AML Policy Drafting for Real Estate Sector

We provide customised AML/CFT policy drafting services for real estate businesses, including brokers, agents, and professionals involved in property transactions, tailored to Federal Decree-Law No. (10) of 2025, its Implementing resolutions, and real estate-specific guidance and circulars.

A customised AML/CFT policy is a mandatory for UAE real estate businesses and professionals. A real estate business’s AML/CFT Policy must include risk-based framework that governs how property transactions, clients, and funds are monitored, reported, and controlled.

A well-drafted Anti-Money Laundering and Combating the Financing of Terrorism (AML/CFT) Policy is vital for ensuring AML compliance within UAE’s Real Estate Sector.

The customised AML/CFT Policy ensures compliance with regulatory standards and provides a clear framework of governance structure that aids in reducing Money Laundering (ML) and Terrorist Financing risks (TF).

Real Estate businesses gain clarity, resilience and accountability with a strong AML/CFT Policy, which is more of a shield for the business rather than just a formality.

What is an AML Policy?

An AML Policy is a formally drafted document that outlines the measures businesses adopt to prevent their services from being misused by illicit actors for furtherance of crime.

Who does AML/CFT Policies Apply to in the Real Estate Sector?

As per Article 3 of Cabinet Decision No. (134) OF 2025, Real Estate Brokers and Agents are classified as Designated Non-Financial Businesses and Professions (DNFBPs) when they carry out activities or transactions on behalf of their customers regarding the purchase or sell of real estate.

Lawyers, notaries and other independent accountants are also deemed to be DNFBPs when they prepare, conduct or execute financial transactions on behalf of their customers regarding the purchase and sell of real estate.

When DNFBPs including Real Estate Brokers and Agents, as well as lawyers, notaries and other independent accountants, carries out specific activities in real estate sector that is classified as covered activities in AML/CFT Decision, they are required to implement robust AML/CFT measures in line with the Federal AML/CFT laws.

This includes establishing, documenting and updating internal AML/CFT Policy in order to identify, assess and mitigate ML/TF/PF risk faced by businesses in real estate sector.

Applicable UAE AML/CFT Laws for Real Estate Businesses

For Real Estate Businesses conducting specific activities, applicable UAE AML/CFT laws are:

regarding the Anti-Money Laundering and Combating the Financing of Terrorism and Proliferation Financing calls for implementing AML/CFT policies.

on the Implementing Regulation of Federal Decree Law No. (10) of 2025, emphasis establishing internal AML/CFT policies commensurate to the nature and size of the business, taking Risk-Based Approach.

Real-Estate Sector specific AML/CFT/CPF Guidelines:

- Supplemental Guidance for Real Estate Sector directs establishing, documenting and updating internal policies to identify, mitigate and manage identified ML/TF/PF risks.

- Ministry of Economy Circular Number 05/2022 on Real Estate Activity Report, requires Real Estate Brokers and Agents to mandatorily submit Real Estate Activity Report (REAR) for freehold property transactions that are settled in cash or virtual currencies. The threshold for cash is property transactions that equals or exceeds AED 55,000. Such transactions are reported via goAML Portal. These requirements need to be incorporated in AML/CFT Policy for Real Estate sector.

- FIU’s Strategic Analysis Report on Real Estate Money Laundering Typologies and Patterns, this report discusses the relevant typologies pertaining to the ML/TF/PF activities in Real Estate Sector. While preparing an AML/CFT Policy, these specific typologies need to be considered.

Why Real Estate AML Policies Cannot Be Generic?

An effective AML/CFT Policy cannot be generic, it should be custom-made based according to the risk to which the real estate business is exposed.

In simple words, an AML Policy is a practical living-breathing framework aimed at safeguarding the businesses interests and not a mere template that is aligned with the legal obligations under the UAE AML laws.

The unique risk factors associated with Real Estate Sector demands the formulation of customised AML/CFT Policy.

The Real Estate Sector poses distinct ML/TF/PF risks due to high value and long-term nature of property transactions. Real Estate laws and practices also vary across Emirates that facilitates different nature of risks depending on the location and nature of the transaction.

Real Estate agents, brokers and other professionals involved in property transactions can perform different roles including representing parties, acting as intermediaries or holding or transferring documents or funds, advising on financing etc. Each of these roles carries varied risk levels.

Customer risk in Real Estate Sector differs significantly based on the customer type (individual, company or a complex legal structure). Geographic risk is also key factor especially when customers are foreign nationals, non-residents or linked to high-risk countries.

Moreover, risk profile of a real estate transaction differs depending on the purpose of property that is residential, commercial, personal use, resale, investment etc.

All these factors combine requires businesses in Real Estate Sector to adopt tailor approach in order to establish and develop their internal AML/CFT policy as requirement for each of them vastly contrasts based on the nature and size of the business.

Purpose of Customised AML/CFT Policy for Real Estate Sector

In the context of Real Estate Sector, businesses in their AML/CFT Policy must include transaction size, property type, use of intermediaries, and funding sources it relies on, to showcase risk-based measures taken to mitigate ML/TF and PF risks.

The customised AML Policy for Real Estate has a purpose to translate complicated AML obligations into a tailored policy framework that adjusts itself into the everyday business operations of a Real Estate enterprise.

Be it a property broker, agent or legal professional involved in a real estate transaction, every Real Estate business needs a customised AML/CFT Policy according to their business’s unique requirements, to reduce ML/FT/PF risks and other related risks.

Instead of depending on generic templates, the customised AML/CFT Policy drafting process for Real Estate ensures that the AML/CFT Policy is aligned with the actual risk exposed to business, its products and transaction patterns.

The AML/CFT Policy must contain internal controls, employee responsibilities, and reporting systems required to manage and mitigate financial crime risks with consistency and discipline, which enables fulfilling AML Compliance obligations.

The purpose of the AML/CFT Policy draft also includes compliance with the Federal Decree Law No. (10) of 2025 and implementing regulation under Cabinet Decision No. (134) of 2025.

The intent of a customised AML Policy Framework is to strengthen the Real Estate business, reduce operational, regulatory and reputational risks, rather than just limit itself to a policy & procedure tick-box.

Complete. Consistent. Accurate.

Engage us to create the most suitable AML/CFT policies, controls, and procedures for your business.

Importance of a Tailored AML/CFT Policy for Real Estate Sector

Real Estate sector is one of the most lucrative sectors for ML/TF actors due to high-value assets and its vulnerability to layered transactions and third-party involvement.

Real Estate brokers/agents, notaries, lawyers, independent accountants, and other independent legal professionals involved in a real estate transaction are required to fulfil specific obligations by UAE’s AML/CFT laws and AML/CFT Decision, which calls for the foundation of an effective risk-based AML/CFT program.

A well-drafted AML/CFT Policy for the Real Estate business is necessary to recognise, evaluate and mitigate ML/TF risks. However, staying compliant with regulatory requirements is a starting step.

The Real Estate Sector is highly appealing to money launderers due to high-cash-intensive transactions and the use of third parties. So, without a customised AML/CFT Policy, it is difficult to manage these vulnerabilities.

The drafting of systematic & risk-focused AML Policy improves the internal controls and builds trust with customers, investors and regulators. It further confirms that there is proper alignment of compliance actions with the actual ML/TF/PF risks the Real Estate business faces.

Also, structured AML/CFT Policy ensures sufficient resources are allocated to high-risk areas, instead of following a blanket approach that doesn’t guarantee effective controls.

Challenges Faced by Real Estate Sector while Drafting an AML/CFT Policy

Implementing AML/CFT Policies is a big hurdle for even far-sighted and well-prepared Real Estate businesses. It is necessary to be aware of these challenges and adopt proper measures to rectify them during drafting an AML/CFT Policy:

Does your AML/CFT Policy include proper ML/FT risk assessment customised to activities such as high cash-intensive transactions, opaque ownership structures, fraudulent loan practices and others?

Does your AML Policy include an adequate Customer Onboarding and Exit Process that records PEPs, third-party transactions, and an accurate source of funds & wealth of high-risk customers?

Is your team aware of major typologies that affect the real estate sector, such as unknown sources of funds, use of intermediaries or family members to hide real owners, instant property flips, usage of mortgage loans, etc?

Are you confident that your team has proper knowledge regarding filing REAR for transactions concerning freeehold properties above AED 55,000, and SAR/STRs via goAML portal for suspicious activity or behaviour?

Have you implemented proper internal controls that restrict tipping off customers during internal investigations or reviews?

Does your AML Policy provide proper guidance to understand the urgency of filing CNMR/PNMR and can differentiate them based on UAE TFS obligations?

Are your frontline and compliance team members checked and effectively trained about AML/CFT obligations, complying with the customer onboarding obligations, analysing Real Estate sector red flags and meeting the reporting requirements?

Is your Compliance Officer competent enough to handle the AML Compliance program and perform their duties efficiently?

Does your AML/CFT Policy have a written procedure for Customer Due Diligence that includes identifying beneficial ownership and proceeding with Enhanced Due Diligence for high-risk customers?

Get Rid of Your Compliance Pain Points!

Engage us to design an AML/CFT Policy for your business to meet regulatory standards.

“In the UAE Real Estate Sector, particularly in high-value markets like Dubai, ML/TF and PF risk emerges through layered property transactions, broker-led deals, and third-party funding structures. An effective AML/CFT Policy must provide for tracking and reporting transactions which often involve brokers, developers, intermediaries, and third-party funding, the AML/CFT Policy must track risks across the full transaction lifecycle, right from client onboarding and source-of-funds verification to title transfer and post-transaction reporting, in alignment with the supervisory expectations of the Ministry of Economy and emirate-level real estate obligations. ”

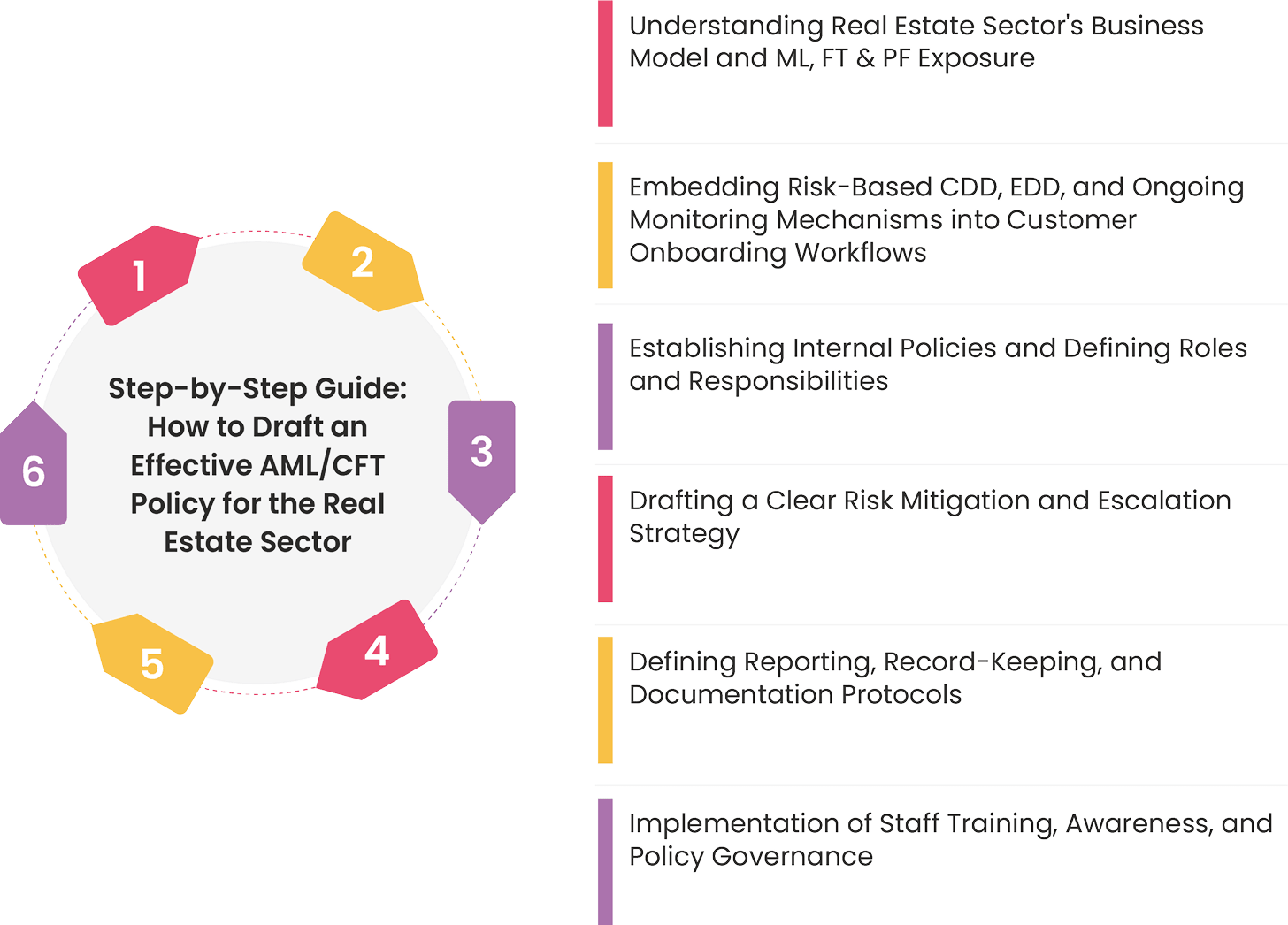

Step-by-Step Guide: How to Draft an Effective AML/CFT Policy for the Real Estate Sector

AML/CFT Policy draft for Real Estate Sector is a structured procedure that begins with understanding the business and risk exposure.

It continues with embedding risk-based CDD, EDD and ongoing monitoring measures into the customer onboarding workflows, followed by establishing internal policies.

The next steps include drafting a risk mitigation and escalation strategy, defining reporting and record-keeping protocols, implementing staff training, and policy governance.

Step 1:

Understanding Real Estate Sector’s Business Model and ML, FT, and PF Risk Exposure

Understanding Real Estate Sector’s Business Model and ML/TF/PF risk exposure is the first step of drafting an AML/CFT Policy.

The basis of drafting a systematic AML/CFT Policy for the Real Estate business starts with evaluating both enterprise-wide risk and customer risks.

This comprises a proper understanding of business operations and risk exposure to the business through conducting an Enterprise-Wide Risk Assessment (EWRA).

The vulnerabilities faced by the Real Estate business are influenced by factors such as customer type, location of property, transaction mode, use of intermediaries, etc.

The AML/CFT Policy draft should mandate performing adequate due diligence while dealing with high-risk customers to address actual risk and not just the assumed risk.

Step 2 :

Embedding Risk-Based CDD, EDD, and Ongoing Monitoring Mechanisms into Customer Onboarding Workflows

This step focuses on integrating Risk-Based CDD, EDD and Ongoing Monitoring Mechanisms into the Customer Onboarding workflows AML/CFT Policy.

Once the Real Estate business assesses its business risks, the next step in effective drafting of AML/CFT Policy is including risk mitigation measures such as Customer Due Diligence (CDD) and Enhanced Due Diligence (EDD) into customer onboarding workflows.

This includes identifying and verifying beneficial owners, third parties, and collected supporting documents. In cases of high-risk customers like PEPs or HNWI.

Step 3:

Establishing Internal Policies and Defining Roles and Responsibilities

Establishing clear internal policies and defining roles and responsibilities, governance structure and escalation mechanism within real estate business’s AML/CFT Policy is the third step.

The AML/CFT Policy should mention clear roles and responsibilities assigned to competent individuals who possess the authority to perform critical functions.

This comprises drafting a clear governance structure, workflows and approvals, including the procedures and escalation channels for CDD, Suspicious Activity Reporting (SAR), Suspicious Transaction Report (STR), and Screening. The Staff Training too must be customised according to the role-specific responsibilities and expertise required.

Step 4:

Drafting a Clear Risk Mitigation and Escalation Strategy

This step is about outlining a clear risk mitigation and escalation strategy that defines how the real estate business will respond to identified ML/TF/PF risks.

The next step in drafting the AML Policy for the Real Estate business is to clearly define within the AML/CFT Policy how the business is going to handle ML/TF/PF risks, if they materialise.

This means clearly stating how the Real Estate business will respond to high-risk scenarios, if they arise, such as encountering sanctioned individual or entity, coming across customer routing transactions through a blacklisted country, etc. The AML/CFT Policy should have a clear RACI matrix for allocating task responsibility and accountability.

Step 5 :

Defining Reporting, Record-Keeping, and Documentation Protocols

This step focuses on defining clear Reporting, Record-Keeping and Documentation rules in real estate business’s AML/CFT Policy as per the regulatory requirements.

An effective AML/CFT Policy should define documentation, reporting and record-keeping procedures for compliance measures taken. This comprises forming an internal workflow that identifies specific red flags and reports them as suspicious.

The reporting procedure should also define when and how a Confirmed Name Match Report (CNMR) and a Partial Name Match Report (PNMR) are filed according to the Targeted Financial Sanctions (TFS) Guidelines for Sanctions Screening.

Further, a clear procedure for filing STR/SAR should be included in the AML/CFT Policy for reporting suspicious transactions or activities. However, the Real Estate business should be careful when they should file REAR and not confuse it with STR/SARs, as it may lead them to legal penalties, so a clear procedure should be defined.

Step 6:

Implementation of Staff Training, Awareness, and Policy Governance

The next step is to ensure that AML/CFT Policy is thoroughly implemented through Staff Training and Awareness.

The final step in drafting the AML/CFT Policy is that it is implemented, understood & executed in totality and not just kept on paper. Real Estate businesses, at this point, should state in their AML/CFT procedures how the company will conduct staff training to identify and mitigate risks to the Real Estate business.

The organisation’s AML/CFT Policy must be based on the outcome of the EWRA and must establish practices to train employees, accordingly.

Ready to Follow this Guide for Your Real Estate Business?

Draft an AML/CFT Policy that fits right for your business.

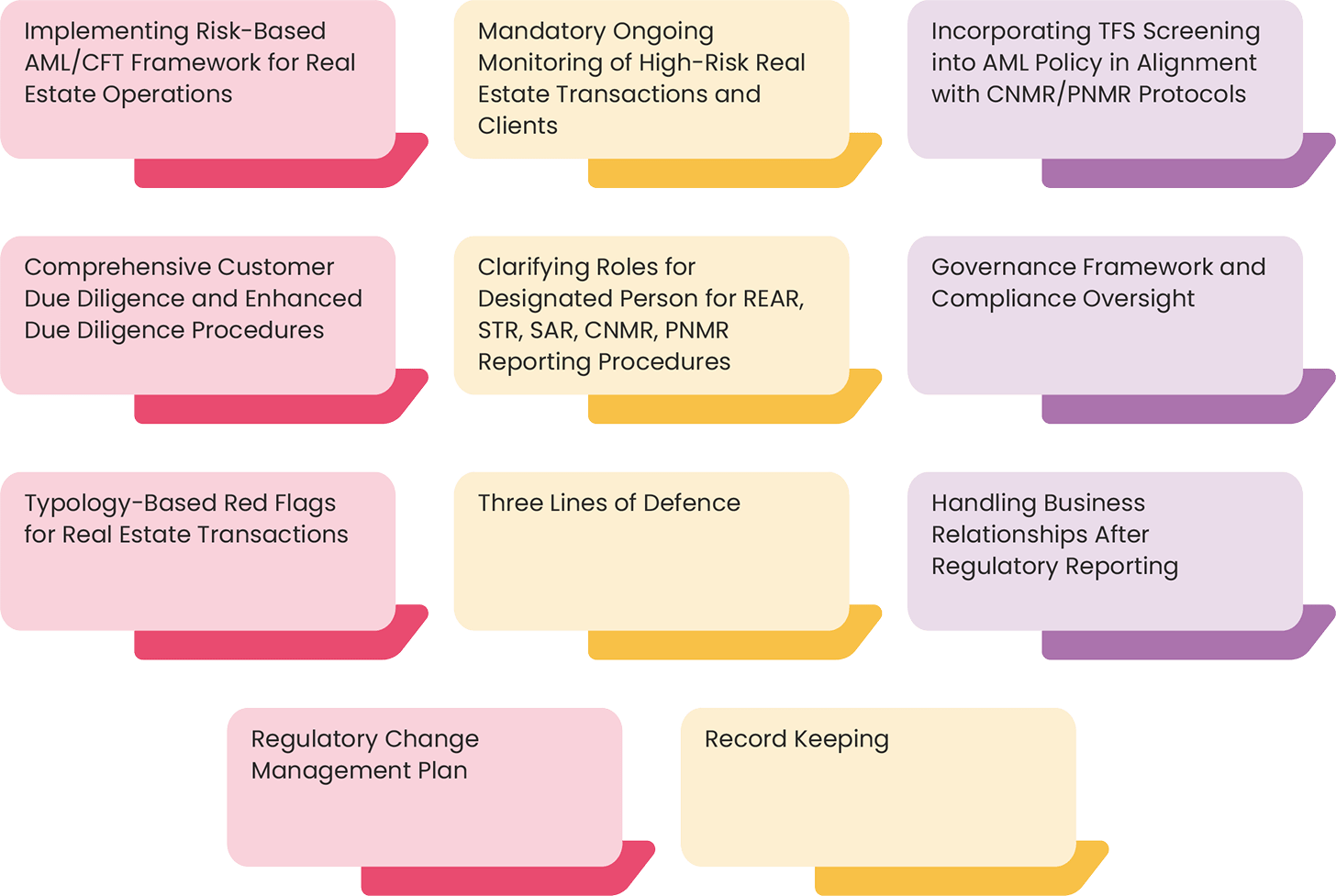

Must Have Elements in an AML/CFT Policy Manual for the Real Estate Sector

UAE Regulators such as MOET expect AML/CFT Policies of Real Estate Professionals to include Risk-Based Approach, Ongoing Monitoring requirements, implementation of TFS measures, CDD, EDD, Regulatory Reporting pathway, Real Estate sector specific typology based red flags, Governance framework along with compliance oversight and Record-keeping requirements.

AML/CFT Policy for Real Estate Sector comprises procedures for implementing a risk-based framework, ongoing monitoring, screening, reporting, record-keeping and governance. The must-have elements in an AML/CFT Policy are explained in detail below:

Implementing Risk-Based AML/CFT Framework for Real Estate Operations

An effective AML/CFT Policy must implement a risk-based approach in accordance with the specific Real Estate business. It should examine ML/TF risks that originate from high-value property transactions, customers from weak AML controls jurisdictions, complex ownership structures, etc.

The other risk areas include large cash deposits, third-party financing, non-face-to-face onboarding, and involvement of many intermediaries, which require a high level of controls.

Mandatory Ongoing Monitoring of High-Risk Real Estate Transactions and Clients

AML/CFT Policy must have a clear plan for performing ongoing monitoring for high-risk customers and transactions for the Real Estate business. This should include a timely check of the land registry to identify ownership changes, quick re-sales and multiple transactions.

For Real Estate business that acts as a trustee, fiduciary or secretarial role, they must have an AML/CFT Policy that specifies methods, tools, and means for conducting ongoing monitoring of financial documents related to the property.

Incorporating TFS Screening into AML Policy in Alignment with CNMR/PNMR Protocols

Real Estate businesses and professionals are required to screen all customers, be it individuals, business partners, UBOs, and even transactions against UN and UAE sanctions lists.

The screening process must be done before customer onboarding. For instance, if a Real Estate broker or agent finds their customer’s name on UAE or UN sanctions lists, the AML/CFT Policy should have proper workflow escalations regarding consequent reporting obligations.

Comprehensive Customer Due Diligence and Enhanced Due Diligence Procedures

An AML/CFT Policy for a Real Estate business must include clear procedures for Customer Due Diligence (CDD) and Enhanced Due Diligence (EDD). When onboarding customers, Real Estate must verify and check the risk associated with them.

This includes performing a comprehensive Know Your Customer (KYC), screening against Sanctions, PEP and Adverse Media, risk assessment and EDD for high-risk customers.

The AML/CFT Policy must mandate EDD under situations like dealing with PEPs, high-risk jurisdictions, shell companies, large or unusual transactions, rapid buying/selling, anonymous ownership, and others.

Clarifying Roles for Designated Person for REAR, STR, SAR, CNMR, PNMR Reporting Procedures

Another important must-have element in an AML/CFT Policy for Real Estate is clarifying roles and designating a responsible person for conducting reporting procedures. This means the policy must clearly define how employees are going to escalate suspicious activities or transactions to the AML CO.

The AML/CFT procedures must define plan of action to execute required internal review steps, confidentiality safeguards, timelines and submissions with goAML. By allotting roles for reporting procedures, the red flags can be detected successfully.

Governance Framework and Compliance Oversight

A robust AML/CFT Policy for Real Estate must include the appointment of an AML Compliance Officer who is competent, experienced, and independent to manage the complete AML/CFT Framework relating to Real Estate.

As instructed by the Supervisory Authority, the AML CO must perform operations at the management level, supervise program effectiveness, report suspicious transactions, staff training, and be free from conflicts of interest.

The AML CO ensures that risk management, governance, and compliance measures align with regulatory obligations. Further, the AML/CFT Policy must be consistent across all branches, and regular assessment should be performed to ensure compliance oversight.

Typology-Based Red Flags for Real Estate Transactions

The AML/CFT Policy must help understand common typologies used for ML/FT/PF activities by criminals and incorporate red flags when such techniques are used.

The typologies include the use of credit finance or complex loans, corporate vehicles, monetary instruments, non-financial professionals, mortgage schemes, investment schemes, and financial institutions.

AML/CFT Policy must warn of suspicious red flags to take effective measures for such customers. For instance, if any customer uses a monetary instrument for the purchase of real estate and it includes large cash payments or money transfers from a third-party account, clear signs for red flag identification must be incorporated.

Three Lines of Defence

The AML/CFT Policy for Real Estate should clearly define the three lines of defence mechanism that it is going to follow for protecting the business from ML/TF/PF risks.

This involves outlining the workflow and responsibilities of the front-line employees, Compliance Officer and Senior Management. For instance, the company may define the responsibilities of front-line staff as assessing risks from third parties and identifying suspicious transactions.

Another example says that it may define the responsibility of the Compliance Officer to be providing AML Policies, overseeing the AML function, investigating suspicious transactions and then filing SAR/STRs.

Handling Business Relationships After Regulatory Reporting

AML/CFT Policy must include measures to prevent ‘tipping off’ and manage business relationships after regulatory reporting. This includes training to front-line staff to identify suspicious behaviour, get proper information and support for reporting such customers without informing them about the reporting done.

This means that AML/CFT Policy must have mandatory rules for keeping strict confidentiality for reporting suspicious behaviours to regulatory bodies.

Regulatory Change Management Plan

Real Estate businesses need to modify their ML/TF/PF risk control measures to align with evolving regulatory changes. The AML/CFT Policy must have a regulatory change management plan to handle risks they may face due to updates in FATF Grey/Blacklists or other regulatory changes.

This includes recognising triggers, reassessing risk factors, reperforming EWRA, and revising the AML Policy with measures to implement changes and define post-implementation goals.

The AML/CFT Policy’s change management plan must also provide for updating changes in CRA parameters, performing re-KYC, EDD for new high-risk customers, staff training and evaluating if controls are implemented properly.

Record Keeping

Maintaining accessible and accurate records functions as a cornerstone of AML/CFT Compliance. A strong AML/CFT Policy should outline the record-keeping scope, covering everything from transaction details, customer information & documents, CDD procedures, ongoing monitoring, reports filed, and others.

This ensures traceability, regulatory preparedness, and confidence at times of investigations or audits. The main purpose of recordkeeping in the AML/CFT Policy Framework is to have a clear track of ongoing activities in the business.

Does Your Generic Policy Cover All These Critical Elements?

Your AML/CFT Policy should not be basic, but an implementation guide of business operations.

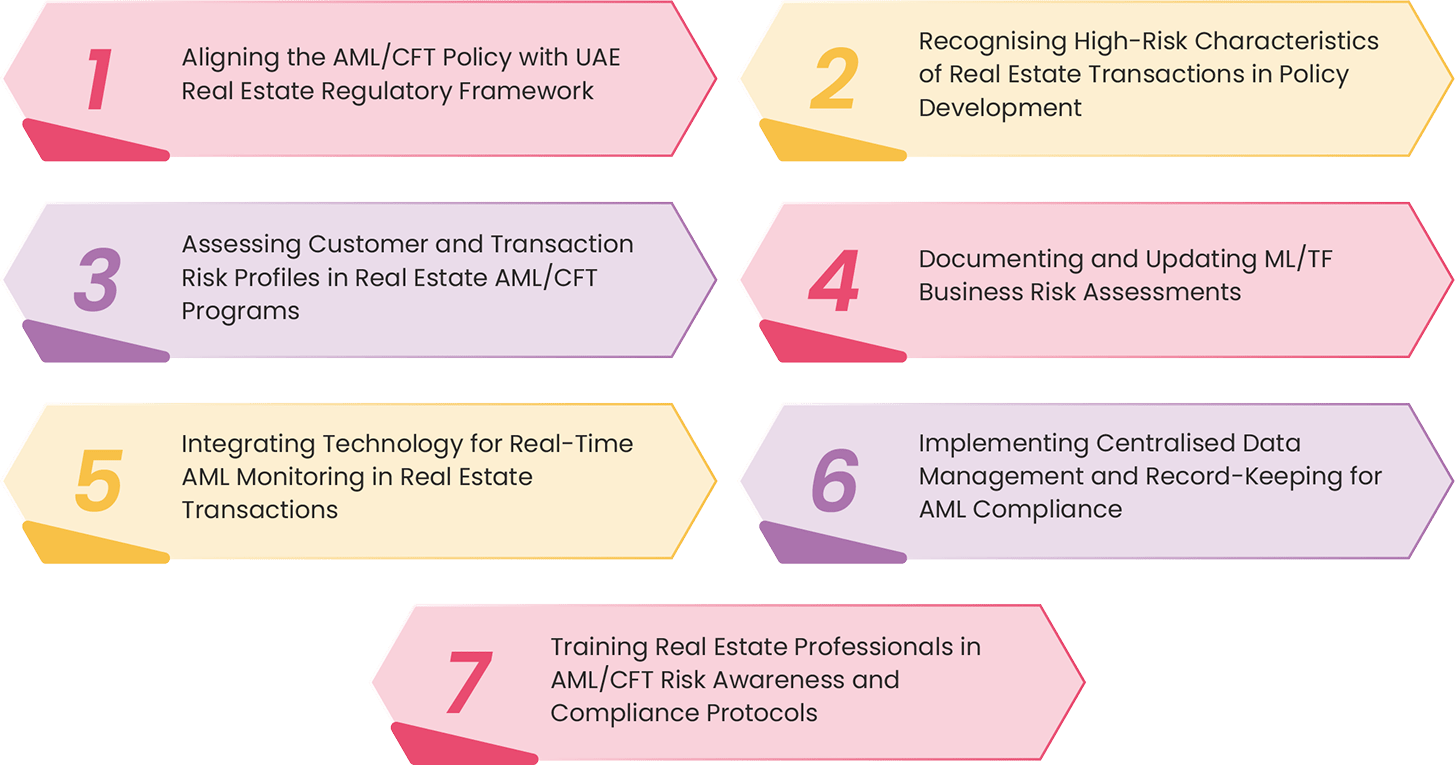

How to Design and Implement AML/CFT Policy for Real Estate Business: Best Practices

The Real Estate businesses should implement an AML/CFT Policy that aligns with UAE regulations, identifies risks, keeps records, trains staff, monitors transactions and integrates technology. The best practices for implementing AML/CFT Policy for the Real Estate Sector are clearly explained below:

1. Aligning the AML/CFT Policy with UAE Real Estate Regulatory Framework

The Real Estate business should draft an AML/CFT Policy that aligns with UAE laws and regulations, Cabinet Decisions, and Supplemental Guidance for Real Estate, comprising measures and workflows to deal with TFS, REAR and STR/SAR obligations.

The AML Policy should reflect adherence to Real Estate Sector obligations, such as sanctions compliance, due diligence, ongoing monitoring and record-keeping, while identifying typologies and reducing red flags to mitigate risks.

2. Recognising High-Risk Characteristics of Real Estate Transactions in Policy Development

The Real Estate sector may attract money launderers as they can easily hide illegal money through property purchase or sale. The common typologies that criminals may use to make their dirty money look clean are the use of cash, luxury property deals, complex ownership structures, high liquidity and rising prices, and openness to foreign purchasers.

Real Estate must design and implement an AML/CFT Policy that defines these typologies and fosters timely recognition of them while dealing with Real Estate transactions.

3. Assessing Customer and Transaction Risk Profiles in Real Estate AML/CFT Programs

Real Estate business requires assessing ML/TF/PF risks depending on their size and the nature of the business. However, they might use either the advanced method by providing risk scores or weightage, or term risk based on qualitative aspects, terming high, low and medium.

Real Estate business must draft their AML/CFT Policy that includes the appropriate method used and the reason for choosing it. Also, it must be mentioned that the same method is applied consistently for all customers and transactions.

4. Documenting and Updating ML/TF Business Risk Assessments

Real Estate businesses must design and implement their AML/CFT Policy in such a way that it ensures maintaining ML/TF risk assessment documents that outline the adopted methodology, risk policies, risk factors identified, analysis, roles and responsibilities, and reporting flows.

Further, it must include a review plan that ensures periodic risk assessments and updates must be made when changes arise.

5. Integrating Technology for Real-Time AML Monitoring in Real Estate Transactions

Real Estate business must also incorporate into its AML/CFT Policy the use of technology for performing screening, KYC, transaction monitoring and record-keeping.

The focus should be on using a technology or AML Software that provides real-time updates to reduce gaps and ensure compliance with AML/CFT laws and regulations. This helps the Real Estate business to reduce human errors, improve efficiency in workflows, and allows real-time monitoring of Real Estate transactions.

6. Implementing Centralised Data Management and Record-Keeping for AML Compliance

Real Estate agents and brokers must incorporate in their AML/CFT Policy a centralised data management and record-keeping procedure for AML Compliance.

It should ensure storing customer records, KYC documents, transaction details and screening results securely in one place. Maintaining complete and accurate records strengthens data integrity, reduces duplication, ensures efficient monitoring and makes the Real Estate business audit ready.

7. Training Real Estate Professionals in AML/CFT Risk Awareness and Compliance Protocols

Real Estate businesses must include an effective training procedure for employees on ML/TF risks in their AML/CFT Policy. They must ensure covering KYC & screening procedures, red flag indicators, record-keeping and reporting obligations.

The training content must be updated periodically to acknowledge recent regulations and typologies. Further, the AML/CFT training component must be tailored according to different roles for proper understanding. AML Training effectiveness must be measured to assess its efficacy.

These best practices together enable Real Estate businesses to develop and maintain AML/CFT policy that is fully compliant with UAE’s regulatory requirements and tailored to the Real Estate sector-specific requirements.

A well-structured AML/CFT policy with the adoption of these best practices integrates Real Estate sector-specific regulatory requirements, risk assessment, technology advancements, documentation, data management, record-keeping and training mandates, that enables timely risk mitigation and regulatory readiness.

Turn Best Practices into Actionable AML/CFT Policy.

Don’t wait for regulators to hit your door with heavy penalties.

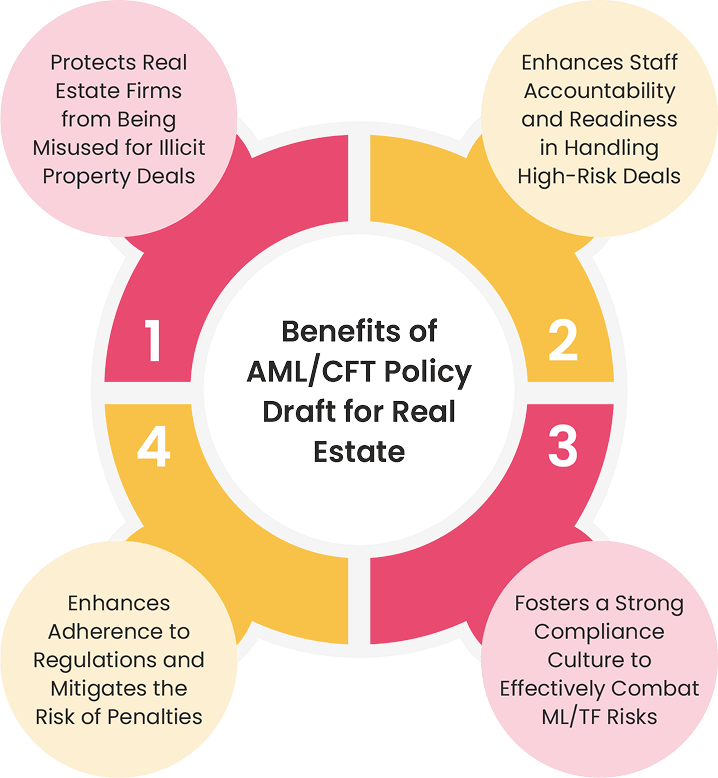

Benefits of a Professionally Drafted AML/CFT Policy for Real Estate

Real Estate businesses gain numerous benefits from a professionally drafted AML/CFT Policy, which includes safeguarding from misuse, adherence to regulations, enhancing staff accountability, and fostering a compliance culture.

Unlike generic AML templates, a customised AML/CFT Policy for Real Estate sector addresses the unique risks associated with high value property transactions, cash intensive payments, cross-border or non-resident transactions and diverse customer profiles.

The information below provides a detailed overview of these benefits:

1. Protects Real Estate Firms from Being Misused for Illicit Property Deals

Weak compliance opens the gates to criminals to misuse the Real Estate Sector for illicit deeds disguised as property deals. A customised AML/CFT Policy draft for the Real Estate business protects the firm on every stage, be it onboarding, monitoring, and handling transactions, ensuring that the ML/FT and PF risk is managed, and misuse of business is prevented.

The AML Policy acts as a shield that helps the Real Estate business reject business relationships that are risky and safeguards it from financial loss and regulatory as well as administrative penalties.

2. Enhances Staff Accountability and Readiness in Handling High-Risk Deals

A robust AML/CFT Policy helps to define tasks for each team member to ensure AML Compliance with efficiency. The AML/CFT Policy draft specifies training requirements, roles, and decision-making authority.

This clarity in roles and responsibilities ensures a risk-based response to red flags, and mitigation measures to be applied. A well-drafted AML Policy helps compliance team to share responsibility, reduce errors, and provide a stronger defence.

3. Fosters a Strong Compliance Culture to Effectively Combat ML/TF Risks

A well-drafted AML/CFT Policy for the Real Estate business fosters a strong internal culture where all employees stand collectively to combat ML/TF/PF risks. It demonstrates approval, support and encouragement by senior management or board members to uphold laws, internal policies, regulations, and ethical standards in business practices.

This signifies that the Real Estate business or professional doesn’t superficially abide by AML Compliance but embeds compliance into its core values and practices.

4. Enhances Adherence to Regulations and Mitigates the Risk of Penalties

An effective AML/CFT Policy helps the Real Estate businesses to meet current and sector-specific AML compliance requirements. It includes every legal requirement and structured procedures for fulfilling them, be it due diligence, ongoing monitoring or timely regulatory reporting.

This ensures adherence to regulations and mitigates the risk of penalties. The AML/CFT Policy draft mirrors the exact operations which demonstrate Real Estate activeness in managing ML/FT risks, instead of using a generic template just to display laws followed.

Secure Your Business with Right AML/CFT Policy

A professionally drafted AML/CFT policy for the real estate sector comprises of essential elements such as Real-Estate sector-specific risk assessment, risk mitigation strategy, Risk-Based CDD and EDD requirements, high-risk client and property transactions management, clear escalation and Regulatory Reporting pathway, robust Record-Keeping, effective use of technology and position-based staff training.

A strong AML/CFT Policy draft for the Real Estate Sector is a backbone for effective business operations, complying with AML/CFT regulations. Real Estate businesses can prevent ML/TF/PF risks by focusing on sector-specific risk factors, forming governance, strong internal controls and continuous monitoring.

This helps the Real Estate businesses to ensure adherence with regulatory obligations, perform operations confidently, and maintain a strong posture in the economy.

Ensure AML Compliance the Right Way.

Secure your Real Estate business with a customised AML/CFT Policy.

Frequently Asked Questions on AML/CFT Policy Drafting Service for Real Estate Professionals

Do real estate businesses need an AML/CFT policy in the UAE?

Yes, Real Estate businesses need an AML/CFT policy in the UAE when they carry out activities on behalf of their customers regarding the purchase or sale of the real estate.

What is an AML/CFT policy drafting service for real estate?

AML/CFT Policy drafting service of real estate is professional assistance in preparing a customised AML/CFT Policy as per the Real Estate sector-specific regulatory requirements of AML/CFT compliance in UAE.

Why is the real estate sector high risk for money laundering?

Real Estate sector particularly is high-risk for Money Laundering due to its high-value property transactions, market stability and ease of using intermediaries or third parties. It is one of the attractive sectors for money launderers to layer illicit funds.

What must a real estate AML/CFT policy include?

A real estate AML/CFT policy must include key elements such as risk identification and mitigation, Real Estate sector-specific red flags, Risk-Based CDD and EDD, Transaction Monitoring requirements, high-risk client management, Sanctions Screening, TFS measures implementation rules, customer onboarding and exit policy, cash acceptance rules, Regulatory Reporting pathway, strong Record-Keeping, role-based staff training and periodic policy review clauses, in sync with the UAE’s AML/CFT Laws.

When should REAR be filed instead of STR/SAR?

In Real Estate sector, Real Estate Brokers and Agents are required to submit Real Estate Activity Report (REAR) when freehold property transactions are settled in cash that equals or exceeds AED 55,000 or in virtual currencies. However, REAR is distinct from STR/SAR.

STR/SAR filing is applicable to all Regulated Entities in UAE for reporting suspicious activities or transactions.

How long must real estate AML/CFT records be retained?

AML/CFT records in Real Estate sector must be retained for at least 5 years as per the UAE’s AML/CFT laws in UAE mainland. For Real Estate entities in DIFC and ADGM, the record-keeping requirements is for 6 years.