Blogs

Published On: 06/25/2026

Protect your business with reliable and effective AML strategies with AML UAE.

Last Reviewed On: 07/23/2026 | Last Updated On: 07/23/2026

Layering at A Glance

- Layering in money laundering refers to obscuring the origin of illicit funds by moving them through multiple transactions.

- Criminals use complex transfers, shell companies, and investment instruments to distance the money from its criminal source.

- The goal of layering is to make detection and tracing extremely difficult.

- Strong AML controls, transaction monitoring, and risk-based checks are essential to detect and prevent layering activities

")

What is Layering in Money Laundering?

Layering in money laundering refers to disguising the source of illicit funds through layers of financial transactions, accounts, entities, assets, or jurisdictions. It is usually the second stage of the money laundering process, after placement and before integration. In simple terms, placement puts illegal money into the financial system, layering hides the money trail, and integration makes the funds appear legitimate.

Layering is often the most complex stage of money laundering to detect because the activity may appear normal when each transaction is viewed in isolation. The suspicion usually becomes clearer when the full pattern is reviewed, such as rapid fund movement, unrelated third-party payments, cross-border transfers, shell companies, complex ownership structures, virtual asset movement, or transactions that do not match the customer profile.

For UAE-regulated entities, understanding the layering stage of money laundering is important because criminals may misuse banks, exchange houses, real estate businesses, dealers in precious metals and stones, virtual asset service providers, lawyers, accountants, auditors, and company service providers to disguise the origin of funds.

This guide explains the meaning of layering in money laundering, how it works, common examples, AML red flags, the differences among layering, placement, integration, structuring, and smurfing, and the controls UAE businesses can use to detect and manage layering risks.

Key Takeaways

Layering is the second stage of money laundering, sitting between placement and integration.

Its purpose is to break the audit trail so funds cannot be traced back to a crime.

Common methods include multiple transfers, cross border movement, shell companies, trade, real estate, precious metals, and virtual assets.

A single transaction may look normal. Layering is usually visible only across the full pattern.

UAE obligations sit under Federal Decree by Law No. 10 of 2025 and its executive regulations in Cabinet Resolution No. 134 of 2025, with suspicious transactions reported to the UAE Financial Intelligence Unit through goAML.

Layering Money Laundering Means, in Simple Terms

Layering is the stage where criminals move, split, convert, transfer, or restructure illicit funds to make the money trail harder to follow. The main goal is to separate the funds from their illegal source by creating several layers of financial activity.

A simple example is this:

- Illegal money enters the financial system.

- The money is transferred through multiple bank accounts.

- It is moved to another country or converted into another currency.

- It is passed through a company, an asset, an investment, or a virtual asset wallet.

- It later appears to come from a legitimate business, sale, loan, investment, or asset transaction.

The more layers criminals create, the harder it becomes for banks, businesses, regulators, and law enforcement agencies to identify the true origin of the funds.

Money Laundering Layering Definition

Layering is the stage of money laundering where illicit funds are moved through complex transactions to conceal their criminal origin, ownership, control, movement, or destination.

Layering can involve financial transactions, legal structures, business arrangements, trade documents, professional intermediaries, physical assets, or digital assets. The objective is to make illegal funds look disconnected from the crime that generated them.

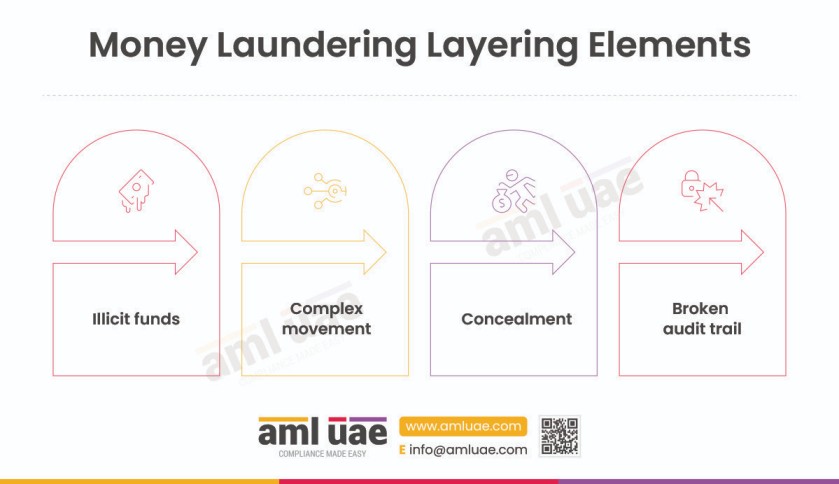

A strong definition of layering should include four elements:

| Element | Explanation |

| Illicit funds | The money or value comes from criminal activity. |

| Complex movement | Funds are transferred, converted, split, combined, or moved through multiple channels. |

| Concealment | The activity is designed to hide the source, owner, controller, or destination. |

| Broken audit trail | The transaction history becomes harder to trace and verify. |

What does Layering Mean in AML?

In AML, layering means using complex transactions, accounts, entities, assets, or jurisdictions to hide the source, ownership, movement, or destination of illicit funds. AML teams identify potential layering by reviewing customer behaviour, transaction patterns, beneficial ownership, sources of funds and wealth, counterparties, jurisdictional risk, and the commercial purpose of transactions.

Layering in AML matters because the activity may not look suspicious as a single transaction. One transfer, invoice, property purchase, virtual asset transaction, or currency exchange may appear ordinary. The risk often becomes visible only when multiple transactions are reviewed together. For example, a customer may receive funds from one company, transfer them to another entity, move part of the money overseas, use part of it to buy precious metals, and later claim that the funds came from business activity. Each step may look explainable on its own, but the full pattern may show an attempt to disguise the origin of funds.

Layering in the wider financial crime context. The same concealment behaviour is sometimes described simply as layering in financial crime or fraud. The principle is identical: value is moved through deliberate layers so the trail back to the original wrongdoing is broken. In an AML programme, this is managed during the layering stage of money laundering, as described throughout this guide.

AML layering risks may appear in many forms:

| AML layering risk | What it may indicate |

| Funds move quickly through an account | The account may be used only as a pass through account. |

| Multiple unrelated parties are involved | The true owner or controller may be hidden. |

| Transactions involve high risk jurisdictions | The money trail may be intentionally complicated. |

| The customer cannot explain the source of funds | The funds may not have a legitimate origin. |

| The transaction has no clear economic purpose | The activity may be artificial or circular. |

| Documents appear weak, vague, or inconsistent | The explanation may be created only to support the transaction. |

AML teams should not look only at transaction value. They should also consider timing, frequency, counterparties, customer profile, expected business activity, documentation, sources of funds, and whether the transaction makes commercial sense.

What is Layering in Banking?

In banking, layering refers to suspicious movement of funds through multiple accounts, transfers, banking products, customers, or jurisdictions to hide the source or ownership of money. Banks may identify possible layering when funds move rapidly in and out, pass through unrelated accounts, involve third-party payments, or do not match the customer’s expected activity.

| Banking pattern | Why it may be suspicious |

| Funds are received and transferred out quickly | May indicate pass through activity. |

| Multiple accounts are opened and closed | May be used to break the audit trail. |

| Funds move through unrelated third parties | May hide the true owner or purpose. |

| Repeated transfers occur without business rationale | May suggest artificial transaction layers. |

| Cross border transfers involve high risk jurisdictions | May increase money laundering risk. |

| Activity does not match the customer profile | May indicate misuse of the account. |

| Funds move between related companies without clear purpose | May indicate circular movement of funds. |

For banks and exchange houses, layering risk is often detected through transaction monitoring, customer due diligence, source-of-funds checks, enhanced due diligence, sanctions screening, politically exposed person screening, and ongoing monitoring of customer behaviour.

Why Layering Matters in AML Compliance?

Layering matters because it is the stage where the money trail becomes harder to follow. At the placement stage, suspicious funds may still be evident through cash deposits, unusual receipts, or unexplained inflows into the financial system. During layering, criminals attempt to create distance between the money and its illegal source. A single transaction may not be enough to prove suspicion. The risk usually becomes apparent when the business reviews the broader pattern.

| Pattern | Why it may indicate layering |

| Funds move in and out quickly with no clear reason | May indicate pass through activity. |

| Multiple parties are involved without a clear role | May hide the beneficial owner or controller. |

| Transactions pass through unrelated jurisdictions | May be used to break the audit trail. |

| Funds are converted into assets or virtual assets | May disguise the form, value, or ownership of money. |

| Transaction value does not match the customer profile | May indicate activity inconsistent with known income or business. |

| Documents do not support the stated purpose | May indicate a false or weak explanation. |

| The customer avoids questions | May suggest unwillingness to disclose the real purpose. |

Layering is not limited to financial institutions. It can involve real estate businesses, dealers in precious metals and stones, auditors, accountants, lawyers, trust and company service providers, virtual asset service providers, and other regulated entities.

Where Layering Sits in the Money Laundering Process

Money laundering is commonly explained in three stages: placement, layering, and integration. FATF material refers to the money laundering cycle as including placement, layering and integration. Layering is the second stage. It comes after placement, when illicit funds enter the financial system, and before integration, when the funds are made to appear legitimate.

| Stage | Meaning | Simple example |

| Placement | Illicit funds are introduced into the financial system. | Criminal cash is deposited, exchanged, or used to buy high value goods. |

| Layering | Funds are moved or converted to hide their origin. | Money is transferred between accounts, companies, countries, assets, or wallets. |

| Integration | Laundered funds re enter the economy as apparently legitimate wealth. | Funds are used to buy property, securities, luxury goods, or business assets. |

The three stages can overlap in practice. A criminal does not always complete placement, then layering, then integration in a neat order. Some schemes combine activities from different stages, especially where companies, trade, real estate, virtual assets, and professional intermediaries are involved.

Looking for the full picture of the stages?

This page focuses on layering. For the complete cycle and each stage in depth, see the dedicated guides:

Layering vs Placement vs Integration

Placement, layering and integration are connected, but each stage has a different purpose.

| Comparison | Placement | Layering | Integration |

| Main purpose | Introduce illicit funds into the system. | Hide the source, ownership, or movement. | Make laundered funds appear legitimate. |

| Simple phrase | Put the money in. | Hide the trail. | Use the money as clean wealth. |

| Typical activity | Cash deposits, currency exchange, monetary instruments. | Wire transfers, shell companies, trade, asset and virtual asset movement. | Real estate, business investment, luxury assets, dividends, loans. |

| AML risk focus | Source of funds and unusual cash activity. | Transaction pattern, beneficial ownership, complexity, jurisdiction risk. | Source of wealth and legitimacy of asset ownership. |

| Common red flag | Large cash activity inconsistent with profile. | Complex transactions without clear purpose. | Funds used to buy assets with unclear source of wealth. |

Layering is about hiding the trail. Integration is about using the funds once they look legitimate. Layering makes integration easier because once funds have moved through several layers, criminals may claim the money came from business activity, asset sale proceeds, investment returns, or loan repayments.

The easiest way to remember the difference is this: placement introduces the money, layering hides the trail, and integration makes the money appear legitimate.

How Layering in Money Laundering Works

Layering works by creating complexity. Criminals move funds through several steps so that investigators, compliance officers, financial institutions, and regulated businesses cannot easily connect the funds to their original criminal source. A typical layering process may look like this:

- Illicit funds are introduced into the financial system.

- The funds are transferred to another account or entity.

- The money is split into different amounts or moved through several counterparties.

- Funds are converted into another currency, an asset, an investment, a precious metal, real estate, or a virtual asset.

- The funds are moved across jurisdictions or through third parties.

- Documents are created to make the transactions appear legitimate.

- The funds are later integrated into the economy as business income, loan repayment, asset sale proceeds, investment returns, or property ownership.

The purpose is not always to make each transaction look perfect. The purpose is to make the overall money trail difficult to understand, verify, and challenge.

Common Methods of Layering in AML

Criminals may use a single method or combine several to layer illicit funds.

| Method of layering | How it works | AML concern |

| Multiple bank transfers | Funds are moved through several accounts. | Breaks the audit trail and hides the original source. |

| Cross border transfers | Money is sent through different countries. | Adds jurisdictional complexity and reduces visibility. |

| Shell companies | Companies with little or no genuine activity are used. | Hides beneficial ownership and control. |

| Trade based money laundering | Invoices, goods, shipment values, or trade documents are manipulated. | Makes value movement look like normal trade. |

| Real estate transactions | Property is bought, sold, transferred, or funded through unclear sources. | Converts illicit funds into high value assets. |

| Precious metals and stones | Gold, diamonds, jewellery, or other high value items are bought and resold. | Portable assets can store and move value. |

| Virtual assets | Funds move through wallets, exchanges, tokens, or chains. | Creates complex digital movement that needs specialist monitoring. |

| Loans and repayments | Fake, circular, or related party loans are created. | Makes funds appear as legitimate debt repayment. |

| Investment products | Funds are moved through securities, funds, or insurance. | Adds financial complexity and creates a paper trail. |

| Professional intermediaries | Lawyers, accountants, auditors, or company service providers are misused. | Adds credibility and distance from the criminal source. |

| Currency conversion | Funds are converted into another currency. | Makes tracing more difficult and may conceal source. |

| Purchase and resale of assets | Assets are bought and later sold. | Converts criminal funds into apparently legitimate sale proceeds. |

Examples of Layering in Money Laundering

Example 1: Shell company transfers

A customer receives funds into a company account from an unrelated third party. The funds are quickly transferred to another company in a different jurisdiction. The customer gives a broad explanation, such as consulting services, but cannot provide contracts, invoices, delivery evidence, or a clear commercial purpose.

Why this may be layering: the transaction chain may be designed to separate the funds from their true source and hide the person who controls them.

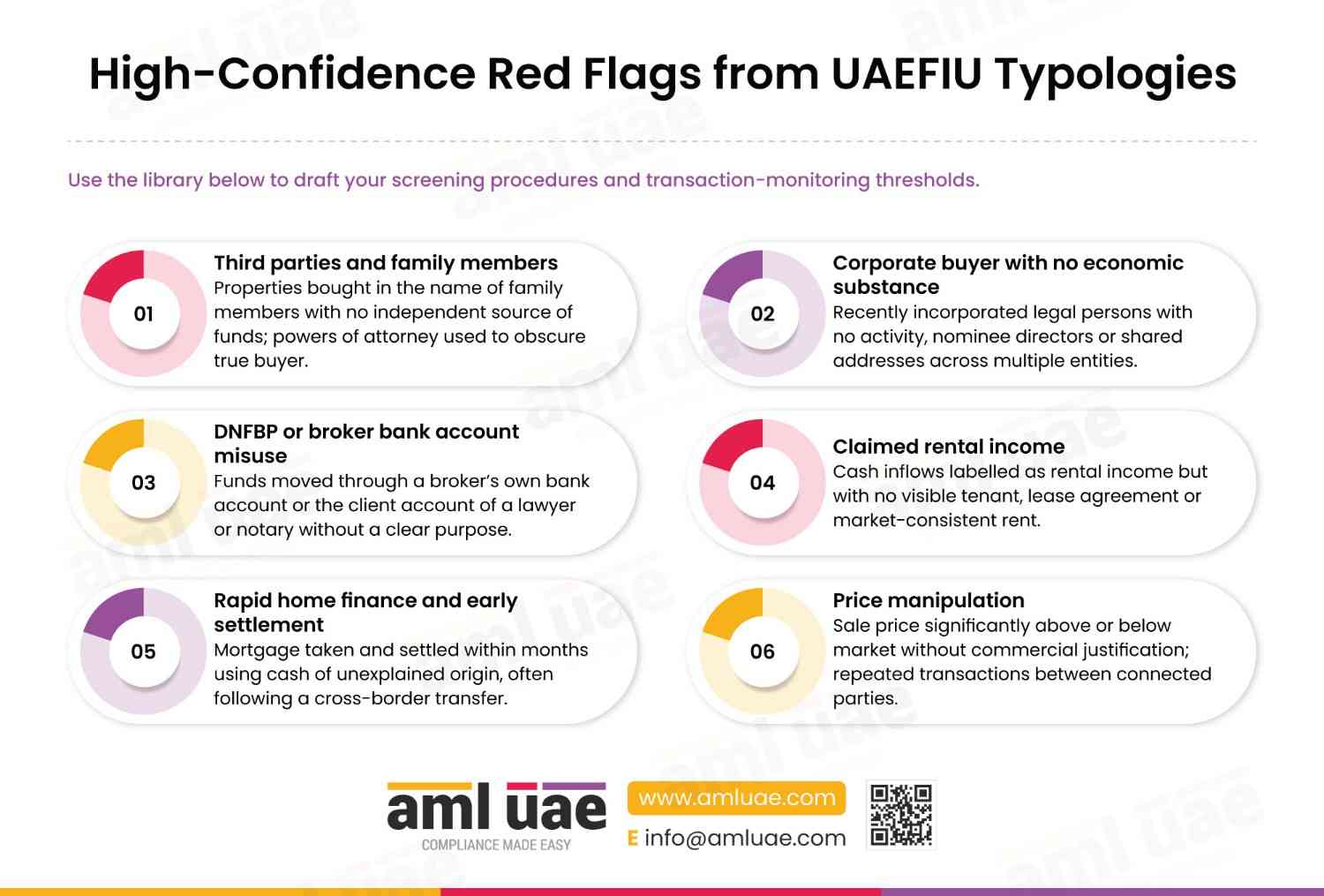

Example 2: Real estate purchase through unclear funds

A buyer uses a newly formed company to purchase property. The funds come from multiple accounts, some of which are overseas, and the beneficial owner is difficult to identify. The buyer is unwilling or unable to explain the source of funds or wealth.

Why this may be layering: real estate can be used to convert illicit funds into an apparently legitimate asset.

Example 3: Precious metals and stones

A customer makes repeated purchases of gold, diamonds, or jewellery through different payment sources. The goods are later sold or transferred, and the customer claims the proceeds are legitimate business income.

Why this may be layering: high-value portable assets can be used to move, store, and convert value while hiding the source of funds.

Example 4: Virtual asset movement

Funds are converted into virtual assets, transferred across multiple wallets, exchanged into another token, and later converted back into fiat currency.

Why this may be layering: the movement of value across wallets, platforms, tokens, and jurisdictions can make the money trail harder to follow.

Example 5: Circular loan arrangement

Company A sends money to Company B. Company B sends the money to Company C. Company C later sends the money back to Company A as a loan repayment or investment return. The companies are connected, but the customer does not clearly explain the commercial purpose.

Why this may be layering: circular movement of funds may create an artificial paper trail, making illicit money appear to come from a legitimate transaction.

Example 6: Multiple account movement

Activities performed by criminals like changing the nature of the assets, i.e. changing cash into casino chips, gold into real estate, etc., indicate layering. Further, t

A customer opens several accounts or uses accounts held by related parties. Funds are deposited into one account, transferred through several others, then withdrawn or used for asset purchases.

Why this may be layering: multiple account movement can make it harder to identify where the money came from and who controls it.

hey also engage in carrying out a series of transactions to facilitate cross-border money transfer, to complicate the detection of an illicit source.

Layering vs Structuring

Layering and structuring are related, but they are not the same. Layering is a stage of money laundering. Structuring is a technique where transactions are split into smaller amounts to avoid reporting thresholds, monitoring rules, or detection.

| Term | Meaning | Example | Relationship to layering |

| Layering | Moving or converting funds to hide their source. | Transferring funds through several companies and accounts. | Main money laundering stage. |

| Structuring | Splitting transactions into smaller amounts to avoid detection. | Repeated smaller deposits instead of one large deposit. | A technique used during placement or layering. |

| Smurfing | Using multiple people or accounts to structure activity. | Several individuals deposit smaller amounts for one controller. | A form of structuring. |

| Integration | Reintroducing funds as apparently legitimate wealth. | Buying property or investing in a business. | Usually follows placement and layering. |

Key takeaway: structuring and smurfing are techniques. Layering is a stage. They are connected, but they should not be treated as the same thing.

Red Flags of Layering in Money Laundering

A red flag does not automatically prove money laundering. It means the transaction, customer, or activity should be reviewed and, where necessary, escalated in accordance with the organisation’s AML and CFT procedures.

| Red flag | What to review |

| Rapid movement of funds in and out of an account | Business rationale, source of funds, customer profile. |

| Multiple transfers with no clear economic purpose | Relationship between parties and transaction documents. |

| Use of shell companies or complex ownership structures | Ultimate beneficial owner and control structure. |

| Unusual cross border transfers | Jurisdiction risk and reason for overseas movement. |

| Third party payments unrelated to the customer | Whether the payer or recipient has a legitimate role. |

| Transactions inconsistent with customer income or business | Customer due diligence and expected activity profile. |

| Purchase and resale of high value assets | Source of funds, asset valuation, and counterparty relationship. |

| Circular transactions between related parties | Whether funds move without genuine commercial substance. |

| Repeated transactions below monitoring thresholds | Possible structuring or smurfing. |

| Customer avoids questions or provides vague documents | Need for enhanced due diligence or escalation. |

| Documents do not match the transaction pattern | Possible false or incomplete explanation. |

| Funds move through many accounts before being used | Possible attempt to create artificial layers. |

Businesses should treat these red flags as indicators for review. The decision to escalate, reject, continue, apply enhanced due diligence, or report should be documented based on the facts of the case.

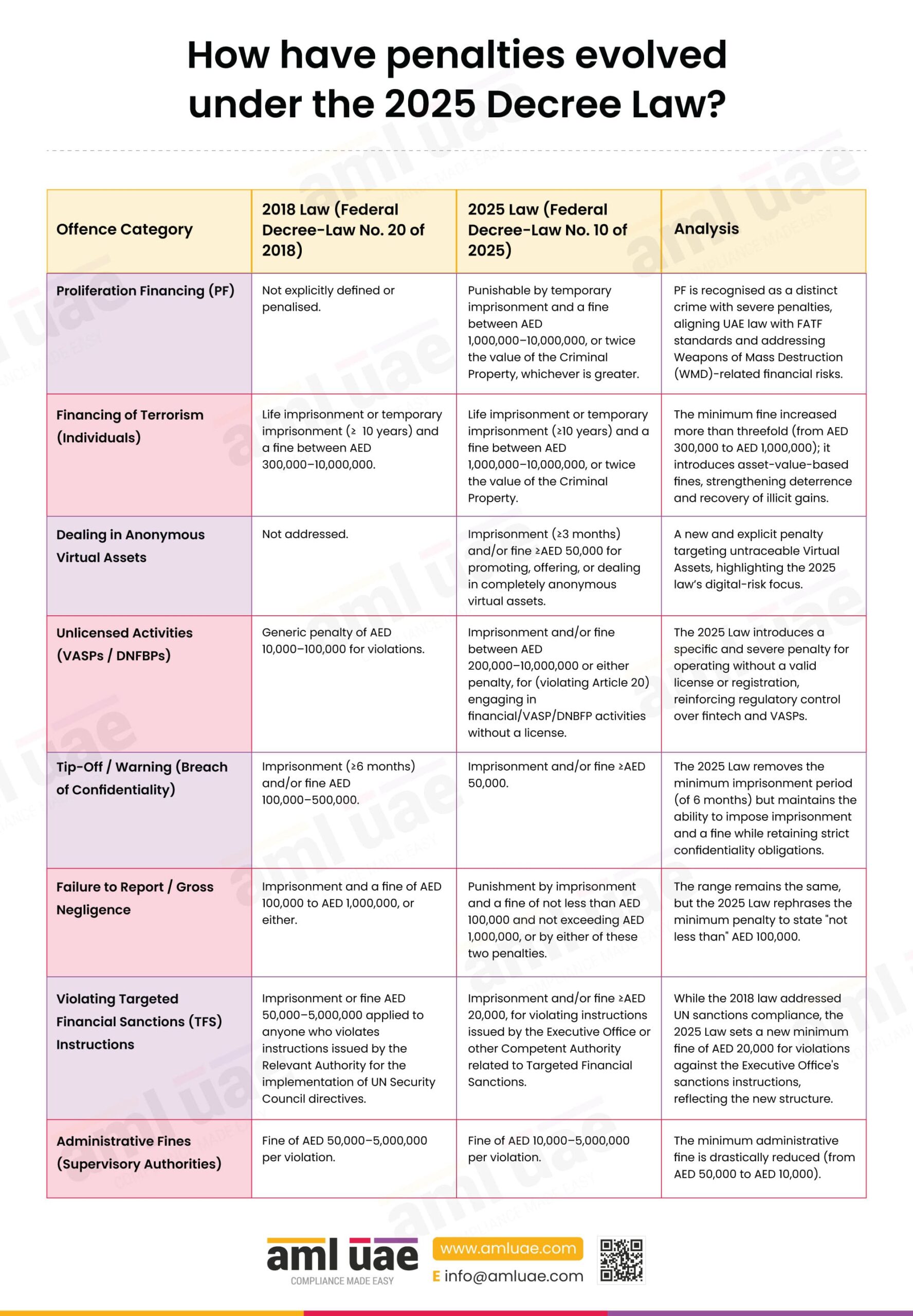

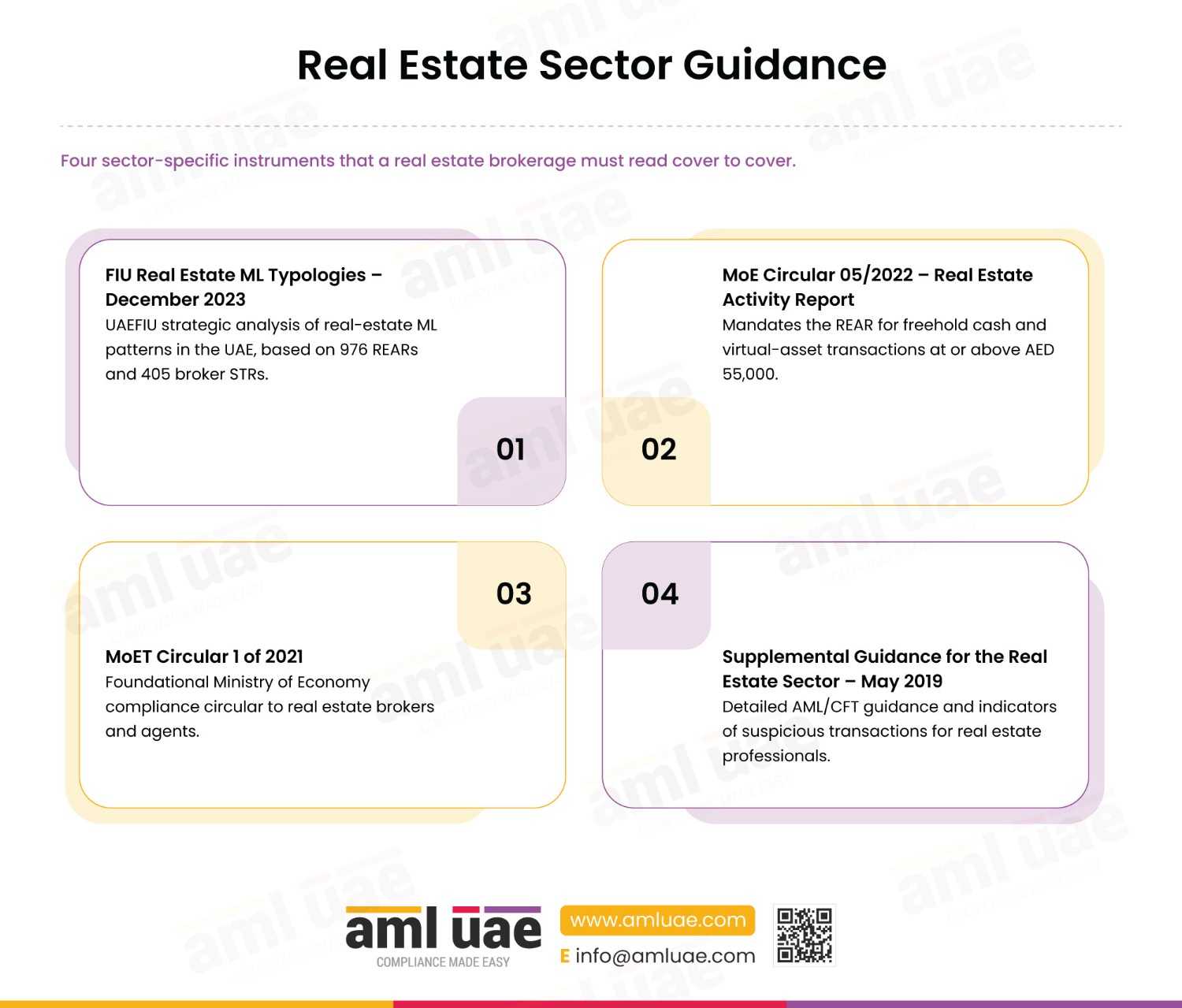

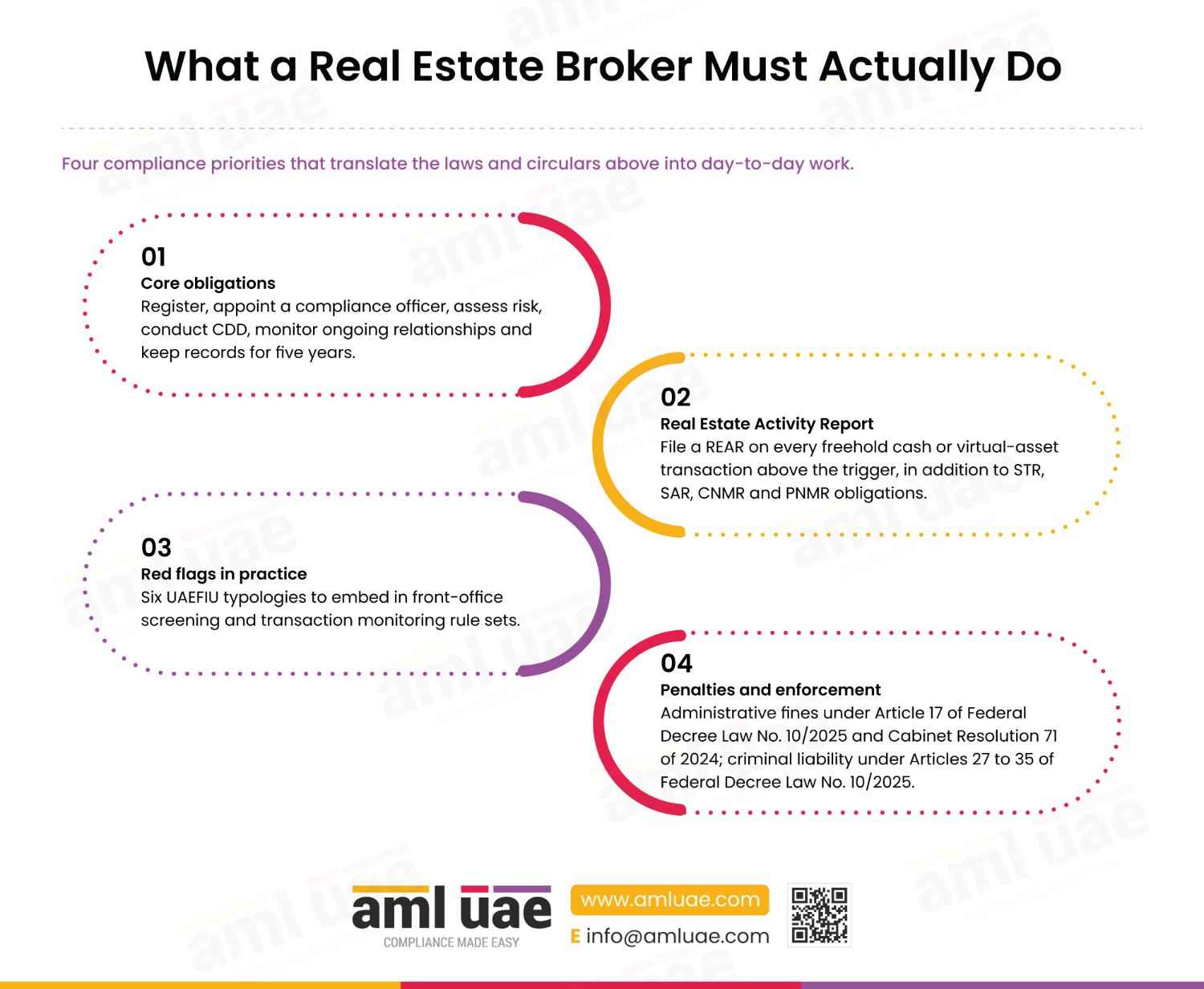

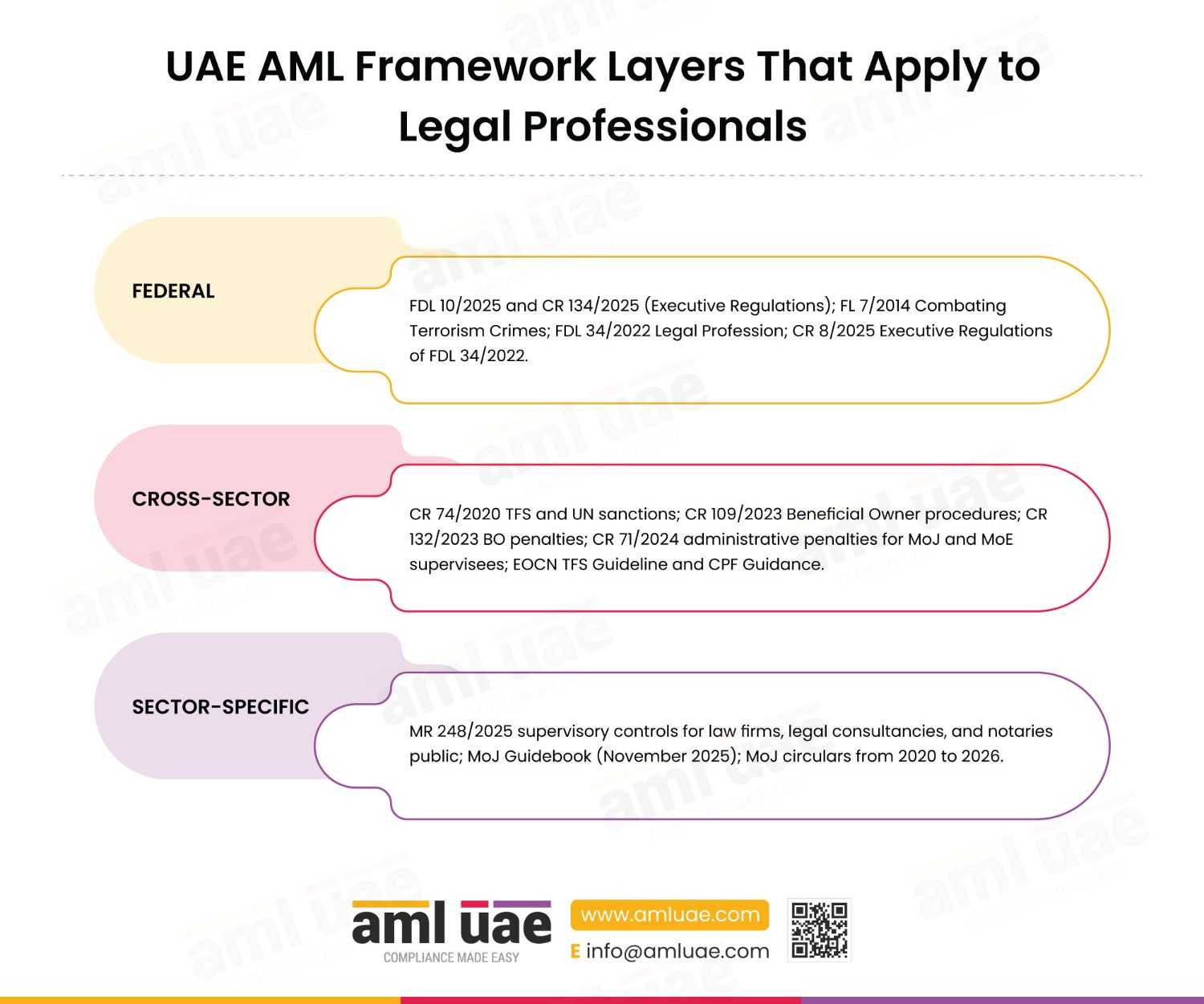

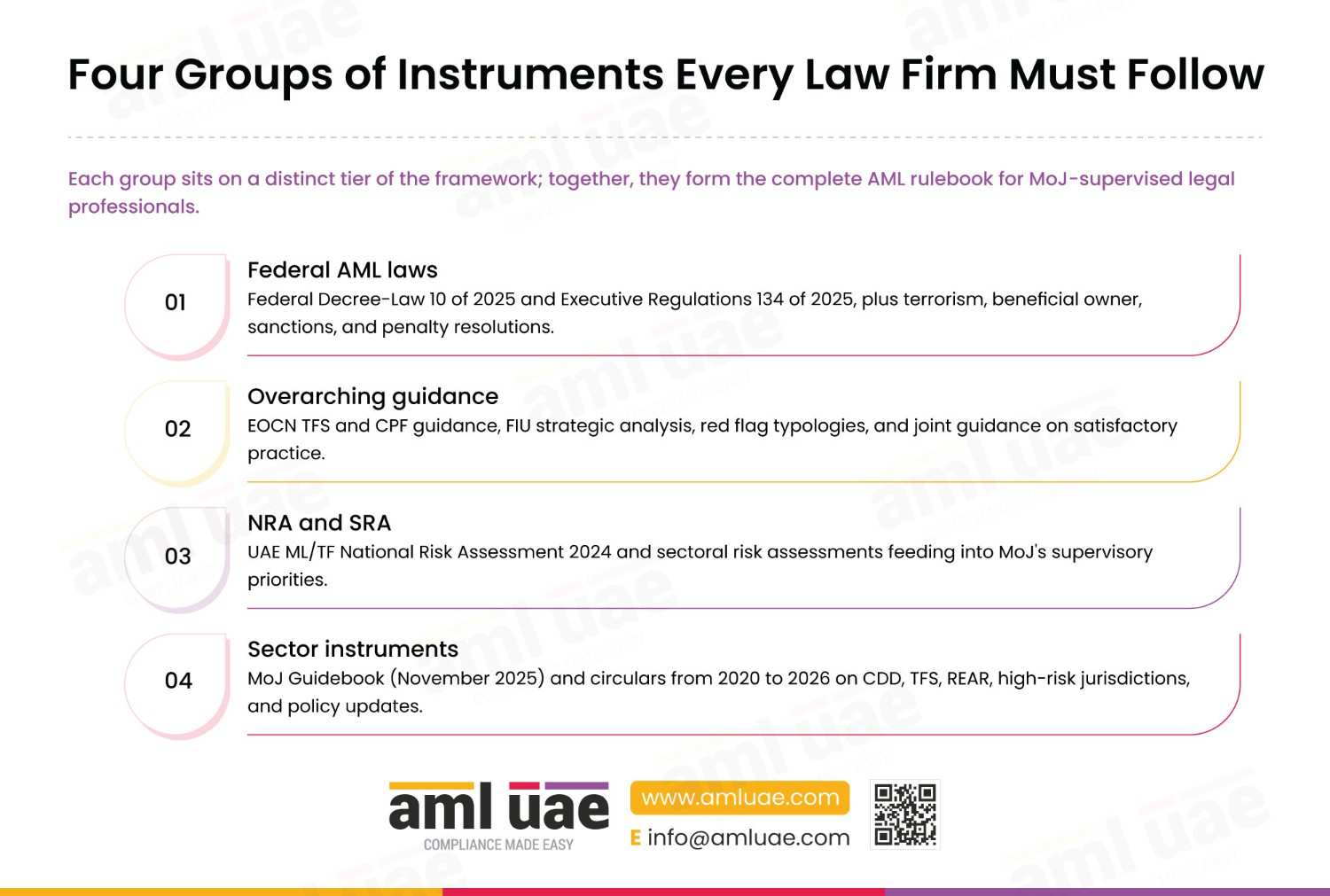

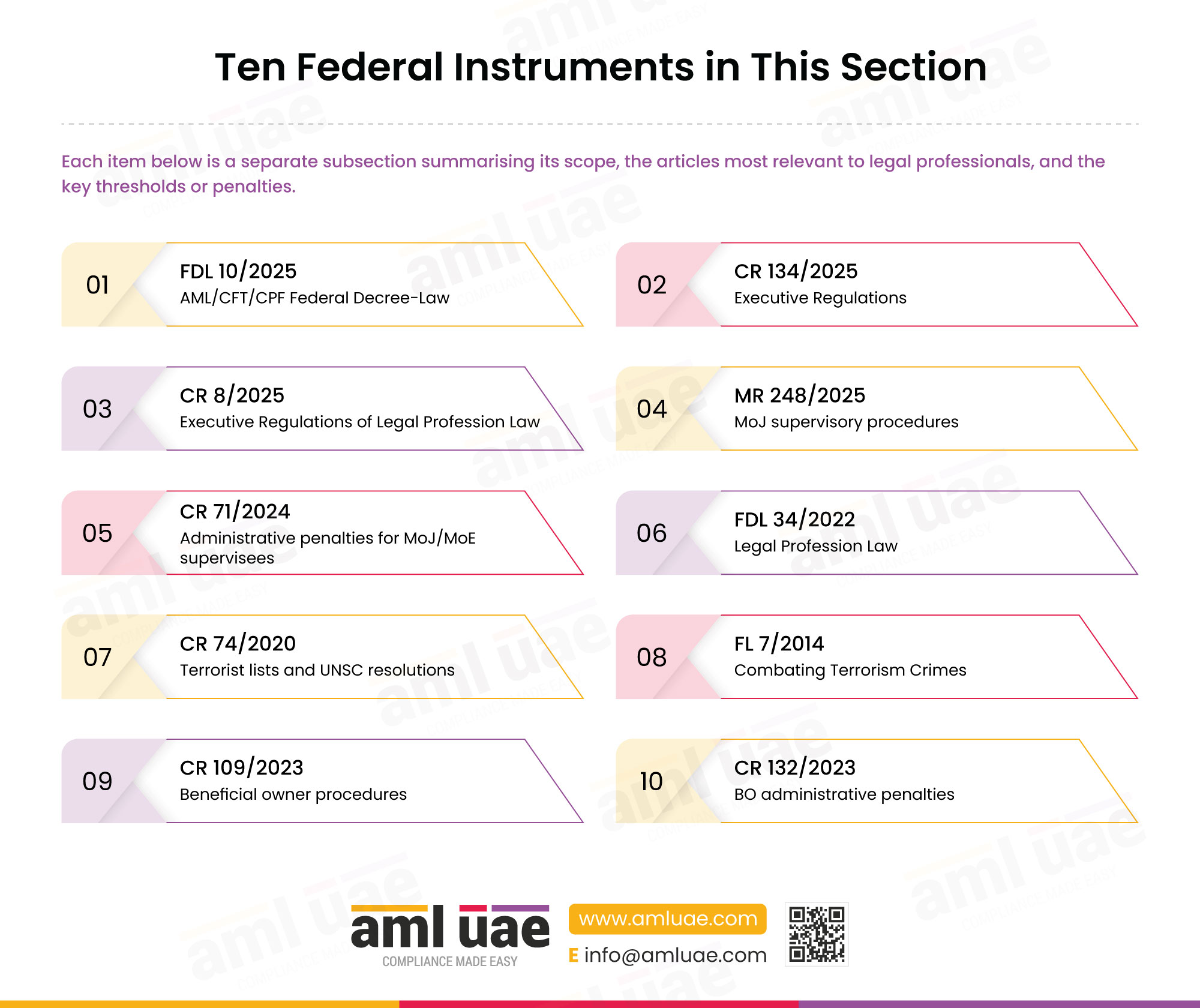

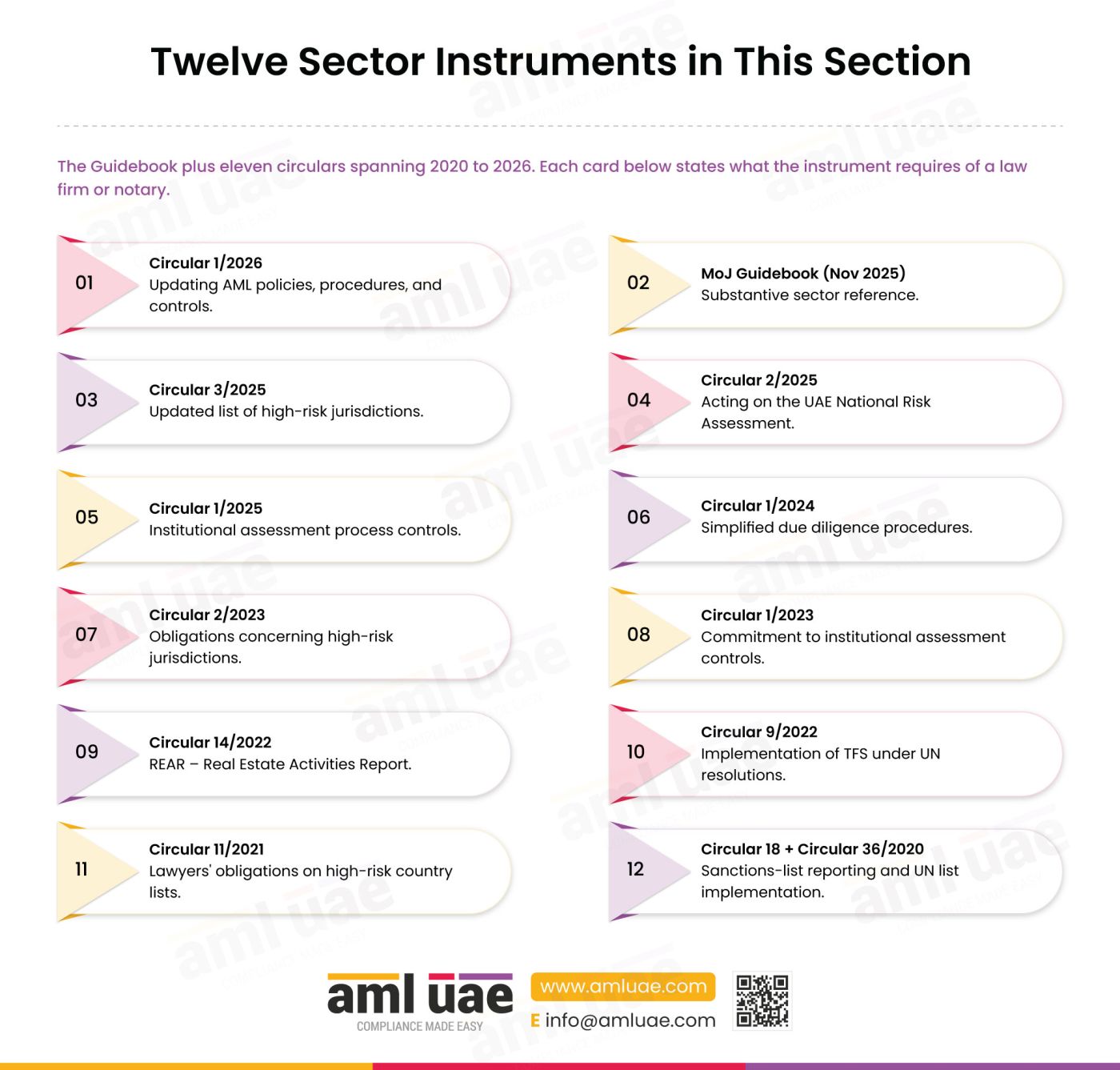

Layering Risks for UAE-Regulated Entities

In the UAE, AML obligations apply to financial institutions, designated non-financial businesses and professions, virtual asset service providers, and non-profit organisations. Federal Decree by Law No. 10 of 2025 is the primary statute on anti-money laundering, combating the financing of terrorism, and the financing of the proliferation of weapons of mass destruction. It was published on 30 September 2025 and took effect about two weeks later, replacing Federal Decree-Law No. 20 of 2018. Cabinet Resolution No. 134 of 2025 sets out the executive regulations under that statute. It was published on 15 November 2025 and took effect on 14 December 2025.

Legal Basis in the UAE

- Primary statute: Federal Decree by Law No. 10 of 2025 on anti money laundering, combating the financing of terrorism, and proliferation financing.

- Executive regulations: Cabinet Resolution No. 134 of 2025.

- Designated sectors: six categories of designated non-financial business and profession under Cabinet Resolution No. 134 of 2025, Article 3: commercial gaming operators; real estate brokers and agents; dealers in precious metals and stones; lawyers, notaries and other independent legal professionals and independent accountants; trust and company service providers; and a sixth, catch-all category that allows further businesses to be designated.

- Reporting: suspicious transactions go to the UAE Financial Intelligence Unit within the Central Bank, through goAML (Federal Decree by Law No. 10 of 2025, Articles 11 and 18; Cabinet Resolution No. 134 of 2025, Article 18).

| UAE sector | Layering risks to monitor | Practical controls | |

| Banks and exchange houses | Rapid fund movement, cross border transfers, third party payments. | Transaction monitoring, source of funds checks, enhanced due diligence. | |

| Real estate brokers and agents | Purchases through companies, nominees, or unclear funding. | Beneficial owner verification, source of wealth checks, red flag review. | |

| Dealers in precious metals and stones | High value purchases, resale of gold or diamonds, third party payments. | Customer identification, transaction review, suspicious activity escalation. | |

| Lawyers, accountants and auditors | Misuse of client accounts, company structures, nominee arrangements. | Beneficial ownership checks, engagement risk assessment, matter monitoring. | |

| Trust and company service providers | Shell entities, nominee shareholders, incorporation of entities with unclear purpose, complex control structures. | Beneficial owner verification, purpose of entity checks, ongoing monitoring. | |

| Virtual asset service providers | Wallet hopping, chain hopping, high risk wallets, rapid conversion. | Wallet screening, blockchain analytics, transaction monitoring. | |

Note: the six designated DNFBP categories are set by Cabinet Resolution No. 134 of 2025, Article 3.

Suspicious transactions are reported immediately and directly to the UAE Financial Intelligence Unit through the goAML portal (Federal Decree by Law No. 10 of 2025, Articles 11 and 18; Cabinet Resolution No. 134 of 2025, Article 18). These designated non-financial businesses and professions are supervised by different authorities depending on the sector, for example the Ministry of Economy and Tourism for real estate brokers, dealers in precious metals and stones, accountants and corporate service providers; the Ministry of Justice for lawyers and other independent legal professionals; and the General Commercial Gaming Regulatory Authority for commercial gaming. Each is required to register and report on goAML. The same portal is used for both suspicious transaction reports and activity-based reports.

How Businesses can Detect Layering

Businesses can detect layering by reviewing the full customer and transaction picture rather than looking at transactions in isolation.

1. Know the customer

Customer due diligence should establish who the customer is, what the customer does, who owns or controls the customer, and what level of activity is expected. If the transaction pattern does not match the customer profile, the business should investigate.

| Question | Why it matters |

| Who is the customer? | Confirms identity and risk profile. |

| What does the customer do? | Helps assess whether activity is expected. |

| Who owns or controls the customer? | Identifies the beneficial owner. |

| What is the expected transaction pattern? | Helps detect unusual activity. |

| Is the transaction consistent with the profile? | Identifies possible suspicious behaviour. |

2. Verify source of funds and source of wealth

The source of funds explains where the money for a transaction came from. The source of wealth explains how the customer built their overall wealth. For higher-risk customers or unusual transactions, both may be relevant.

| Check | Meaning |

| Source of funds | Where the money for this transaction came from. |

| Source of wealth | How the customer generated overall wealth. |

| Supporting documents | Evidence that supports the customer explanation. |

| Consistency check | Whether the explanation matches the customer profile. |

A customer explanation should be reasonable, specific, and supported by documents. Vague explanations such as business income, family funds, or investment returns may not be enough if the transaction is high-risk or unusual.

3. Monitor transaction behaviour

Transaction monitoring should identify unusual volume, speed, frequency, value, destination, counterparties, and transaction purpose. Layering often appears as a pattern rather than a single suspicious transaction.

| Factor | What to review |

| Speed | Are funds moving in and out quickly? |

| Frequency | Are there repeated transactions without clear purpose? |

| Value | Does the transaction value match the customer profile? |

| Counterparty | Are the payer and recipient connected to the stated purpose? |

| Jurisdiction | Are high risk or unrelated countries involved? |

| Purpose | Is there a clear commercial reason? |

| Documentation | Do documents support the transaction? |

4. Review beneficial ownership

Complex ownership structures, nominee arrangements, or unexplained control by third parties may indicate that the true owner is being hidden.

| Beneficial ownership issue | Risk |

| Multiple layers of companies | True ownership may be hidden. |

| Nominee shareholders or directors | Control may sit with another person. |

| Ownership in high risk jurisdictions | Reduced transparency. |

| No clear business purpose for the structure | Possible shell company risk. |

| Customer avoids beneficial owner questions | Possible concealment. |

5. Apply enhanced due diligence where risk is high

Enhanced due diligence may be needed for high-risk customers, high-risk jurisdictions, politically exposed persons, unusual transactions, complex structures, or activity that does not match the customer profile.

| Enhanced due diligence measure | Purpose |

| Additional identity checks | Confirms customer identity. |

| Beneficial owner verification | Confirms who owns or controls the customer. |

| Source of funds review | Checks where transaction funds came from. |

| Source of wealth review | Checks how the customer generated wealth. |

| Senior management approval | Adds oversight for high risk cases. |

| More frequent monitoring | Tracks ongoing risk. |

| Additional documents | Supports or challenges the customer explanation. |

6. Escalate suspicious activity

If suspicion remains after review, the matter should be escalated to the compliance officer or money laundering reporting officer in line with internal AML and CFT procedures. Where reporting is required, suspicious activity or suspicious transactions should be reported through the appropriate channel, such as goAML in the UAE.

How to Prevent Layering in Money Laundering

A single control cannot prevent layering. Businesses should use a risk-based AML framework that combines customer due diligence, transaction monitoring, staff awareness, escalation, and reporting.

| AML control | How it helps prevent or detect layering |

| Business risk assessment | Identifies where the business is exposed to money laundering risk. |

| Customer risk assessment | Identifies customers who need closer monitoring. |

| Customer due diligence | Confirms identity, activity, ownership, and expected behaviour. |

| Enhanced due diligence | Applies deeper checks to high risk relationships. |

| Transaction monitoring | Detects unusual movement, speed, value, or counterparties. |

| Sanctions and PEP screening | Identifies designated and politically exposed persons. |

| Beneficial ownership checks | Reveals who ultimately owns or controls the customer. |

| Source of funds checks | Tests whether transaction funds have a legitimate explanation. |

| Source of wealth checks | Tests whether customer wealth is reasonable and supported. |

| Staff training | Helps employees recognise and escalate suspicious patterns. |

| Independent AML review | Tests whether controls are working effectively. |

| STR and SAR reporting procedures | Ensures suspicious activity is escalated and reported correctly. |

| Record keeping | Supports auditability and regulatory review. |

The objective is to identify suspicious patterns early, ask the right questions, document decisions, and report suspicious activity where required.

What Should a UAE Business do If It Detects Red Flags of Layering?

If a UAE business detects possible layering, it should not ignore the activity or rely only on the customer’s verbal explanation. The business should follow its AML and CFT policy and apply a documented review process.

- Review the customer profile, risk rating, and expected activity.

- Check the transaction purpose, counterparties, jurisdictions, and supporting documents.

- Request source-of-funds or source-of-wealth information where appropriate.

- Assess whether the activity has a reasonable commercial or lawful explanation.

- Escalate the matter internally to the compliance officer or money laundering reporting officer.

- Decide whether enhanced due diligence, rejection, exit, account restrictions, or reporting is required.

- Keep records of the review, decision, and supporting evidence.

- File a suspicious transaction report or suspicious activity report where required.

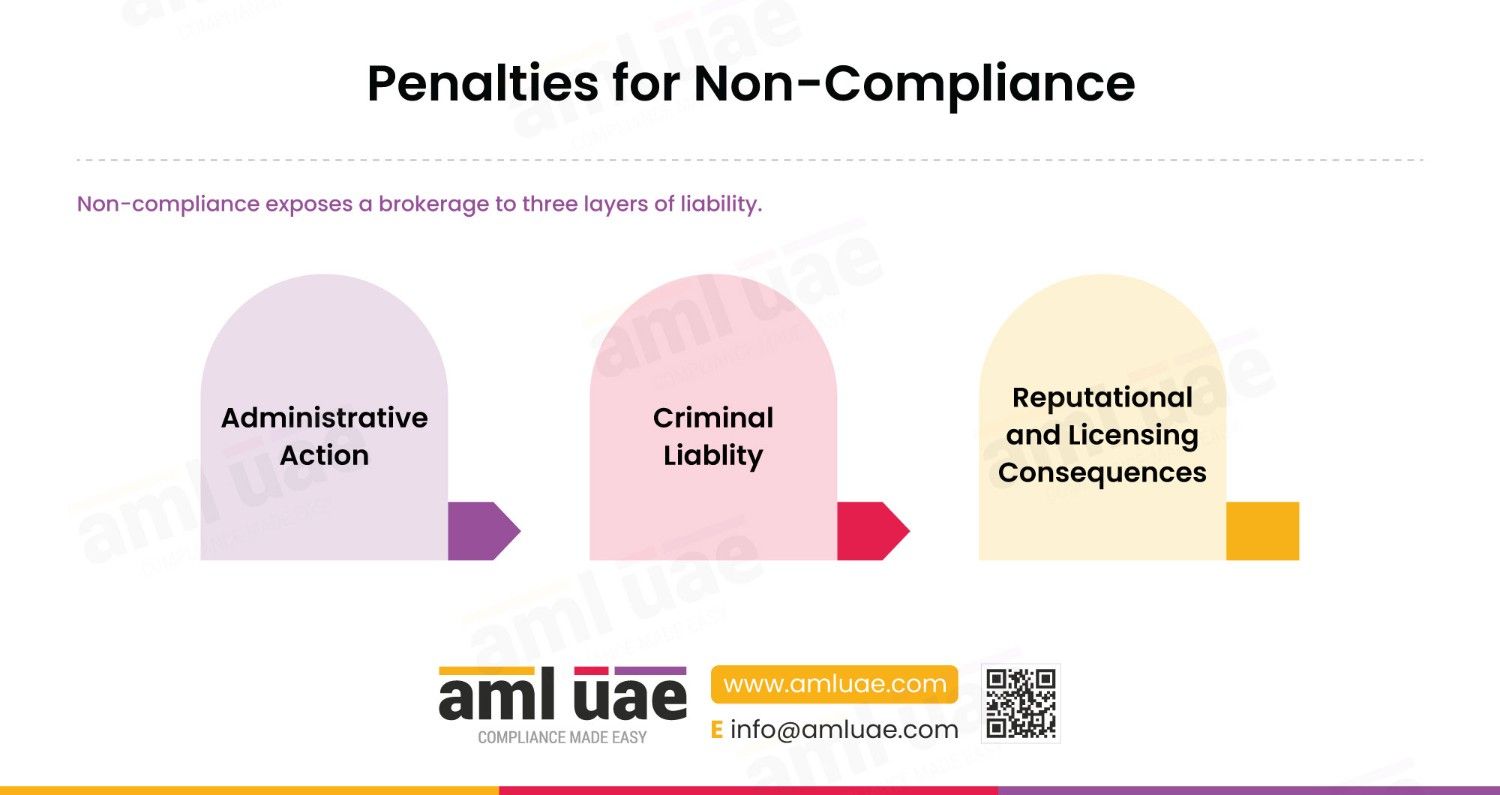

Do not tip off the customer. Do not inform the customer that a suspicious transaction report has been or may be filed, or that an investigation may be underway. This prohibition on tipping off is a legal requirement (Cabinet Resolution No. 134 of 2025, Article 19), and a breach carries criminal penalties (Federal Decree by Law No. 10 of 2025, Article 29). Internal escalation and external reporting should be handled confidentially.

Practical AML UAE Layering Checklist

Use this checklist when reviewing transactions that may involve layering.

| Question | Yes or No |

| Is the transaction consistent with the customer known business or income? | |

| Is the source of funds clear and supported by documents? | |

| Is the source of wealth reasonable for the customer profile? | |

| Are the counterparties connected to the stated transaction purpose? | |

| Are any high risk jurisdictions involved? | |

| Is there a clear commercial reason for the transaction structure? | |

| Are funds moving quickly in and out without a business reason? | |

| Are shell companies, nominees, or complex ownership involved? | |

| Are payments being made by or to unrelated third parties? | |

| Has the customer avoided questions or submitted weak documentation? | |

| Are the transaction documents consistent with the pattern? | |

| Has the customer risk rating been reviewed? | |

| Should enhanced due diligence be applied? | |

| Should the matter be escalated to the compliance officer or MLRO? | |

| Should a suspicious transaction or activity report be considered? |

This checklist is a practical review tool, not a substitute for legal advice or the organisation’s AML and CFT policies and procedures.

Quick Answers About the Layering Stage

Which money laundering stage refers to the separation of illicit proceeds from their source?

The layering stage refers to the separation of illicit proceeds from their source. This is done by creating complex layers of financial transactions, accounts, entities, assets, or jurisdictions, making the origin of the funds harder to identify.

Which stage involves multiple transactions designed to separate the money from its source?

The layering stage involves multiple transactions designed to separate illicit money from its source. These may include transfers, conversions, purchases, withdrawals, deposits, movement through different accounts, or movement through different jurisdictions.

What is the main goal of the layering stage in money laundering?

The main goal of the layering stage is to hide the origin of illicit funds and break the audit trail, so that banks, regulators, businesses, and law enforcement agencies cannot easily trace the money back to criminal activity.

Which of the following are methods of the layering stage of money laundering?

Common methods of layering include multiple bank transfers, cross-border transactions, currency conversions, shell companies, trade-based transactions, purchases and resales of high-value assets, virtual asset transfers, and movement through multiple financial institutions.

In the context of money laundering, layering refers to the act of what?

In the context of money laundering, layering refers to moving, converting, transferring, splitting, or restructuring illicit funds through complex transactions to disguise their origin, ownership, movement, or destination.

What stage of money laundering is the most complex and difficult to detect?

Layering is often considered the most complex and difficult stage to detect, because it may involve several transactions, accounts, entities, jurisdictions, assets, and documents. The suspicious pattern may only become clear after the full transaction trail is reviewed.

What is the correct sequence of stages of money laundering?

The commonly used sequence is placement, layering, and integration. Placement introduces illicit funds into the financial system, layering hides the trail, and integration makes the funds appear legitimate.

At which stage is money laundering relatively easy to detect?

Money laundering is often easier to detect at the placement stage, because illicit funds are first introduced into the financial system. Unusual cash deposits or unexplained funds may be more visible before the funds are moved through layers of transactions.

How AML UAE Can Help

AML UAE helps businesses build and strengthen AML and CFT compliance frameworks designed to identify, assess, monitor, and report money laundering risks, including layering risks.

| AML support area | How it helps |

| AML and CFT business risk assessment | Identifies exposure to money laundering, terrorist financing, and proliferation financing risks. |

| Customer risk assessment methodology | Helps classify customers based on risk. |

| AML and CFT policies and procedures | Documents how the business manages AML obligations. |

| Customer due diligence framework | Helps verify customers and understand expected activity. |

| Enhanced due diligence framework | Applies stronger checks for higher risk customers and transactions. |

| Transaction monitoring rules | Helps identify suspicious layering patterns. |

| Red flag indicators | Helps employees identify unusual behaviour. |

| Suspicious transaction escalation process | Guides internal review and reporting decisions. |

| goAML registration and reporting support | Assists with reporting readiness. |

| AML training | Helps employees understand risks and responsibilities. |

| Independent AML compliance review | Tests whether controls are working effectively. |

A strong AML framework helps regulated entities detect suspicious patterns early, document decisions properly, and meet their AML and CFT obligations with greater confidence.

Need help identifying layering risks in your business?

Speak with AML UAE to review your AML and CFT controls, red flags, transaction monitoring framework, and suspicious activity escalation process.

Let us together fight money laundering by preventing the layering of illicit funds

This article has been prepared with reference to the following sources, verified against the UAE AML law library.

- Federal Decree by Law No. 10 of 2025 on Anti Money Laundering, and Combating the Financing of Terrorism and Proliferation Financing. Published in the UAE Official Gazette on 30 September 2025, in force from about 14 October 2025.

- Cabinet Resolution No. 134 of 2025 on the Executive Regulations of Federal Decree by Law No. 10 of 2025. Published 15 November 2025, in force from 14 December 2025. UAE Official Gazette

- UAE Financial Intelligence Unit and goAML reporting, and Ministry of Economy and Tourism guidance on designated non-financial businesses and professions registration. moec.gov.ae

- FATF guidance and materials on the money laundering cycle of placement, layering and integration. fatf-gafi.org

FAQs about Layering on Money Laundering

What is layering in money laundering?

Layering is the stage in which illicit funds are moved through complex transactions, accounts, entities, assets, or jurisdictions to conceal their criminal origin. It is usually the second stage, after placement and before integration.

What is layering in money laundering terms?

It is the process of separating illicit funds from their criminal source by moving, converting, or transferring them through multiple transactions, accounts, entities, assets, or jurisdictions.

What is layering in AML?

In AML, layering refers to using complex transactions or structures to conceal the source, ownership, movement, or destination of illicit funds. It is detected through transaction monitoring, customer due diligence, source-of-funds checks, beneficial ownership review, and jurisdiction risk assessment.

What are the three stages of money laundering?

The three stages of money laundering are:

- Placement

- Layering and

- Integration

Why is layering considered to be the most difficult stage of money laundering to detect?

Layering is the second stage of money laundering. What makes layering in money laundering difficult to detect is the way it is broken down into smaller transactions and the conversion of money from one form to another.

What is an example of layering in money laundering?

Transferring illicit funds through several bank accounts and companies in different jurisdictions, then using the funds to buy property, precious metals, securities, or virtual assets. This creates distance between the funds and their criminal source.

What is the second stage of money laundering?

Layering, also known as structuring is the second stage of money laundering.

What is layering in banking?

Layering in banking is the suspicious movement of funds through multiple accounts, transfers, products, customers, or jurisdictions to hide the source or ownership of money. Banks often detect it through transaction monitoring and customer profile reviews.

What is layering in financial crimes?

Layering is the second stage in money laundering. It is a structuring process in which criminally derived funds are legalized and their ownership and source is disguised.

What is another word for layering?

Structuring is the another word for layering.

What is the process of layering?

Layering is structuring a transaction in such a way that the orgin of the criminal proceeds is disguised for the purpose of money laundering.

How to identify layering in the fight against money laundering?

Several red flags indicate the layering of funds in money laundering. Banking transactions involving large cash deposits into various banks, international bank transfers, investment and resell of jewellery, art, and other high-value items, fund transfer using shell companies, etc., indicates that the funds are being layered to make the detection of their origin as difficult as possible.

What is the main goal of the layering stage of money laundering?

The main goal of the layering stage of money laundering is to make the detection of the source of illicit money as difficult as possible.

What is the difference between placement and layering in money laundering?

Placement is the first stage, where illegal funds are introduced into the financial system through small deposits or cash purchases. Layering is the second stage, where those funds are moved through complex transactions such as trusts, shell companies, etc. to hide their criminal origin.

In simple terms: placement puts the money in; layering hides its trail.

What is called layering?

Layering is one of the stages in money laundering where the launderer makes numerous transactions to take the illegal proceeds far from their original source. Launderers layer illicit money with several transactions to hide its source.

What are the 4 stages of money laundering?

The four stages in the money laundering process are placement, layering, integration, and spending. At the placement stage, illicit funds are introduced into the financial system. The stage in which money is dispersed and disguised in the system is known as layering, where complex transactions are used to hide the origin of funds. Integration refers to money re-entering the economy as apparently legitimate earnings or profits.

Which money laundering stage refers to the separation of illicit proceeds from their source by creating complex layers of financial transactions?

The stage referred to is layering. The stage in which money is dispersed and disguised in the system is known as layering, where criminals move illicitly obtained funds through multiple financial transactions to conceal their origin.

What's the main goal of the layering stage of money laundering?

The primary goal behind the layering stage is to separate the illicit proceeds from their questionable origin through layers of multiple financial transactions, making it difficult for investigators to trace money back to the original source of criminal activity.

What is the difference between placement, layering and integration?

Placement introduces illicit funds into the financial system. Layering hides their source and movement through complex transactions. Integration makes the funds appear legitimate by using them for assets, investments, or business activity.

What is the difference between layering and structuring?

Layering is a stage of money laundering. Structuring is a technique in which transactions are split into smaller amounts to avoid detection by reporting thresholds or monitoring rules. Structuring may be used during placement or layering, but it is not the same as layering.

Is smurfing the same as layering?

No. Smurfing is a structuring technique that uses multiple people, accounts, or transactions to split funds into smaller amounts. Layering is a broader stage where funds are moved or converted to hide their origin.

What are common layering red flags?

Rapid fund movement, third-party payments, shell companies, unexplained cross-border transfers, circular transactions, complex ownership, inconsistent customer activity, and repeated transactions below monitoring thresholds.

How can UAE businesses detect layering?

By applying customer due diligence, transaction monitoring, source of funds checks, beneficial ownership verification, enhanced due diligence for higher risk cases, staff training, internal escalation, and suspicious transaction reporting where required.

What should a business do if layering is suspected?

Review the customer and transaction details, collect supporting information where appropriate, escalate to the compliance officer or MLRO, document the decision, and file a suspicious transaction or activity report where required.

Share via :

About the Author

Pathik Shah

FCA, CAMS, CISA, CS, DISA (ICAI), FAFP (ICAI)

Pathik is an ACAMS-certified AML consultant specialising in governance, risk, and compliance for regulated entities in the UAE. He brings over 28 years of experience, with 1,000+ hours of AML training and 200+ advisory engagements across DNFBPs, VASPs, and FIs. He supports businesses in aligning with AML/CFT requirements from the CBUAE, DFSA, MoET, MoJ, VARA, CMA, FSRA, and FATF. Known for translating complex regulations into audit-ready procedures, Pathik enables operational clarity and compliance readiness.

Reach Out to Pathik