Blogs

Published On: 04/29/2026

Protect your business with reliable and effective AML strategies with AML UAE.

Last Reviewed On: 07/21/2026 | Last Updated On: 07/21/2026

AML Regulations for Lawyers, Notaries, and Other Legal Professionals in UAE: At a Glance

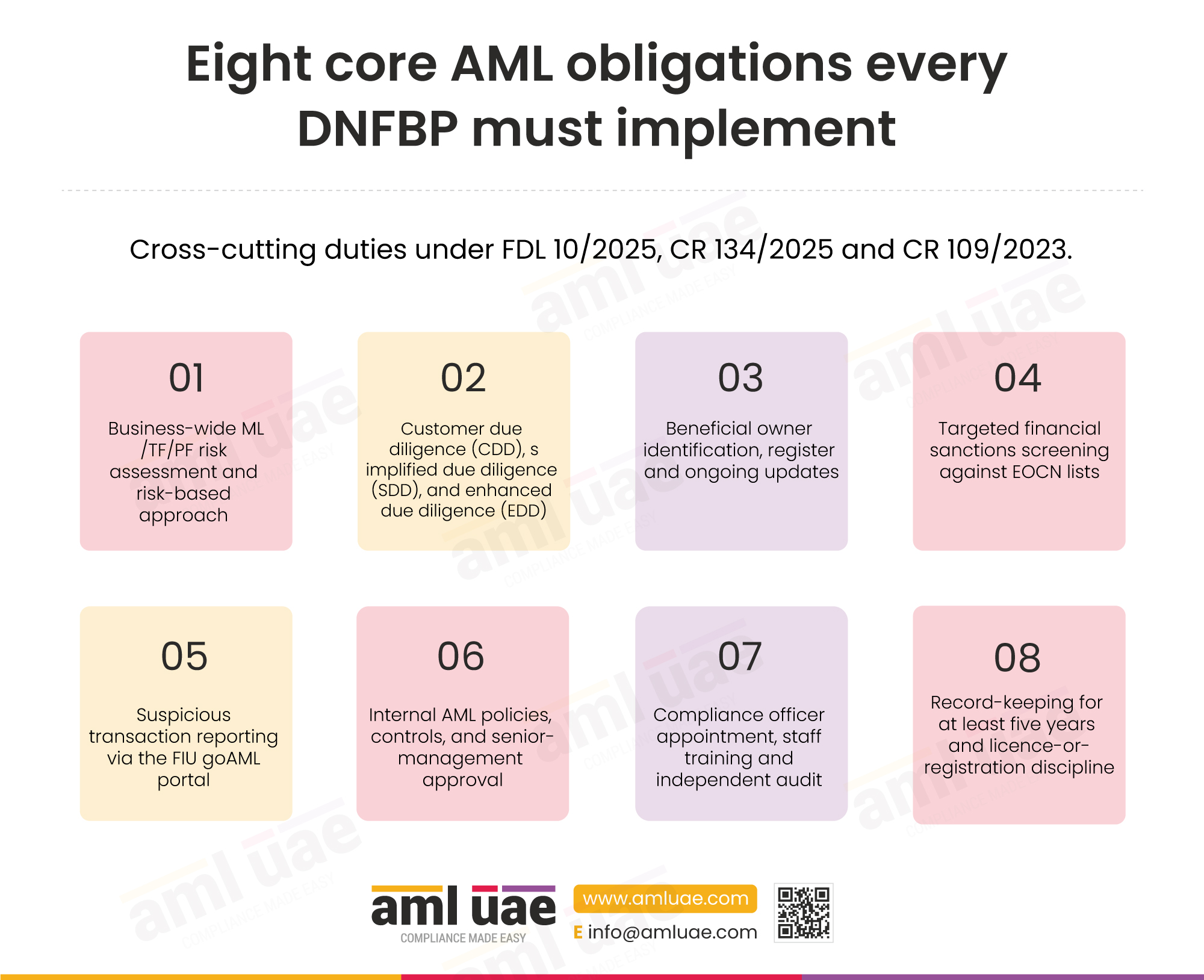

- Covered activities: Five activities under Article 3(4) of Cabinet Resolution 134/2025 bring a lawyer, notary, or legal consultant inside the AML regime.

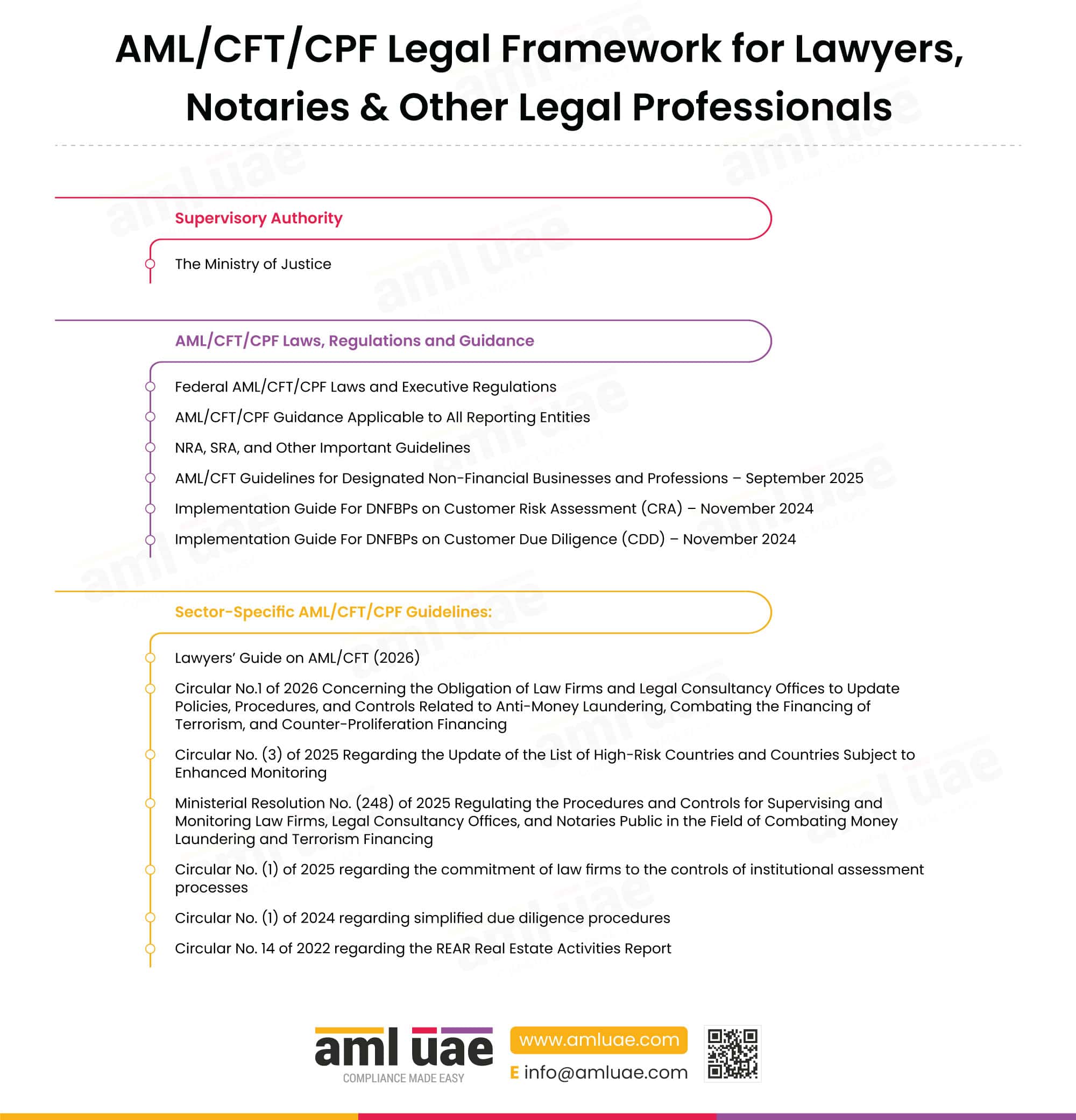

- Supervisory authority: The Ministry of Justice (MoJ) supervises law firms, legal consultancy offices, and notaries public under Ministerial Resolution 248 of 2025.

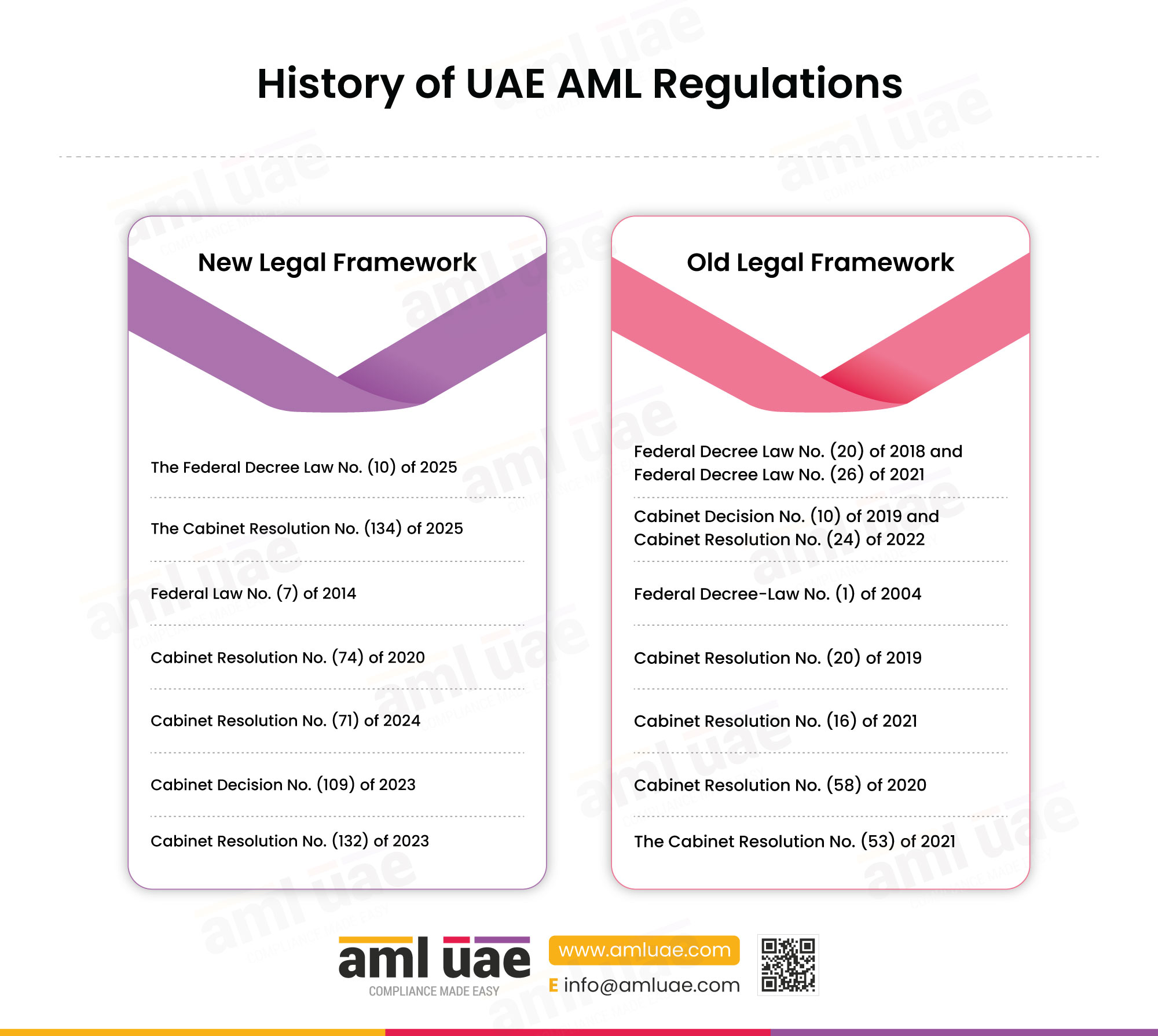

- Primary legislation: Federal Decree-Law 10 of 2025 and Cabinet Resolution 134 of 2025 replace Federal Decree-Law 20 of 2018; all unrepealed circulars remain valid.

- Administrative penalties: Forty-one violation categories under Cabinet Resolution 71 of 2024 carry fines ranging from AED 50,000 to AED 1,000,000, doubled on repetition.

- Legal privilege: Article 18(2) of both Federal Decree Law No. (10) of 2025 and Cabinet Resolution No. (134) of 2025 protects defence, representation, arbitration, mediation, and legal opinion activities from the STR duty.

- Reporting channel: Suspicious transactions go to the Financial Intelligence Unit through the goAML platform.

- Record retention: Five years for customer records and all AML documentation, starting from the end of the business relationship or the completion of the transaction.

- Free-zone carve-out: Firms licensed in ADGM and DIFC sit under ADGM (RA) and DFSA respectively; MoJ supervision does not apply to them.

AML Regulations for Lawyers, Notaries, and Other Legal Professionals in UAE

AML regulations for lawyers in UAE place five defined activities inside the anti-money-laundering perimeter and require lawyers, legal consultants, and notaries public under the supervisory remit of the Ministry of Justice. The current framework is anchored in Federal Decree-Law No. (10) of 2025 Regarding Anti-Money Laundering, and Combating the Financing of Terrorism and Proliferation Financing and its Executive Regulations in Cabinet Resolution No. (134) of 2025, both of which repealed Federal Decree-Law No. (20) of 2018 and its earlier Executive Regulations, while preserving every circular and notification that has not been specifically revoked.

This spoke article sits inside the DNFBPs regulatory cluster on AML UAE and focuses only on legal professionals supervised by the Ministry of Justice. Firms licensed in Abu Dhabi Global Market or the Dubai International Financial Centre sit under the ADGM Registration Authority (RA) and the DFSA, respectively, so this guide addresses their position only in the carve-out note at the end of the supervisor section. Every specific article number, penalty figure, timeline, and threshold below is traceable to a named instrument published on uaelegislation.gov.ae or to a named Ministry of Justice publication on moj.gov.ae. For the federal law in its own right, see the guide to anti-money laundering laws in UAE.

Scope of this page:

This page covers lawyers, notaries, and legal consultants performing the five covered activities under Article 3(4) of Cabinet Resolution 134/2025, supervised by the Ministry of Justice. Accountants, auditors, and trust and company service providers are addressed on their own sibling pages in the DNFBPs cluster. Where cross-sector rules are common to every DNFBP (for example beneficial owner disclosure, targeted financial sanctions, and administrative penalties), this page states what they require of legal professionals specifically and links to the pillar page for the wider framing.

Who Counts as a Lawyer, Notary, or Legal Professional for AML Purposes in UAE?

A lawyer, legal consultant, or notary public is inside the UAE AML regime when they prepare, carry out, or assist a client with any of the five activities listed in Article 3, Clause 4 of Cabinet Resolution 134 of 2025.

The Five Covered Activities Under Article 3(4) of Cabinet Resolution 134 of 2025

The Executive Regulations list the activities that bring an independent legal professional inside the AML perimeter. Each is a transactional or representational act carried out for or on behalf of a client; performing any one of them triggers customer due diligence, record keeping, suspicious transaction reporting, and the wider obligations set out in Federal Decree-Law 10 of 2025.

1. Real estate transactions

Buying or selling real estate, whether the professional acts for the buyer, the seller, or holds client funds in the course of the transaction.

2. Managing client money

Managing customer funds, securities, or other assets held in a professional or fiduciary capacity.

3. Account management

Managing bank accounts, savings accounts, or securities accounts for a client.

4. Company contributions

Organising contributions for establishing, operating, or managing companies.

5. Legal persons and arrangements

Establishing, operating, or managing legal persons or legal arrangements, or performing any trading or buying and selling of commercial entities.

Source: Article 3, Clause 4, Cabinet Resolution No. 134 of 2025. The same five activities appear in the definition of designated non-financial businesses and professions in Article 1 of Federal Decree-Law No. 10 of 2025, read with Article 3, Clause 2 of the Executive Regulations.

Notaries Public

A notary public is a public officer who authenticates signatures, declarations, powers of attorney, contracts, and other legal documents. Notaries working in the private sector, private notaries, and the notarial sections of law firms are brought within the AML, in line with Article 3(4) of Cabinet Resolution 134 of 2025. Ministerial Resolution 248 of 2025 explicitly extends the Ministry of Justice supervisory framework to notaries public alongside law firms and legal consultancy offices.

Work Outside the AML Perimeter

From a professional secrecy perspective, Article 18, Clause 2 of Federal Decree-Law 10 of 2025 and Article 18, Clause 2 of Cabinet Resolution 134 of 2025 both carve out work involving assessing the client’s legal position, defending the client, or representing the client in judicial, administrative, arbitral, or mediation proceedings. Firms must still apply AML controls to the transactional elements of a matter even if the advocacy elements fall within privilege.

AML Supervisory Authority for Lawyers, Notaries, and Other Legal Professionals in UAE

The Ministry of Justice is the supervisory authority for law firms, legal consultancy offices, and notaries public in the Mainland. This was confirmed when Cabinet Resolution No. 134 of 2025 designated the Ministry of Justice as the authority responsible for supervising lawyers and legal firms for AML/CFT purposes. Ministerial Resolution No. (248) of 2025, issued on 29 April 2025, replaces Ministerial Resolutions 532 and 533 of 2019 and sets out the supervisory procedures and controls in their current form.

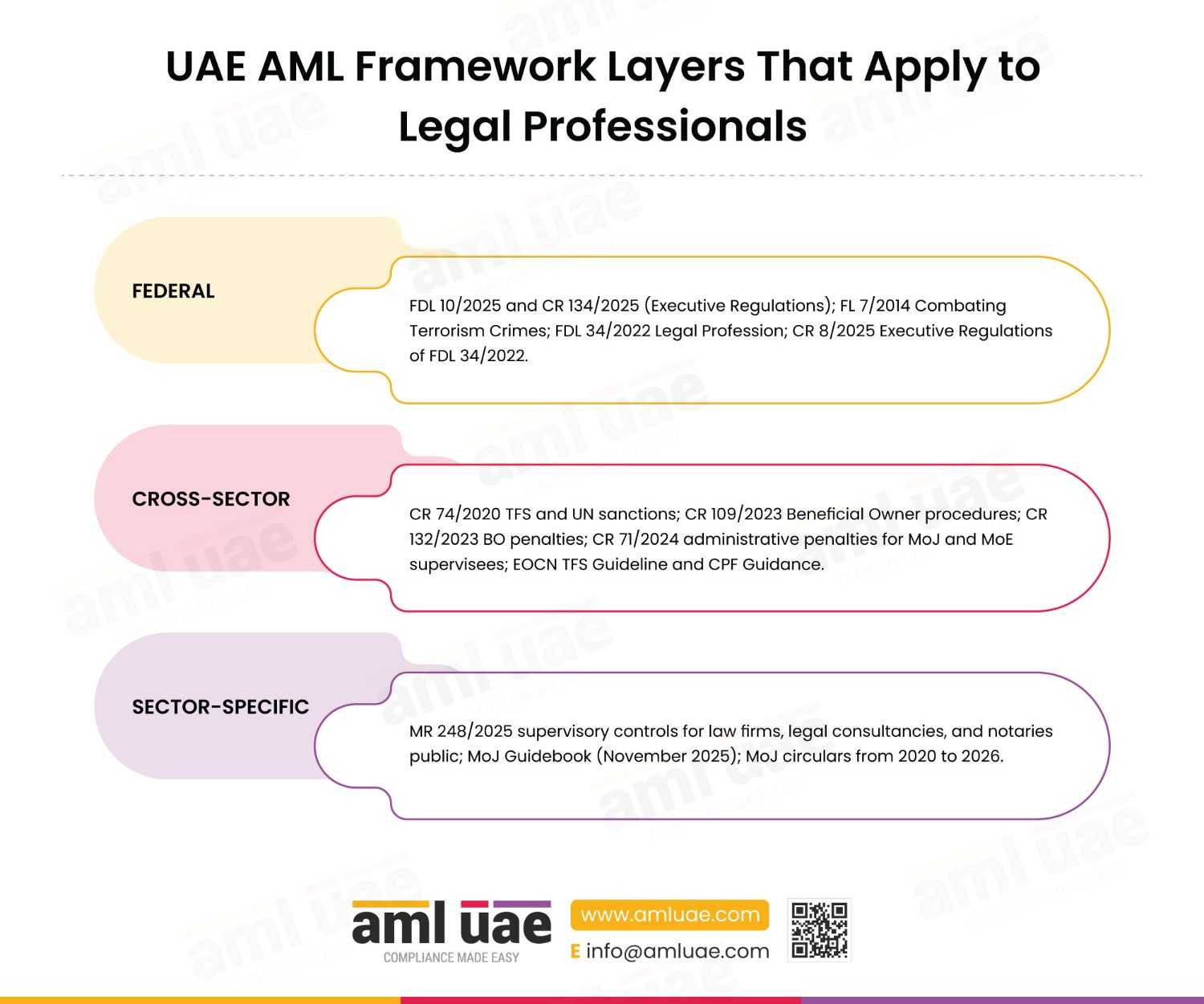

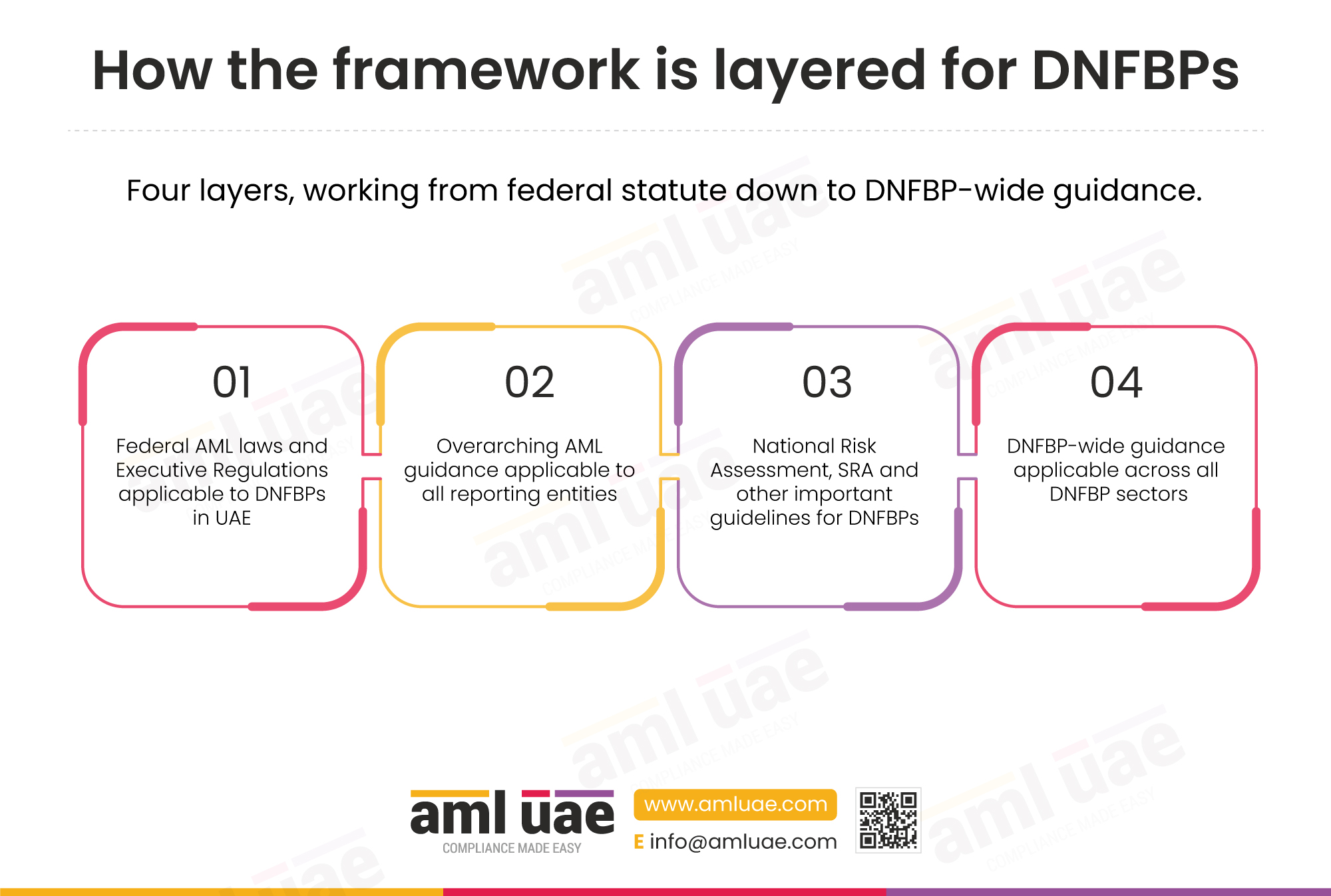

UAE AML Framework Layers That Apply to Legal Professionals

| FEDERAL | FDL 10/2025 and CR 134/2025 (Executive Regulations); FL 7/2014 Combating Terrorism Crimes; FDL 34/2022 Legal Profession; CR 8/2025 Executive Regulations of FDL 34/2022. |

| CROSS-SECTOR | CR 74/2020 TFS and UN sanctions; CR 109/2023 Beneficial Owner procedures; CR 132/2023 BO penalties; CR 71/2024 administrative penalties for MoJ and MoE supervisees; EOCN TFS Guideline and CPF Guidance. |

| SECTOR-SPECIFIC | MR 248/2025 supervisory controls for law firms, legal consultancies, and notaries public; MoJ Guidebook (November 2025); MoJ circulars from 2020 to 2026. |

How the Ministry of Justice supervises the sector

Three operational building blocks explain how MoJ plans, conducts, and concludes supervisory action over legal professionals.

AML/CTF Department

The dedicated AML/CTF Department inside MoJ is the operational face of supervision, assigning inspectors and issuing guidance.

Risk-based inspections

Inspections follow a risk-based methodology that weights firm size, client profile, and the five covered activities.

Administrative sanctions

Breaches are dealt with under Cabinet Resolution 71 of 2024 and Article 6 of Ministerial Resolution 248 of 2025.

The MoJ AML/CTF Department and Its Fifteen Functions

The Guidebook for Law Firms and Legal Consultancy Offices on Combating Money Laundering, Countering the Financing of Terrorism and Countering Proliferation Financing, Second Edition, published by the Ministry of Justice in November, sets out fifteen functions for the Department. These include, among others, supervising law firms, legal consultancy offices, and notaries public for AML/CFT/CPF compliance; carrying out risk-based on-site and off-site inspections; imposing administrative sanctions and escalating suspected criminal conduct to prosecutors; cooperating with the Financial Intelligence Unit, the Executive Office for Control and Non-Proliferation, and other domestic and foreign counterparts; maintaining typologies; issuing sector guidance; and running awareness programmes.

Risk-Based Supervision and Inspection Readiness

Ministerial Resolution 248 of 2025 requires MoJ to adopt a risk-based approach when planning and conducting inspections and when deciding the scope and depth of each visit. Practically, this means firms are rated using factors such as client geographies, types of covered activities, complexity of legal persons being established or managed, cash handling, and past supervisory history.

A firm that is well prepared keeps a complete documentation pack at all times, including its firm-wide risk assessment, client risk assessments, sanctions screening logs, transaction risk assessments, STR-decision logs, training records, and a corrective action register showing how any previous findings have been closed out.

Inspection readiness is a continuous state, not a reaction

MoJ inspectors are entitled to request any AML document, client file, or system log at short notice. Firms that treat inspection readiness as a perpetual discipline, rather than a pre-visit scramble, consistently score better against the Guidebook’s controls.

Administrative Sanctions and Appeals

Article 6 of Ministerial Resolution 248 of 2025 provides that the AML Department may impose any of the administrative penalties set out in Cabinet Resolution 71 of 2024 on a law firm, legal consultancy office, or notary public that breaches the AML rules. The Guidebook identifies seven types of sanctions, which can include warnings, fines, restrictions on activity, suspension of managers or compliance officers, and suspension or cancellation of the licence.

A grievance may be filed with the Minister of Justice within twenty working days from the date of notification under Article 7 of MR 248 of 2025, with the Ministry responding within thirty working days under Article 8, failing which silence amounts to rejection per the general forty-day rule in Cabinet Resolution 71 of 2024.

Financial Free-Zone Carve-Out

Firms licensed in Abu Dhabi Global Market are supervised by the Registration Authority, and firms licensed in the Dubai International Financial Centre are supervised by the Dubai Financial Services Authority under the DIFC regulatory regime. MoJ supervision does not apply to them. A dual-licensed group of companies can adopt a group-wide AML programme while retaining separate records and applying the rulebook of the authority that licenses each leg of the business.

| Dimension | Mainland | ADGM | DIFC |

|---|---|---|---|

| Supervisory authority | Ministry of Justice | Registration Authority (RA) | Dubai Financial Services Authority (DFSA) |

| Licensing authority | Ministry of Justice; Executive Council decisions for notaries | Registration Authority of ADGM | DIFC Authority |

| Core AML rulebook | FDL 10/2025, CR 134/2025, CR 71/2024, MR 248/2025 | FSRA AML Rulebook under ADGM Financial Services and Markets Regulations | DFSA AML Module under the DIFC Regulatory Law |

| Sector guidance | MoJ Guidebook for Law Firms and Legal Consultancy Offices (November 2025) | FSRA-issued AML guidance for DNFBPs in ADGM | DFSA-issued AML guidance for DNFBPs in DIFC |

Preparing for a MoJ inspection?

AML UAE runs pre-inspection readiness reviews against the MoJ Guidebook's ten obligations and Cabinet Resolution 71 of 2024 violations, with a prioritised remediation plan.

AML Regulations Applicable to Lawyers, Notaries, and Other Legal Professionals in UAE

The AML rulebook for legal professionals in the UAE is a stack. At the base sit the federal law and its Executive Regulations, followed by cross-sector resolutions on sanctions, beneficial ownership, and penalties. Sector-specific layers come next: Ministerial Resolution 248 of 2025 for supervision, the MoJ Guidebook for substantive controls, and a sequence of MoJ circulars that operationalise particular obligations. Overarching guidance from the Executive Office for Control and Non-Proliferation, the Financial Intelligence Unit, and the National Anti-Money Laundering and Combating the Financing of Terrorism Committee completes the picture.

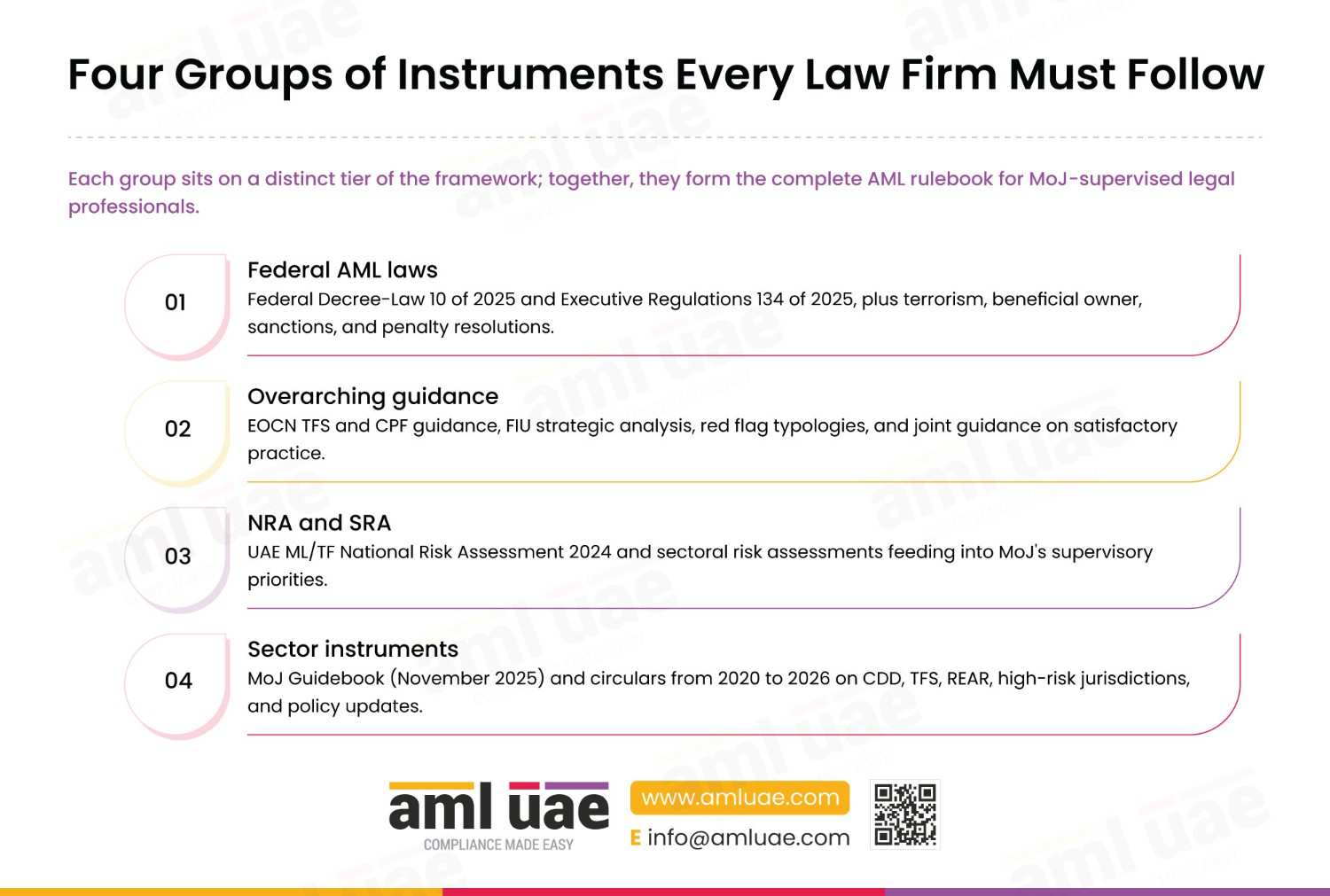

Four groups of instruments every law firm must follow

Each group sits on a distinct tier of the framework; together, they form the complete AML rulebook for MoJ-supervised legal professionals.

1. Federal AML laws

Federal Decree-Law 10 of 2025 and Executive Regulations 134 of 2025, plus terrorism, beneficial owner, sanctions, and penalty resolutions.

2. Overarching guidance

EOCN TFS and CPF guidance, FIU strategic analysis, red flag typologies, and joint guidance on satisfactory practice.

3. NRA and SRA

UAE ML/TF National Risk Assessment 2024 and sectoral risk assessments feeding into MoJ’s supervisory priorities.

4. Sector instruments

MoJ Guidebook (November 2025) and circulars from 2020 to 2026 on CDD, TFS, REAR, high-risk jurisdictions, and policy updates.

Federal AML Laws and Executive Regulations Applicable to Lawyers, Notaries, and Legal Professionals

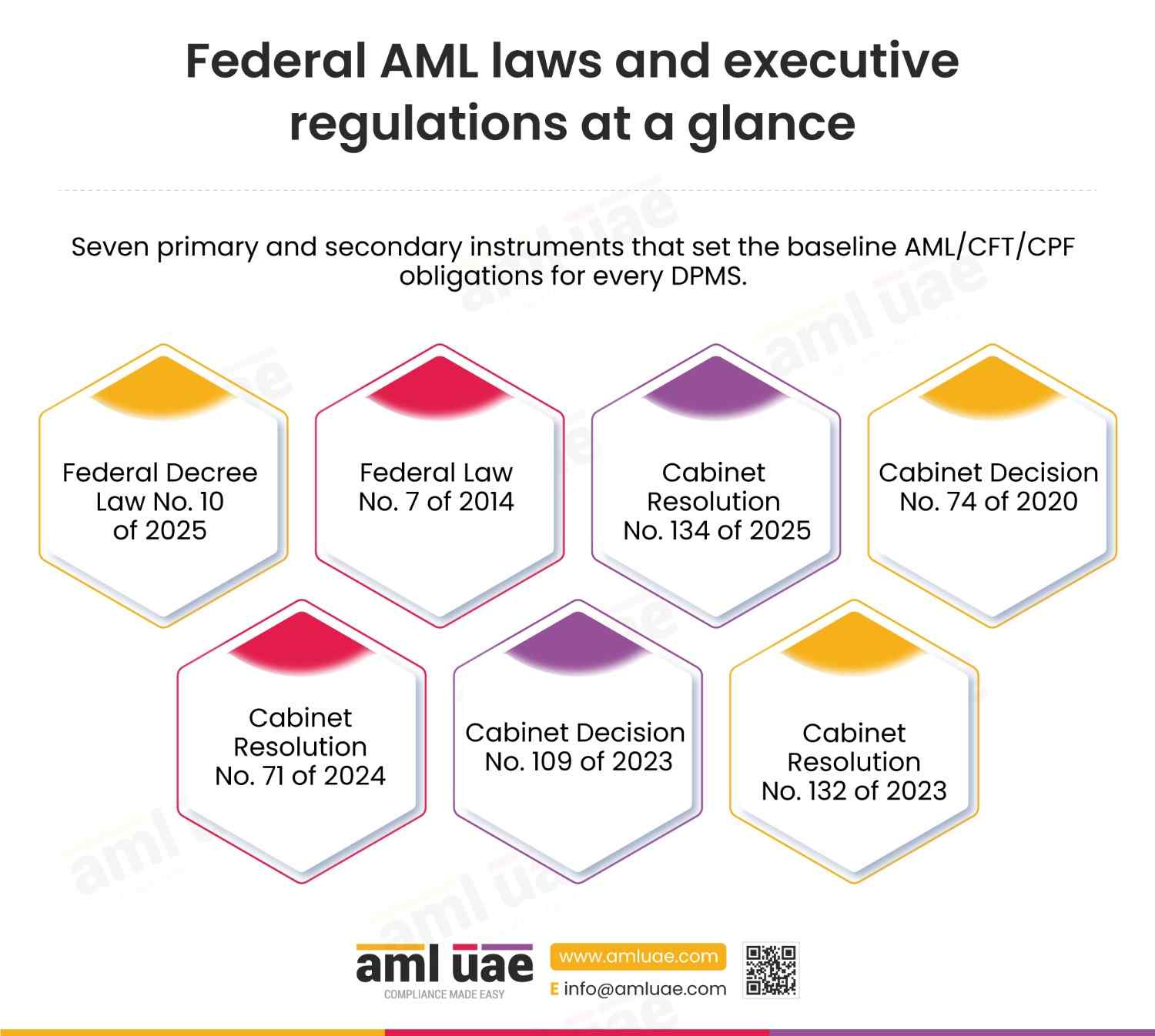

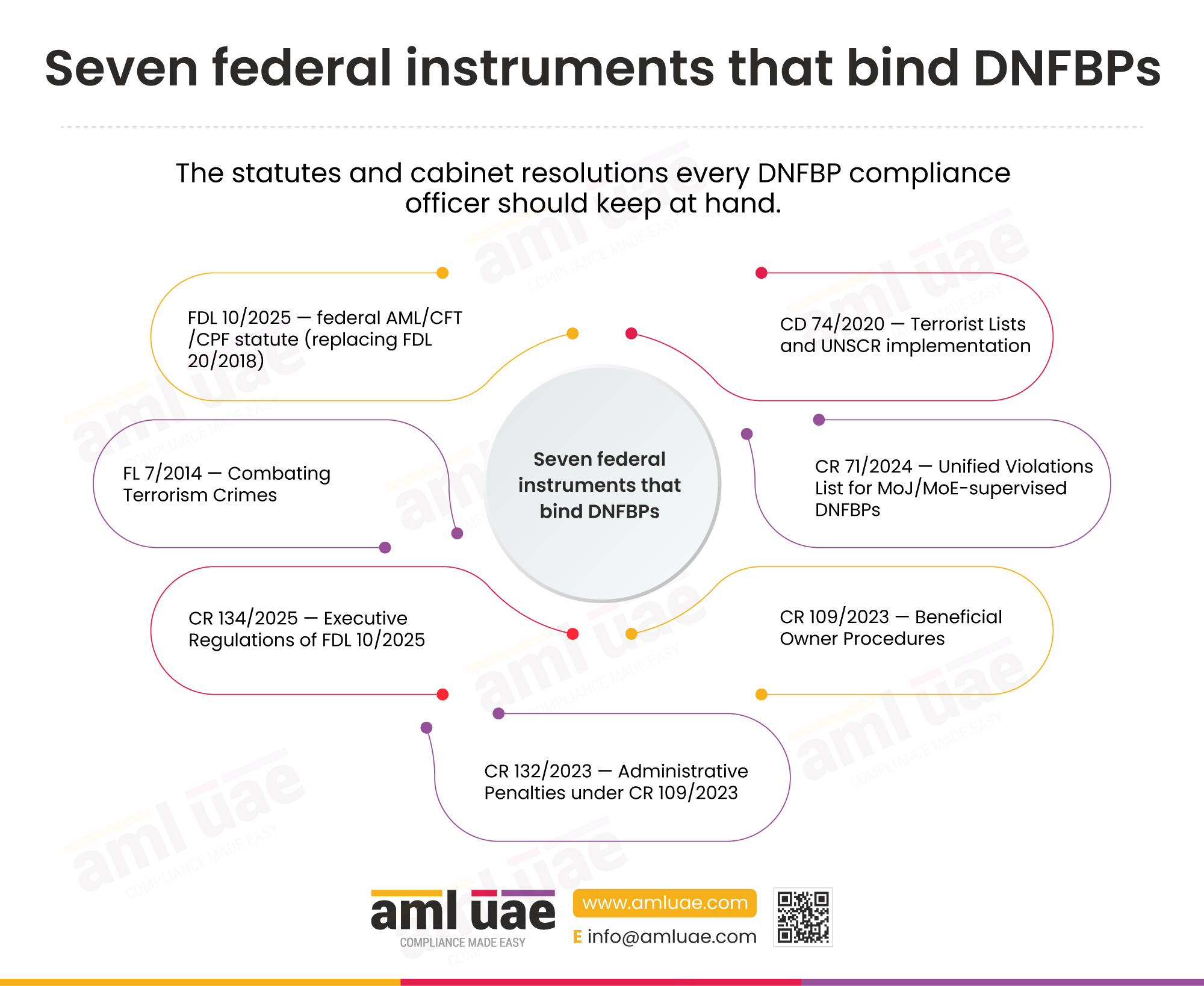

Eleven federal instruments form the statutory base for AML compliance by lawyers, notaries, and legal consultants in UAE. They range from the primary AML decree law and its Executive Regulations through to sector-neutral resolutions on sanctions, beneficial ownership, and penalties, and two instruments specific to the profession itself.

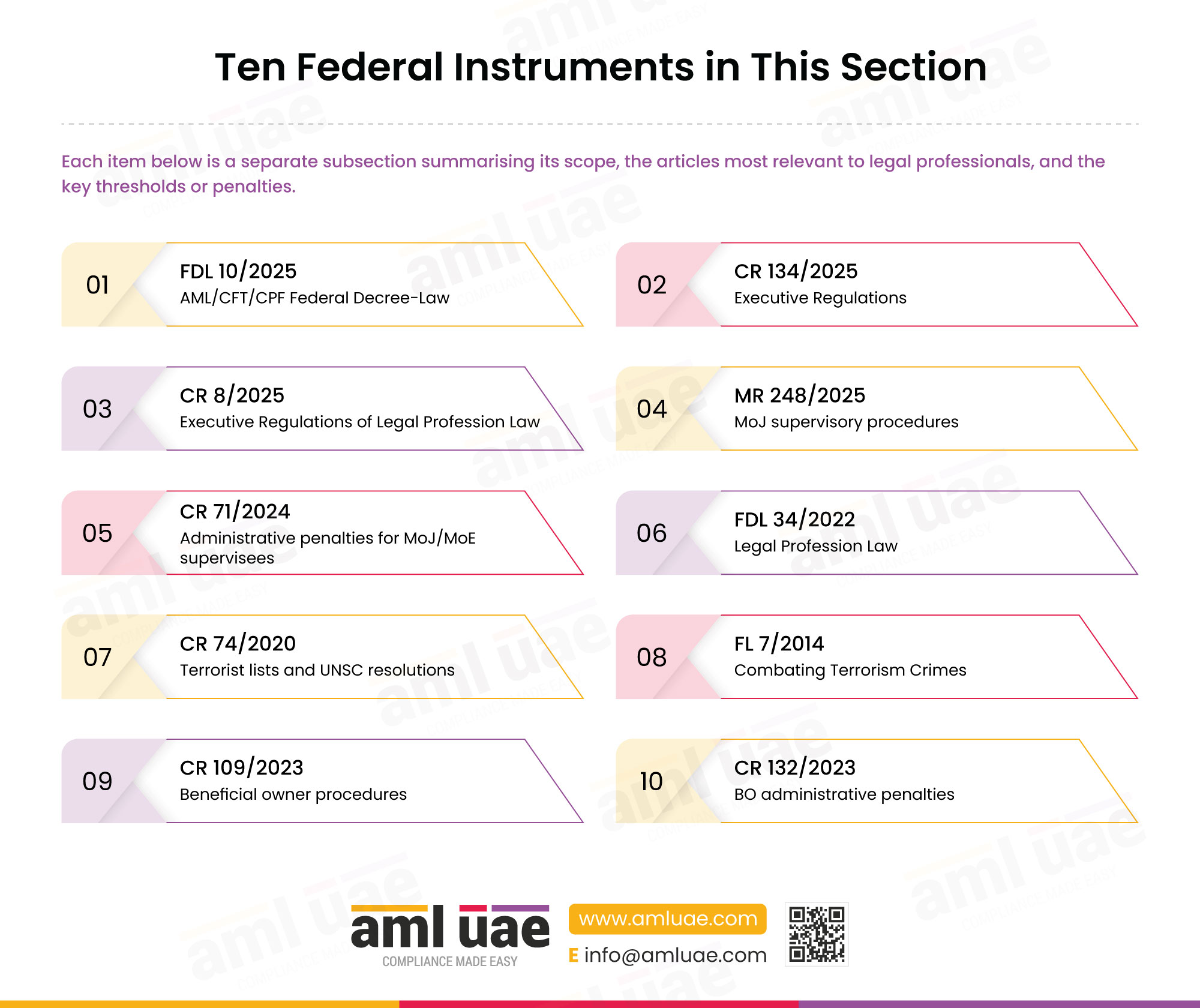

Ten federal instruments in this section

Each item below is a separate subsection summarising its scope, the articles most relevant to legal professionals, and the key thresholds or penalties.

01. FDL 10/2025

AML/CFT/CPF Federal Decree-Law

02. CR 134/2025

Executive Regulations

03. CR 8/2025

Executive Regulations of Legal Profession Law

04. MR 248/2025

MoJ supervisory procedures

05. CR 71/2024

Administrative penalties for MoJ/MoE supervisees

06. FDL 34/2022

Legal Profession Law

07. CR 74/2020

Terrorist lists and UNSC resolutions

08. FL 7/2014

Combating Terrorism Crimes

09. CR 109/2023

Beneficial owner procedures

10. CR 132/2023

BO administrative penalties

1. Federal Decree by Law No. (10) of 2025 Regarding Anti-Money Laundering, and Combating the Financing of Terrorism and Proliferation Financing

Federal Decree-Law No. (10) of 2025, issued on 30 September 2025, is the primary AML statute for the UAE. Article 41 repealed Federal Decree-Law No. (20) of 2018 and superseded its Executive Regulations, subject to any instruments issued under the old law remaining in force until amended, unless inconsistent with the new decree.

For lawyers, notaries, and legal consultants the most important provisions are Articles 2 and 3 which criminalise money laundering, financing of terrorism, and the financing of the proliferation of weapons of mass destruction; Article 18 which imposes the suspicious transaction reporting duty on DNFBPs subject to the privilege carve-out in clause 2; Article 19 on the prohibition on tipping off; Article 26 setting imprisonment from one to ten years and fines from AED 100,000 to AED 5,000,000 for laundering; Article 27 setting legal-person fines of AED 5,000,000 to AED 100,000,000; Article 28 imposing AED 100,000 to AED 1,000,000 for breaches of Article 18; Article 29 setting fines from AED 50,000 for tipping off; and Article 33 setting fines from AED 20,000 for breaches of targeted financial sanctions.

2. Cabinet Resolution No. (134) of 2025 Concerning the Executive Regulations of Federal Decree-Law No. (10) of 2025

Cabinet Resolution No. (134) of 2025 is the operational manual for the federal decree law. Article 3, Clause 4 lists the five covered activities that bring lawyers, notaries, and independent legal professionals inside the AML regime.

Article 18, Clause 2 preserves legal professional privilege over assessment of the client’s legal position, defence, representation, arbitration, mediation, and the issuing of a legal opinion.

Article 19, Clause 2 makes clear that dissuading a client from engaging in an unlawful act is not tipping off.

3. Cabinet Resolution No. (8) of 2025 Regarding the Executive Regulations of Federal Decree-Law No. (34) of 2022 Regulating the Legal Profession and Legal Consultation Profession

Cabinet Resolution No. (8) of 2025 is the Executive Regulations of the Legal Profession Law. While its scope is the profession generally rather than AML specifically, it governs licensing, categories of registration, conduct rules, disciplinary committees, and registers maintained by the Ministry of Justice, and it therefore sets the institutional foundation against which AML sanctions, such as suspension or cancellation of a licence, actually operate. Compliance officers should read it alongside Federal Decree-Law No. (34) of 2022 when assessing the consequences of supervisory action.

4. Ministerial Resolution No. (248) of 2025 on Supervising Law Firms, Legal Consultancy Offices, and Notaries Public

Ministerial Resolution No. (248) of 2025, issued on 29 April 2025, regulates the procedures and controls for supervising and monitoring law firms, legal consultancy offices, and notaries public in the field of combating money laundering and terrorism. It establishes the AML/CTF Department as the competent body; sets out inspection methodology; confirms application of Cabinet Resolution 71 of 2024 penalties through Article 6; provides a twenty-working-day grievance window in Article 7; mandates a thirty-working-day response window in Article 8; and repeals Ministerial Resolutions 532 and 533 of 2019.

5. Cabinet Resolution No. (71) of 2024 Regulating Violations and Administrative Penalties Imposed on Violators of AML/CFT Measures Under the Supervision of MoJ and MoE

Cabinet Resolution No. (71) of 2024, issued on 8 July 2024, is the administrative penalties grid for DNFBPs supervised by MoJ and by the Ministry of Economy. It repeals Cabinet Resolution No. (16) of 2021 and sets out forty-one categories of violation with fines ranging from AED 50,000 to AED 1,000,000. Article 4 provides a twenty-working-day notification window, a thirty-working-day grievance window, and a forty-day deemed-rejection rule where the grievance is not filed. Article 5 allows fines to be doubled on repetition within a set period. A selection of the schedule is reproduced below for orientation; firms should consult the full text for the complete list.

| Art | Violation summary | Fine (AED) |

|---|---|---|

| 1. | Failure to apply customer due diligence measures to new or existing clients. | 50,000 – 200,000 |

| 2. | Failure to identify the beneficial owner or to take reasonable steps to verify beneficial ownership information. | 50,000 – 200,000 |

| 3. | Failure to conduct ongoing monitoring of the business relationship and to scrutinise transactions. | 50,000 – 500,000 |

| 4. | Failure to conduct ongoing monitoring of the business relationship and to scrutinise transactions. | 100,000 – 500,000 |

6. Federal Decree-Law No. (34) of 2022 Regulating the Legal Profession and Legal Consultation Profession

Federal Decree-Law No. (34) of 2022 is the governing law of the legal profession. It sets out licensing conditions, categories of lawyers, conduct duties, disciplinary committees, and the powers of the Ministry of Justice and the Executive Council. For AML purposes, it is the upstream instrument that defines who is a lawyer or legal consultant and whose license may be suspended or cancelled when penalties under Cabinet Resolution 71 of 2024 are imposed.

7. Cabinet Decision No. (74) of 2020 Regarding Terrorism Lists and Implementation of UN Security Council Resolutions

Cabinet Decision No. (74) of 2020 regulates the UAE’s domestic terrorism lists and the implementation of United Nations Security Council resolutions on the suppression and combating of terrorism, terrorist financing, countering the proliferation of weapons of mass destruction, and related resolutions. It creates the obligation on every DNFBP, including law firms and notaries, to screen customers, transactions, and related parties against the UN Consolidated List and the UAE Local List; to apply without delay freezing measures on any confirmed match; and to report Confirmed Name Match Reports and Partial Name Match Reports to the FIU.

8. Federal Law No. (7) of 2014 on Combating Terrorism Crimes

Federal Law No. (7) of 2014 on Combating Terrorism Crimes is the criminal statute on terrorism offences, including financing. It defines terrorist acts, terrorist organisations, and the financing of terrorism, and it underpins the obligation in Federal Decree-Law 10 of 2025 to report suspicions of terrorism-related activity. Legal professionals should read it alongside Cabinet Decision 74 of 2020 when drafting STR scripts and training modules.

9. Cabinet Decision No. (109) of 2023 on Regulating the Beneficial Owner Procedures

Cabinet Decision No. (109) of 2023 governs beneficial owner disclosure for legal persons in the UAE. For legal professionals, the instrument is particularly relevant when they establish or manage companies for clients: they must help the entity meet the requirements to maintain a beneficial owner register, a nominee director register where applicable, and a partners or shareholders register; keep the information accurate and current; and file prescribed beneficial owner information with the registrar. The 25 per cent ownership threshold referenced in Cabinet Resolution 134 of 2025 mirrors the BO identification trigger used across the UAE framework.

10. Cabinet Resolution No. (132) of 2023 Concerning Administrative Penalties for Violations of Cabinet Decision No. (109) of 2023

Cabinet Resolution No. (132) of 2023 is the administrative penalties grid for beneficial owner breaches. Law firms that provide company formation and ongoing management services should understand these penalties because, although the penalty is imposed on the legal person, the firm’s role in maintaining the register and filing the data can attract parallel administrative liability under Cabinet Resolution 71 of 2024 as part of its AML obligations.

Quick Reference Timeline of Federal AML Instruments Affecting Legal Professionals

2014 CRIMINAL LAW Federal Law No. (7) of 2014 on Combating Terrorism Crimes Defines terrorism offences including financing and underpins STR scripts. |

2020 CROSS-SECTOR Cabinet Decision No. (74) of 2020 on terrorism lists and UNSC resolutions Creates screening, freezing, and EOCN reporting duties for every DNFBP. |

2022 PROFESSION Federal Decree-Law No. (34) of 2022 Regulating the Legal Profession Governs licensing, categories of lawyer, and disciplinary framework. |

2023 CROSS-SECTOR Cabinet Decision No. (109) of 2023 on Beneficial Owner Procedures Registers, filings, and 25 per cent identification threshold for legal persons. |

2023 CROSS-SECTOR Cabinet Resolution No. (132) of 2023 on BO Administrative Penalties Penalty grid for beneficial owner non-compliance. |

2024 CROSS-SECTOR Cabinet Resolution No. (71) of 2024 on AML/CFT Administrative Penalties Forty-one violations; fines AED 50,000 to AED 1,000,000; doubling on repetition. |

2025 PROFESSION Cabinet Resolution No. (8) of 2025 Executive Regulations of FDL 34/2022 Operational rules for licensing, registers, and disciplinary action. |

2025 SECTOR Ministerial Resolution No. (248) of 2025 on supervision of law firms and notaries Establishes MoJ AML/CTF Department, inspection methodology, and grievance windows. |

2025 FEDERAL Federal Decree-Law No. (10) of 2025 on AML/CFT/CPF Primary AML statute; repeals FDL 20/2018; imprisonment and fine bands. |

2025 FEDERAL Cabinet Resolution No. (134) of 2025 Executive Regulations of FDL 10/2025 Five covered activities; privilege carve-out; thresholds; BO rule. |

Need to map these laws to your firm's existing AML manual?

AML UAE performs gap-analysis mapping each article in FDL 10/2025, CR 134/2025, and CR 71/2024 to your current policies and procedures.

Overarching AML Guidance Applicable to Lawyers, Notaries, and Legal Professionals

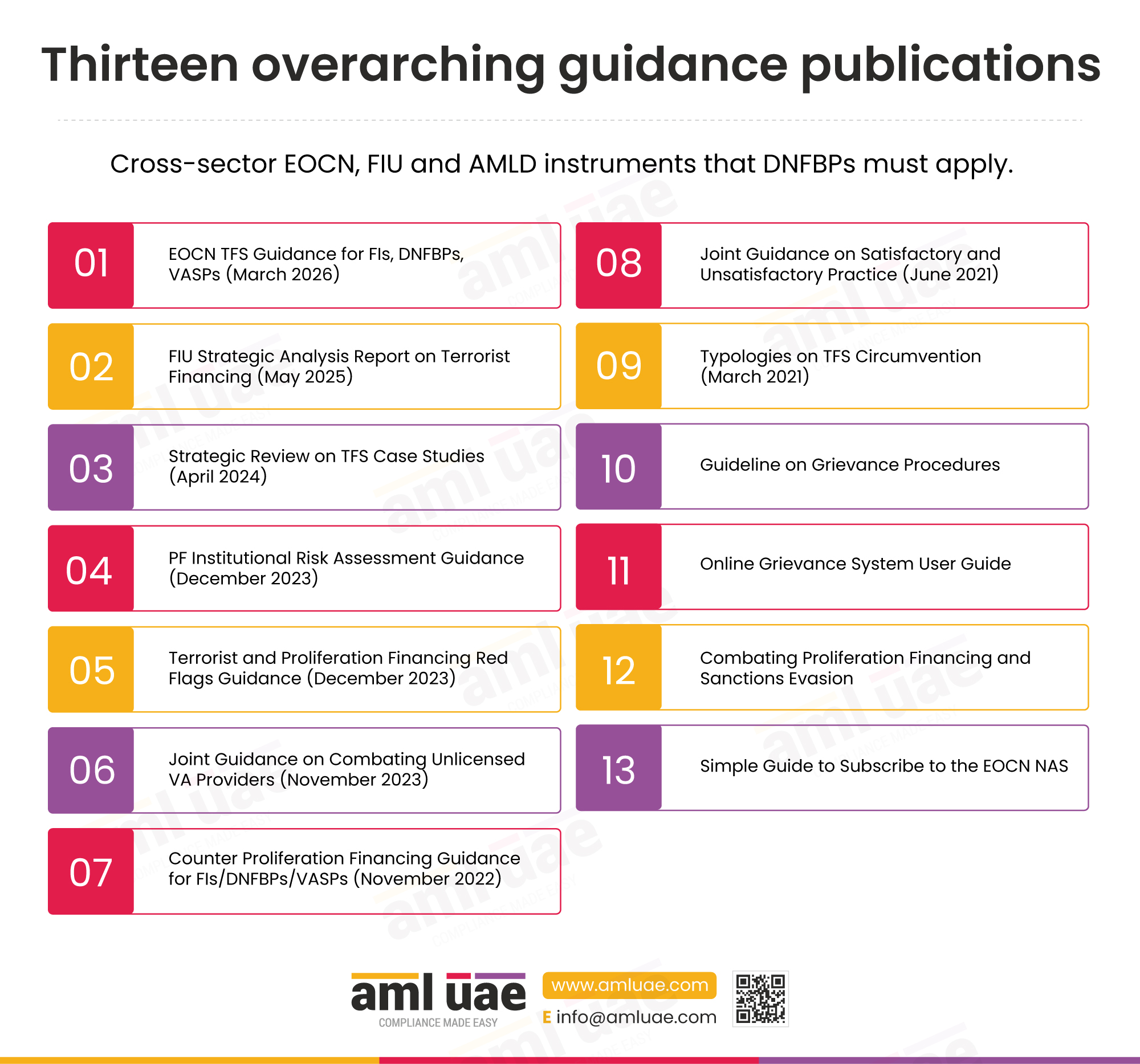

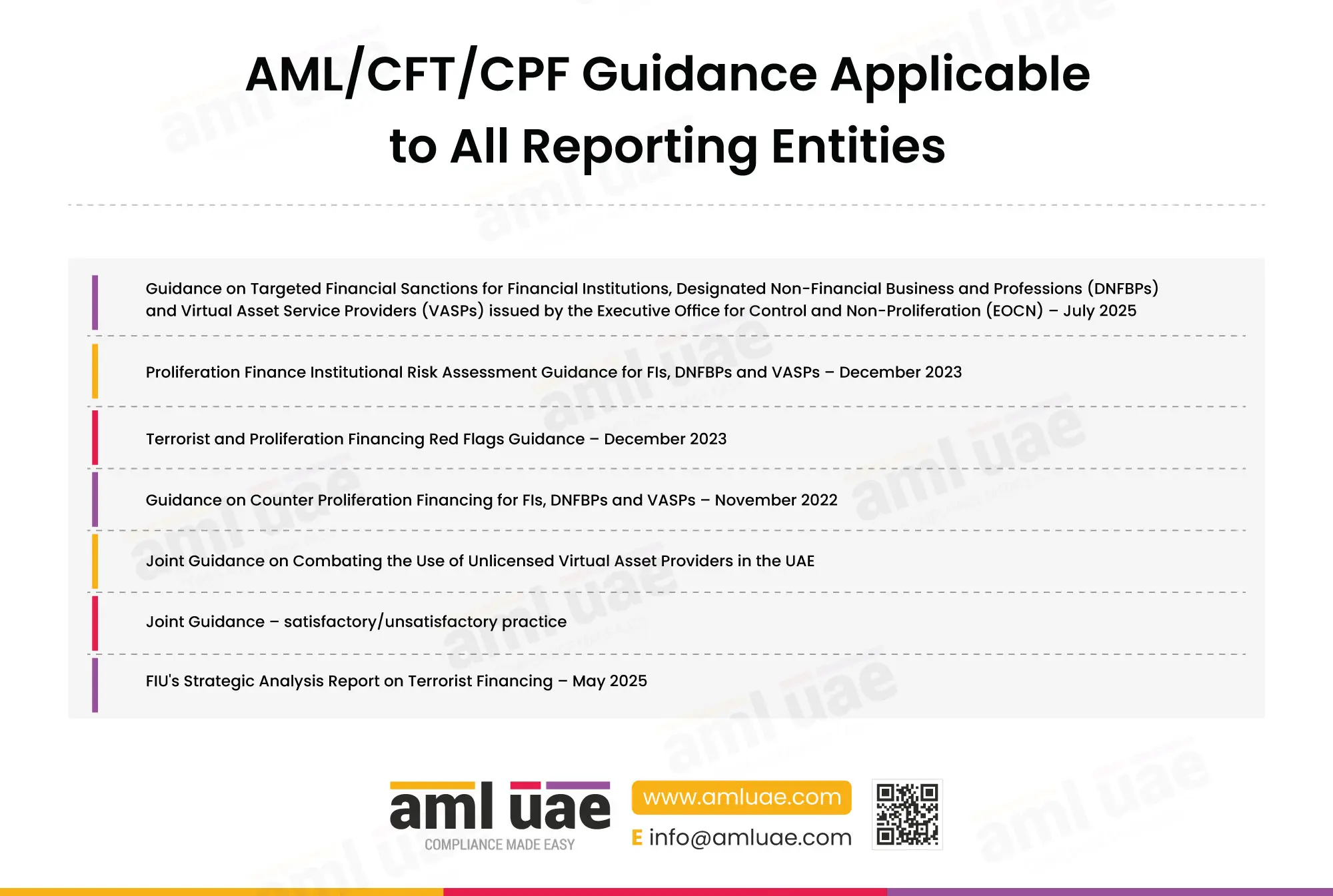

Beyond federal statutes, legal professionals must follow a library of cross-sector guidance issued by the Executive Office for Control and Non-Proliferation, the Financial Intelligence Unit, and the National AML/CFT Committee. These documents are not stand-alone rulebooks, but failure to act on them is regularly cited as a contributing factor when administrative penalties are imposed under Cabinet Resolution 71 of 2024.

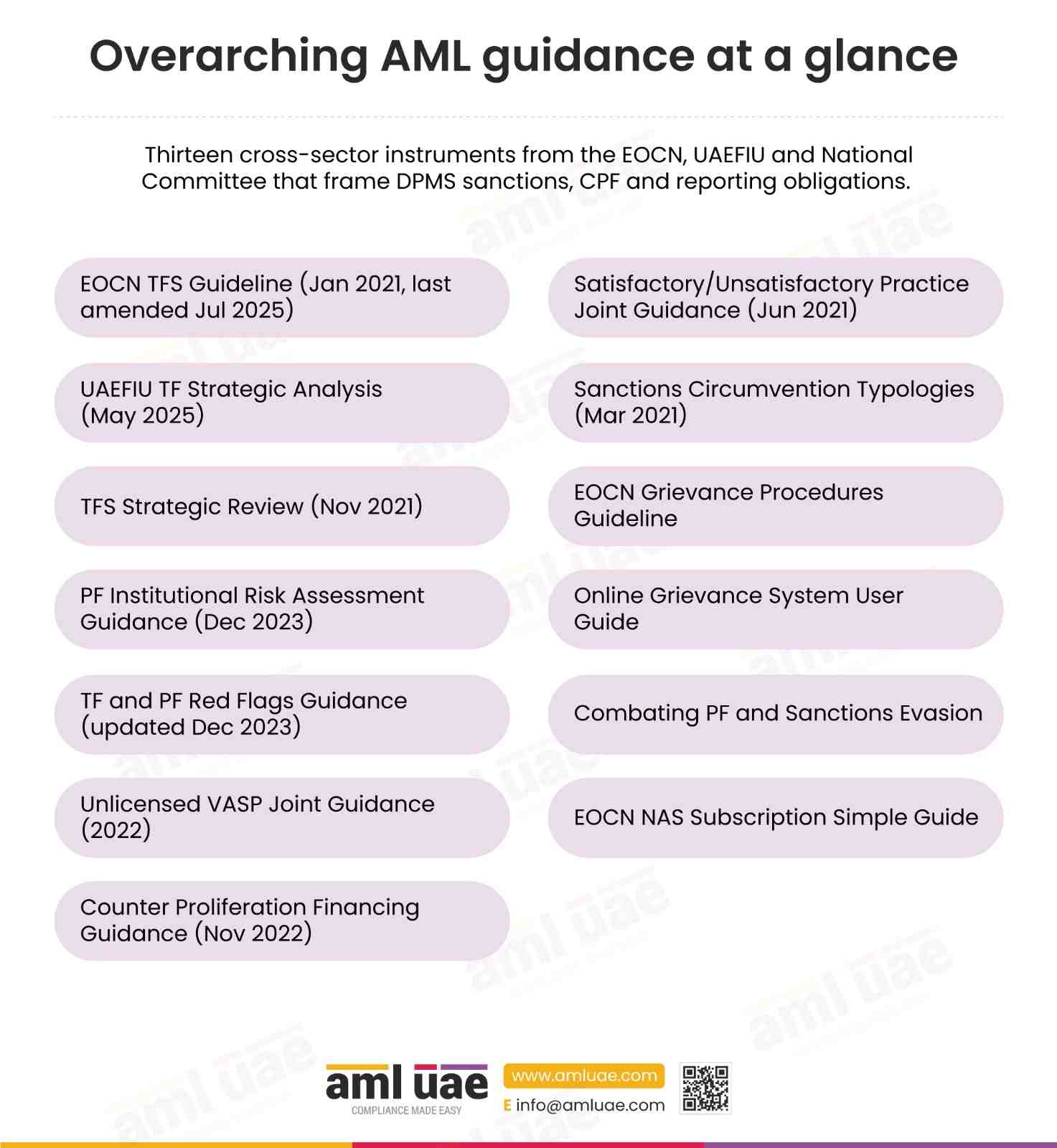

Thirteen cross-sector documents in this section

Dates, issuers, and scope; each gets its own reference card below.

01. TFS Guidance (EOCN)

AML/CFT/CPF Federal DecCore guidance on targeted financial sanctions for FIs, DNFBPs, and VASPs. ree-Law

02. FIU Strategic Analysis

Terrorist financing typologies and facilitators, May 2025

03. Strategic Review

TFS case studies covering 2019 to 2021.

04. PF Institutional RA

Proliferation finance institutional risk assessment guidance.

05. TF and PF Red Flags

Red flag indicators on terrorist and proliferation financing.

06. Unlicensed VA Providers

Joint guidance on combating unlicensed virtual asset providers.

07. CPF Guidance

Counter proliferation financing guidance for FIs, DNFBPs, and VASPs.

08. Satisfactory Practice

Joint guidance on satisfactory and unsatisfactory practice.

09. TFS Typologies

EOCN typologies on circumvention of targeted sanctions.

10. Grievance Guideline

Framework for challenging supervisory decisions.

11. Online Grievance Guide

Step-by-step user guide for the MoJ online grievance system.

12. Combating PF & Sanctions Evasion

Cross-agency publication on PF and sanctions evasion.

13.NAS Simple Guide

How to subscribe to the EOCN Notification Alert System.

1. Guidance on Targeted Financial Sanctions for FIs, DNFBPs and VASPs (EOCN)

Issued January 2021; Last amended March 2026

Guidance on Targeted Financial Sanctions for Financial Institutions, Designated Non-Financial Businesses and Professions, and Virtual Asset Service Providers

Central EOCN guidance explaining the legal framework for TFS, scope of application, freezing without delay, reporting of Confirmed Name Match Reports and Partial Name Match Reports, use of the goAML and EOCN Notification Alert System, and expectations on sanctions screening, governance, and training. Published on eocn.gov.ae.

2. FIU Strategic Analysis Report on Terrorist Financing (May 2025)

May 2025

Terrorist Financing Typologies and Facilitators – A Strategic Analysis Report

UAEFIU public version strategic analysis setting out TF typologies and facilitator profiles observed in UAE STR data; complements sector red-flag catalogues and informs MoJ risk-based inspection priorities.

3. Strategic Review on Targeted Financial Sanctions Case Studies (April 2024)

April 2024 (content: November 2021, IEC-SR.01.22)

Strategic Review on Targeted Financial Sanctions Case Studies 2019-2021

EOCN review of case studies drawn from UAE TFS implementation, highlighting common failings such as delayed screening, weak governance, and unreported partial matches. Useful for law firms drafting sanctions-screening logs.

4. Proliferation Finance Institutional Risk Assessment Guidance (December 2023)

Published December 2023

Proliferation Finance Institutional Risk Assessment Guidance for FIs, DNFBPs and VASPs

Methodology for conducting a firm-level PF risk assessment, including jurisdiction, customer, product, and delivery-channel risk. Expected input into a law firm’s enterprise-wide risk assessment.

5. Terrorist and Proliferation Financing Red Flags Guidance (December 2023)

Published September 2023; updated December 2023

Terrorist and Proliferation Financing Red Flags Guidance

Concise catalogue of TF and PF red flags designed to be embedded in STR decision trees. Firms should map each indicator to their goAML reporting workflow.

6. Joint Guidance on Combating the Use of Unlicensed Virtual Asset Providers (November 2023)

Issued March 2022 (Supervisory Authority Sub-Committee)

Joint Guidance on Combating the Use of Unlicensed Virtual Asset Providers in the United Arab Emirates

Expectations on DNFBPs, including law firms handling digital-asset company formations, to screen for unlicensed virtual asset activity and reject onboarding where red flags are present

7. Guidance on Counter Proliferation Financing for FIs, DNFBPs, and VASPs (November 2022)

Published 01 November 2022 – EOCN-PF.01.23

Counter Proliferation Financing Guideline

Authoritative EOCN guidance on CPF obligations, including understanding dual-use goods typologies, sanctions evasion tactics, and the expected governance response.

8. Joint Guidance on Satisfactory and Unsatisfactory Practice (June 2021)

June 2021

Anti-Money Laundering and Countering Terrorist Financing Guidelines – Satisfactory and Unsatisfactory Practice

Supervisory Authority Sub-Committee guidance contrasting practices that are considered satisfactory with those that are unsatisfactory. A reliable benchmark for internal audits.

9. Typologies on the Circumvention of Targeted Sanctions (March 2021)

Issued 20 March 2021; last amended 11 May 2021

Typologies on the Circumvention of Targeted Sanctions against Terrorism and the Proliferation of Weapons of Mass Destruction (United Arab Emirates)

EOCN typology paper focusing on evasion techniques including shell companies, trade-based methods, and misuse of legal persons. Particularly relevant to law firms establishing and managing entities.

10. Guideline on Grievance Procedures

Undated (EOCN publication)

Guideline on Grievance Procedures

Framework guidance on filing grievances against supervisory decisions across federal authorities. Read alongside Articles 7 and 8 of MR 248 of 2025 for timelines.

11. Online Grievance System User Guide

Undated

Online Grievance System – User Guide

Step-by-step walkthrough of the online grievance platform, including registration, grievance submission, and status tracking

12. Combating Proliferation Financing and Sanctions Evasion

EOCN publication

Combating Proliferation Financing & Sanctions Evasion

Reference text on PF typologies and evasion techniques; integrates with the CPF Guidance and the Typology Paper.

13. Simple Guide to Subscribe to the EOCN Notification Alert System (NAS)

EOCN publication

Simple Guide to Subscribe to the EOCN Notification Alert System (NAS)

Short operational guide to subscribing to the NAS, which delivers near real-time notifications of UN and UAE list updates and is a standard control for every law firm’s sanctions programme.

Turning guidance into workable controls

AML UAE converts cross-sector guidance into operational checklists, screening-log templates, and STR decision trees tailored to your firm's covered activities.

NRA, SRA, and Other Important Guidelines Applicable to Lawyers and Legal Professionals

The UAE Money Laundering and Terrorist Financing Risk Assessment Report is the single most important cross-cutting risk document for every DNFBP, including law firms and notaries. Published by the National Anti-Money Laundering and Combating the Financing of Terrorism and Financing of Illegal Organisations Committee, it sets the macro picture against which sectoral risk assessments and firm-level risk assessments are calibrated.

UAE Money Laundering and Terrorist Financing Risk Assessment Report – 2024

National AML/CFT Committee

UAE Money Laundering and Terrorist Financing National Risk Assessment Report

The NRA assesses ML and TF threats and vulnerabilities across the UAE financial, VASP, and DNFBP sectors. In the UAE, the Law Firms and Legal Consultations Sector is classified as Medium-Low risk for ML since there are no evidence showing that the sector has been abused for ML, or any predicate offences

to ML. For legal professionals it highlights risks associated with the establishment and management of legal persons and arrangements, real estate transactions, and complex cross-border structures, feeding into the MoJ’s sector supervision plan. Circular No. (2) of 2025 of the Ministry of Justice directly instructs law firms to reflect NRA findings in their firm-wide risk assessments.

Does your firm's risk assessment reflect the NRA?

AML UAE helps law firms translate NRA findings into firm-specific risk factors and weight them appropriately in the customer risk methodology.

Sector-Specific Guidelines Applicable to Lawyers, Notaries, and Legal Professionals

Sector-specific instruments are issued by the Ministry of Justice. They fall into two groups: the central Guidebook that explains what satisfactory compliance looks like, and a sequence of circulars that direct firms to act on discrete obligations (policy updates, high-risk country lists, TFS implementation, and the real-estate activities report). All circulars listed below are officially published by the Ministry of Justice; the 2023, 2024, 2025, and 2026 policy update circulars are available on the MoJ website, while the earlier circulars are published in Arabic on the MoJ portal.

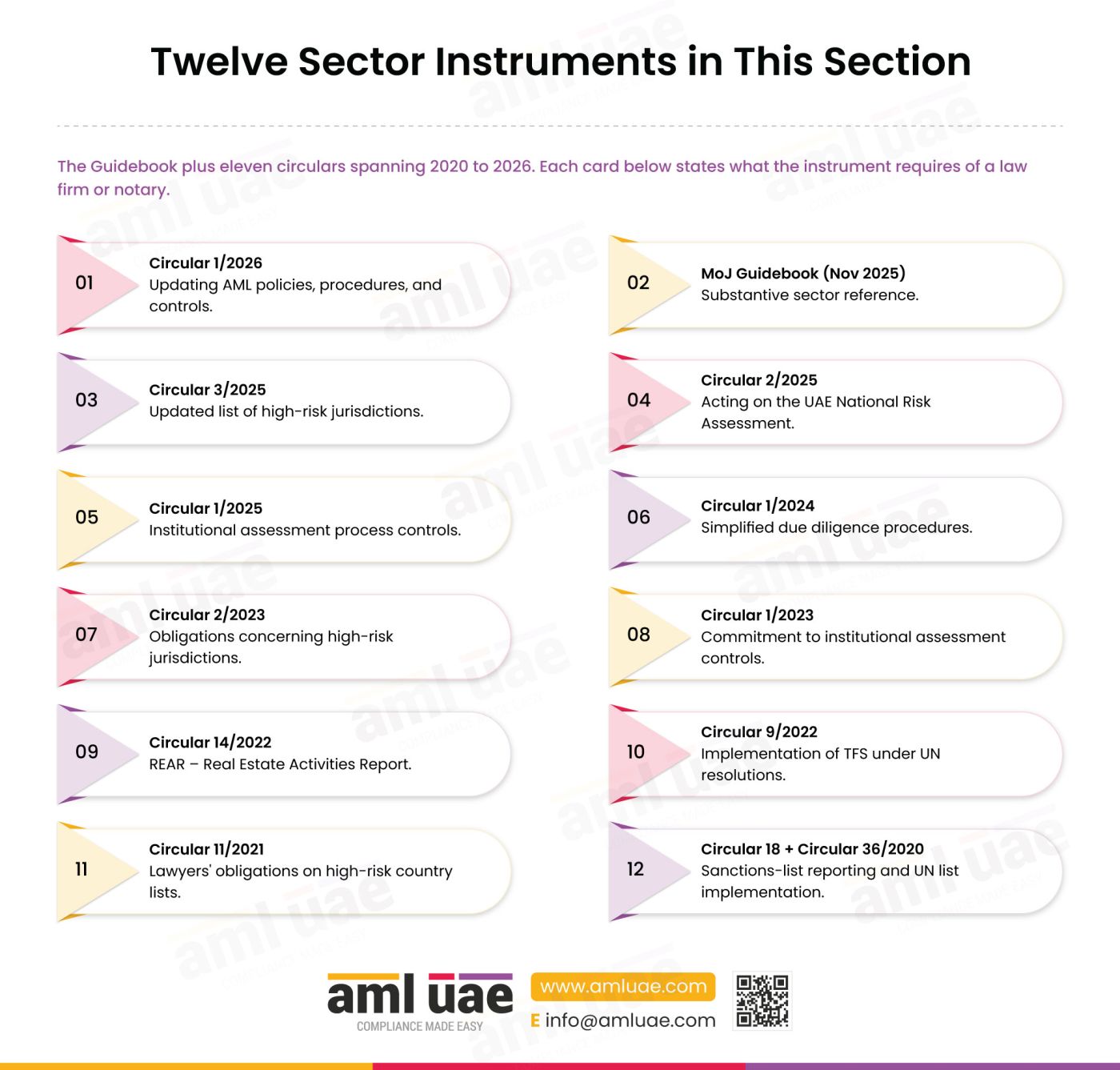

Twelve sector instruments in this section

The Guidebook plus eleven circulars spanning 2020 to 2026. Each card below states what the instrument requires of a law firm or notary.

01.Circular 1/2026

Updating AML policies, procedures, and controls.

02. MoJ Guidebook (Nov 2025)

Substantive sector reference.

03. Circular 3/2025

Updated list of high-risk jurisdictions.

04. Circular 2/2025

Acting on the UAE National Risk Assessment.

05. Circular 1/2025

Institutional assessment process controls.

06. Circular 1/2024

Simplified due diligence procedures.

07. Circular 2/2023

Obligations concerning high-risk jurisdictions.

08. Circular 1/2023

Commitment to institutional assessment controls.

09. Circular 14/2022

REAR – Real Estate Activities Report.

10. Circular 9/2022

Implementation of TFS under UN resolutions.

11. Circular 11/2021

Lawyers’ obligations on high-risk country lists.

12. Circular 18 + Circular 36/2020

Sanctions-list reporting and UN list implementation.

1. Circular No. (1) of 2026 Concerning the Obligation of Law Firms and Legal Consultancy Offices to Update Policies, Procedures, and Controls Related to AML/CFT/CPF (Arabic only)

Issued 2026

Circular No. 1 of 2026 – Updated AML/CFT/CPF policies, procedures, and controls

Directs law firms and legal consultancy offices to refresh their internal AML/CFT/CPF policies, procedures, and controls to reflect Federal Decree-Law 10 of 2025 and Cabinet Resolution 134 of 2025, and to update documentation accordingly. Published by the Ministry of Justice; currently available in Arabic only.

2. Guidebook for Law Firms and Legal Consultancy Offices on AML/CFT/CPF (November 2025)

Second Edition, published 25 November 2025

Guidebook for Law Firms and Legal Consultancy Offices on Combating Money Laundering, Countering the Financing of Terrorism and Countering Proliferation Financing

The principal sector reference issued by the Director of the AML/CTF Department at the Ministry of Justice. It covers relevant legislation, supervisory structure, AML Department functions, key obligations, compliance-officer requirements, STR reporting via goAML, five-year record retention, TFS 24-hour freeze and one-business-day EOCN notification, administrative sanctions, appeal procedures, and sources of assistance including amlctf@moj.gov.ae and the EOCN address iec@uaeiec.gov.ae

3. Circular No. (3) of 2025 Regarding the Update of the List of High-Risk Countries and Countries Subject to Enhanced Monitoring (Arabic only)

Issued 2025

Circular No. 3 of 2025 – Updated list of high-risk countries

Directs lawyers and law firms to apply enhanced due diligence to clients from the updated FATF high-risk jurisdictions and jurisdictions subject to increased monitoring. Currently available in Arabic only on the Ministry of Justice website.

4. Circular No. (2) of 2025 Regarding the National Risk Assessment (Arabic only)

Issued 2025

Circular No. 2 of 2025 – National Risk Assessment

Requires law firms to align their firm-wide risk assessments, client risk methodologies, and control environments with findings in the UAE National Risk Assessment. Currently available in Arabic only.

5. Circular No. (1) of 2025 Regarding Commitment of Law Firms to the Controls of Institutional Assessment Processes (Arabic only)

Issued 2025

Circular No. 1 of 2025 – Institutional assessment process controls

Sets expectations on the institutional assessment process that law firms must follow, including documentation, sign-off, and periodic review. Currently available in Arabic only.

6. Circular No. (1) of 2024 Regarding Simplified Due Diligence Procedures (Arabic only)

Issued 2024

Circular No. 1 of 2024 – Simplified due diligence procedures

Clarifies the circumstances in which simplified due diligence is permitted, aligning with Cabinet Resolution 134 of 2025 on low-risk scenarios. Currently available in Arabic only

7. Circular No. (2) of 2023 Regarding Obligations of Lawyers Concerning the Updated List of High-Risk Countries (Arabic only)

Circular No. 2 of 2023 concerns lawyers’ obligations concerning the updated list of high-risk countries. A copy of this circular was not available to us in PDF form at the time of writing; the text is referenced in the Ministry of Justice archive, but firms should obtain the current version directly from the Ministry before applying it.

8. Circular No. (1) of 2023 Regarding Commitment of Law Firms to the Controls of Institutional Assessment Processes (Arabic only)

Issued 2023

Circular No. 1 of 2023 – Institutional assessment controls

Earlier MoJ circular requiring law firms to commit to the controls of institutional AML assessment processes; superseded in substance by Circular No. 1 of 2025 on the same subject.

9. Circular No. (14) of 2022 Regarding the REAR Real Estate Activities Report (Arabic only)

Issued 2022

Circular No. 14 of 2022 – REAR (Real Estate Activity Report)

Instructs law firms involved in real estate transactions to file the Real Estate Activity Report on relevant transactions, consistent with the requirements that apply across DNFBPs handling real estate.

10. Circular No. (9) of 2022 on Implementation by Lawyers of Targeted Financial Sanctions Under UN Security Council Resolutions (Arabic only)

Issued 2022

Circular No. 9 of 2022 – Implementation by lawyers of targeted financial sanctions

Reaffirms that lawyers must implement targeted financial sanctions stipulated by UN Security Council resolutions and the UAE cabinet, with without-delay freezing and reporting via EOCN.

11. Circular No. (11) of 2021 Regarding Lawyers' Obligations on Updated List of High-Risk Countries (Arabic only)

Issued 2021

Circular No. 11 of 2021 – Lawyers’ obligations on high-risk countries

Requires lawyers to apply enhanced due diligence to clients from high-risk jurisdictions; predecessor to Circular 3 of 2025 on the same subject.

12. Circular No. (18) Regarding Lawyers' Implementation of Obligations to Report Clients on Sanctions Lists (Arabic only)

Issued 2020

Circular No. 18 – Reporting of clients on international or local sanctions lists

Directs law firms to report clients appearing on international or local sanctions lists in accordance with federal and EOCN procedures.

13. Circular No. (36) of 2020 Regarding the International and Local Sanctions Lists (Arabic only)

Issued 2020

Circular No. 36 of 2020 – International and local sanctions lists

Implements UN Security Council and cabinet sanctions lists at the level of lawyers and law firms, including obligations to screen clients and report matches.

Conclusion

AML regulations for lawyers in UAE are neither a single rulebook nor a single set of penalties. They are a federated framework anchored in Federal Decree-Law No. (10) of 2025 and its Executive Regulations, built up through Cabinet Resolution No. (74) of 2020 on sanctions, Cabinet Decision No. (109) of 2023 on beneficial ownership, Cabinet Resolution No. (132) of 2023 on BO penalties, and Cabinet Resolution No. (71) of 2024 on administrative penalties, and made operational for the legal sector through Ministerial Resolution No. (248) of 2025, the Ministry of Justice Guidebook of November 2025, and a sequence of MoJ circulars from 2020 to 2026.

What this means in practice for law firms, legal consultancy offices, and notaries public is that compliance is continuous rather than episodic. A satisfactory firm will maintain an enterprise-wide risk assessment that reflects the UAE National Risk Assessment; a client-onboarding process that systematically tests whether a matter falls within one of the five covered activities; sanctions-screening logs and Confirmed Name Match Report workflows that support the 24-hour freeze and one-business-day EOCN reporting; STR decision trees that operate through goAML and respect the privilege carve-out in Article 18, Clause 2 of FDL 10 of 2025 and CR 134 of 2025; a five-year records retention architecture; policies and procedures that are refreshed whenever a new MoJ circular is issued; and a training programme that keeps partners, lawyers, paralegals, and notaries public current on the framework.

Firms licensed in ADGM or DIFC operate inside their respective free-zone regimes and should look to FSRA and DFSA rulebooks rather than MoJ instruments. For every other MoJ-supervised legal professional, the rulebook above is the benchmark the AML/CTF Department will use on an inspection.

Found this guide useful?

If this article helped you clarify your firm's AML obligations, a short Google review helps other legal professionals find clear, sourced UAE guidance.

Frequently Asked Questions

When do lawyers and legal consultants fall under UAE AML law?

A lawyer, legal consultant, or notary public falls under UAE AML law when they prepare or carry out any of the five covered activities under Article 3, Clause 4 of Cabinet Resolution 134 of 2025: buying or selling real estate; managing client money, securities, or assets; managing bank, savings, or securities accounts; organising contributions for a company; or establishing, operating, or managing legal persons or arrangements. Pure litigation, arbitration, mediation, and legal opinion work is protected by the privilege carve-out in Article 18, Clause 2 of Federal Decree-Law 10 of 2025.

Which regulator supervises lawyers for AML in the UAE?

The Ministry of Justice supervises law firms, legal consultancy offices, and notaries public through its AML/CTF Department, following Cabinet Decision No. (1/3 W) of 2019 and Cabinet Decision 65 of 2024, which upgraded the AML section into a full department. Ministerial Resolution No. (248) of 2025 sets out the current supervisory procedures and controls. Firms licensed in ADGM are supervised by FSRA; firms licensed in DIFC are supervised by DFSA.

What practical AML records should a law firm maintain?

A law firm should maintain its firm-wide risk assessment; each client risk assessment; CDD and enhanced due diligence files; beneficial ownership information; transaction records and transaction risk assessments for covered activities; sanctions-screening logs, including CNMR and PNMR records and EOCN correspondence; STR decision records and goAML submission receipts; training and attendance records; and a corrective action register. Retention is for five years from the end of the business relationship or completion of the transaction, per the MoJ Guidebook of November 2025 and Cabinet Resolution 134 of 2025.

What does the 2025 MoJ resolution change?

Ministerial Resolution No. (248) of 2025, issued on 29 April 2025, replaces Ministerial Resolutions 532 and 533 of 2019. It confirms the MoJ AML/CTF Department as the competent supervisory body for law firms, legal consultancy offices, and notaries public; applies the Cabinet Resolution 71 of 2024 penalty schedule through Article 6; provides a 20-working-day grievance window in Article 7; and requires a 30-working-day response in Article 8. Firms should refresh their sanctions, STR, and governance policies to align with the new instrument.

Do law firms in ADGM and DIFC follow separate AML rules?

Yes. Law firms licensed in Abu Dhabi Global Market are supervised by the Registration Authority and follow the ADGM Financial Services and Markets Regulations together with the FSRA AML Rulebook. Law firms licensed in the Dubai International Financial Centre are supervised by the Dubai Financial Services Authority and follow the DIFC Regulatory Law and DFSA AML Module. These free-zone regimes are distinct from the Mainland MoJ regime described above and are covered on the ADGM and DIFC pages in this cluster.

Talk to AML UAE about your firm's compliance programme

Whether you are setting up a new law firm, responding to a MoJ inspection, or refreshing policies following Circular 1 of 2026, AML UAE helps legal professionals implement the full framework.

Share via :

About the Author

Pathik Shah

FCA, CAMS, CISA, CS, DISA (ICAI), FAFP (ICAI)

Pathik is an ACAMS-certified AML consultant specialising in governance, risk, and compliance for regulated entities in the UAE. He brings over 28 years of experience, with 1,000+ hours of AML training and 200+ advisory engagements across DNFBPs, VASPs, and FIs. He supports businesses in aligning with AML/CFT requirements from the CBUAE, DFSA, MoET, MoJ, VARA, CMA, FSRA, and FATF. Known for translating complex regulations into audit-ready procedures, Pathik enables operational clarity and compliance readiness.

Reach Out to Pathik

")