Rental Income Schemes

Last Updated: 05/15/2026

Protect your business with reliable and effective AML strategies with AML UAE.

Rental Income Schemes - Brief Overview

Masking criminal proceeds as legitimate rental income, rental income schemes exploit inflated rents, fabricated tenancy agreements, and opaque corporate ownership to complete the integration stage of money laundering. In the UAE, real estate agents, banks, and trust and company service providers face binding AML obligations triggered without a monetary threshold. Effective detection requires transaction monitoring, enhanced customer due diligence, and verified occupancy evidence.

What are Rental Income Schemes?

A rental income scheme is a money laundering typology in which a criminal introduces illicit funds into the financial system by generating artificial or inflated rental payments on real property. The scheme typically involves an illicit operator arranging for connected parties to pay above-market rents on a property held through an opaque ownership structure, depositing those payments into bank accounts, and declaring the proceeds as legitimate income from a property business.

The typology operates at the integration stage of the money laundering cycle. By the time funds appear as rental receipts, they carry the appearance of earned commercial income and a paper trail that is difficult to challenge without forensic cross-referencing of rental values, occupancy records, and ownership structures.

Regulatory Framework related to Rental Income Schemes

The UAE’s primary AML statute is Federal Decree Law No. 10 of 2025 Regarding Anti-Money Laundering and Combating the Financing of Terrorism and Proliferation Financing (FDL 10/2025), which entered into force on 14 October 2025 and repealed Federal Decree Law No. 20 of 2018. Article 2 of FDL 10/2025 criminalises money laundering across four actus reus elements; ML is an independent crime, and a prior conviction for the predicate offence is not required.

The operative AML/CFT obligations for real estate brokers and agents derive from Cabinet Resolution No. 134 of 2025 on the Executive Regulations for FDL 10/2025 (CR 134/2025), which is effective as of December 2025. Article 3(2) of CR 134/2025 establishes that real estate brokers and agents are DNFBPs when concluding purchase or sale transactions on behalf of a customer. No monetary threshold applies.

Supervisory Body and the FIU

The Ministry of Economy and Tourism (MoET) is the primary supervisory authority for real estate brokers and agents in the UAE.

The Central Bank of the UAE hosts the Financial Intelligence Unit (FIU), established under FDL 10/2025 Article 11. All STRs and SARs must be submitted to the FIU via goAML.

Reporting or Compliance Obligations and Channels

Real estate brokers, agents, and financial institutions face multiple reporting obligations where rental income schemes may be relevant. The STR (Suspicious Transaction Report) is filed without delay whenever ML or TF suspicion arises, regardless of transaction value.

The REAR is filed via goAML for cash freehold transactions at or above AED 55,000 (MOEC-Cir-5-2022-REAR). However, REAR submission is not required for leasehold, rental property management, or other non-freehold transactions.

In addition, institutions may also be required to submit other reports through goAML, including Confirm Name Match Report (CNMR), Partial Name Match Reports (PNMR), High-Risk Country Reports (HRC), High-Risk Country Transaction Reports (HRCA), and Suspicious Activity Reports (SAR), particularly where sanctions exposure, name screening alerts, or jurisdictional risk triggers are identified.

Geographies and Contexts of Concern

The UAE National Risk Assessment 2024 and the FATF DNFBP risk framework both identify the real estate sector as a high-risk area. Cross-border rental payments originating from jurisdictions with weak AML frameworks or active FATF grey-listing are a specific concern under CR 134/2025.

What Do Rental Income Schemes Mean?

A rental income scheme works like submitting an expense claim for a journey that was never made. A criminal arranges for a connected party to pay rent on a property at a rate far above the market, transfers that inflated rent through a bank account, and presents the deposits as earned property income. The property provides the cover story, the tenancy agreement provides the paper trail, and the bank account delivers the laundered result.

Why Rental Income Schemes Matter for Compliance

Rental income schemes pose a particular challenge because they exploit a commercially normal activity. Every legitimate landlord earns rental income; every bank holds accounts for property businesses; every real estate agent concludes tenancy transactions. The laundering mechanism is embedded in that routine.

The UAEFIU December 2023 Real Estate ML Typologies Report recorded AED 648.8 billion in UAE real estate transaction value for 2022 alone. During the July 2020 to June 2023 review period, the MOET issued AED 22.6 million in fines across 225 violations. Those figures confirm that real estate sector AML deficiencies are not theoretical; they have attracted enforcement consequences.

The integration stage means that by the time funds appear as rental receipts, they carry commercial legitimacy.

How Rental Income Schemes Work

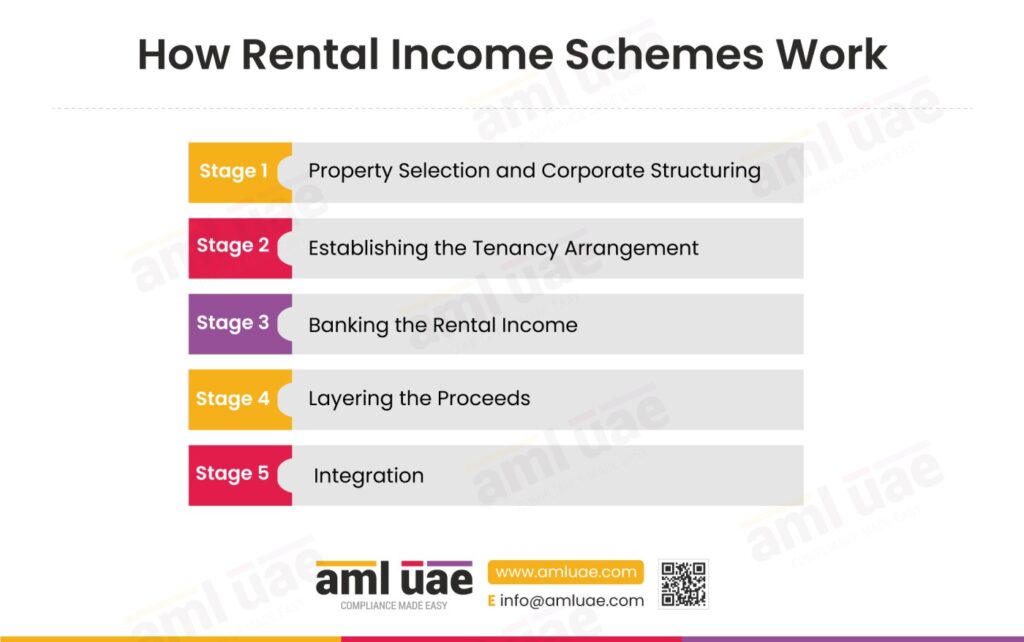

Rental income schemes operate in stages, with distinct actors contributing to different phases of the laundering architecture. The five-stage sequence below maps the mechanism from initial property selection through to the integration of clean funds.

Stage 1: Property Selection and Corporate Structuring

The illicit operator selects one or more real properties and arranges ownership through a shell company or front company with no genuine commercial activity. Trust and company service providers (TCSPs) may be engaged to establish the ownership vehicle, appoint nominee directors, and maintain the company in a jurisdiction with limited beneficial ownership disclosure requirements.

Stage 2: Establishing the Tenancy Arrangement

A real estate professional or the illicit operator directly arranges a tenancy. The tenant is connected to the illicit operator: a family member, associate, or further entity under common control. The tenancy agreement specifies a rental rate that significantly exceeds local market rates, or the property has no genuine occupancy at all.

Stage 3: Banking the Rental Income

The tenant remits rent payments into a bank account held by the shell company or front company. These payments may be structured as regular monthly deposits that mirror a legitimate rental cycle. In some variants, large upfront payments covering multiple months are deposited at once, often in cash.

Stage 4: Layering the Proceeds

Immediately following the deposit, the rental income is transferred to a secondary account, frequently at a different institution or in a different jurisdiction. This rapid post-deposit movement indicates money laundering rather than genuine income accumulation.

Stage 5: Integration

The funds re-enter the legitimate economy bearing the complete paper trail of a property business: rental agreements, bank statements showing regular income, company accounts, and, in some cases, filed tax returns. The illicit operator can now use the funds to invest in further assets or support business activities without any appearance of unexplained wealth.

Real-World Examples of Rental Income Schemes

Scenario 1: The Inflated Commercial Lease

A beneficial owner of a small commercial property arranges for a trading company under their indirect control to lease the property at twice the market rental rate. The bank sees a commercial landlord receiving regular rental income from a legitimate-looking tenant. Over 24 months, AED 4.8 million moves through the rental arrangement, of which approximately half represents criminal proceeds that have acquired the identity of earned property income.

The scheme is ultimately identified when a transaction monitoring alert on rapid post-deposit transfers triggers a file review, and investigation reveals the trading company’s declared turnover is insufficient to sustain the rental payments recorded.

The operational lesson is that rental income accounts require market-rate validation at onboarding and periodic review.

Scenario 2: The Phantom Residential Portfolio

An individual registers several residential properties in the name of a company with minimal operational activity and undisclosed beneficial ownership. Tenancy agreements are prepared for each property showing a different tenant. The tenants are nominees or do not exist. Monthly rental deposits enter the company’s account from multiple sources, creating the appearance of a diversified property management business.

The scheme surfaces during an MoET inspection when the agent managing three of the properties cannot produce verifiable evidence of actual occupancy, and the tenancy agreement dates do not correspond to any registration in the Ejari system.

Scenario 3: Multi-Jurisdictional Rental Layering

An illicit operator holds a property through a company registered in a jurisdiction with weak beneficial ownership disclosure. A related entity in a third country pays rental income that originates from criminal proceeds generated elsewhere. The rent is remitted as a regular international wire transfer, described as rental income for a commercial property.

Cross-border third-party payments involving multiple jurisdictions are commonly recognised indicators of real-estate money laundering typologies and may also raise sanctions-evasion concerns.

How Do Rental Income Schemes Facilitate Money Laundering?

Rental income schemes operate at the integration stage of the money laundering process. By the time rental income is deposited, the predicate proceeds have already been placed and layered through earlier stages. The rental mechanism provides the integration cover: a commercially ordinary activity, a documented contractual basis, a verifiable bank account, and a recurring income stream that is associated with legitimate property investment.

The tactical value is that integration through rental income achieves a clean exit from the laundering cycle at a relatively low operational cost. A property already owned provides the infrastructure; the scheme requires only a connected tenant, a bank account, and documentation that survives routine review.

How Do Criminals Exploit Rental Income Schemes?

Banks are exploited as the primary vehicle for receiving and distributing rental income. A bank account used to receive inflated or fictitious rent payments carries the appearance of a legitimate property business account. Banks relying on standard CDD procedures without market-rate benchmarking, beneficial ownership verification, or occupancy confirmation may inadvertently provide the laundering infrastructure.

Illicit operators design and control the scheme. They establish the ownership structure, arrange the tenancy, and direct the movement of funds post-deposit. Real estate professionals may be complicit or unknowing participants. Shell and front companies provide the critical ownership layer. Trust and company service providers (TCSPs) establish and maintain the corporate vehicles used to hold rental properties.

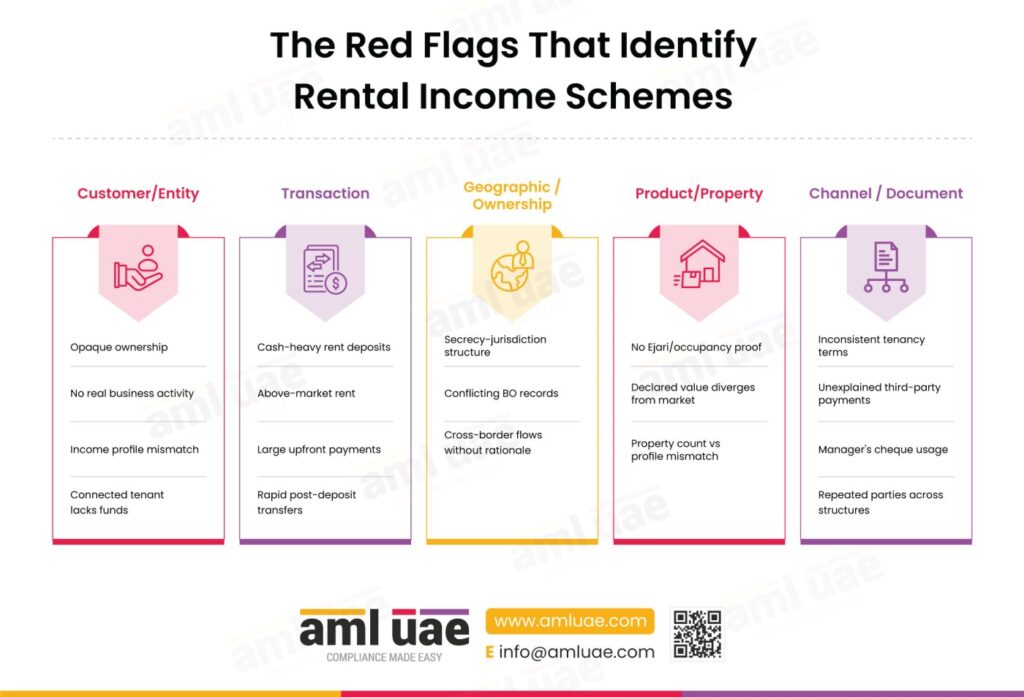

What Are the Red Flags That Identify Rental Income Schemes?

| Category | Observation |

| Customer / Entity | Property is held through a company with no verifiable operational activity, undisclosed beneficial owners, or a recently established registration with no credible commercial history. |

| Customer / Entity | The rental income account holder’s declared business profile is inconsistent with the scale or number of properties generating income. |

| Customer / Entity | Tenant or connected party has no verifiable legitimate source of funds sufficient to sustain the stated rental level. |

| Customer / Entity | A property manager or letting agent processes rental transactions across multiple unrelated properties or jurisdictions without a clear commercial rationale. |

| Customer / Entity | The customer has PEP status or confirmed associations with persons facing criminal proceedings in other jurisdictions. |

| Transaction | Rental income deposits include unusually high volumes of cash exceeding what market rates for the relevant property type would generate. |

| Transaction | Declared rental amounts diverge significantly from independently verifiable local market rates for comparable properties. |

| Transaction | Large upfront rental payments covering multiple months arrive from individuals with no verified legitimate source of funds. |

| Transaction | Funds are rapidly transferred to other accounts shortly after the rental income deposit. |

| Transaction | Rental payments are deposited on an irregular schedule, deviating from standard monthly lease cycles. |

| Transaction | Rental income deposits originate from parties in high-risk jurisdictions without a documented commercial explanation. |

| Geographic / Ownership | Rental property is held through a legal structure registered in a secrecy jurisdiction with minimal beneficial ownership disclosure requirements. |

| Geographic / Ownership | Beneficial ownership records are contradictory or incomplete across multiple accounts connected to the same property. |

| Product / Property | Rental income deposits are linked to properties with no verifiable evidence of actual occupancy or Ejari registration. |

| Product / Property | Market value and declared transaction value diverge materially without a documented commercial explanation. |

| Channel / Document | Tenancy agreements contain inconsistencies in key terms, parties, dates, or signatures, indicating possible fabrication. |

| Channel / Document | Third-party rental payments are received from parties unconnected to the stated tenant without explanation. |

| Channel / Document | Manager’s cheques or cashier’s cheques are used to settle rental amounts, obscuring the source of funds. |

| Channel / Document | The same individuals appear as directors, tenants, and beneficial owners across multiple property structures. |

Key Controls Against Rental Income Laundering Schemes

| Control | What It Disrupts | Type | Key Limitation |

| Customer Due Diligence (CDD) | Anonymous or opaque property ownership at onboarding | Prevents | Effectiveness depends on the quality of documentation provided |

| Enhanced Due Diligence (EDD) | High-risk customer profiles, including offshore corporate owners | Prevents | Resource-intensive; risk-tiering misclassification bypasses it |

| OSINT and External Verification | Fabricated income claims and undisclosed beneficial ownership | Detects | Offshore BO data may not be publicly available |

| Ongoing Due Diligence | Pattern changes in rental income accounts after onboarding | Detects | Alert fatigue reduces quality at high transaction volumes |

| Risk-Based Customer Profiling | Blanket low-risk assignment to property companies | Prevents | Static profiles miss dynamic risk escalation |

| Staff AML Training | Undetected red flags at onboarding and account review | Detects | Generic training is insufficient for typology-specific indicators |

| Third-Party Risk Management | Property manager intermediary risk | Detects | Contractual reliance does not transfer legal liability |

| Transaction Monitoring | Layering through rapid post-deposit transfers | Detects | Generic rules will miss rental-specific behavioural patterns |

How Do AI and RegTech Automate Detection of Rental Income Schemes?

Rental income schemes produce distinctive behavioural signatures that are well-suited to automation, provided the underlying rules and models are calibrated to the specific pattern rather than to generic suspicious activity.

Transaction monitoring platforms can apply scenario-based rules that flag accounts exhibiting rapid post-deposit fund movement where the account description is a property or rental business. Systems that incorporate peer-group benchmarking can compare deposit volumes against market rental rates for the declared property type and location, generating alerts where declared income materially exceeds achievable market rents.

Network analytics and graph intelligence tools identify the relationship structures that underlie rental income schemes. When a beneficial owner controls multiple entities appearing as both landlord and tenant counterparties within the same transaction network, graph analytics will surface the circular relationship that manual review may miss.

Machine learning anomaly detection models trained on verified rental income typology cases can identify deviation from expected deposit and withdrawal patterns without requiring specific rule definitions. Unsupervised clustering can group property accounts by their behavioural signatures and surface outliers whose deposit timing, counterparty diversity, and post-deposit movement are inconsistent with legitimate property businesses.

What Data Should Compliance Teams Collect to Detect Rental Income Schemes?

| Data Point | Source System | What It Reveals |

| Beneficial ownership records | Company and beneficial ownership registries | Identifies true controllers of property-holding companies; surfaces offshore structures |

| Rental market rate benchmarks | Third-party property market databases | Validates whether declared rental income is consistent with achievable market rates |

| Tax filings and declared income | Financial, business, and tax records | Reveals inconsistencies across tax returns, bank statements, and corporate accounts |

| KYC and CDD profile data | KYC and customer due diligence records | Tests rental income volume against economic profile; records PEP status and adverse media |

| Ejari registration and occupancy data | Real estate and high-value asset records (UAE Ejari) | Confirms whether a tenancy agreement is formally registered and occupancy is genuine |

| Transaction history | Transaction logs | Identifies cash-heavy deposits, irregular schedules, and rapid post-deposit transfers |

| Corporate registry records | Company and beneficial ownership registries | Reveals recently established entities with large transactions; identifies dissolved-and-re-established vehicles |

How Do Rental Income Schemes Aggravate Customer Risk and Product Risk?

Customer risk is elevated primarily through the use of corporate ownership structures to conceal the beneficial owner of the rental property and, by extension, the beneficial owner of the rental income account. When a property is held through a company with undisclosed beneficial owners, the regulated entity’s customer is a legal fiction whose risk profile cannot be properly assessed. The true controller may be a PEP, a person subject to sanctions, or an individual with a criminal record in another jurisdiction.

Product risk is elevated because bank accounts and property management arrangements are standard products, not intrinsically suspicious. The rental income typology specifically exploits the low inherent risk perception attached to property businesses. Product risk is highest where institutions have not calibrated assessments to include a rental market validation component for property-linked accounts.

What Compliance Officers Observe When Rental Income Schemes are Present

Rental income schemes produce observable patterns at multiple review points. A compliance officer would typically observe one or more of the following: deposits described as rental income on accounts where the beneficial owner cannot be independently verified against a property registry; tenancy documentation that is internally inconsistent in dates, parties, or rental rates; deposit amounts inconsistent with the declared size, type, or location of the property; rapid outbound transfers within few hours of rental income deposits, particularly to counterparties in different jurisdictions; and cash rental deposits disproportionately large relative to comparable properties in the same market.

Sectors at Highest Exposure

| Sector | Risk Rating | Reasoning |

| Retail and Private Banking | Critical | Bank accounts are the primary mechanism for rental income deposit and layering; the absence of rental-specific TM rules carries the highest residual exposure. |

| Real Estate Brokerage and Agency | Critical | Real estate agents conclude transactions establishing property ownership and tenancy arrangements; MoET recorded 225 violations during the review period. |

| Trust and Company Service Providers | High | TCSPs establish shell and front company structures that conceal beneficial ownership; the UAEFIU 2023 report identifies legal person abuse as a specific typology pattern. |

| Property Management | High | Property managers process rental payments on behalf of owners; they can become unwitting intermediaries without adequate CDD. |

| Commercial and Corporate Banking | Moderate | Business bank accounts used by property-linked companies may receive rental income that is harder to validate without specific sector risk parameters. |

Best Practices for Rental Income Schemes Risk Management

- File STR reports independently and without delay. If the transaction generates suspicion, file the STR separately under FDL 10/2025 Article 18.

- Identify and verify beneficial owners of all property-holding companies before establishing or maintaining an account. CR 134/2025 Article 10 and CR 109/2023 set a 25% threshold for BO identification. Request the BO register, articles of association, and independent registry confirmation. Do not accept nominee directorship structures as the endpoint of the BO identification process.

- Benchmark declared rental income against market rates at onboarding and at each periodic review. Obtain market rental data for the declared property type, size, and location from a recognised property market source. Where declared income materially exceeds market rates without a credible explanation, treat the discrepancy as a risk indicator and escalate to EDD.

- Verify occupancy through formal registration records, not document review alone. For UAE residential and commercial tenancies, confirm Ejari registration. Where a tenancy is declared but cannot be verified through the formal registration system, treat the discrepancy as a significant red flag.

- Apply Enhanced Due Diligence to property accounts held through offshore or multi-layered corporate structures. Any property-linked account where the ownership chain includes entities registered in secrecy jurisdictions or companies that cannot demonstrate genuine economic activity should be escalated to EDD regardless of whether the beneficial owner has been tentatively identified.

- Configure transaction monitoring rules specifically for rental income behavioural patterns. Implement rules that flag: cash deposits to property business accounts; rapid post-deposit outbound transfers; deposit schedules deviating from standard monthly rental cycles; and cross-border transfers to high-risk jurisdictions on accounts with a domestic property income description.

- Conduct property-specific OSINT at onboarding and at enhanced due diligence review. Check BO registries, property registry records, adverse media for the property address and associated parties, court records, and sanctions lists.

- Assess the risk profile of property managers and letting agents who intermediate rental payments. Where a property manager collects and remits rental income on behalf of a client, treat the property manager as a third party. Document your assessment of the property manager’s CDD procedures.

- Train relationship managers and front-line staff on rental income-specific red flags. Annual training must include scenarios drawn from documented UAE rental income typologies, including the patterns identified in the UAEFIU December 2023 typology report.

Best practices work when they run as one routine, not separate checklist items. Comparing declared rent against the local market at onboarding catches most schemes early, and confirming the tenancy through Ejari closes the door on fabricated contracts.

How Rental Income Schemes and Real Estate-Based Methods Are Related

Rental income schemes are a specific variant within the broader category of real estate-based money laundering methods. Real estate-based methods are the parent typology that encompasses all techniques in which immovable property is used as either the vehicle or the mechanism for the movement and integration of criminal proceeds.

Rental income schemes are distinct because the laundering does not depend on the property transaction itself. The laundering occurs at the income level, not the capital level. This directs detection efforts towards financial institutions and account-level monitoring rather than transaction-level conveyancing scrutiny.

| Term | Connection to Rental Income Schemes |

| Real Estate-based Methods | Parent typology; rental income schemes are one variant of real estate-based laundering techniques. |

| Shell Companies | Primary corporate vehicle used to hold rental properties and obscure beneficial ownership. |

| Front Companies | Companies with apparent commercial activity used to produce rental income paper trails. |

| Beneficial Ownership | The concept that rental income schemes are specifically designed to defeat |

| Customer Due Diligence (CDD) | Primary preventive control; CDD failures in property-linked accounts are the main enabler. |

| Enhanced Due Diligence (EDD) | Applied to high-risk property accounts with opaque corporate ownership structures. |

| Suspicious Transaction Report (STR) | Reporting mechanism triggered when ML/TF suspicion arises under FDL 10/2025 Article 18 |

| Real Estate Activity Report (REAR) | MoET-mandated report for cash freehold transactions at or above AED 55,000 |

| Integration | The money laundering stage at which rental income schemes operate |

| Layering | Stage 4 of the rental income scheme; rapid post-deposit fund transfers |

| Transaction Monitoring | Detective control is most effective against the post-deposit layering behaviour. |

What Financial Instruments Do Criminals Use in Rental Income Schemes?

Bank accounts are the central instrument in rental income schemes. The scheme cannot function without a bank account to receive the inflated or fictitious rental payments and to provide the deposit records that constitute the integration evidence. Criminals exploit standard business bank accounts by presenting them as property management accounts and insulating the beneficial owner behind a corporate account holder.

Cash is introduced at the deposit stage in schemes where criminal proceeds are not yet in the banking system. Cash rental deposits allow the illicit operator to bypass wire transfer records by presenting the criminal funds as rental income received in cash from a connected tenant.

Real estate is the foundational instrument that provides the scheme with commercial credibility. The property creates the rationale for the rental income stream. Criminals exploit real estate both to hold criminal capital in a tangible asset and to generate the income narrative that supports the integration of further proceeds.

| Variant or Synonym | Context or Jurisdiction | Distinction from Primary Term |

| Rental income laundering | General financial crime vocabulary | Descriptive synonym; no structural distinction |

| Property income manipulation | UK and Australian AML reporting contexts | May include income from property sales as well as rental income |

| Fictitious rental scheme | FATF typology literature | Specifically refers to schemes where the property is not genuinely let; a subset. |

| Inflated rental scheme | UAEFIU and MoET guidance | Refers specifically to above-market-rate variants where genuine occupancy exists |

| Real estate income laundering | Cross-border regulatory discourse | A broader term that encompasses both rental income and property sale proceeds |

What Products and Services Do Criminals Abuse in Rental Income Schemes?

Business bank accounts are abused by presenting criminal proceeds as commercial rental income and routing them through accounts held in the name of property companies. Where the bank has not verified the beneficial owner of the corporate account holder or benchmarked the declared rental income against market rates, the account becomes a laundering vehicle with commercial camouflage.

Property management services are abused where property managers process rental collections on behalf of property owners without conducting their own CDD on the origin of the rental income. A property manager who collects, consolidates, and remits rents across multiple properties can aggregate inflated payments into a single remittance that appears to be diversified legitimate income.

Real estate services are abused at the point of property acquisition and tenancy arrangement. Real estate agents who conclude transactions for property used as laundering vehicles contribute the transaction documentation, valuation records, and tenancy agreements that constitute the paper trail of the scheme.

Trust and corporate services are abused to create and maintain the corporate structures through which rental properties are held. TCSPs who establish companies and appoint nominees without adequate CDD on the ultimate beneficial owner provide the legal infrastructure for the ownership opacity that rental income schemes require.

How AML UAE Helps Manage Rental Income Schemes Risk Effectively

The core AML risk that rental income schemes expose is the gap between what a property business declares and what the underlying property market and ownership records confirm. Closing that gap requires sector-specific expertise in UAE real estate CDD and the ability to calibrate transaction monitoring for rental income behavioural patterns.

AML UAE provides compliance advisory specifically built around the UAE regulatory framework under FDL 10/2025. For financial institutions and DNFBPs with exposure to property-linked accounts, this means guidance on beneficial ownership identification, transaction monitoring rule design for rental income typologies, and EDD procedures for high-risk property accounts held through corporate structures.

AML training programmes from AML UAE address rental income-specific scenarios alongside the broader DNFBP obligations under CR 134/2025. Training content is built from verified UAE typology case patterns, giving front-line staff the specific indicators that generic courses do not cover.

Conclusion - Rental Income Schemes

Rental income schemes succeed because they exploit the gap between the appearance of a legitimate property business and the reality of what is producing the income. That gap is not visible in a single transaction; it is visible only when deposit volumes are tested against rental market data, ownership structures are traced to their beneficial owners, and occupancy records are verified through formal registration systems.

The UAE regulatory framework is comprehensive. FDL 10/2025 and CR 134/2025 impose clear obligations on real estate agents, financial institutions, and TCSPs. The CR 109/2023 beneficial ownership register requires every UAE legal person to identify its beneficial owners at the 25% threshold. The MoET’s enforcement record confirms that supervisory scrutiny of real estate sector compliance is active, not aspirational.

The starting point is sector-specific expertise aligned to the typologies the UAEFIU has documented, the controls CR 134/2025 mandates, and the inspection standards the MoET enforces. If your CDD procedures for property accounts, your transaction monitoring rules for rental income patterns have not been reviewed against the current FDL 10/2025 framework, the time to address that gap is before the next inspection, not after it.

Frequently Asked Questions - Rental Income Schemes

A rental income scheme is an integration-stage money laundering typology in which criminal proceeds are introduced into the financial system by disguising them as rental income from real property. The scheme typically uses inflated rental rates, fabricated tenancy agreements, or fictitious tenants to generate deposit records that present criminal funds as earned property income.

Federal Decree Law No. 10 of 2025 (FDL 10/2025) criminalises money laundering under Article 2. ML penalties for natural persons range from one to ten years’ imprisonment and fines between AED 100,000 and AED 5,000,000 under Article 26. Legal persons face fines between AED 5,000,000 and AED 100,000,000.

A shell company holds the rental property as the registered owner, separating the beneficial owner from the direct link to the rental income account. Cabinet Resolution No. 109 of 2023 requires all UAE legal persons to maintain a beneficial ownership register with a 25% identification threshold and update it within 15 days of any change.

The most operationally significant red flags are: rental income deposits linked to properties where the BO of the holding company cannot be independently verified; deposit amounts that materially exceed market rental rates for the declared property type; rapid outbound transfers within a few hours of rental deposits to counterparties in different jurisdictions; and cash deposits to accounts described as property businesses.

Administrative penalties for DNFBPs under CR 71/2024 reach AED 500,000 for STR filing failure. Under FDL 10/2025 Article 17, administrative penalties may reach AED 5,000,000 per violation. Criminal liability for STR failure or CDD breach is established under FDL 10/2025.

Transaction monitoring detects rental income schemes when rules are calibrated to the specific behavioural patterns the typology produces. Effective rules flag: rapid post-deposit outbound transfers exceeding a defined percentage within 48 hours; deposit schedules deviating from standard monthly rental cycles; and deposit amounts exceeding a market-rate benchmark for the declared property.

Verification requires cross-referencing four data points: the declared rental rate against market data for comparable properties; the tenancy agreement against Ejari registration; the identity of the tenant against CDD records; and the BO of the property holding company against registered BO records. Where any element cannot be confirmed, the discrepancy is treated as a red flag requiring escalation.

Integration-stage schemes are the hardest to detect because criminal proceeds have already been placed and layered before they appear as rental income. Detection depends on file-level analysis and behavioural monitoring rather than transaction-by-transaction screening, making onboarding and periodic review the most effective detection windows.

Protect Your Real Estate Portfolio

Build stronger AML controls around rental activity, tenant verification, and source-of-funds checks.

Share via :

About the Author

Pathik Shah

FCA, CAMS, CISA, CS, DISA (ICAI), FAFP (ICAI)

Pathik is an ACAMS-certified AML consultant specialising in governance, risk, and compliance for regulated entities in the UAE. He brings over 28 years of experience, with 1,000+ hours of AML training and 200+ advisory engagements across DNFBPs, VASPs, and FIs. He supports businesses in aligning with AML/CFT requirements from the CBUAE, DFSA, MoET, MoJ, VARA, CMA, FSRA, and FATF. Known for translating complex regulations into audit-ready procedures, Pathik enables operational clarity and compliance readiness.

Reach Out to Pathik