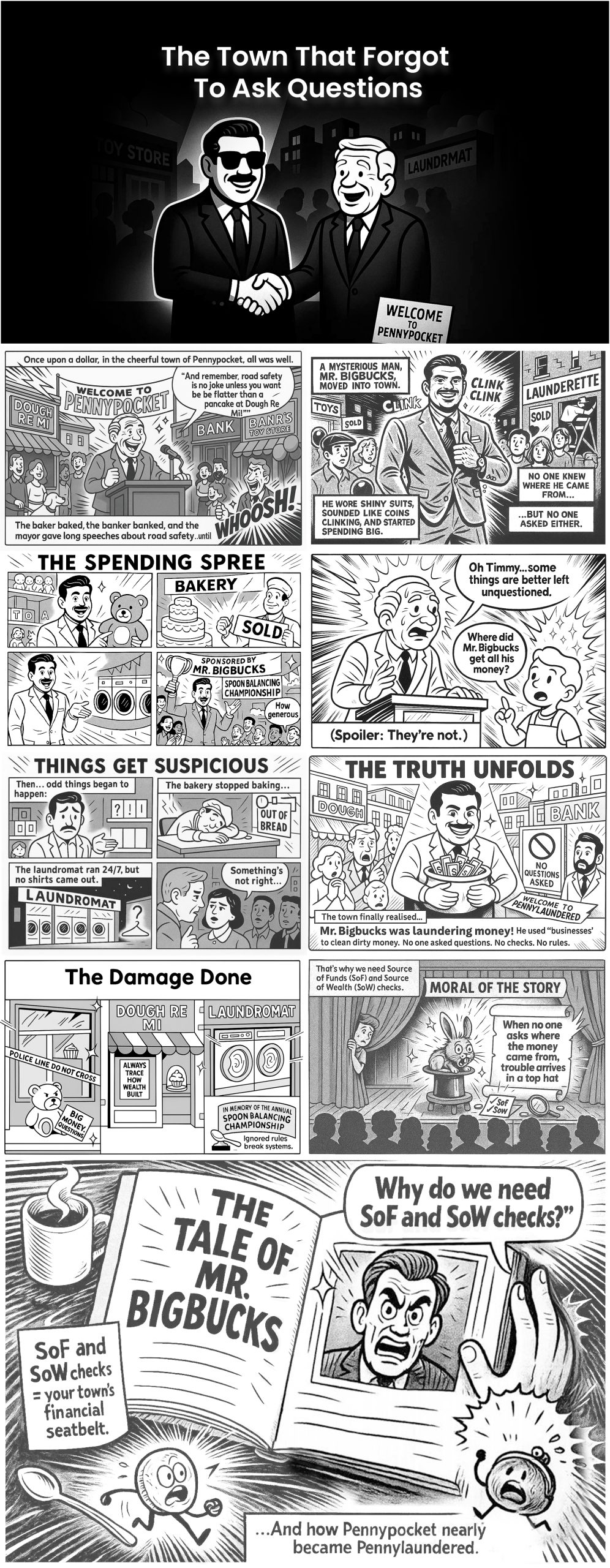

The Town That Forgot To Ask Questions

The Town That Forgot To Ask Questions

A story about what happens when no one checks where the money came from.

Once upon a dollar, in the cheerful town of Pennypocket, everything ran in fine shape. The baker baked, the banker banked, and the mayor gave overly long speeches about road safety. Everyone was happy until one day, strange things began to happen.

A mysterious man named Mr. Bigbucks moved into the town. No one knew where he came from, but he wore shiny suits, had a laugh that sounded like coins clinking, and he started spending big. Really big.

He brought the toy store, the bakery, the laundromat (ironically), and even sponsored the town’s annual ‘Spoon Balancing Championship’. “How generous,” said the townspeople. “He must really love spoons.”

But little Timmy raised an eyebrow.

“Where did Mr. Bigbucks get all his money?” he asked.

“Oh, Timmy,” said the mayor, chuckling, “Some things are better left unquestioned.”

(Spoiler alert: They’re not)

Soon things took a turn. The toy store stopped selling toys and only stored locked boxes. The bakery stopped selling cakes. The laundromat? It was running 24/7, but not a single shirt came out of it. Suspicious, right?

That’s when the town realised: Mr. Bigbucks wasn’t a hero, he was laundering money!

His fancy investments were a clever disguise to make the illegal money look clean. Without checks, rules, or questions, dirty money had walked right into town and brought everything.

By the time the truth came out, it was too late. The bakery was bankrupt, the toy story was under investigation, and the Spoon Balancing Championship was permanently cancelled (a national tragedy).

Moral of the story

If you don’t ask where the money comes from, you might accidentally invite trouble with top hats and gold watches into your home. And that’s exactly what Source of Funds (SoF) and Source of Wealth (SoW) checks are for. It’s the AML/CFT control that checks, double-checks, and sometimes triple-checks the money in the system, so people like Mr. Bigbucks don’t enter with sacks of shady coins.

AML compliance is like the town guard with a magnifying glass. It’s the reason your bank asks for KYC documents. It’s the reason financial institutions investigate suspicious behaviour. It’s to protect the town.

So, the next time someone asks, “Why do we need SoF and SoW checks?”

Tell them the tale of Mr. Bigbucks and how Pennypocket almost became Pennylaundered.

Where did the money come from? Where is it going? Know and keep it flowing safely.

Related Infographics

- Critical Risk Assessment Criteria for PEPs

- PEP and PEP Screening under UAE AML Regulations

- AML UAE PEP Screening Guide

- Onboarding high-risk customers in DPMS

- The importance of unified AML software in meeting compliance requirements

- Know Your Customer (KYC) requirements under AML regulations in UAE

- Consequences for Non-compliance with UAE AML Regulations

- Best Practices for Choosing a RegTech for AML Compliance Automation

Related Videos

- Video on Politically Exposed Person (PEP) and PEP screening requirements in UAE

- Video on Enhanced Due Diligence as part of the AML Program

- Video on Identifying the Right AML Solution

- Video on Avoiding Risky Business Relationships UAE AML Law

- Essential Element of Sanctions Compliance in UAE – Filing Partial Name Match Report

- Video on Enhanced Due Diligence

- Video on the Complete Guide on Identity Verification

- Video on Elements of an effective AML Policy and Procedures

Related Articles

- A Guide to Establishing an Effective AML/CFT Framework in Your Business

- What is Know Your Customer (KYC)?

- A Guide to Sanction and PEP Screening in Customer Onboarding Process

- Addressing an Existing Low-Risk Customer’s Shift to High-Risk Status

- How To Find The Best Anti-Money Laundering Software?

- A Comprehensive Guide to AML Customer Risk Assessment for DNFBPs in UAE

- The Challenges of The Sanction Screening Process

- Checklist for AML Compliance: Best Practices for Anti-Money Laundering Compliance

Related eBooks:

Share via :

Share via :