Risk-Based Approach For Dealers in Precious Metals and Stones (DPMS)

Protect your business with reliable and effective AML strategies with AML UAE.

Risk-Based approach for Dealers in Precious Metals and Stones (DPMS)

The importance of the Risk-based approach for Dealers in Precious Metals and Stones (DPMS) is understood from the nature of the business itself. Jewellers deal in precious metals, stones, jewellery, and by their nature, these items carry high value, and can be easily transported.

Unless a risk-based approach is applied in the jewelry business, it becomes too difficult for the DPMS to comply with the legal requirements of anti-money laundering law in the UAE.

How should DPMS assess the risks involved?

Therefore, you must assess the risks associated with all your business activities and services. Here are the four primary areas that you need to address while performing while determining your risk.

- Geography of the potential clients.

- Business relationships and the clients of your potential customer.

- Products, services, and delivery channels.

- Other relevant factors.

In order to do so, you must consider the nature and behavior of your clients, the products or services you deliver, and the ways or mediums in which you provide your offerings. However, if you identify any of the

situations that suspect unusual or illicit activities, you should instantly control these risks by implementing all the probable mitigation measures.

Read more about AML Compliance Requirements for jewellery business in UAE

What is a risk-based approach cycle?

- Identifying the inherent risks of your company

- Creating risk-reduction or mitigation measures and critical controls

- Efficient implementation of your risk-based approach

- Reviewing your applied risk-based approach

- Business-Based Risk Assessment

- Relationship-Based Risk Assessment

Business-based risk approach

1- Product and delivery channel

- Buying precious metals, stones, and precious jewels

- Sale of precious metals, stones, and precious jewels

- Indirect transactions with unknown clients. These could take place through the internet, mail, or a telephone.

- Assess your products as per the type of market you are operating into, along with the kind of clients they are curated for.

- Assessing the physical characteristics of your jewellery items is also a critical aspect that you must watch out for. Portability, value, storage options, etc., are considered as the physical characteristics of the products.

- The jewellery products which are lesser in value usually aren’t subject to significant risks.

- Determining the modes of communication with your client also has a role to play: face-to-face communication or any form of virtual communication that occurs through the mail, telephone, or video conferencing.

- Considering the mode of delivering your jewellery items is also crucial and should be thoroughly monitored. Needless to say, the mode of the transaction should also be observed.

Here are a few examples of potentially high-risk products if you are a DPMS.

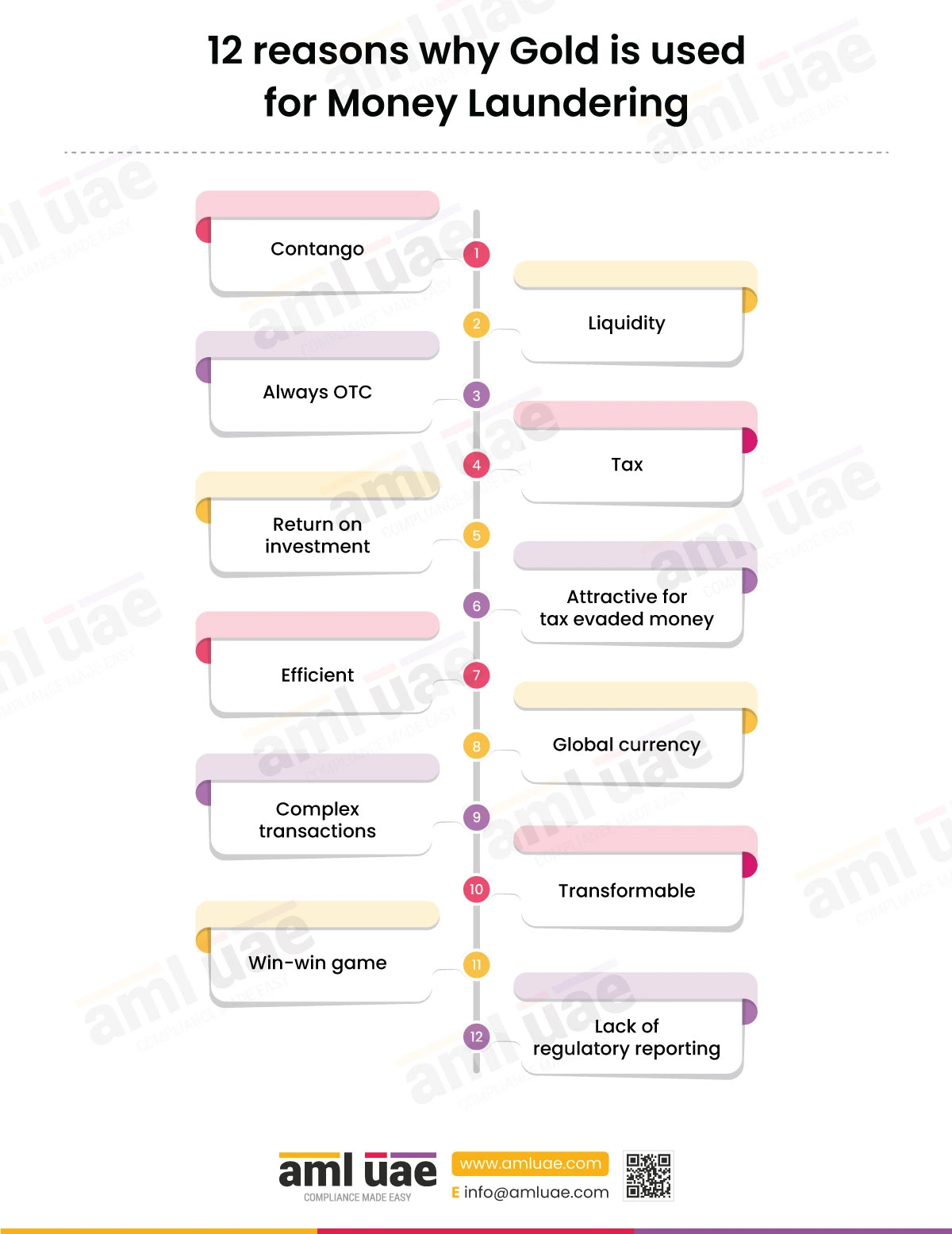

Gold

Gold is undoubtedly a high-risk product because it is transformable, exchangeable, and potentially provides secrecy in the transactions. In addition to that, gold has a universal price standard, and it can be used as a currency.

Here are a few red flags associated with the trading of gold.

- An existing customer buying substantial quantities of gold bullion without any legitimate or explainable reason, or a potentially new customer asking for converting vast amounts of gold into bullion.

- An existing or potential buyer purchases a massive quality of gold and makes the payment in cash.

- Any known or unknown foreign national buying vast quantities of gold bullion in a relatively short span.

- The purity, weight, value, and origin of gold are misclassified misleading on the custom declaration forms.

- Unlicensed individuals or companies producing and commercializing gold.

- Gold bullion does not meet the industry quality standards.

- Higher gold prices as compared to the local markets.

Diamonds

Here are a few red flags associated with the trading of Diamonds.

- A customer is buying diamonds in bulk without having logically explainable or reasonable reasons. The trading of diamonds could be illogical both economically and from a business point of view.

- Trading of diamonds whose origin is quite suspicious. This is particularly the case with raw diamonds, which are not accompanied by legitimate Kimberley process certificates.

- A Kimberley process certificate that comes with an exceptionally long validity or is forged.

- A supplier or customer who is known for trafficking conflict diamonds.

- A customer or a supplier who is unaware of the best trade practices or the one who seeks help from third parties before finalizing a transaction.

- Bulk trading of diamonds and the payment is made in cash from the geographical locations where such transactions are unusual.

- Any customer who requests to purchase polished diamonds in bulk without any logical reasons.

Compliance. Trust. Transparancy

Customized and cost-effective AML compliance services to support your business always

Behavior of counter parties in some transaction

- Any counterparty that proposes any unusual transaction which is entirely insensible and baseless or the transactions that are pretty high veiled or include high potential profits.

- Any counterparty who leverages the power of non-banking financial institutions and money service business for no logical and legitimate business reason.

- Any counterparty that frequently changes bank accounts, especially when on foreign land.

- Any counterparty seeks secrecy by conducting ordinary business transactions with the help of lawyers, accountants, or any other intermediary.

Various other indicators of High Risk

- A supplier who is not willing to provide accurate or complete contact information, business affiliations, and financial references.

- Offering loose diamonds in bulk which retains their wholesale value because they can be easily liquidated.

- Offering risky stones like diamonds through indirect means and to clients whom you haven’t been in direct touch with. These types of transactions are hazardous.

2- Geography

When you assess your geography, you have to consider whether the geographic locations in which you operate or your clients are based out possess high risks of money laundering activities or terrorist financing. Depending upon the operations of your business, this can range from your immediate surrounding to a province or a territory.

Here are a few examples of geographic elements that are required in your risk assessment.

- Locations that experience a considerably higher crime rate may lead to the enhanced potential risk of money laundering or terrorist financing.

- A rural area where the customers are known to you could present a lesser risk as compared to an urban area where new and anonymous clients are more likely to bring significant risks involved with them.

- Is your company closely located near a border crossing? If yes, it could elevate the risks involved because your company can be the first entry into the enormous financial systems.

- If your potential clients are located in countries subject to sanctions or embargoes, you must consider their high risks.

Compliance. Trust. Transparancy

Customized and cost-effective AML compliance services to support your business always

Various other factors relevant to your company, if applicable

- The product you are offering and the channel of delivering you are opting for.

- The geographical location of either your existing or potential client.

- The characteristics of your clients.

- The financial activities and transactional patterns of your clients.

Here are a few examples of the characteristics of your clients that you might consider as high-risk.

- A client who is not at all disturbed or concerned about the price.

- A client who makes the payment for expensive jewelry in cash.

- A client who tries to use a third-party credit card or a cheque.

- A client buying precious metals or stones without having any legitimate interest in the value, size, or color.

- A client who has unexplainable distance from the offerer or you in this case. A client who orders precious items in bulk makes payment in cash, cancels the order, and gets the refund, preferably through cheque.

- A client who is not willing to share adequate and accurate amounts of information.

- Transactions that look structured in order to avoid reporting requirements.

- Any transactions that involve third parties, either as payers, or recipients of payment, without apparent logical purpose.

- Use non-bank financial mechanisms, like currency exchange or money remitters, instead of a legitimate banking system.

- Any kind of unusual payment methods, like large amounts of cash, multiple numbers of money orders, cashier’s cheque, traveler’s cheque, or any type of payment from third parties.

- Funds that come from an offshore financial center instead of a local bank.

- There are multiple affiliated entities in the payments chain.

Final words

Dealers in precious metals and stones are already more prone to dramatic risks. But it is essential to apply a risk-based approach in the same. The entire process is quite challenging and needs expert advice and help, and this is when AML UAE comes into the picture to provide its expert AML Consultancy Services.

Frequently Asked Questions (FAQs)

Here are a few frequently asked questions.

Which all types of risks should be assessed in order to carry out risk profiling for DPMS?

- Product, service, and transaction-related risk

- Supply channel-related risks

- Geographical risk

- Client-based risk

How to handle customers while conducting the KYC and due diligence process?

The entire industry is prone to high risks. In order to keep yourself safe from reputational losses and regulatory penalties, you have to follow a few things deliberately.

- Ask your clients to fill up a KYC form and submit legally authorized documents to verify the details provided.

- You must also check the name of the purchaser in sanction lists, PEPs list, or adverse media reports details.

- Verify the details, and if any suspicious activity is diagnosed, you must immediately follow an enhanced due diligence process.

- If you suspect any type of money laundering or terrorist financing, you

must immediately file a STR.

The entire process can be pretty time-consuming, and your clients might

feel frustrated. However, there are a few things you can do in order to engage with them while all other essential aspects are being carried out.

- Offer some refreshments

- Engage the client by showing a video of your warehouse where the jewelry masterpieces are being designed and curated.

- Ask the client whether they would like some loyalty cards for future purchases.

Annex A: Business-based Risk Assessment

Here are the instructions in order to complete the business based risk-assessment which includes products, geography, delivery channels, and many other relevant factors.

AList of FactorsEffectively describe your products, factors

related to geographic locations, and delivery

channelsBRisk RatingThere are multiple risk factors, and all you have

to do is to rate all of your risk factors. Risk

factors include delivery channels, nature of

products & services, geographic locations, and many other relevant factors. It is important to note that you can have either a low or high-risk category or to have a legitimate complex rating scale. Moreover, the scale you develop should be established, tailored as per the size and

nature of your business.CRationaleWhenever you assign a risk rating to all the risk factors, it is important to provide a reason for that. Furthermore, if required, you can even

make a reference to a website, a report, or a

published paper.DDescribe Mitigation

Measures For High-Risk

FactorsAll the factors identified as high-risks should be

addressed with documented mitigation

measures. Written policies and procedures will make it easy for you to explain how you will reduce or control these risks in your daily activities.

Here are a few examples of mitigation

measures you might want to consider.

- Enhance your awareness of high-risk

situations in your company line across

your enterprise.

- Facilitate targeted training to staff regarding probable red flags and indicators of high-value, high-risk products such as diamonds or gold.

- Facilitate adequate controls for relatively higher-risk products like management

approvals.

- Enhance the overall frequency of

monitoring transactions that are associated with relatively high risks.

Annex B: Client relationship-based risk

assessment

Here are the instructions in order to complete the client relationship-based risk assessment:

AHigh-Risk Clients

or Business RelationshipsDetermine all your high-risk business

relationships and clients. You might want to assess risk each business relationship

individually or maybe in groups that share

almost the same characteristics.BRisk RatingYou must rate each of your business

relationships. You might use a scale of the

low, medium, or high in order to risk rate your

business relationships.CRationaleMention a reason why you assigned a

particular risk rating to each of your clients or business relationship.DDescribe Enhanced

Measures In Order To Determine The Identity of or Existence of High-

Risk ClientsDescribe how the identity was determined or how the existence of a high-risk entity for

each high-risk client or business relationship

was identified.

Here are a few examples.

- Seeking some additional information

beyond even the minimum requirements in order to ascertain the identity of the client.

- Get the independent verification of the gathered information.

- Establishing more strict and rigid

thresholds for ascertaining identification.

EDescribe Mitigation

Measures For High-Risk FactorsYou have to mitigate and control the risks of

each high-risk client or business relationship

you have identified.

Here are a few examples of mitigation

measures you might want to consider.

- Set limits to transaction amount in

specific situations.

- Ask about the source of funds in case of

- any cash payment.

- Conduct a few transactions only in

person.

FDescribe How Will

You Keep Client

Information Updated For High- Risks Business

Relationship And

ClientsYou are required to build policies on how and often you will update the information of the high-risk clients or business relationships. The

information that usually needs to be constantly updated includes the following.

- If the client is an individual, name,

address, contact number, and the occupation of that individual.

- If the client is a corporation, name,

address, and the name & address of the

directors of the corporation.

- If the client is an entity or something

more than a corporation, name, address, and the principal place of the

business.

Methods to keep client identification updated include asking the client to provide

information to confirm or update information

related to your identification.

GDescribe Enhanced

Monitoring For High-Risk Clients And Business

RelationshipsFor high-risk clients and business

relationships, you require to conduct

enhanced monitoring.

Here are the things that you need to keep in

mind when it comes to the enhanced monitoring process.

- What should be the frequency of the

enhanced monitoring?

- How is it conducted?

- How will it be reviewed?

Here are a few examples of how enhanced

monitoring is conducted and reviewed for

high-risk clients and business relationships.

- Ask for additional information like volume of assets, occupation, and

information available through public

databases.

- Review transactions on the basis of an approved schedule that includes

management sign-offs.

- Set business parameters or limits

related to transactions that would figure

out early warning signs.

- Try to review transactions more

frequently against any type of suspicious activities related to high-risk clients or business relationships.

Why is precious metal high risk?

What is Ghost shipping in AML?

How are precious metals traded?

Share via :

Add a comment

Related Blogs

About the Author

Pathik Shah

FCA, CAMS, CISA, CS, DISA (ICAI), FAFP (ICAI)

Pathik is an ACAMS-certified AML consultant specialising in governance, risk, and compliance for regulated entities in the UAE. He brings over 28 years of experience, with 1,000+ hours of AML training and 200+ advisory engagements across DNFBPs, VASPs, and FIs. He supports businesses in aligning with AML/CFT requirements from the CBUAE, DFSA, MoET, MoJ, VARA, CMA, FSRA, and FATF. Known for translating complex regulations into audit-ready procedures, Pathik enables operational clarity and compliance readiness.

Reach Out to Pathik