Blogs

Last Updated: 12/17/2025

Protect your business with reliable and effective AML strategies with AML UAE.

AML/CFT Remedial Action Plans at a Glance

- RAPs are corrective roadmaps used to address AML/CFT deficiencies identified by regulators or audits

- A RAP clearly defines issues, remedial actions, ownership, timelines, and validation, ensuring accountable remediation.

- Strong governance, monitoring, and reporting are critical to demonstrate progress, transparency, and regulatory compliance.

- Proper RAP execution strengthens long-term AML/CFT controls.

What Is a Remedial Action Plan (RAP) in AML/CFT?

A Remedial Action Plan (RAP) is also referred to as remediation action plan, compliance remediation plan or simply a remedial plan; which is a structured corrective program used in AML/CFT framework that Regulated Entities implement when supervisory authorities identify gaps, deficiencies or breaches in their AML/CFT compliance program.

When Is an AML/CFT Remediation Action Plan Required?

An AML/CFT Remediation Action Plan is required whenever regulators or internal audits identify weaknesses, gaps, or non-compliance within an entity’s AML framework. This may occur after supervisory inspections, regulatory notices, or when institution itself detects failures in due diligence, monitoring, sanctions, screening, reporting, or governance.

Authorities may require an entity to implement a regulatory compliance remediation program when risk management controls are inadequate or when serious breaches occur. Entities may also voluntarily initiate AML remediation as a part of broader compliance remediation strategy to proactively fix issues before they escalate.

Key Components of an Effective Remedial Action Plan Template (RAP Template)

An effective Remedial Action Plan (RAP) template also referred to as a remedial plan template provides a structured format for documenting and executing corrective actions.

The key components of a remediation action plan template cover what needs to be fixed, how it will be fixed, who is responsible, the timeline for completion and how remediation will be validated.

A compliance action plan template clearly outlines identified issues, the remedial actions required, ownership and accountability, priority level, timelines, and resources needed for completion, along with validation methods and reporting status to evidence progress and closure.

A solid remedial action plan template typically includes steps related to updating policies, improving CDD/EDD processes, enhancing internal controls, rectifying reporting failures (e.g. STR delays), staff training, progress monitoring and evidence-based validation to demonstrate regulatory compliance.

AML remediation ensures the entity meets regulatory expectations, reduces ML/TF risk, and prevents penalties or supervisory actions.

Governance, Oversight, and Regulatory Reporting for RAP Execution

In the UAE, strong governance and oversight are essential for executing a Regulatory Action Plan (RAP) in line with national AML/CFT program requirements. Regulators such as the Central Bank of the UAE (CBUAE), Ministry of Economy & Tourism (MoET), Securities and Commodities Authority (SCA), Dubai Financial Services Authority (DFSA), and Financial Services Regulatory Authority (FSRA) expect entities to maintain robust RAP monitoring, and timely progress tracking.

Regular internal reviews and a formal RAP Audit process help ensure accurate AML reporting and demonstrate transparency and accountability throughout the remediation process.

AML/CFT Remedial Action Plan (RAP) Implementation Steps and Best Practices

As a part of its supervisory function, the relevant Supervisory Authority conducts investigations on the level of AML/CFT compliance of a regulated entity (Financial Institution, Designated Non-Financial Business or Profession – DNFBP, Virtual Asset Service Provider – VASP). The Supervisory Authority often issues an AML/CFT Remedial Action Plan directing the reporting entity to fill the gaps in its AML/CFT compliance framework or implementation. The Remedial Action Plan (RAP) enumerates the actions to address these identified deficiencies. It mentions the applicable provision, area of concern, and required remediation.

Some of these AML/CFT investigations carried out by the Supervisory Authority to include various aspects such as:

- Review of Enterprise-Wide Risk Assessment carried out by the entity

- Adoption of necessary policies, procedures, and controls for the AML framework

- On-time submission of STRs, SARs, DPMSR, REAR, HRC, HRCA, CNMR, PNMR, and other sector-relevant reports to the FIU

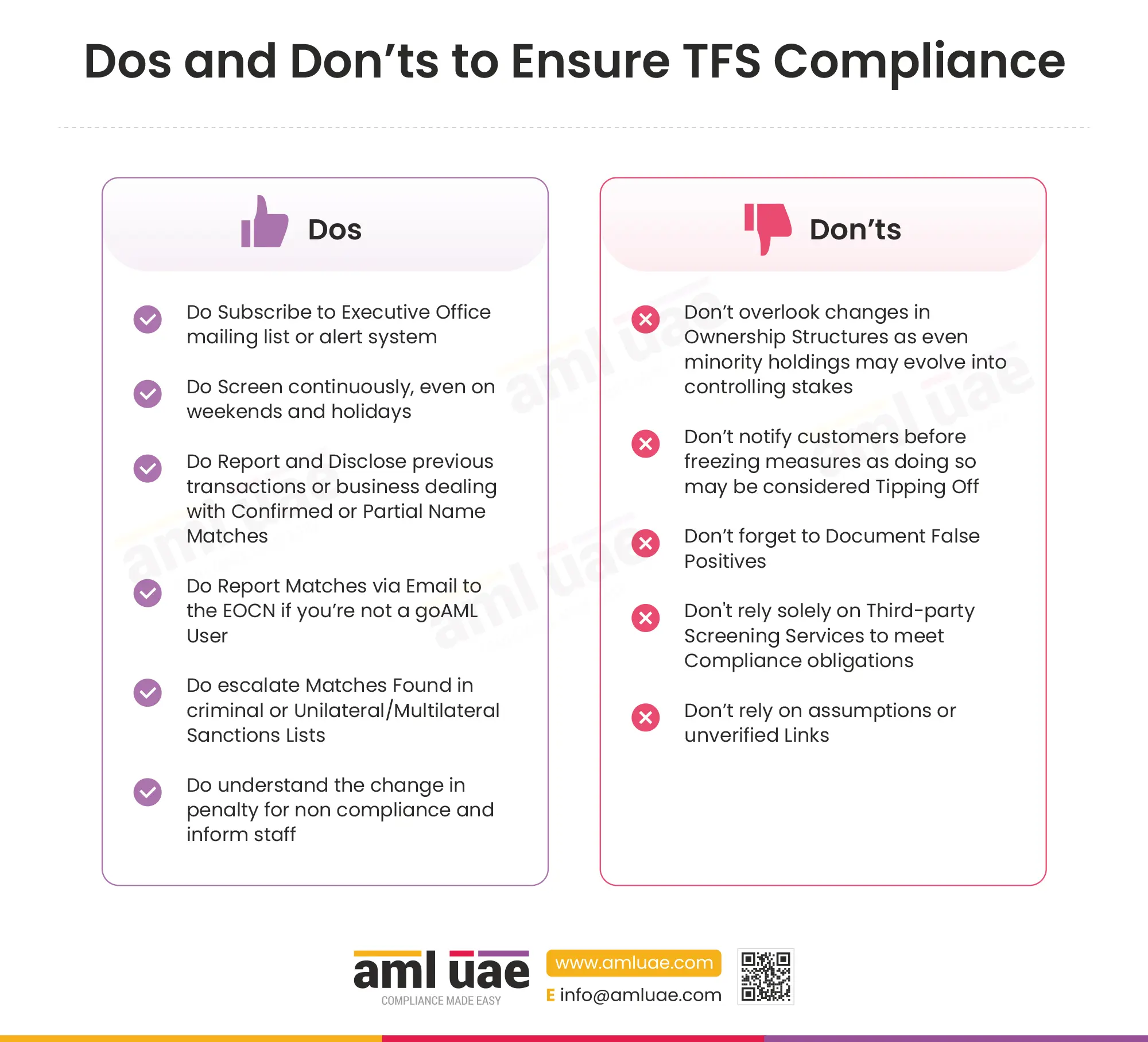

- Compliance with Targeted Financial Sanctions (TFS) requirements

- Compliance with Proliferation Financing (PF) requirements

- Identification and verification of customers through KYC, CDD, and AML screening

- Ongoing monitoring of transactions and business relationship

- Appointment of an AML compliance officer and dedicated team to ensure AML compliance

- Measures for understanding the reason and type of business relationships

- Implementation of enhanced due diligence measures against high-risk customers

- Training programs for employees for AML awareness and methods

- Record-keeping requirements compliance

Entities receiving such remediation action plans from the Supervisory Authority must understand their importance. It is an opportunity for you to improve your AML Compliance Program. Such improvements can lead to the prevention or mitigation of money laundering threats. So, you must commit to following and implementing the action plans in your business.

Worried about the deficiencies in your AML compliance framework?

Talk to our team for a complete, effective, and efficient AML action plan.

Step-by-Step Procedure to Implement the Remedial Action Plan (RAP)

Once a Remedial Action Plan is issued, the next stage for the entity is to initiate the step-by-step RAP implementation, by following the requisite RAP implementation and remediation steps:

1. Review the complete remedial action plan word-by-word

The first thing that you must do is review the remedial action plan thoroughly. Read every word of RAP and try to understand. Specifically, focus on the remediation strategy suggested by the Supervisory Authority. Make a note of the submissions you need to make to the authorities.

Ask the Supervisory Authority for more guidance if you do not understand any part of it. Also, discuss with the AML compliance team and the officer if they are unclear on any topic. The senior management and AML compliance team must understand every plan aspect and discuss the execution amongst themselves.

2. Deliberate over the plan with stakeholders

The compliance team and the relevant manager must have all information on this remedial action plan. So, it would be best if you discussed it with everyone involved in AML compliance tasks. They must know the loopholes and participate in deciding the actions you need to take.

It’s equally critical to discuss the impending changes for employees. To prepare for them, employees must know what changes will come in the processes. They must also learn about their roles in executing these remedial actions and how they can contribute to better AML compliance for the entity.

3. Make a list of the tasks and set priorities

When you review and discuss the remedial action plan with stakeholders, you must list the tasks. You must assess the remedial activities to understand their importance and urgency. Now, list them per their priority.

You can define a strategy, including the tasks, resources required, and time needed. You will be clear on what to do and how long it will take. Thus, you can take a proactive approach to address the serious issues first, followed by the unimportant ones.

4. Form a team focused on the execution of the RAP

Already, you have an AML compliance team handling all the specific tasks related to AML. For RAP, make a special team focusing on implementing the recommendations. The other AML team members must pay attention to the daily AML tasks and activities.

Once you select the remedial action plan execution team members, define their roles. Allocate responsibilities to each to manage every single task mentioned in RAP. Also, ensure the appointment of a manager or auditor who will oversee the quality performance of these tasks.

5. Execute the remedial measures

Once you form the team, you are ready for the actual action. You must manage it quickly and accurately to comply with the RAP before the deadlines. So, start the execution.

Implement each of the actions as mentioned in the RAP. Monitor each action and check the quality of deliverables. Keep assessing the deliverables at every step to ensure compliance with the law and RAP.

6. Maintain enough records and documents

The RAP will need you to submit some reports or documents by a specific date. You must prepare these reports in the required format and structure. Be ready with them for submission to the Authority before the deadline date.

Also, maintain records and documents of each action you have taken per the RAP. You might be asked for them during audits or if the Authority wants to check the compliance with the Remedial Action Plan. Keep track of the deadlines mentioned by the Supervisory Authority, as compliance before that is mandatory.

7. Update the Supervisory Authority on the progress and support needed

You must stay in constant communication with the Supervisory Authority. Regular communication lets you clarify your doubts on any point mentioned in the RAP. You must also update the Authority on the actions taken and the success achieved. The Authority must know the effectiveness of the remedial measures you took. The Compliance Officer and the Senior Management must sign the RAP.

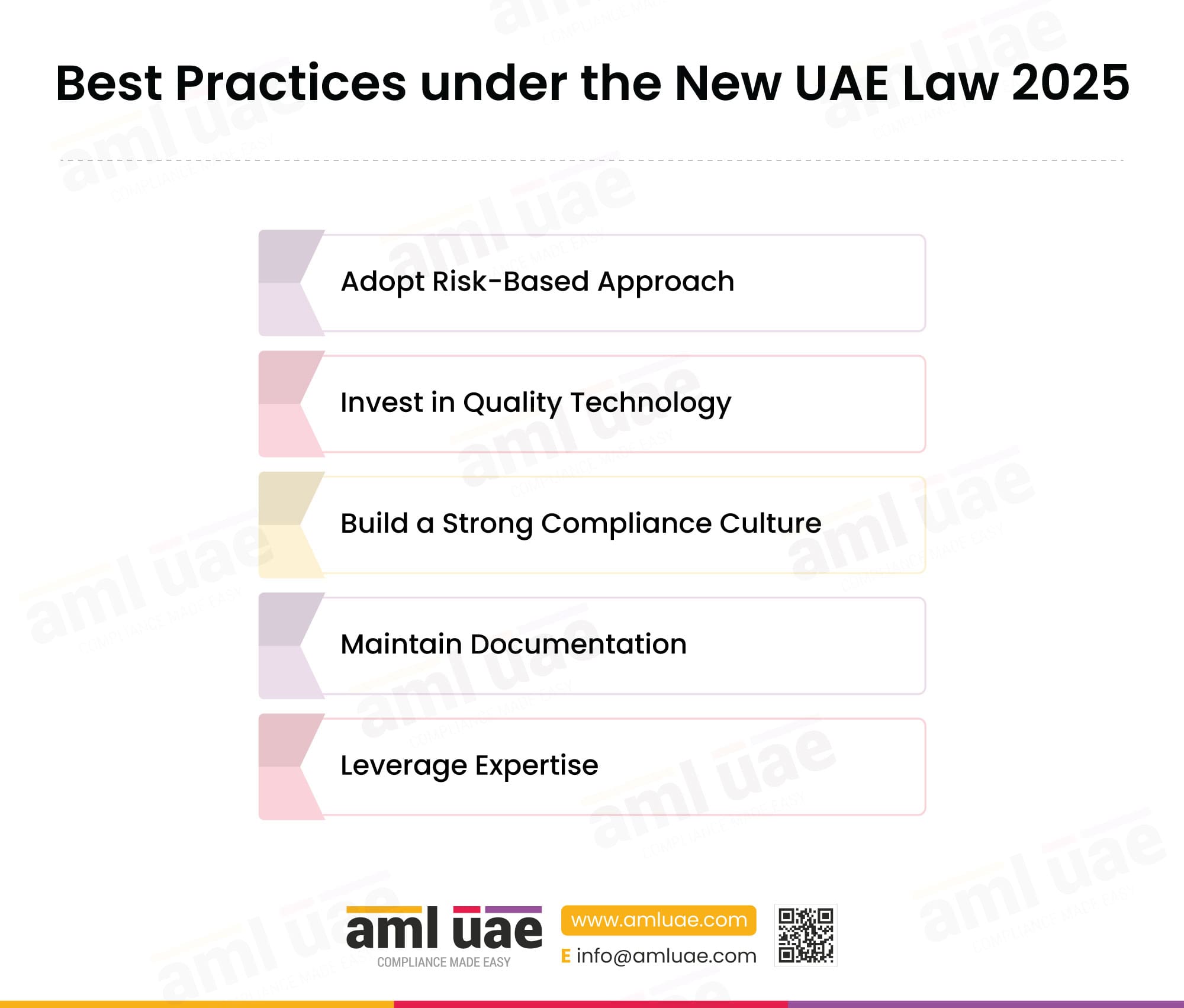

Best Practices to Implement Remedial Action Plan:

Implementing an AML/CFT Remedial Action Plan requires a disciplined and a structured approach. An effective compliance remediation strategy focuses on addressing gaps, strengthening control, improving documentation and building long-term AML/CFT compliance resilience.

Adopting the following remediation best practices help entities establish a robust compliance environment.

Make continuous improvements in AML processes

The remediation strategies mentioned by the Supervisory Authority are an opportunity for you to improve your AML program. You know the usual mistakes you make. Also, you know the expectations of the Authority from you.

So, revamp your AML compliance program. Include steps of constant monitoring and improvement to align with the regulatory expectations. Review the areas with gaps and improve them. Monitor the internal processes and AML controls and tweak them for higher effectiveness.

Thus, the RAP gives you a direction to follow to make your operations AML-compliant.

Conduct training and awareness programs for employees

If you want to have a smooth experience of AML compliance, it is necessary to prepare your employees. They need preparation in terms of:

- Awareness of the importance of AML compliance

- Training on the different tasks to achieve AML compliance

- Change management programs to accept the changes in operations due to new regulatory requirements

You must engage in such awareness and training programs to prepare your employees for the impending changes. They must have the necessary skills and expertise to work on AML compliance processes. They must also be ready for such supervisory engagements of authorities in AML compliance assessments.

Engage in internal audits to check AML compliance

The RAP from the Authority is helpful in understanding the importance of implementing a strong AML/CFT compliance program. Since you didn’t give it a serious thought earlier or lacking in your efforts, you have to face the RAP. So, now you must take a proactive approach to reviewing your AML compliance.

For this, you must engage in regular internal audits. Such audits will reveal where you lack and what areas need improvement. You can implement the corrective actions and be fully compliant with AML regulations.

Implement relevant advanced technology solutions

Technology solutions can be a big help in making your AML compliance a reality. Explore what are the possible uses of technology in AML processes. You can use it in the following:

- Risk assessments

- KYC and CDD

- Transaction monitoring

- Record-keeping and reports

Use solutions for these processes to automate them, leading to more efficiency and accuracy. These systems make your compliance with AML regulations faster and easier.

Seek help from professional AML consultants

Besides all these best practices, one tip that can help you the most is seeking professional assistance. AML compliance is not an easy task. A lot is on your plate to manage and handle, so you can’t achieve AML compliance.

In such a case, the best action to take is to hire a specialist AML consultant. They give a professional touch to your AML compliance procedures. They ensure all your systems, procedures, and internal controls meet the AML requirements. With their expert help, you will not face remedial activities from the authorities.

AMLUAE – your partner for professional AML consulting services

AML UAE is a leading provider of AML consulting services to clients in different industries. Our specialised AML remediation support and RAP consultancy ensure your entity meets regulatory expectations.

Our comprehensive offerings include the following:

- Business risk assessments

- Execution of KYC and CDD measures

- Transaction monitoring

- AML training

- Creation of AML framework customized to your business

- Selection of AML software

- Submission of relevant reports to authorities

- Responding to authorities on concerns, submissions, or reviews

- Forming an AML compliance team and appointing an AML compliance officer

- Monitoring of AML policies, procedures, and controls

- Audits of AML operations to suggest corrective actions

- Legal advisory services

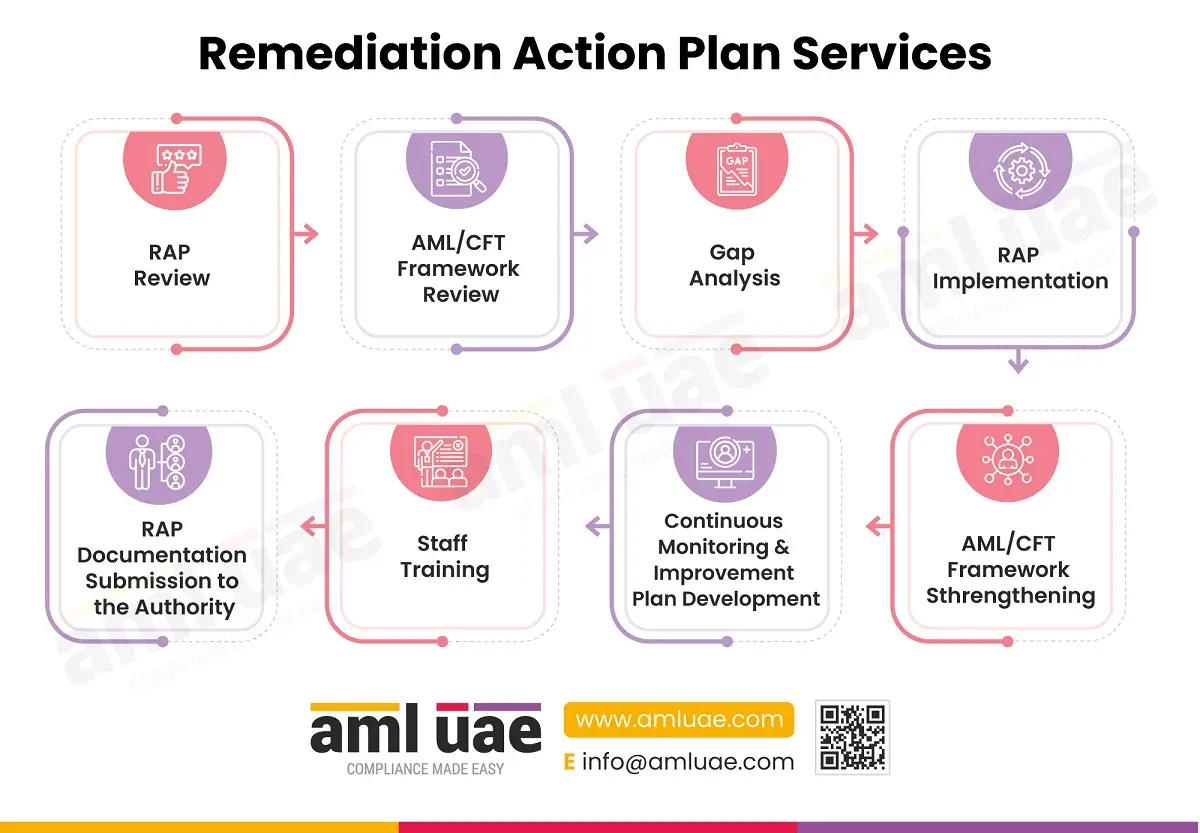

We can even help you implement the RAP received from the Supervisory Authority. We understand the requirements of such RAPs and their importance. We review the findings, discuss them with your management, and get down to the real action.

On receiving RAP, our services include the following:

- RAP Review

- AML/CFT Framework Review

- Gap Analysis

- RAP Implementation

- AML/CFT Framework Strengthening

- Continuous Monitoring & Improvement Plan Development

- Staff Training

- RAP Documentation Submission to the Authority

Frequently Asked Questions (FAQs) on RAP

What are remedial actions in a remediation project?

Remedial actions in the AML/CFT context mean the specific corrective measures taken to fix AML/CFT weaknesses such as updating policies, enhancing controls, conducting staff training, etc.

When is an AML remediation action plan required?

AML RAP is required when the regulators, auditors, or internal reviews identify compliance gaps often following inspections, enforcement actions, supervisory findings and risk-assessment.

What is the difference between a remedial action and corrective action?

A remedial action addresses existing deficiencies or past non-compliance, while a corrective action focuses on preventing recurrence by fixing root causes and strengthening future controls.

How do you implement a remediation action plan (RAP)?

RAP implementation involves prioritising issues, assigning ownership/responsibilities, executing remedial actions, tracking progress, validating completion, and reporting outcomes to management and regulators.

What are common remediation steps in AML/KYC programs?

Common remediation steps in AML/KYC program includes identifying gaps, conducting the requisite due diligence, updating customer records, revising policies, training staff, upgrading systems, and implementing ongoing monitoring to ensure compliance.

What is AML remediation and why is it important?

AML remediation is the process of correcting weaknesses in an AML/CFT Framework. It is important to reduce regulatory risk, prevent financial crime, avoid penalties, and maintain regulatory compliance.

How does a compliance remediation plan work?

A compliance remediation plan works by translating regulatory findings into actionable tasks, tracking their execution, validating effectiveness, and demonstrating closure to regulators.

What does RAP mean in audit and compliance?

In audit and compliance, RAP refers to a formal action plan developed to address audit findings, regulatory observations, or compliance breaches within defined timelines.

What are the key components of a RAP work plan?

The RAP work plan’s key components include a clear issue description, specific remedial actions, required evidence, a validation method, and a system for tracking status, owners/responsible persons, and deadlines to ensure accountability and completion.

What are typical KYC remediation actions?

Typical KYC remediation actions include updating customer information, verifying beneficial ownership, obtaining missing/additional documents, reassessing customer risk, and enhanced due diligence for high-risk clients.

How is a remediation plan monitored and reported?

A remediation plan is monitored through progress trackers, internal audits, and reviews. Reporting is done via periodic updates to senior management and submissions to regulators, supported by evidence.

What is a RAP framework in AML/CFT?

A RAP framework is the overall structure governing remediation, including governance, accountability, execution, validation, and regulatory reporting mechanisms.

What are the best practices for AML/CFT remediation?

The best practices for AML/CFT remediation include using the RAP as opportunity to strengthen AML controls, continuously monitor and improve internal processes, train employees on compliance responsibilities, conduct internal audits, leverage AML technology nd seek expert support where needed.

Scared of the consequences of AML non-compliance?

Get started with our AML compliance services now.

Share via :

About the Author

Jyoti Maheshwari

CAMS, ACA

Jyoti has over 11 years of hands-on experience in regulatory compliance, policymaking, risk management, technology consultancy, and implementation. She holds vast experience with Anti-Money Laundering rules and regulations and helps companies deploy adequate mitigation measures and comply with legal requirements. Jyoti has been instrumental in optimizing business processes, documenting business requirements, preparing FRD, BRD, and SRS, and implementing IT solutions.

Reach Out to Jyoti