Precious Commodity Smuggling

Last Updated: 06/26/2026

Protect your business with reliable and effective AML strategies with AML UAE.

Precious Commodity Smuggling: In Brief

Physically transporting gold, diamonds, or gemstones across borders without customs declaration converts criminal proceeds into portable, untraceable value. DPMS entities represent a structural vulnerability within this typology, as smuggled commodities routinely re-enter the legitimate economy through dealers. They therefore face binding AML/CFT obligations under FDL 10/2025 and CR 134/2025, including customer and enhanced due diligence, sanctions screening, DPMSR filing for covered transactions at or above AED 55,000, and STR filing through goAML where suspicion of money laundering, terrorist financing, or proliferation financing arises. Market-rate comparison and responsible-sourcing checks are practical risk-based controls that support this framework.

What is Precious Commodity Smuggling?

Summary: Precious commodity smuggling is the illegal cross-border movement of high-value goods such as gold, diamonds, and gemstones, hidden from customs to disguise the origin of criminal funds.

Precious Commodity Smuggling is the illegal transportation of highly valuable items, such as gold, diamonds, precious metals, or gemstones, across international or domestic borders while deliberately hiding them from customs and border authorities.

What makes it particularly attractive to criminals is the characteristic of the commodities themselves. The high value, physical compactness, and global convertibility of these assets allow criminals to transport illicit proceeds in a form that resists paper-trail scrutiny. Precious commodities do not require a bank account, do not generate wire transfer records, and can be melted, recut, or alloyed to destroy physical evidence of their origin.

The Financial Action Task Force (FATF) identifies precious metals and stones as high-risk instruments for trade-based money laundering and terrorist financing, owing to their capacity to store and transfer value across jurisdictions with minimal regulatory oversight.

Regulatory Framework Related to Precious Commodity Smuggling

UAE Regulatory Snapshot

| Requirement | UAE position |

| Main AML law | Federal Decree-Law No. 10 of 2025 (FDL 10/2025) |

| Executive regulation | Cabinet Resolution No. 134 of 2025 (CR 134/2025) |

| DPMS supervisor | Ministry of Economy and Tourism (MoET) |

| Financial intelligence unit | UAEFIU, operating within the Central Bank (CBUAE) |

| Reporting platform | goAML |

| Threshold report | DPMSR for covered cash transactions, and entity wire transfers, at or above AED 55,000 (single or linked) |

| Suspicion report | STR or SAR filed where suspicion of money laundering, terrorist financing, or proliferation financing arises |

Summary: In the UAE, the obligations sit under FDL 10/2025 and CR 134/2025, which bring dealers in precious metals and stones into DNFBP scope and impose CDD, DPMSR, STR/SAR, and record-keeping obligations according to transaction type, threshold, and suspicion indicators.

The primary legislative instrument governing anti-money laundering obligations in the UAE is Federal Decree-Law No. (10) of 2025 Regarding Anti-Money Laundering, Combating the Financing of Terrorism and Proliferation Financing. (FDL 10/2025).

Article 2 criminalises money laundering, including converting or transferring proceeds from predicate offences to conceal their illicit origin.

Article 10 mandates that any person entering or leaving the state must disclose the amount of cash, bearer negotiable instruments, precious metals and valuable stones they are carrying, in accordance with the national disclosure framework.

Articles 18 and 19 impose statutory reporting obligations and preventive measures on all regulated Financial Institutions (FIs), Designated Non-Financial Businesses and Professions (DNFBPs), and Virtual Asset Service Providers (VASPs). These include filing a Suspicious Transaction Report (STR) on suspicion, identifying customers, and applying enhanced due diligence in higher-risk situations.

Cabinet Resolution No. (134) of 2025 (CR 134/2025) operationalises (FDL 10/2025) for all regulated entities. Article 3(3) brings Dealers in Precious Metals and Stones (DPMS) within the DNFBP scope, triggering customer due diligence, DPMSR, and record-keeping obligations for covered transactions at or above AED 55,000 (single or linked), while an STR or SAR is required where suspicion of money laundering, terrorist financing, or proliferation financing arises.

Article 5 requires all regulated entities to conduct an Enterprise-Wide Risk Assessment that incorporates sector-specific typology intelligence and establish internal policies to manage and mitigate the identified risk.

The Supplemental Guidance for DPMS 2026 obligates DPMS to file a Dealers in Precious Metals and Stones report (DPMSR) for any cash transaction with a resident or non-resident individual at or above AED 55,000, and for any transaction with a corporate entity at or above AED 55,000, whether settled in cash or by wire transfer, including linked transactions.

Ministerial Decree No. (68) of 2024 and the Ministry of Economy & Tourism (MoET) Due Diligence Regulations for Responsible Sourcing of Gold, impose a legally binding five-step supply chain due diligence framework on gold refineries and supply chain participants, directly targeting the smuggling and conflict origin commodity typology.

Regulatory Reference

Federal Decree-Law No. (10) of 2025, Article 2 (ML criminalisation); Article 18 (STR obligation); Article 19 (preventive measures); Article 10 (Disclosure) | Cabinet Resolution No. (134) of 2025, Articles 3(3), 5, 15,16,17, 18,19,20, 23 | Supplemental Guidance for Dealers in Precious Metals and Stones (March 2026) obligating DPMSR goAML threshold reporting | Ministerial Decree No. (68) of 2024: Gold Refinery Responsible Sourcing

Supervisory Body

Summary: The UAE Ministry of Economy and Tourism (MoET) supervises dealers in precious metals and stones for AML/CFT, while the Financial Intelligence Unit, housed within the Central Bank, receives all reports through the goAML portal.

The Ministry of Economy and Tourism (MoET) is the supervisory authority for all DNFBPs, including DPMS entities. MoET conducts risk-based onsite and offsite inspections, issues administrative penalties under (CR 71/2024), and supervises compliance with CDD, goAML reporting, and AML/CFT policy requirements.

The UAE Financial Intelligence Unit (UAEFIU), established as an independent unit within the Central Bank of the UAE (CBUAE), receives all STRs, SARs, and DPMSRs via the goAML platform and conducts strategic analysis of typology patterns, including commodity smuggling.

Reporting Obligations and Channels of Precious Commodity Smuggling

DPMSR, STR and SAR: Which Report Applies

| Report | When it applies | Trigger |

| DPMSR | Covered DPMS transactions | Cash transaction with an individual, or a cash or wire transaction with an entity, at or above AED 55,000 (single or linked transactions) |

| STR | A specific suspicious transaction | Reasonable suspicion of money laundering, terrorist financing, or proliferation financing, regardless of amount or threshold |

| SAR | Suspicious activity or conduct | Suspicion relating to activity or behaviour not tied to a single transaction, including attempted or refused dealings |

Summary: Regulated dealers file STRs on suspicion and DPMSRs for covered cash or entity transactions at or above AED 55,000, all submitted to the UAEFIU via goAML.

Regulated DPMS entities must file a DPMSR via goAML for every cash transaction at or above AED 55,000, whether conducted by individuals or entities. For entity counterparties, the same threshold applies to wire transfers.

Required DPMSR fields, including the involved person’s nationality, place of incorporation, and business activity, must be fully populated. DPMS entities must also file an STR without delay via goAML when suspicion of money laundering, terrorist financing, or proliferation financing arises, regardless of transaction value.

Gold refineries must additionally comply with the five-step responsible sourcing framework under the MoET Due Diligence Regulations, which requires due diligence on each gold supply, appointment of a compliance officer at the senior level, and an independent third-party audit by an MoET-accredited reviewer.

Enforcement Actions

Summary: CR 71/2024 sets the administrative penalty schedule, with fines reaching AED 500,000 for enhanced due diligence failures and AED 1,000,000 for failing to freeze funds on a sanctions match.

Precious commodity smuggling may involve predicate offences such as customs evasion, fraud, sanctions evasion, and organised crime, and UAEFIU typology analysis recognises the misuse of precious metals and stones as a channel that can support terrorist financing. This typology has been observed in cross-border network schemes.

The UAE’s regulatory authorities have demonstrated a robust and proactive enforcement posture across the DPMS sector. The FDL 10/2025, Cabinet Resolution No. (71) of 2024 (CR 71/2024), together with the 2026 DPMS supplemental guidance, has tightened controls, broadened personal liability, and strengthened supply chain traceability.

REGULATORY REFERENCE

Cabinet Resolution No. (71) of 2024: Administrative Penalties for AML/CFT Violations by DNFBP entities supervised by MoET | Maximum fine for TFS-related violations: AED 1,000,000 (CR 71/2024, Violation 35) | Maximum fine for EDD failures: AED 500,000 (CR 71/2024, Violations 15-17)

What Does Precious Commodity Smuggling Mean?

Summary: The term covers the illicit movement of precious metals and stones to obscure the source of criminal proceeds, overlapping with but narrower than broader commodity smuggling.

Picture a gold trading shop in a busy market having a trade license, looking completely legitimate. Behind the operations, the gold is coming from an illegal mine, smuggled across borders, hidden inside a cargo box or strapped to a courier who declared nothing at customs. Once the gold arrives, it is melted down and reshaped into clean bars or jewellery, sold at full market price and the profit is recorded as normal business income. Through this mechanism, criminals turn illegal gold into legitimate, spendable money.

Why Detecting Precious Commodity Smuggling Matters

Summary: As one of the world’s largest gold trading hubs, the UAE carries concentrated exposure, making precious-commodity controls central to the integrity of its trade and financial system.

Precious commodities carry a high value-to-weight ratio, move across borders without generating bank records and can be melted or recut to permanently destroy evidence of origin. These characteristics make precious commodities a near-perfect vehicle for the placement stage of money laundering.

The UAE sits at the heart of this risk, as one of the world’s largest gold trading hubs. The CBUAE September 2025 Quarterly economic review reports continued year-on-year growth in the UAE’s non-oil foreign trade, with gold and jewellery a significant component. These volumes of transactions make the detailed scrutiny of every deal operationally challenging for both DPMS entities and supervisory authorities.

Recognising this risk, the UAE has responded with a clear regulatory framework. CR 134/2025 requires regulated entities to apply customer due diligence, conduct an enterprise-wide risk assessment, file DPMSRs for covered threshold transactions, and apply enhanced due diligence where higher-risk indicators arise. Failure to maintain adequate controls may expose the entity to administrative penalties under CR 71/2024, which prescribes fines up to AED 500,000 for EDD failures and AED 1,000,000 for failures to freeze assets where a TFS match is identified.

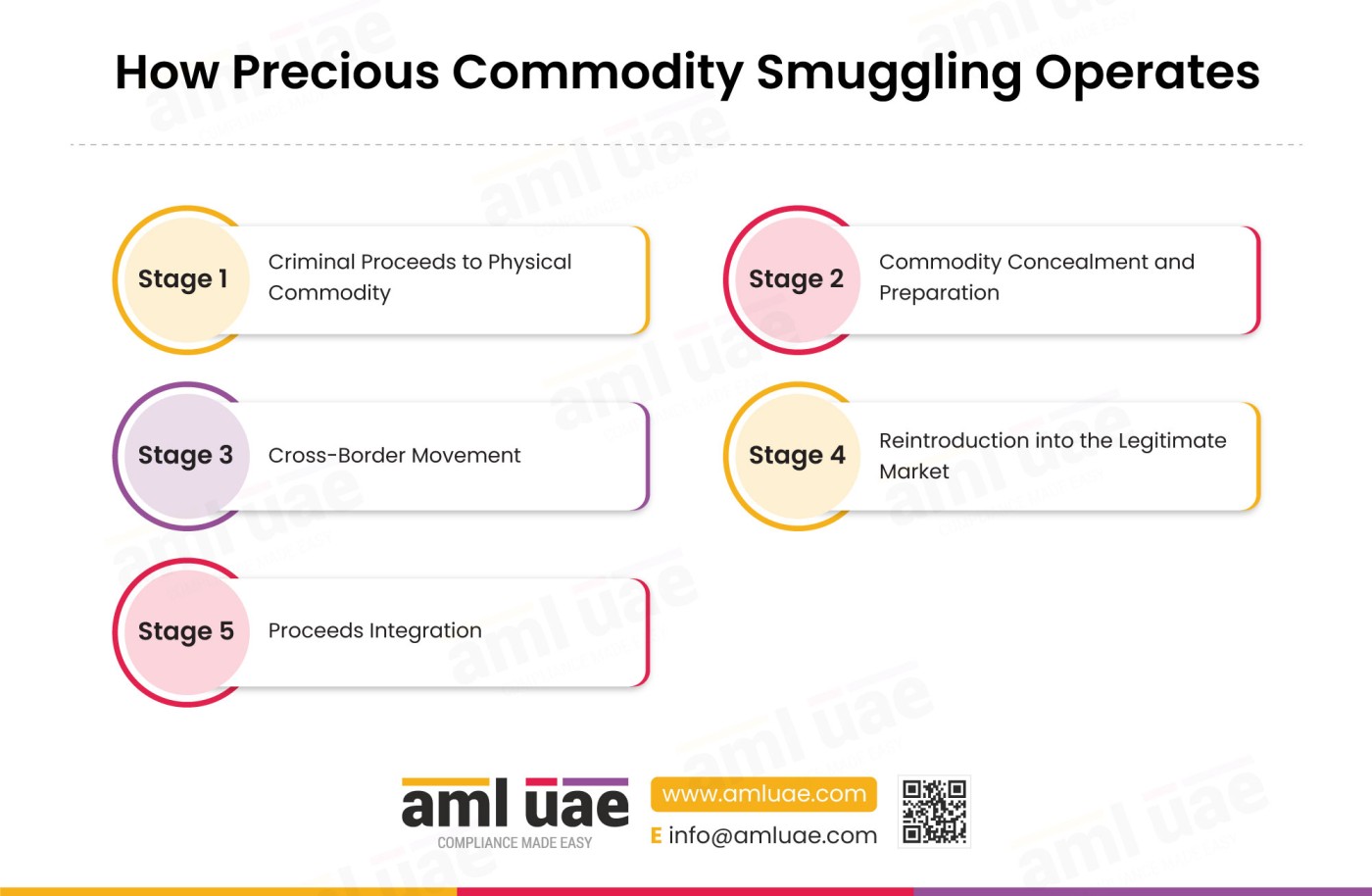

How Precious Commodity Smuggling Operates

Summary: Schemes move through five stages, converting criminal proceeds into physical commodities, concealing and transporting them across borders, then reintroducing the value into the legitimate market.

Stage 1: Criminal Proceeds to Physical Commodity

Criminal proceeds, which may have originated from drug trafficking, fraud, extortion, or other predicate offences, are converted into physical precious commodities through direct cash purchases. Purchases may be split into several transactions kept below the AED 55,000 threshold to avoid reaching the DPMSR and goAML reporting obligations. Multiple transactions across different vendors, spread over days or weeks, aggregate to a significant value without triggering any single filing.

Stage 2: Commodity Concealment and Preparation

Once acquired, the commodity is physically altered to evade customs identification. Gold bars are melted and recast into common objects such as car parts, tools, or jewellery pieces. Gemstones are mixed with legitimate cargo or misclassified on shipping documentation as low-value industrial minerals. Couriers carry commodities in checked luggage declared below customs declaration thresholds, relying on inconsistent enforcement at border crossings.

Stage 3: Cross-Border Movement

The prepared commodity crosses an international border, typically from a conflict-affected region towards a major trading hub, without a declaration reflecting true value or origin. In documented cases, gold has entered the country through land borders, sea cargo, and passenger baggage channels, often after transit through one or more intermediate jurisdictions with minimal customs controls.

Stage 4: Reintroduction into the Legitimate Market

At the destination, the smuggled commodity enters the legitimate precious metals and stones supply chain through DPMS entities, refineries, or jewellery manufacturers. A refinery that melts and reprocesses the commodity destroys its physical traceability. The gold or gems are then sold through normal trade channels, with the sale proceeds appearing on paper as legitimate business income from commodity trading.

Stage 5: Proceeds Integration

Sale receipts from the commodity are deposited into bank accounts, transferred through letters of credit, or applied to loans secured against commodity holdings. At this point, the criminal proceeds have been fully layered and are reintegrated into the financial system as legitimate trade income. The link to the original predicate offence has been severed by the physical transformation and multiple border crossings, making it difficult for authorities to identify the source of funds.

Real-World Examples of Precious Commodity Smuggling

Summary: Common patterns include conflict gold routed through intermediary refineries, structured jewellery purchases converted quickly to cash, and under-invoiced trade documentation.

Conflict Gold Routed Through an Intermediary Refinery

Criminal networks sourcing gold from conflict-affected areas export the commodity to a country with limited due diligence requirements for gold trade. The exporter presents falsified certificates of origin identifying a neutral, low-risk jurisdiction. A refinery in the destination country purchases the gold at market rate, processes it, and sells gold bars carrying the refinery’s own hallmark, which is internationally recognised and trusted. The illicit origin of the underlying gold is permanently obscured by the hallmarking process.

The key detection opportunity lies at the supply chain onboarding stage: a refinery that does not apply the OECD-based five-step due diligence framework per MOE Due Diligence Regulations cannot detect this substitution.

(Source: FATF | https://www.fatf-gafi.org/en/publications/Methodsandtrends/Moneylaundering-gold.html)

Structured Jewellery Purchases and Rapid Conversion

A criminal with significant cash proceeds from fraud makes a series of jewellery purchases at multiple DPMS vendors over several weeks, keeping each transaction below the reporting threshold. The jewellery is transported to a second jurisdiction, where it is sold at market value through a pawnbroker or commodity exchange. The proceeds are deposited into a business account and described as income from jewellery trading.

The detection failure occurs at the DPMS vendor level: no single vendor observes the cumulative value of purchases, no enhanced due diligence is applied despite the customer’s cash-intensive behaviour, and no STR is filed. Aggregating transaction data across vendors, which goAML’s analytical tools support, would reveal the full pattern.

Trade Document Manipulation and Under-Invoicing

An organised crime group exports a consignment of gold bullion from a source country to a trading hub and deliberately under-invoices the consignment, declaring its value as USD 50,000 instead of its actual market value of USD 500,000. The receiving DPMS entity purchases the goods at the declared value and pays the seller accordingly. This under-invoicing allows value to be transferred from the importing jurisdiction to the exporting party without generating a financial transfer record.

Compliance officers reviewing trade documentation against prevailing commodity market price data would identify the discrepancy; the failure occurs when no market-rate cross-check is performed on the declared value of the imported commodity.

How Does Precious Commodity Smuggling Facilitate Money Laundering?

Summary: Precious commodities act as a portable store of value that breaks the audit trail, letting criminals place, layer, and integrate illicit funds without bank records.

The fact that a commodity can be layered into the financial system without a trace is essential to money launderers. Unlike wire transfers and bank deposits, physical commodities do not require an account or institution through which the transfer must be recorded.

A criminal who acquires gold with cash has completed the placement stage and immediately entered the layering stage without engaging any regulated financial institution. Each subsequent border crossing adds a jurisdictional layer that makes the asset’s history harder to reconstruct, particularly once the commodity is processed by a refinery or incorporated into manufactured goods.

How Do Criminals Exploit Precious Commodity Smuggling?

Summary: Criminals exploit weak provenance checks, cash-intensive dealing, and the ease of melting or recutting goods to obscure their origin and ownership.

There are two ways in which precious commodity smuggling is exploited through organised crime groups and shell or front companies.

Organised crime groups provide the operational capacity to execute multi-jurisdictional smuggling routes. They maintain relationships with corruption-prone customs officers, courier networks, and commodity traders across multiple countries.

These groups exploit inconsistencies in precious metal customs controls between jurisdictions, specifically choosing routes where cargo inspection rates are low, declaration thresholds are high, or penalty regimes for under-declaration are modest.

Shell or front companies provide the legal and financial infrastructure through which the commodity purchase and sale are executed. A shell company incorporated in a secrecy jurisdiction may acquire gold from an organised crime group and sell it to a refinery or jeweller, while concealing the identity of the ultimate beneficial owner (UBO)

Front companies that conduct legitimate precious metals trade alongside illicit activity are particularly difficult to detect because they generate real invoices, customers, and banking relationships, which obscure the suspicious transactions.

What Are the Red Flags That Identify Precious Commodity Smuggling?

Summary: Key warning signs cluster around structured or cash payments, opaque ownership, inconsistent trade documents, and sourcing linked to conflict-affected or high-risk areas.

| Category | Red Flag |

| Customer | Multiple cash purchases of gold or diamonds, each below AED 55,000 threshold, within a short period from the same or different vendors. |

| Customer | Customer’s known financial profile or stated business activity does not align with the scale or frequency of precious commodity acquisitions. |

| Customer | Customer is associated with registered addresses or counterparties in jurisdictions with limited precious metals regulatory oversight. |

| Customer | Customer applies for a commodity-backed loan without adequate documentation supporting lawful acquisition of the pledged commodity. |

| Customer | Customer or associated company appears in adverse media or open-source intelligence (OSINT) databases in connection with smuggling, organised crime, or sanctions. |

| Transaction | Invoices or shipping documents classify precious metals or gemstones as lower-value materials or omit the commodity type, weight, or purity. |

| Transaction | Declared transaction value is materially inconsistent with prevailing market rates for the stated commodity specification. |

| Transaction | Ownership structure of the commodity changes through rapid sequential sales, purchase immediately followed by resale, without definite commercial rationale. |

| Transaction | Physical commodity holdings are rapidly converted into cash or liquid assets shortly after acquisition without documented commercial rationale. |

| Transaction | Payment for high-value commodity transactions received from third parties unconnected to the declared buyer or transaction purpose. |

| Geographic | Precious commodity purchase is immediately followed by international travel to a jurisdiction with limited AML/CFT frameworks for precious metals trade. |

| Geographic | Counterparty, supplier, or recipient is located at or associated with a Conflict-Affected and High-Risk Areas (CAHRA) region. |

| Geographic | Commodity routed through multiple intermediary jurisdictions before destination, inconsistent with the direct trade route for a legitimate transaction. |

| Product | Commodity arrives without verifiable chain of custody, responsible sourcing certification, or supplier due diligence documentation. |

| Product | Storage in offshore vaults or safe deposit boxes inconsistent with the customer’s declared commercial activity. |

| Channel | Transactions structured across multiple DPMS vendors so that no single entity observes the full value of purchases. |

| Channel | Letter of credit used where the underlying trade documentation misrepresents the commodity type or value. |

Which Controls Disrupt Precious Commodity Smuggling?

Summary: Effective controls combine risk-based CDD and EDD, source-of-funds verification, responsible-sourcing due diligence, sanctions screening, and timely STR and DPMSR reporting.

| Control | What It Disrupts | Type | Limitation |

| Enhanced Due Diligence (EDD) | Obscured beneficial ownership and false business profiles | Detects | EDD is only as effective as information gathered; sophisticated false documentation may defeat it. |

| Risk-Based Customer Profiling | Unrestricted access by high-risk customers | Prevents (entry stage) | Profiling depends on data quality at onboarding; post-onboarding risk changes may not be captured. |

| Trade Monitoring | Document manipulation and under/over-invoicing | Detects | Requires live commodity price data feeds; without benchmarks, invoice comparison cannot be automated. |

| Transaction Monitoring | Structuring and rapid conversion patterns | Detects | Effective only if transaction data is captured across multiple sessions; cash-only vendors generate no monitorable data. |

| Information Sharing and Collaboration | Information asymmetry across DPMS vendors, customs, and FIU | Detects (cross-sector) | Formal sharing frameworks between DPMS and customs are not yet standardised in all jurisdictions. |

How Do AI and RegTech Automate Detection of Precious Commodity Smuggling?

Summary: AI and RegTech tools automate transaction monitoring, network and graph analytics, sanctions screening, and document verification to surface smuggling patterns at scale.

Transaction monitoring systems configured with precious commodity typology rules can identify threshold structuring, rapid conversion patterns, and counterparty irregularities in real time. Rules calibrated to the AED 55,000 DPMSR threshold can flag cash purchase sequences where multiple transactions aggregate near or above that value within a defined observation window.

Network analytics and graph-based relationship mapping trace connections between customers, counterparties, suppliers, and shell entities, revealing ownership paths that manual CDD reviews may miss. A shell company with undisclosed beneficial ownership linked to a conflict-affected jurisdiction can be flagged automatically when graph analytics identify the connection.

Natural language processing applied to trade documentation can extract commodity descriptions, purity grades, and declared values from invoices and compare them against commodity market databases. Discrepancies between declared values and live market rates trigger a document review alert without requiring a compliance officer to perform the comparison manually.

OSINT platforms aggregate adverse media, customs enforcement records, sanctions lists, and conflict-zone risk databases into scoring models. Machine learning anomaly detection identifies deviations from expected transaction patterns for peer groups of DPMS customers with similar profiles.

What Data Should Compliance Teams Collect to Detect Precious Commodity Smuggling?

Summary: Teams should capture customer and beneficial-owner identity, source of funds and wealth, transaction and shipment detail, provenance records, and counterpart geography.

| Data Point | Source System | What It Reveals |

| Commodity market price benchmarks | London Bullion Market Association (LBMA) price feeds, or others depending on the trade corridors | Enables immediate comparison of declared invoice values against live market rates to identify under/over-invoicing. |

| DPMS transaction history | Core transaction log or point of sale system | Reveals structuring patterns, threshold avoidance, and rapid conversion behaviour across multiple sessions. |

| Customs and import/export declarations | Border agency records (via formal information-sharing) | Identifies discrepancies between declared commodity type/value at border and documentation at DPMS entity. |

| Customer and counterparty jurisdictional risk scores | Geographical risk database (FATF lists, EOCN country data) | Flags transactions involving parties in CAHRA regions, secrecy jurisdictions, or FATF grey/black-listed countries. |

| KYC records including Beneficial Ownership (BO) documentation | KYC and CDD platform | Supports completeness check required by CR 134/2025 Articles 9 and 10 (customer and beneficial owner identification); identifies gaps indicating deliberate opacity. |

| Loan agreements and collateral documentation | Lending and credit facility records | Detects commodity backed loan structures used to extract value without generating a sale record. |

| OSINT and sanctions database results | OSINT platform, Notification Alert System (NAS), sanctions screening engine | Identifies customer or counterparty connections to organised crime, CAHRA sourcing, or Targeted Financial Sanctions listed entities. |

| Safe deposit box and vault access records | Safe deposit facility or freeport access log | Detects commodity storage patterns inconsistent with the customer’s declared commercial activity. |

| Trade documentation (invoices, bills of lading) | Trade finance or documentary review system | Source of over/under-invoicing evidence; reveals false classification of commodity type. |

| goAML DPMSR and STR filing history | goAML reporting system | Cross-references declared transactions against filed reports; identifies gaps in mandatory reporting obligations. |

How Does Precious Commodity Smuggling Aggravate Jurisdictional Risk and Product Risk?

Summary: Smuggling raises jurisdictional risk through exposure to high-risk and conflict-affected regions, and product risk through the inherent liquidity and anonymity of precious commodities.

Precious commodities significantly increase Product Risk because the characteristics make them inherently difficult to subject to standard AML controls. Commodities can undergo physical transformation achievable through refining, recutting, or alloying, which permanently detaches the evidential link to the commodity’s origin.

Jurisdictional Risk is elevated because precious commodity smuggling schemes deliberately exploit divergences in regulatory stringency between source, transit, and destination jurisdictions. A gold shipment that originates in a CAHRA region, transits through a country with minimal precious metals customs controls, and enters a major trading hub benefits from the progressive erosion of provenance information at each border.

What Observable Patterns Signal Precious Commodity Smuggling During Transaction Monitoring?

Summary: Monitoring should flag rapid buy-and-resell cycles, threshold-avoiding structuring, mismatches between declared value and shipment, and dealings tied to high-risk corridors.

A compliance officer reviewing a customer file or transaction records for this typology should look for the following observable patterns.

Multiple cash transactions conducted within days or weeks, each structured below the AED 55,000 threshold, cumulatively amounting to a significant aggregate value, signal deliberate avoidance of DPMSR reporting obligations.

A pattern where a customer presents large sums of cash for gold or diamond purchases without accompanying documentation about the source of those funds, and without a verifiable business purpose.

Invoices presented for commodity purchases that describe the goods in vague or incorrect terms: omission of purity or weight specifications, declaration of value materially below the market rate for the commodity, indicate that documentation has been prepared to conceal value rather than describe it.

Loan facilities secured against precious commodity holdings, particularly where the commodity was recently acquired with cash, may indicate an attempt to convert illiquid holdings into liquid funds without generating a direct sale record.

Sectors at Highest Exposure

| Sector | Risk Rating | Reasoning |

| Dealers in Precious Metals and Stones (DPMS) | Critical | Primary direct exposure; processes the transaction for acquisition and introduction into legitimate trade. |

| Gold Refineries | Critical | The processing stage that destroys traceability of illicit-origin gold. |

| Commercial Banks and Trade Finance Providers | High | Issues Finance letters of credit and commodity-backed loans exposes TBML risks from under/over-invoiced trade documentation. |

| Freight Forwarding and Logistics | High | Physical transport of commodity; documentary manipulation and mislabelling occur at this node. |

| Free Zone Entities | Moderate | Storage and transit of commodity through UAE free zones, which historically have had variable oversight intensity. |

Best Practices for Precious Commodity Smuggling Risk Management

Summary: Leading practice pairs an enterprise-wide risk assessment with responsible-sourcing due diligence, robust CDD and EDD, sanctions screening, staff training, and five-year record retention.

- DPMS entities must identify and assess risk across customer, supply chain, delivery channels, product type, jurisdiction exposure, and delivery channel, and implement a documented and proportionate risk-based approach to mitigate ML/TF/PF risk.

- Gold refiners must implement the five-step responsible sourcing framework for supply chain participants. Gold refineries and supply chain participants must comply with the requirements of due diligence on each supply of gold, a supply chain policy, identification of CAHRA risk, and an independent third-party audit.

- Entities should adopt risk-based commodity price checks against recognised market benchmarks, especially for high-value, unusual, cross-border, or CAHRA-linked transactions. A risk-based market-rate comparison, checking the declared or invoice value against a recognised benchmark, disrupts the under-invoicing mechanism that TBML schemes depend on.

- Apply EDD and senior management approval on all customers presenting large-volume cash transactions, multi-jurisdictional profiles, or CAHRA-linked supply chains. EDD must establish the source of funds, the source of wealth, and the specific business rationale for each transaction.

- Subscribe to and screen against the NAS operated by EOCN. Sanctions screening must be applied to all customers, counterparties, beneficial owners, and associated parties, regardless of transaction value. Failure to subscribe to NAS carries a maximum administrative penalty of AED 1,000,000 under Cabinet Resolution No. (71) of 2024.

- Customise transaction monitoring rules to detect structuring below the AED 55,000 threshold. The rule should aggregate cash purchases by customer across a rolling 30-day window and flag when the cumulative value approaches or exceeds AED 55,000, even if no single transaction triggered it.

- Verify the chain of custody and certificate of origin for all incoming commodity shipments. Trade documentation review must confirm that the declared origin of the commodity is consistent with the supplier’s geographic profile and due diligence records. Documentation that lacks a certificate of origin should trigger EDD on the supplier.

- File an STR without delay when suspicion arises, regardless of whether a transaction has been completed. The obligation to file arises on suspicion, not on certainty, per FDL 10/2025 Article 18.

- Maintain a five-year retention record of CDD documentation, transaction records, accurate goAML records, including all DPMSR, STR, and SAR filings, per Article 25 of CR 134/2025.

How Precious Commodity Smuggling and Commodity Smuggling Are Related

Summary: Precious commodity smuggling is a high-value subset of commodity smuggling, sharing concealment and trade-misinvoicing techniques but carrying far greater value density.

Precious commodity smuggling is a variant within the broader typology of Commodity Smuggling.

Commodity Smuggling is the practice of physically moving any goods, such as electronics, tobacco, or pharmaceuticals, across borders without lawful declaration to evade duties, circumvent trade controls, or transfer criminal value. The distinguishing factor between the two is that precious metals and stones carry an enormous amount of money in a very small, lightweight package, while having a consistent global trade value, something that simply isn’t possible with any other kind of commodity.

The compliance officer should vigilantly monitor large-volume freight, as the two typologies can operate simultaneously, and precious commodities may be concealed within bulk shipments of other commodities.

Related Terms

| Term | Connection |

| Commodity Smuggling | Parent typology; the broader category within which precious commodity smuggling operates as a specialised sub-method. |

| Trade-Based Money Laundering (TBML) | Overlapping technique; under/over-invoicing and false commodity classification are TBML methods employed within precious commodity smuggling schemes. |

| Shell Companies | Enabling structure; shell companies are used to acquire, hold, and sell smuggled commodity, obscuring the beneficial owner at each stage. |

| Layering | ML stage; precious commodity smuggling is predominantly a layering mechanism, converting cash to a portable physical asset and moving it across jurisdictions. |

| Enhanced Due Diligence (EDD) | Primary control; EDD is the mandatory response when a customer or transaction presents indicators associated with this typology. |

| Dealers in Precious Metals and Stones (DPMS) | Regulated sector; DPMS entities are the direct regulated entities at which the commodity enters the legitimate trade chain. |

| goAML | Reporting platform; the mandatory platform for DPMSR, STR, and SAR filing for all UAE regulated entities. |

| Suspicious Transaction Report (STR) | Compliance obligation; the report that must be filed without delay when precious commodity smuggling indicators are identified. |

| Conflict-Affected and High-Risk Areas (CAHRA) | Geographic risk concept; CAHRA designation is the primary risk trigger for supply chain due diligence on gold sourcing. |

| Beneficial Ownership | CDD target; identifying the true beneficial owner of shell companies used in commodity smuggling schemes. |

What Financial Instruments Do Criminals Use in Precious Commodity Smuggling Schemes?

Summary: Beyond cash, schemes rely on cash equivalents such as cashier’s cheques and money orders, trade finance, and informal value transfer to move and legitimise proceeds.

Jewellery is a uniquely versatile instrument in money laundering because it serves simultaneously as a transport vehicle for moving value across borders and as an entry point into the legitimate economy. Criminal proceeds are used to purchase gold jewellery or gem-set pieces, physically carried as personal items and later sold to dealers, pawnbrokers, or retail consumers, generating a receipt that is indistinguishable on paper from legitimate personal asset disposal.

Precious metals and gemstones in raw or semi-processed form, including gold bars, gold grain, rough diamonds, cut gemstones, and silver bullion, are the primary instruments in wholesale and industrial-scale smuggling schemes. These commodities can be processed in three different ways to generate legal value: provided to refineries for melting and recasting to destroy traceability, traded on commodity exchanges at market price for documented lawful proceeds, or used as collateral against credit facilities through the banking system into legitimate financial transactions.

Variants and Synonyms

| Term | Context or Jurisdiction | Distinction |

| Gold Smuggling | Global; most common variant in enforcement literature | Restricts the typology to gold specifically; the primary term covers all precious metals and gemstones. |

| Conflict Mineral Smuggling | CAHRA-focused regulatory contexts; OECD; African Union | Emphasises the connection to armed conflict and revenue generation for terrorist or criminal groups. |

| Gemstone Trafficking | Enforcement contexts involving diamonds, rubies, emeralds | Focuses on cut or rough gemstones rather than metals; common in East and Southern African enforcement cases. |

| Precious Metals TBML | Financial intelligence and FATF typology reports | Focuses specifically on the invoicing manipulation dimension of the broader smuggling typology. |

| Illicit PMS Trade | UAE UAEFIU and MoET supervisory communications | Regulatory shorthand used in UAE enforcement notices; equivalent in scope to the primary term. |

What Products and Services Do Criminals Abuse in Precious Commodity Smuggling Schemes?

Summary: Refining, jewellery retail, free-zone trading, safe-deposit and consignment services, and trade-finance facilities are the products and services most exposed to abuse.

Freight forwarding and shipping services are abused at the transportation level. Criminal networks build relationships with customs brokers, airline cargo handlers, and port authorities to arrange commodity shipment by preparing cargo manifests and bills of lading that describe the shipments in terms to avoid commodity-specific customs declarations.

Letters of credit are bank-issued payment guarantees that underpin international commodity trade; criminals exploit them by smuggling commodities through the same mechanism, presenting clean shipping documents to the bank that has no visibility into whether the declared value is genuine. Transforming the physically smuggled commodity into a bank-financed, fully documented trade transaction.

Commodity brokers, bullion dealers, and exchange-traded commodity platforms are abused at the integration stage when they purchase precious commodities from sellers who cannot verify legitimate acquisition. A dealer who fails to establish a chain of custody and source of funds effectively completes the laundering process by converting illegal physical assets into clean market proceeds. UAE-registered precious metals trading firms are regulated DNFBPs and are obligated under Cabinet Resolution No. (134) of 2025 to apply customer due diligence to covered transactions and enhanced due diligence where higher-risk indicators arise, treating an unverified source as a primary indicator of illicit origin.

How AML UAE Helps

The regulatory governing principles are substantially sound. The gap lies in detection. Compliance officers may not always identify the relevant indicators or know the appropriate action to take.

AML UAE’s compliance resources are purpose-built to close this detection gap. Our team brings a deep understanding of the UAE regulatory framework and international AML standards, supporting entity employees and senior management in identifying red flags and control gaps, building structural controls to detect precious commodity smuggling, and delivering staff training on commodity-specific red flags and indicators.

We provide UAE-registered entities with Enterprise-wide risk assessment development, incorporating sector-specific typology intelligence, alongside comprehensive CDD and EDD procedure frameworks tailored to the nature and scale of the business.

To meet the STR obligations under FDL 10/2025, AML UAE provides dedicated guidance on goAML registration, DPMSR filing, form completion, and filing protocols, ensuring reporting obligations are met accurately and without procedural delay.

“Over the last 28 years, I have worked with many dealers in precious metals and stones across the UAE. One pattern stands out consistently: the documentation often appears complete on its face. The real scrutiny lies in reconciling commodity values against recognised benchmarks, identifying linked transactions, and verifying the chain of custody beyond the immediate seller. If those checks create unresolved suspicion, the goAML reporting obligation must be considered without delay.”

Pathik Shah - CAMS, FCA, CISA | Founder and Principal Consultant, NIYEAHMA Consultants LLP

Frequently Asked Questions

Precious commodity smuggling involves the physical, undeclared movement of high-value goods across borders. Trade-based money laundering uses legitimate trade documentation to manipulate declared values or misrepresent goods. The two typologies overlap when a smuggled commodity is documented through false invoices, but smuggling can also occur without any trade documentation at all, for example, when a courier carries undeclared gold in personal luggage.

All DPMS entities registered to conduct business in the UAE and engaged in cash or wire transfer transactions in precious metals, gemstones, or jewellery at or above AED 55,000 (single or linked) are subject to full AML/CFT obligations under Cabinet Resolution No. (134) of 2025 Article 3(3).

A DPMSR (Dealers in Precious Metals and Stones Report) is the mandatory goAML report type for DPMS threshold transactions. It must be filed for all cash transactions at or above AED 55,000, and for wire transfers at the same threshold where the counterparty is an entity rather than an individual.

The AED 55,000 threshold applies to both single transactions and linked transactions that, individually below the threshold, together constitute a transaction of or above that amount. Cash-equivalent instruments, including cashier’s cheques, bearer bonds, and money orders, are treated as cash for threshold purposes.

Yes. Sanctions screening obligations are not threshold dependent. All customers, counterparties, beneficial owners, and related parties must be screened against the UAE Sanctions Lists, UN Consolidated Lists, and all applicable TFS databases regardless of transaction value. The AED 55,000 DPMSR threshold affects reporting obligations only, not the obligation to screen.

Cabinet Resolution No. (71) of 2024 prescribes maximum administrative penalties of AED 500,000 for EDD failures (Violations 15-17). MoET may also issue written warnings, suspend licences, and refer cases for criminal prosecution under Federal Decree-Law No. (10) of 2025.

The five-step framework under MOE Due Diligence Regulations Version 9, made legally binding by Ministerial Decree No. (68) of 2024 requires gold refineries and supply chain participants to establish supply chain governance, identify and assess supply chain risks, manage those risks, commission an independent third-party audit, and submit an annual due diligence report.

An STR must be filed without delay via goAML. The compliance officer must not tip off the customer or any associated party about the suspicion or the filing. If the customer matches a TFS designation, an immediate freeze must be implemented and a Confirmed Name Match Report filed with EOCN. All relevant documentation must be retained for a minimum of five years.

The EOCN TFS Strategic Review of Case Studies (2021) documented a pattern in which gold sourced from conflict-affected regions was routed through intermediary countries into UAE refineries, with proceeds transferred to designated terrorist organisations. Gold smuggling is therefore relevant not only to money laundering compliance but also to TFS screening and PF risk assessments.

According to the UAEFIU DPMS Strategic Analysis Report (October 2025), the leading reasons for reporting in the DPMS sector over the period July 2021 to June 2025 were negative media coverage (14%), lack of appropriate documentation (13%), incomplete or missing file documentation (11%), TFS suspicion (10%), and sanctions list inclusion (10%).

Closing Summary

Precious commodity smuggling is a well-documented layering stage typology that exploits the physical and financial properties of high-value goods to transfer criminal value across borders without generating a banking record. The UAE’s position as one of the world’s largest gold trading hubs means that DPMS entities, refineries, and trade finance providers face meaningful operational and compliance exposure to this typology.

The most actionable response is the implementation of specific controls: risk-based market-rate invoice comparison, CAHRA-focused supply chain due diligence, complete DPMSR filing, and enhanced due diligence on all cash-intensive or multi-jurisdictional commodity transactions.

The UAE’s updated AML/CFT framework accommodates all these practices under FDL 10/2025, requiring all entities to include sector-specific risk assessment and development of internal policies and procedures through which the typology usage could be identified and dealt with. The current UAE regulatory framework leaves limited tolerance for material control gaps.

If your institution is exposed to this typology and the procedures are not reviewed under the current FDL 10/2025 and CR 134/2025 framework, the entity and responsible persons may face regulatory findings, administrative penalties under CR 71/2024, and remediation directions. Addressing those gaps now reduces that exposure. AML UAE is available to support the assessment, remediation and ongoing monitoring processes your institution needs to manage the risk within the law.

Want to Strengthen Your Financial Crime Controls?

Our experts can help you identify and mitigate risks linked to precious commodity smuggling.

Share via :

About the Author

Pathik Shah

FCA, CAMS, CISA, CS, DISA (ICAI), FAFP (ICAI)

Pathik is an ACAMS-certified AML consultant specialising in governance, risk, and compliance for regulated entities in the UAE. He brings over 28 years of experience, with 1,000+ hours of AML training and 200+ advisory engagements across DNFBPs, VASPs, and FIs. He supports businesses in aligning with AML/CFT requirements from the CBUAE, DFSA, MoET, MoJ, VARA, CMA, FSRA, and FATF. Known for translating complex regulations into audit-ready procedures, Pathik enables operational clarity and compliance readiness.

Reach Out to Pathik