AML compliance challenges associated with inadequate record-keeping

AML compliance challenges associated with inadequate record-keeping

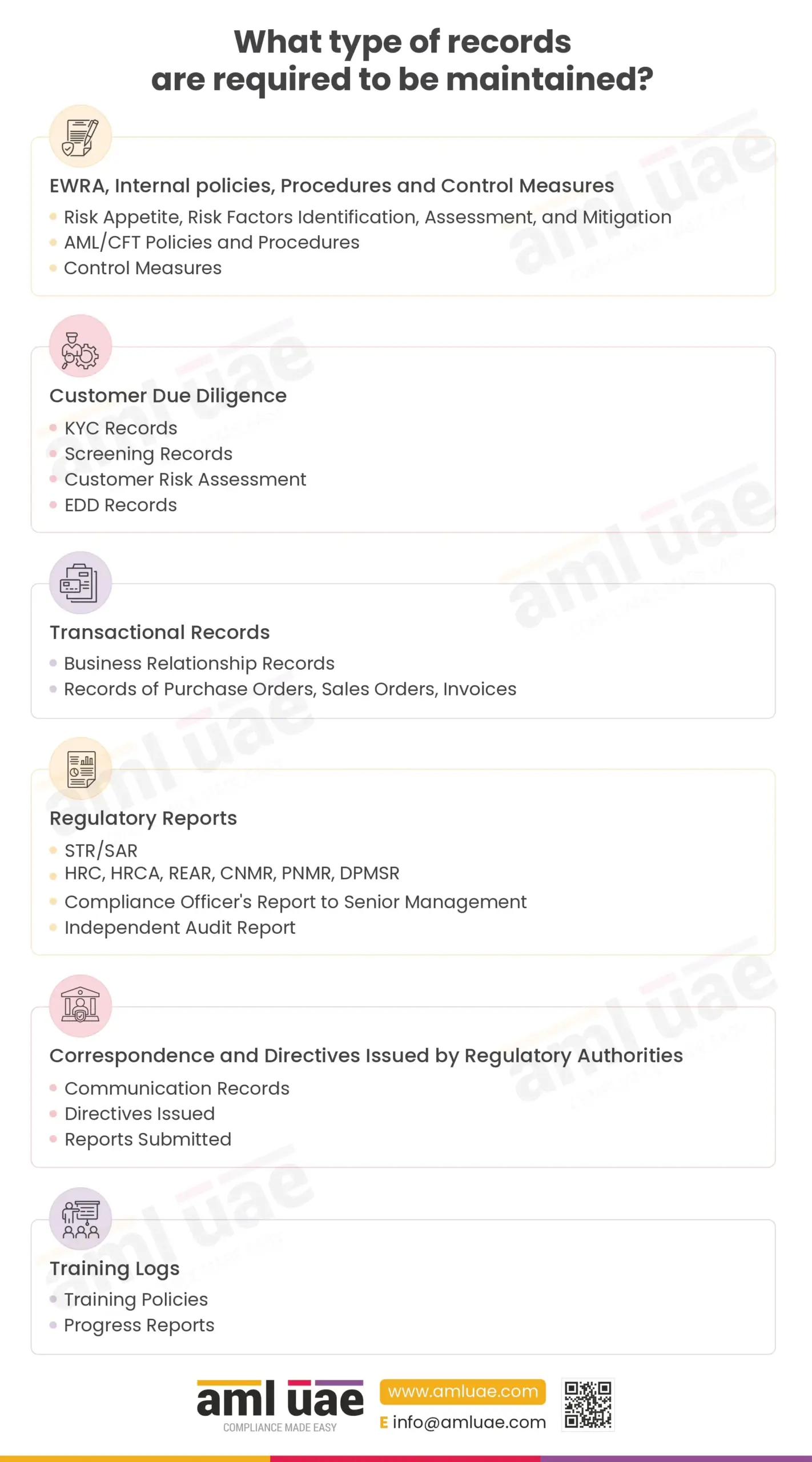

Designated Non-Financial Businesses and Professions (DNFBPs), Virtual Asset Service Providers (VASPs), and Financial Institutions (Fis) operating in UAE are required to comply with the regulations governing Anti-Money Laundering and Combating the Financing of Terrorism (AML/CFT). As per the AML/CFT regulatory framework in the UAE, regulated entities must keep a proper record of AML compliance measures.

However, if the regulated entities fail to maintain adequate AML records, they face various challenges. Inadequate AML record-keeping results in having no evidence of complying with the legal requirements. Further, the lack of data results in the inability to conclude Enterprise-Wide Risk Assessment and Customer Risk Assessment. It becomes extremely difficult to identify patterns and define rules to detect suspicious transactions. This affects the efficiency of AML-related measures aimed at detecting and preventing ML/FT activities.

Thus, it is important that regulated entities maintain adequate records to achieve excellence in AML measures.

The following is the list of challenges that regulated entities come across due to inadequate maintenance of AML records:

Compliance Risk

According to the UAE legal landscape, all regulated entities are required to maintain records of the AML-related compliance measures implemented to prevent ML/FT and PF. Inadequate record-keeping or failure to maintain records results in fines and penalties and consequential reputational damage.

Ineffective Risk Assessment

Regulated entities are required to conduct risk assessments. However, if there is no properly maintained data to work from, then the risk assessments that are carried out by the entities will be ineffective. Failure to carry out a proper risk assessment would result in deploying inadequate controls to counter ML/TF and the entity may end up establishing a business relationship with criminals.

Ineffective Monitoring

Regulated entities must engage in ongoing monitoring of transactions and business relationships in order to counter ML/TF. The monitoring procedures and controls are dictated by the data that is gathered and held. However, when record management is not effectively undertaken, then regulated entities have no access to historical data to analyse. Hence, the entire monitoring procedure becomes meaningless.

Increased Financial Risks

As stated above, without effective records, risk assessment and monitoring are ineffective. This leaves the regulated entities exposed to financial crime, including ML/FT and other PF activities.

Inaccurate Audit

Regulated entities are required to undergo an AML/CFT audit. They are required to appoint an independent auditor for this purpose. For the auditor to understand the AML compliance measures adopted by the entity, record-keeping is a must. The auditor would require access to the AML/CFT program, EWRA, KYC, Screening, and Customer Risk Assessment records. He would also need access to transaction monitoring records. Without adequate record-keeping, an independent AML audit cannot be carried out.

Reputational Damage

Failure to maintain records would result in regulatory fines and penalties, spoiling the reputation of the company. In some cases, the regulators have also required businesses to shut down their operations, and hence, record-keeping is a must.

Increased Cost

Regulated entities are required to carry out AML measures continuously in order to adapt to changes. Poor data requires more focus on the measures and calls for deeper investigation, which increases the overall cost. Moreover, the levying of fines and penalties for non-adherence to the regulatory requirement also adds to the cost.