Protect your business with reliable and effective AML strategies with AML UAE.

Capital Markets provide platforms where buyers and sellers trade stocks, bonds, and other financial assets, fuelling economic growth by connecting businesses with investors. However, these markets are vulnerable to exploitation by financial criminals. In this blog, we will examine Anti-Money Laundering (AML), Combatting the Financing of Terrorism (CFT), and Counter Proliferation Financing (CPF) measures for securing capital markets against financial crime risks.

Let us begin by first understanding the meaning of capital markets.

What Are Capital Markets?

Capital Markets connect those who need capital and those who have capital and want to invest the same. Capital markets thus facilitate economic growth. Entities operating in the capital market sector offer various types of products and services, such as:

- securities and commodities brokerage,

- investment advice and management,

- securities consultation and analysis,

- fund service businesses,

- exchanges, depository services, etc.

These products and services encourage investment. In UAE, the capital market sector is supervised by the Securities and Commodities Authority (SCA). It is the apex authority in-charge of overseeing and regulating the capital markets in the UAE. This includes monitoring the AML/CFT/CPF compliance of Financial Institutions operating within the UAE’s capital markets. However, there’s an exception to this – the Financial Services Regulatory Authority (FSRA) and the Dubai Financial Services Authority (DFSA) oversee the operations of the capital market players registered and operating from the Abu Dhabi Global Market (ADGM) and Dubai International Financial Centre (DIFC), respectively.

Now, let us discuss exactly what types of Financial Institutions operating in the capital market are subject to and regulated under AML/CFT/CPF regime of UAE.

Financial Institutions Operating in Capital Markets that Are Regulated under AML/CFT/CPF Regime of UAE

Under Cabinet Resolution No. (134) of 2025, the following types of financial activities or operations are relevant in the context of Capital Markets:

- Providing Monetary brokerage services

- Engaging in securities transactions, issuing securities, providing financial services related to issuing of securities, finance, and finance leasing

- Trading, making investments in, operating or managing:

- Assets

- Options contracts

- Future financial contracts

- Exchange and interest rate transactions

- Financial derivatives

- Negotiable financial instruments

- Providing custody of funds services

- Management of investment and other types of funds and portfolios

Further, the SCA provides to the following categories:

Category 1: Entities Dealing in Securities

This category includes trading and clearing brokers, global market trading brokers, trading brokers of OTC derivatives, OTC commodities contracts, currencies in spot market, financial products dealers, etc.

Category 2: Entities Dealing in Investments

These entities include those involved in investment fund management, family business investment management, portfolio management, fund administration, profit sharing investment account management, etc.

Category 3: Entities Dealing in Custody, Clearing, and Registration

These include custody, general clearing, issuer of covered warrants, depository bank of depository receipts, depository bank agents of depository receipt, registrar of private joint stock companies, etc.

Category 4: Credit Rating Agencies

Category 5: Entities Dealing in Arrangement and Advice

These include entities such as financial consulting, financial advisor, listing adviser, introducing services, promotion services, etc.

Category 6: Crowdfunding Platform Operators

Category 7: Virtual Assets Services Providers

This category includes entities engaged in virtual asset brokerage and custody of virtual assets. VASPs operate as a distinct category of regulated entities under AML, CFT, CPF and TFS regime of UAE, alongside Financial Institutions and Designated Non-Financial Businesses and Professions (DNFBPs).

Therefore, all Financial Institutions licensed by the SCA and providing any of the financial transactions or activities associated with the capital market listed under Cabinet Resolution No. (134) of 2025 are regulated under AML/CFT/CPF regime of UAE.

Now, let us understand why capital markets are vulnerable to financial crimes, highlighting why Financial Institutions operating in the capital markets of UAE need strong AML/CFT/CPF compliance programs.

Join the Fight against Financial Crimes!

Protect your business with reliable and effective

AML strategies with AML UAE.

Why are Financial Institutions in the Capital Market Sector Vulnerable to Financial Crime Risks

Capital markets provide access to the financial system. Certain characteristics of the capital market make it susceptible to criminals seeking to commit financial crimes such as Money Laundering (ML) , Terrorism Financing (TF), and Proliferation Financing (PF) . These characteristics include the following:

Large Volume and Value of Transactions:

Financial Institutions operating in the capital markets process an enormous volume of transactions daily, often involving substantial sums of money. The large volume and value of transactions makes monitoring difficult, allowing illicit activities to sometimes go undetected.

Rapid Execution of Transactions:

Transactions in the capital market are executed at high speed, often within seconds or minutes. This rapid movement of funds makes it challenging for Financial Institutions to detect and intervene in real-time. Financial criminals often exploit this feature to quickly transfer dirty money before suspicious patterns are identified.

Involvement of Multiple Intermediaries:

Transactions conducted in the capital markets often involve a complex network of intermediaries, including brokers, investment funds, custodians, and clearing houses. This fragmentation of transactions provides anonymity to financial criminals, as no single intermediary has full visibility of the entire audit trail of the transaction. This lack of oversight enables illicit fund movements.

Complexity of Financial Transactions, Instruments, and Products:

Capital markets provide a wide range of financial products and services, such as derivatives, bonds, multiple types of securities, investment options, etc. Criminals exploit these sophisticated instruments offered by Financial Institutions to create intricate money trails that make it difficult to track and trace illicit funds

High Liquidity:

The high liquidity of the Financial Institutions in the capital market instruments allows assets to be quickly converted into cash or other financial instruments. This makes it easier for criminals to integrate illicitly gained funds into the formal economy.

Movement of Capital across Various Geographies:

The capital market is global, with funds moving across different jurisdictions and financial systems. Cross-border transactions make it difficult to detect ML/TF/PF risks, monitor suspicious activities, and adopt appropriate risk mitigation measures.

Pre-Emptive Detection of ML/TF/PF is Challenging

Financial criminals often structure transactions in a way that makes them appear legitimate at face value. This makes it difficult for Financial Institutions to proactively identify illicit activities before they occur. By the time suspicious patterns emerge, the funds may have already been moved.

Lack of Visibility of the Entire Chain of Transactions:

The sophisticated nature of capital market transactions, coupled with the use of intermediaries, makes it difficult to keep track of the entire chain of transactions. This lack of visibility hinders the detection of ML/TF/PF risks.

These characteristics make Financial Institutions in the Capital Market Sector in the UAE vulnerable to financial crime risks. Now, let us discuss the common financial crime typologies that criminals misuse to conduct ML/TF/PF through Financial Institutions.

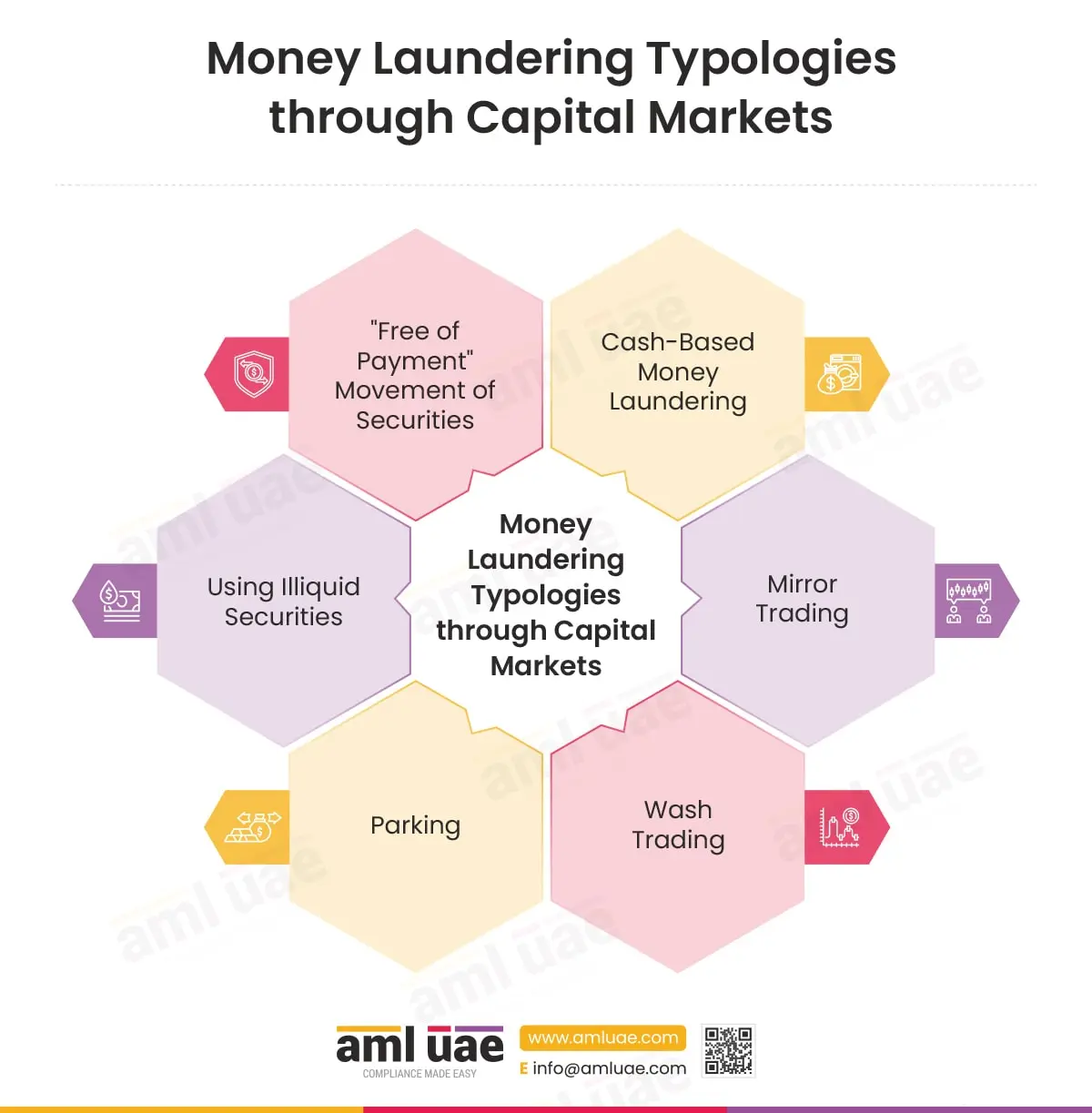

Financial Crimes Through Capital Markets: Common Typologies

To effectively detect and prevent the misuse of capital markets for financial crimes, Financial Institutions operating in the capital market must stay informed about common and emerging ML/TF/PF typologies. These typologies include the following:

“Free of Payment” Movement of Securities:

Free of payment movement is essentially a transfer of securities and other capital market instruments without any corresponding payments. It is used to conduct ML/TF/PF by creating layers of transactions. For example, criminals may transfer securities between multiple trading accounts through the services of many brokers across different jurisdictions without any payment, making it difficult to trace the original source of funds. Each broker that facilitates these transactions may have limited visibility regarding the entire audit trail, making it difficult to detect the financial crime involved.

Cash-Based Money Laundering:

While capital markets are not usually considered a cash-intensive sector, financial criminals often try to place illicitly sourced cash in trading accounts and quickly move them through multiple securities trading accounts to avoid detection. Often trading accounts are held with different Financial Institutions, and therefore, they have limited visibility with respect to entire trail of transactions.

Mirror Trading:

Mirror trading can be exploited for financial crimes by executing identical buy and sell transactions across different jurisdictions through two connected individuals. To brokers in separate countries, these individuals may appear unrelated. A criminal may deposit illicit funds into a brokerage account and simultaneously buy securities in one country while selling them in another (as only these two transactions match each other and are settled at the prices determined by these two connected parties). Since the trades cancel each other out, there is no market risk, but the money appears as a legitimate trade transaction. This technique effectively launders illicit funds across borders and disguises their origin.

Wash Trading:

In this typology, a trader buys and sells the same financial asset at nearly identical prices to give the trading activity an appearance of legitimacy. Despite the trading activity, no market risk is assumed, and the financial criminal’s market position remains unchanged.

Parking:

In this typology, a person transfers assets to another, often without any legitimate reason or economic rationale, with an understanding that the person will repurchase the same later.

Using Illiquid Securities:

Financial criminals often make use of illiquid securities to conduct financial crimes. Illiquid securities are those assets that do not have a real market, or are low volume, or are of obscure companies, etc. Illiquid securities are used because their prices can be easily manipulated. Trading in illiquid securities is conducted to move around illicitly gained funds.

The typologies discussed in the above section can be detected pre-emptively through red flags that indicate financial crime risks. Let us now discuss these red flags.

Red Flags Indicating Financial Crime Risks in Capital Markets

- False or Misleading Information: The customer gives Financial Institutions false, misleading, or incorrect information

- One Directional Transactions: The customer has some accounts mainly for deposits and other accounts primarily for outgoing payments in relation to securities trading activities

- Customer Hesitant to Provide CDD Information: The customer is hesitant or declines to provide Financial Institutions with CDD information such as Source of Funds or Source of Wealth

- Frequent and Small Deposits: The customer frequently deposits small amounts of cash, which are later used to buy a specific securities product that is quickly sold or redeemed

- Third-Party Involvement: The customer’s account receives deposits from third parties, which corresponds to outgoing transfers to other third parties

- Trading in Securities not in the Name of the Customer: The security, bonds, or any other capital market instrument that the customer seeks to trade, or deposit is not in the customer’s own name.

- Parties to the Transaction are Interconnected: On each side of a trading transaction, the parties are interconnected, have the same UBOs, business transactions, personnel, etc.

- No Economic Rationale: The trading strategies of the customer has no economic rationale, or logical reason. The transactions seem irrational. For example, the customer is making a loss, trading at a value below market price, redeeming long-term funds within a short span of time, etc.

- Transactions in Quick Succession: Customers conduct transactions in quick succession in a short span of time

- Circumventing De-Risking: Previous customers of the Financial Institutions seek to reapply and seek services of the entity through a different legal person in order to circumvent de-risking or client exit measures adopted by the Financial Institutions for those previous customers.

- Misalignment with Known Customer Profile: The transaction does not match the customer’s profile, trading history, and trading position. Customer uses denominations or amounts of currencies that do not align with their profile

- Rapid Change in Customer Details: There may be small but quick changes in CDD details of the customer such as address, directors, Ultimate Beneficial Owners (UBOs), etc.

- Funding Patterns Are Abnormal: The customer’s account receives funds from third parties with no apparent connection to the customer, or the deposits are done through multiple payment methods, significant funds received in a short time, etc. For example, the customer deposits a significant sum of money in small-denomination currency to fund the account or purchase securities

- Trading Account Linked by Many Devices: Trading account of the customer is accessed through multiple devices such as PC, different mobile handsets International Mobile Equipment Identity (IMEI) numbers, etc.

After having understood how capital markets are exploited by financial criminals, and how financial crimes can be detected, understanding the common typologies and red flags, let us now discuss AML/CFT/CPF measures Financial Institutions operating in the capital markets can take to strengthen their defence against financial crimes.

We Simplify AML Compliance so You Can

Amplify Your Business

AML UAE provides proactive AML solutions to secure your business from financial crimes

AML/CFT/CPF Measures for Financial Institutions Operating in Capital Markets: Challenges and Best Practices

Financial Institutions, DNFBPs, and VASPs are regulated under AML/CFT/CPF regime of UAE and need to adhere to certain compliance obligations. We have detailed these obligations, through an easy-to-understand infographic on AML Compliance Requirement in UAE.

Let us now discuss and focus on specific AML/CFT/CPF measures, challenges in their implementation, and best practices to conduct them effectively, specifically for financial institutions operating in the capital markets.

Enterprise-Wide Risk Assessment (EWRA)

Financial Institutions operating in the capital markets are exposed to financial crime risks – both directly through transactions undertaken by their customers, and indirectly, through ML/TF/PF risks emanating from customers themselves. EWRA helps in assessing these risks on an institutional level, facilitating adoption of proportionate and effective ML/TF/PF risk management system and controls, suitable to the nature and size of the business.

Challenges Contributing to the Ineffective Implementation of EWRA:

- Adopting Generic EWRA: Financial Institutions may use generic or template EWRA or fail to fully assess the specific financial crime risks they face due to their specific business model. As a result, there may be a lack of awareness across the entity about how criminals could exploit them, leaving a few vulnerabilities unidentified and unattended.

- Not Defining EWRA Methodology: Failing to define an EWRA methodology weakens a Financial Institution’s ability to identify and mitigate ML/TF/PF risks. Without a structured approach, EWRA may become inconsistent, emerging threats may go unnoticed, and resources invested in AML/CFT/CPF compliance processes may be misallocated.

- Not Updating EWRA when ML/TF/PF Risk Exposure Changes: ML/TF/PF risk exposure of the Financial Institutions may change due to many reasons, such as the introduction of new financial products, expansion of business to other countries, etc. When Financial Institutions do not update their EWRA to incorporate ML/TF/PF risk exposure arising from their changed circumstances, it may lead to the adoption of inadequate risk mitigation measures, which in turn may lead to failure in preventing financial crimes.

- Not Considering How EWRA Feeds into ML/TF/PF Controls: The risk assessed through EWRA must translate into risk controls adopted by the Financial Institution. When this is not done, the risk control measures adopted are not relevant or adequate to mitigate the specific ML/TF/PF risks the Financial Institutions is exposed.

Best Practices for Effective Implementation of EWRA:

- Adopting Tailored and Relevant EWRA: EWRA should be customised to assess the actual ML/TF/PF risks a regulated entity is exposed to. It must take into consideration the ML/TF/PF risks emanating from the customer base of the Financial Institution, the geographies it operates in, its own products and services, the delivery channels used, the transactions it is exposed to, etc. It must also assess the financial crime typologies it is vulnerable to and adopt necessary controls accordingly. EWRA must also incorporate a red flag analysis to ensure that ML/TF/PF typologies are detected and dealt with.

- Clearly Documenting EWRA Methodology: A clear, documented methodology ensures consistency and enhances ML/TF/PF risk detection capabilities of the Financial Institution. The methodology must include both qualitative and quantitative assessment parameters.

- Defining Triggers and Updating EWRA when They Occur: Financial Institutions should define scenarios that would trigger a need to update their EWRA. Whenever these triggers occur, the financial crime risk exposure of the Financial Institutions changes, and therefore, EWRA must be updated to incorporate the ML/TF/PF risks emanating from such incidents. These triggers include incidents such as the Financial Institutions introducing new products, the Financial Action Task Force (FATF) updating its Grey List, etc.

- Ensuring that ML/TF/PF Risks Assessed through EWRA is Mitigated through Appropriate Controls: Adopting proportional and relevant risk controls based on the particular risk exposure of a Financial Institution is the very essence of a risk-based approach. The risks assessed through the EWRA must be mitigated through the Financial Institution’s AML/CFT/CPF Policies, Procedures, and Controls.

We Simplify AML Compliance so You Can

Amplify Your Business

AML UAE provides proactive AML solutions to secure your business from financial crimes

Customer Due Diligence (CDD)

Customer Due Diligence (CDD) is the process of understanding the identity of a customer, the ML/TF/PF risks emanating from them, and adopting risk-based ML/TF/PF controls to manage these risks.

Challenges Contributing to the Ineffective Implementation of CDD:

- Not Documenting Information on Expected Account Activity and Client’s Expectations: One of the challenges in implementing effective Customer Due Diligence (CDD) is the failure to document expected account activity and client expectations. Without a clear record of how an account is expected to function, Financial Institutions may struggle to identify unusual transactions that may indicate financial crime risks.

- De-Risking in a Wholesale Manner without Considering ML/TF/PF Risks: Some Financial Institutions restrict services to entire customer groups without properly conducting ML/TF/PF risk assessment for them. Effective risk management requires a targeted, risk-based approach rather than broad de-risking measures. Simply cutting off services without sufficient rationale can lead to unintended consequences such as financial exclusion and regulatory non-compliance.

- Not Re-conducting CDD when Customer’s Circumstances Change: CDD is not a one-time process, it must be dynamic and responsive to changes in a customer’s profile. If a customer’s CDD information undergoes changes, such as a change in ownership, business structure, transaction patterns, etc., but the Financial Institution does not conduct a fresh CDD review, it may lead to incomplete CRA, resulting in the adoption of inadequate ML/TF/PF control measures for the customer.

- CDD Review is Conducted in an Alphabetical Manner and not a Risk-Based Manner: Some Financial Institutions may conduct periodic CDD reviews in a systematic but ineffective manner, such as reviewing customers alphabetically rather than based on the degree of ML/TF/PF risks they pose. This method does not prioritise high-risk clients, leaving potential financial crime risks undetected for extended periods.

Best Practices for Effective Implementation of CDD:

- Collecting Adequate Information on Expected Account Activity and Client’s Expectations: Financial Institutions operating in capital markets usually offer financial services geared toward investments and trading in securities. Their clients may have certain expectations as to their account activity and expected returns. Financial Institutions should understand the same to ensure that any mismatch is identified in the future.

- Creating a Matrix of AML Requirements for Each Customer Type Based on Risk-Based Approach: A one-size-fits-all approach is ineffective in AML/CFT/CPF compliance. Financial Institutions should develop a structured matrix, questionnaire, or checklist outlining specific AML/CFT/CPF tasks that need to be completed for each customer based on different customer types and their associated ML/TF/PF risk levels. This risk-based approach allows for improved efficiency and ensures the optimum allocation of resources.

- Conducting Periodic Review of CDD in a Risk-Based Manner: Regular CDD reviews are important for maintaining up-to-date customer risk profiles. Financial Institutions should establish triggers for periodic reviews, such as extended periods of non-trading, changes in account activity, updates in regulatory requirements, Financial Action Task Force’s Grey List or Blacklist updates, etc. Further, for periodic reviews, risk-based approach should drive the review schedule, ensuring that high-risk customers receive more frequent and thorough CDD reviews than low-risk ones.

- Clearly Defining CRA Parameters, Methodology for Calculating Risk Scores and Overrides: A well-defined Customer Risk Assessment methodology is important for consistency and accuracy in the evaluation of ML/TF/PF risks each customer poses to a Financial Institution. Therefore, they should establish clear parameters for assessing financial crime risk, document the methodology for calculating risk scores, and outline procedures for overriding default CRAs where justified.Further, Financial Institutions should tailor their CRA methodologies to include parameters specific to capital markets, such as trading behaviours and investment patterns. This enhances the effectiveness of ML/TF/PF risk management for Financial Institutions.

Transaction Monitoring and Reporting Suspicious Transactions

Financial Institutions operating in the capital markets need to report suspicious activities and transactions by filing Suspicious Activity Report (SAR) and Suspicious Transaction Report (STR) with UAE’s Financial Intelligence Unit (FIU).

Challenges Contributing to Ineffective Implementation of Transaction Monitoring and STR/SAR Reporting Mechanisms:

- Conducting Transactions Monitoring Manually: Manual transaction monitoring poses challenges for Financial Institutions, including difficulty in assessing and applying relevant transaction monitoring rules and insufficient resources to review suspicious transactions effectively. These factors can lead to inefficiencies, increased operational costs, and potential compliance risks, which hinder the Financial Institution’s ability to manage large volumes of transactions.

- Mismatch between Increase in Volume of Trade and Scalability of Transactions Monitoring Solution: A mismatch between transaction monitoring capacity and trade volumes undertaken by the Financial Institutions can create risks of AML non-compliance. Financial Institutions may fail to upgrade their transaction monitoring systems in line with their business expansion, leading to them being overloaded and causing delays in detecting suspicious transactions. This issue becomes aggravated when Financial Institutions rely on outdated technologies or systems that cannot handle large datasets efficiently.

- Not Utilising Capital Market Specific Transaction Monitoring Rules: When Financial Institutions utilise generic transaction monitoring rules that do not give sufficient importance to capital market-specific risks, they reduce their suspicious transaction detection capabilities. Without industry-specific rules, Financial Institutions may fail to detect complex financial crime typologies that target capital markets.

- Not Considering Contextual Information while Monitoring Transactions: Often, transactions may not appear suspicious when considering them on their own, without assessing them in the context of a customer’s KYC information, CRA profile, Screening results, changes in Ultimate Beneficial Owners (UBOs), etc. This results in suspicious transactions slipping notice.

- Transactions Monitoring Systems are not Regularly Reviewed: Transaction monitoring systems require periodic reviews and vulnerability assessments to ensure they remain effective in detecting financial crime risks. Failure to assess the adequacy of transaction monitoring systems regularly may lead to outdated detection mechanisms that use ineffective rules and thresholds, produce excessive false positives, etc.

- Knowledge Gained Through Transaction Monitoring Not Fed Back into EWRA, Controls, and Staff Training: A key challenge is the failure to integrate insights gained from transaction monitoring into EWRA internal controls, and staff training. Transaction monitoring generates valuable intelligence on patterns of financial crimes, their red flags, and typologies. If these insights are not used to refine the existing EWRA, financial crime controls, and staff training, AML/CFT/CPF measures adopted by the Financial Institutions will remain outdated, inefficient, and static, increasing the likelihood of financial crimes slipping through the cracks.

- Not Documenting Transaction Monitoring Alerts in a Customer’s Profile: Whenever a suspicious transaction alert related to a customer is generated, it must be recorded in the customer’s profile. When alerts are not stored against customer profiles, Financial Institutions may find it difficult to track the history of red flags of suspicious behaviour over time.

Best Practices for Effective Implementation of Transaction Monitoring and STR/SAR Reporting Mechanisms:

- Utilising Scalable and Customised Transaction Monitoring Software: Financial Institutions should invest in advanced transaction monitoring software that is scalable and tailored to the capital market sector. AI-driven and machine-learning enabled systems can help detect unusual patterns, even in complex transactions involving sophisticated financial instruments. These solutions should have the ability to scale with business growth and volume of transactions. Additionally, implementing real-time monitoring capabilities enables firms to detect suspicious transactions promptly and take immediate action on submitting STR or SAR.

- Defining and Utilising Risk-Based Transaction Monitoring TriggersTo improve detection capabilities, transaction monitoring rules should be customised based on the specific risks associated with different clients, products, and services. For example, customers engaging in high-frequency trading may require different monitoring parameters than customers opting for long-term investment funds.

- Monitoring Transactions in a Contextual Manner: Effective transaction monitoring goes beyond simple analysis of transactions and investigating alerts, it requires evaluating activities in the broader context of customer risk profiles, historical behaviour, KYC data, screening results, etc. By doing so, Financial Institutions can improve their capabilities of detecting sophisticated financial crime typologies that may not be apparent on the face value from the transactions alone.

- Regularly Reviewing Transaction Monitoring Software: Transaction monitoring systems should undergo periodic reviews and vulnerability assessments to assess the effectiveness of transactions monitoring rules and thresholds, and overall system performance. Updates should be made in response to new regulatory requirements, emerging financial crime typologies and red flags, change in Financial Institution’s financial crime risk exposure, etc.

- Incorporating Knowledge Gained Through Transaction Monitoring Into EWRA, Controls, and Staff Training: Financial Institutions should establish a feedback loop that integrates insights and knowledge gained through transaction monitoring into their EWRA, internal controls, and staff training programs. By doing so, they can continuously improve the effectiveness of their AML/CFT/CPF Program. Transaction monitoring alerts and their resolution can also provide case studies as a way to train staff members on the practical aspects of detecting financial crime risks.

- Documenting Transaction Monitoring Alerts in Customer’s Profile: Transaction monitoring alerts related to a customer should be documented in that customer’s profile. Systematically storing alerts, and the investigation conducted to resolve the same ensures that Financial Institutions create valuable data on customer behaviour. This helps tracking patterns of suspicious transactions over time.

We Simplify AML Compliance so You Can

Amplify Your Business

AML UAE provides proactive AML solutions to secure your business from financial crimes

AML/CFT/CPF Staff Training

AML/CFT/CPF Training for staff of the Financial Institutions operating in capital markets ensures that each employee understands their role in the AML/CFT/CPF Program of the Financial Institutions and performs their responsibility properly.

Challenges Contributing to Ineffective Implementation of AML/CFT/CPF Staff Training:

- Conducting Generic AML/CFT/CPF Training: One of the most prevalent deficiencies in AML/CFT/CPF training is the use of generic, one-size-fits-all training programs. Many Financial Institutions rely on broad-based modules that fail to address the specific financial crime risks faced by the Financial Institution.

- Not Conducting Role-Based Training: Financial Institutions often fail to tailor their AML/CFT/CPF training to different employee roles and responsibilities. Effective training programs must differentiate between front-line employees, compliance officers, risk managers, senior management, and other stakeholders.

- Not Compiling and Incorporating Near-Miss Data: A major oversight in AML/CFT/CPF training programs is the failure to analyse and incorporate near-miss incidents, cases where financial crimes almost occurred but were ultimately prevented. Near-miss data is a valuable resource for refining training strategies and improving employees/ ability to detect and respond to suspicious activities.

- Not Regularly Testing the Effectiveness of Training: Even when AML/CFT/CPF training is conducted, Financial Institutions often neglect to assess its effectiveness. Without regular testing and evaluation, it is difficult to determine whether employees have truly learned key concepts and can apply them while performing their roles.

Best Practices for Effective Implementation of AML/CFT/CPF Staff Training

- Tailoring Training to the Financial Institution’s Needs: Each Financial Institution has a different business model, ML/TF/PF risk exposure, products and services, size, customer-base, etc. Training should be tailored, keeping in mind the specific characteristics and needs of the business.

- Conducting Role-Specific Training: Role-specific training ensures that each employee understands their specific responsibilities in the AML/CFT/CPF program of the Financial Institutions properly and executes the same effectively.

- Using Near-Miss Data to Improve Training: A near-miss is an incident that could have resulted in issues such as non-compliance, missing the attempted ML/TF/PF activity, etc., but did not result in the same. These incidents must be reported to ensure continuous improvement in the AML/CFT/CPF compliance function of the Financial Institutions. Financial Institutions should ensure that data regarding these near-misses are incorporated into training material so that the likelihood of them occurring reduces or the possibility of their timely prevention by the staff increases.

- Testing the Effectiveness of Training: The effectiveness of staff training should be checked through measures such as tests, quizzes, spot checks, feedback, etc.

AML/CFT/CPF Governance and Oversight

The AML/CFT/CPF measures discussed are important components of AML/CFT/CPF Policies, Procedures, and Controls. These measures need proper governance and oversight to ensure their proper functioning.

Challenges Contributing to Ineffective Implementation of Governance and Oversight Mechanisms

- Not Inculcating a Culture of AML/CFT/CPF Compliance: Financial Institutions may struggle to instill a culture of AML/CFT/CPF compliance due to a lack of commitment from senior management, insufficient training, and failure to integrate AML/CFT/CPF compliance into everyday operations. This may result in risks of non-compliance.

- Not Documenting Senior Management Decisions and Discussions: Financial Institutions may fail to document management discussions and decisions related to AML/CFT/CPF compliance. Without proper documentation, it becomes difficult to track compliance discussions, ensure accountability for decision-making, or communicate the decisions to the employees of the Financial Institutions. This lack of documentation can also result in an inability to audit past compliance actions effectively.

- Not Having Open Communication Channels in Place: The absence of open communication channels hinders the timely escalation of ML/TF/PF risks. Employees may be hesitant to report suspicious transactions due to fear of retaliation or unclear reporting structures.

- Not Having Proper Mechanisms to Address Possible Conflict of Interests: Conflicts of interest can undermine the integrity of AML/CFT/CPF measures. Financial Institutions that lack mechanisms to identify, report, and prevent conflicts of interest may find themselves vulnerable to ML/TF/PF risks. For example, if an employee of a Financial Institution is in any way related to a customer, such conflict of interest may be exploited by financial criminals and, therefore, is important to prevent.

Best Practices for Effective Implementation of Governance and Oversight Mechanisms

- Setting an AML/CFT/CPF Compliance Culture: To establish a strong culture of AML/CFT/CPF compliance, senior management of the Financial Institution should lead by example by emphasising the importance of compliance through consistent messaging and actions. Such a culture leads to an atmosphere where AML/CFT/CPF compliance is prioritised throughout the organisational structure of the Financial Institution. Other methods, such as AML/CFT/CPF training for employees, AML/CFT/CPF program evaluations through regular audits, etc, also facilitate establishing a strong compliance culture.

- Properly Documenting Senior Management Decisions and Approvals: Comprehensive documentation of Senior Management discussions and decisions related to AML/CFT/CPF compliance ensures internal accountability. This documentation serves as an audit trail, ensuring that decisions related to AML/CFT/CPF compliance are communicated and implemented effectively and can be reviewed when necessary.

- Setting a Transparent Channel of Communication: Financial Institutions should establish clear and accessible communication channels for any concerns related AML/CFT/CPF compliance processes. Employees must have designated reporting structures and whistleblower protections to encourage the reporting of suspicious transactions without fear of retaliation.

- Adopting Mechanisms to Address Conflict of Interests: Effective governance requires financial institutions to proactively identify and address conflicts of interest. Establishing clear policies on conflict disclosure, independent oversight committees, and regular audits can help minimise biased decision-making, reducing the risk of occurrence of ML/TF/PF. Employees should be required to declare potential conflicts of interest. For example, financial criminals may use their connections within the Financial Institutions to influence its AML/CFT/CPF compliance processes for that customer. Having conflict of interest disclosure requirements reduces this risk.

Risk-Proof Your Business with Expert AML Services

AML UAE, your Partner in turning compliance challenges into confidence

Customer Risk Assessment (CRA) Questionnaire: Sample Parameters That Financial Institutions Can Imbibe

Let us now discuss some Customer Risk Assessment (CRA) parameters that Financial Institutions operating in Capital Markets can incorporate. Giving due weightage to capital market sector-specific CRA parameters helps Financial Institutions operating in capital markets comprehensively and accurately analyse the ML/TF/PF risks emanating from their customers. These parameters can be used in conjunction with general CRA parameters.

Securing Capital Markets against Financial Crime Risks: Concluding Remarks

Criminals exploit vulnerabilities in capital markets to engage in Money Laundering, Terrorism Financing, and Proliferation Financing, making it imperative for Financial Institutions to implement strong and effective AML/CFT/CPF compliance measures. By understanding financial crime typologies in capital markets, recognising red flags, and adopting best practices as discussed in the blog, Financial Institutions can strengthen their defences against financial crimes.

Risk-Proof Your Business with Expert AML Services

AML UAE, your Partner in turning compliance challenges into confidence

Share via :

About the Author

Pathik Shah

FCA, CAMS, CISA, CS, DISA (ICAI), FAFP (ICAI)

Pathik is an ACAMS-certified AML consultant specialising in governance, risk, and compliance for regulated entities in the UAE. He brings over 28 years of experience, with 1,000+ hours of AML training and 200+ advisory engagements across DNFBPs, VASPs, and FIs. He supports businesses in aligning with AML/CFT requirements from the CBUAE, DFSA, MoET, MoJ, VARA, CMA, FSRA, and FATF. Known for translating complex regulations into audit-ready procedures, Pathik enables operational clarity and compliance readiness.

Reach Out to Pathik