Responsible AI Adoption in AML Compliance

Last Updated: 03/31/2026

Protect your business with reliable and effective AML strategies with AML UAE.

Responsible AI Adoption in AML Compliance: Key Takeaways

- Businesses are increasingly relying on Artificial Intelligence (AI) to streamline transaction monitoring, customer risk profiling, and AML investigations.

- Responsible AI Adoption in AML Compliance ensures that AI systems are established with controls proportionate to their regulatory and operational impact.

- AI use cases that influence regulatory reporting or AML compliance decisions require stronger oversight and human review.

- Effective AI Governance in AML compliance includes model validation, human oversight, data governance, and continuous monitoring, which supplements responsible AI Adoption in AML compliance.

- Aligning AI risk management with existing risk-based AML frameworks helps businesses adopt AI responsibly while ensuring regulatory compliance.

- Embedding Human-in-Command, Human-in-the-Loop, and Human-on-the-Loop oversight within existing AML governance frameworks helps ensure responsible AI Adoption in AML Compliance with UAE laws.

- The UAE’s regulatory framework, guided by the National Committee and Supervisory Authority, recognises the impact of new and developing technologies, including AI, in financial crime detection and calls for responsible AI Adoption in AML compliance.

- UAE regulations consistently emphasise that Senior Management and the appointed Compliance Officer remain fully accountable for the outcomes of AI-assisted compliance processes.

- The Senior Management is legally vested with the authority to make strategic decisions and is required to approve all internal controls, acting as the ultimate “Human-in-Command”.

Definition: Responsible AI Adoption in AML Compliance

Responsible AI Adoption in AML Compliance refers to the practice of responsibly implementing artificial intelligence systems according to their potential impact on regulatory reporting, AML compliance decisions and financial crime risk management

With this approach, businesses can apply governance controls that are proportionate to the extent of ML/TF and PF risk associated with each AI application. This ensures that AI tools support AML compliance processes without undermining regulatory accountability or professional judgment.

What Is Responsible AI Adoption in AML Compliance?

A Responsible AI Adoption in AML Compliance involves evaluating and implementing AI applications according to their potential impact on regulatory compliance, operational risk, and financial crime detection outcomes.

This concept aligns with the risk-based approach already embedded in AML/CFT frameworks, where businesses allocate resources and controls in proportion to the level of financial crime risk.

In terms of practical application, responsible AI Adoption in AML compliance or risk-based AI governance involves:

- Identifying where AI is used within AML compliance and ML/TF, and PF risk mitigation processes

- Assessing the risks associated with such AI applications

- Implementing governance controls commensurate with those risks

- Maintaining human accountability for AML compliance decisions.

By applying commensurate oversight, businesses can ensure that AI tools used during ML/TF and PF risk mitigation measures support AML compliance operations without replacing human judgment.

This structured approach ensures that AI improves operational efficiency concerning compliance obligations without undermining regulatory compliance or accountability or exposing the business to unidentified or incidental risks arising from relying on AI tools.

Why Businesses Are Using AI in AML Compliance

Businesses face increasing pressure to detect and report financial crime schemes while managing growing volumes of data. AI technologies offer a tremendous opportunity to simplify and streamline AML programs by improving the speed and accuracy of analysis and output. AI can support AML compliance teams by:

- Detecting complex transaction patterns and anomalies

- Assisting with Customer Risk Profiling

- Accelerating investigative and reporting workflows

- Summarising large volumes of due diligence documentation and case files.

These capabilities of AI tools allow compliance professionals like KYC Analysts, Screening Analysts, Transaction Monitoring Analysts, Risk Analysts, and AML Compliance Officers to focus on high-risk cases and regulatory reporting activities, improving the overall efficacy of AML programs.

The use of AI across various ML/TF and PF risk mitigation measures is elaborated below, necessitating responsible AI Adoption in AML compliance with use cases depicting how AI can be leveraged by the compliance function across the AML lifecycle.

AI Use Cases Across the AML Lifecycle

In order to understand the risks of AI use in AML compliance and ensure responsible AI adoption in AML compliance, it’s important to understand some of its use cases where AI is usually relied upon by compliance teams while carrying out AML compliance obligations.

| AML Compliance Stages | Potential AI Use Cases in AML Compliance |

| Customer Onboarding / KYC | Using Gen AI to ingest KYC documentation and customer identity verification |

| Sanctions Screening | Alert analysis, primary disambiguation and entity resolution |

| Customer Risk Profiling | AI-assisted customer risk scoring and customer risk profiling |

| Transaction Monitoring | Pattern detection and anomaly identification |

| Enhanced Due Diligence | Source of Wealth and Source of Funds analysis and comparative analysis with customer profile |

| AML Investigations | Case summarization and evidence review |

| Suspicious Activity/ Transaction Reporting | Drafting internal SAR/STR narratives for escalation to AML Compliance Officer or MLRO |

| Ongoing Monitoring | Trend detection across transactions and behaviour |

| Recordkeeping | Automated compliance documentation, archival, and retrieval |

Thinking of Using AI in Your AML Program?

We provide Risk Assessments and AML Compliance Advisory

How to Ensure Responsible AI Adoption in AML Compliance

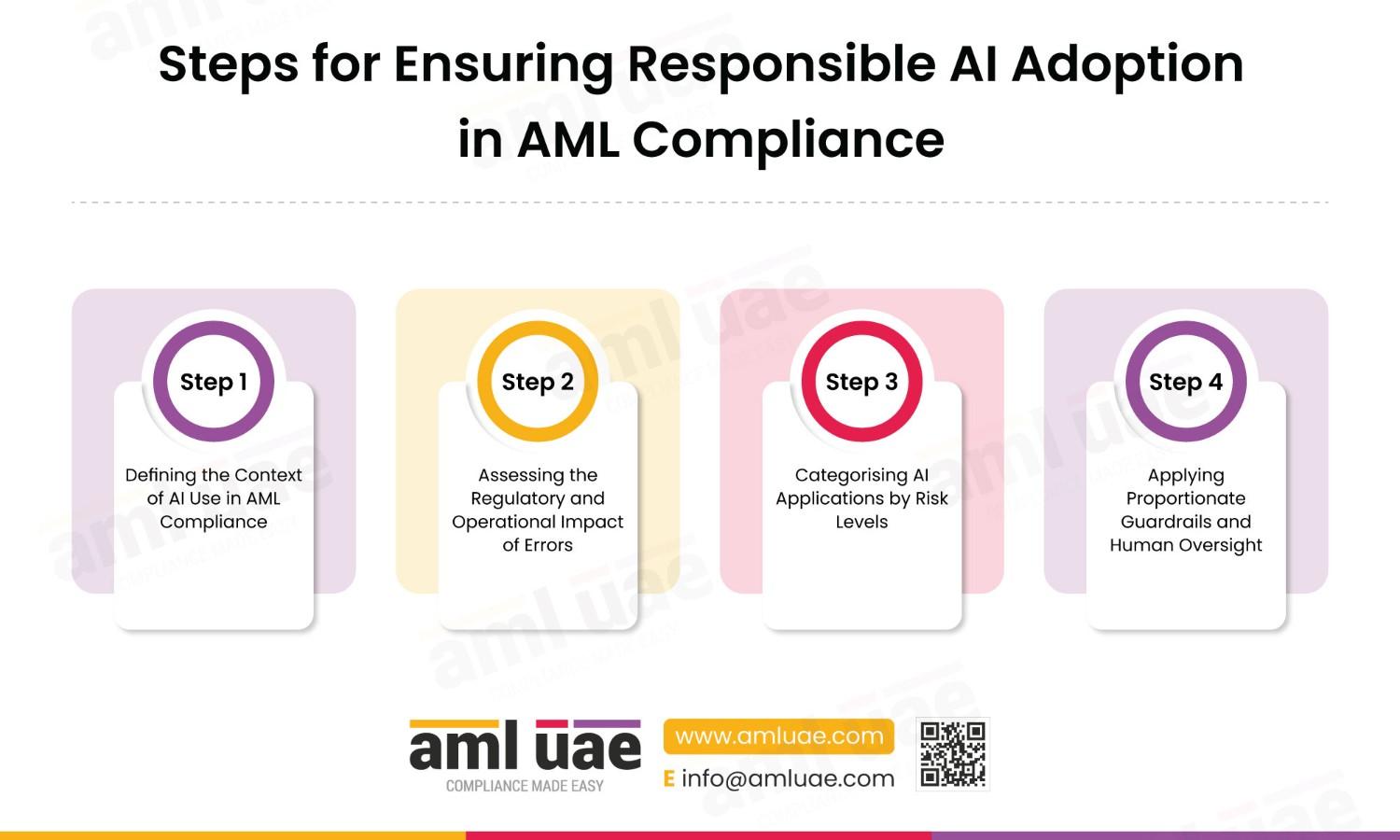

Businesses considering the use of AI in compliance environments should adopt a structured risk evaluation process. This process typically involves four core stages:

- Step 1: Defining the Context of AI Use in AML Compliance

- Step 2: Assessing the Regulatory and Operational Impact of Errors

- Step 3: Categorising AI Applications by Risk Levels

- Step 4: Applying Proportionate Guardrails and Human Oversight

Let us discuss each step in detail.

Step 1: Defining the Context of AI Use in AML Compliance

The first step is to determine how AI outputs will be used by compliance teams within the organisation. Businesses must be mindful of distinguishing between internal analytical and escalation use and external regulatory reporting use.

Internal uses of AI in AML compliance may include:

- Summarising transaction monitoring alerts during initial AML investigations

- Generating case summaries for internal escalation to the AML Compliance Officer or MLRO

- Analysing transactions as well as behavioural patterns and indicators linked to potential money laundering typologies

- Supporting customer risk profiling and re-CDD

- Assisting with instant CDD file reviews

- Summarising and tracing beneficial ownership documentation

- Analysing adverse media and sanctions screening outcomes for quicker disambiguation

- Conducting regulatory research and policy implementation

- Generating internal risk briefings for compliance committees or senior management for review

- Assisting with EWRA reviews and recalibrations.

In the context of internal uses, AI primarily functions as a decision support or a productivity tool, enabling compliance teams to process large datasets, identify patterns, and summarise information more efficiently. However, the outputs must remain subject to human review and professional judgment, as businesses regulated under UAE’s AML regime remain responsible for the accuracy and completeness of compliance requirements.

Businesses must ensure that internal AI outputs are validated before influencing compliance decisions such as risk ratings, investigation outcomes, or escalation to the Compliance Officer.

External uses of AI in AML compliance may include:

External use refers to situations where AI outputs contribute towards documents, records, or communications that may be reviewed or inspected by regulators, supervisory authorities, or law enforcement agencies. Examples of AI assistance are as follows:

- Suspicious Transaction Reports (STRs) or Suspicious Activity Reports (SARs) narratives and details to be submitted to the UAE FIU through the goAML portal

- Documentation supporting SAR/STR and CNMR/PNMR decision-making

- Responses to supervisory authorities’ queries or information requests

- Documentation supporting account freezing or reporting decisions for TFS compliance

- Internal escalation and investigation reports that may be later disclosed to relevant authorities during inspection.

Under UAE AML legislation, businesses are required to file these reports without delay to FIU. Because these reports may trigger investigations, freezing orders, or other enforcement actions, any AI involvement in their preparation must undergo scrutiny by an AML Compliance Officer or MLRO, as most of these responsibilities come under their accountability under AML law and any inaccuracy could undermine investigations and expose the business to regulatory risk.

Why does the distinction matter?

Defining the context of AI use facilitates businesses to align AI governance with the UAE AML/CFT framework is necessary as AML laws in UAE require regulated businesses to:

- Identify and assess risks associated with products, services, geography, customers, and technologies.

- Implement and establish internal policies, procedures and control measures approved by the senior management and overseen by AML compliance officer.

- Ensure that controls are proportionate to the ML/TF and PF risks the business faces.

By distinguishing between internal analytical uses and externally relied upon outputs, businesses can ensure that governance controls are calibrated according to risk proportion. This helps ensure that internal analytical assistance is separated from outputs that could influence regulatory obligations or supervisory involvement, substantiating responsible AI Adoption in AML compliance by businesses.

Step 2: Assessing the Regulatory and Operational Impact of Errors

Once the intended use of the AI system has been established, businesses need to evaluate the consequences of potential errors. Questions that businesses should consider include:

- Could inaccurate outputs by AI-assisted or AI-generated compliance processes affect regulatory reporting?

- Could the use of an AI system influence customer risk classification/ratings?

- Could errors create legal, financial, or reputational consequences, such as fines, penalties, a ban, or license revocation?

Where the potential consequences due to AI system use, or errors, are materially significant, businesses should apply stronger oversight mechanisms and validation procedures to make sure their operations are embedded with responsible AI Adoption in AML compliance.

Step 3: Categorising AI Applications by Risk Levels

Following the risk assessment of the regulatory and operational impact of errors, AI applications or tools used by businesses need to be further categorised according to their potential impact on AML compliance outcomes.

- Low-Risk AI Applications: These involve routine operational activity with minimal regulatory implications. Examples include administrative summarisation tasks or internal documentation support. The oversight model that can be relied upon to mitigate risk is a human-in-the-loop supervision, where compliance teams monitor AI outputs and intervene if and when necessary.

- Medium-Risk AI Applications: These involve AI systems whose use may influence investigative workflows or compliance analysis, but do not directly determine regulatory outcomes. Examples include transaction monitoring analysis or document summarisation at the time of due diligence reviews. The oversight model that can be relied upon to mitigate risk is human-in-the-Loop (HITL) validation prior to decision-making, to ensure that AI outputs are reviewed before influencing compliance actions.

- High-Risk AI Applications: These involve AI use cases that directly contribute to regulatory reporting or compliance decisions with legal implications. Examples include SAR, STR, CNMR, PNMR, and similar regulatory reporting activities, as well as communications with regulatory or supervisory authorities. The oversight model that can be relied upon to mitigate risk is human-in-the-loop (HITL) review and approval, which needs to be mandatory, while human-in-command (HIC) governance helps ensure that AI systems used in such sensitive processes operate within the business’s risk appetite.

Step 4: Applying Proportionate Guardrails and Human Oversight

After categorising AI systems by risk levels, businesses need to implement controls that are strictly proportional to the risk materiality of the AI system’s use case. Because KYC and AML reporting processes pose a high risk, they may require rigorous, extensive enforcement of guardrails. Chief among these is HITL, with mandates that human experts review and validate the extracted data and retain ultimate responsibility for the final compliance decision.

The guardrails involving human oversight and their categories are discussed. More at length in further paragraphs, enabling businesses to understand responsible AI Adoption in AML compliance.

Aligning Human Oversight Models with UAE AML Regulatory Expectations

When AI is used within AML programs, the responsibilities of Senior Management and the AML Compliance Officer (or MLRO) could ideally align closely with locally as well as internationally recognised and layered human oversight models, which guide a responsible AI Adoption in AML compliance.

- Under Cabinet Decision No. 134 of 2025 on Combating Money Laundering and Terrorism Financing, businesses must implement governance structures that ensure accountability for AML/CFT compliance.

- Furthermore, the Central Bank of UAE (CBUAE) issued Guidance Note on the Consumer Protection and Responsible Adoption and Use of Artificial Intelligence and Machine Learning by Licensed Financial Institutions in the U.A.E., which outlines the guidance for responsible adoption and use of AI and ML and harps upon documenting and adopting a governance framework for AI use. This guidance is issued in alignment with CBUAE Guidelines for Financial Institutions adopting Enabling Technologies.

- The guidance recommends that businesses maintain an inventory of AI models, systems, and technologies in alignment with CBUAE’s Model Management Standards and Model Management Guidance (2022).

- International guidance, such as FATF Recommendation 15 on new technologies, emphasises that businesses must identify and assess risks emanating from technological innovations before implementing them into AML frameworks.

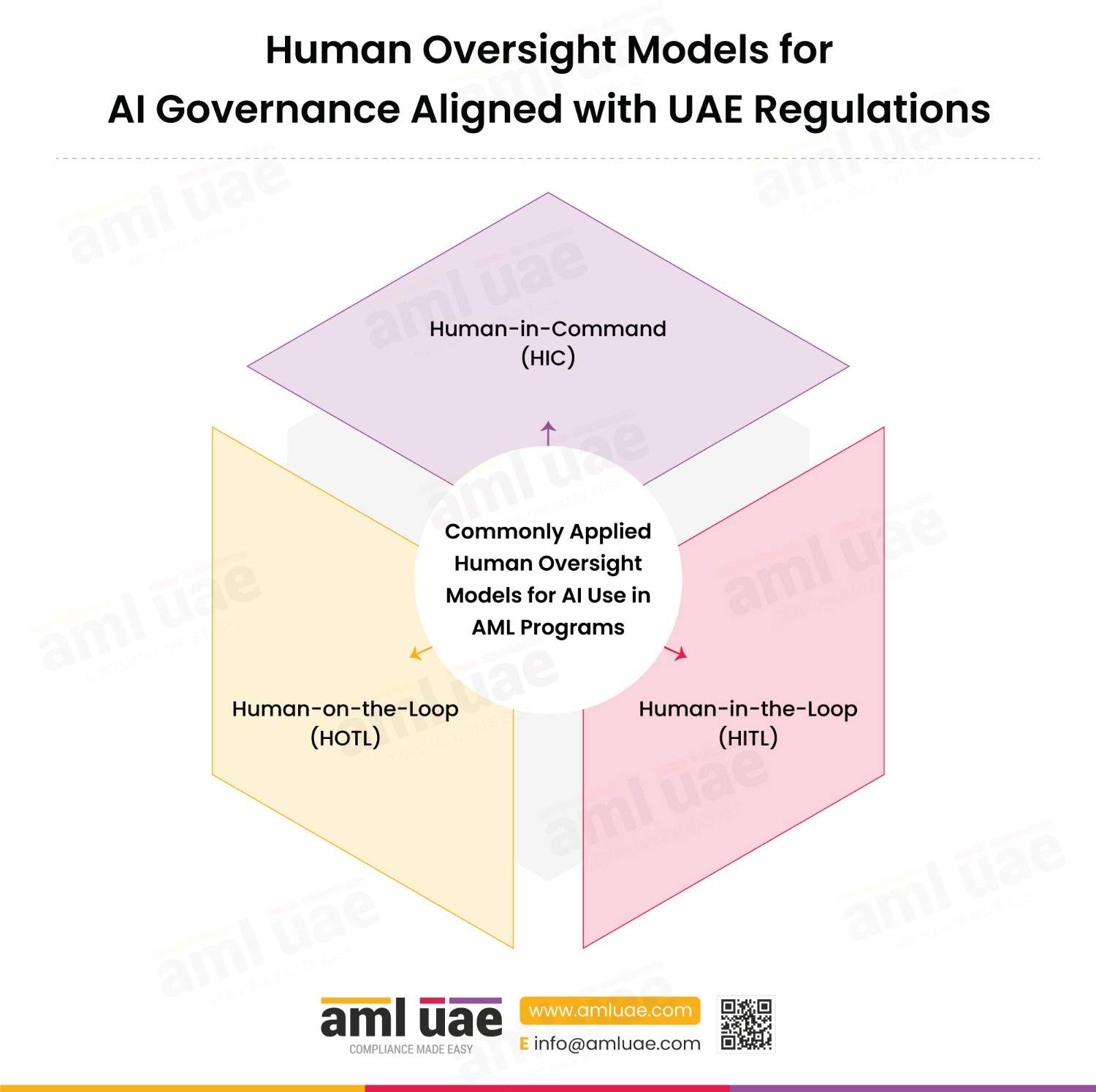

Three human oversight models that are commonly applied to ensure responsible AI Adoption in AML compliance are:

- Human-in-Command (HIC)

- Human-in-the-Loop (HITL)

- Human-on-the-Loop (HOTL)

These models help businesses implement risk-based AI governance for AML compliance while maintaining accountability under UAE law.

Human-in-Command (HIC)

Human-in-Command refers to the highest level of oversight in AI governance. Under this model, humans retain ultimate strategic authority over the establishment, governance, and risk appetite for the use of AI systems.

UAE Governance Alignment: In accordance with legal requirements, Senior Management functions as the Human-in-Command layer for the overall AML/CFT governance framework. Their responsibilities for the HIC layer include:

- Approving and finalising AML/CFT policies, internal controls, and procedures

- Defining the business’s ML/TF/PF risk appetite

- Approving technology and monitoring systems used in AML programs

- Reviewing AML compliance reports submitted by the AML Compliance Officer

- Directing enhancements to AML systems and controls where deficiencies are identified.

In the context of AI governance, Senior Management ensures that AI systems used in AML compliance operate within the business’s approved risk management framework, which helps ensure responsible AI Adoption in AML compliance.

Human-in-the-Loop (HITL)

Human-in-the-Loop oversight refers to direct human review and approval before a medium- or high-risk decision is finalised. This model is essential where AI outputs directly influence regulatory reporting or compliance decisions.

UAE Governance Alignment: In accordance with legal obligations, both Senior Management and the Compliance Officer act as HITL control points for critical compliance decisions.

– Senior Management HITL responsibilities: Include approval of certain high-risk business decisions, including:

- Continuing or establishing business relationships with Politically Exposed Persons (PEPs)

- Approving correspondent banking relationships

- Authorising specific high-risk financial transactions and business relationships.

These approvals require mandatory human review before high-risk actions are taken.

– Compliance Officer HITL responsibilities: The AML CO or MLRO acts as the primary HITL for suspicious activity or transaction detection and reporting. Their responsibilities include:

- Reviewing alerts generated by monitoring systems

- Analysing customer records, transaction patterns, and reports or files created

- Making a final decision on whether to file SAR/STR or CNMR/PNMR with the FIU when internal reports are escalated to them.

Even when AI or automated systems detect anomalies, the AML CO or MLRO must independently review and validate their findings before initiating regulatory reporting to ensure responsible AI Adoption in AML compliance.

Human-on-the-Loop (HOTL)

Human-on-the-Loop oversight refers to continuous monitoring of systems rather than reviewing every individual output. The human supervisor oversees system performance and intervenes when anomalies or risks arise.

UAE Governance Alignment: In alignment with UAE laws, the AML Co or MLRO performs the HOTL role for ongoing AML operations, including:

- Overseeing transaction monitoring systems

- Reviewing alerts generated by automated or AI-assisted monitoring tools

- Assessing whether internal processes are aligned with the prevailing regulations

- Identifying emerging financial crime risks and system weaknesses

- Recommending improvements to AML controls and systems.

Through this function, the AML CO or MLRO ensures responsible AI Adoption in AML compliance and makes sure that including AI tools remains effective, compliant, and responsive to emerging ML/TF risks.

Accordingly, regulated Businesses in UAE must demonstrate the following measures to substantiate that there exists a responsible AI Adoption in AML compliance:

- Documented AI Governance Frameworks: Internal policies, controls, and procedures must be expressly approved by Senior Management.

- Clear accountability for AI-assisted decisions: Ensuring the Compliance Officer maintains independent decision-making authority for reviewing and analysing suspicious transactions or activities, serving as the required human-in-the-loop.

- Proactive Risk Assessments: Documenting risk assessments conducted prior to the launch or use of any new AI technologies, products, or processes.

- Transparent Validation and Ongoing Monitoring: Deploying an independent audit function to test the effectiveness and adequacy of the AI-assisted internal policies and controls.

However, businesses remain exposed to risks when relying on AI for their compliance programs, a fact that warrants adequate consideration.

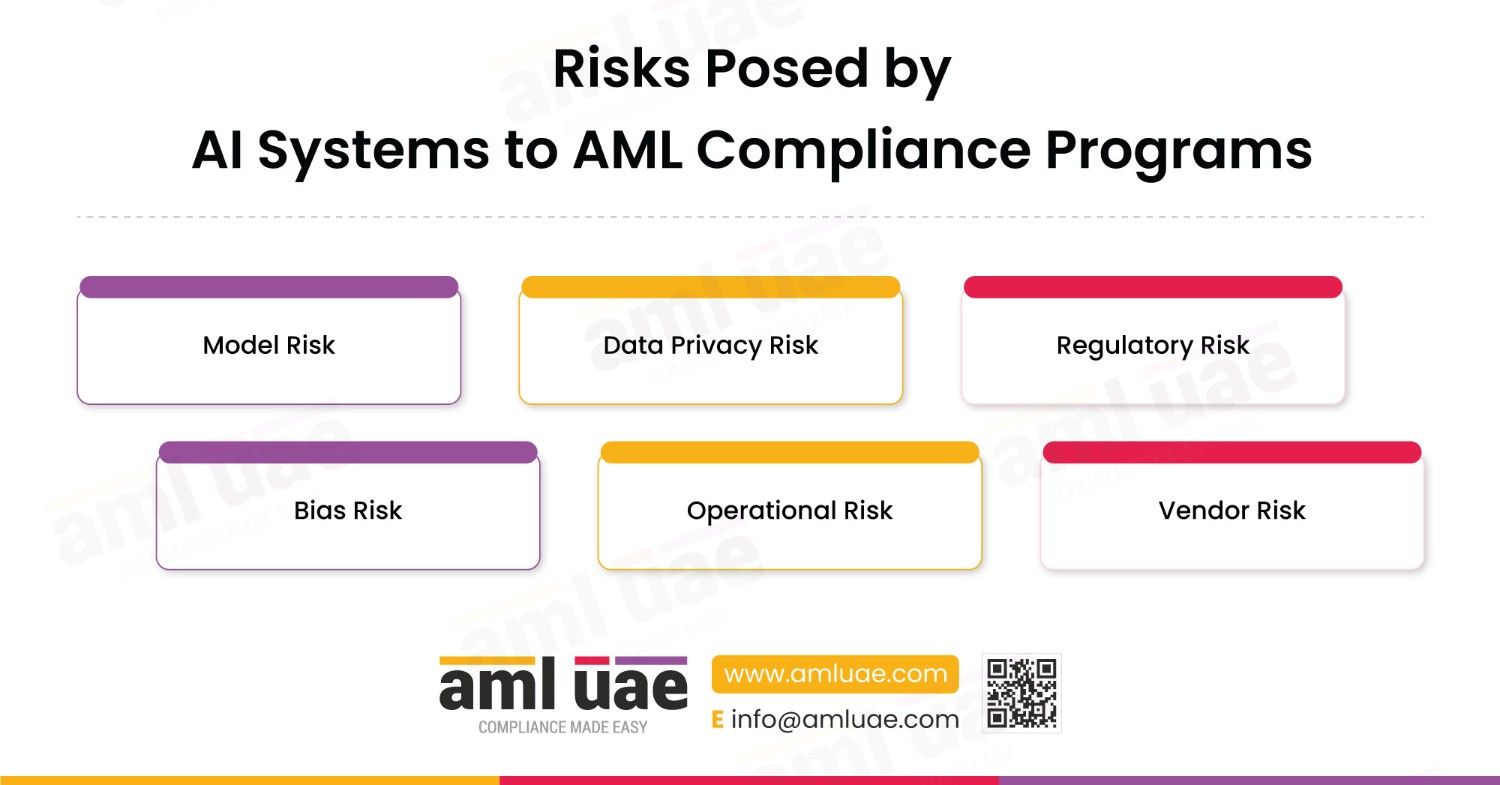

AI Risks in AML Compliance Programs

The introduction of AI into AML processes introduces a number of distinct risk categories that regulated businesses must manage. These risks include: Model Risk, Data Privacy Risk, Regulatory Risk, Bias Risk, Operational Risk, and Vendor Risk.

- Model Risk: Arises where AI systems produce inaccurate alerts or flawed findings, such as customer risk ratings, due to training data limitations or model design issues.

- Data Privacy Risk: Arises when sensitive customer information is processed through AI systems without explicit consent, unclear purpose limitations, and appropriate safeguards.

- Regulatory Risk: Emerges if AI-generated outputs contribute to inaccurate regulatory reporting and incorrect or inadequate regulatory submissions and correspondence.

- Bias Risk: Presents itself when training data leads to unfair or inaccurate customer risk ratings or risk allocation.

- Operational Risk: Develops when compliance teams become overly reliant on automated outputs and fail to implement risk-based HITL, HOTL, or HIC oversight.

- Vendor Risk: Arises where businesses depend on third-party AI systems which lack transparency, governance controls or adequate safeguards.

These risks reinforce the importance of structured governance of AI-reliant compliance frameworks to ensure responsible AI Adoption in AML compliance.

Unsure How to Assess AI Risks in AML Compliance?

We assist with the AML Health Check support

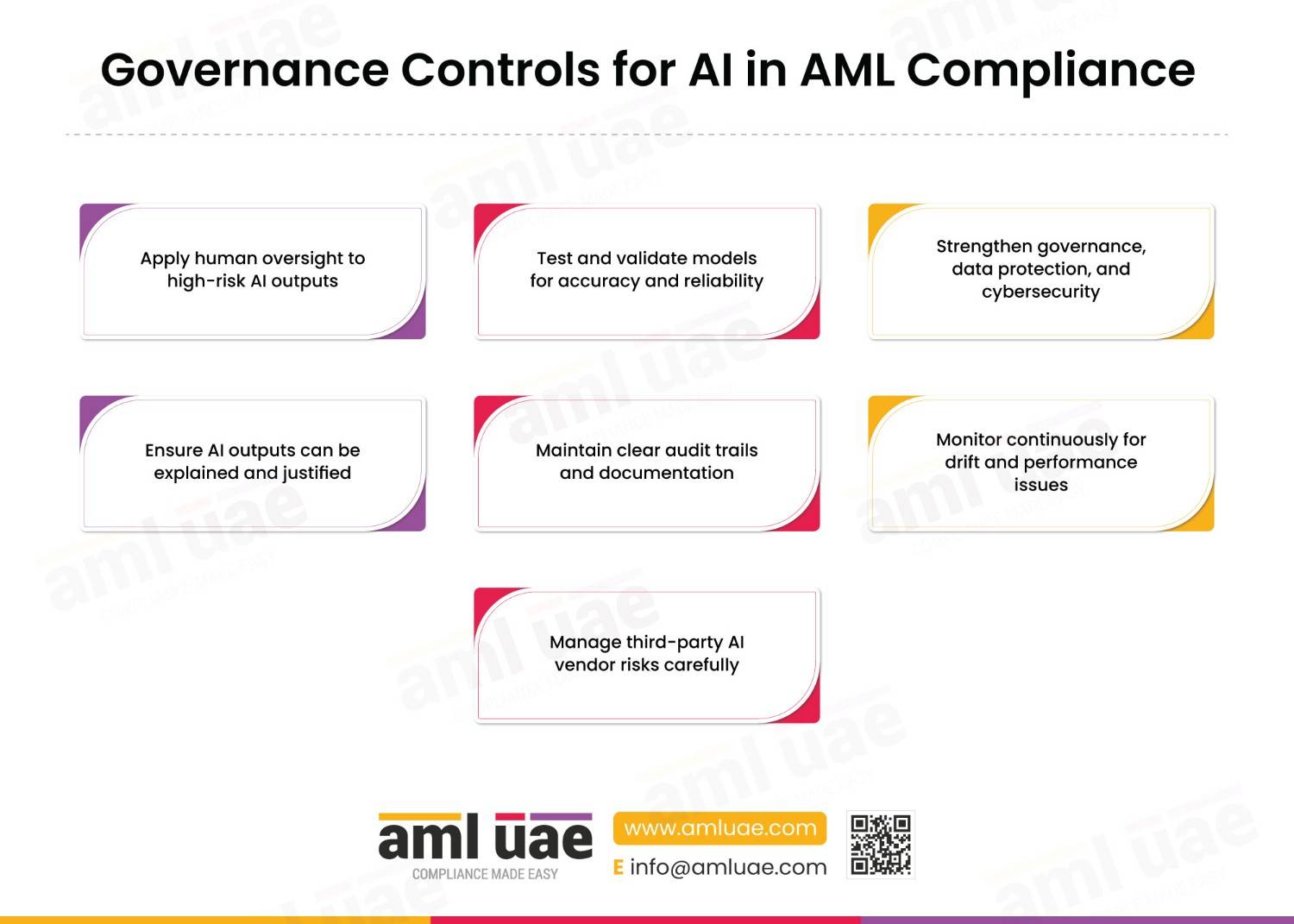

Governance Controls for AI in AML Compliance

Effective governance for AI systems used for AML compliance requires both technical safeguards and operational oversight. Key governance measures to ensure responsible AI Adoption in AML compliance usually include:

- Establishing robust human oversight mechanisms for high-risk outputs, such as HIC or HITL

- Conducting AI model testing and validation to ensure accuracy and reliability

- Establishing strong governance frameworks aligned with UAE AML laws to protect sensitive information, as well as ensure cybersecurity, and ensure data integrity

- Relying on explainability tools or taking measures to allow AI outputs to be interpreted and justified in the event of regulatory inspections

- Creating detailed audit trails and documentation to support regulatory review and ensure compliance with record-keeping requirements

- Conducting continuous monitoring to identify model drift or performance degradation and take remedial measures to bridge the gap between expected outcomes and achieved outcomes.

- Ensuring comprehensive vendor risk management when engaging with third-party AI providers.

These controls help ensure that AI systems remain aligned with both regulatory expectations and institutional risk management standards.

AI Guardrails Businesses Can Implement Across the AML Lifecycle

Guardrails are safety measures that businesses can implement across various use cases of AI in AML compliance. Some of the AML obligations, example use cases, corresponding risks and recommended guardrails are tabulated hereunder:

| AML Obligations | Example of AI Use Case | Key Risks When Relying on AI Tools | Recommended Guardrails to Mitigate Risks of AI in AML Compliance |

| Customer Onboarding / KYC | CDD Document extraction and UBO identification in complex ownership structures | Data Privacy risks | Human review and secure AI systems |

| Sanctions Screening | Alert analysis and disambiguation | False Positives or Negatives | Analyst validation |

| Risk Profiling | Customer risk scoring and profiling | Model bias | Model validation and explainability |

| Transaction Monitoring | Pattern detection through behaviour and transaction analysis | Model drift | Continuous monitoring |

| AML Investigations | Case summarization and reporting | Hallucinated or inaccurate outputs | Fact-checking |

| Enhanced Due Diligence | Sources of Funds and Sources of Wealth analysis | Inaccurate analysis | Cross-checking information |

| Regulatory Reporting | Draft narratives and preliminary internal reports | Regulatory inaccuracies or misalignment | Human approval |

| Ongoing Monitoring | Trend analysis in terms of behaviour and transactions | Model degradation and redundancies | Periodic recalibration of ongoing monitoring model |

Implementing governance safeguards directly into AML processes ensures that AI adoption remains consistent with the broader risk-based framework used in financial crime compliance and ensures responsible AI Adoption in AML compliance.

Best Practices for Responsible AI Adoption in UAE AML Compliance

Businesses implementing AI within AML programs should adopt several practical measures to ensure responsible use that complies with Federal Decree Law and Cabinet Resolutions pertaining to AML compliance. These best practices include: Establishing Internal AI Governance Policies, Documenting AI Use Cases and Associated Risk Assessments, Maintaining Human Accountability for Compliance Outcomes, Conducting Ongoing Model Validation and Performance Monitoring, and Training Compliance Teams on AI Limitations and Risks.

- Establishing Internal AI Governance Policies: Creating and regularly updating risk-based procedures and controls to mitigate ML/TF and PF risks and ensuring that such procedures and protocols are formally approved by Senior Management and that due process for such approval is followed and documentation maintained.

- Documenting AI Use Cases and Associated Risk Assessments: Identifying and assessing specific ML, TF, and PF risks that arise from using new AI technologies before they are implemented takes businesses a step closer to responsible AI Adoption in AML compliance.

- Maintaining Human Accountability for Compliance Outcomes: Making sure that AML CO or MLRO at the management level actively monitors internal reports on filing CNMR/PNMR, implementing freezing measures, suspicious activities and transactions and takes the final decision on regulatory reporting to the FIU through goAML portal helps businesses ensure responsible AI Adoption in AML compliance.

- Conducting Ongoing Model Validation and Performance Monitoring: Conducting and relying on independent controls and systems audit to ensure that AI systems remain consistent with the provisions of the Decree-Law and Cabinet Decision No. 134 of 2025, ensuring responsible AI Adoption in AML compliance.

- Training Compliance Teams on AI Limitations and Risks: Developing, implementing, and documenting ongoing training programs and capacity building to ensure that the AML CO/MLRO and compliance team understand technology and related crime-prevention methods and contribute towards achieving responsible AI Adoption in AML compliance.

Together, these best practices support responsible technological innovation while maintaining the compliance integrity demanded by UAE’s financial ecosystem.

How AML UAE Helps with Responsible AI Adoption in AML Programs

At AML UAE, our AML Consultants assist Regulated Entities in responsibly integrating AI into their AML Compliance Program. Our advisory services include risk assessments, AML compliance department setup, AML software testing and validation, and integrating AI controls into existing AML policies and procedures.

This ensures that AI technologies enhance compliance effectiveness while remaining aligned with regulatory obligations, risk-based AML fundamentals, and help ensure responsible AI Adoption in AML compliance.

Final Thoughts: Balancing AI Innovation and AML Compliance

AI presents significant opportunities to strengthen AML compliance programs. However, its responsible adoption in AML compliance must be substantiated by clear governance, structured risk assessments, and strong human oversight.

By relying on a risk-based approach to AI integration, businesses can enhance financial crime detection capabilities while maintaining regulatory compliance and operational resilience within their AML compliance program.

Build a Robust AML Compliance Program

We provide customised AML/CFT Policies and Procedures that are compliant with UAE Laws

Frequently Asked Questions on AI in AML Compliance

Can artificial intelligence replace AML compliance professionals?

No, AI cannot replace AML compliance professionals. AI simplifies and makes the responsibilities of compliance professionals easy by helping them analyse large datasets, identify suspicious transactions or patterns, draft narratives and reports for escalations. In fact, regulatory expectations require human professionals to remain accountable for compliance decisions, regulatory reporting, and communication.

What are the main risks of using AI in AML compliance programs?

– Main risks of using AI in AML compliance programs are:

- Model errors

- Bias in risk scoring

- Data privacy concerns

- Over-reliance on automated outputs

Therefore, businesses must take adequate measures to ensure responsible AI Adoption in AML compliance.

What role does human oversight play in AI-enabled AML programs?

Human oversight ensures that AI outputs are reviewed, validated, and accurately interpreted before influencing compliance decisions, such as regulatory reporting and filings. High-risk compliance tasks, such as SAR/STR filings, require human-in-the-loop review and approval.

Can AML consultants help financial institutions implement AI responsibly?

Yes, AML Consultants can assist businesses in conducting AI risk assessments, designing governance frameworks, validating models and helping businesses with responsible AI Adoption in AML compliance.

Share via :

About the Author

Pathik Shah

FCA, CAMS, CISA, CS, DISA (ICAI), FAFP (ICAI)

Pathik is an ACAMS-certified AML consultant specialising in governance, risk, and compliance for regulated entities in the UAE. He brings over 28 years of experience, with 1,000+ hours of AML training and 200+ advisory engagements across DNFBPs, VASPs, and FIs. He supports businesses in aligning with AML/CFT requirements from the CBUAE, DFSA, MoET, MoJ, VARA, CMA, FSRA, and FATF. Known for translating complex regulations into audit-ready procedures, Pathik enables operational clarity and compliance readiness.

Reach Out to Pathik