Migrant Smuggling

Published On: 06/15/2026

Protect your business with reliable and effective AML strategies with AML UAE.

Last Reviewed On: 07/24/2026 | Last Updated On: 07/24/2026

Migrant Smuggling - Key Takeaways

Migrant smuggling generates illicit proceeds through remittance services, cash businesses, and cross-border layering. The UAE Second National Risk Assessment 2024 rates smuggling as a high money laundering threat. It assesses smuggling as a general category rather than migrant smuggling specifically, but migrant smuggling’s cross-border, cash-intensive proceeds fall within that threat and warrant risk-calibrated monitoring under Federal Decree-Law No. (10) of 2025. The critical compliance action is identifying remittance patterns matching known smuggling fees and cross-referencing with beneficial ownership records showing unexplained changes.

What is Migrant Smuggling?

Migrant smuggling is the facilitation of the illegal crossing of international borders by persons not entitled to legal entry, in exchange for a financial or material benefit paid to the smuggling operator.

Migrant smuggling may constitute a predicate offence for money laundering where the underlying conduct amounts to an offence under UAE law or satisfies the applicable predicate-offence test, and the fees charged to migrants, combined with corruption payments to border officials and proceeds from document forgery operations, constitute illicit proceeds that must be concealed through the financial system.

Smuggling networks are large-scale commercial operations. They generate predictable, high-volume revenue from individual fee payments, manage complex multi-jurisdictional logistics, and require sophisticated financial infrastructure to distribute proceeds and reinvest in network capacity.

Migrant smuggling is distinct from human trafficking, although the two can overlap. Smuggling is a transnational offence against border-control law. It involves procuring illegal entry for a financial or material benefit, the migrant generally consents, and the proceeds arise from the smuggling fee. Human trafficking is an offence against the person. It involves recruitment or movement for the purpose of exploitation through coercion, deception, or abuse of a position of vulnerability; consent is legally irrelevant where those means are present, and the proceeds arise from the exploitation itself. The distinction matters for AML because the financial signatures, the victims, and the underlying predicate offences differ.

Regulatory Framework Related to Migrant Smuggling

Migrant smuggling is subject to the full UAE AML/CFT framework. Federal Decree-Law No. (10) of 2025, Article 2, criminalises money laundering arising from predicate offences, and Article 1 defines predicate offences to encompass all offences generating proceeds subject to laundering, including smuggling and trafficking crimes under UAE criminal law. The UAE’s cross-border geographic position as a major international transit hub means that smuggling-related financial flows frequently pass through UAE-based financial institutions and money service businesses.

Cabinet Resolution No. (134) of 2025, Article 5, requires all regulated entities to conduct enterprise-wide risk assessments that take into account the results of the UAE National Risk Assessment, which identifies smuggling, as a general category, as a high money laundering threat.

Articles 6 through 9 of the same resolution impose customer due diligence obligations that may be applied to accounts identified as carrying smuggling-linked transaction patterns.

Article 18 requires immediate suspicious transaction report filing via goAML when reasonable grounds for suspicion of money laundering from any predicate offence that may include migrant smuggling.

Cabinet Resolution No. (71) of 2024 prescribes administrative penalties of up to AED 500,000 under Serial Number 22 for failure to file a suspicious transaction report, and up to AED 1,000,000 under Serial Number 7 for failure to take the NRA into account in the entity-wide risk assessment, making NRA-awareness a separately penalised compliance obligation.

Supervisory Body

The UAE Financial Intelligence Unit (FIU), established under Federal Decree-Law No. (10) of 2025, Article 11, within the Central Bank of the UAE, receives all suspicious transaction reports via goAML.

The Ministry of Economy and Tourism (MoET) supervises DNFBPs. The Central Bank of the UAE supervises financial institutions. Money service businesses are supervised by the Central Bank.

UAE law enforcement coordination for migrant smuggling involves the federal and emirate-level authorities responsible for border security, the Attorney General’s office, and Interpol coordination through the UAE’s international enforcement cooperation framework.

Reporting or Compliance Obligations and Channels of Migrant Smuggling

Regulated entities that identify transactions linked to migrant smuggling proceeds must file a suspicious transaction report without delay via goAML under Federal Decree-Law No. (10) of 2025, Article 18. The cash transaction reporting obligation applies where cash transactions meet applicable thresholds. Trade monitoring obligations apply to regulated entities processing trade finance that may involve shipping or logistics companies used by smuggling networks. Records must be retained for a minimum of five years under Cabinet Resolution No. (134) of 2025, Article 25.

Recent Developments, Enforcement Actions, or Supervisory Priorities

The UAE Second National Risk Assessment 2024 rates smuggling, as a general category, as a high threat to money laundering; it does not assess migrant smuggling separately.

This rating reflects the UAE’s geographic position as a major international transit point and the documented use of UAE-based financial infrastructure by smuggling networks operating across multiple corridors.

The NRA identifies six priority national actions, including improving DNFBP compliance and strengthening cross-border financial intelligence, both of which are directly relevant to migrant smuggling risk management.

The NAMLCFTC Joint Guidance on Satisfactory and Unsatisfactory AML Practice identifies failure to assess geographic exposure in customer risk profiling as a recurring DNFBP deficiency, which may be particularly significant for smuggling risk, given its inherently cross-border financial signature.

Corridor or geographic risk should not be used as a standalone basis for suspicion. It must be combined with the customer’s profile, transaction behaviour, source of funds, and counterparty information, so that monitoring targets conduct rather than nationality or migration status.

What does Migrant Smuggling Mean?

Think of a logistics company that charges a fee to move goods across borders. The fee is collected before the journey, the logistics are handled by the company’s network, and the revenue is distributed among the operators at each stage. Migrant smuggling operates identically, except the cargo is human beings who pay a fee, often borrowed against future earnings, to be moved across borders without legal authorisation. The fee revenue, collected in cash, remittance transfers, and structured deposits, is the proceeds that smuggling networks must launder to fund their continued operations.

Why Detecting Migrant Smuggling Matters

The UAE Second National Risk Assessment 2024 rates smuggling as a high money laundering threat. This reflects the scale of financial flows associated with smuggling networks and the UAE’s geographic exposure as a regional transit hub. The NRA assesses smuggling as a general category and does not rate migrant smuggling separately.

Compliance teams should assess whether their monitoring frameworks adequately address smuggling-related risks identified in the UAE’s National Risk Assessment. Depending on an institution’s risk profile, this may include configuring monitoring scenarios to detect smuggling-related transaction patterns. Deficiencies in risk assessment, risk mitigation, or ongoing monitoring may be subject to administrative penalties under Cabinet Resolution No. (71) of 2024, with certain violations carrying fines of up to AED 1,000,000.

Migrant smuggling differs from other typologies in that its proceeds are collected in very regular, predictable amounts that correspond to the per-person or per-route fee structure of the network.

This fee-based revenue model creates a distinctive transaction pattern: remittance services and money transfer accounts in specific corridors show transaction volumes that track smuggling activity levels, and cash-intensive businesses in proximity to known smuggling routes show deposit patterns that correlate with network operations.

Institutions that overlook smuggling-linked transaction patterns because the individual amounts are not large are missing the compliance signal that the pattern provides.

A series of transactions whose values align with known route fees, whose timing coincides with migration events, and whose geographic origin or destination is a known smuggling corridor is a suspicious pattern regardless of the amount of any single transaction.

How Migrant Smuggling Works

How Smuggling Networks Collect Proceeds from Migrants

Smuggling fee collection begins before the journey. Migrants pay a portion of the agreed fee to the operator or a local intermediary, with the balance due on arrival or drawn against remittances from family members abroad.

The collection mechanism varies by route and operator: cash payments to local facilitators, remittance transfers through MSBs to the operator’s account in the transit or destination country, and, in some cases, advances against future employment wages that create ongoing debt obligations.

The financial signature of fee collection is inbound cash, or remittance flows from a geographically diverse set of individual payers, each making similar-value payments in a short time window, to a small number of aggregator accounts.

How Documents Are Forged, and Corruption Payments Are Made

Document forgery is a cost centre for smuggling networks. Forged passports, visas, and border crossing documents require payment to specialised criminal service providers. Corruption payments to border security, port authorities, and transportation company employees are a significant operational expense for large-scale smuggling operations. These payments are made in cash or through structured transfers to individual accounts, creating a corruption-payment financial signature: high-value disbursements to individuals employed in border or transportation roles, with no commercial explanation for the payment amounts or frequency.

How Proceeds Are Layered Through Cash-Intensive Businesses

Smuggling proceeds that have been collected in cash are laundered through cash-intensive businesses that provide plausible commercial explanations for large cash deposits. Travel agencies, restaurants, casinos, and transportation companies in proximity to smuggling routes or operated by network participants receive cash deposits that are recorded as business revenue.

The detection signal is revenue substantially above the industry average for comparable businesses, combined with unusual deposit timing and geographic inconsistency in the customer base relative to the business’s stated market.

How Remittance Services Distribute Network Revenue

Remittance services are dual-use for smuggling networks. They are used both to receive fee payments from migrants’ families in source countries and to distribute proceeds to network operators across multiple jurisdictions. Individual remittances in amounts that correspond to known route fees, originating from countries with active smuggling routes, and directed to accounts with no commercial relationship to the sender, are a key transaction-level indicator.

Money service businesses with large volumes of transactions in specific corridors must apply adequate monitoring to detect smuggling-fee distribution patterns.

How Structuring Conceals Smuggling Fee Aggregation

Large smuggling fee payments are frequently broken into multiple smaller transfers to avoid cash transaction reporting thresholds. A single migrant’s fee may be paid in three or four instalments from different family members across different channels to the same ultimate recipient account.

At the aggregator level, the smuggling operator receives many such structured payments, which aggregate to a total that reflects the operation’s throughput.

Monitoring for structuring patterns, deposits or transfers of similar amounts, from multiple sources, targeting the same account in a compressed time window, is essential for detecting this aggregation method.

Real-World Examples of Migrant Smuggling

Travel Agency and Remittance Network

A money service business processes a significant volume of inbound remittances from a country with documented smuggling corridors. Analysts notice that a cluster of incoming transfers, each in amounts consistent with known route fees for that corridor, arrive within the same seventy-two-hour window and are directed to a local travel agency account.

The travel agency has no website, no identifiable client base, and a business registration address that matches the MSB operator’s personal address.

Outbound transfers from the travel agency account show payments to individuals employed at a regional airport. Investigation reveals the account is the central financial node for a smuggling network using a travel agency structure to receive fees and pay corruption costs at the departure point.

The detection lesson: travel agency accounts receiving high-frequency remittance inflows from smuggling-corridor countries, combined with outbound payments to transportation sector employees, constitute a recognisable smuggling proceeds processing pattern.

Casino and Entertainment Venue Cash Layering

A compliance review of a casino’s large cash transaction reports reveals a pattern of cash buy-ins that are not associated with extended gambling activity.

Customers make large cash purchases of chips at the cash desk and cash out shortly afterwards with minimal play. The cash-out receipts provide an apparently legitimate commercial explanation for the cash. Analysis of the timing of these transactions shows peaks that correlate with dates on which smuggling vessel arrivals from a high-risk corridor have been documented by border authorities.

The detection lesson: casino cash transactions that follow a buy-in-and-cash-out pattern without corresponding gaming activity, particularly when timed to coincide with documented smuggling route activity, are a classic smuggling proceeds layering signal.

Commercial gaming is a newer regulated activity in the UAE, supervised by the General Commercial Gaming Regulatory Authority, and the 2024 National Risk Assessment did not assess the sector. The pattern described above is drawn from international casino typologies and applies where such services are legally permitted and operational.

Shipping and Logistics Company Corruption Network

A shipping company account receives multiple high-value wire transfers from counterparties in jurisdictions with documented smuggling corridor activity.

The wire transfer descriptions reference cargo shipping contracts; however, document verification reveals that the cargo manifests submitted to the institution contain inconsistencies and that the stated cargo types do not match industry-standard pricing for the transaction amounts.

Cross-referencing with customs and border records identifies that several of the vessels associated with the company’s declared cargo have been flagged for irregular routing.

The detection lesson: shipping company accounts where cargo documentation inconsistencies align with geographic patterns of smuggling corridor activity require trade monitoring escalation and enhanced due diligence into the beneficial ownership of the company.

How Do Criminals Exploit Migrant Smuggling?

The actors who operationalise migrant smuggling range from specialised document forgers and corrupt public officials to organised crime groups that operate full-service smuggling franchises. Shipping and logistics companies are exploited for route access, territorial control, and cargo concealment.

Terrorist organisations have been identified in FATF and regional intelligence reporting as using smuggling networks both for financing and for moving personnel across borders.

The tactic of illicit acquisition is present throughout: each stage at which a fee is collected, a corruption payment is distributed, or a document forgery product is sold generates illicit proceeds.

How Does Migrant Smuggling Facilitate Money Laundering?

Migrant smuggling generates high-volume, structured illicit proceeds from per-person fees collected across multiple source countries. These proceeds must be aggregated, layered, and integrated into the legitimate economy. The placement stage involves cash deposit structuring, remittance aggregation, and cash business revenue inflation. The layering stage involves rapid transfers between intermediary accounts across multiple jurisdictions and the use of cash-intensive business fronts to generate revenue documentation. The integration stage involves investment in further network capacity, asset purchases, and distribution to network participants as what appear to be commercial payments.

What Are the Red Flags That Identify Migrant Smuggling?

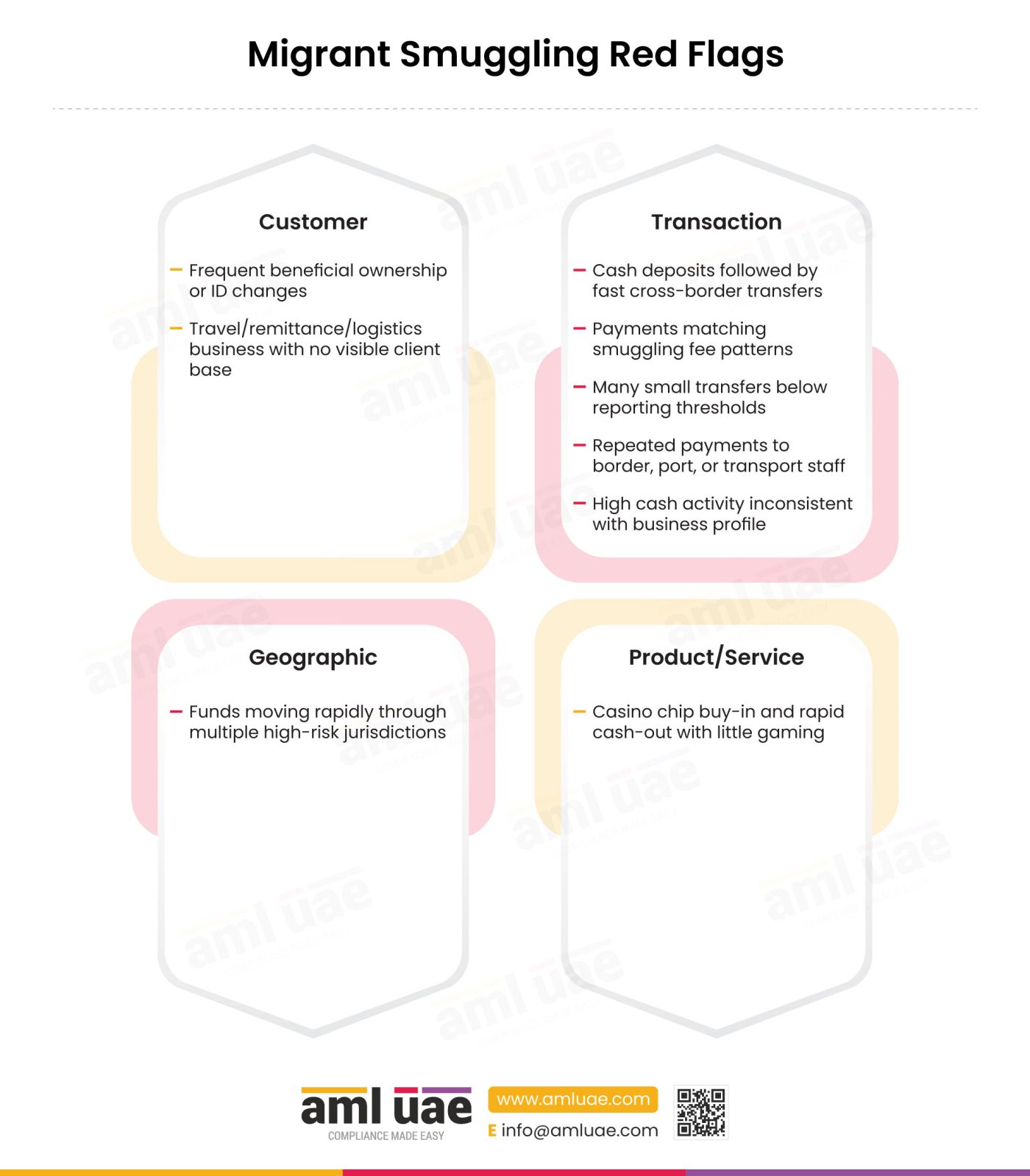

| Category | Red Flag Observation |

| Customer | Frequent changes in beneficial ownership records or rapidly updated customer identification details that do not align with any legitimate business event. |

| Customer | Business account, particularly a travel agency, remittance service, or logistics company, with no verifiable client base or commercial website. |

| Transaction | Currency deposits into accounts, followed by rapid wire transfers to countries identified as having active migrant smuggling routes. |

| Transaction | Multiple international wire transfers originating from or directed to jurisdictions with documented links to known smuggling corridors, with no legitimate commercial relationship explanation. |

| Transaction | Frequent use of remittance services where transaction values match known individual route fees for specific smuggling corridors. |

| Transaction | Incoming or outgoing cross-border payment references explicitly mentioning travel-related terms such as passports, visas, or family assistance in contexts inconsistent with declared business activity. |

| Transaction | Structuring of large sums into multiple smaller deposits or transfers that are deliberately kept below cash transaction reporting thresholds. |

| Transaction | Anomalous cross-border financial movement volumes that are disproportionate to the declared scale and nature of the business. |

| Transaction | Repeated or high-value disbursements to individuals employed by border security agencies, port authorities, or transportation companies with no commercial explanation for the payments. |

| Transaction | Frequent high-value cash deposits into accounts of businesses such as casinos, restaurants, or travel agencies in areas proximate to known smuggling routes. |

| Geographic | Complex layering patterns where funds pass rapidly through multiple intermediary accounts across jurisdictions identified in the NRA as high-risk for smuggling. |

| Product | Casino chip buy-in-and-immediate-cash-out patterns without corresponding gaming activity, particularly in timing consistent with documented smuggling route activity. |

Which Controls Counter Migrant Smuggling?

| Control | What It Disrupts | Detects / Prevents / Deters | Specific Limitation |

| Customer Due Diligence (CDD) | Onboarding of accounts used as fee aggregation points | Detects an inconsistency between the declared business profile and the actual transaction pattern at onboarding | CDD checks for remittance businesses may not include smuggling-corridor-specific risk assessment |

| Enhanced Due Diligence (EDD) | High-risk account management for smuggling-linked patterns | Detects the source of funds inconsistency for travel agency and remittance accounts with corridor-specific inflows | EDD may be applied too narrowly; it should cover all accounts in sectors proximate to smuggling route activity |

| Transaction Monitoring | Remittance corridor fee-matching and structuring detection | Detects remittance patterns matching known route fees and deposit structuring below reporting thresholds | Generic rules do not incorporate smuggling corridor fee range data from intelligence sources |

| Suspicious Activity Reporting (SARs/STRs) | Under-reporting of smuggling-related transaction patterns | Detects mandatory reporting of all suspicious transactions, including smuggling proceeds indicators | Staff training may not cover corridor-specific smuggling red flags |

| Country Risk Assessment | Under-weighting of smuggling corridor geographies | Prevents, accurate risk weighting triggers monitoring for specific corridor patterns | Country risk assessments are updated infrequently relative to the pace at which smuggling routes evolve |

| Trade Monitoring | Documentation inconsistencies in logistics and shipping accounts | Detects cargo documentation inconsistencies that correlate with smuggling route activity | Trade monitoring requires specialist knowledge of cargo documentation norms that is not universally present in compliance teams |

| Employee Background Screening | Placement of network participants in regulated entity roles | Prevents screening to identify prior association with smuggling-linked entities | Background screening does not detect all forms of association; family and social connections are rarely screened |

| OSINT and External Source Verification | Adverse media and public record links to smuggling networks | Detects court filings and media reports linking business accounts to smuggling operations | OSINT coverage of smuggling networks in non-English-language jurisdictions is frequently incomplete |

| Enhanced Due Diligence (EDD) for PEPs | Corruption payments to border and transportation officials | Detects the PEP status of recipients of high-value disbursements from smuggling network accounts | PEP screening may not capture mid-level border security and transportation employees |

How Do AI and RegTech Automate Detection of Migrant Smuggling?

Transaction monitoring platforms can be configured with rule sets that flag remittance transactions in specific corridors where the transaction value falls within the documented fee range for that route.

Intelligence from law enforcement agencies, FATF typology reports, and regional risk assessments provides the fee range data that makes this rule configuration possible. When a money service business account shows multiple incoming transfers in the fee range from a high-risk corridor country within a short window, the alert triggers human review.

Network analytics tools identify the aggregation structures used by smuggling networks.

Remittance accounts that receive funds from many individual senders and rapidly redistribute to a small number of recipients in destination countries exhibit the network topology of a smuggling proceeds clearing account. Graph analytics can identify these structures across accounts and institutions that would appear unrelated in standard transaction monitoring outputs.

Geographical transaction data tools cross-reference ATM usage locations and branch deposit addresses with known smuggling route geography. Deposits made at locations proximate to known crossing points, seaports, or transportation hubs that are identified in national intelligence as smuggling corridor nodes are surfaced for review.

Machine learning anomaly detection identifies remittance service accounts whose transaction patterns deviate from industry baselines in ways consistent with fee aggregation: higher-than-average transaction frequency in specific corridors, unusual payment timing correlating with migration events, and transfer amounts that cluster around documented fee benchmarks rather than following a normal distribution.

These tools support human judgement; they do not replace it. Corridor-risk and anomaly models can generate false positives, are sensitive to data quality, and can embed bias if poorly governed, particularly where a corridor or geography proxies for nationality. Entities should document model logic, thresholds, testing, exception handling, and the outcomes of human review, and should not treat an automated alert, or its absence, as a substitute for a reasoned suspicion assessment.

What Data Should Compliance Teams Collect to Detect Migrant Smuggling?

| Data Point | Source System | What It Reveals About Migrant Smuggling |

| Remittance corridor transaction volumes and amounts | MSB transaction records | Identifies fee-range clustering and volume anomalies in smuggling-risk corridors |

| Geographical transaction data and ATM locations | Geolocation data / core banking | Maps transaction geography to known smuggling route nodes |

| Company and beneficial ownership registry data | Company registry / KYC platform | Identifies rapid ownership changes and shell structures used as fee aggregation fronts |

| Customs and border records | Trade monitoring/customs data feeds | Cross-references declared cargo with routing patterns consistent with smuggling activity |

| Document verification outcomes | Document verification platform | Identifies forged or altered travel and business documents submitted by smuggling network accounts |

| KYC and CDD records for travel and logistics accounts | KYC platform | Enables periodic reassessment of beneficial ownership consistency in high-risk business categories |

| MSB registry data | Money service business licensing records | Confirms whether remittance accounts are operated by licensed MSBs or unlicensed operators |

| OSINT adverse media | OSINT platform | Links account holders and businesses to court proceedings and media reports on smuggling network activity. |

| Correspondent and cross-border transaction data | Correspondent banking records | Identifies high-risk corridor fund flows through correspondent relationships |

How Does Migrant Smuggling Aggravate Jurisdictional Risk?

Migrant smuggling aggravates Jurisdictional Risk because the entire business model of a smuggling network depends on operating across jurisdictions with different levels of border security, law enforcement capability, and AML framework effectiveness.

Networks deliberately route financial flows through jurisdictions with weak AML supervision to create distance between the proceeds and the originating offence.

The UAE National Risk Assessment 2024 identifies smuggling, as a general category, as a high threat, and the national priority actions it defines include strengthening cross-border financial intelligence cooperation, reflecting the inherently international dimension of smuggling proceeds flows.

The jurisdictional risk is compounded by the involvement of corrupt public officials. Payments to border and transportation officials in jurisdictions with systemic corruption are nominally commercial but actually bribes. Regulated entities in the UAE that process these payments without adequate monitoring are potentially facilitating corruption-predicate money laundering in addition to smuggling-predicate money laundering.

How Do Transaction Patterns Reveal Migrant Smuggling?

A compliance officer analysing a travel agency account associated with a smuggling network will observe a pattern of high-frequency inbound remittances from a limited geographic source, each in amounts that cluster around a consistent value.

The outbound pattern shows rapid distributions to multiple individuals in a transit jurisdiction, combined with occasional large payments to entities in the destination country.

Periodic large cash deposits supplement the remittance inflows. The absence of any identifiable client base in the business’s declared market, combined with the geographic concentration of inbound flows in a known smuggling corridor, is the defining detection signal.

Sectors at Highest Exposure

| Sector | Risk Rating | Specific Reasoning |

| Money service businesses and remittance providers | Critical | Smuggling fee collection and distribution primarily uses remittance infrastructure; corridor-specific monitoring is essential. |

| Travel agencies and tour operators | Critical | Travel industry fronts are the most commonly used business cover for smuggling proceeds aggregation. |

| Retail banking (personal and business accounts) | High | Structured cash deposits and rapid intermediary account transfers are the primary bank-level placement and layering mechanisms. |

| Shipping and logistics | High | Networks exploit logistics companies for route access and cargo concealment; trade documentation inconsistencies are the detection signal. |

| Gambling services | Moderate | Casino and gambling venues are used for classic cash layering through buy-in-and-cash-out schemes. |

Best Practices for Migrant Smuggling Risk Management

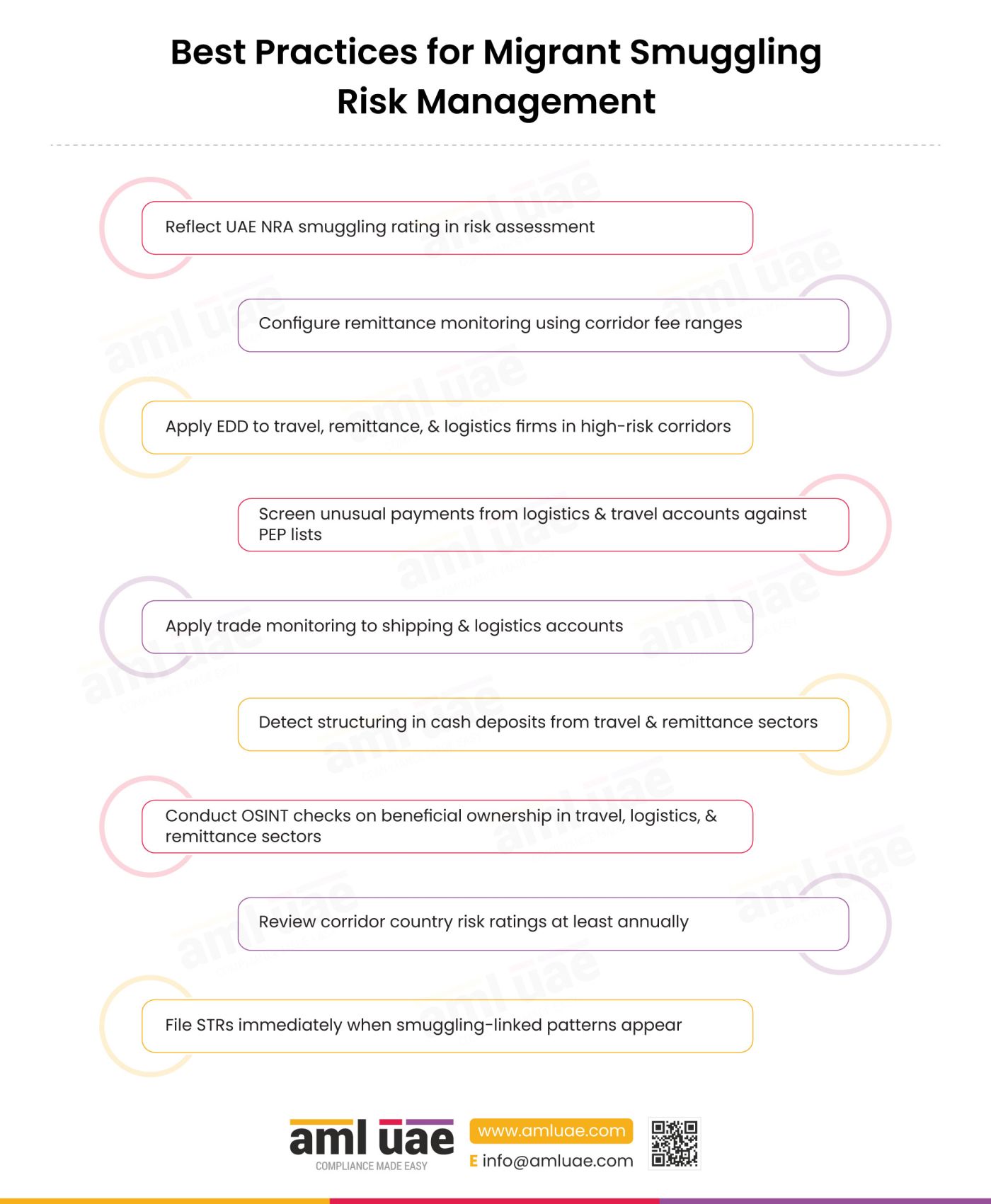

- Integrate the UAE NRA smuggling threat rating into the entity-wide risk assessment. Cabinet Resolution No. (134) of 2025, Article 5, requires the EWRA to take NRA results into account. The NRA’s high smuggling threat rating should be reflected in the risk assessment and translated into specific monitoring obligations for business lines with exposure to smuggling corridors.

- Configure remittance monitoring rules using documented corridor fee ranges. Transaction monitoring for money service businesses should include rules that flag incoming transfers in the fee range associated with specific smuggling routes. Intelligence sources, including FATF typology reports, UNODC data, and law enforcement advisories, provide fee benchmarks that compliance teams can translate into monitoring parameters.

- Apply enhanced due diligence to travel agencies, remittance services, and logistics companies in high-risk corridor geographies. These business categories are the most commonly exploited by smuggling networks.

- Screen all high-value disbursements from logistics and travel accounts against politically exposed person lists. Corruption payments to border security and transportation officials are a standard operational expense for smuggling networks. PEP screening of recipients of unusual payments from logistics and travel accounts should be included in the monitoring framework.

- Apply trade monitoring to shipping and logistics accounts. Compliance teams must verify that cargo documentation submitted by logistics company accounts is consistent with the transaction amounts and the declared routing. Inconsistencies between cargo manifest descriptions, transaction values, and route geography are a key detection signal for smuggling network logistics infrastructure.

- Detect structuring patterns in cash deposits from travel and remittance sector accounts. Regular cash deposits below the reporting threshold from accounts in the travel and remittance sectors should trigger pattern-based review. Cabinet Resolution No. (134) of 2025, Article 8, requires ongoing monitoring of the business relationship, and Article 17 addresses the indicators of suspicious transactions that must be reported; structuring of cash deposits is a recognised red-flag indicator.

- Conduct an OSINT review for beneficial ownership of accounts in travel, logistics, and remittance sectors. Adverse media and court filing reviews for accounts in these high-risk categories should be conducted at onboarding and periodically thereafter. Emerging criminal proceedings in source or transit jurisdictions are a key indicator that an account may be connected to a smuggling network.

- Assess country risk ratings for all remittance corridors using current NRA and FATF data. Country risk ratings must be reviewed and updated at least annually to reflect current NRA findings and FATF increased monitoring list additions. A corridor that was not high risk in the previous assessment cycle may have become high risk due to evolving smuggling route patterns.

- File suspicious transaction reports without delay upon identifying smuggling-linked patterns. Federal Decree-Law No. (10) of 2025, Article 18, requires immediate filing. Where a smuggling proceeds pattern gives rise to suspicion or reasonable grounds for suspicion that funds represent proceeds of crime, the entity should file an STR without delay and need not wait for a full law-enforcement investigation. The compliance team must still assess the surrounding context before concluding that the reporting threshold is met.

Related Terms and Concepts

Migrant smuggling sits at the intersection of multiple AML risk categories. It is directly linked to organised crime groups and corruption, both of which generate independent predicate offences alongside the smuggling offence itself. The document forgery component links it to identity fraud typologies. The reliance on remittance infrastructure connects it to the risk of informal value transfer systems.

| Related Term | Connection |

| Human Trafficking | Closely related, smuggling networks frequently transition migrants into trafficking situations. |

| Sexual Exploitation | Downstream risk, smuggled migrants are vulnerable to exploitation upon arrival. |

| Child Exploitation | Downstream risk, unaccompanied minors in smuggling networks are at extreme exploitation risk. |

| Cash Structuring | Layering technique, smuggling proceeds are placed through structured cash deposits below reporting thresholds. |

| Corruption and Bribery | Related predicate, corruption payments to border officials are a standard smuggling operational expense. |

| Money Service Business (MSB) Risk | Delivery channel, MSBs are the primary financial infrastructure for smuggling fee collection and distribution. |

| Suspicious Transaction Reports (STRs) | Reporting obligation, smuggling proceeds patterns trigger mandatory STR filing. |

What Financial Instruments Do Criminals Use in Migrant Smuggling Schemes?

Bank accounts are used as aggregation points for both inbound fee payments and outbound network distributions. A smuggling network operator may maintain multiple personal and business accounts in different names, each receiving a portion of the total fee flow, to reduce the detectability of the aggregate volume.

Cash is the dominant instrument for fee collection in physical smuggling operations, particularly at the initial engagement stage in source countries. Cash is also used for corruption payments to border officials and transportation employees, where a traceable payment method would create unacceptable evidence risk.

Casino chips function as a physical cash equivalent for money laundering purposes. The buy-in-and-cash-out mechanism converts illicit cash into casino receipts that carry no indicator of the original cash source, providing an integration vehicle for smuggling proceeds that does not require a commercial business structure.

| Variant / Synonym | Context or Jurisdiction | Distinction from Primary Term |

| Human smuggling | US law enforcement and immigration enforcement | Functionally equivalent term; emphasises that the smuggled person is a human being |

| People smuggling | Australian and UK law enforcement | Common usage in English-speaking jurisdictions outside the US |

| Irregular migration facilitation | International migration policy frameworks | Policy-neutral framing that describes the facilitation function without criminal characterisation |

| Coyote operation | US-Mexico border enforcement context | Refers to the ground-level smuggling operator who physically accompanies migrants across the border |

What Products and Services Do Criminals Abuse in Migrant Smuggling Schemes?

Business bank accounts are maintained in the names of travel agencies, logistics companies, and general trading companies to provide commercial cover for smuggling proceeds aggregation and distribution.

Cash transaction services are used to deposit fee proceeds and corruption payment collections in fragmented cash amounts that aggregate to the network’s total illicit revenue.

Gambling services are used for the classic buy-in-and-cash-out smuggling proceeds layering scheme, converting cash into casino receipts that provide a plausible commercial explanation for the funds.

Money transfer and remittance services are the primary channel for both fee collection from migrants’ families and network revenue distribution to operators across multiple jurisdictions. MSBs with active corridor business are the highest-exposure entities in the financial system for smuggling proceeds.

Travel and related services provide the business cover for smuggling network operations. Travel agency accounts that receive high volumes of remittances from specific corridors with no identifiable tourism client base are a primary smuggling detection indicator.

Trust and corporate services are used to establish the legal entity structures through which smuggling network operators hold assets, manage accounts, and obscure beneficial ownership. Rapid changes in beneficial ownership are a detection signal for these structures.

Wire transfer services are used for cross-border network revenue distribution, connecting fee aggregation accounts in the UAE to operator accounts in transit and destination jurisdictions.

How AML UAE Helps in Managing Migrant Smuggling Risk

Migrant smuggling risk management requires monitoring configurations that go beyond standard threshold-based transaction surveillance. The detection signal for smuggling proceeds lies in corridor-specific patterns, fee-range clustering, and the correlation between transaction timing and migration events, none of which are captured by generic AML rule sets.

AML UAE works with compliance teams in financial institutions, money service businesses, and DNFBPs operating in the travel, logistics, and remittance sectors to build smuggling-specific monitoring frameworks calibrated to UAE-relevant corridors.

AML UAE also supports compliance teams in integrating the UAE NRA’s high smuggling threat rating into their entity-wide risk assessments in a manner that satisfies the Cabinet Resolution No. (134) of 2025 requirement. The risk assessment update process, monitoring rule calibration, and staff training package form a comprehensive response to the smuggling risk identified in the NRA, meeting both the letter and the spirit of UAE regulatory obligations.

Smuggling proceeds are the most consistently under-detected AML risk in the remittance and travel sectors. The individual transactions are unremarkable; the detection signal is entirely in the pattern. Compliance teams that build corridor-specific fee-range monitoring rules and cross-reference remittance flows with known route activity will detect smuggling networks that generic monitoring fails to catch.

Frequently Asked Questions

Yes. Federal Decree-Law No. (10) of 2025, Article 2, criminalises money laundering arising from predicate offences. Article 1 defines predicate offences to include all offences generating proceeds subject to laundering, which may encompass smuggling crimes under UAE criminal law.

The UAE Second National Risk Assessment 2024 rates smuggling as a high money laundering threat. It assesses smuggling as a general category and does not assign migrant smuggling a separate rating, but migrant smuggling falls within that broader threat and should be reflected in all regulated entities’ entity-wide risk assessments under Cabinet Resolution No. (134) of 2025, Article 5.

MSBs must apply customer due diligence under Cabinet Resolution No. (134) of 2025, Articles 6 through 9, to all customers. For high-risk corridors identified in the UAE NRA as smuggling-exposure routes, enhanced due diligence is required. Suspicious transaction patterns must be reported without delay via goAML under Federal Decree-Law No. (10) of 2025, Article 18.

Cabinet Resolution No. (71) of 2024, Serial Number 7, prescribes a maximum administrative penalty of AED 1,000,000 for failure to take the National Risk Assessment results into account in the entity-wide risk assessment. This makes NRA integration a separate and highly penalised compliance obligation.

Travel agencies are not automatically DNFBPs merely because they provide travel services; the DNFBP categories listed in Cabinet Resolution No. (134) of 2025, Article 3, do not include travel agencies. A travel business falls within the AML/CFT framework only where it also carries on a regulated activity that brings it within a DNFBP category or requires financial institution licensing. Travel agency accounts that are not themselves DNFBPs are customers of financial institutions and subject to the institution’s customer due diligence framework.

Regulated entities processing trade finance for logistics and shipping companies must verify that cargo documentation is consistent with transaction values and routing patterns. Inconsistencies that correlate with smuggling route geography are suspicious indicators requiring escalation under the institution’s STR framework.

Cabinet Resolution No. (134) of 2025, Article 19, prohibits any disclosure to an account holder that a suspicious transaction report has been filed or that an investigation is underway. This may apply to smuggling investigations in the same way as any other predicate offence.

Cabinet Resolution No. (134) of 2025, Article 25, requires five-year retention of all CDD, transaction, and STR records. For smuggling-linked investigations, trade monitoring outputs, correspondent banking data, and OSINT reports should be preserved alongside standard documentation.

Closing Summary

Smuggling is one of the UAE NRA’s high-rated money laundering threats, and migrant smuggling’s financial signature is one of the most distinctive in the typology landscape: remittance corridor fee clustering, structured cash deposits, and corruption payments to border officials create a pattern that may be recognisable to any compliance team with the right monitoring configuration.

The regulatory framework is clear, the EWRA must reflect the NRA, CDD must be applied to high-risk accounts, STRs must be filed without delay and the penalty framework under Cabinet Resolution No. (71) of 2024 creates significant exposure for institutions that have not implemented these obligations.

The sectors most exposed to smuggling proceeds are money service businesses, travel agencies, and logistics companies. These are precisely the business categories that receive the least sophisticated AML scrutiny in many compliance programmes.

Addressing this gap requires not only rule configuration but a genuine understanding of how smuggling networks use these sectors as financial infrastructure, which is only possible when compliance teams are trained on the specific indicators that distinguish smuggling activity from legitimate commercial operations in the same sectors.

Every institution that processes remittance flows in UAE-relevant corridors has a regulatory obligation to assess its smuggling exposure and configure its monitoring accordingly. That obligation is not aspirational; it is a legally mandated component of the entity-wide risk assessment under Cabinet Resolution No. (134) of 2025.

Disclaimer: This article is provided for general information only and does not constitute legal or compliance advice. It summarises the UAE AML/CFT framework as at the date of publication, and the law and supervisory guidance may change. Regulated entities should verify the current text of the relevant legislation and obtain qualified advice before acting on any obligation, penalty, or reporting requirement described here.

Is Your Business at Risk?

Review your exposure to migrant smuggling proceeds and improve your AML response with practical guidance.

Share via :

About the Author

Pathik Shah

FCA, CAMS, CISA, CS, DISA (ICAI), FAFP (ICAI)

Pathik is an ACAMS-certified AML consultant specialising in governance, risk, and compliance for regulated entities in the UAE. He brings over 28 years of experience, with 1,000+ hours of AML training and 200+ advisory engagements across DNFBPs, VASPs, and FIs. He supports businesses in aligning with AML/CFT requirements from the CBUAE, DFSA, MoET, MoJ, VARA, CMA, FSRA, and FATF. Known for translating complex regulations into audit-ready procedures, Pathik enables operational clarity and compliance readiness.

Reach Out to Pathik