Blogs

14 top videos on AML compliance: Defending against financial crime

In this article, we will explore 14 top videos which will help you understand various concepts and legal requirements around AML/CFT compliance. Starting with the goAML registration requirements to submitting various regulatory reports, including REAR, FFR, PNMR, SAR, and STR, it will help you develop a sound understanding of the AML compliance requirements.

Politically Exposed Person (PEP) and PEP screening requirements in UAE

This video will help you grasp the essential concepts around:

- Who the politically exposed person is, the Definition of PEP

- Who is covered within the definition of PEP, including the person himself and his associates

- What action you should take once you know someone is a PEP or associated with a PEP

- How to deal with domestic PEPs, foreign PEPs, and heads of international organizations.

- Why PEPs are treated as high-risk customers

- What are the deciding factors to conclude that a PEP carries high-risk

- How to manage ML/TF risks around PEPs

- What are the requirements for carrying out Enhanced Due Diligence (EDD) when working with Politically Exposed Persons

- Ongoing monitoring of transactions with PEPs

Chapters:

- 0:00 PEP Introduction

- 0:25 Who is PEP?

- 0:44 associated PEP

- 0:54 3 categories of PEP

- 1:06 Domestic PEP

- 1:12 Foreign PEP

- 1:18 Head of International Organization

- 1:29 High risk

- 1:38 Factors considered while determining PEP

- 2:11 MLFT Risk with associated PEP

- 2:34 KYC & EDD

- 2:41 Treated as High risk

- 3:15 Regarding PEP

Related Articles

Related Videos

Related Infographics

AML Business Risk Assessment (BRA) and how to conduct BRA

This video will help you understand the key concepts around the AML Business Risk Assessment (BRA). The AML Business Risk Assessment is also known as the Enterpiese-Wide Risk Assessment, Firm-Wide Risk Assessment, Entity-Wide Risk Assessment, or simply, ML/TF Risk Assessment.

- The need for AML Business Risk Assessment (BRA)

- Risk-Based Approach

- Risk appetite

- Risk Factors to consider while performing EWRA

- The concept of gross risk and how to arrive at it

- Evaluation of controls and their effectiveness

- The concept of net risk or residual risk and how to arrive at it

Chapters:

Related Videos

Related Articles

Related Infographics

Role of AML Compliance Officer under UAE AML Regulations

The ultimate responsibility to comply with UAE AML regulations remains with the top management, but the AML Compliance Officer is responsible for implementing the AML/CFT program in the company, imparting training to the staff, submitting regulatory reports, and overseeing the compliance function. This video will help you understand the role of the AML Compliance Officer in the entity.

- Key responsibilities of the AML Compliance Officer

- AML/CFT program development and its implementation

- Regular updates to the AML/CFT policies and procedures

- AML training program

- Suspicious Transactions Report (STR) and other regulatory reporting

- AML/CFT Record Keeping

Chapters:

Related Infographics

Related Articles

Related Videos

Know Your Customer Process under UAE AML Regulations

This video focuses on the Know Your Customer (KYC) requirements under the UAE AML Regulations. It helps you understand various concepts and requirements around customer identification and customer verification. The video highlights various important aspects of KYC:

- What is Know Your Customer (KYC)

- KYC requirements for individual customers

- KYC requirements for corporates

- Why maintain a standardized KYC form

Related Articles

- What is Know Your Customer (KYC)?

- Best practices for KYC compliance

- Accurate AML Compliance with KYC Automation

- KYC Transformation From Manual KYC Checks to Automated

- Know the Differences between KYC and AML

- Identity Verification for Partnership Firms: Navigating the essential element of customer onboarding under UAE AML Law

- Know Your Transaction (KYT) and Know Your Virtual Asset Service Providers (KYV)

- Customer Lifecycle Management and AML Compliance in the Digital World

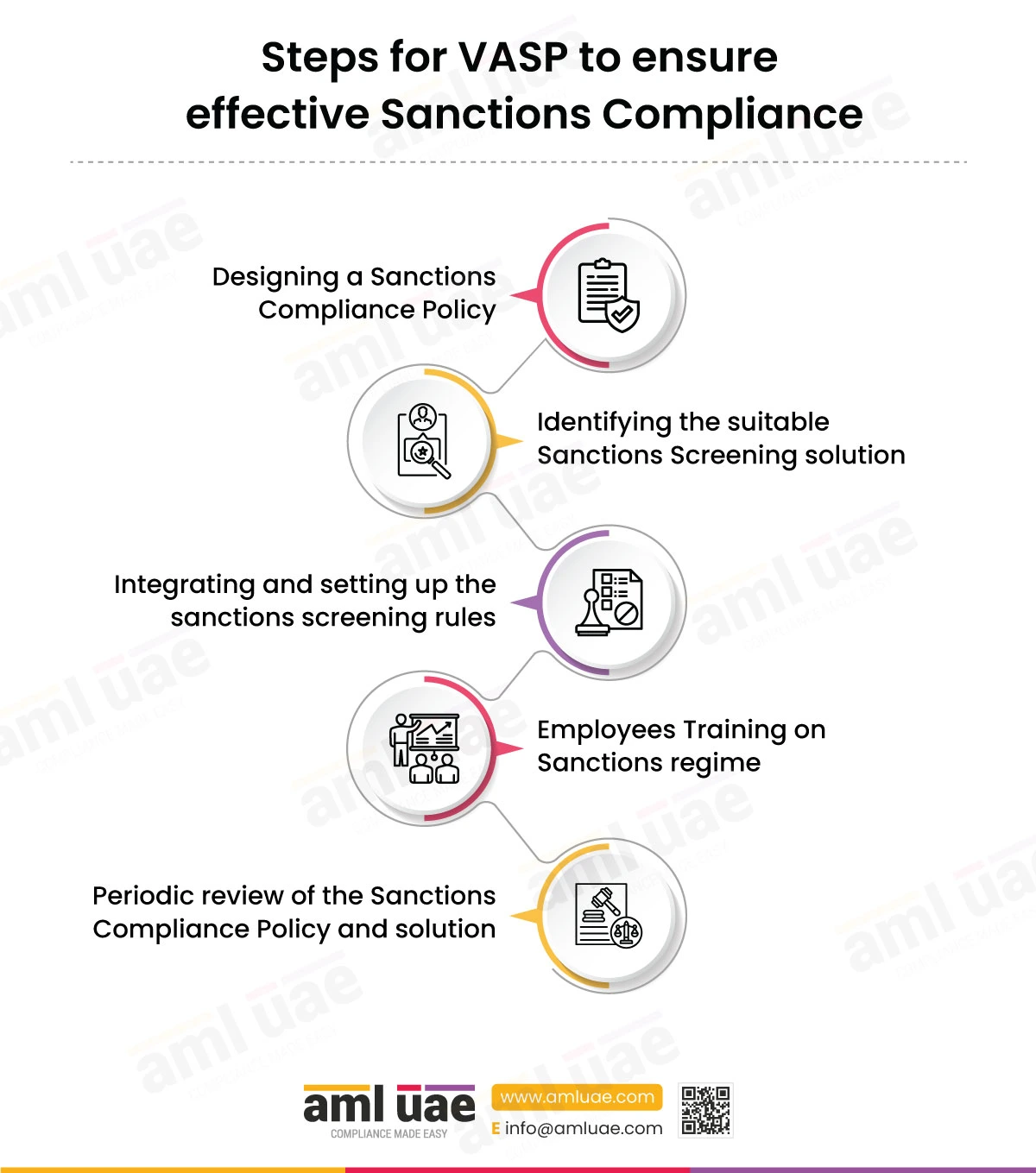

Sanction Screening in UAE

This video will help you understand the basic concepts around sanctions screening, what it is, what sanctions list to include as per UAE AML requirements, how to conduct sanctions screening, and more:

- What is sanctions screening

- UAE Local List and UNSC List

- When to conduct sanctions check

- The requirements around the EOCN mailing list subscription

- Sanctions screening process

- What to while dealing with sanctioned individuals and entities

- Partial Name Match and Fund Freeze Report Submission with the FIU goAML portal

Chapters:

Related Videos

Related Infographics

- Sanctions screening regulatory requirements in UAE

- Countering the Proliferation Financing: Concept and Mitigation Measures

- Filing of Fund Freeze Report (FFR) under UAE AML Laws

- PEP and PEP Screening under UAE AML Regulations

- PEP Screening Guide

- Filing of Partial Name Match Report (PNMR) under UAE AML Laws

Related Articles

- A Guide to Sanction and PEP Screening in Customer Onboarding Process

- What is a sanction list?

- Targeted Financial Sanctions (TFS): Legal Requirements in UAE

- Sanctions Compliance by VASPs in UAE: Safeguarding the Virtual Asset segment against financial crimes

- TFS Implementation Criteria: Ownership, Control, and Acting on behalf of a Designated Person

- What are Economic Sanctions?

- Choosing an apt AML Software for DPMS

- Updated list of FATF high-risk countries and countries under increased monitoring

- How do you do a Sanction Screening?

- Role of FATF: The Financial Action Task Force

- What are FATF Blacklist and Grey list countries?

- The Challenges of The Sanction Screening Process

- Simple Guide to Subscribe to Sanctioned List

- The Role of Sanctions in Achieving International Peace and Security

- Socio-economic impact of money laundering

- Funds Freeze Report (FFR) and Partial Name Match Report (PNMR) filing with goAML

- What is Proliferation and Proliferation Financing?

- A complete guide to global AML regulations

Elements of an effective AML Policy and Procedures

This video will help you understand the elements of an effective AML policy and procedures. Regarding AML/CFT policy and procedures, it is important to get it approved by top management. The video touches upon the important aspects around risk identification, risk-based approach, customer onboarding, identification and reporting of suspicious transactions, other reporting requirements, record keeping, governance, and targeted financial sanctions (TFS).

Chapters:

Related Articles

Related Templates

- AML Policy Template for the VASP in UAE

- AML Policy Template for the Trust and Company Service Providers (TCSP) in UAE

- AML Policy Template for the Jewellers in UAE

- AML Policy Template for the lawyers, notaries, and other legal professionals in UAE

- AML Policy Template for Real Estate Agents and Brokers in UAE

- AML Policy Template

Related Infographics

Staying ahead in AML compliance: Understanding when to file STRs

This video highlights the importance of knowing red flags around suspicious activities and suspicious transactions. It will help you distinguish between suspicious activities and suspicious transactions. Further, it provides information about the regulatory reporting requirement in the form of a Suspicious Transaction Report. It will help you understand when you are supposed to file STR with the goAML portal maintained by the UAE, FIU.

- What is STR

- Who is obligated to submit STR with goAML portal maintained by the FIU, UAE

- The distinction between a Suspicious Activity and a Suspicious Transaction (SAR vs STR)

- Red flags indicating a suspicious transaction

- STR submission

Related Videos

Related Infographics

Compliance with AML Laws: Guide to Filing a Fund Freeze Report

This video highlights the important procedure around filing a Fund Freeze Report with the goAML portal. A fund Freeze Report must be filed with the FIU goAML portal when a regulated entity finds a match with the UNSC or UAE local list. It also highlights the importance of sanctions screening.

- What is a Fund Freeze Report

- When to file a Fund Freeze Report

- Sanctions Screening

- What to do when you find a confirmed match with the sanctions list

- Timeline for filing Fund Freeze Report

Chapters

Related Articles

- Funds Freeze Report (FFR) and Partial Name Match Report (PNMR) filing with goAML

- A Guide to Sanction and PEP Screening in Customer Onboarding Process

What is a sanction list?

Targeted Financial Sanctions (TFS): Legal Requirements in UAE

Sanctions Compliance by VASPs in UAE: Safeguarding the Virtual Asset segment against financial crimes - TFS Implementation Criteria: Ownership, Control, and Acting on behalf of a Designated Person

- What are Economic Sanctions?

- Choosing an apt AML Software for DPMS

- Updated list of FATF high-risk countries and countries under increased monitoring

- How do you do a Sanction Screening?

- Role of FATF: The Financial Action Task Force

- What are FATF Blacklist and Grey list countries?

- The Challenges of The Sanction Screening Process

- Simple Guide to Subscribe to Sanctioned List

- The Role of Sanctions in Achieving International Peace and Security

- Socio-economic impact of money laundering

- What is Proliferation and Proliferation Financing?

- A complete guide to global AML regulations

Related Videos

Related Infographics

- Sanctions screening regulatory requirements in UAE

- Countering the Proliferation Financing: Concept and Mitigation Measures

- Filing of Fund Freeze Report (FFR) under UAE AML Laws

- PEP and PEP Screening under UAE AML Regulations

- PEP Screening Guide

- Filing of Partial Name Match Report (PNMR) under UAE AML Laws

Checklist for Filing STR and SAR on the goAML portal

This video will help you understand the importance of an AML/CFT program and how your policies and procedures should be defined to ensure reporting all suspicious activities and transactions to the UAE FIU.

- Identification of suspicious activities and suspicious transactions

- Procedures around Internal Suspicious Transactions Reoprt (STR) and Internal Suspicious Activity Report (SAR)

- Preliminary investigation by the compliance officer

- Decision to submit SAR or STR with the goAML portal

- Supporting Documents around SAR or STR

- Submission of SAR or STR on the goAML portal

Chapters:

Related Videos

Related Articles

Related Infographics

Money Laundering 101: Three Stages of Money Laundering

Money laundering is a global concern, with an estimated 2-5% of global GDP being laundered every year. This video will help you understand the three stages of money laundering, viz., placement, layering, and integration:

- Three stages of money laundering

- Placement

- Layering

- Integration

Chapters:

Related Infographics

Related Articles

Related Videos

Filing of Real Estate Activity Report (REAR) on goAML

Real estate agents, brokers, lawyers, and independent legal firms must report specified transactions related to real estate to FIU in the prescribed format called Real Estate Activity Report (REAR). This video will help you understand various requirements around REAR report submission.

- REAR applicability to Real Estate Agents and Brokers

- REAR applicability to lawyers and independent legal firms

- Circumstances warranting submission of REAR on the goAML portal

- REAR applies to buying and selling of freehold property only

- Monetary threshold around REAR submission for cash and crypto transactions

- Documents to be submitted along with REAR

Chapters:

Related Templates

Related Infographics

Related Articles

- Role of an AML Compliance Officer in a real estate agent or brokerage firm in UAE

- AML Compliance Requirements for Law Firms in UAE

- A detailed analysis of the AML/CFT requirements for lawyers, notaries, and legal professionals in the UAE

- A deep dive into the AML compliance requirements for the real estate sector in the UAE

- Conducting Independent AML Audits in DNFBPs: A Comprehensive Handbook

- Enhanced Money Laundering Risks In The Real Estate Sector

Related Videos

goAML Registration in the UAE

Financial Institutions, Virtual Asset Service Providers, and Designated Non-Financial Businesses and Professions (DNFBPs) must register on the goAML portal to fulfill their regulatory reporting requirements. In this video, we will look at the process of registering on the goAML portal.

- What is goAML portal

- The objective behind UAE FIU’s goAML portal

- Entities required to register on the goAML portal

- The two-stage process of goAML Registration

- SACM Registration – First Stage of goAML Registration

- Second Stage of goAML Registration

- Documents required for goAML Registration

- Regulatory Reporting on goAML Portal

Chapters:

- 0:00 Introduction to goAML Registration

- 0:39 Objectives of goAML platform

- 1:04 Entities to detect and report suspicious transactions

- 1:26 SACM Registration on goAML portal

- 1:48 goAML Registration using Google Authenticator

- 2:23 Documents needed for goAML Registration

- 3:00 AML-related reports to be Submitted after approval

- 3:30 Conclusions

Related eBook

Related Infographics

- Reporting on goAML Portal under UAE AML Regulations

- Simplifying UAE FIU goAML Registration: A Visual Guide

- Checklist for filing STR and SAR on goAML portal under UAE AML Laws

Filing of Real Estate Activity Report (REAR) on goAML under UAE AML Laws - Filing of Partial Name Match Report (PNMR) under UAE AML Laws

- Filing of Fund Freeze Report (FFR) under UAE AML Laws

- When to file STR under UAE AML Law?

- When to file SAR under UAE AML Law?

Related Articles

Related Videos

- A Guide to Anti Money Laundering AML Laws in UAE | DNFBPs

- Differentiating: Suspicious Activity vs. Suspicious Transaction

- Staying Ahead in AML Compliance: Understanding When to File STRs

- Checklist For Filing STR and SAR on the goAML Portal

- Compliance with AML Laws: Guide to Filing a Fund Freeze Report (FFR)

- Essential Element of Sanctions Compliance in UAE – Filing Partial Name Match Report

- Sanctions Compliance in UAE and Conducting Sanctions Screening Using AML Software

Defeating Financial Crime: Inside the AML Training Program

The video provides essential insights into the coverage of the AML training program. In order to succeed in fighting financial crimes, the reporting entity must get support from the top management and the employees. The employees must know various typologies and red flags to counter money laundering and terrorist financing. In this video, we will look at the critical topics that must be included in the AML training program of the entity.

- What is ML/TF, typologies, red flags, case studies

- AML/CFT laws and regulations in the UAE

- International organisations – FATF, UNSC, MENAFATF, etc.

- Enterprise-wide Risk Assessment

- AML/CFT Policy, Procedures, and Controls

- KYC, CDD, EDD, Customer Risk Assessment

- Transaction Monitoring

- Regulatory reporting requirements

- Governance Structure

- Sanctions compliance

- Record-keeping requirements

Chapters:

- 0:00 Introduction on Defeating Financial Crime

- 0:43 Aspects of AML training program

- 0:53 ML/FT Concepts

- 1:01 AML regulations in UAE

- 1:08 International efforts to fight ML/FT

- 1:16 goAML Registration

- 1:21 Business Risk Assessment

- 1:30 Customer Onboarding

- 1:40 Enhanced Due Diligence

- 1:50 Ongoing Monitoring

- 1:59 Suspicious transactions

- 2:15 Record Keeping

- 2:23 Roles and responsibility of the compliance officer

- 2:30 AML Compliance program and governance

- 2:45 TFS Implementation

- 2:54 Reporting with FIU

- 3:04 Ultimate Beneficial Owner

- 3:14 Conclusion

Related Videos

- A Guide to Anti Money Laundering AML Laws in UAE | DNFBPs

- Differentiating: Suspicious Activity vs. Suspicious Transaction

- Staying Ahead in AML Compliance: Understanding When to File STRs

- Checklist For Filing STR and SAR on the goAML Portal

- Compliance with AML Laws: Guide to Filing a Fund Freeze Report (FFR)

- Essential Element of Sanctions Compliance in UAE – Filing Partial Name Match Report

- Sanctions Compliance in UAE and Conducting Sanctions Screening Using AML Software

- Politically Exposed Person Screening (Hindi)

- Politically Exposed Person Screening (Gujarati)

- Politically Exposed Person – PEP Screening Requirements in UAE

- Factors for AML Enterprise Wide Risk Assessment

- Promoting Compliance Culture: Role of Senior Management towards AML

- Differentiating: Suspicious Activity vs. Suspicious Transaction

- A Guide to Anti Money Laundering AML Laws in UAE | VASPs

- AML Business Risk Assessment and How to Conduct Business Risk Assessment

- Role of AML Compliance Officer under UAE AML Regulations

- Know Your Customer Process under UAE AML Regulations

- Elements of an Effective AML Policy and Procedures

- Money Laundering 101: Three Stages of Money Laundering

- goAML Registration in the UAE

Related Infographics

- Reporting on goAML Portal under UAE AML Regulations

- Simplifying UAE FIU goAML Registration: A Visual Guide

- Checklist for filing STR and SAR on goAML portal under UAE AML Laws

Filing of Real Estate Activity Report (REAR) on goAML under UAE AML Laws - Filing of Partial Name Match Report (PNMR) under UAE AML Laws

- Filing of Fund Freeze Report (FFR) under UAE AML Laws

- When to file STR under UAE AML Law?

- When to file SAR under UAE AML Law?

- PEP and PEP screening under UAE AML Regulations

- AML UAE PEP Screening Guide

- An illustrative list of factors for conducting AML Business Risk Assessment

- How to conduct AML Business Risk Assessment?

- Enterprise Risk Assessment

- Sanctions screening regulatory requirements in UAE

- Countering the Proliferation Financing: Concept and Mitigation Measures

- Role of AML Compliance Officer in UAE

- Elements of AML Compliance Officer’s Report to Senior Management under UAE AML Regulations

- What are the basic elements of AML Policy in UAE?

- Checklist for implementing an effective AML Program

- AML Compliance Framework with adequate Transaction Monitoring Rules

- How Suspicious Transaction differs from Suspicious Activity under UAE AML regulations

- Stages of money laundering

- Terrorist financing process

- UAE’s 12 Strategic Goals to fight money laundering and terrorism financing

- AML Compliance Requirements in UAE

- AML Compliance Journey for VASPs in UAE

- Filing of Real Estate Activity Report (REAR) on goAML under UAE AML Laws

- Exploring the ML/FT risk indicators associated with Real Estate Sector

Related Articles

- Suspicious Transaction Reports (STRs) filing with goAML portal of FIU UAE

Funds Freeze Report (FFR) and Partial Name Match Report (PNMR) filing with goAML - High-Risk Country Reporting: HRC and HRCA

- A guide to Anti Money Laundering AML Laws in UAE | 2023

- The risk-based approach in Anti-Money Laundering Compliance

- Risk-Based Approach For Dealers in Precious Metals and Stones (DPMS)

- AML implications for Politically Exposed Person (PEP)

- A Guide to Sanction and PEP Screening in Customer Onboarding Process

- What is Know Your Customer (KYC)?

- Best practices for KYC compliance

- Accurate AML Compliance with KYC Automation

- KYC Transformation From Manual KYC Checks to Automated

- Know the Differences between KYC and AML

- Identity Verification for Partnership Firms: Navigating the essential element of customer onboarding under UAE AML Law

- Know Your Transaction (KYT) and Know Your Virtual Asset Service Providers (KYV)

- Customer Lifecycle Management and AML Compliance in the Digital World

- What is a sanction list?

Targeted Financial Sanctions (TFS): Legal Requirements in UAE

Sanctions Compliance by VASPs in UAE: Safeguarding the Virtual Asset segment against financial crimes - TFS Implementation Criteria: Ownership, Control, and Acting on behalf of a Designated Person

- What are Economic Sanctions?

- Choosing an apt AML Software for DPMS

- Updated list of FATF high-risk countries and countries under increased monitoring

- How do you do a Sanction Screening?

- Role of FATF: The Financial Action Task Force

- What are FATF Blacklist and Grey list countries?

- The Challenges of The Sanction Screening Process

- Simple Guide to Subscribe to Sanctioned List

- The Role of Sanctions in Achieving International Peace and Security

- Socio-economic impact of money laundering

- What is Proliferation and Proliferation Financing?

- A complete guide to global AML regulations

- AML Compliance Officer: Role and Responsibilities

Role of an AML Compliance Officer in a real estate agent or brokerage firm in UAE - The Vital Role of an AML Compliance Officer in Safeguarding VASPs in the UAE

- What skills should an AML compliance officer possess?

- What are the Important terms in the AML-CFT Compliance Program?

- A guide To establishing an Effective AML/CFT Framework in your business

- What is Placement in Money Laundering?

- What is Layering in Money Laundering?

- What is smurfing in money laundering? Smurfing technique, risks, and protective measures

- Role of an AML Compliance Officer in a real estate agent or brokerage firm in UAE

- AML Compliance Requirements for Law Firms in UAE

- A detailed analysis of the AML/CFT requirements for lawyers, notaries, and legal professionals in the UAE

- A deep dive into the AML compliance requirements for the real estate sector in the UAE

- Conducting Independent AML Audits in DNFBPs: A Comprehensive Handbook

- Enhanced Money Laundering Risks In The Real Estate Sector

Related eBook

Mitigating high MLFT risk with Enhanced Due Diligence

This video focuses on the Enhanced Due Diligence (EDD) which is an advanced/ extended form of Customer Due Diligence, wherein additional checks are required to be done to manage the increased financial crime risks. The regulated entities (Financial Institutions, DNFBPs and Virtual Asset Service Providers) are required to undertake robust and rigorous version of CDD when it involves high risks customers. This video will help you understand what is EDD, situations when EDD is to be performed and measures to be applied. Following measures can be adopted to be performed as part of EDD.

- Entities must increase the scrutiny around customer identities to ensure that customers are what they say they are.

- Entities must get more information on the customer’s business, products, or services and conduct detailed inquiries about the purpose of the business relationship.

- Entities must determine the legitimacy of the customer’s source of funds and wealth.

- A thorough background search on the customers must be performed through public and private databases, internet research, social media, and adverse media checks to understand the customer’s connections with financial crimes.

- The customer profile must be subject to increased monitoring.

- The regulated entities must get senior management approval before establishing any business relationship or transaction with high-risk customers.

- Asking the customer to make the first payment from the bank account in its name, ensuring the third-party funds are not used in the proposed business relationship or transaction.

Chapters:

- 0:00 Introduction on Enhanced due diligence

- 0:31 Meaning of EDD

- 0:58 Performing the KYC process

- 1:22 High-risk customers

- 1:36 High-risk countries

- 1:43 Doubt about the appropriateness

- 1:50 Red flag indicators

- 2:01 Increase scrutiny around customer identities

- 2:25 Getting more information on customer’s business

- 2:39 Thorough background check

- 2:51 Detailed analysis and frequent monitoring

- 3:01 Management approval

- 3:10 Insist 1st payment from bank account

- 3:21 Short brief on EDD

Related Videos

Related Articles

Related eBook

Related Infographics

- What does Enhanced Due Diligence (EDD) help you with?

- Applying Enhanced Due Diligence measures under UAE AML Regulations

- Elements of the Customer Due Diligence Process

- Source of funds and source of wealth

- Customer Due Diligence Process Chart

- Understand the types of CDD measures to effectively mitigate the ML/FT risks

Make significant progress in your fight against financial crimes,

With the best consulting support from AML UAE.

Share via :

About the Author

Pathik Shah

FCA, CAMS, CISA, CS, DISA (ICAI), FAFP (ICAI)

Pathik is an ACAMS-certified AML consultant specialising in governance, risk, and compliance for regulated entities in the UAE. He brings over 28 years of experience, with 1,000+ hours of AML training and 200+ advisory engagements across DNFBPs, VASPs, and FIs. He supports businesses in aligning with AML/CFT requirements from the CBUAE, DFSA, MoET, MoJ, VARA, CMA, FSRA, and FATF. Known for translating complex regulations into audit-ready procedures, Pathik enables operational clarity and compliance readiness.

Reach Out to Pathik