Document Forgery

Last Updated: 05/26/2026

Protect your business with reliable and effective AML strategies with AML UAE.

Document Forgery - Brief Overview

Falsifying identification documents, financial records, trade instruments, and legal documentation to conceal criminal origins or obscure beneficial ownership is known as Document Forgery. Regulated entities may face administrative penalties where they fail to apply required CDD, verification, recordkeeping, internal control, or reporting measures in response to forged or suspicious documentation.

Apply document verification controls, cross-reference findings against public registries, and submit an STR through the FIU’s electronic system where suspicion or reasonable grounds to suspect arise.

What is Document Forgery?

The fabrication, alteration, or counterfeiting of official documents, identity records, financial instruments, trade documentation, or legal instruments for the purpose of facilitating money laundering or concealing the origin of criminal proceeds is known as Document Forgery. As a concealment mechanism, it operates across all three stages of the money laundering cycle: enabling anonymous placement by bypassing identity verification controls, supporting layering by creating false audit trails, and providing the appearance of legitimate business activity during integration.

Document forgery is not a standalone typology, but a supporting technique deployed alongside other money laundering methods. Its effect is to undermine the integrity of the CDD and beneficial ownership identification processes that regulated entities depend on to detect criminal activity.

Regulatory Framework Related to Document Forgery

Federal Decree Law No. (10) of 2025 (FDL 10/2025) is the primary AML/CFT statute. Article 2 criminalises money laundering as an independent offence, while document falsification and fraud may constitute predicate offences generating criminal proceeds subject to ML criminalisation.

For legal professionals, the Ministry of Justice Guidebook for Law Firms (2nd Edition, 2026) provides guidance on verifying and corroborating client documentation against reliable or independent sources, where appropriate.

For auditors and accountants, the MoET Supplemental Guidance for Auditors Section 11.7.5 requires particular attention to document authenticity when approving financial instruments (including securities, bonds, title deeds, loan or mortgage documents, promissory notes, or other documents and information) involving legal entities.

Primary Authority or Supervisory Body

The Ministry of Justice (MoJ) supervises lawyers, notaries, and legal consultancy offices. The Ministry of Economy and Tourism (MoET) supervises accountants, auditors, real estate brokers, DPMS entities, and TCSPs.

The UAE FIU receives Suspicious Transaction Reports and other information submitted through its electronic system, and has identified professional money laundering as one of the highest ML threats in the UAE, encompassing scenarios in which professionals are exploited through document forgery.

Reporting or Compliance Obligations and Channels

Where the regulated entities identify forged, falsified, or unverifiable documentation, transactions, or onboarding processes, they can proceed in line with applicable customer due diligence obligations. CR 134/2025 Article 18 establishes suspicious transaction reporting obligations through the FIU’s electronic system or any other approved means (goAML in practice) on the basis of suspicion or reasonable grounds to suspect, regardless of transaction value.

Relevant recordkeeping obligations, including retention of document verification records, are addressed under CR 134/2025 Article 25.

What does Document Forgery Mean?

Think of it this way: a regulated entity’s entire compliance process rests on documents. The customer presents identification; the lawyer checks provenance records; the auditor reviews financial statements; the trade finance team examines shipping invoices. A skilled document forger replaces the truth at each of these checkpoints with a fabricated version. Once forged documents are accepted as genuine, the compliance system validates rather than detects the criminal activity. The fraud is the lock-pick; the document forgery is the key.

Why Document Forgery Matters

Document forgery is the enabler behind many of the most difficult money laundering cases to detect. Its effect is not to money laundering itself, but to disable the controls that would detect the laundering. A compliance officer who accepts a forged identity document has unknowingly confirmed a false identity. An auditor who approves accounts built on falsified invoices has provided external validation to a fraudulent financial record.

The MoET Supplemental Guidance for Auditors identifies five major ML/TF typology categories, two of which, concealment of beneficial ownership and concealment of illicit origin of funds, are directly dependent on document forgery as an enabling mechanism. Every shell company scheme, trade-based ML operation, and identity-substitution fraud uses forged documents at some point in the cycle.

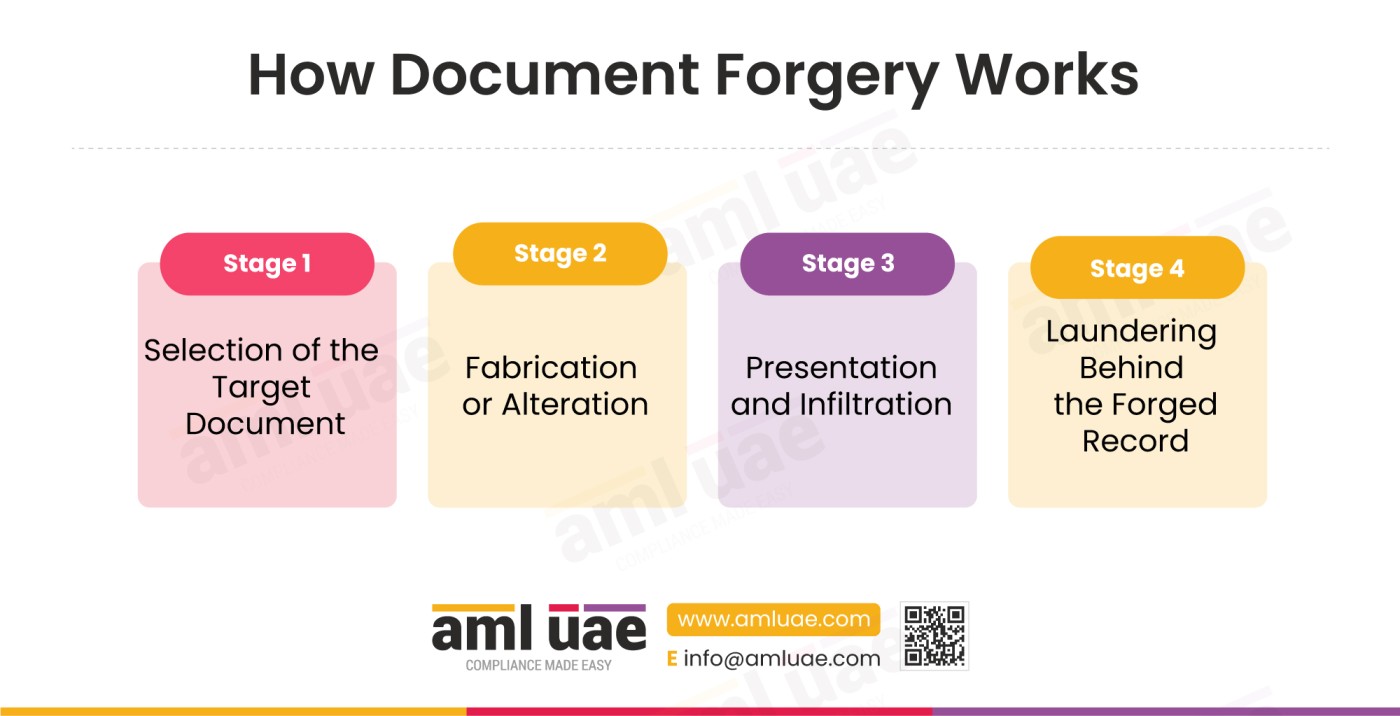

How Document Forgery Works

Document forgery operates as a support technique across the money laundering cycle. The document forger, legal professional, and professional money launderer each contribute at distinct stages.

Stage One: Selection of the Target Document

The criminal or their professional money launderer identifies which document type will disable the targeted compliance control. For KYC bypass, the target is identity documentation. For trade finance fraud, the target is trade documentation, including invoices and bills of lading. For beneficial ownership concealment, the target is corporate and legal documentation, including articles of association, shareholder registers, and trust deeds.

Stage Two: Fabrication or Alteration

A specialist document forger produces or modifies the target document. Fabrication creates a document with no genuine original, such as a passport for a fictitious identity or an invoice for goods never shipped. Alteration modifies a genuine document, changing a name, value, date, or security feature such as watermarks, holograms, or microprinting.

Stage Three: Presentation and Infiltration

The forged document is presented to a regulated entity as part of KYC onboarding, a financial transaction, a trade finance application, or a legal services engagement. The presenting party relies on the assumption that compliance teams will not conduct independent verification, or that the forgery is sophisticated enough to pass visual inspection.

Stage Four: Laundering Behind the Forged Record

Once accepted, the forged document becomes part of the institution’s CDD record. Subsequent compliance reviews reference that document as evidence that due diligence was completed. Criminal proceeds move through the financial system, using the false document as their apparent basis for legitimacy.

Real-World Examples of Document Forgery

Identity Fraud to Bypass KYC at Onboarding

A professional money launderer uses a forged passport to open a bank account in a fictitious name. The bank’s automated system checks document format but does not cross-reference the identity against external government databases. The account is opened. Criminal funds are deposited and withdrawn before a periodic review flags an inconsistency between the stated name and publicly available information.

Independent document verification using reliable third-party verification tools, or corroboration against available official or commercial sources, would have identified the inconsistency before account opening.

Forged Trade Documentation in a Cross-Border Scheme

An importer and exporter agree to over-invoice a shipment by a factor of three. The exporter issues invoices, bills of lading, and certificates of origin reflecting the inflated value. The trade finance provider advances funds without verifying declared values against commodity benchmarks. Excess proceeds are distributed to accounts controlled by both parties.

The MoET Supplemental Guidance for Auditors identifies trade-based ML as a primary typology category. A compliance team with commodity market pricing data would identify declared invoice values deviating materially from market rates as a red flag requiring escalation.

Falsified Corporate Records to Conceal Beneficial Ownership

A professional money launderer provides a law firm with articles of association, a shareholder register, and a board resolution listing nominee shareholders rather than the true beneficial owner. The law firm conducts the covered activity without independently verifying the corporate structure against the commercial registry.

The MoJ Guidebook for Law Firms (2026) includes guidance relating to beneficial ownership identification, including reference to the 25% ownership thresholds and use of reliable or independent sources for verification purposes.

What Are the Red Flags that Identify Document Forgery?

| Category | Red Flag |

| Customer | Identity documents appear to lack or have altered security features: missing holograms, incorrect watermarks, or inconsistent microprinting relative to the issuing authority’s known standards |

| Customer | Discrepancies in personal data exist between submitted documents and independently verified sources: name, address, date of birth, or document number format. |

| Customer | Customer is reluctant to consent to independent verification of identity or BO through external databases, commercial registries, or government records. |

| Customer | Repeated submission of documentation across multiple transactions shows consistent signs of tampering, suggesting systematic rather than accidental irregularities. |

| Customer | The customer cannot produce the original document for in-person inspection, offers only low-resolution images, or declines face-to-face verification without explanation. |

| Transaction | Bank statements, invoices, or transactional records display signs of tampering: erased figures, misaligned columns, inconsistent font types, or irregular spacing within a single document. |

| Transaction | Automated document verification checks fail due to anomalies in document design elements, mismatched security patterns, or barcode data that does not correspond to printed text. |

| Transaction | Financial records show round-figure amounts, unusually consistent payment intervals, or identical transaction descriptions, suggesting records were generated rather than recorded. |

| Transaction | An invoice or financial instrument presents a declared value materially inconsistent with prevailing market prices for the described goods, services, or assets. |

| Transaction | The same document number or reference code appears on documents presented by different counterparties, indicating mass production of forged instruments. |

| Geographic | Documents purportedly issued by authorities in jurisdictions with high document forgery prevalence or weak authentication infrastructure, particularly FATF grey or blacklist countries. |

| Geographic | Shipping or customs documentation describes cargo routes or jurisdictions inconsistent with the declared goods type, quantity, or commercial logic of the transaction. |

| Product | Corporate documents contain formatting irregularities or inconsistent fonts that do not match standard templates issued by the relevant company registration authority. |

| Product | Authenticity certificates or professional opinions bear the signature or credentials of an issuing authority that cannot be independently verified. |

| Channel | Document preparation or notary services are used in a jurisdiction where verification of the issuing authority is difficult, without an apparent commercial reason. |

| Channel | Documents are transmitted through informal channels or unverified third parties rather than directly from the issuing authority. |

| Channel | Legal advisory or accounting services are used to prepare documentation packages on behalf of a customer who cannot explain the underlying business rationale. |

Key Controls to Mitigate Document Forgery Risk

| Control | What It Disrupts | Detects/Prevents/Deters | Limitation |

| Customer Due Diligence (CDD) | Identity substitution and false BO presentation by requiring verification through reliable, independent sources | Detects | Depends on the quality of verification sources; CDD relying solely on client-supplied documents is insufficient. |

| Enhanced Due Diligence (EDD) | Document forgery in high-risk scenarios requires additional verification and senior management approval. | Detects | Applies after high-risk classification; initial forgery often occurs at the standard CDD stage. |

| OSINT and External Source Verification | False identity and BO claims by cross-referencing against public registries, government databases, and adverse media | Detects | Coverage varies by jurisdiction; data quality in high-risk countries is often limited. |

| Employee Background Screening | Internal facilitation by ensuring staff with document access are verified and free from conflicts of interest | Deters | Addresses internal threat only; does not prevent external presentation of forged documents |

| Staff AML Training and Awareness | Front-line acceptance of forged documents by ensuring staff can identify visual indicators of tampering | Deters | Insufficient for high-quality forgeries; visual inspection must be supplemented by technology. |

| Trade Monitoring | Trade document forgery by comparing declared values against commodity benchmarks and known patterns | Detects | Requires commodity price data access; limited for complex multi-leg transactions |

How Do AI and RegTech Automate Detection of Document Forgery?

Computer vision and OCR platforms analyse document images at the pixel level, detecting inconsistencies in font rendering, alignment, colour profiles, and security feature placement invisible to human reviewers. These systems compare submitted documents against databases of genuine document templates from issuing authorities worldwide, flagging deviations in layout, typography, or security feature positioning. A forged passport that passes visual inspection may fail a computer vision check within seconds.

NLP tools applied to textual document analysis identify semantic inconsistencies: amounts in figures that do not match amounts in words; logically inconsistent dates; address formats that do not conform to the declared jurisdiction’s conventions. These tools also detect repetition patterns in mass-produced invoices with identical descriptions or sequential document numbers indicating batch fabrication.

Blockchain-based document provenance systems, where issuing authorities record document hashes at issuance, enable regulated entities to verify authenticity by comparing the presented document’s hash against the authority’s immutable record. This technology is increasingly adopted in trade finance, where bill of lading and letter of credit forgery is a significant fraud risk.

Machine learning models trained on historical document fraud datasets identify anomalous structural characteristics across CDD document portfolios, escalating customer files for manual review and potential STR assessment.

What Data Should Compliance Teams Collect to Detect Document Forgery?

| Data Point | Source System | What It Reveals |

| Company and BO registry records | UAE commercial registry, MOET, free zone registrars | Whether corporate documents submitted accurately reflect the registered ownership structure |

| Contractual and invoice data | Contract management and accounts payable systems | Whether declared transaction values, payment terms, and counterparty details are internally consistent. |

| Customs and border records | UAE Federal Customs Authority and port authority records | Whether declared cargo descriptions, values, and routes on trade documents match actual import/export records |

| Document management system records | Internal document management and CDD platforms | History of all documents submitted, enabling pattern detection across multiple transactions |

| Document verification results | KYC platform and document verification services | Automated verification outcomes and exception records indicating document anomalies |

| Individual, entity, and public records databases | External intelligence databases, commercial registries, government records | Whether identity claims in submitted documents can be corroborated against independent sources |

| KYC and CDD records | KYC platform and client onboarding system | Complete CDD file including all documents submitted, verification methods applied, and inconsistencies noted |

| Legal documentation and records | Legal records management systems and external legal registries | Whether trust deeds, powers of attorney, and corporate resolutions match records at issuing authorities |

| Trade documentation | Freight management systems, shipping invoices, trade finance platforms | Whether bills of lading, certificates of origin, and customs declarations are internally consistent |

How Does Document Forgery Aggravate Customer Risk and Product Risk?

Customer risk is directly elevated because Document Forgery is specifically designed to present a false customer profile that passes the regulated entity’s risk assessment at a lower risk rating than the true profile. A customer who is a PEP presents as an ordinary individual; a corporate vehicle owned by a sanctioned entity presents as a clean commercial company.

Product risk is aggravated because products that depend on documentary evidence of value, ownership, or provenance are the most vulnerable. Letters of credit, invoice financing, real estate title transfers, and trust administration are designed to accept the document as the basis for a financial or legal transaction. A forged invoice financing a trade transaction introduces a false commercial record into the bank’s portfolio; a forged trust deed creates a false legal framework for asset management.

What Document-Level Signs Alert Compliance Officers to Document Forgery?

Compliance officers reviewing CDD files should examine the physical and structural characteristics of submitted documents rather than their content alone. A genuine identity document has consistent typography, standardised security features in known positions, and physical properties reflecting the issuing authority’s printing standards. Inconsistent font sizes, misaligned margins, or security features positioned outside known boundaries are structural indicators visible before the content is even assessed.

For financial and trade documents, the internal consistency test is the primary detection tool. A genuine invoice has consistent formatting across all invoices in the series, progressive invoice numbers with logical date sequencing, and amounts arithmetically consistent with the stated unit price and quantity. Any inconsistency warrants independent verification against counterparty records or commodity benchmarks.

For corporate and legal documents, the registry cross-reference is the definitive verification tool. For example, if a customer declines to authorise a registry check, or if the check contradicts the submitted document, CDD remediation obligations under CR 134/2025 Articles 7, 9, and 10 apply. Where the circumstances give rise to suspicion or reasonable grounds to suspect money laundering, Article 18 reporting obligations should be assessed.

Sectors at Highest Exposure

| Sector | Risk Rating | Specific Reasoning |

| Lawyers and Notaries | Critical | Directly relied upon to verify the authenticity of legal documents in covered activities; professional authority can be exploited to lend legitimacy to forged corporate or title documents. |

| Independent Auditors and Accountants | Critical | MoET Auditors Guidance section 11.7.5 includes guidance relating to document authenticity and verification measures. Financial statements and related records may be vulnerable to falsification or manipulation in certain ML-related contexts. |

| Trade Finance Providers | Critical | Invoice, bill of lading, and letter of credit forgery are primary instruments in trade-based ML, identified as a major typology. |

| Trust and Company Service Providers (TCSPs) | Critical | BO concealment through forged corporate documents is identified as a primary ML typology category for TCSPs |

| Real Estate Brokers and Agents | High | Title deeds, ownership transfers, and property valuations are targeted for forgery in real estate-based ML schemes. |

| Freight Forwarding and Shipping Services | High | Customs declarations, bills of lading, and certificates of origin are frequent targets for alteration to support trade-based ML. |

| Dealers in Precious Metals and Stones | Moderate | Authentication certificates and provenance records are vulnerable to forgery in collectables-based ML. |

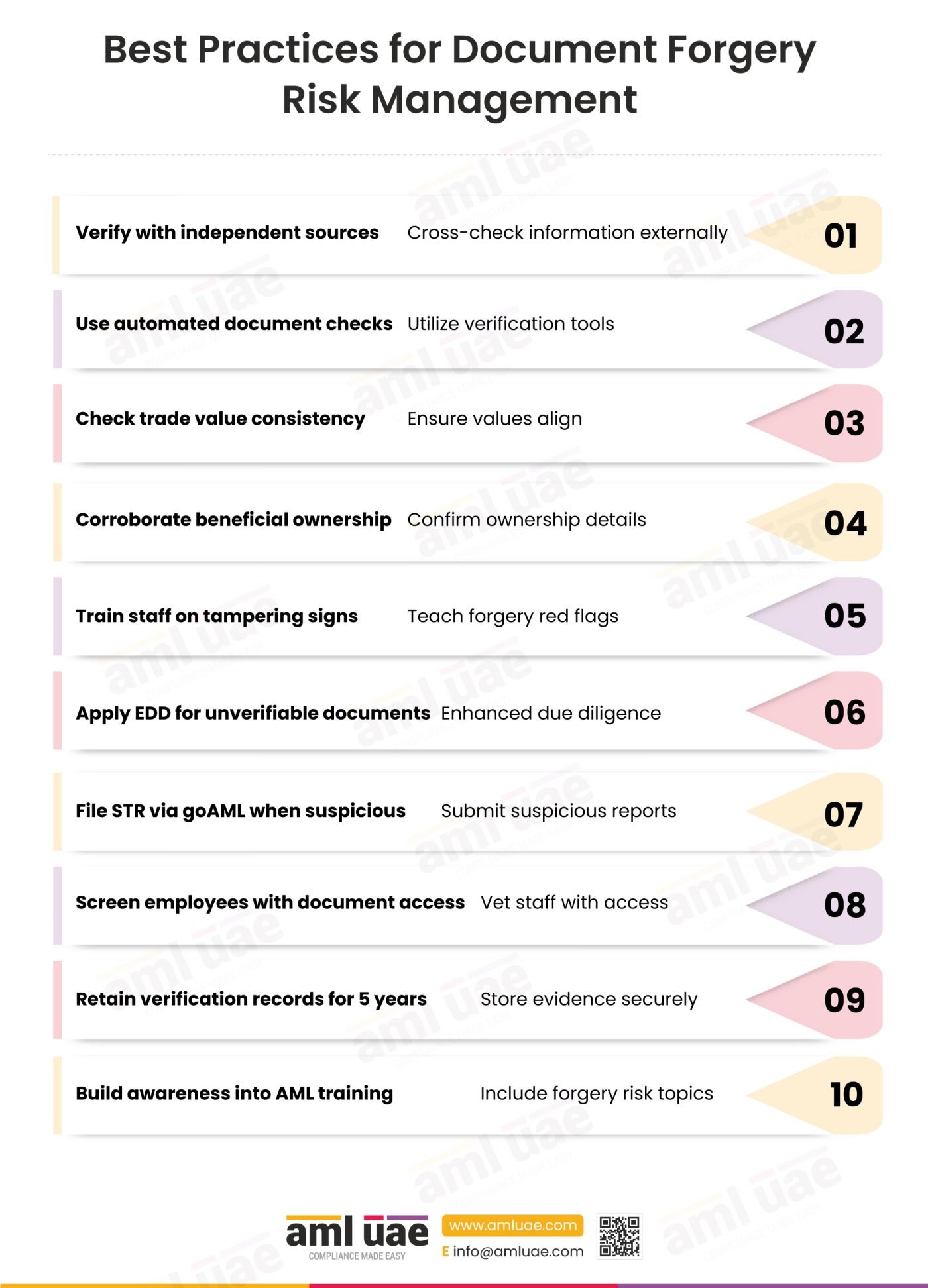

Best Practices for Document Forgery Risk Management

- Never rely solely on client-supplied documentation for identity or beneficial ownership verification. CR 134/2025 Articles 9 and 10 require customer and beneficial owner verification using original documents, data, or information obtained from reliable and independent sources. Cross-reference identity documents against commercial registries, government identity databases, or accredited third-party verification services.

- Deploy automated document verification technology at the point of onboarding and for periodic review. Computer vision and OCR-based platforms detect structural and formatting anomalies that human reviewers cannot reliably identify at scale.

- Apply a value consistency check to all trade documents before processing. Compare declared values against commodity price benchmarks. A material deviation between declared and market value is a primary red flag for forged trade documentation.

- Implement a structured corroboration process for all beneficial ownership claims. Verify ownership structures against the relevant commercial registry or other independent sources. A refusal or inability to support registry or independent verification may indicate that CDD cannot be completed satisfactorily and should trigger escalation or remediation.

- Train staff to identify visual indicators of document tampering at the point of submission. Training should cover the security features of documents commonly encountered in the entity’s business and the physical characteristics distinguishing genuine from forged documents.

- Apply enhanced review or EDD where document concerns remain unresolved or materially increase the customer’s risk profile. Consider elevating the risk rating to high where the facts justify it, which may require additional documentation, business purpose analysis, and senior management approval before the relationship proceeds.

- Submit an STR through the FIU’s electronic system (goAML in practice) without delay where document forgery creates suspicion or reasonable grounds to suspect ML, TF, or PF. The STR obligation under CR 134/2025 Article 18 is triggered by suspicion, not confirmed proof.

- Conduct employee background screening for all staff with access to document management and CDD systems.

- Retain all document verification records, including failed and anomalous checks, for a minimum of five years per CR 134/2025 Article 25.

- Integrate document forgery typology awareness into regular AML training programmes. The MoET Auditors Guidance Section 11.7.8 includes broader guidance relating to AML/CFT awareness, training, and risk indicators relevant to audit and compliance professionals.

Related Terms and Concepts

| Term | Connection |

| Shell Companies | Shell companies depend on forged or misleading corporate documents to obscure beneficial ownership; document forgery is the enabling technique. |

| Beneficial Ownership | BO concealment is the most common purpose of corporate document forgery; forged shareholder registers and trust deeds are the primary instruments. |

| Trade-Based Money Laundering | Trade documentation forgery, including invoice over-invoicing, is the central technique in trade-based ML. |

| Money Mule Exploitation | Money mule networks use forged identity documents to open bank accounts without creating a genuine identity trail. |

| Professional Money Laundering | Professional money launderers, a top UAE NRA ML threat, are the primary orchestrators of sophisticated document forgery schemes. |

| Customer Due Diligence (CDD) | CDD measures are an important control designed to identify forged documentation. |

| Enhanced Due Diligence (EDD) | EDD is the prescribed response when document irregularities are identified during CDD |

| Suspicious Transaction Report (STR) | Where document forgery is suspected, STR obligations through goAML may arise regardless of the transaction value. |

| Structuring | Structuring is often combined with document forgery to obscure both the transaction pattern and the transacting parties’ identity. |

| Identity Fraud | Identity fraud using forged documents is the placement-stage application of the document forgery typology. |

What Financial Instruments Do Criminals Use in Document Forgery Schemes?

Accounts receivable and invoices are the most frequently forged financial instruments. An invoice creates an obligation to pay; a forged invoice creates a false obligation justifying the transfer of funds between parties who are in fact co-conspirators.

Invoice forgery is the foundation of trade-based money laundering, enabling the movement of value through an apparent supply chain transaction.

Bank accounts are the targets of forged-document schemes. Once a forged identity or corporate document enables account opening, the account holds funds under a false name. Cheques carry a named payee and drawer, both of which may be forged, creating a documentary record that appears to validate an underlying business transaction.

Equity interests in legal entities are forged through false shareholder registers, forged share certificates, and falsified articles of association, enabling a criminal to control a legal entity while appearing to have no ownership interest. Letters of credit are targeted because they are among the highest-value documentary instruments in international trade finance; a forged letter of credit can generate a payment obligation against a completely fictitious or inflated transaction.

Trust beneficial interests are forged through false trust deeds, false deeds of appointment, and false letters of wishes, enabling a criminal to control trust assets while appearing to be neither settlor nor beneficiary of record.

| Term | Context or Jurisdiction | Distinction from Primary Term |

| Document Fraud | Criminal law community | Broader term encompassing all forms of document falsification, not limited to the ML context |

| Identity Fraud | Financial crime context | Subset specifically targeting identity documents for KYC bypass purposes |

| Invoice Manipulation | Trade finance and AML context | Subset specifically targeting commercial invoices in trade-based ML |

| Beneficial Ownership Concealment via Documentation | FATF and MoET guidance | Describes the use of forged corporate or legal documents to disguise true ownership structures |

What Products and Services Do Criminals Abuse in Document Forgery Schemes?

Accounting, auditing, and bookkeeping services may be exposed to misuse in circumstances where a professional money launderer engages an accounting firm to certify financial statements built on falsified records, lending apparent authenticity to forged financial data.

Business bank accounts are abused as the destination for proceeds from document-enabled transactions, holding funds under a false name. Document preparation services are directly abused, either by engaging a legitimate service using false instructions or by engaging a specialist forger under the cover of a preparation business.

Freight forwarding and shipping services add transactional substance to forged trade documentation by generating tracking records and customs clearances alongside forged invoices.

Invoice financing services advance funds against submitted invoices without independently verifying the underlying transaction, creating an immediate cash advance against a transaction that may never have occurred.

Legal advisory services are abused when lawyers draft documents or provide opinions on transactions where the underlying instructions or evidence have been falsified.

Notary services may be misused where forged signatures or false translations are presented for authentication. Trade documentation and trade finance services are abused through forged bills of lading, certificates of origin, and commercial invoices to support drawdowns against non-existent transactions. Trust and corporate services are abused when TCSPs establish or administer legal entities on behalf of criminals using forged instructions or documentation of ownership and control.

How AML UAE Helps in Managing Document Forgery Risk

The specific compliance gap that Document Forgery exploits is a reliance on client-supplied documentation as the primary evidence base for compliance decisions. Most CDD processes are designed to collect and file documents; fewer are designed to systematically verify them. The shift from document collection to document verification requires technology, trained staff, and documented verification protocols that most DNFBPs and smaller financial institutions have not fully implemented.

AML UAE helps regulated entities design and implement document verification frameworks that meet the requirements of FDL 10/2025, CR 134/2025, the MoJ Guidebook for Law Firms, and the MoET DNFBP Guidelines.

Our services include document verification policy design, vendor selection support for automated verification technology, staff training on visual forgery indicators, and CDD procedure review to ensure independent verification is embedded at every stage of the customer lifecycle.

For law firms, accounting practices, TCSPs, and trade finance providers, we provide sector-specific training and compliance gap analysis tailored to the document types and verification methods most relevant to the regulated entity’s product mix and customer base.

Conclusion - Document Forgery

Document Forgery is a concealment mechanism that operates by disabling the compliance controls that detect money laundering rather than by moving money itself.

Its target is the document-based trust that regulated entities extend to customers during CDD. For legal professionals, auditors, accountants, trade finance providers, and TCSPs, CR 134/2025 requires customer and beneficial owner verification using reliable and independent sources. For higher-risk scenarios or where documents are inconsistent, independent corroboration should be applied as part of a risk-based CDD process. The MoJ Guidebook (2026) and MoET Auditors Guidance provide sector-specific guidance on document corroboration.

The technology to automate document verification exists and is accessible to entities of all sizes. Computer vision platforms, NLP document analysis tools, and external registry integration do not require large technology budgets to detect the majority of document forgery attempts. What they require is a deliberate decision to shift from document collection to document verification as the core of the CDD process.

For any regulated entity whose CDD procedures depend primarily on reviewing documents that clients have submitted rather than independently verifying them against authoritative sources, the compliance question is not whether Document Forgery is a risk. It is whether the current verification controls are sufficient to detect it before the criminal proceeds past the onboarding stage.

Document forgery is an attack on the foundation of every compliance process. You can have the most sophisticated transaction monitoring in the world, but if the name, the identity, and the corporate structure in your CDD file are all false, the transaction monitoring is watching the wrong person. The investment most UAE compliance teams need to make is in independent verification: not just collecting documents but proving they are genuine before relying on them. That shift, from collection to verification, is where the real risk reduction happens.

Frequently Asked Questions

Document Forgery is a concealment mechanism in which criminals fabricate, alter, or counterfeit official documents, identity records, financial instruments, or legal documentation to bypass compliance controls, conceal beneficial ownership, or provide false evidence of legitimate commercial activity. It operates across all three stages of the money laundering cycle.

Cabinet Resolution No. 134 of 2025, Articles 6 to 10, sets out CDD, customer identification, and beneficial owner identification obligations. Article 9 deals with customer verification, while Article 10 deals with beneficial owner verification using documents, data, or information from a reliable and independent source. Article 18 sets out STR reporting obligations.

Pause or escalate the matter in accordance with internal procedures; avoid tipping off; document the anomalies identified and the verification method used; seek independent verification where appropriate; assess whether circumstances warrant STR submission through the FIU’s electronic system under CR 134/2025 Article 18; escalate to senior management if EDD or relationship termination is under consideration. Retain all records for a minimum of five years.

Yes. The MoET Supplemental Guidance for Auditors, Section 11.7.5, discusses document authenticity as an important consideration for auditors when reviewing transactions or activities involving legal entities.

Failure to implement required CDD, verification, recordkeeping, or reporting controls may expose the entity to administrative penalties under FDL 10/2025 Article 17 (AED 10,000 to AED 5,000,000). Deliberate or grossly negligent breach of Article 18 reporting obligations may attract criminal liability under FDL 10/2025 Article 28.

Document forgery enables BO concealment by producing false shareholder registers, trust deeds, nominee agreements, or corporate resolutions listing nominees rather than true beneficial owners. Presented to regulated entities during CDD, these documents cause institutions to record false ownership structures in their compliance files.

Invoice forgery supports trade-based ML by misrepresenting the price, quantity, or description of traded goods, creating an artificial justification for a transfer of value between co-conspirator counterparties. The forged invoice creates a documentary record that appears to legitimate a commercial payment.

The professional secrecy carve-out in CR 134/2025 Article 18(2) covers the assessment of a client’s legal position and representation or advice connected with judicial, arbitration, or mediation proceedings. The exemption should be applied narrowly and assessed against the circumstances described in Article 18(2). It does not apply to CDD carried out in the course of covered activities or to general financial transaction advice.

The MoET Supplemental Guidance for Auditors Section 11.7.9 includes thirty case examples of ML/TF schemes, several involving falsified financial records. It identifies misuse of client accounts through fraudulent contracts or invoices as a major typology category.

Computer vision platforms performing pixel-level analysis against known genuine template databases are the most effective automated tools. NLP tools that identify semantic inconsistencies complement visual analysis. Blockchain-based provenance systems provide definitive verification by comparing document hashes against immutable registry records.

Protect Your Business from Forged AML Documentation

Fraudulent documents can weaken due diligence processes and increase regulatory exposure. Learn how to strengthen your defence framework.

Share via :

About the Author

Pathik Shah

FCA, CAMS, CISA, CS, DISA (ICAI), FAFP (ICAI)

Pathik is an ACAMS-certified AML consultant specialising in governance, risk, and compliance for regulated entities in the UAE. He brings over 28 years of experience, with 1,000+ hours of AML training and 200+ advisory engagements across DNFBPs, VASPs, and FIs. He supports businesses in aligning with AML/CFT requirements from the CBUAE, DFSA, MoET, MoJ, VARA, CMA, FSRA, and FATF. Known for translating complex regulations into audit-ready procedures, Pathik enables operational clarity and compliance readiness.

Reach Out to Pathik