Pathik Shah

Last Updated: 12/09/2025

Protect your business with reliable and effective AML strategies with AML UAE.

Business Risk Assessment for VASPs: At a Glance

- Business Risk Assessment helps VASPs identify, assess and mitigate ML/TF/PF Risks.

- Covers key risk factors for VASPs: Customers, Geography, Transactions, Products/Services, Delivery Channels.

- Business Risk Assessment must be aligned with the VARA Rulebook, Federal AML/CFT Laws, UAE NRA and other sectoral risk assessments.

- VASPs must regularly update BRA to reflect new products, typologies and emerging risks.

- A Robust BRA supports stronger controls, enhanced decision making and regulator-ready compliance.

Regulator-Ready Business Risk Assessment for VASPs in UAE

A Business Risk Assessment (BRA) is a structured analytical process for Virtual Assets Service Providers (VASPs) in UAE. It assesses the nature of VASP’s business model, customer base, products, technologies and transaction patterns with an aim to determine the impact of these factors in exposing the business to financial crime risks.

The BRA facilitates identification of the inherent risks, evaluation of the already implemented control measures, calculation of the residual risks and is based on the risk appetite of VASPs. BRA provides insights into the actual Money Laundering (ML), Terrorist Financing (TF), and Proliferation Financing (PF) risks the business is exposed to.

Why VASPs Require a Structured BRA?

VASPs operate in an ecosystem where transactions move fast, across borders and often without traditional financial intermediaries. It offers a platform which covers anonymity in financial transactions. And it is a consensus that where anonymity lies, the chances of ML/TF/PF risks are higher.

Unlike traditional financial transactions, in VASPs, the activities happen without face-to-face interaction, and users may deposit or withdraw funds from anywhere in the world.

This creates a business environment where risks are not always visible on the surface. In order to get a comprehensive view of the ML/TF/PF threats, VASPs are required to undertake a structured BRA.

Business Risk Assessment through risk weighing and risk scoring provides a foretelling vision into the risk areas that are more vulnerable to the chain of financial crimes.

A well-done BRA helps a VASP break down the risk factors in a systematic way instead of relying on assumptions or scattered observations.

It ensures that the VASP get a full vision to understand where its vulnerabilities lie, how its products can be misused, which controls are working and which aren’t, and how it is exposed to on-chain threats.

Without a structured BRA, VASP is essentially operating in the dark, making decisions without a clear grasp of its own risk exposure. An efficiently conducted Business Risk Assessment not only protects the business from probable financial crimes but also ensures that resources are prioritized in a better manner, specifically in areas that are weak.

Regulatory Mandate for VASPs to Conduct BRA under AML/CFT Framework of UAE

Virtual Assets Service Providers (VASPs) in UAE are regulated and supervised by Virtual Assets Regulatory Authority (VARA). VARA issues periodic guidelines and rulebooks that VASPs are obligated to adhere.

The Virtual Assets and Related Activities Regulations 2023 recognise the Federal AML/CFT Laws (Federal Decree by Law No. (10) of 2025 Regarding Anti-Money Laundering and Combating the Financing of Terrorism and Proliferation Financing and its implementing Cabinet Decision No. (10) of 2019).

It mandates VASPs to comply with all Federal AML/CFT Laws, regulatory requirements, rules and directives with respect to VASPs’ AML/CFT obligations.

The Federal Decree by Law No. (10) of 2025 calls for a comprehensive Business Risk Assessment for VASPs to identify, assess and mitigate the ML/TF/PF within the business model.

Additionally, VARA rulebook Part III D talks about the Business Risk Assessment obligations of VASPs.

Rule III.D of VARA rulebook requires VASPs to conduct and maintain a documented and data-driven AML/CFT Business Risk Assessment in order to understand, identify and assess ML/TF risks specific to their business.

BRA must be carried out at least once every 3 months, and when there are changes in business model, products/services, customer base, technology, or new regulatory requirements. The AML/CFT policies, procedures, systems, and controls must align with the BRA, and high-risk areas must be prioritized for resource allocation.

Unsure where to start with the new AML/CFT law?

Partner with us to quickly realign your policies and procedures with the new law.

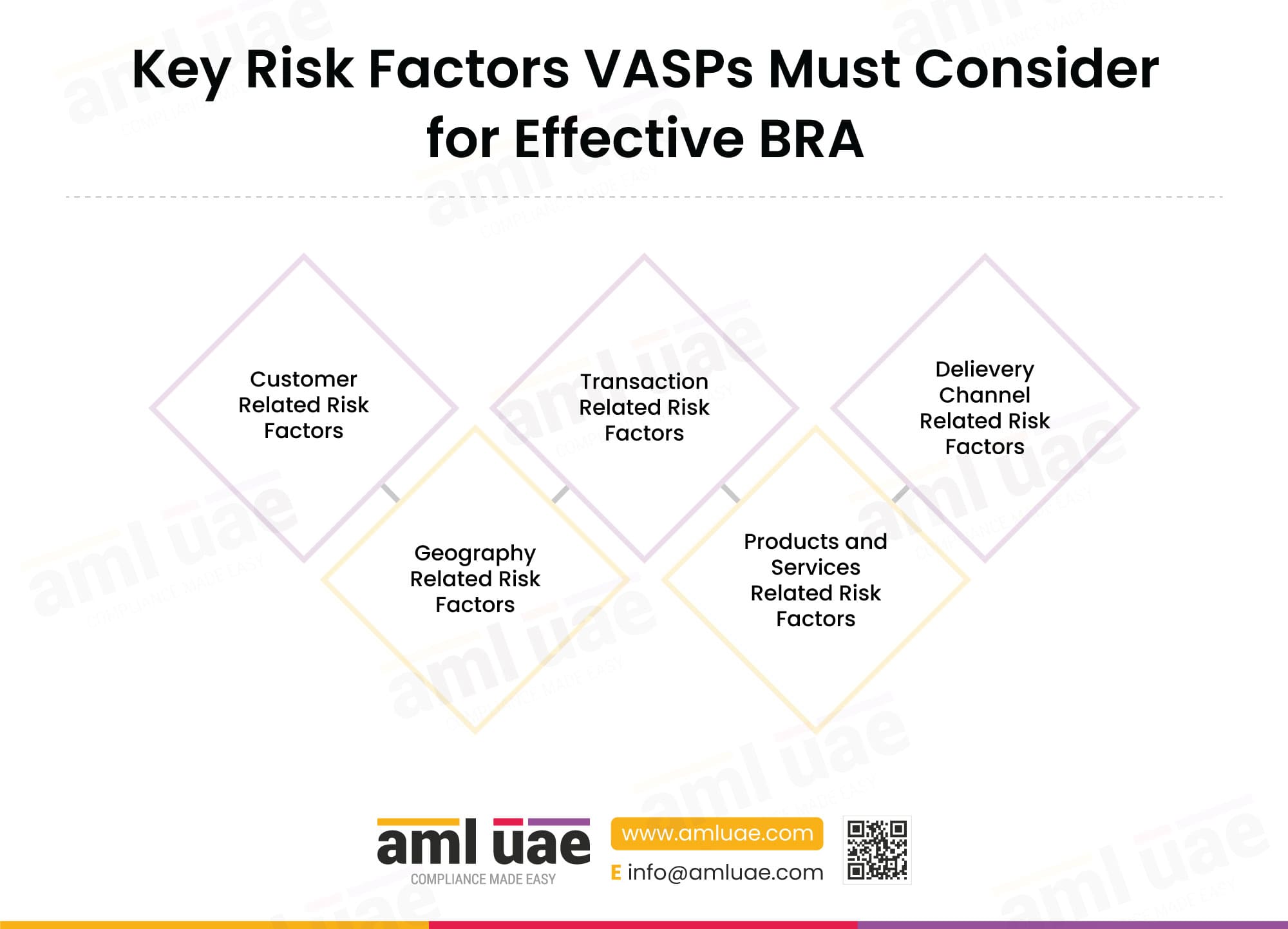

Key Risk Factors VASPs Must Consider for Effective BRA

An effective BRA starts with identifying what can expose a VASP to financial crime risks. The risk is often enveloped in the form of customers, jurisdictions, transactions, products, services and delivery channels.

Evaluating these areas helps the VASP build a realistic picture of where vulnerabilities exist. While conducting Business Risk Assessment, VASPs must consider risk factors related to these key areas.

The following infographic depicts the key risk factors VASPs must take into consideration while performing Business-Wide Risk Assessment.

Customer Related Risk Factors

While conducting Enterprise-Wide Risk Assessment (EWRA), the VASP must assess customer profiles, behavior patterns and wallet activities. Factors such as weak KYC data, customers with cloudy sources of funds, PEPs, high-net worth individuals dealing in large volumes or showing inconsistent behavior increase vulnerability.

Assessing these risks helps VASPs understand which customer segments require additional AML/CFT controls, such as Enhanced Due Diligence (EDD)to prevent misuse of the platform.

Geography Related Risk Factors

Another major key factor to consider while conducting Business-Wide Risk Assessment is to analyze VASP’s risk exposure through where customers and counterparties are located. Crypto flows are borderless, that makes the destination of originators and beneficiaries a major risk factor.

Hence, considering geographic risk in the BRA helps the VASPs to identify potential links to high-risk or sanctioned nations and jurisdictions associated with illicit crypto flows.

Transaction Related Risk Factors

In the Virtual Assets sector, the transactions are pseudonymous, which is a major risk factor for financial crime if controls are not deployed appropriately. Therefore, while conducting a comprehensive Business Risk Assessment, VASPs are required to consider transaction related risk factors.

This includes sudden spikes in transactions, irregular or unusual transaction patterns, bizarre amounts and frequency of transactions that have no logical explanation, source of funds or wealth that have traces to criminal activities.

Products and Services Related Risk Factors

In the Virtual Assets sector, different crypto products carry different inherent risks. These include trading platforms with high-value movement, NFT platforms with anonymized transfers or OTC desks dealing in large, off-exchange transactions.

Evaluating the risk of particular products and services that VASPs offer allows them to understand the offerings which are more vulnerable to ML/TF/PF activities. This facilitates putting additional AML/CFT controls at places that are weak.

Delivery Channel Related Risk Factors

While developing the business risk profile, VASPs must consider delivery channel related risk factors, as how users access the VASPs affects the likelihood of abuse. For instance, online onboarding may face identity spoofing, API-based services can enable high-speed activities, and integration with third-party platforms may introduce risks that VASPs cannot fully control.

Therefore, assessing delivery channel related risks helps the VASPs to identify where additional verifications or oversight mechanisms are required.

Stay Ahead of Evolving Virtual Assets Risks

Get Expert Guidance to Ensure Your BRA Covers All VA-Specific Typologies.

Step-by-Step Guide for VASPs to Undertake Comprehensive Business Risk Assessment

VASPs often feel overwhelmed to conduct an effective BRA, especially because the Virtual Assets ecosystem moves fast and ML/TF risks evolve even faster. A structured step-by-step approach helps bring clarity to this process.

Key steps for VASPs to undertake an extensive Business Risk Assessment include

- collecting business data, categorizing risks,

- developing methodology for risk calculations,

- assessing inherent risk, evaluating control measures,

- finding residual risk,

- conducting gap analysis of findings, documenting it, and

- preparing the final BRA report.

The below infographic illustrates the chronological approach for VASPs to conduct efficient Enterprise-Wide Risk Assessment.

Collecting and Mapping Business Data

The process of Business Risk Assessment (BRA) for VASPs begins with collecting all relevant information regarding the operating model through a customized questionnaire. This involves collecting structured data on customer types, regions, products, transactions and delivery channels. Further, the analysis of the National Risk Assessment and Sectoral Risk Assessment is performed to ensure thorough compliance with them.

Through mapping of this information, VASP establishes a factual basis that anchors the entire risk assessment. It ensures that every decision is grounded in how the business truly functions rather than mere assumptions.

Identifying and Categorizing Risks

Once the data mapping process is over, identifying and categorizing risks based on the gathered data takes place. VASPs disambiguate the collected data and scatter into different risk factors.

This includes categorizing possible risks such as risky customers, high-risk countries, complex products, unusual transactions, weak onboarding channel, etc.

These risks are later grouped into categories, so they are easy to analyze. In simpler terms, this step basically is to recognize “Where can things go wrong”.

Developing a Structured Methodology for Risk Calculation

Post categorizing the risk into different risk factors, VASPs develops a structured methodology for risk calculation.

Designing a repeatable and auditable approach, defining scales and risk weightings (likelihood, impact), outlining qualitative and quantitative thresholds, specifying how to combine scores (matrix, weighted average), and setting governance rules for calibration, helps VASPs in turning a list of risks into a measurable framework.

Assessing Inherent Risks

Post determining a structured methodology for risk calculation, the inherent risk of the VASP’s business model is evaluated. Inherent risk is basically the ML/TF/PF risk that is omnipresent in the business from its inception, before applying any controls.

To assess the inherent risk, the likelihood of occurrence or materialization of identified ML/TF risk and the impact of that risk on the VASP is calculated using both quantitative and qualitative methods.

Evaluating Mitigation Controls

Once the inherent risk of the VASP is identified, the following process is to evaluate the mitigating controls that are already present in the business.

This includes checking the efficacy of AML/CFT Policies and Procedures, KYC Processes, Screening tools, Transaction Monitoring rules, Regulatory Reporting pathways and other control measures.

Determining the Residual Risks

After evaluating the effectiveness of mitigation controls, the subsequent stage is to determine the level of residual risks. Residual risk is basically ML/TF risk that is remaining in VASP after safeguards.

Residual Risk in VASP business model is calculated through a structured methodology that is inherent risk minus the controls. This uniform approach helps VASPs to produce consistent residual ratings across risk categories.

Conducting Gap Analysis

After assigning the residual risk score to each risk category, the following workflow is to conduct a gap analysis. Undertaking analysis of differences with reference to the risk appetite of the VASP provides a full insight into the actual weaker areas and facilitates developing a roadmap that is required to fulfill that gap.

These gaps are subjective and can differ from entity to entity, as it depends on the individual risk appetite. For VASPs, conducting a thorough gap analysis is of utmost importance as it shows the strengths and weaknesses of the business through raw approach.

Documenting Findings and Risk Scoring

Following the gap analysis, documenting the findings and ultimate risk scoring captures the full assessment in a structured record for VASPs. This documentation also includes recording risk inventory, scoring rationale, data inputs, control assessments and version history in an organized manner.

The explanation and logic for reaching the final risk scoring are required to be documented. Thorough documentation ensures transparency and reduces the chances of errors.

Preparing the Final BRA Report

The final stage of an effective Business Risk Assessment for VASPs is preparing the final BRA report. It is a consolidated report that summarizes the VASP’s risk posture, high-risk exposure areas, key vulnerabilities, and residual risk priorities, along with a thorough recommended remediation plan.

This action plan outlines resource allocation, suggests updating AML/CFT policies/procedures and provides a roadmap for effective implementation and impactful decision-making to combat the risk of ML/TF/PF activities.

Is Building a Structured Business Risk Assessment Too Cumbersome?

Get Specialized Solutions for End-to-End BRA Support.

Unlocking the Benefits of Business Risk Assessment for VASPs in UAE

The advantages of a well-articulated Business Risk Assessment show up across the entire organization. It sharpens the way business understands its risk exposure, highlights which areas need stronger controls and removes guesswork from decision-making.

Provides a Multidimensional and Balanced View of ML/TF/PF Risks

A robust Business Risk Assessment provides a comprehensive perspective on ML/TF/PF risks that a VASP is exposed to. It takes multiple dimensions into consideration, such as customer related risks, geographical risks, product/services related risks, delivery channel and transaction patterns related risks.

This multidimensional approach offered by BRA enables VASPs to make nuanced risk-based decisions regarding financial crime risk management and controls.

Facilitates the Development of an Informed and Curated ML/TF/PF Risk Appetite

A Well-defined and analyzed Business-Wide Risk Assessment (BWRA) provides VASPs a clear vision into their risk areas.

Moreover, it offers necessary data to VASPs to understand the exposure of financial crimes to their business model. That helps them to develop an informed and carefully curated ML/TF/PF risk appetite commensurate with the nature, size and risk exposure of the VASPs.

Drives Efficient Allocation of Resources Towards ML/TF/PF Risk Management

An efficient Business Risk Assessment framework ensures that resources are deployed appropriately. It facilitates VASPs to prioritize areas that pose a high risk of ML/TF/PF activities and reduces underutilization of its resources.

By analyzing each risk area it helps VASPs to plan their risk management efforts to optimize their AML/CFT/CPF compliance.

Strengthens Competence in ML/TF/PF Risk Management

An effective BRA framework enhances the overall competency of VASPs in managing financial crime risks. With the right assessment of risk exposure, calculation of inherent risk, residual risks and evaluation of control measures, VASPs help to build a more knowledgeable and risk-aware workforce.

It supports data-driven decision making, ensuring management of financial crime risks.

Ensures Alignment with National Risk Assessment and Sectoral Risk Assessment

An efficient BRA framework ensures that a VASP aligns with the findings of the National Risk Assessment and Sectoral Risk Assessments.

By incorporating outcomes from these assessments, VASPs can enhance their understanding of ML/TF/PF risks.

Supports Long-Term Growth Through Risk-Informed Decisions

A good Business-Risk Assessment helps VASPs to understand where risks are and how to manage them.

This lets the business make smarter decisions, plan safely and grow without unexpected problems. Over time, it builds a stronger and more stable business.

Make Your Business Risk Assessment Work Harder for Your VASP

Develop Methodologies for BRA that Unlock Its Full Potential

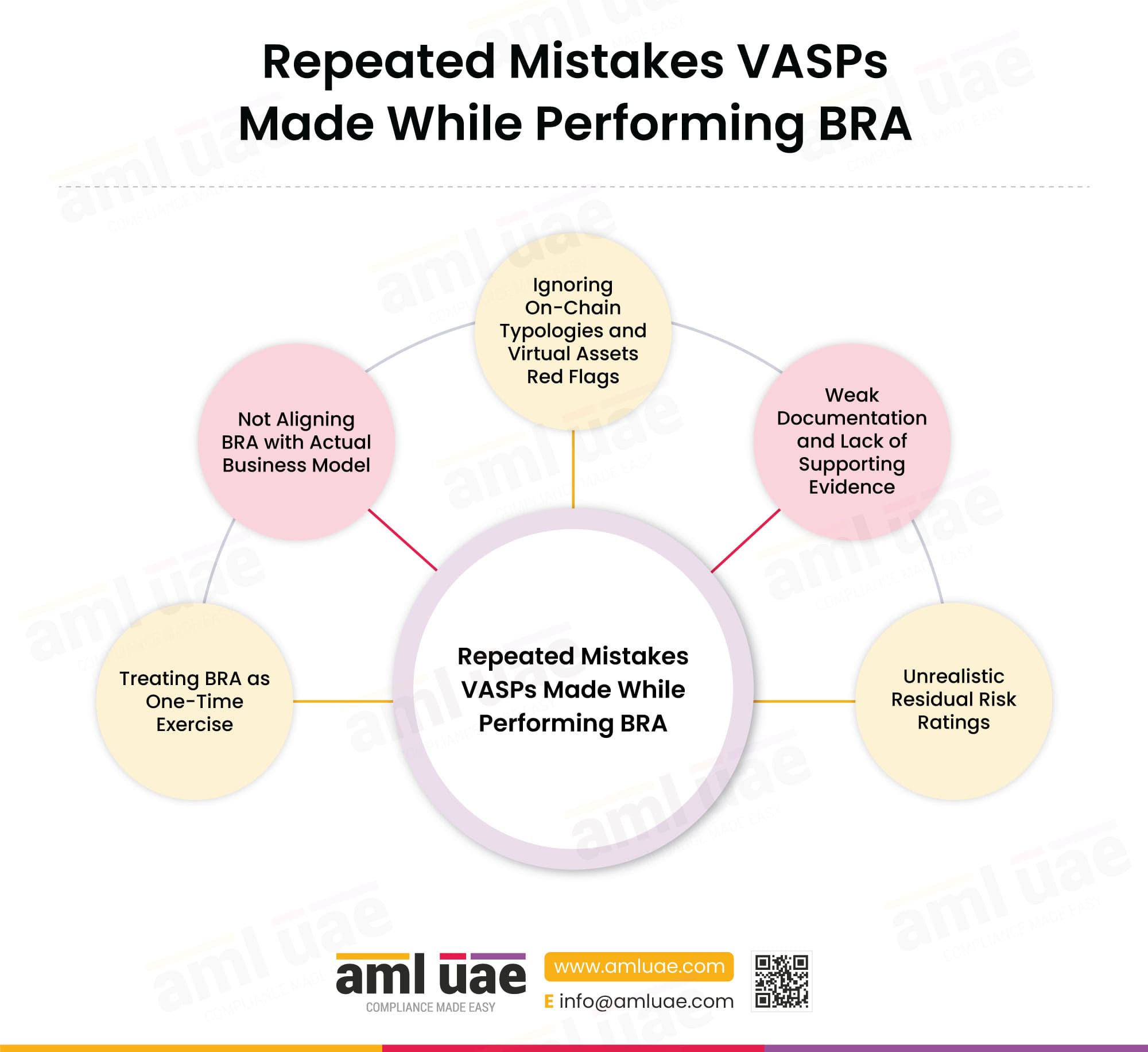

Repeated Mistakes VASPs Made While Performing BRA

Despite clearly defined regulatory expectations, many VASPs fall into similar traps when conducting BRA. The basic mistakes often repeated by VASPs often come from rushing the process with unrealistic risk scoring, misalignment with the actual business model, absence of documentation and treating the Business Risk Assessment as a single time exercise.

These mistakes often weaken the objective of conducting Business Risk Assessment and end up introducing VASPs to regulatory penalties when expectations of regulators are not met.

The infographic below demonstrates the common mistakes replicated by VASPs while performing Business Risk Assessment.

Treating BRA as One-Time Exercise

There is a wide-spread misjudgment among VASPs that Business Risk Assessment is a single time exercise. The BRA is mistakenly treated as a static document instead of a living assessment.

This results in BRA that no longer reflects the VASP’s real ML/TF/PF exposure as the risk factors affecting it keep changing. The approach to treating Business Risk Assessment as One-time activity quickly makes it outdated.

Not Aligning BRA with Actual Business Model

Some VASPs prepare BRA that appears good on paper; however, they lack the substance. The prepared Business Risk Assessment does not resonate with the actual business model, its products, customers, supply chains, or transaction patterns.

Inaccurate representation makes risk assessment theoretical rather than practical. A BRA that is disconnected from the core business model cannot lead to true and effective decision-making.

Ignoring On-Chain Typologies and Virtual Assets Red Flags

One of the major roadblocks for VASPs to conduct an effective Business Risk Assessment is focusing on traditional financial crime risks while ignoring the Blockchain-specific ML/TF/PF Typologies.

The nature of the Virtual Assets (VA) Sector is quite different from the basic financial or DNFBPs sector. And this uniqueness requires a unique approach, which VASPs fail to implement.

Failing to consider VA specific red flags and typologies in the BRA underestimates the real risk exposure and weakens monitoring strategies.

Weak Documentation and Lack of Supporting Evidence

A lot of VASPs lag behind in preparing regulator-ready BRA because the findings are not supported by a clear rationale, data and evidence. The assessment tends difficult to defend during audits or regulatory reviews due to illogical, scattered and undocumented assumptions.

A strong BRA requires a documented methodology, scoring explanations and consistent use of risk metrices. The failure to incorporate these practices in BRA makes it sluggish and incompetent.

Unrealistic Residual Risk Ratings

A very common mistake repeated across multiple VASPs is the inefficiency in realistically rating the residual risks.

Residual Risk is a very important aspect of an accurate Business Risk Assessment, as it paves the way for sound decision-making and gives a real idea of financial crime risk exposure to VASPs.

However, wrongly calculating it by overestimating control effectiveness or underestimating inherent risk exposure creates a false sense of security.

No Scope for Mistakes Anymore

Reign Over Basicness with Regulator-Ready Business Risk Assessment

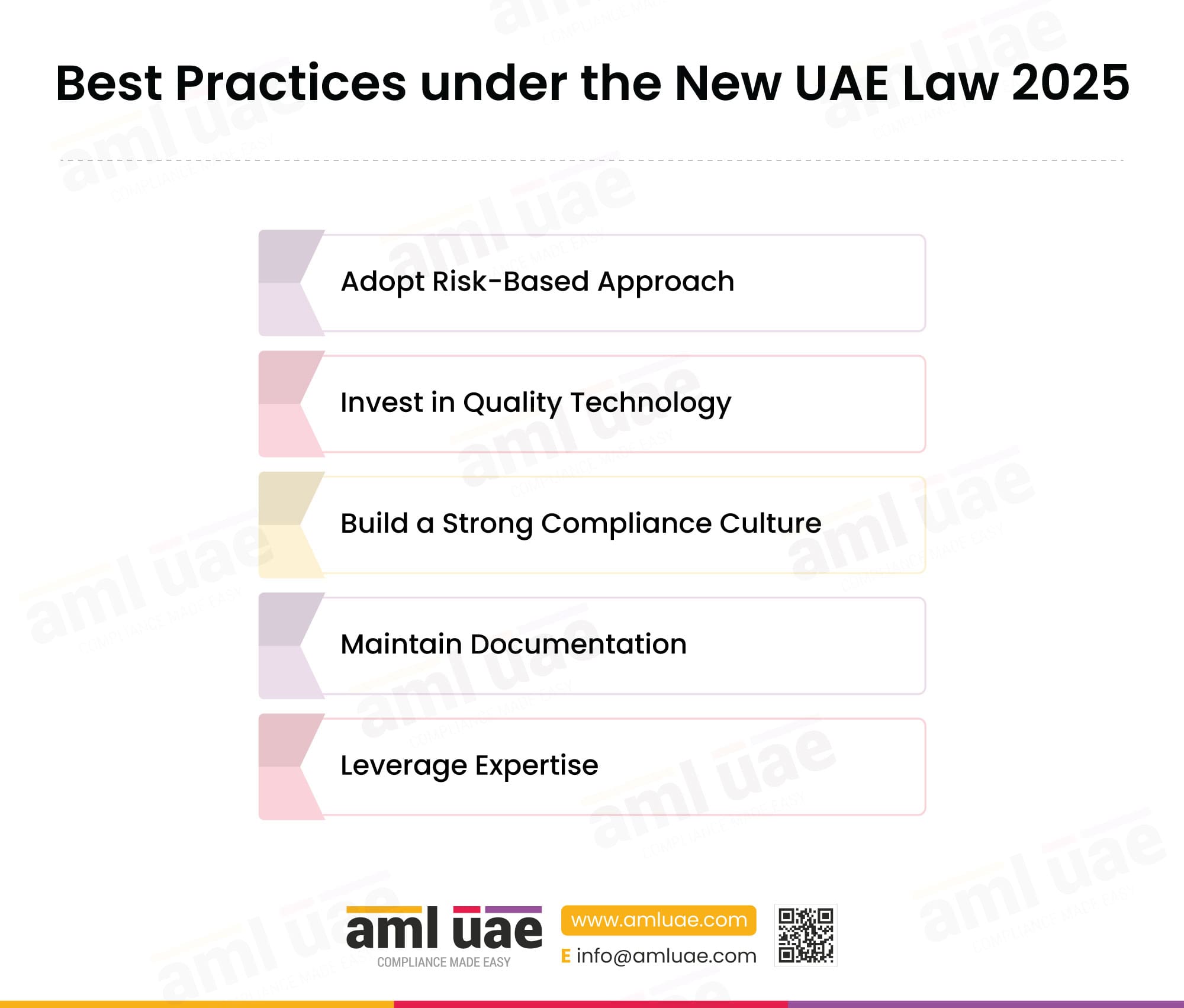

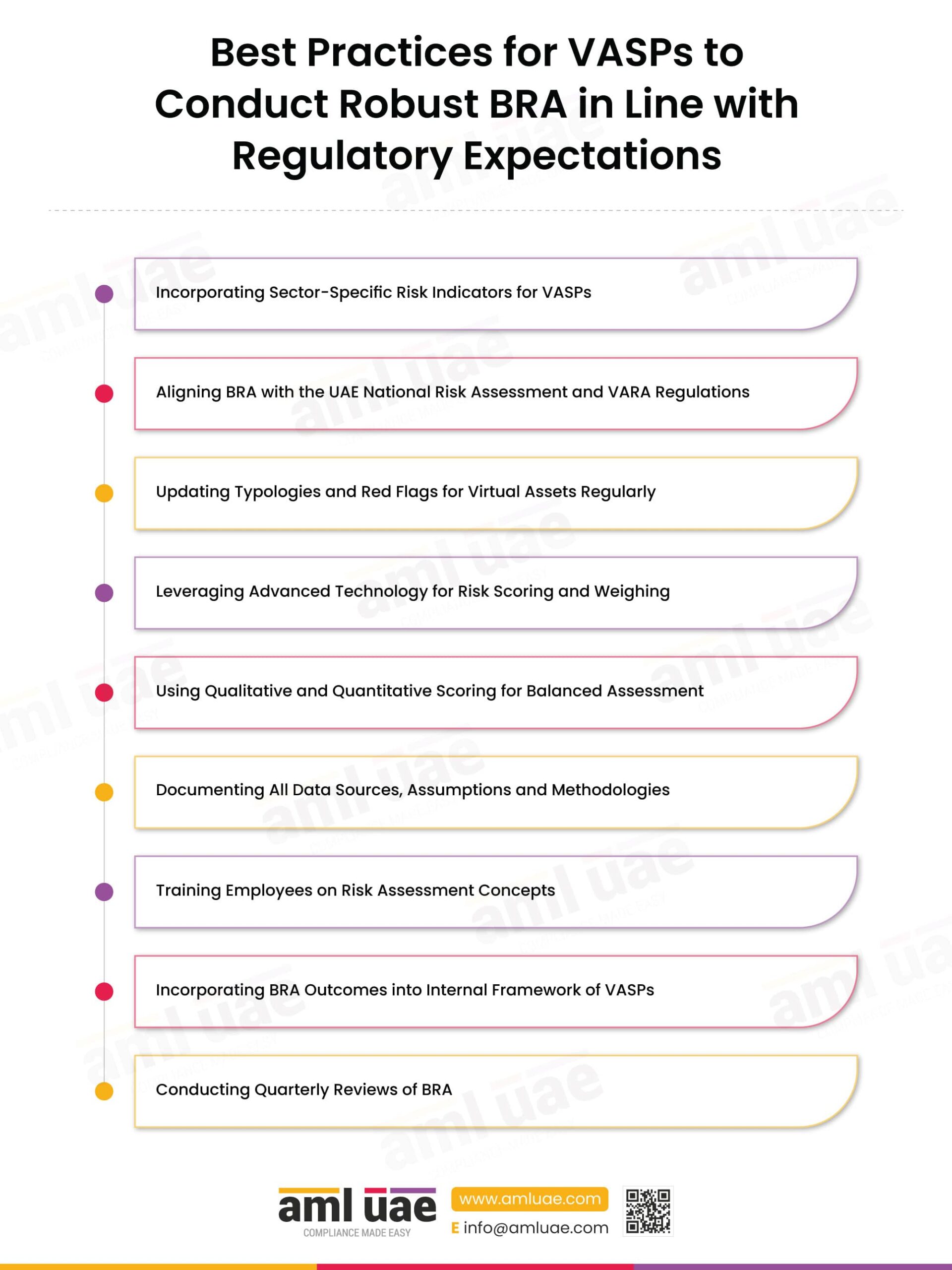

Best Practices for VASPs to Conduct Robust BRA in Line with Regulatory Expectations

As the regulators often find Business Risk Assessment by VASPs underwhelming, here comes the savior. With the implementation of certain best practices while performing an Enterprise-Wide Risk Assessment ensures that it fulfills the regulator’s expectations.

These best practices include incorporating sector-specific risk indicators, alignment with UAE NRA and VARA, periodic updates in VA-specific typologies, leveraging AI for risk scoring, using qualitative/quantitative scoring, training employees and documenting all assumptions, data, rationale and methodologies.

Moreover, integrating the Business Risk Assessment outcomes into the internal framework and conducting quarterly reviews ensures the robustness of BRA.

The following infographic represents the best practices for VASPs to conduct BRA that are in line with the Regulatory expectations.

Incorporating Sector-Specific Risk Indicators for VASPs

For an accurate Business Risk Assessment, VASPs must include ML/TF/PF risk indicators that are specific to the Virtual Assets Sector. This includes indicators like wallet anonymity, cross-chain transfers, decentralized platforms or high-velocity trading patterns.

Embedding these VA-specific risk indicators into the BRA ensures that VASPs reflect actual threats rather than solely relying on traditional sayings.

Aligning BRA with the UAE National Risk Assessment and VARA Regulations

VASPs must ensure that it aligns Business Risk Assessment with the results of National Risk Assessment (NRA), VARA Regulations and UAE’s Federal AML/CFT Laws. The risks and industry findings identified in UAE NRA and relevant Sectoral Risk Assessments must be considered in the VASP’s risk rating methodology.

This alignment ensures that VASP’s internal view of risk matches the country’s identified threats and regulatory expectations.

Updating Typologies and Red Flags for Virtual Assets Regularly

Since financial crime methods evolve rapidly in the crypto landscape, VASPs must continuously refresh their knowledge of typologies and red flags.

This includes staying updated on emerging schemes such as Anonymity-Enhanced Transactions, new or evolving Virtual Assets Products etc. Keeping the typology database current ensures that VASP is using the latest intelligence to judge ML/TF/PF risk exposure accurately in BRA.

Leveraging Advanced Technology for Risk Scoring and Weighing

For a robust Business Risk Assessment, VASPs must leverage advanced technology rather than solely relying on manual judgement.

VASPs should integrate help from tools such as blockchain analytics platforms, automated scoring engines, visual heatmaps and AI-based gap detection in BRA. This improves accuracy and consistency in risk scoring.

Using Qualitative and Quantitative Scoring for Balanced Assessment

VASPs must combine qualitative and quantitative scoring scales for a balanced approach in Business Risk Assessment. This includes merging numerical scoring with approximate judgment.

This blending approach in the risk scoring model prevents the BRA from becoming overly mechanical. It ensures that VASPs evaluate the ML/TF/PF risks of their business from both a data-driven and practical perspective.

Documenting All Data Sources, Assumptions and Methodologies

In order to create a structured Business Risk Assessment, VASPs must document every data source used, the assumptions behind scoring, the logic for weightings and the rationale behind the final risk rating.

These are some of the most important aspects of BRA. Such documentation strengthens governance and ensures that BRA can be defended during regulatory audits.

Training Employees on Risk Assessment Concepts

For an effective and sound Business Risk Assessment, it is essential that VASPs must provide periodic training for their employees on risk assessment concepts.

The accuracy of BRA relies on informed people. Providing training on VA-specific typologies and scoring methodologies builds internal competency. It ensures consistent judgment across VASP and creates shared understanding of how risk decisions are made.

Incorporating BRA Outcomes into the Internal Framework of VASPs

For an effective implementation of Business Risk Assessment, it is crucial that VASPs incorporate the findings and recommendations of BRA Report into the internal framework of their organization.

This includes integrating BRA outcomes into VASP’s AML/CFT Policies and Procedures, Customer Risk Assessment, Transaction Monitoring Calibration, internal audit and other compliance monitoring plans. Allocating Resources as per the results of BRA, increases the efficiency of VASPs.

Conducting Quarterly Reviews of BRA

The best practice to make the BRA current is to conduct periodic reviews of it. VASPs must establish framework to quarterly review the BRA against any new developments, supervisory findings and emerging typologies.

Moreover, VARA expects VASPs to analyze key operational data and material changes, at least once every quarter. This ensures that BRA remains relevant and accurately reflects the risk landscape throughout the year.

Turn Your Business Risk Assessment into Regulator-Ready Backbone for Your VASPs Operations

A well-articulated Business Risk Assessment is not just a compliance requirement, but a foundation for an effective AML/CFT Program for VASPs. As Virtual Assets sector continues to evolve, regulators expect VASPs to display real understanding of their own ML/TF/PF risk exposure. An organized and regularly updated Business Risk Assessment facilitates VASPs to stay ahead of these expectations instead of reacting at the last minute.

AML UAE= Your Trusted Partner to Conduct Robust Business Risk Assessment

Let Us Take Charge of Your Compliance Journey!

Frequently Asked Questions (FAQs)

What is Business Risk Assessment for VASPs in UAE?

Business Risk Assessment is a structured review of the financial crimes risks faced by VASPs’ business model. It gives insight into risk exposure considering wide-ranging factors such as customer base, delivery channels, geographies, transaction patterns, and product/services offered.

How often should VASPs in the UAE update their Business Risk Assessment?

VASPs in UAE should update their Business Risk Assessment at every quarter or occurrence of significant events as mandated and expected by the UAE’s regulatory authorities.

What risks should VASPs evaluate in a UAE Business Risk Assessment?

VASPs should evaluate customer related risks, transaction related risks, geographical risks, product/services related risks, delivery channel related risk and other relevant risks for an effective Business Risk Assessment.

How to perform a Business Risk Assessment?

To perform a Business Risk Assessment, collect mandatory business data, assess inherent risk, evaluate existing control measures, calculate residual risk with a structured methodology, prepare a report and document all the data and rationale.

Are VASPs required to align their Business Risk Assessment with UAE National Risk Assessment and FATF Guidance?

Yes, VASPs are required to align their Business Risk Assessment with the outcomes of UAE’s National Risk Assessment and FATF Guidance.

How do I conduct a Business Risk Assessment for a VASP in UAE?

To conduct a Business Risk Assessment for a VASP, first understand the regulatory requirements and the nature of the business, gain a grasp over VA-specific typologies, then determine the risk appetite, develop a board-approved methodology and commence with the assessment with relevant business-related data.

How can AI be used for Business Risk Assessment of VASPs in UAE?

AI facilitates VASPs to perform BRA by analyzing large customer sets, transactions and on-chain data sets more accurately. It also automates scoring and identifies anomalies that a manually conducted Business Risk Assessment may miss.

Share via :

About the Author

Pathik Shah

FCA, CAMS, CISA, CS, DISA (ICAI), FAFP (ICAI)

Pathik is an ACAMS-certified AML consultant specialising in governance, risk, and compliance for regulated entities in the UAE. He brings over 28 years of experience, with 1,000+ hours of AML training and 200+ advisory engagements across DNFBPs, VASPs, and FIs. He supports businesses in aligning with AML/CFT requirements from the CBUAE, DFSA, MoET, MoJ, VARA, CMA, FSRA, and FATF. Known for translating complex regulations into audit-ready procedures, Pathik enables operational clarity and compliance readiness.

Reach Out to Pathik