Protect your business with reliable and effective AML strategies with AML UAE.

What Is The Role of Technology In Anti-Money Laundering Compliance

This blog discusses the exponentially growing role of technology in Anti-Money Laundering compliance. With criminals using advanced tactics to successfully evade the suspicious activities and transaction detection techniques used by financial institutions, Designated Non-Financial Businesses and Professions (DNFBPs) and Virtual Assets Service Providers (VASPs) need to understand the role of technology in Anti-Money Laundering (AML) compliance.

The DNFBPs and VASPs must take the help of technological advancements such as Artificial Intelligence (AI), Machine Learning, Data Analytics, Cloud-based solutions and more to counter ML/TF and comply with regulatory requirements.

Limitations of Traditional Anti-Money Laundering Processes

Traditional and legacy AML processes suffer from challenges relating to cost, time, and human intervention. Following are the difficulties faced by financial institutions, DNFBPs and VASPs in AML compliance while using traditional or legacy AML processes:

Resource-Intensive

The annual cost of anti-money laundering (AML) compliance for financial institutions and reporting entities is enormous.

This cost may rise in the upcoming years due to the scaling of the business, requiring a higher volume of AML activity, rigorous checks, complex investigations, greater people-centric costs, and an ever-expanding scope of offences.

In practice, reporting entities spend a significant portion of the budget on Customer Due Diligence (CDD), followed by internal investigation and data collection. CDD is the process by which reporting entities identify or verify client information. This adds pressure on the workforce, thus increasing the entity’s labour costs.

Ineffective Customer Due Diligence (CDD) Measures

With legacy and traditional CDD, businesses risk gathering outdated, irrelevant, or incorrect information. They are prone to human error, technical incompetence, and lack of expertise. With all in place, it becomes difficult to identify patterns if all CDD measures do not align properly. This can cause failure to identify red flags and put businesses at risk.

Time-Consuming

AML compliance is inherently time-consuming as it requires proper risk assessment of customers, obtaining and verifying customer information from multiple public and private sources, including customer sanctions lists and continuous monitoring.

At a time when customers are looking for one-tap access to services and instant approvals, any delay or loss of productivity and rounds of information gathering may result in a negative customer experience.

Scope for Human Error

The AML/CFT guidance for DNFBPS categorises three lines of defence in an AML program.

The Three Lines of Defence in the AML Program comprises the employees who execute KYC or Customer Due Diligence, compliance officers or money laundering reporting officers who ensure the obligation of AML/CFT regulations, independent auditors who assess the effectiveness of the first and second line of defence.

Any scope for human error on either line of defence can weaken the organisation’s entire AML program.

In the First Line of defence:

Lack of adequate front–line employee training to recognise red flags can result in establishing business relationships with suspicious individuals and entities. It also results in failure to submit a Suspicious Activity Report (SAR) or Suspicious Transaction Report (STR) with the UAE FIU.

In the Second Line of defence:

Compliance officers and professionals involved in AML compliance processes often face burnout due to the high volume of important daily decisions they make for their clients. Such decisions can range from a simple onboarding task to reporting suspicious activities.

Decisions are highly likely to vary due to differences in opinion, experience, and knowledge and susceptibility to bias, which increases the scope for human error.

In the Third Line of defence:

Ensure the auditors have the relevant training, expertise and experience to conduct AML audit functions. Any relaxation can allow irregularities to go unnoticed.

It is also important for an auditor to understand the nature and size of the business, applicable laws and regulations, sanctions regime, and risk appetite of the financial institution, DNFBPs, or VASPs. Any deviation by the auditor can elevate the organisation’s risk.

Sophisticated Money-Laundering Tactics

The virtual asset space has evolved a lot in recent years, providing new possibilities for offenders. The creation of synthetic identities, i.e., a mix of real and fake identities, the use of privacy coins, mixers, and tumblers to conceal the origin of funds, and other Anonymity-Enhanced Currencies (AEC) make it difficult for financial institutions, VASPs, DNFBPs, and regulatory authorities to trace transactions. Non-fungible Tokens (NFTs) are blockchain-backed images, videos, audio, or memberships that a holder owns by owning the data associated with such items.

Lack of High-Quality and Real-Time Data

AML compliance is a highly data-driven process. One of the biggest challenges in legacy AML compliance is the lack of high-quality, real-time data. The primary reason behind this is the practice of storing data in silos. It is impossible for any small, medium, or large organisation to manually analyse the abundance of available data with their limited processing power. This raises issues such as unnecessary duplication of information, redundant tasks, and bottlenecks within the organisation.

The lack of availability of quick and real-time data directly impacts the data-driven AML compliance processes such as sanctions screening, which, if not screened across real-time data, would give false results, causing sanctioned individuals or entities to pass through the filter of sanctions screening, leading to their establishment of business relationship with them, exposing business to ML/TF and PF risks.

Rule-Based Systems and High False Results

When deciding if a transaction is suspicious, AML professionals rely on a certain set of principles, which can be rule-based or risk-based. Every transaction involves details such as parties engaged, money consideration, mode of payment, and place of transaction.

Rule-based systems rely on rules framed by industry experts to guide the decision-making process. This includes threshold-based, transaction-based, location-based, and customer-based rules. The rule-based system is rigid and views transactions from a single lens, which can lead to high false positives, making the job of compliance officers more cumbersome.

The inefficiency in the legacy rule-based systems is causing regulatory and reporting entities to adapt to new and advanced technologies in compliance processes.

Enabling Regulatory Framework

The present regulatory framework endorses relying on novel innovations for AML compliance. However, it also cautions Financial Institutions, DNFBPs and VASPs about their potential risks. The following laws and regulations deal with the adoption of modern technologies.

The Cabinet Resolution No. (134) of 2025 concerning the Implementing Regulation of Federal Decree by Law No. (10) of 2025:

- Enables Financial Institutions and DNFBPS to adopt modern technologies to counter Money Laundering and Terrorism Financing challenges that may arise.

AML/CFT Guidance for DNFBPS

- Requires the reporting entities to ensure risk management of modern technologies.

- Suggests reporting entities use technology to counter ML/TF risks effectively.

Specific guidance for Financial Institutions on Digital Identification for Customer Due Diligence (CDD) by the Central Bank of UAE.

- Enables the use of Digital ID Systems to prove a person’s identity online using electronic databases, digital credentials, and Application Program Interfaces (APIs).

- Components of Digital Identification Systems include:

- Identity Proofing and Enrolment: It establishes a person’s identity account by collecting and validating available information about the person.

- Identity Authentication: It verifies a person’s identity using authenticators.

- Transferability and Integration Mechanisms: These mechanisms allow the verification of other customer relationships using a person’s identity.

The digital identification system is in line with the Key Principles issued by the Supervisory Authorities for Financial Institutions adopting AML Enabling Technologies.

Key Principles for AML enabling technologies:

1. Data Protection: Financial Institutions, DNFBPs, and VASPs must comply with all prevailing laws and regulations on data protection at all stages of data handling, use, transmission, and storage.

2. Control Functions: Regulated entities should adopt a risk-based approach and employ proper controls to mitigate risks.

3. Independent Review: Institutions should conduct formal, independent reviews/audits. Additionally, while appointing an AML auditor, regulated entities should ensure that the auditor understands the entity’s operations and risks.

4. Skill, Knowledge, and Expertise: Organizations should ensure that their staff possess relevant resources, skills, knowledge, and expertise specific to their roles when adopting a new technology.

5. Training: Organizations should provide adequate training to relevant staff for handling modern technologies.

Evolution of AML Technology

The AML Mechanisms have undergone drastic changes over the years due to the crime’s evolving nature. Earlier, AML practices heavily relied on manual, rule-based processes that suffered from numerous challenges.

The static nature of manual mechanisms could not cope with the complexities of the crime. For instance, compliance officers used to search through various government and private sources to collect relevant information and verify it with documents provided by the client. This straightforward process assumed substantial time, energy, and resources without guaranteeing accuracy.

The industry slowly moved onto systems that used data analytical models, also known as legacy systems. While these systems saved time and resources, they came with their challenges. Many technological models adopted were also rule-based and failed to detect behavioural patterns. Data quality deteriorated due to redundancy, insufficiency, and potential human bias. The advent of artificial intelligence and cloud-based services has opened new opportunities for reporting entities to overcome the challenges posed by traditional and legacy systems, with the scope for real-time tracking and data analysis.

Key Technologies in AML

Artificial Intelligence (AI)

Artificial Intelligence is a technology that allows computers and machines to perform tasks that replicate Human Intelligence. Institutions can apply AI in AML compliance for pattern recognition, task automation, and predictive analytics to streamline operations and enhance customer experience.

Machine Learning (ML)

Machine Learning is a subset of artificial intelligence (AI). It uses data and algorithms to enable AI to imitate human learning, thus gradually improving its accuracy. Machine learning provides the scope for accuracy and scalability in automation.

Big Data Analytics

Big data analytics is the process of gathering, verifying, and analysing enormous amounts of data to quickly and efficiently discover market trends, insights, and patterns. Professionals can utilise advanced tools such as sophisticated algorithms and statistical models. Big Data Analytics is the practical manifestation of AI and Machine Learning.

Blockchain and Distributed Ledger Technology (DLT)

Blockchain and other distributed ledger technologies (DLTs) provide a safe method of executing and documenting digital asset transfers without the interference of any central authority. The scope of assets that may be monitored and exchanged on a blockchain network is enormous. It includes intangible assets like patents, copyrights, and trademarks and tangible assets like real estate, cars, money, and land. This adaptability lowers costs and minimises risks for all parties involved.

Robotic Process Automation (RPA)

Robotic Process Automation (RPA) uses modern automation technology for data collection, form filling, file transferring, and other repetitive office tasks. Bots are being increasingly used in customer service. Their ease of use makes them a popular choice among small businesses that can adopt either semi-automation or complete automation.

RegTech and RiskTech Solutions

Companies and their compliance teams should always be aware of changes in the regulatory environment. However, not every company has the resources to hire a compliance team. This is where RegTech (Regulatory Technology) comes into play. RegTech is a FinTech (Financial Technology) branch that uses technology to manage regulatory procedures. Its key features include regulatory monitoring, reporting, and compliance.

Besides regulatory compliance, risk assessment and risk management are other major functions of the AML Process. RiskTech encompasses the use of technology to manage risks. Regulated entities can better understand risk exposure and improve risk-related decision-making using RiskTech technologies.

Natural Language Processing Models

Natural language processing (NLP) is a branch of machine learning that allows computers to interpret, manipulate, and comprehend human language. It can decipher large amounts of unstructured data and is extensively used in chatbots and other communication tools to enhance customer experience while complying with AML/CFT legal requirements.

Helping you with AML software selection that streamlines

Your AML, CFT, and KYC compliance procedures.

Integrating Technology in Anti-Money Laundering

At present, there are different technological solutions for different AML processes. This variety of solutions can confuse small financial institutions, payment service providers, DNFBPs, and VASPs when deciding which solution works best according to their risk appetite and integrating it into their existing compliance program. So, it is important to understand the application of innovative solutions in AML processes.

Data Management and Information Sharing

Natural Language Processing can simplify standard AML tasks such as screening client names and related parties across various lists for sanctions, negative news, risk indicators, and political exposure. Moreover, it automatically verifies and resolves alerts and activates accounts based on their usage and available records. Machines can identify, score, prioritise, enhance, close, or archive alerts more quickly than people.

Sanctions Screening

Sanctions Screening is an integral part of the AML system. Customer screening includes matching customer data with existing governmental and international databases and lists of Politically Exposed Persons (PEP)and adverse news. Robotic Process Automation (RPA) software enables the automation of the screening process by instantly processing customer information against multiple sanctions screening databases, alert processing, automatic closure of alerts in case of a false positive, or directing alerts to relevant personnel based on priority, risk, and geographical factors. It also compiles data from various internal and external sources.

KYC (Know Your Customer)

The time gap in periodic KYC processes exposes organisations to financial risks. Perpetual KYC (pKYC) uses AI and machine learning to assess customers based on their increased probability of committing crimes. A pKYC model can automatically re-verify existing documents, significantly reducing compliance professionals’ time and resources. Businesses can utilise pKYC to streamline customer onboarding and verification based on data sources such as national identity databases, eKYC, face recognition databases, corporate registries, and tax databases.

Risk Assessment

AI-powered AML systems can integrate and analyse diverse data, discover intricate hidden transaction patterns, assess and highlight high-risk regions with complex systems, swiftly respond to rapid fund movements, and detect discrepancies between customer information and behaviour.

Example: Companies use AI to recognise patterns, assign a score to risk activities that pose a greater danger of money laundering, and flag alerts that need priority action.

Transaction Monitoring and Case Management

AI allows real-time transaction monitoring that can effectively prevent and help in the early investigation of money laundering activities. This speed in monitoring can help reporting entities and supervisory authorities to remain one step ahead of the offenders.

Example: Financial Institutions use AI-powered solutions to monitor transactions as they occur. This allows prompt alerts on all fraudulent activities.

Anti-money laundering (AML) case management is a crucial step in which experts at financial institutions examine suspicious activity. The experts build a case by examining the parties, accounts, and transactions involved. Finally, they report suspicious activity to the government. Sophisticated AML compliance software solutions use robust engines to identify patterns that automatically improve using machine learning.

It then builds a case based on the activity. Each case makes it easy to briefly see all the relevant parties, accounts, and transactions and inquire in-depth into each one. For instance, it can identify similar transactions made by other parties.

Regulatory Reporting

Specialised AML software can automate reporting procedures by eliminating manual intervention, ensuring fast and accurate data delivery while reducing human errors. These procedures include categorisation, processing and preparation, data validation, regulatory monitoring, case management, and analytical calculations.

Record Keeping

The regulatory framework on money laundering mandates reporting entities to maintain all records, data and transactions, and correspondence for the duration of the business relationship. The regulations also obligate them to retain such records for five years or more, depending on the circumstances. However, the Abu Dhabi Global Market (ADGM) and Dubai International Financial Centre (DIFC) require reporting entities to keep records for at least six years.

At the same time, The Virtual Assets Regulatory Authority (VARA) requires Virtual Asset Service Providers (VASPs) to retain records for at least eight years. Similarly, the Securities and Commodities Authority (SCA) requires regulated entities to maintain records for at least ten years.

Independent AML Audit

The purpose of an independent AML audit is to provide an unbiased assessment of the effectiveness of a company’s AML program and the status of its regulatory compliance. Artificial Intelligence removes any scope for familiarity, recency, or attention bias humans are prone to. Tech-based independent auditing can provide data-driven insights into the effectiveness of a client’s AML program. AI and Big Data Analytics can simplify the benchmarking process to identify areas where a company’s AML efforts fall short of industry expectations.

Accountability and Overall Good Governance

Blockchain networks make data openly accessible to network participants using technologies like block explorers, allowing them to inspect holdings and transactions associated with public addresses. This transparency ensures that all parties know the transactional activity, lowering the potential for bias or manipulation. Further, blockchain’s rigidity ensures that once a transaction is entered into the ledger, it cannot be modified or deleted, providing a permanent audit trail of financial transactions.

To make the most of your investment in AML screening software

Get the professionals to validate and test the systems now!

How Does Technology Ease Anti-Money Laundering Processes?

Digital Transformation is no longer an option or an advantage; it is now a necessity for AML compliance. Artificial Intelligence is expanding the scope of Anti-Money Laundering (AML) processes and making them more vigilant towards illicit activities. The most significant benefit of incorporating advanced technologies is that they improve recognition, comprehension, and handling of ML/TF risks. They can assess and process extensive data sets more quickly, accurately, and efficiently, improving quality.

The biggest boon for small enterprises is technological tools’ ability to perform complex tasks at lower cost. Reporting entities need access to the entire channel of suspicious transactions to comprehend the nature and risk of suspicious transactions completely. Often, such channels or parts of such channels belong to unrelated entities or are available beyond borders. Innovative technologies can traverse borders to provide reporting entities with a comprehensive picture.

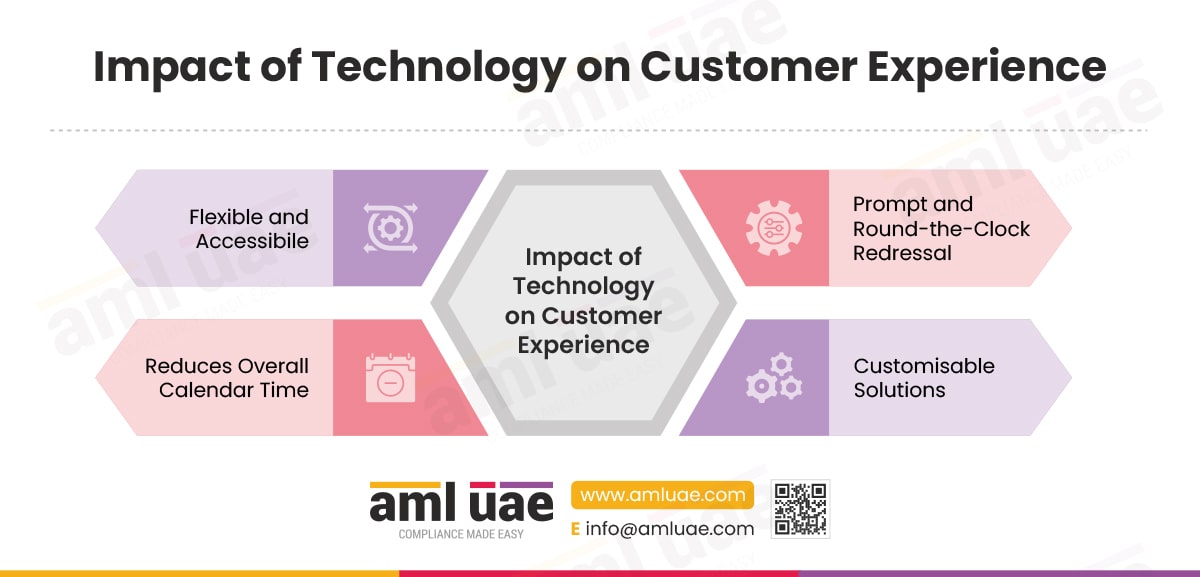

The Impact of Technology on Customer Experience

Increased efficiency and effectiveness of AML compliance instil trust and confidence in customers and make AML programs more dependable. Here are ways in which technology positively impacts customer experience:

- Automates compliance procedures involving customer participation, such as digital KYC, reducing overall calendar time and providing flexibility in information sharing.

- Perpetual KYC (pKYC) eliminates the need for repeated. Identity verification reduces the burden on customers.

- Chatbots resolve frequently raised queries, allowing prompt and hassle-free customer grievance redressal.

- Custom automation of e-mails supplements chatbots to provide context-specific answers to more complex questions.

- The anytime-anywhere flexibility options have increased the overall accessibility of the customer.

Significance of Quality Data in Digital Anti-Money Laundering Compliance

Data is the backbone of any AML program—traditional, Legacy, or Digital. Compliance professionals and software rely on available data to perform tasks from customer screening to reporting. Digital AML programs use Big Data. Big data refers to extremely large or voluminous data that is organised, structured, and continues to expand over time.

Big Data can be characterised by the 3Vs.

The 3Vs of Big Data are:

- Volume: The sheer quantity of information processed by AML software is beyond the capacity of any individual or group.

- Velocity: The AML software processes an enormous amount of information in fractions of a second, speeding up the time-consuming processes.

- Variety: The diverse nature of different data sets processed by AML software reduces the scope for any error or bias.

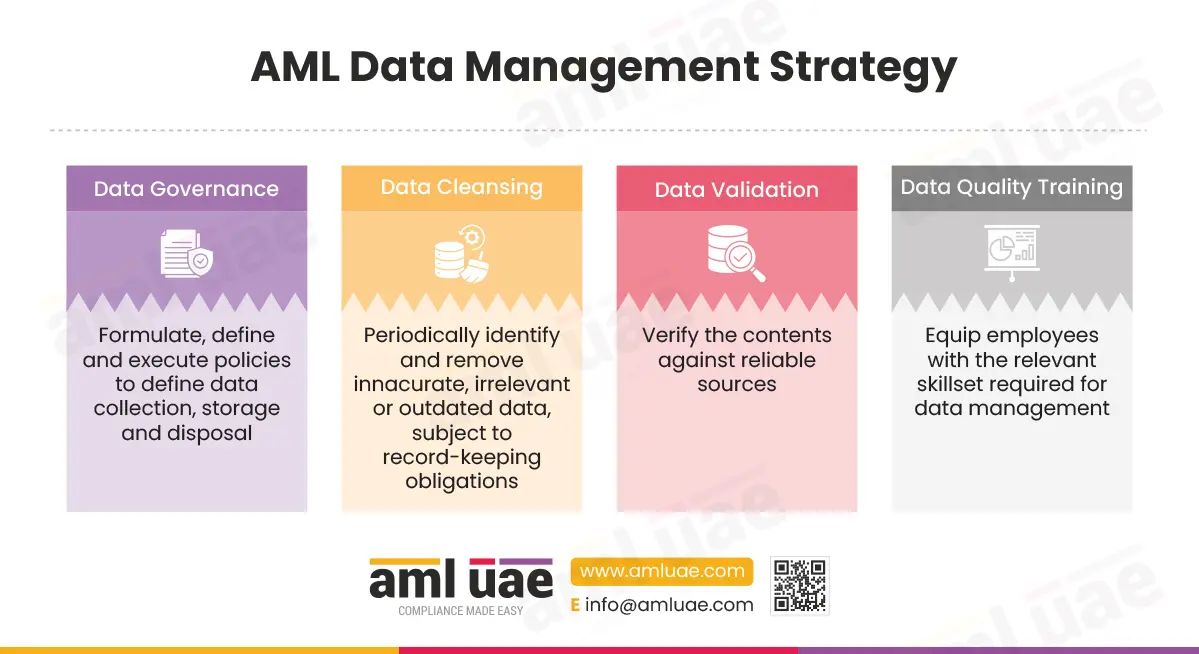

However, data is only as good as its quality. Good quality data is accurate, complete, consistent, and updated. Hence, it is crucial for reporting entities to ensure the authenticity of the data they use. Reporting entities can ensure high-quality data by implementing a data management strategy that includes:

Data Governance: The primary objective of Data Governance is to ensure that the data stored by any organisation is secure, accurate, accessible, and usable. The business must have an adequate data protection and privacy policy that determines the data collection, storage, and disposal protocols.

Data Cleansing: When data is gathered from multiple sources, replication, insufficiency, or inconsistency may occur. Data cleansing is identifying irregularities, fixing them, and deleting redundant data while considering record-keeping obligations.

Data Validation: Data Validation is a form of data cleansing which ensures that the data stored is accurate and credible by corroborating it with verified sources.

Data Quality Training: This training ensures that personnel know the value of quality and implement the principles of data governance from the first line of defence.

Step-By-Step Transition from Manual to Technology-backed AML Processes

For any business that has relied on manual AML/CFT compliance procedures for a long time, switching to digital measures might seem complex. So, here is a breakdown of steps a business should take before switching to advanced technological models for AML compliance:

1. Evaluate the current AML/CFT strategy: Assess the present risks and potential upcoming threats to the organisation and evaluate the effectiveness of current investigative programs in identifying suspicious activities.

2. Define the purpose of modernisation: Define a clear objective for adopting modern technology and the expected outcome to be achieved.

3. Prepare a blueprint and action plans: A clear strategy should be framed for achieving the goal considering the following factors:

- Specific: Identify specific processes that require technological intervention.

- Measurable: The outcome to be derived from digitalisation should be quantitative.

- Achievable: The goal should be set considering the relative expertise of staff and infrastructural availability.

- Relevant: Innovative RegTech solutions must resolve not just present but also potential future problems.

- Timely: There must be a desired timeline for step-by-step integration of new RegTech solutions.

4. Select Appropriate technological tools: Identify specific AML software or tools that meet organisational requirements.

5. Train the workforce: Provide appropriate technical assistance to the workforce and conduct pilot runs to ensure proper technology integration in the AML compliance system.

6. Implementation: Replace or update the existing systems with new AML compliance solutions and inform customers and other stakeholders.

7. Feedback and Reviews: Take regular feedback to customise the AML software accordingly.

Challenges in Adopting Technological Tools in AML Compliance

Lack of Regulatory Incentives

The current position of international and national regulatory authorities is neutral toward adopting modern technologies, with minimum to no incentives for organisations that invest in modern technologies.

Data Inconsistencies

Technological models rely on public and private, domestic, and international data. The lack of standard data increases the operational burden and cost for reporting entities. These inconsistencies restrict reporting entities from unlocking the full potential of big data analytics.

Data Privacy and Data Protection Concerns

AML compliance requires reporting entities to collect and store vast personal data, including biometrics and sensitive financial information. The lack of effective oversight mechanism to ensure proper data management and protection is a cause of concern.

The involvement of a third-party for providing technological services increases risk of breaches for customers and reporting entities alike, creating an environment of distrust among stakeholders. There is also a call for stricter regulation and supervision on RegTech service providers.

Greater transparency and accountability between regulated entities and their customers are needed to ensure the proper use of personal data.

Adoption and Application Issues

Reporting entities such as DNFBPs and VASPs have reservations about adapting to new and untested technological solutions and struggle with time, energy, and resources to train their staff to adopt modern technologies. It is difficult to incorporate technology into existing legacy systems, and complete replacement is even more challenging due to the complex nature of innovative solutions and the inadequate expertise of AML professionals. Moreover, smaller regulated entities lack the capacity to determine which solution works best for their risk appetite.

In practice, the complexity of adopting innovative solutions is far greater than traditional models. While the acceptance of traditional models is lower. Thus, businesses generally prefer a mix of traditional practices and innovative solutions.

Implementation and Associated Costs

Companies consider the cost of transitioning to digital AML programs to be more than the benefits and are reluctant to invest in modern technologies due to the potential complications in their integration into legacy systems. Many institutions lack the adequate digital infrastructure required for the implementation of innovative solutions. This may increase the cost burden when shifting to modern technologies.

Post-operational Challenges

Post implementation of a modern technology, entities often lack the technical ability to use the technology correctly and effectively. Technologies also become outdated and need further investment in newer solutions or they fail to satisfy regulatory requirements. Even in case of proper implementation, AI models are dependent on the data using human input, making them vulnerable to not just algorithmic bias but also human bias.

Want to settle the hiccups in your AML Software?

Get the AML software testing and validation services from the experts at an affordable cost!

Human Element in AML Compliance Automation

It is evident that technology is not the panacea for all AML challenges, and relying on just one model may not be the most prudent approach. There must be a constructive collaboration between the human element and automation. Most entities are now automating repetitive tasks while reserving strategic decision–making for experts who can be trusted to recognise, evaluate, and implement suitable mitigation measures for any residual risks posed by modern technologies.

Ideally, the efficiency and accuracy of digital solutions combined with the analytical abilities of an experienced workforce will result in a more responsible and reliable system that is compliant with regulatory requirements. Following are the ways to leverage technological solutions in manual processes:

- Separate strategic tasks from repetitive tasks: It is important to clearly differentiate strategic tasks that require careful consideration from repetitive tasks that can be easily automated.

- Foster a data-driven decision-making culture: It is important to develop a culture where any decision is backed by data to improve its authenticity.

- Combine AI accuracy with human experience: Technological tools suffer from various biases such as algorithmic bias, cognitive bias, technical bias, and novelty bias. These biases can lead to inaccurate and discriminatory results and high false positives. So, to safeguard the organisation from technological biases, it is important to establish a dual-check mechanism requiring human expertise.

- Supplement intuition with analysis: The years of human experience and expertise leveraged to identify red flags can be substantiated by an in-depth analysis using innovative solutions.

Cryptocurrency and RiskTech Solutions

Cryptocurrency is a type of virtual asset that is traded digitally across the globe. Unlike fiat money, government authority does not back cryptocurrency.

The speedy transferability and anonymity features of cryptocurrency make it a favourable destination for criminals to transfer the proceeds of their illegal activities through cross-border transactions. Currently, domestic and international guidelines are in place to restrict money laundering through cryptocurrencies.

For instance, the FATF has issued Guidance for a Risk-Based Approach to Virtual Assets and Virtual Asset Service Providers, The Virtual Asset Regulatory Authority (VARA) has published a rulebook on Virtual Assets Transfer and Settlement pursuant to the Virtual Assets and Related Activities Regulations 2023.

In this modern case of cosmic justice, where technology is the question, technology is also the answer. Cryptocurrency is backed by blockchain technology.

The ledger system of blockchain is immutable, so it records every transaction that occurs by way of cryptocurrency, and it is possible to track them later. KYC compliance can be another big deterrent to money laundering using crypto.

Best Practices to Follow in AML Compliance Automation

Here are a few the best practices to follow when adopting a modern technology to safeguard institutions from the adversaries in case of unavailability or misuse.

Ensure Responsible Adoption of New Technologies

- Institutions should establish a documented governance framework to ensure proper decision-making, management and control of the risks arising from the use of innovative solutions.

- Ensure that the Cloud Computing system is auditable by maintaining necessary records.

- Institutions should devise a comprehensive business continuity plan with the objective of maintaining the continuity of the service/process performed by the enabling technology in the event of an incident that adversely affects the availability of such technology.

Place Adequate Risk Mitigation Measures

Ensure that formal, independent reviews/audits of enabling technologies are conducted periodically.

Adhere to the Data Privacy and Data Protection Standards

Ensure that the AML software adheres to the data privacy and data protection standards to instil trust among customers and third parties.

Provide Effective Training to Relevant Personnel

Design training campaigns and provide hands-on experience to the employees and workers before implementing new compliance technologies.

Ensure Transparency

- Institutions should be transparent with their customers regarding the use of AI and big data analytics.

- Establish procedures and controls to safeguard customer profiles against vulnerabilities and unauthorised access or disclosure during the authentication process.

Future Technological Trends in AML Compliance

Looking forward, Artificial Intelligence and Machine Learning predictive analysis are set to take centre stage as opposed to a supportive role in identifying patterns, trends, and unusual behaviour. Here are the upcoming digital processes that may be applied in AML processes in times to come:

Biometric Processes

Biometric verification has so far transformed AML and KYC processes. Moving forward, multi-model biometric systems combining voice recognition and fingerprints with facial recognition will be a go-to option for regulators and reporting entities. It will be interesting to understand how safety will balance security.

Quantum Computing

According to scientific theories, quantum computers can use ‘Quantum Walks’ to reveal hidden transaction chains while examining parallel routes at once via transaction networks. This may allow regulatory authorities and reporting entities to uncover hidden connections among unrelated accounts that traditional computers are not able to recognise. Quantum Computers are quite a possibility for the future of AML compliance.

Open-Source Intelligence (OSINT)

Open-Source Intelligence is the intelligence produced by utilizing openly available information to address specific questions. With the increasing digitalization and globalization, the role of OSINT is analysing digital footprints, Dark Web monitoring and blockchain analysis is bound to grow.

AML personnel should, therefore, be open to new developments and technologies that make their task easier while being cautious of their incidental effects and keep investing in research and development to keep technological systems secure.

How can AML UAE assist you?

AML UAE can help you identify and document your AML/CFT automation requirements. We assist you in selecting the right AML technology for your compliance process automation. Be it KYC, Screening, Risk Assessment, AML Audit, Case Management, Transaction Monitoring, or Regulatory Reporting, we help you choose the best technology to automate your business functions.

FAQs

Anti-Money Laundering (AML) technologies use automated digital tools and solutions to assist in the prevention, detection, investigation, and reporting of suspicious activity.

Artificial Intelligence and its branches, such as Machine Learning, Big Data Analytics, Blockchain and Distributed Ledger Technology (DLT), Robotic Process Automation, Natural Language Processing Models, RegTech and RiskTech Solutions. Entities may adopt any of the tools depending on their industry and risk requirements.

Artificial Intelligence (AI) can be used to analyse vast amounts of data in real time and identify patterns; it can automate manual tasks such as transaction monitoring and customer due diligence; overall, it can streamline existing processes and make them faster and cost-effective.

Modern technologies can make anti-money laundering (AML) and counter–terrorism financing measures (CFT) quick, efficient, and cost-effective. Technology can enhance data collection, processing, and analysis and help regulators and regulated entities identify and manage money laundering and terrorist financing (ML/TF) risks more effectively in real–time.

RegTech solutions automate biometric verification, use facial recognition, voice recognition, or fingerprint scanning and document verification through optical character recognition (OCR) to verify passports, driver’s licenses, and other identity documents. RegTech also reduces the overall calendar time by allowing self-KYC and faceless KYC.

Effective AML consulting services

make your business dealings brighter, smoother, and better

Share via :

About the Author

Pathik Shah

FCA, CAMS, CISA, CS, DISA (ICAI), FAFP (ICAI)

Pathik is an ACAMS-certified AML consultant specialising in governance, risk, and compliance for regulated entities in the UAE. He brings over 28 years of experience, with 1,000+ hours of AML training and 200+ advisory engagements across DNFBPs, VASPs, and FIs. He supports businesses in aligning with AML/CFT requirements from the CBUAE, DFSA, MoET, MoJ, VARA, CMA, FSRA, and FATF. Known for translating complex regulations into audit-ready procedures, Pathik enables operational clarity and compliance readiness.

Reach Out to Pathik