Misappropriation of Public Funds

Last Updated: 06/26/2026

Protect your business with reliable and effective AML strategies with AML UAE.

Misappropriation of Public Funds - At a Glance

State assets diverted by a public official may generate proceeds of a predicate offence where the underlying conduct amounts to a felony or misdemeanour under applicable UAE law, or a qualifying foreign offence satisfying the conditions in Federal Decree by Law No. (10) of 2025 (FDL 10/2025). Regulated entities that fail to apply PEP enhanced due diligence face significant regulatory penalties. Take reasonable measures to identify source of wealth and source of funds for foreign PEPs and high-risk domestic or international-organisation PEPs, with independent verification where the risk profile requires it, and file STRs immediately when account patterns suggest fund diversion.

Misappropriation of public funds occurs when a public official diverts state money, property, or assets for personal benefit or for another person or entity. In AML compliance, the risk arises when the proceeds are moved through banks, real estate, companies, trusts, money services businesses, or professional advisers. UAE-regulated entities should assess PEP exposure, take reasonable measures to identify source of wealth and source of funds where required, support higher-risk files with independent verification, monitor unusual transactions, and file an STR without delay where suspicion or reasonable grounds arise.

Who should read this article? This article is useful for MLROs, compliance officers, DNFBPs, financial institutions, real estate firms, TCSPs, lawyers, accountants, DPMS businesses, VASPs, and senior managers responsible for PEP risk, source-of-wealth verification, beneficial ownership review, and STR filing in the UAE.

What is Misappropriation of Public Funds?

The United Nations Convention Against Corruption (UNCAC), Article 17, defines this conduct as the intentional embezzlement, misappropriation, or other diversion by a public official of property, public or private funds, securities, or any other thing of value entrusted to that official by virtue of their position, for the official’s own benefit or for the benefit of another person or entity.

In the context of anti-money laundering, misappropriation of public funds may constitute a predicate offence capable of generating criminal proceeds that are subsequently laundered through the financial system. FDL 10/2025 criminalises any attempt to convert, transfer, conceal, disguise, acquire, possess, or use such proceeds in the UAE, regardless of where the underlying theft occurred.

The proceeds of public fund misappropriation are often substantial, long-standing, and protected by the political influence of the perpetrator. This combination makes detection significantly more difficult than for conventional financial crime.

Regulatory Framework related to Misappropriation of Public Funds

The UAE regulatory framework addresses misappropriation of public funds through two intersecting pillars: the criminalisation of money laundering derived from predicate offences, and the enhanced customer due diligence obligations triggered by politically exposed person (PEP) status.

FDL 10/2025, Article 2 criminalises money laundering in four forms, including the conversion, transfer, concealment, and acquisition of proceeds derived from any predicate offence. Misappropriation of public funds generates proceeds of a predicate offence where the underlying conduct amounts to a felony or misdemeanour under applicable UAE law, or a qualifying foreign offence satisfying the conditions in FDL 10/2025; corruption and bribery are recognised under UAE predicate-offence analysis and fall within FATF’s designated categories of offences, and such proceeds may then become the subject of money laundering under Article 2.

Cabinet Resolution No. (134) of 2025, Article 16 establishes the specific obligations applicable to PEPs. Foreign PEPs are subject to the specified enhanced measures, including senior management approval, source-of-funds and source-of-wealth measures, and enhanced ongoing monitoring. Domestic PEPs and PEPs of international organisations are subject to those measures where the business relationship is assessed as high risk.

FATF Recommendation 12 requires countries and their regulated sectors to apply enhanced due diligence measures to foreign PEPs and to take reasonable measures regarding domestic PEPs and PEPs from international organisations. The UAE framework reflects this Recommendation 12 structure.

Politically Exposed Persons: Foreign vs Domestic Obligations

| Requirement | Foreign PEP | Domestic PEP / international-organisation PEP |

| Risk classification | Treated as high risk in all cases | Risk-assessed; enhanced measures apply where the relationship is high risk |

| Senior management approval | Required before establishing and to continue the relationship | Required where the relationship is high risk |

| Source of wealth and source of funds | Take reasonable measures to identify, with independent verification proportionate to the risk | Take reasonable measures to identify source of funds and source of wealth where the relationship is high risk, with verification proportionate to the risk |

| Enhanced ongoing monitoring | Required in all cases | Required where the relationship is high risk |

| Legal basis | CR 134/2025 Article 16; FATF Recommendation 12 | CR 134/2025 Article 16; FATF Recommendation 12 |

Legal Basis at a Glance

| Instrument / Provision | What it covers |

| UNCAC, Article 17 | International definition of embezzlement and misappropriation of public funds by a public official |

| FDL 10/2025, Article 1 | Key definitions, including beneficial owner, proceeds, and suspicious transactions |

| FDL 10/2025, Article 2 | Money laundering offence: conversion, transfer, concealment, and acquisition of predicate-offence proceeds |

| FDL 10/2025, Article 18 | STR obligation to the UAEFIU; professional secrecy carve-out for legal professionals |

| CR 134/2025, Article 10 | Beneficial ownership identification (25% threshold; control and senior-managing-official fallbacks) |

| CR 134/2025, Article 16 | PEP obligations: senior management approval, source of wealth and source of funds, enhanced monitoring |

| CR 134/2025, Article 18 | STR filing procedure via goAML; professional secrecy carve-out |

| CR 134/2025, Article 25 | Record-keeping: minimum of five years |

Supervisory Body

The Central Bank of the UAE (CBUAE) supervises licensed financial institutions for AML/CFT compliance, including banks, exchange houses, finance companies, insurance companies, payment service providers, and registered hawala providers, and applies PEP due diligence requirements.

The Ministry of Economy and Tourism (MOET) supervises designated non-financial businesses and professions (DNFBPs), including real estate agents, dealers in precious metals and stones, accountants, and trust and company service providers.

The Ministry of Justice (MoJ) supervises lawyers, notaries, and independent legal professionals.

In the financial free zones, the Dubai Financial Services Authority (DFSA) supervises entities in the DIFC and the Financial Services Regulatory Authority (FSRA) supervises entities in the ADGM.

The Capital Market Authority (CMA) supervises securities and capital-market activities, and the General Commercial Gaming Regulatory Authority (GCGRA) supervises the commercial gaming sector.

The UAE Financial Intelligence Unit (UAEFIU), established as an independent unit within CBUAE under FDL 10/2025 Article 11, is the sole recipient of all suspicious transaction reports from regulated entities. STRs must be filed with the UAEFIU immediately and without delay through its electronic reporting system, currently goAML, or any other channel the FIU approves.

At the international level, the United Nations Office on Drugs and Crime (UNODC) serves as the custodian of the UNCAC framework, which provides the primary global standard for preventing, criminalising, and combating corruption, including the misappropriation of public funds.

Reporting or Compliance Obligations and Channels of Misappropriation of Public Funds

Any regulated entity that suspects a customer is a PEP involved in the diversion of public funds must file a Suspicious Transaction Report immediately and without delay through the UAEFIU’s electronic reporting system, currently goAML, or any FIU-approved channel, as required by FDL 10/2025 Article 18 and Cabinet Resolution No. (134) of 2025 Article 18. Filing must occur regardless of whether a transaction has been completed, merely attempted, or declined.

In addition to STR obligations, regulated entities must apply the specified enhanced measures to foreign PEPs under CR 134/2025 Article 16, and apply enhanced measures to domestic PEPs and PEPs of international organisations where the business relationship is assessed as high risk. An entity may, as a matter of internal risk appetite, treat all PEP relationships as high risk, but that is a policy choice rather than a uniform legal requirement.

For those PEP relationships to which the specified enhanced measures apply, this includes obtaining senior management approval before establishing or continuing the relationship, taking reasonable measures to identify source of funds and source of wealth, and applying enhanced ongoing monitoring for the duration of the business relationship.

Records must be maintained for a minimum of five years from the end of the business relationship under CR 134/2025 Article 25.

Legal professionals should also consider the professional secrecy carve-out where applicable. Lawyers, notaries, other independent legal professionals, and independent legal auditors are not required to file an STR where the relevant information was obtained in circumstances subject to professional secrecy, such as assessing a client’s legal position or representing the client in legal proceedings, under FDL 10/2025 Article 18 and CR 134/2025 Article 18. This does not remove AML obligations generally; it affects the reporting obligation in those protected contexts.

Once a suspicion arises, the entity and its staff must not disclose to the customer or any third party that a Suspicious Transaction Report has been or may be filed, or that an investigation is underway. This tipping-off prohibition applies under FDL 10/2025 Article 29 and CR 134/2025 Article 19, and is the reason an entity should not seek clarification from the customer in a way that reveals the reporting concern.

Recent Developments, Enforcement Actions, or Supervisory Priorities

The UAE’s second National Risk Assessment (NRA 2024) identifies fraud as a High ML threat, with corruption proceeds and foreign predicate offences constituting a significant component of illicit funds entering the UAE financial system. The NRA confirms that legal persons and corporate structures remain a Medium-High vulnerability for beneficial ownership concealment, directly relevant to the layering techniques used in misappropriation schemes.

Supervisory priorities for 2025 to 2026 include strengthening DNFBP compliance, improving beneficial ownership data quality, and enhancing financial intelligence on PEP-linked transactions.

FDL 10/2025, which entered into force on 14 October 2025, replaces the previous AML statute and consolidates criminal and administrative penalties into a single framework. Its Executive Regulation, Cabinet Resolution No. (134) of 2025, took effect on 14 December 2025. The maximum administrative fine for a single AML/CFT violation is now AED 5,000,000 under Article 17.

REGULATORY REFERENCE

FDL 10/2025, Article 1 (definitions); Article 2 (money laundering criminalisation; predicate offences); Article 18 (STR obligation); Article 19 (preventive measures); Article 28 (penalty for STR failure); Article 29 (tipping-off); Cabinet Resolution No. (134) of 2025, Article 10 (beneficial ownership); Article 16 (PEP enhanced due diligence obligations); Article 18 (STR filing procedure); Article 25 (record-keeping); UNCAC Article 17 (Misappropriation, embezzlement or diversion by a public official)

What does Misappropriation of Public Funds Mean?

Think of a trusted employee who manages the petty cash box in an office. Everyone assumes the money is safe because they are the designated custodian. Over time, this person removes notes one at a time, replaces cash receipts with forged ones, and eventually moves the money into their own wallet. Now scale that to a government budget worth hundreds of millions of dirhams, controlled by a single minister or procurement director. That is misappropriation of public funds: the abuse of a position of official trust to redirect state money for personal enrichment.

Why Detecting Misappropriation of Public Funds Matters

The financial damage caused by misappropriation of public funds is rarely contained within the originating jurisdiction. Proceeds move swiftly through the international financial system, exploiting gaps in PEP due diligence, weak beneficial ownership transparency, and the ability of professional enablers to create opaque holding structures. Any regulated entity that accepts, manages, or facilitates financial activity for a foreign PEP, a high-risk domestic PEP, a high-risk international-organisation PEP, or any PEP treated as high risk under its internal policy, without applying the specified enhanced measures under CR 134/2025 Article 16, faces potential regulatory penalties and the risk of becoming an unwitting conduit for stolen state assets.

The professional enablers who help structure misappropriation proceeds, including lawyers who establish nominee companies, accountants who certify false financial statements, and real estate agents who facilitate property purchases with unexplained funds, face criminal exposure under FDL 10/2025 alongside the principal perpetrators. The absence of a direct employee relationship with a corrupt official offers no protection where professional services are rendered knowingly or recklessly. A transaction processed for a PEP without documented, verified source-of-wealth evidence may create supervisory concern, particularly where the customer is a foreign PEP or the relationship is otherwise high risk.

How Does Misappropriation of Public Funds Facilitate Money Laundering?

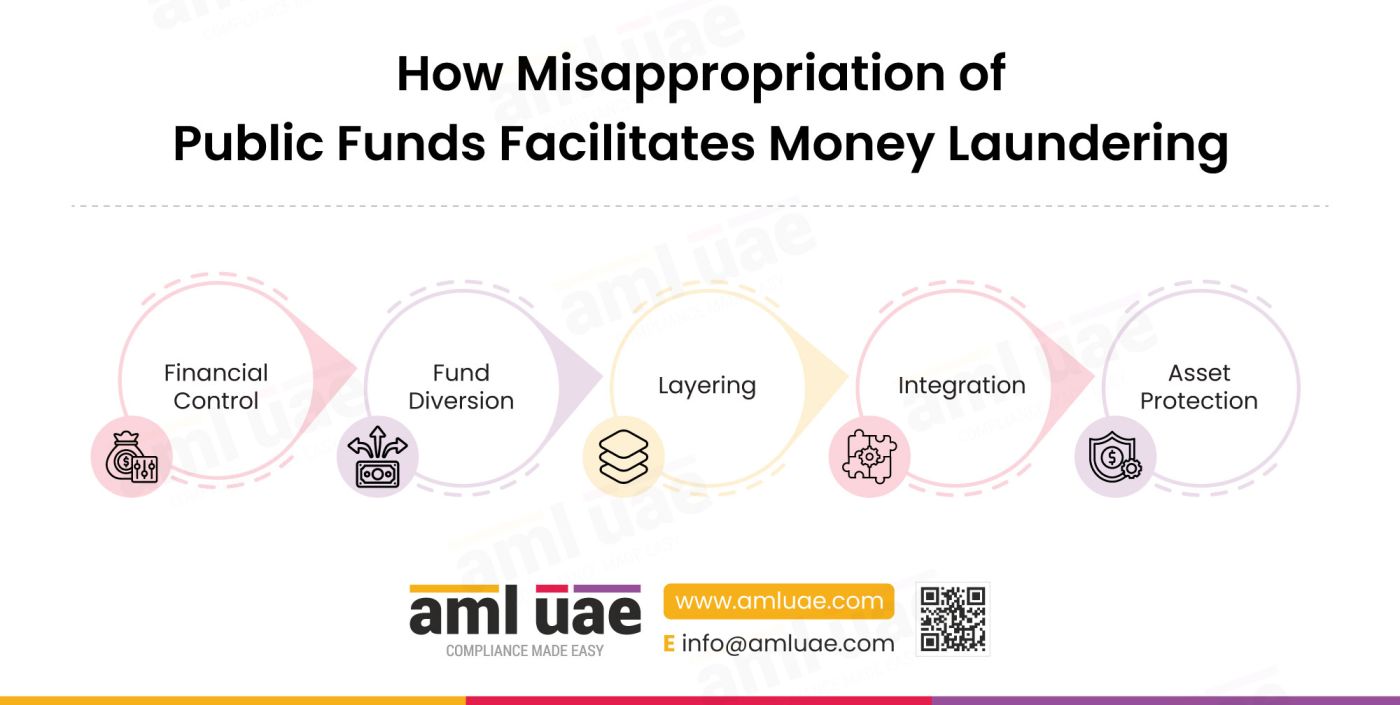

Misappropriation of public funds operates as a structured, multi-stage scheme rather than a spontaneous act of theft. Each stage is designed to increase the distance between the perpetrator and the stolen funds, while simultaneously creating a surface appearance of legitimacy.

Stage 1: Establishing a Position of Financial Control

The scheme begins when a public official or employee gains control over government financial processes. This control may be legitimate, such as a procurement director with authority to approve contracts up to a defined threshold, or it may be acquired through corruption or appointment by a complicit superior. Centralisation of financial authority in a single individual, with minimal oversight, is the structural precondition for misappropriation.

Stage 2: Diverting the Funds

Once financial authority is established, the official activates one or more diversion mechanisms. Common methods include approving payments to fictitious or shell vendors for services never rendered, inflating contract values and routing the excess to controlled accounts, submitting false expense claims against a government budget line, creating ghost employees on a public payroll, or directly transferring funds to personal accounts during brief windows when oversight is reduced. Business entities and money services businesses are frequently used as conduits at this stage.

Stage 3: Layering to Obscure Origin

After extraction, the proceeds are subjected to layering techniques designed to sever the audit trail. This may involve converting funds into cash, foreign currency, or cryptocurrency; routing through multiple bank accounts held in different names; using DNFBPs such as law firms and company formation agents to establish shell or front companies that receive the funds; and making real estate purchases that generate paper trails appearing to reflect legitimate investment. Shell and front companies are a primary vehicle at this stage.

Stage 4: Integration into the Legitimate Economy

Integration occurs when the layered funds are reintroduced into the economy in a form that is difficult to distinguish from legitimate wealth. A PEP who has misappropriated state funds may invest in commercial real estate, acquire equity stakes in operating businesses, fund luxury asset purchases, or transfer assets to family members and close associates to place them further from scrutiny. Trust beneficial interests and offshore banking services are routinely used at this stage.

Stage 5: Asset Protection and Insulation

The final stage involves protecting the integrated assets from confiscation or recovery proceedings. This is typically achieved through layered corporate structures, trusts settled in secrecy jurisdictions, nominee directors and shareholders, and ongoing use of professional advisers who maintain the appearance of legitimate business activity. The offshore structure creates a legal barrier that requires extensive international cooperation to penetrate.

Illustrative Typology Scenarios of Misappropriation of Public Funds

The following scenarios are constructed from documented typologies and do not represent specific named individuals or cases. They illustrate how the mechanics described in Block 5 manifest in practice.

The Inflated Procurement Scheme

A senior procurement official at a national infrastructure ministry maintains authority to approve contracts up to USD 15 million without secondary sign-off. Over a period of three years, this official awarded a series of contracts to a limited liability company.

The company’s registered beneficial owner is a nominee, while the official’s sibling holds the equity interests. Invoices are submitted for consulting services with no deliverables verified. Payments are received in the company’s account, converted to foreign currency, and transferred to an offshore banking account held in the name of a trust.

A real estate agent later facilitates the purchase of two residential properties by the trust, presenting certified accounts from an accountancy firm as evidence of commercial income.

No PEP check is conducted because the purchase is made through the trust rather than in the official’s personal name. Detection occurs only when a foreign jurisdiction’s asset recovery team requests information on the trust.

Operational lesson: Trusts and nominee structures routinely obscure PEP connections. Source-of-wealth verification must pierce the corporate veil at every customer layer, not just at the direct customer level.

The Ghost Payroll Operation

A human resources manager at a state-owned enterprise controls employee registration and payroll processing. Over eighteen months, this manager creates 40 fictitious employee records, directing salary payments to a cluster of bank accounts that the manager controls through power of attorney arrangements.

The accounts are held at different financial institutions to avoid triggering a single-bank threshold alert. Funds are periodically aggregated through a money services business and wired to a foreign account, which is then used to purchase luxury goods and real estate in a third country. The scheme unravels during an internal financial audit when the fictitious employees cannot be matched to physical workspace records.

Operational lesson: Segregation of duties failures are the structural vulnerability that enables payroll fraud. Compliance teams at financial institutions should scrutinise frequent, regular, identically structured transfers to newly opened accounts held by individuals with no verifiable employment history.

The Emergency Procurement Override

A local government official exploits an emergency procurement protocol during a public health crisis to award contracts without competitive tender. Approved suppliers receive payments at double the market rate. The overpayment is routed to a business entity that the official controls through a silent equity interest. The entity converts the funds through currency exchange services, purchases real estate, and ultimately sells the property to a third party.

Transaction monitoring alerts generated by the original payments are cleared as routine government procurement. Post-clearance review later identifies that the counterparty entity had no prior operating history and no verifiable employees.

Operational lesson: Regulatory urgency or crisis conditions are frequently exploited to bypass oversight controls. Financial institutions serving government agencies or contractors should treat emergency procurement transactions as elevated-risk regardless of the official source of funds.

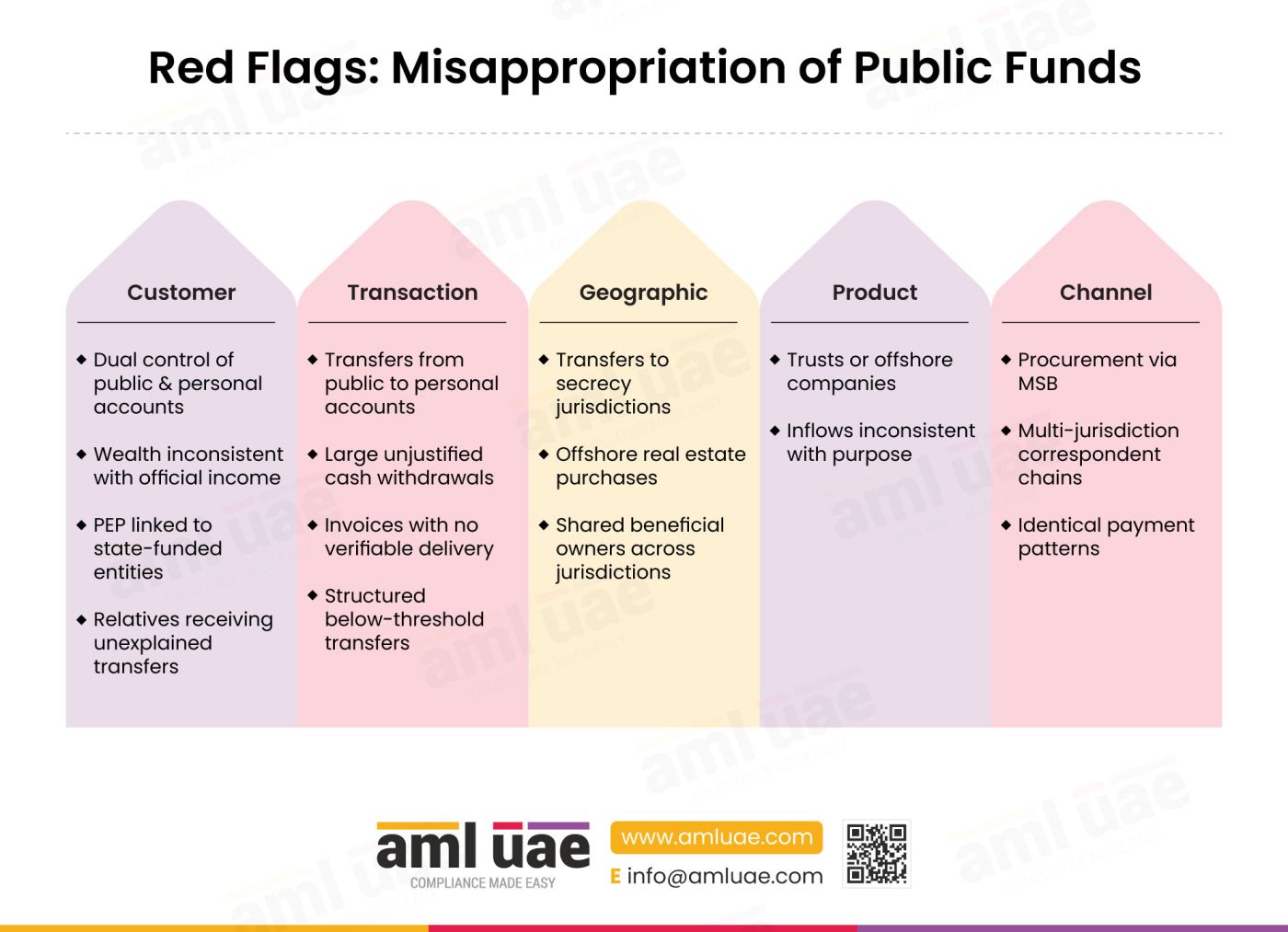

What Are the Red Flags That Identify Misappropriation of Public Funds?

The following red flags are observed behaviours and account patterns. Each is an observation, not a conclusion. The presence of one or more indicators should trigger enhanced scrutiny and, where suspicion arises, an STR via goAML.

Category | Red Flag |

Customer | A public official or PEP holds signature authority over government accounts and also controls personal or corporate accounts at the same institution |

Customer | A customer’s declared source of income as a public official is inconsistent with the value and frequency of their personal transactions |

Customer | An individual listed as a PEP holds equity interests in entities that receive government contracts or public funds |

Customer | A public official resigns or is dismissed shortly after an internal audit identifies anomalous transactions in their area of responsibility |

Customer | A customer declares asset holdings in a formal asset declaration that are materially inconsistent with their financial activity at the institution |

Customer | Close relatives or associates of a public official open accounts and begin receiving large regular transfers with no verifiable commercial justification |

Transaction | Transfers are made from a government or public entity account to personal accounts held by an official who has signing authority over that account |

Transaction | Large cash withdrawals are made from an account linked to a public entity, lacking operational justification in the entity’s business profile |

Transaction | Payments are made to vendors whose invoices describe services with no verifiable delivery, with amounts just below approval thresholds |

Transaction | Structured transactions are made across multiple accounts in amounts that individually fall below reporting thresholds but collectively reflect a pattern of diversion |

Transaction | Frequent large-value foreign currency exchanges are conducted by a public official with no legitimate trade or operational purpose |

Transaction | Accounts receivable records reflect payments from a government entity to a company that has no employees, no premises, and no prior commercial activity |

Geographic | Funds are transferred from a domestic public entity account to bank accounts in jurisdictions with strong secrecy laws, limited BO transparency, or known ML risks |

Geographic | A PEP or their close associate makes repeated real estate purchases in jurisdictions commonly used to hold offshore wealth |

Geographic | Wire transfer recipients in multiple jurisdictions share a common beneficial owner who is related to or associated with a domestic public official |

Product | Trust structures, offshore companies, or nominees are inserted into the ownership chain of assets acquired shortly after a public official is known to have had access to large funds |

Product | Accounts managed on behalf of a trust or foundation show inflows inconsistent with the stated purpose of the arrangement |

Channel | Government procurement payments are routed through a money services business rather than a regulated bank account |

Channel | Transactions linked to public funds are processed through correspondent banking chains in multiple jurisdictions before reaching a final destination account |

Channel | Multiple accounts at different institutions, each under different registered controllers, display identical payment patterns linked to a single government source |

Which Controls Counter Misappropriation of Public Funds?

|

Control |

What it disrupts |

Detects / Prevents / Deters |

Specific Limitation |

|

Enhanced Due Diligence (EDD) for PEPs |

Identification of beneficial owners connected to public office |

Detects and surfaces the official link before the relationship is established |

Effective only where PEP lists are comprehensive and up to date; domestic PEPs are often under-screened |

|

Customer Due Diligence (CDD) with source-of-wealth verification |

Use of nominees and trusts to mask PEP connection |

Detects and forces documentation of wealth origin |

Relies on the accuracy of declarations; fabricated documentation is not always detectable at onboarding |

|

Ongoing Due Diligence and account monitoring |

Concealment of fund diversion over time |

Detects and identifies transaction patterns inconsistent with the customer’s verified profile |

Alert thresholds may be set too high to catch structured transactions below reporting levels |

|

Sanctions and Watchlist Screening |

Use of sanctioned entities or sanctioned jurisdiction structures |

Prevents and blocks relationships with designated persons |

Covers only listed individuals; corrupt officials not yet sanctioned will not trigger alerts |

|

OSINT and External Source Verification |

Validation of declared sources of wealth against publicly available information |

Detects cross-references to asset declarations, corporate registry data, and adverse media |

Coverage is incomplete in jurisdictions with limited public records |

|

Transaction Monitoring |

Real-time detection of unusual payment flows |

Detects and deters; generates alerts on structuring, unusual counterparty patterns, and disproportionate fund volumes |

Rules-based monitoring can be gamed by anyone with knowledge of the alert thresholds |

|

Trade Monitoring |

Detection of inflated procurement or false invoicing |

Detects and surfaces mismatches between payment values and verified market rates |

Requires sector-specific market knowledge; generic monitoring rules lack the granularity needed |

|

Service Restriction |

Prevention of the account being used as a diversion vehicle once red flags are confirmed |

Prevents and deters; removes the regulated entity as a channel |

Only effective once suspicion is already established; it does not prevent earlier stages of the scheme |

|

Staff AML Training |

Recognition of PEP-linked red flags at the frontline |

Deters; trained staff are less likely to be complicit or to miss indicators |

Training must be scenario-specific; generic AML awareness does not equip staff to identify PEP misappropriation patterns |

How Do AI and RegTech Automate Detection of Misappropriation of Public Funds?

Detection of misappropriation of public funds requires monitoring systems that can connect identities, relationships, and transaction patterns across multiple data dimensions simultaneously. Rules-based transaction monitoring alone is insufficient because the perpetrators of these schemes are typically aware of the reporting thresholds and structure their activity accordingly.

Network analytics and graph technology are the most effective automated tools for detecting the relationship patterns that characterise misappropriation. Graph analytics platforms map connections between customers, counterparties, corporate entities, and beneficial owners, surfacing situations where a public official, their relatives, or entities linked to their equity interests appear in payment chains originating from government accounts. These systems can identify non-obvious links that would never be captured by a single customer-level rule.

Behavioural analytics and machine learning anomaly detection operate by establishing a baseline of expected account activity for each customer segment, including public officials and PEP-adjacent relationships. Machine learning models identify deviations from that baseline, such as a sudden increase in account activity following an appointment to a senior public position, or a change in payment counterparty profiles after a procurement cycle. These models are particularly effective for detecting the early-stage diversion patterns that rules-based systems miss.

Natural language processing (NLP) for adverse media monitoring continuously scans news sources, court filings, regulatory announcements, and open-source intelligence in multiple languages to identify adverse media references linked to customer names, entities, or related parties. For PEPs involved in misappropriation, adverse media often emerges in foreign-language sources or local-jurisdiction media before it reaches international databases. NLP systems that process multi-language feeds in near real time significantly reduce the lag between a public event and a compliance response.

Automated PEP screening platforms use regularly updated databases to perform continuous screening, not only at onboarding but throughout the life of the business relationship. Automated screening platforms reduce the manual effort of PEP identification and ensure that changes in a customer’s political status are captured promptly, triggering an EDD review when a customer is newly designated as a PEP.

Document verification and identity proofing technology examines the integrity of source-of-wealth documentation, cross-referencing declared asset values against public records, corporate registries, and real estate databases. These tools identify inconsistencies between declared wealth and documented holdings, surfacing a critical red flag for misappropriation schemes that rely on false wealth narratives.

What Data Should Compliance Teams Collect to Detect Misappropriation of Public Funds?

|

Data Point |

Source System |

What it Reveals |

|

PEP status and screening result |

PEP screening platform, watchlist database |

Whether the customer holds or has held public office triggers EDD obligations. |

|

Account activity logs |

Core banking/transaction monitoring |

Patterns of transfers to personal accounts from government entity accounts, structured withdrawals, and unusual counterparty activity |

|

Asset declarations |

Customer-provided documentation, OSINT |

Declared official assets; discrepancy with observed financial activity suggests undisclosed wealth from diverted funds |

|

Bank account data |

Core banking |

Account opening patterns, signatories, linked accounts, and payment counterparties that indicate PEP-connected structures |

|

Company and beneficial ownership registries |

Corporate registry OSINT, KYC platform |

Whether the customer or their associates control corporate vehicles that receive government payments |

|

Contractual and invoice data |

Document management system, trade finance platform |

Whether invoices from vendors receiving government payments have verifiable service deliverables and market-consistent pricing |

|

Correspondent and cross-border transaction data |

Transaction monitoring, correspondent banking system |

Fund flows to and from secrecy jurisdictions or high-risk countries associated with offshore wealth structures |

|

Currency exchange transactions |

Treasury/FX system, transaction monitoring |

Frequency and volume of foreign currency transactions by PEPs lacking operational justification |

|

Adverse media and court filings |

NLP adverse media screening platform |

Public reports of corruption investigations, asset recovery proceedings, or dismissal from public office |

|

KYC and CDD records |

KYC platform |

Currency and completeness of source-of-wealth verification, EDD approval records, and ongoing monitoring logs |

|

Real estate and high-value asset ownership records |

Real estate registry, OSINT, asset tracing tools |

Assets registered in the name of the PEP or associates, cross-referenced against declared wealth |

|

System and network access logs |

Audit management system, IT security |

For government financial systems: whether the official accessed procurement or payment systems outside normal working patterns |

|

Transaction logs |

Transaction monitoring |

Aggregate payment volumes over time, including identification of structuring patterns |

|

Geopolitical and jurisdictional risk data |

Sanctions databases, FATF high-risk lists, NRA data |

Whether the jurisdiction associated with counterparty accounts or corporate vehicles presents elevated ML or secrecy risks |

|

Employee records |

HR system (for government entities), background screening |

Verifying the employment status and remuneration level of the official to cross-reference against observed wealth |

|

Politically exposed persons list |

Dedicated PEP database, commercial screening vendor |

Breadth of PEP coverage, including domestic PEPs, their immediate family members, and close associates |

How Does Misappropriation of Public Funds Aggravate Customer Risk and Jurisdictional Risk?

Customer Risk is significantly elevated when a public official or PEP is the beneficial owner of an account or entity seeking financial services. The primary driver is the opacity of the origin of wealth: a public official’s salary is a matter of public record, but the true source of their financial activity is not. Where that activity substantially exceeds what salary and declared assets can explain, the compliance team faces a verification gap that heightens the risk that funds are derived from the diversion of public resources. Close associates and family members of the official amplify this risk because they operate outside the direct PEP screening framework, yet may hold assets on behalf of the official.

Jurisdictional Risk is compounded wherever the misappropriated funds originate in, or are routed through, jurisdictions with weak public financial management, limited asset declaration enforcement, opaque BO registers, or secrecy protections for corporate vehicles. The UAE’s geographic position as a regional financial and trade hub means that regulated entities regularly encounter customers whose wealth has been aggregated across multiple high-risk jurisdictions before arriving. Where the originating jurisdiction is identified on FATF’s high-risk and other monitored jurisdictions list, or features in the UAE NRA 2024 as a source jurisdiction for foreign predicate offences, the level of due diligence must be commensurate with that elevated risk.

What Observable Patterns Indicate Misappropriation of Public Funds?

A compliance officer conducting a file review, CDD update, or transaction monitoring review may observe the following patterns in accounts linked to public officials and their associated entities:

Transfers from accounts controlled by a public entity to personal accounts held by an individual with signing authority over that entity, without documented operational justification. Vendor payments that are round-figure amounts, issued to recently incorporated entities with no verifiable track record, and bearing invoices describing broadly worded consultancy or advisory services. A sudden increase in account transaction volumes coinciding with a change in the official’s public role or a procurement cycle. Asset purchases (particularly real estate and equity interests) occurring shortly after large government disbursements, in amounts that exceed the customer’s declared earnings. A pattern of foreign currency exchange transactions, structured wire transfers, or cash withdrawals that individually remain below alert thresholds but cumulatively represent a volume inconsistent with the customer’s legitimate profile.

Sectors at Highest Exposure

The rating column shows each sector’s UAE NRA 2024 residual ML-risk tier (Low, Medium-Low, Medium, Medium-High, High). The reason column explains each sector’s specific exposure to public-fund misappropriation, which can be elevated relative to its general NRA rating.

| Sector | Risk Rating | Specific Reason |

| Financial Institutions (Banks) | Medium-High | UAE NRA 2024 rates mainland banking Medium-High; banks are the primary conduit for initial diversion, structuring, and international transfer of misappropriated proceeds |

| Real Estate | High | UAE NRA 2024 rates real estate as a high risk; property is the preferred integration vehicle for large-scale misappropriated funds |

| Trust and Company Service Providers (TCSPs) | Medium | Create the corporate structures used to receive and hold misappropriated funds at arm’s length from the public official |

| Legal Professionals (Lawyers and Notaries) | Medium | Establish legal vehicles, draft trust deeds, facilitate property transfers, and provide a professional imprimatur to layering structures |

| Dealers in Precious Metals and Stones (DPMS) | Medium-High | High-value assets that convert cash into portable, underreported wealth |

| Money Services Businesses | High | Used to convert, exchange, and wire funds quickly with limited counterparty documentation |

| Accountants and Auditors | Medium-Low | May certify financial statements or accounts that conceal misappropriated fund flows |

Geographies and Contexts of Concern

In the UAE context, misappropriation risk may be heightened where customers are linked to high-risk source jurisdictions identified in the UAE NRA 2024, including countries where foreign predicate offences are documented as a significant ML threat. The UAE’s FATF Recommendation 12 PEP obligations apply in full to foreign PEPs regardless of the country of origin, and supervised entities must not apply reduced diligence on the basis that the originating country has its own enforcement system.

Best Practices for Misappropriation of Public Funds Risk Management

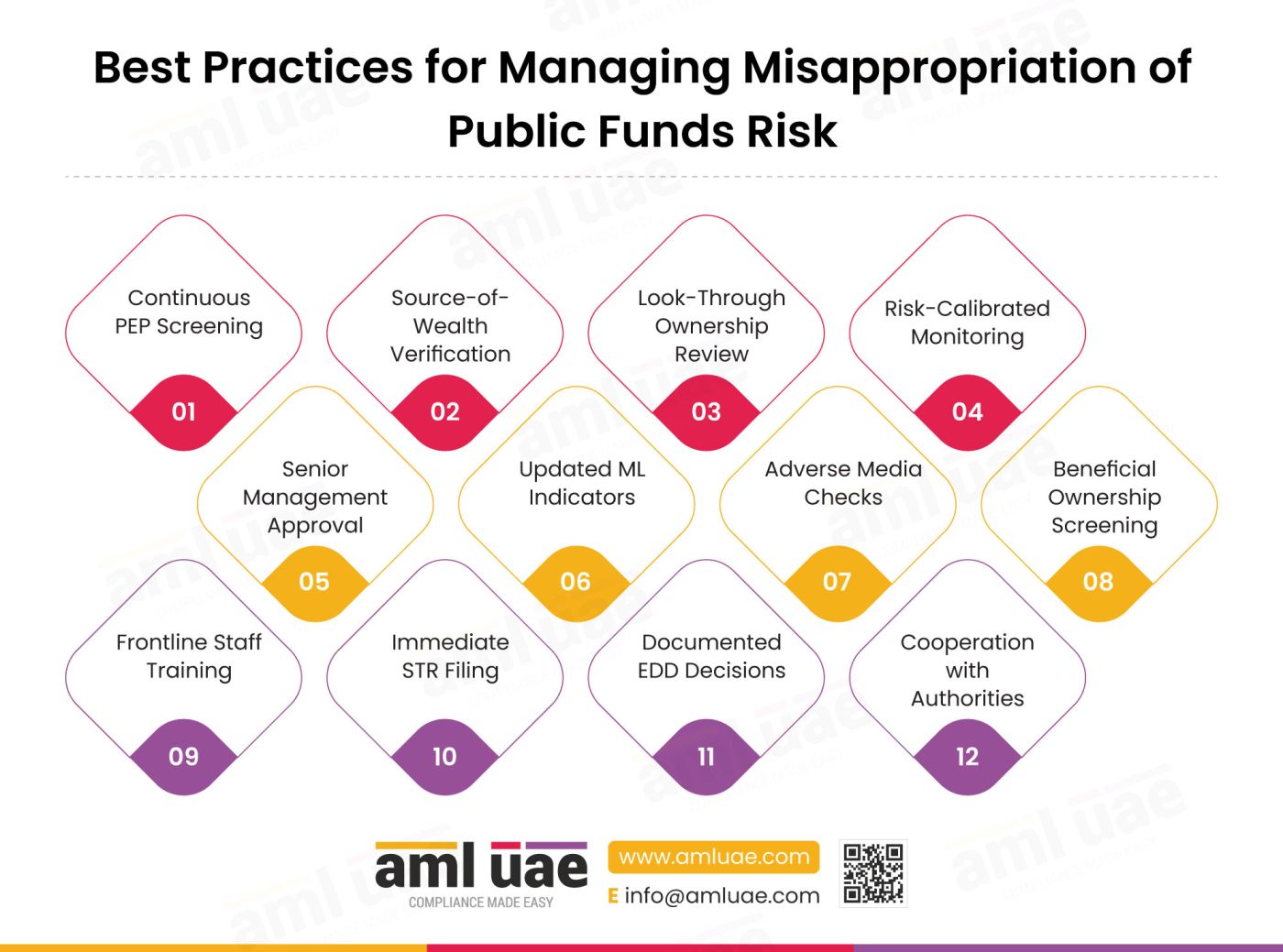

- Incorporate the UAE NRA 2024 sector findings into the entity’s enterprise-wide risk assessment (EWRA). Cabinet Resolution No. (134) of 2025, Article 5 requires each regulated entity to identify, assess, and document its ML, TF, and PF risks; the public-official and PEP exposures described in this article should be reflected in that assessment and refreshed as national risk findings are updated.

- Screen all customers and beneficial owners against comprehensive PEP databases at onboarding and on an ongoing basis. PEP status is not static; a customer may be appointed to public office after a relationship is established. Automated continuous screening is the only reliable way to capture this event and trigger an EDD review. Generic periodic reviews conducted annually are insufficient for a risk category with the velocity and complexity of PEP-linked misappropriation.

- Take reasonable measures to identify source of funds and source of wealth for foreign PEPs, high-risk domestic PEPs, high-risk international-organisation PEPs, or all PEPs where the entity’s internal policy treats all PEP relationships as high risk, supported by independent verification where the risk profile requires it, before approving the business relationship. Documentation must be specific, dated, and cross-referenced against independent sources such as corporate registry data, land registry records, and OSINT. Declaration letters signed by the customer alone are not sufficient evidence of the source of wealth; the documentation must be independently corroborated.

- Apply a substance-over-form test to all entities in the ownership chain of PEP-associated customers. Where a company or trust holds an account or an asset on behalf of a PEP or their associate, the compliance team must conduct full CDD and EDD as though the PEP were the direct customer. The interposition of a legal vehicle does not reduce the risk; it amplifies it.

- Set transaction monitoring rules specifically calibrated to public official risk profiles. Rules must be designed to detect the diversion patterns described in this article: payments from government accounts to personal accounts, round-figure vendor payments to recently incorporated entities, structuring across multiple accounts, and FX transactions inconsistent with the customer’s declared activities. Generic rules designed for mass-market retail customers are not sufficient for this risk category.

- Obtain senior management approval before establishing or continuing a business relationship for foreign PEPs, high-risk domestic PEPs, high-risk international-organisation PEPs, or all PEPs where the entity’s internal policy treats all PEP relationships as high risk. Cabinet Resolution No. (134) of 2025, Article 16 requires the same. The approval should be formally documented, including the rationale for risk acceptance and the specific EDD measures applied, and should be revisited at every significant change in the customer’s circumstances.

- Maintain and regularly update internal indicators for PEP-linked misappropriation. CR 134/2025 Article 17 requires regulated entities to establish and update indicators of ML suspicion. Indicators for misappropriation must be reviewed following material changes in the customer’s public role, following significant government disbursements in sectors served by the entity’s customers, and whenever a supervisory body or the UAEFIU issues updated guidance.

- Conduct enhanced negative news and adverse media checks for PEP customers at onboarding and on a risk-based basis thereafter. Adverse media monitoring should cover sources in the customer’s public role’s language and jurisdiction. Relevant adverse media includes reports of dismissal from public office, parliamentary or audit committee investigations, asset declaration discrepancies, and foreign asset recovery proceedings targeting the customer or their associates.

- Build beneficial ownership verification into every transaction involving a corporate or trust counterparty that receives government payments. Where a regulated entity processes payments to entities that receive government procurement funds, the BO of those entities must be identified and screened against PEP databases. The volume of a government payment does not replace the need for BO transparency; it increases it.

- Train frontline staff to recognise the specific red flags associated with misappropriation, not only general PEP risk. Staff should be able to identify the patterns described in the red flags table in this article, including the use of nominees, inflated vendor payments, and inconsistency between a public official’s declared salary and their financial activity. Training should include the obligation to escalate to the compliance officer rather than to resolve the concern through direct customer inquiry.

- File STRs immediately and without delay when suspicion arises. FDL 10/2025 Article 18 and CR 134/2025 Article 18 require the same. Suspicion does not require certainty; a compliance officer who observes a pattern consistent with misappropriation must report rather than resolve the doubt by seeking further information from the customer. Seeking clarification from a customer who may be involved in misappropriation risks, tipping off.

- Maintain comprehensive records of all EDD decisions, including decisions not to apply enhanced measures. Where a regulated entity assesses a PEP-linked customer as standard risk, the rationale for that decision must be documented, dated, and signed off by the compliance officer. Undocumented risk acceptance decisions are treated as the absence of a CDD process in supervisory examinations.

- Cooperate fully with information requests from the UAEFIU, supervisory authorities, and foreign authorities under mutual legal assistance frameworks. FDL 10/2025 Articles 11 and 18 require regulated entities to provide information requested by the UAEFIU. Delays, omissions, or obstructive responses to authority information requests are standalone violations, separate from any underlying ML offence.

How Misappropriation of Public Funds and Corruption Are Related

Misappropriation of public funds is a specific sub-technique within the broader concept of corruption. While corruption encompasses any abuse of entrusted power for private gain, including bribery, extortion, nepotism, and influence peddling, misappropriation is the most directly financial form: the actual taking of state property or money entrusted to a public official. The distinction matters for compliance teams because misappropriation generates specific proceeds that enter the financial system and require laundering, whereas other forms of corruption may involve the distortion of decisions rather than the direct removal of funds.

Detection and mitigation strategies for misappropriation of public funds build on the general corruption framework but require additional focus on financial account activity, procurement processes, and asset disclosure verification. A compliance officer who understands corruption as a category will recognise the elevated risk associated with PEPs; one who also understands misappropriation as a sub-technique will know which specific transaction patterns and account structures to investigate.

Related Term

| Related Term | Connection |

| Corruption | Parent technique: misappropriation is a specific form of corruption involving the direct diversion of public property or funds |

| Politically Exposed Person (PEP) | Primary actor category: public officials and their associates are the core subject of EDD obligations designed to detect misappropriation |

| Shell Companies | Layering vehicles; shell companies are a primary tool for concealing the beneficial ownership of misappropriated funds |

| Front Company | Layering vehicle; front companies with no legitimate business purpose receive procurement payments as part of the diversion mechanism |

| Beneficial Ownership | Control concept: identifying the true beneficial owner of corporate vehicles is the central challenge in detecting misappropriation structures |

| Enhanced Due Diligence (EDD) | Control mechanism; the specified enhanced-measures framework under CR 134/2025 Art. 16 is the primary regulatory response to PEP-linked misappropriation risk |

| Customer Due Diligence (CDD) | Foundation control: CDD provides the baseline identity and source-of-wealth verification on which misappropriation detection depends |

| Suspicious Transaction Report (STR) | Reporting obligation: the required disclosure mechanism when a regulated entity suspects a customer is involved in misappropriation |

| Source of Wealth | Verification concept: establishing a verifiable wealth origin is the principal challenge in assessing PEP financial activity |

| Trade-Based Money Laundering (TBML) | Typology overlap; false invoicing used in misappropriation schemes shares characteristics with TBML; both exploit trade documentation |

| Kleptocracy | Political concept; systemic state capture where misappropriation operates at a national scale; relevant for jurisdictional risk assessment |

| Asset Recovery | Legal remedy: UNCAC Chapter V and the UAE international cooperation provisions enable the repatriation of misappropriated state assets |

Related Process

| Related Process | Connection |

| Procurement Fraud | The most common mechanism for misappropriating public funds at scale; contracts are awarded to controlled entities without competitive oversight |

| Payroll Fraud | A common diversion mechanism in which fictitious employees or inflated salaries direct public funds to the perpetrator’s accounts |

| False Invoicing | A documentary technique used in misappropriation to create the appearance of a legitimate transaction, justifying a public payment |

Related Control or Obligation

| Related Control or Obligation | Connection |

| PEP EDD (CR 134/2025 Art. 16) | The specific regulatory framework for foreign PEPs and for domestic or international-organisation PEPs where the relationship is assessed as high risk, designed to detect and mitigate misappropriation risk |

| BO Identification (CR 134/2025 Art. 10) | Mandatory identification of beneficial owners at 25% threshold is essential for piercing corporate structures used in misappropriation |

| STR Obligation (FDL 10/2025 Art. 18) | Immediate filing obligation triggered when suspicion of misappropriation arises |

| UNCAC Asset Recovery (Chapter V) | International legal framework enabling the tracing and repatriation of misappropriated public funds across jurisdictions |

What Financial Instruments Do Criminals Use in Misappropriation of Public Funds Schemes?

Accounts receivable and commercial invoices are exploited in misappropriation schemes to generate documentary evidence of a legitimate commercial transaction where none exists.

A procurement official approves payment against a fraudulent invoice submitted by a controlled entity. The invoice, which may bear the names of real suppliers or describe real service categories, creates a paper trail that appears to justify the outflow from the government account. Because accounts receivable instruments are routine in public procurement, their misuse is difficult to detect without price benchmarking and counterparty verification.

Bank accounts are the primary vehicle for receiving, holding, and moving diverted funds. Personal accounts, business accounts held in the name of nominees, and accounts at foreign financial institutions are all used at different stages of the scheme. The pattern of multiple accounts, each receiving small tranches of the total diverted amount, is a structuring technique designed to avoid triggering transaction monitoring alerts.

Cash is used for the direct extraction of public funds in contexts where physical cash handling is part of normal government operations, such as cash-based procurement, petty cash accounts, or government disbursements to recipients in areas with limited banking infrastructure. Cash removes the audit trail at the point of diversion, making tracing extremely difficult without forensic accounting.

Equity interests in legal entities provide the structural mechanism for holding misappropriated funds in a form that generates ongoing income and appreciates in value. A public official who uses misappropriated funds to acquire equity in a commercial enterprise creates an asset that is difficult to distinguish from a legitimate business investment. The equity interest also provides an explanation for any future dividend or income that would otherwise be unexplained.

Real estate is the most widely documented integration asset in misappropriation cases globally. Property provides a stable store of value, generates rental income that launders the underlying funds, and can be transferred between beneficial owners through layered corporate structures without appearing on the official’s personal asset declaration.

Trust beneficial interests allow the public official to benefit economically from assets without appearing in any public registry as the owner. A trust settled in favour of the official’s family members or under discretionary terms controlled by a professional trustee holds the assets, while the official retains effective control through mechanisms such as a protector role or a letter of wishes.

|

Variant or Synonym |

Context or Jurisdiction |

Distinction from Primary Term |

|

Embezzlement |

Common law jurisdictions |

Specifically refers to misappropriation by a person who lawfully holds property as an employee or agent; broader than the public-sector-specific framing of misappropriation of public funds |

|

Diversion of State Assets |

International law and asset recovery |

Preferred terminology in asset recovery and UNCAC discussions; includes both cash and non-cash state property |

|

Kleptocracy |

Political science and international relations |

Refers to systemic or institutional misappropriation where state structures are captured by ruling elites; the individual typology operates at a smaller scale |

|

Public Sector Corruption |

Supervisory and regulatory usage |

Broad category covering multiple forms of official misconduct, including misappropriation, bribery, extortion, and abuse of functions |

|

Misuse of Public Office |

UK and Commonwealth jurisdictions |

A criminal offence distinct from embezzlement; covers deliberate breach of official duty for personal gain, including but not limited to financial diversion |

|

Corruption Proceeds |

ML and asset recovery context |

Refers specifically to the financial proceeds generated by corruption, including misappropriation; used in the context of predicate offence analysis |

What Products and Services Do Criminals Abuse in Misappropriation of Public Funds Schemes?

Currency exchange services are abused in misappropriation schemes to convert diverted funds from the domestic currency of the originating jurisdiction into more widely traded currencies, reducing the traceability of the original source. A public official who has extracted government funds in a local currency will frequently use a money exchange provider to convert those funds into US dollars, euros, or UAE dirhams before moving them into the international financial system. The conversion creates a break in the documentary chain that makes source tracing more difficult.

Offshore banking services are used to receive and hold misappropriated funds outside the jurisdiction in which the theft occurred, placing the assets beyond the immediate reach of domestic law enforcement and asset recovery proceedings. Offshore accounts held in jurisdictions with strong banking secrecy laws, limited information exchange with the originating country, and minimal beneficial ownership disclosure requirements are the preferred deposit vehicle for large-scale misappropriation proceeds.

Offshore company incorporation services are used to create the corporate wrappers through which misappropriated funds are channelled. A public official who cannot hold funds personally without triggering asset declaration scrutiny will direct those funds through a series of offshore companies, each incorporated in a different jurisdiction, with nominee directors and shareholders obscuring the true beneficial owner. Company formation services that fail to conduct rigorous BO identification on their clients are directly complicit in enabling these structures.

Real estate transaction services facilitate the conversion of liquid misappropriated funds into immovable property. Real estate agents and transaction advisers who do not verify the source of funds used to purchase property are a critical vulnerability in the AML control chain. The UAE NRA 2024 identifies real estate as a High-risk sector specifically because large cash transactions, unknown sources of funds, and property price manipulation are documented characteristics of ML in the sector.

Trust and corporate services provided by TCSPs create the legal holding structures that give the misappropriating official long-term control of assets without visible ownership. A discretionary trust with a professional trustee, holding a portfolio of real estate and equity investments on behalf of undisclosed beneficiaries, is one of the most resilient asset-protection structures available to a corrupt official. TCSPs that establish trusts without identifying the settlor’s source of wealth and without conducting ongoing monitoring of the trust relationship are facilitators of the integration stage of misappropriation proceeds.

Wire transfer services move misappropriated funds between accounts, across borders, and through multiple financial institutions at speed. The international wire transfer system is the primary mechanism by which proceeds exit the originating jurisdiction and enter the UAE or other financial centres. Each routing step through an additional correspondent bank adds a layer of opacity to the transaction trail.

How AML UAE Helps in Managing the Risk of Misappropriation of Public Funds

The article above has identified a specific compliance gap: most regulated entities have PEP policies, but far fewer have the operational processes, training, and systems required to detect misappropriation of public funds as a distinct typology. The gap between knowing that PEPs are high-risk and knowing how to detect the specific transaction patterns, corporate structures, and source-of-wealth inconsistencies that signal misappropriation is where most enforcement exposure lives.

AML UAE works with financial institutions, DNFBPs, and professional service firms to build compliance programmes that close that gap. This includes designing PEP EDD frameworks that go beyond name screening to cover source-of-wealth verification, corporate structure mapping, and ongoing monitoring rules specific to public-sector risk profiles. It also includes typology-specific training that equips frontline staff and compliance officers to recognise misappropriation indicators in the account activity and customer documentation they see every day.

For regulated entities that handle government agency relationships, procurement counterparties, or corporate customers with PEP-linked beneficial owners, AML UAE provides structured risk assessment and policy development support aligned to FDL 10/2025, CR 134/2025, and the FATF PEP standards. For entities facing supervisory review or information requests related to PEP-linked accounts, AML UAE provides advisory support grounded in the current UAE regulatory framework.

Frequently Asked Questions

Yes. FDL 10/2025, Article 2 criminalises money laundering in relation to the proceeds of any predicate offence. Misappropriation of public funds generates predicate-offence proceeds where the underlying conduct amounts to a felony or misdemeanour under applicable UAE law, or a qualifying foreign offence satisfying the conditions in FDL 10/2025. A person who launders proceeds derived from public fund misappropriation commits a money laundering offence, independent of whether they were involved in the original misappropriation.

Bribery involves the payment or receipt of a benefit in exchange for an official exercising their discretion in a particular way. Misappropriation is the direct taking of public property or money by an official who has control over it. The two offences may overlap in complex corruption schemes, but their AML implications differ: bribery generates proceeds at the point of receipt by the official, while misappropriation generates proceeds at the point of diversion from public funds.

For foreign PEPs, and for domestic or international-organisation PEPs where the relationship is high risk, it involves obtaining senior management approval before establishing or continuing the business relationship, taking reasonable measures to identify the customer’s source of funds and source of wealth with independent verification proportionate to the risk, conducting enhanced ongoing monitoring of transactions, and updating EDD documentation whenever the customer’s public role or risk profile changes.

Banks, real estate agents and brokers, TCSPs, lawyers, and dealers in precious metals and stones are the sectors with the highest exposure. The UAE NRA 2024 rates real estate as High risk and TCSPs as Medium risk for ML, with PEP-linked misappropriation contributing to both ratings.

Yes, but with different mandatory measures. Under FATF Recommendation 12, foreign PEPs must receive mandatory EDD. Domestic PEPs and PEPs from international organisations must receive risk-based enhanced measures. Under CR 134/2025 Article 16, foreign PEPs receive the full specified measures, including mandatory senior management approval; domestic PEPs and PEPs of international organisations receive these enhanced measures where the relationship is assessed as high risk. An entity may choose to treat all PEPs as high risk as a matter of internal policy.

An STR must be filed immediately and without delay when suspicion arises. Suspicion does not require certainty or proof. Under FDL 10/2025 Article 18 and CR 134/2025 Article 18, the obligation to file is triggered by the formation of suspicion, not by confirmation of a criminal act. A compliance officer who identifies a pattern consistent with misappropriation and delays filing to gather more evidence is in breach of the STR obligation.

Under FDL 10/2025, Article 28, a deliberate or grossly negligent failure to file an STR may result in imprisonment and a fine of AED 100,000 to AED 1,000,000. Separately, supervisory authorities may impose administrative fines of AED 10,000 to AED 5,000,000 per violation under Article 17, with incremental fines where a violation recurs within one year.

The UAE ratified UNCAC and is committed to its provisions, including Chapter V on asset recovery. UNCAC Article 17 defines the misappropriation offence, and Chapter V requires states to provide the widest possible mutual legal assistance in tracing, freezing, seizing, and returning misappropriated assets. Mutual legal assistance and cross-border asset recovery operate between competent authorities under FDL 10/2025 Article 21. Regulated entities, for their part, must provide information requested by the UAEFIU under FDL 10/2025 Articles 11 and 18.

No. Under CR 134/2025 Article 10, beneficial owner identification must pierce nominee arrangements to identify the natural person who ultimately owns or controls the entity. Where a TCSP acts as a nominee for a PEP or PEP associate, the underlying beneficial owner must be identified and subjected to the same EDD framework as a direct PEP customer.

goAML is the UAEFIU’s secure online reporting platform. STRs from regulated entities in the UAE must be filed with the UAEFIU through its electronic reporting system, currently goAML, or any other FIU-approved channel, under FDL 10/2025 Article 18. goAML submissions must include all available data on the customer, the transactions, and the basis for suspicion. Registration on goAML is a mandatory prerequisite for reporting; entities that fail to register are unable to comply with their statutory reporting obligations and may be subject to regulatory enforcement where reporting failures occur.

Under CR 134/2025 Article 25, all CDD and EDD records must be retained for a minimum of five years from the end of the business relationship or the completion of an occasional transaction. For PEP relationships, the EDD documentation includes source-of-wealth verification, senior management approval records, ongoing monitoring logs, and all STRs filed in relation to the account.

No. Corruption is the broader category and misappropriation of public funds is one type of corruption offence. Corruption also covers bribery, abuse of office, trading in influence, and illicit enrichment. Misappropriation specifically involves a public official diverting state money, property, or assets under their control for personal benefit or for another person. For AML purposes, both can generate proceeds of a predicate offence under FDL 10/2025, Article 2.

Under CR 134/2025 Article 16, senior management approval is required before establishing, and to continue, a business relationship with a foreign PEP. For domestic PEPs and PEPs of international organisations, the same approval applies where the relationship is assessed as high risk. The approval should be documented and revisited whenever the customer’s public role or risk profile changes.

Source of funds is the origin of the specific money used in a particular transaction or relationship, for example the salary, sale proceeds, or loan behind a payment. Source of wealth is the origin of the customer’s overall net worth, explaining how the total wealth was accumulated over time. For PEP-linked misappropriation risk, both should be identified through reasonable measures and supported by independent documentation where the risk profile requires it, under CR 134/2025 Article 16.

It can, which is why beneficial ownership identification is central to the control. Trusts and nominee arrangements can place legal title in a name other than the PEP’s while the PEP keeps ultimate control or benefit. Regulated entities must identify the natural person who ultimately owns or controls the customer, applying the 25% ownership or control test and the control and senior-managing-official fallbacks under CR 134/2025 Article 10, and screen those persons for PEP status rather than relying on the named account holder.

Closing Summary

Misappropriation of public funds may generate proceeds of a predicate offence where the underlying conduct amounts to a felony or misdemeanour under applicable UAE law, or a qualifying foreign offence satisfying the conditions in FDL 10/2025, and those proceeds require concealment through the formal financial and professional services sectors.

The regulatory obligation for regulated entities in the UAE is clear: foreign PEP relationships require the specified enhanced measures under CR 134/2025 Article 16, while domestic PEPs and PEPs of international organisations require those measures where the relationship is assessed as high risk, and an entity may choose to treat all PEP relationships as high risk under its internal risk appetite.

Across PEP relationships this means taking reasonable measures to identify source of funds and source of wealth, supported by independent verification where the risk profile requires it, and immediate STR filing when suspicion arises.

The typology described in this article spans the placement, layering, and integration stages of money laundering, exploiting real estate, corporate vehicles, trust structures, wire transfers, and professional service providers at each stage.

Detection requires a combination of accurate PEP identification, network analytics that map relationships between customers and corporate counterparties, and ongoing monitoring rules calibrated to the behavioural signature of public-fund diversion rather than general retail banking risk profiles.

Compliance teams that treat PEP obligations as a static onboarding check miss the dynamic nature of misappropriation risk. A customer’s public role, the procurement cycles affecting their sector, and the geopolitical environment of the originating jurisdiction all change over time. An EDD framework that does not respond to those changes in real time is not fit for purpose against this typology.

Strengthening Your AML Compliance Framework?

Ensure your controls can address risks associated with the misuse of public funds.

Share via :

About the Author

Pathik Shah

FCA, CAMS, CISA, CS, DISA (ICAI), FAFP (ICAI)

Pathik is an ACAMS-certified AML consultant specialising in governance, risk, and compliance for regulated entities in the UAE. He brings over 28 years of experience, with 1,000+ hours of AML training and 200+ advisory engagements across DNFBPs, VASPs, and FIs. He supports businesses in aligning with AML/CFT requirements from the CBUAE, DFSA, MoET, MoJ, VARA, CMA, FSRA, and FATF. Known for translating complex regulations into audit-ready procedures, Pathik enables operational clarity and compliance readiness.

Reach Out to Pathik