Trade Misinvoicing

Last Updated: 06/09/2026

Protect your business with reliable and effective AML strategies with AML UAE.

Key Highlights: Trade Misinvoicing

Deliberate falsification of price, quantity, or description on commercial invoices moves illicit value across borders disguised as legitimate trade.

Under Federal Decree Law No. (10) of 2025, regulated entities in the UAE must apply customer due diligence, ongoing monitoring, and regulatory reporting for suspicious activities or transactions.

Verify invoiced values against commodity benchmarks, confirm goods descriptions against shipping records, and cross-reference counterparty ownership before processing any trade transaction.

What is Trade Misinvoicing?

Falsification of the price, quantity, or description of goods on commercial trade documents, trade misinvoicing, is a broad-based form of trade-based money laundering that enables criminals to transfer illicit value across borders under the cover of legitimate commercial activity. Unlike techniques that target only the pricing of goods, trade misinvoicing encompasses any deliberate distortion of invoice data, whether the manipulation is applied to the stated value, the declared quantity, or the description of the goods being traded.

The Financial Action Task Force identifies trade-based money laundering, of which trade misinvoicing is a central technique, as one of the three primary methods by which criminal organisations move and integrate illicit funds globally. The FATF’s analysis confirms that the deliberate distortion of trade transaction data consistently appears across all major international money laundering schemes.

Regulatory Framework Related to Trade Misinvoicing

Federal Decree Law No. (10) of 2025 is the UAE’s apex statute for combating money laundering, terrorist financing, and proliferation financing. Article 2 criminalises the conversion, transfer, acquisition, possession, or use of funds, knowing they are proceeds of a predicate offence. Trade misinvoicing, when used to transfer illicit funds through falsified commercial documents, is captured directly within Article 2’s scope.

Article 19 of Federal Decree Law No. (10) of 2025 requires all regulated entities to identify, assess, and manage their money laundering and terrorist financing risks.

For institutions involved in trade finance, international payments, or cross-border investment services, the obligation extends to trade-specific risk controls calibrated to the falsification techniques their product portfolios are most exposed to. Failure to maintain adequate controls attracts administrative penalties under Article 17, ranging from AED 10,000 to AED 5,000,000 per violation.

Separate criminal penalties apply where the facts involve money laundering, terrorist financing, proliferation financing, or deliberate failure to comply with statutory reporting obligations.

Cabinet Resolution No. (134) of 2025 sets out the operative compliance framework. Article 5 requires an Enterprise-Wide Risk Assessment addressing product-level vulnerabilities, including trade finance and cross-border payment instruments. Articles 6 through 9 define customer due diligence obligations applicable to all trade finance relationships. Article 25 requires all transaction records and supporting trade documentation to be retained for a minimum of five years from the date of completion.

Primary Authority or Supervisory Body

The UAE Financial Intelligence Unit (UAEFIU), established within the Central Bank of the UAE under Article 11 of Federal Decree Law No. (10) of 2025, is the national authority for receiving, analysing, and disseminating financial intelligence. All suspicious transaction reports related to trade misinvoicing are submitted to the UAEFIU via the goAML platform, regardless of entity type or sector.

The Ministry of Economy and Tourism (MoET) supervises mainland and commercial free zone DNFBPs including real estate agents, dealers in precious metals and stones, trust and company service providers, and accountants. The Ministry of Justice (MoJ) supervises lawyers, notaries, and other legal professionals. Financial institutions are supervised by the Central Bank of the UAE. Capital Market companies are supervised by the Capital Market Authority (CMA).

Reporting or Compliance Obligations and Channels

Where a regulated entity identifies documentation anomalies consistent with trade misinvoicing that meet the threshold of suspicion, it must file a Suspicious Transaction Report with the UAEFIU without delay. Article 18 of Federal Decree Law No. (10) of 2025 requires the report to be submitted immediately upon reasonable grounds for suspicion, with no minimum transaction value. All reports are submitted exclusively via goAML.

Beyond STR filing, entities processing trade finance transactions should apply customer due diligence measures as set out in Articles 6 through 9 of Cabinet Resolution No. (134) of 2025. Where indicators of goods description falsification, quantity manipulation, or price distortion are present, entities should apply enhanced due diligence.

Further, Article 5, which requires identifying, assessing and managing business risk, entities should also include trade monitoring in their risk management programme.

Recent Developments, Enforcement Actions, or Supervisory Priorities

Federal Decree Law No. (10) of 2025 was published on 30 September 2025 and entered into force on 14 October 2025, replacing Federal Decree Law No. (20) of 2018 and all its amendments. Cabinet Resolution No. (134) of 2025, the executive regulation governing operative compliance obligations, entered into force on 14 December 2025.

The UAE National Risk Assessment 2024 rates trade-based money laundering as a Medium-High risk, specifically noting the country’s position as a global re-export hub. The EOCN’s 2023 TF and PF Red Flags Guidance identifies trade documentation inconsistencies as risks specific to trade finance, giving trade misinvoicing a dual AML and CPF risk profile.

What does Trade Misinvoicing Mean?

Picture a shipment of electronics listed on the customs declaration as ‘spare parts’ and valued at USD 20,000. The shipment actually contains high-value components worth USD 200,000. The declared value clears customs, duties are paid at the lower rate, and USD 180,000 in value moves across the border without commercial scrutiny.

The same result can be achieved by overstating the price of legitimate goods, under-counting the quantity shipped, or reclassifying a product as a lower-value category. In every case, the manipulation is on the document, not the goods themselves; the paper creates the gap, and the gap carries the illicit value.

Why Detecting Trade Misinvoicing Matters

Trade misinvoicing is operationally significant precisely because it can be applied to any commercial transaction involving the movement of goods. Its multi-axis structure makes it adaptable to any trade corridor, any product category, and any jurisdictional environment, and resistant to controls that address only one dimension of the problem.

The UAE’s exposure is particularly acute. Its role as a global re-export hub, combined with extensive free-zone infrastructure and high volumes of commodity and manufactured goods flowing in multiple directions, creates a trading environment where documentation verification is structurally challenging. Without automated trade monitoring systems specifically calibrated to detect all three falsification types, the scheme moves through undetected.

The consequences of non-detection are substantial. Under Federal Decree Law No. (10) of 2025, Article 17, administrative fines for compliance failures reach AED 5,000,000 per violation. The undetected trade misinvoicing schemes in sensitive product categories carry a dual regulatory exposure: both AML and Counter Proliferation Financing supervisory sanctions may apply.

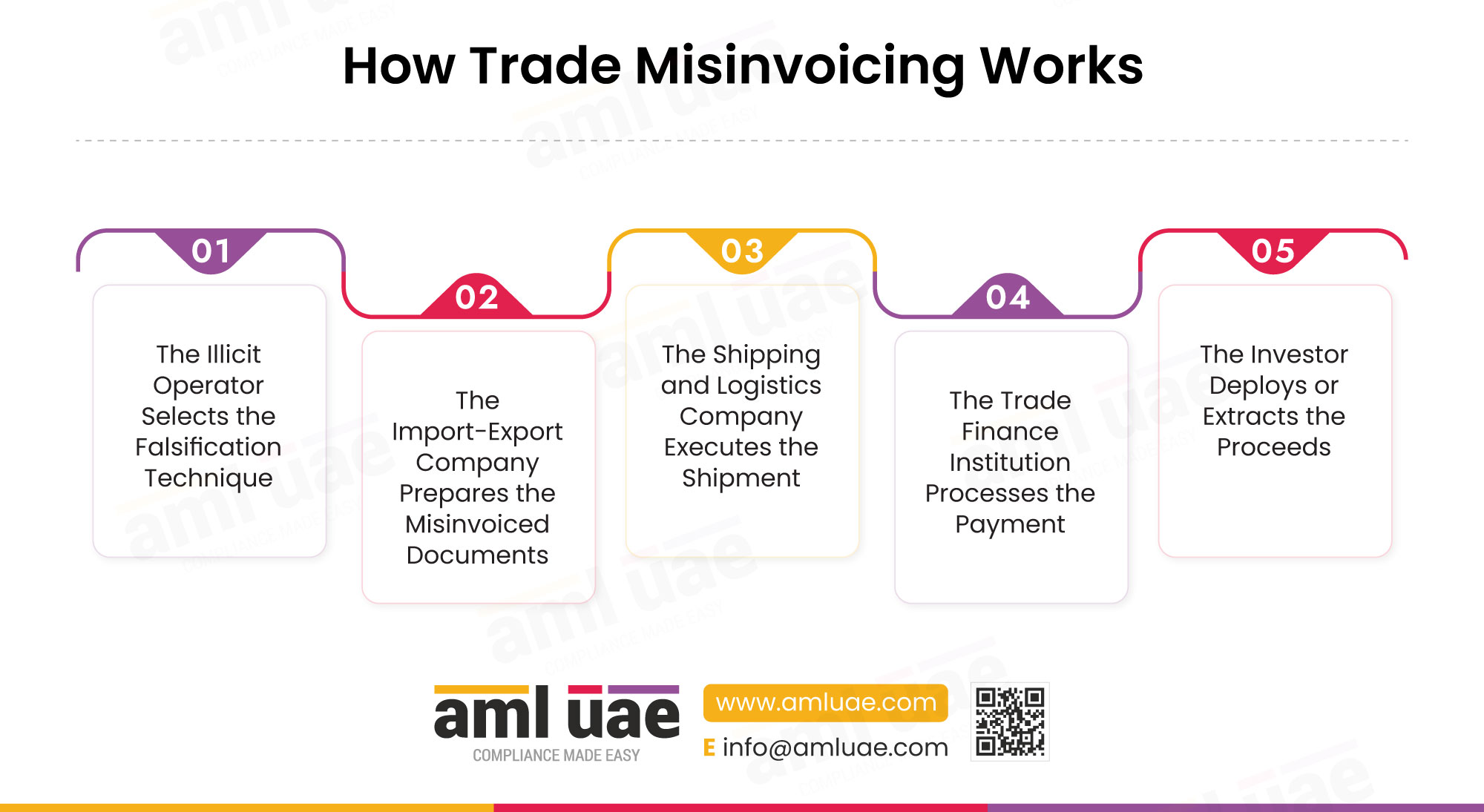

How Trade Misinvoicing Works

Stage One: The Illicit Operator Selects the Falsification Technique

An illicit operator reviews the trade corridor and selects the falsification technique best suited to its characteristics. Where commodity price benchmarks are readily available, description falsification is preferred because it obscures the nature of the goods and defeats price comparison. Where goods categories have wide legitimate price variation, price manipulation is selected. Where customs screening focuses on value rather than quantity, quantity manipulation is deployed.

The operator often combines techniques: a shipment may be described vaguely, undervalued, and understated in quantity simultaneously, compounding the value gap while reducing the detectability of any single indicator. Corridors with limited customs verification capacity, low commodity market transparency, or restricted information-sharing with UAE authorities are actively preferred.

Stage Two: The Import-Export Company Prepares the Misinvoiced Documents

An import-export company, often a legitimately incorporated trading entity, prepares the commercial invoice, packing list, and certificate of origin at falsified values. Internal document sets are made consistent with one another: if the invoice states 500 units, the packing list states 500 units, and the bill of lading is instructed to show 500 units. This internal consistency means that document-compliance-based reviews detect no discrepancy across the document set itself.

The falsification is only detectable by comparing the documents against external data: physical goods, independent valuations, or third-party shipment records. The company’s banking relationship, established trading history, and otherwise compliant business profile make it a low-suspicion counterparty. This is by design: legitimacy in all observable dimensions except the document values is what gives the scheme its durability.

Stage Three: The Shipping and Logistics Company Executes the Shipment

A shipping and logistics company physically transports the goods. In some scheme variants, the logistics company is a knowing participant: it accepts booking confirmations at the falsified quantities, issues bills of lading that match the commercial invoice, and may reroute shipments through transit jurisdictions to further obscure the cargo trail. In other variants, the logistics company is entirely unaware of the falsification and simply fulfils the booking as presented.

The bill of lading that the shipping company issues becomes part of the trade document set presented to the bank. If the shipping company has issued a bill of lading for 500 units and the invoice states 500 units, the bank’s document compliance review passes and payment is authorised. The gap between the 500 declared units and the 2,000 actually shipped is only detectable at the physical inspection stage.

Stage Four: The Trade Finance Institution Processes the Payment

A trade finance institution receives the misinvoiced document set and processes payment against it. The institution’s review is, in most cases, limited to documentary compliance: do the documents match each other, do the names align, does the letter of credit condition set permit payment on these terms? Where the letter of credit terms do not require independent goods valuation or quantity verification, the institution is contractually obligated to pay against the documents irrespective of their accuracy.

The payment settles at the falsified value. The excess value over the true commercial worth of the goods is now in the beneficiary’s account, clothed in the apparent legitimacy of a bank-processed international trade payment. This is the moment at which the layering is complete.

Stage Five: The Investor Deploys or Extracts the Proceeds

In the most sophisticated trade misinvoicing schemes, the extracted proceeds are channelled into Foreign Direct Investment flows. An investor, operating through a corporate structure in a second or third jurisdiction, deploys the laundered funds as apparent FDI into the origin country. This creates a circular flow: illicit funds exit the origin country through misinvoiced trade, are cleaned through the trade finance channel, and return as ostensibly legitimate foreign investment.

This FDI variant is particularly difficult to detect because it requires compliance teams to connect separate transaction streams, outward trade payments and inward investment flows, across potentially different institutions and jurisdictions. The investment label suppresses further scrutiny and provides a compelling cover story for the source of funds.

Real-World Examples of Trade Misinvoicing

The Misclassified Goods Scenario

A trading company ships a consignment of high-specification electronic components to an overseas buyer. The commercial invoice and customs declaration describe the goods as ‘general electrical components’ and list the unit value at a fraction of the actual market price.

The customs authority in the receiving jurisdiction clears the shipment at the declared value, which falls below the threshold requiring enhanced scrutiny. The buyer pays the declared invoice amount plus a separate consultancy fee transfer that accounts for the true value of the components.

The detection lesson is specific: description falsification is detectable only by matching the declared goods category against the actual goods. A review process that treats ‘general electrical components’ as an acceptable description, without verifying the specification against the tariff code, will miss the reclassification. Customs and border records, when cross-referenced against the trade documentation, would reveal the mismatch.

The Quantity Discrepancy Scheme

An importer declares a shipment of 1,000 units of a physical commodity at a stated unit price. The actual shipment contains 4,000 units. The declaration understates the quantity so that the total declared value stays below the level at which the importing institution would trigger an enhanced review. The importer pays at the declared rate for 1,000 units; the remaining 3,000 units are effectively transferred free of charge under the commercial document.

The lesson for compliance teams is that quantity verification requires physical inspection data or independent logistics records compared against the invoice at the point of payment authorisation. Pre-shipment finance providers are directly exposed because their facility is sized against the declared quantity, not the actual shipment.

The FDI-Linked Misinvoicing Arrangement

A series of export shipments from one jurisdiction to another are invoiced at below-market prices over an extended period. The receiving entity in the destination jurisdiction accumulates a significant financial surplus from the under-priced imports relative to their market value. This surplus is subsequently channelled into a Foreign Direct Investment vehicle structured in a third jurisdiction and announced as new inward investment into the exporting country.

The lesson here concerns the compliance response to sudden inward FDI flows from high-risk jurisdictions with no prior economic relationship. The correct detection sequence is to assess source-of-funds documentation for any inward FDI against known trade flows in the same corridor, verify the investor entity’s ownership and commercial history, and apply country risk assessments to both the origin jurisdiction and the corporate structures through which the investment is routed.

How Does Trade Misinvoicing Facilitate Money Laundering?

Trade misinvoicing operates at the layering stage of the money laundering cycle, creating documentary distance between illicit funds and their criminal origin by embedding the value transfer inside an apparently legitimate commercial transaction. Its particular effectiveness lies in its ability to distort value across multiple dimensions simultaneously, with each manipulation appearing as a plausible commercial variance when reviewed in isolation.

The layering effect is compounded by the number of parties, institutions, and jurisdictions involved in a standard trade transaction. By the time the payment settles, the transaction record will typically include a purchase order, a commercial invoice, a bill of lading, a certificate of origin, a letter of credit, and a bank payment confirmation, all internally consistent with the falsified values. Unpicking this chain after settlement requires access to data sources outside the document set itself.

The jurisdictional dimension of trade misinvoicing makes it particularly valuable to criminal networks operating across borders. Unlike cash-based placement schemes, which are constrained by the geography of the criminal’s location, trade misinvoicing allows value to be moved to any jurisdiction with international trade links. The choice of trade corridor can be optimised for regulatory weakness, distance from the criminal’s base, and the availability of investment vehicles for the reintegration stage.

How Do Criminals Exploit Trade Misinvoicing?

Illicit operators design the scheme and determine which falsification techniques are deployed in which combinations. They maintain the operational separation between the different legs of the transaction and coordinate the recycling of extracted value into investment vehicles or further laundering stages. Their involvement is consistently concealed through nominee structures, corporate layering, and jurisdictional separation.

Import-export companies provide the commercial infrastructure. A company with a genuine trading history, established banking relationships, and a diversified customer base is far more valuable to an illicit operator than a purpose-built shell, because its legitimacy provides an extended runway before suspicion arises.

Investors enter the scheme at the FDI integration stage. They receive the laundered proceeds and deploy them as apparent foreign direct investment, using holding companies, investment funds, or real estate vehicles to present the funds as commercially generated returns. The investor’s role distances the original criminal from the funds and provides a plausible economic explanation for the wealth.

Shipping and logistics companies either participate knowingly by accepting and recording falsified quantities on transport documents, or they are unknowing facilitators whose documentation is used to provide surface legitimacy to misinvoiced quantities.

Trade finance institutions are the central processing mechanism. Their willingness to release funds against document-compliant presentations, without independent verification of the goods’ value, quantity, or description, is structurally necessary for the scheme’s completion. Enhanced document review procedures and trade-specific monitoring are the primary controls that can break this link.

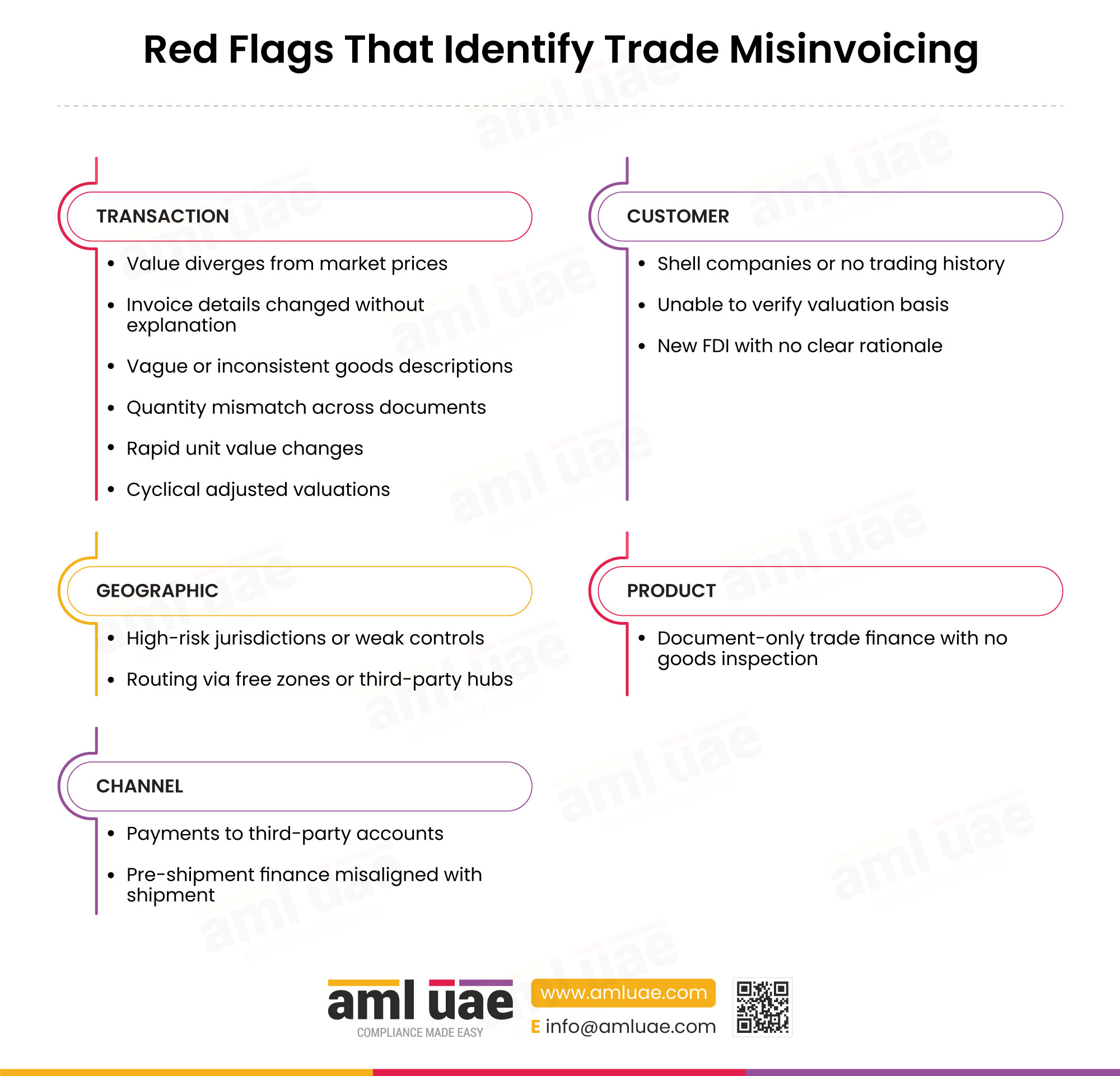

What Are the Red Flags That Identify Trade Misinvoicing?

| Category | Red Flag |

| Transaction | The declared value of goods on the commercial invoice materially diverges from independently verifiable commodity market prices for the same goods category, origin, and quantity. |

| Transaction | Invoice amounts or goods descriptions are amended after the initial document submission, with no written commercial explanation for the revision provided to the financing institution. |

| Transaction | The description of goods on the commercial invoice uses broad, non-specific terminology that would not normally appear on a professional invoice for those goods (for example, ‘general merchandise’ for a specific manufactured product). |

| Transaction | The goods description is inconsistent across different documents in the same trade package: the invoice, the packing list, and the bill of lading describe the same consignment using different terminology or product codes. |

| Transaction | The quantity stated on the commercial invoice differs materially from the quantity recorded on the bill of lading, the packing list, or the customs entry in the destination jurisdiction. |

| Transaction | Rapid and unexplained changes in the declared unit value of goods appear across consecutive shipments in the same trade relationship, with no identifiable commodity market movement to explain the variation. |

| Transaction | A pattern of cyclical shipments to the same foreign jurisdiction shows systematically adjusted valuations across each shipment, suggesting coordinated manipulation of declared values over time. |

| Customer | One or more parties to the transaction are shell companies or entities with no established trading history, no identifiable physical premises, and no independently verifiable commercial activity. |

| Customer | The buyer or seller is unable to provide documentation verifying the basis for the goods valuation, such as purchase agreements, independent appraisals, or commodity price benchmarks. |

| Customer | The transaction is followed within a short period by an inward foreign direct investment flow from the same or a related jurisdiction, with no disclosed investment rationale or prior commercial relationship. |

| Geographic | The trade corridor runs between the UAE and a jurisdiction identified in FATF or UAEFIU guidance as presenting elevated trade misinvoicing risk, limited customs verification capacity, or restricted information-sharing capacity. |

| Geographic | Goods are routed through a transit free zone or third jurisdiction with minimal customs documentation requirements, adding an obscuring layer to the documentation chain. |

| Product | The trade finance product used does not require independent goods valuation as a disbursement condition, enabling payment to proceed solely on the basis of document compliance. |

| Channel | The settlement payment is directed to a third-party account not named in the original commercial documentation, or is split across multiple correspondent banking routes for the same invoice. |

| Channel | Pre-shipment finance is requested at a level inconsistent with the declared goods value, or the drawdown schedule does not correspond to the shipment timeline in logistics records. |

Which AML Controls Counter Trade Misinvoicing?

| Control | What It Disrupts | Detect / Prevent / Deter | Specific Limitation |

| Country Risk Assessment | Routing through high-risk corridors | Detects high-risk jurisdiction exposure; triggers enhanced scrutiny on all transactions in elevated-risk corridors | Requires up-to-date risk ratings for all active corridors; static assessments quickly become outdated |

| Customer Due Diligence (CDD) | Shell companies with no genuine commercial activity | Identifies parties with no verifiable business purpose or trading history before the facility is established | CDD captures entity identity but does not directly verify the commercial accuracy of individual trade transactions |

| Enhanced Due Diligence (EDD) | High-risk customer relationships and counterparty opacity | Requires deeper commercial verification for elevated-risk counterparties | EDD is resource-intensive; only scalable if risk-based triggers are well-calibrated |

| Independent Audit and Testing | Internal compliance failures and systematic control gaps | Identifies where trade monitoring rules or document review processes are not functioning as designed | Audit cycles may be too infrequent to catch emerging typology variants; requires auditor expertise in TBML |

| OSINT and External Source Verification | Price and description falsification | Enables direct comparison of declared goods values against commodity market data and trade statistics | Not scalable for high-volume trade portfolios without automation |

| Ongoing Due Diligence | Gradual escalation of misinvoicing schemes within established relationships | Detects pattern changes in declared goods values, counterparties, or trade corridors after initial CDD | Ongoing monitoring must be calibrated to TBML indicators; generic transaction review will miss the pattern |

| Service Restriction | Continued use of facilities by high-risk customers | Prevents further falsified transactions by suspending or terminating trade finance access | Requires clear internal escalation and legal sign-off before restriction is imposed |

| Staff AML Training and Awareness | Front-line identification failures in document review | Equips trade finance staff to recognise all three falsification types | Effectiveness decays without reinforcement; must be updated as typology variants evolve |

| Trade Monitoring | Systematic falsification across multiple transactions | Detects anomaly patterns across a customer’s trade portfolio by comparing declared values and descriptions against benchmarks | Requires trade-specific monitoring tools; commodity benchmarks not available for all product categories |

| Transaction Escrow Management | Payment release before goods compliance is verified | Holds payment in escrow until independent confirmation of goods delivery and value is received | Commercially disruptive for routine trade; typically applicable only to high-value or high-risk transactions |

| Transaction Monitoring | Individual payment anomalies and unusual settlement patterns | Detects settlement amounts inconsistent with declared values and third-party payment routing | Standard rules optimised for payment-level signals; trade-specific rules must be separately designed |

How Do AI and RegTech Automate Detection of Trade Misinvoicing?

Trade misinvoicing presents a more complex detection challenge than single-dimension price manipulation, because falsification can occur on three axes simultaneously and can be spread across a time series of transactions rather than appearing in a single anomalous invoice. AI and RegTech solutions address this through four primary mechanisms, each targeting a different dimension of the scheme.

Multi-dimensional price and description analytics apply machine learning to trade document data, simultaneously validating the declared price, the commodity code, the goods description, and the declared quantity against external reference data. Where a price benchmarking system alone would miss description falsification, a multi-dimensional model flags any combination of anomalies across the document set.

Network analytics linking trade flows and investment flows address the FDI integration variant. By mapping the relationship between a customer’s outbound trade payments and any subsequent inward investment receipts, graph-based tools identify the circular flow pattern that distinguishes trade-integrated money laundering from legitimate commercial activity.

Optical character recognition and document consistency checking automate the cross-document verification that is the primary defence against description and quantity falsification. These tools extract the goods description, quantity, and value from each document in the trade package and flag any inconsistencies. A system that checks every document against all others in the same set detects the internal inconsistencies that manual review would miss at scale.

Jurisdiction-specific risk scoring incorporates country risk assessments and geospatial transaction data to apply dynamic risk weights to every trade corridor in a portfolio. Where a customer’s trade flows shift towards higher-risk corridors, the system automatically escalates the review requirement for that relationship without requiring a manual trigger.

What Data Should Compliance Teams Collect to Detect Trade Misinvoicing?

| Data Point | Source System | What It Reveals |

| Commodity market price, classification, and description benchmarks | Commodity market data and trade intelligence platforms | Whether the declared price and goods description correspond to the standard classification and market value for that commodity code in the origin jurisdiction |

| Commodity transaction data: historic trade flows for the customer | Commodity transaction data platforms and trade registries | Whether the customer’s declared trade volumes and values are consistent with their industry position and historic activity profile |

| Beneficial ownership of all commercial counterparties | Company and beneficial ownership registries | Whether any counterparty is a shell entity, has no verifiable trading history, or shares ownership with other parties in the transaction chain |

| Correspondent and cross-border transaction data | Correspondent banking and cross-border payment records | Whether payment routing corresponds to the declared trade counterparty and whether settlement flows are consistent with standard correspondent banking patterns for the corridor |

| Customs and border records in the destination jurisdiction | Customs authority data-sharing channels and import declaration databases | Whether the receiving customs authority recorded the same goods description, quantity, and value as declared on the original commercial documents |

| Geographical and jurisdictional risk data | FATF, UAEFIU, and EOCN country risk databases | Whether the trade corridor or counterparty jurisdiction is assessed as elevated risk for trade-based money laundering, sanctions evasion, or proliferation financing |

| Geographical transaction data: trade flow mapping | Geospatial transaction analytics platforms | Whether the declared trade route reflects a logical commercial corridor or involves unnecessary routing through transit jurisdictions |

| Individual, entity, and public records databases | Company registries, litigation databases, and adverse media screening | Whether any party to the transaction is subject to adverse media, regulatory action, or known associations with financial crime |

| Trade documentation: complete set for each shipment | Internal document management and trade finance processing systems | Whether all documents in the same shipment package are internally consistent in goods description, quantity, declared value, and counterparty identities |

How Does Trade Misinvoicing Aggravate Jurisdictional Risk and Product Risk?

Jurisdictional Risk measures the degree to which a regulated entity’s exposure to a particular geography increases its overall money laundering and terrorist financing risk. Trade misinvoicing aggravates jurisdictional risk in two ways. First, it is structurally dependent on jurisdictional differentials: the scheme works because the origin and destination jurisdictions have different levels of customs scrutiny, commodity market transparency, or information-sharing capacity.

Second, the FDI integration variant creates a secondary jurisdictional exposure: the investment vehicle that receives the laundered proceeds is typically domiciled in a third jurisdiction chosen for its opacity, adding a second geographic risk layer to the transaction chain. An entity that processes trade finance for high-risk corridors, therefore, carries jurisdictional risk that is directly amplified by the scheme’s mechanics.

Product Risk is aggravated because trade finance products, including letters of credit, documentary collections, pre-shipment finance, and supply chain financing, are structurally incapable of verifying the accuracy of the commercial data against which they pay. The product’s own design assumes document accuracy; it has no mechanism for independently validating the goods. The greater the reliance on document compliance as the sole disbursement criterion, the greater the product’s structural exposure to this typology.

What Documentation Patterns Signal Trade Misinvoicing to a Compliance Officer?

The compliance officer reviewing a trade document package should treat the following as immediate escalation triggers. A goods description that uses generic or non-standard terminology where the product category would normally require specific technical descriptors indicates possible reclassification falsification.

A declared unit price that is inconsistent with current commodity market pricing for that specific goods category, combined with a bill of lading that records the same quantity as the invoice, suggests that quantity has been used as the falsification axis rather than price.

Where the same counterparty has presented multiple shipments over a short period with progressively adjusted declared values in the same direction, all upward or all downward, without any commodity market movement to explain the trend, the pattern is strongly indicative of systematic trade misinvoicing.

The compliance officer who builds a time-series view of a customer’s declared trade values, rather than reviewing each invoice in isolation, is far better positioned to detect this pattern before it reaches settlement.

Sectors at Highest Exposure

| Sector | Risk Rating | Reasoning |

| Trade Finance: banks and non-bank financial institutions | Critical | All three falsification types exploit the document-compliance structure of trade finance products; institutions paying against misinvoiced documents are the primary mechanism through which value transfer is completed |

| Import and Export Companies | Critical | Core actors as the entities generating and presenting falsified documents; their commercial legitimacy provides the cover for the scheme |

| Shipping and Logistics Companies | High | Potential knowing participants in quantity falsification through bill of lading misrepresentation; also inadvertent facilitators whose documentation supports misinvoiced claims |

| Foreign Direct Investment Vehicles | High | Used in the FDI integration variant to receive and recycle laundered proceeds as apparently legitimate inward investment |

| Free Zone Companies and Re-exporters | High | Free-zone infrastructure reduces customs documentation requirements at the point of re-export, enabling transit-based obscuring of goods provenance and value |

| Pre-Shipment Finance Providers | Moderate | Facilities sized against declared goods values are directly exposed when those values are deliberately understated or manipulated |

For Designated Non-Financial Businesses and Professions, trade misinvoicing risk arises indirectly. DNFBPs may not process the trade payment, but they may encounter clients whose source of funds derives from import-export activity, free zone trading, high-value goods transactions, or investment flows linked to trade proceeds. Suspicious ownership structures, source of funds explanations that rely on trade income without supporting documentation, and commercial arrangements that lack an evident economic rationale are the primary signals.

Under Cabinet Resolution No. (134) of 2025, Articles 6 through 9, CDD and EDD obligations apply where these signals are present regardless of whether the DNFBP is directly involved in the trade transaction.

Geographies and Contexts of Concern

The UAE’s position as a major re-export hub creates a specific structural exposure to trade misinvoicing across multiple vectors. High volumes of goods enter the UAE, are processed through free zones, and re-exported with amended documentation.

The UAE National Risk Assessment 2024 rates trade-based money laundering as a Medium-High risk. High-risk trade corridors include flows between the UAE and jurisdictions with limited customs verification capacity, opaque corporate registry infrastructure, or documented trade misinvoicing histories as confirmed in FATF typology reports.

Trade misinvoicing is also relevant to sanctions evasion and proliferation financing, where goods are misclassified, routed through third countries, or described in generic terms to obscure their dual-use or controlled nature. Compliance teams should treat vague goods descriptions, unusual routing, and counterparties linked to sanctioned or high-risk jurisdictions as escalation triggers under both AML and CPF frameworks.

Best Practices for Trade Misinvoicing Risk Management

- Apply multi-dimensional document verification to every trade finance transaction, covering price, quantity, and goods description simultaneously. A review process that checks only one dimension will miss falsification on the other two. Require that each document package is cross-checked against commodity market data for price, against shipping records for quantity, and against tariff code databases for goods description accuracy before payment is authorised.

- Integrate country risk assessment into the trade finance approval workflow. Before establishing any new trade finance facility, confirm that the proposed trade corridors have been assessed against FATF, UAEFIU, and EOCN high-risk jurisdiction lists. Apply enhanced scrutiny to all transactions in elevated-risk corridors and review the assessment whenever the counterparty adds new trade routes to the facility.

- Conduct beneficial ownership verification for all commercial counterparties before establishing or renewing any trade finance relationship. Cross-reference the disclosed counterparty against national and international registries. Any counterparty that cannot demonstrate a verifiable commercial history, physical premises, and an identifiable ultimate beneficial owner should be treated as a high-risk entity and conduct enhanced due diligence.

- Build trade-specific transaction monitoring rules that detect all three falsification types across a customer’s transaction history over time. A single anomalous invoice may not be detectable; the pattern across multiple shipments usually is. Design monitoring rules that flag progressive changes in declared goods values, sudden shifts in goods descriptions, and quantity inconsistencies across consecutive shipments in the same trade relationship.

- Require independent goods valuation for high-value or high-risk trade transactions as a disbursement condition within the letter of credit or documentary collection structure. Where the transaction value, corridor risk, or goods category presents elevated misinvoicing risk, condition payment on receipt of an independent third-party survey or inspection certificate confirming goods value and description.

- Cross-reference customs and border records in the destination jurisdiction against the original trade documentation. Establish information-sharing relationships with trade partners and customs authorities where available. Where destination customs records show a different quantity, value, or goods description than the original commercial documents, treat the discrepancy as a significant red flag and initiate an enhanced review.

- Apply transaction escrow management to high-risk trade finance transactions. Holding payment in escrow until goods delivery and independent value confirmation are received inserts a verification gate that prevents irrevocable value transfer before the accuracy of the commercial documents has been confirmed. This control is particularly effective for transactions in high-risk corridors or involving counterparties with limited verifiable trading history.

- Screen all inward Foreign Direct Investment flows for links to prior outward trade payments in the same corridor. Where an entity receiving inward FDI has also been a counterparty in outward trade payments, apply enhanced due diligence to the investment source-of-funds documentation and verify that the declared investment rationale has a credible commercial basis independent of the trade relationship.

- Maintain complete records such as all trade documentation, including invoices, bills of lading, packing lists, certificates of origin, letters of credit, independent inspection certificates, and payment instructions, for a minimum of five years as required by Article 25 of Cabinet Resolution No. (134) of 2025. Records must be linked to the relevant customer and transaction and be retrievable for supervisory inspection without delay.

- Conduct ongoing due diligence reviews of established trade finance relationships at regular intervals, not only at onboarding. Trade misinvoicing schemes often emerge within existing relationships after an initial period of legitimate activity. Periodic reviews should assess whether declared trade values, counterparties, and trade corridors remain consistent with the customer’s declared commercial purpose and risk profile.

- Provide trade-specific AML training to all staff involved in document review, pre-shipment finance approval, trade relationship management, and correspondent banking oversight. Training must address all three falsification variants, the documentation patterns that distinguish trade misinvoicing from legitimate commercial variance, and the escalation process for suspicious document packages. Refresher training must be delivered at least annually and whenever new UAEFIU or FATF guidance is issued on trade-based typologies.

- When a red flag is identified during document review or transaction monitoring, a compliance officer should follow a structured escalation sequence. The steps below apply to trade finance institutions; DNFBPs should adapt them to their own client-facing context.

- Pause or escalate the transaction before settlement where operationally possible. Do not allow payment to proceed while the review is open.

- Obtain clarification and supporting documentation from the customer. Request purchase agreements, independent appraisals, commodity price benchmarks, and any prior correspondence relevant to the declared goods value or description.

- Cross-reference the full document package: invoice, packing list, bill of lading, purchase order, letter of credit terms, and any available customs records. Identify every discrepancy across all three falsification dimensions.

- Conduct counterparty and ultimate beneficial owner checks against national registries, FATF high-risk jurisdiction lists, and sanctions lists. Confirm that all parties to the transaction have a verifiable commercial identity.

- Apply Enhanced Due Diligence if concerns remain after the initial review. Document the additional steps taken and the outcome of each.

- File a Suspicious Transaction Report through goAML without delay, where reasonable grounds for suspicion are formed. The obligation arises regardless of transaction value and is not contingent on completing the investigation.

- Do not disclose the STR or the existence of the review to the customer or any party to the transaction. Tipping off is a criminal offence under Article 29 of Federal Decree Law No. (10) of 2025.

How Trade Misinvoicing and Invoice Manipulation Are Related

Trade misinvoicing is a sub-technique within the broader category of invoice manipulation. Invoice manipulation covers any deliberate falsification of commercial invoice data, including value distortion, quantity misrepresentation, multiple invoicing for the same consignment, and phantom invoicing for goods that were never shipped. Trade misinvoicing encompasses the three most operationally common variants of these falsification methods.

It differs from inflated transaction pricing, which targets only one of those dimensions, in that it can exploit any combination of the three. A control framework calibrated to a single falsification type will miss the others entirely.

Understanding trade misinvoicing, a sub-technique within invoice manipulation, also informs compliance training design. Staff trained to recognise invoice manipulation generically acquire a conceptual framework that encompasses all variants; staff trained only on inflated transaction pricing acquire a more limited detection vocabulary.

Related Terms and Concepts

| Term | Connection to Trade Misinvoicing |

| Invoice Manipulation | Parent technique: trade misinvoicing is a sub-technique covering the three primary falsification axes, price, quantity, and description |

| Inflated Transaction Pricing | Sibling sub-technique within Invoice Manipulation, covering specifically the price over-statement axis; trade misinvoicing is broader |

| Trade-Based Money Laundering | The overarching typology family; trade misinvoicing is one of its primary operationalised techniques |

| Layering | The ML cycle stage at which trade misinvoicing operates, creating documentary distance between illicit funds and their criminal origin |

| Shell Companies | Frequently used as trading counterparties in misinvoicing schemes, providing apparent commercial justification for falsified transactions |

| Beneficial Ownership | Critical detection control: identifying the true owner of trading counterparties reveals affiliated-entity structures central to systematic misinvoicing |

| Letters of Credit | A primary trade finance instrument exploited in trade misinvoicing; its document-compliance payment structure creates the gap the scheme uses |

| Enhanced Due Diligence | The CDD standard applicable to high-risk trade relationships. |

| Suspicious Transaction Report | The obligatory report filed via goAML when grounds for suspicion of trade misinvoicing are identified and cannot be resolved |

| Jurisdictional Risk | The risk dimension most directly aggravated by trade misinvoicing, given the scheme’s structural dependence on cross-border regulatory differentials |

| Country Risk Assessment | The control that maps the jurisdictional risk dimension and triggers appropriate scrutiny for high-risk corridors |

Related Processes and Typologies

| Process or Typology | Connection |

| Trade-Based Money Laundering (TBML) | Overarching typology family |

| Under-Invoicing | Price manipulation variant: declaring a lower price than the true commercial value, used for customs duty evasion and value transfer |

| Over-Invoicing | Price manipulation variant: declaring a higher price to extract surplus funds through the trade payment |

| Multiple Invoicing | Sibling technique: generating more than one invoice for the same consignment |

| Phantom Invoice Fraud | Sibling technique: invoicing for goods that were not actually shipped |

Related Controls and Obligations

| Control or Obligation | Connection |

| Enterprise-Wide Risk Assessment (Article 5, CR 134/2025) | Requires product-level and corridor-level risk identification for all trade finance activities |

| Customer Due Diligence (Articles 6-9, CR 134/2025) | Foundational control for identifying counterparty ownership and commercial legitimacy |

| STR Obligation (Article 18, FDL 10/2025) | The reporting obligation triggered when grounds for suspicion of trade misinvoicing are formed |

| Record-Keeping (Article 25, CR 134/2025) | Five-year retention requirement for all trade documentation |

What Financial Instruments Do Criminals Use in Trade Misinvoicing Schemes?

Accounts receivable invoices are the foundational document of trade misinvoicing. Every falsification variant, price, quantity, or description is executed through the commercial invoice. The invoice is the primary determinant of the value declared to the bank, the value cleared through customs, and the value recorded on the payee’s books. By controlling the invoice, the criminal controls all downstream records of the transaction.

Letters of credit are the preferred payment instrument for large-value trade misinvoicing because they create an irrevocable bank payment commitment against the face value of the invoice. Once issued, the bank’s obligation to pay is tied to the document set, not to the goods. A letter of credit issued against a misinvoiced document package that passes the bank’s document compliance review will be paid in full.

Bank accounts facilitate both the settlement of trade payments and the cross-border movement of surplus value. Correspondent banking accounts are used to route payments between jurisdictions in ways that reduce the visibility of the end beneficiary. In the FDI integration variant, bank accounts in the receiving jurisdiction hold the laundered proceeds before they are channelled into investment vehicles.

Trade finance instruments generally, including pre-shipment finance, supply chain financing, and documentary collections, are exploited for the same structural reason as letters of credit: their payment obligations are tied to commercial document values rather than to independently verified goods values.

What Products and Services Do Criminals Abuse in Trade Misinvoicing Schemes?

Trade finance encompasses the full range of bank and non-bank products that facilitate international goods transactions. All trade finance products are structurally exposed to trade misinvoicing because they process payment based on commercial documents whose accuracy they do not independently verify. Letters of credit, documentary collections, supply chain financing, and invoice financing facilities each create a payment trigger tied to the declared document value.

Cross-border payment services are used to settle trade transactions and to move extracted surplus value between jurisdictions after the primary trade payment has been processed. Payment service providers with limited trade document integration cannot verify whether a cross-border payment corresponds to an accurate commercial transaction or carries laundered surplus above the true goods value.

Foreign investment services are abused in the FDI integration stage of the scheme. Investment advisers, fund administrators, and corporate structuring services that facilitate the deployment of proceeds from trade misinvoicing into investment vehicles provide the integration layer that makes the laundered funds appear as legitimate capital returns.

Freight forwarding and shipping services are integral to the physical execution of the scheme. Where a logistics provider issues transport documentation that records falsified quantities or assists in routing goods through transit jurisdictions to obscure provenance, it becomes a functional component of the misinvoicing infrastructure.

Invoice financing and pre-shipment finance are directly exposed when the underlying commercial documents have been falsified. A facility sized against a misinvoiced invoice, or against a pre-shipment financing request based on a falsified purchase order, advances funds against a false commercial value. The financing provider bears both the credit loss and the money laundering exposure.

Supply chain financing, trade documentation services, and trade facilitation services provide an administrative infrastructure for processing high volumes of trade documents. Without embedded price and description verification, these platforms are scalable channels for the submission of misinvoiced documents across a large transaction portfolio.

How AML UAE Helps Manage Trade Misinvoicing Risk

Trade misinvoicing is the broadest and most operationally adaptable technique within the invoice manipulation, requiring compliance frameworks to address price, quantity, and description falsification simultaneously and across a customer’s full transaction history rather than within individual invoices. Most institutions have controls designed for payment-level anomalies; very few have controls calibrated to all three falsification axes of trade misinvoicing.

AML UAE assists regulated entities in closing this gap through Enterprise-Wide Risk Assessment services that develop a trade-finance-specific risk profile, mapping exposure across all active trade corridors and product types.

For compliance teams building or upgrading their trade monitoring programmes, AML UAE’s transaction monitoring review service evaluates whether existing rules cover all three falsification axes and recommends targeted rule enhancements. AML UAE’s training programmes deliver scenario-based exercises across all three trade misinvoicing variants so that document reviewers, relationship managers, and senior compliance staff can identify the full range of red flags described in this article.

Closing Summary

Trade misinvoicing is distinguished from other invoice manipulation sub-techniques by its multi-axis structure. An institution whose detection controls address only one falsification dimension has solved only part of the problem. The remaining dimensions move through unimpeded, and the institution carries a risk exposure that its compliance programme has not measured.

Trade misinvoicing compliance also serves a dual regulatory purpose: failure to detect it creates AML exposure and CPF supervisory risk simultaneously. For compliance officers in UAE trade finance institutions, the practical priority is reviewing existing trade monitoring controls for coverage across all three falsification dimensions and confirming that country risk assessments for active corridors reflect current FATF guidance.

Frequently Asked Questions

Trade misinvoicing is a form of trade-based money laundering in which the price, quantity, or description of goods on commercial trade documents is deliberately falsified to transfer illicit value across borders. Unlike techniques that target only the invoice price, trade misinvoicing encompasses any dimension of the commercial document that can be distorted to create a gap between the declared and actual value of the transaction.

Inflated transaction pricing is specifically the overstatement of the invoice price above the true market value of the goods. Trade misinvoicing is broader: it encompasses price manipulation as one of three falsification axes and additionally covers deliberate misrepresentation of goods quantity and goods description. A compliance framework designed only to detect price anomalies will miss schemes that use description or quantity falsification as their primary mechanism.

Federal Decree Law No. (10) of 2025 is the primary legal instrument. Article 2 criminalises money laundering, which encompasses falsified trade documents. Article 19 mandates preventive measures. Cabinet Resolution No. (134) of 2025 provides operative compliance obligations, including EWRA at Article 5, CDD at Articles 6 through 9, STR filing at Article 18, and record-keeping at Article 25.

The three falsification axes are: price manipulation, in which the stated invoice value differs from the true market price; quantity manipulation, in which the declared number of units differs from the physical quantity shipped; and description falsification, in which the goods are misclassified or described inaccurately to obscure their true nature or market value. Each axis can be used independently or in combination.

Detection requires cross-referencing three datasets against the commercial document. The declared price must be checked against commodity market benchmarks. The declared quantity must be verified against independent shipping records or physical inspection data. The goods description must be confirmed against the tariff code and any available product specification documentation. Where any comparison produces a material discrepancy, the transaction should be escalated for enhanced review.

Trade misinvoicing is structurally dependent on jurisdictional risk: the scheme works because the origin and destination jurisdictions have different levels of customs scrutiny, regulatory capacity, or information-sharing willingness. Corridors with high jurisdictional differentials provide a more reliable environment for the scheme than flows between two well-regulated jurisdictions.

Regulated entities that identify documentation anomalies suggesting trade misinvoicing are required to file an STR with the UAEFIU via goAML, under Article 18 of Federal Decree Law No. (10) of 2025, STR must be filed without delay, with no minimum transaction value threshold. Suspicion arising from any combination of price, quantity, or description anomalies, including a pattern across multiple transactions, is sufficient to trigger the reporting obligation.

Financial institutions are supervised by the Central Bank of the UAE. Designated Non-Financial Businesses and Professions are supervised by the Ministry of Economy and Tourism (MoET) and the Ministry of Justice (MoJ). The UAEFIU receives all STRs and conducts financial intelligence analysis.

Administrative penalties under Article 17 of Federal Decree Law No. (10) of 2025 range from AED 10,000 to AED 5,000,000 per violation. Failure to file an STR carries criminal liability under Article 28, including imprisonment and fines between AED 100,000 and AED 1,000,000. DNFBP-specific penalties under Cabinet Resolution No. (71) of 2024 reach AED 500,000 for EDD and monitoring failures.

Transaction escrow management inserts a verification gate between the payment trigger and the irrevocable settlement of funds. By holding the payment in escrow until independent confirmation of goods delivery, quantity, and value is received, the institution retains the ability to stop a misinvoiced payment before it clears. This is one of the few controls that can reduce payment release risk in high-risk trade arrangements, although its commercial application is typically limited to high-value or elevated-risk transactions.

Strengthen Your Trade Finance Controls

See how better due diligence and document review can help reduce exposure to misinvoicing risk.

Share via :

About the Author

Pathik Shah

FCA, CAMS, CISA, CS, DISA (ICAI), FAFP (ICAI)

Pathik is an ACAMS-certified AML consultant specialising in governance, risk, and compliance for regulated entities in the UAE. He brings over 28 years of experience, with 1,000+ hours of AML training and 200+ advisory engagements across DNFBPs, VASPs, and FIs. He supports businesses in aligning with AML/CFT requirements from the CBUAE, DFSA, MoET, MoJ, VARA, CMA, FSRA, and FATF. Known for translating complex regulations into audit-ready procedures, Pathik enables operational clarity and compliance readiness.

Reach Out to Pathik