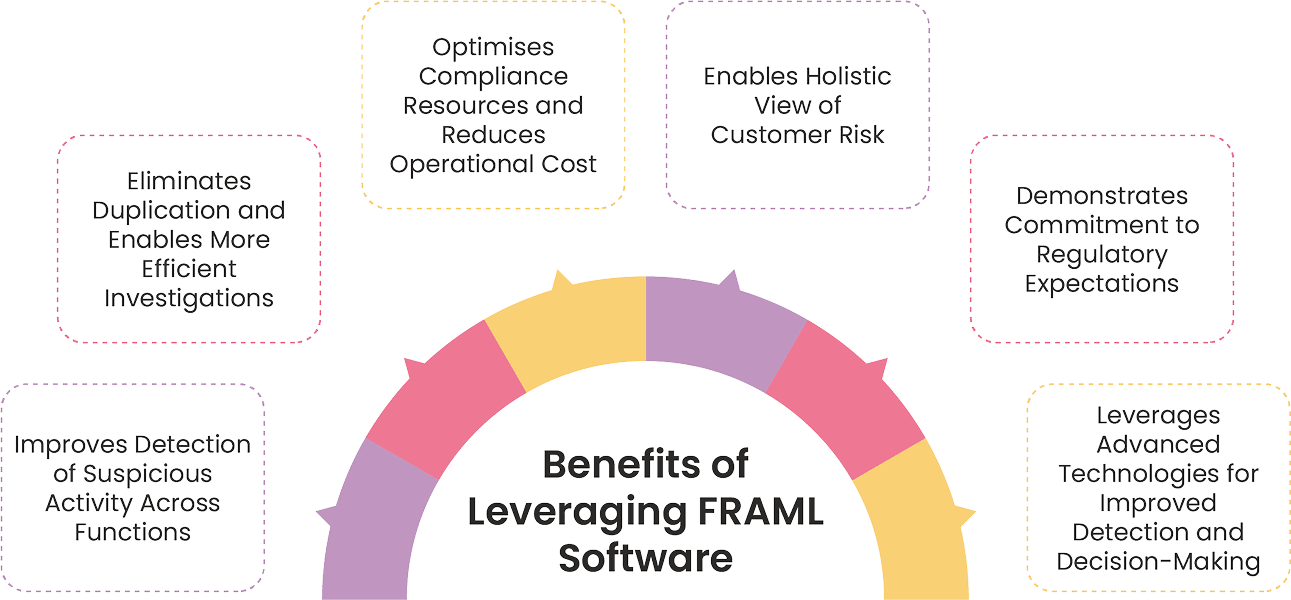

Benefits of Leveraging FRAML Software

Leveraging FRAML Software provides benefits to Regulated Entities such as a unified customer risk view, regulatory commitment, better usage of resources, faster investigations, suspicious activity detection and improved decision making. These benefits are explained below in a detailed format:

Improves Detection of Suspicious Activity Across Functions

The integration of Fraud prevention and AML systems enables Regulated Entities to identify red flags that may otherwise go unnoticed in isolated systems. A combined FRAML Software helps uncover such links early, enhancing the institution’s risk detection capabilities.

Eliminates Duplication and Enables More Efficient Investigations

Without a consolidated approach, AML and Fraud teams may unknowingly investigate the same suspicious activity separately, leading to fragmented intelligence and slower response times. FRAML Software allows for a coordinated review and analysis of cases, thereby improving the efficiency of internal investigations and reporting obligations.

Optimises Compliance Resources and Reduces Operational Cost

By allowing shared use of technology, cross-trained personnel, and consolidated workflows, FRAML Software contributes to more efficient use of human and technical resources. This save costs and strengthens the capacity of Regulated Entities to manage compliance risks without expanding teams or systems unnecessarily.

Enables Holistic View of Customer Risk

Isolated systems can limit the ability to assess customer risk comprehensively. FRAML Software allows for a unified risk view by combining insights from both Fraud and AML touchpoints, improving customer risk rating and enabling more informed decisions around onboarding, transaction monitoring, and escalation.

Demonstrates Commitment to Regulatory Expectations

The adoption of a FRAML Software aligns with international best practices and regulatory expectations that advocate for an integrated response to financial crime risks. This demonstrates a proactive compliance posture that reinforces institutional credibility with regulators and supports long-term risk mitigation.

Leverages Advanced Technologies for Improved Detection and Decision-Making

FRAML Software enables seamless integration of AI, Generative AI, and Machine Learning, enhancing the speed and accuracy of detecting suspicious activity. This supports faster decision-making and aligns with regulatory expectations for the use of advanced technologies in financial crime risk management.

How to Select and Implement FRAML Software:

Best Practices for DNFBPs, VASPs, and SCA- Regulated Entities

Regulated Entities should map FRAML Capabilities with AML & Fraud Risk mitigation requirements to select and implement FRAML Software. The other best practices include enabling real-time transaction monitoring, incorporating KYC, Risk Scoring & Customer Risk Profiling, configuring customer risk scenarios & thresholds, automating goAML Reporting, ensuring strong data security, confidentiality and data protection.

Key considerations for selecting and implementing FRAML Software for Financial Institutions, DNFBPs, VASPs & SCA in UAE are as follows:

Map FRAML Software Capabilities with AML andFraud Risk Mitigation Requirements

Regulated Entities should ensure that FRAML Software aligns with Federal Decree by Law No. (10) of 2025, Cabinet Resolution No. (134) of 2025 & FATF 40 Recommendations. It should detect both internal and external fraud risks and support comprehensive AML/CFT compliance tailored for UAE-regulated entities.

Enable Real-Time Transaction Monitoring with Behavioural Analytics

Regulated Entities should select and implement FRAML software that integrates real-time transaction monitoring with advanced AI and machine learning capabilities. The platform must be capable of instantly detecting suspicious patterns and anomalies. Essential features to implement include behavioural profiling, device fingerprinting, and geolocation tracking to prevent sophisticated digital fraud schemes and money mule activities.

Incorporate KYC,

Risk Scoring and Dynamic Customer Risk Profiling

Regulated Entities should adopt a platform that automates KYC and CDD processes while enabling risk scoring and dynamic customer risk profiling. Implementation should ensure seamless integration of KYC data with AML and fraud detection modules to identify Politically Exposed Persons (PEPs), sanctioned individuals, and high-risk clients.

Configure Custom Risk Scenarios and Thresholds by Business Model

Entities should configure the solution to support both rule-based and AI-based alerting mechanisms tailored to their specific transaction behaviours, customer demographics, and risk appetite. The implementation must reflect the entity’s business model, whether in real estate, crypto, or high net worth client services, ensuring precise detection and minimal false positives.

Automate goAML & Regulatory Reporting Requirements

Businesses must implement a FRAML platform with built-in automation for goAML reporting, including STRs, Confirmed Name Match Report (CNMR), and Partial Name Match Reports (PNMRs). This ensures timely and accurate filing directly to the UAE’s FIU through the goAML portal, maintaining full regulatory compliance.

Ensure Strong Data Security, Confidentiality & UAE Data Protection Compliance

Implementation should prioritise robust data security features, including end-to-end encryption, secure APIs, and role-based access controls. The selected platform must be fully compliant with Federal Decree Law No. 45 of 2021 Regarding the Protection of Personal Data to safeguard client identities, transaction records, and sensitive investigation data throughout the system lifecycle.

FRAML Software That Fits: Tailored Solutions for the UAE’s Compliance Landscape

Too complex. Too expensive. Too disconnected. Fighting fraud and ML (FRAML) doesn’t have to feel like fighting fraud with your hands tied. Here’s how an efficient FRAML Software flips the script with smart, scalable solutions built for the battlefield you’re actually on.

Detect Fraud and Money Laundering in Real Time.

Your Compliance Team Deserves Better Tools.

From Risk to Resilience: Empowering UAE Compliance Through FRAML Software

In today’s high-risk financial landscape, UAE Regulated Entities can no longer afford to treat Fraud and Money Laundering as separate challenges. FRAML Software offers a unified, intelligent solution built specifically for the UAE’s regulatory and risk environment. By combining AML and Fraud detection into one platform, it simplifies compliance, reduces operational burden, and ensures faster, more accurate threat response. AML UAE team helps Regulated Entities navigate, implement, and stay ahead with FRAML best practices. Let us help you build a stronger, smarter FRAML strategy.