Cash Deposits

Last Updated: 05/18/2026

Protect your business with reliable and effective AML strategies with AML UAE.

Cash Deposits: Key Highlights

Placing physical currency into a bank account is the primary act through which criminal proceeds enter the financial system at the placement stage of money laundering.

Institutions without adequate cash monitoring and reporting face criminal and administrative liability under Federal Decree Law No. (10) of 2025.

Compliance teams must monitor structuring patterns across accounts and branches, not only individual threshold events.

What are Cash Deposits?

Cash deposit is the act of depositing physical currency into a bank account or equivalent financial product, which constitutes the most direct method of introducing illicit proceeds into the regulated financial system. In the context of anti-money laundering, cash deposits refer to any transaction in which banknotes or coins are placed into an account at a financial institution, whether through a branch teller, automated teller machine (ATM), or cash deposit machine, for the purpose of disguising the criminal origin of those funds.

The placement stage of money laundering, as documented in the Financial Action Task Force (FATF) methodology, treats physical cash as the most vulnerable point in a laundering cycle because it is the moment when criminal proceeds have the greatest physical traceability. Once deposited and recorded as bank transactions, the funds acquire the appearance of legitimacy and become significantly harder to identify.

Regulatory Reference

Federal Decree Law No. (10) of 2025 on Anti-Money Laundering, Combating the Financing of Terrorism and Proliferation Financing.

Article 2: Criminalises the acquisition, possession, use, or deposit of funds while knowing they are proceeds of a predicate offence.

Article 19: Requires all financial institutions and DNFBPs to establish preventive measures, including customer due diligence, to detect and prevent the entry of illicit funds into the financial system.

What does Cash Deposits Mean?

Think of the banking system as a large reservoir connected to the clean water supply. Illicit cash is muddy water that criminals need to pour in without triggering an alarm.

The reservoir has filters and sensors, but if the muddy water is poured in slowly, in small amounts, or through multiple entry points simultaneously, those filters can be overwhelmed.

Cash deposits work in the same way. Criminal proceeds are introduced through branches, ATMs, or third-party account holders, often in amounts calibrated to stay below detection thresholds, by criminals, to blend their illicit funds with the reservoir of legitimate deposits already circulating in the financial system.

Regulatory Framework Related to Cash Deposits

Federal Decree Law No. (10) of 2025, Article 2, criminalises the deposit of funds known to be proceeds of a predicate offence.

Article 19 requires all regulated entities to implement preventive measures sufficient to detect suspicious cash deposit activity.

Cabinet Resolution (134) of 2025, Article 18 imposes the obligation to file a suspicious transaction report immediately upon the formation of reasonable grounds for suspicion.

Article 7 sets the cash transaction CDD trigger for financial institutions at AED 55,000 for occasional transactions, whether single or linked.

Article 8 requires ongoing monitoring of all business relationships, with particular attention to transactions inconsistent with the institution’s knowledge of the customer’s financial profile.

Article 25 requires all records related to cash transactions to be retained for a minimum of five years.

Supervisory Authorities in UAE

The Central Bank of the UAE supervises financial institutions for AML/CFT compliance and establishes the Financial Intelligence Unit that receives suspicious transaction reports via goAML. For DNFBP sectors, the Ministry of Economy and Tourism and the Ministry of Justice are the primary supervisory authorities. The Gaming sector falls under the General Commercial Gaming Regulatory Authority.

Reporting or Compliance Obligations and Channels

All financial institutions and regulated DNFBPs must file suspicious transaction reports via the goAML platform immediately upon the formation of reasonable grounds for suspicion, under Federal Decree Law No. (10) of 2025, Article 18.

The STR obligation is not subject to a minimum transaction amount.

Cash transaction reports must be filed for transactions meeting or exceeding the applicable threshold, submitted via goAML.

The tipping-off prohibition under Federal Decree Law No. (10) of 2025, Article 29, carries criminal liability, including imprisonment and fines, for any disclosure that an STR has been filed.

Recent Developments, Enforcement Actions, or Supervisory Priorities

The introduction of Federal Decree Law No. (10) of 2025 and Cabinet Resolution No. (134) of 2025, effective December 2025, represents the most significant update to the UAE AML/CFT framework since Federal Decree Law No. (20) of 2018.

Compliance teams should verify that their policies and procedures reference the 2025 legislative instruments rather than the superseded 2018 framework.

The UAE National Risk Assessment 2024 identified cash as a high-risk instrument for money laundering. Supervisory authorities have signalled that cash transaction monitoring is a priority area in upcoming inspection cycles.

Why Cash Deposit Activity Matters for AML Compliance

Undetected cash deposit typologies allow criminal proceeds to transition from physical, traceable currency into electronically transferable funds within hours. Once that transition is complete, the funds can be moved internationally, converted into assets, or layered through a series of further transactions that rapidly obscure their origin.

Money laundering is most vulnerable to detection at the placement stage, which is precisely why regulatory frameworks in the UAE place explicit obligations on financial institutions to monitor cash transaction activity rigorously.

Financial institutions that allow structuring behaviour, third-party cash deposits, or disproportionate cash volumes to pass without scrutiny face substantial regulatory exposure.

Under Federal Decree Law No. (10) of 2025, Article 28, failure to file a suspicious transaction report where grounds for suspicion exist carries criminal liability, including imprisonment and fines of up to AED 1,000,000.

The administrative penalty schedule under Cabinet Resolution No. (71) of 2024 imposes fines of up to AED 500,000 for STR filing failures and up to AED 200,000 for customer due diligence deficiencies.

In addition, the consequence of inadequate cash deposit monitoring is the sustained facilitation of predicate crimes ranging from drug trafficking to fraud.

The UAE Financial Intelligence Unit receives suspicious transaction reports via the goAML platform and depends on the quality and timeliness of those reports to generate actionable intelligence.

Institutions that underinvest in cash monitoring capabilities not only expose themselves to regulatory penalties but also weaken the effectiveness of the national AML framework.

How Cash Deposits Operate as a Money Laundering Technique

The mechanics of cash deposit-based money laundering reflect a structured exploitation of the gap between the volume of cash transactions a financial institution processes and its capacity to apply granular scrutiny to each one.

The technique operates in stages, each stage designed to reduce detectability and increase the distance between the deposited funds and their criminal origin.

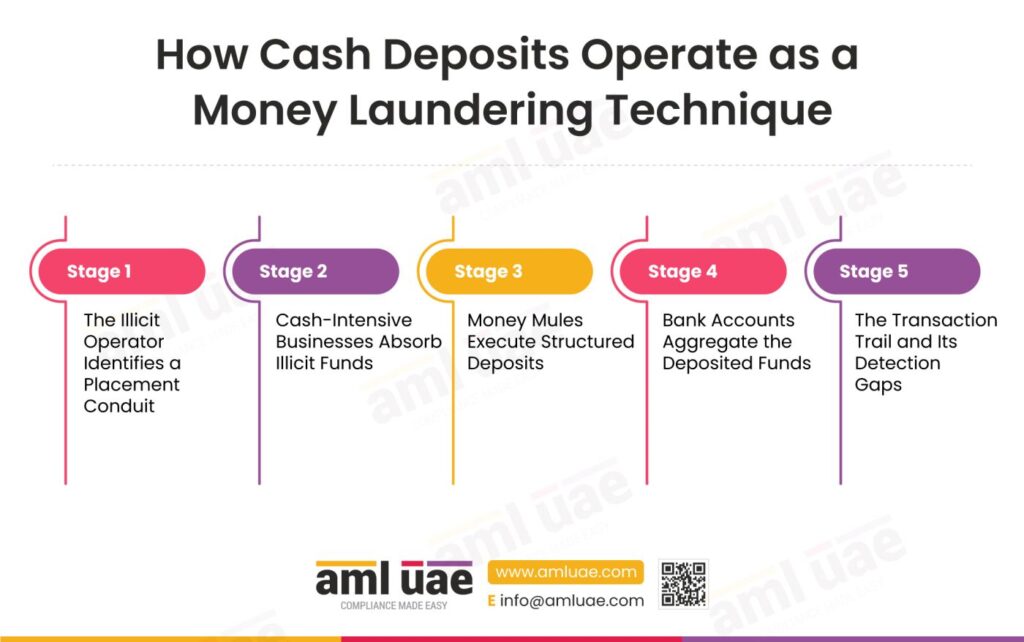

Stage One: The Illicit Operator Identifies a Placement Conduit

Before a single banknote enters a branch, the illicit operator conducts the equivalent of reconnaissance. The operator assesses which financial institutions, account types, and deposit channels impose the weakest scrutiny on incoming cash.

Institutions with legacy transaction monitoring systems, high-volume retail branches, or gaps in their automated cash deposit machine oversight are prioritised.

The operator then selects the mechanism, for instance, direct deposit through a cash-intensive business they control, engagement of third-party depositors, or a combination of both.

Stage Two: Cash-Intensive Businesses Absorb Illicit Funds

A cash-intensive business operated or controlled by the criminal network provides the most credible cover for placement.

Restaurants, retail outlets, car washes, and similar enterprises generate legitimate cash revenue on a daily basis.

Illicit cash is commingled with genuine takings, recorded in the business accounting records at inflated revenue figures, and deposited as a single consolidated amount.

The deposit appears consistent with the nature of the business.

Compliance teams reviewing the account in isolation see a business that deposits cash regularly and in amounts plausible for its declared sector.

Stage Three: Money Mules Execute Structured Deposits

Where a legitimate business front is unavailable or insufficient for the volume of cash to be placed, the illicit operator recruits money mules, which means individuals who deposit cash on behalf of the criminal network into their own accounts or into accounts opened specifically for this purpose. Each mule deposits an amount calibrated to remain below the cash transaction reporting threshold, a technique known as structuring or smurfing.

Mules operate across multiple branches and sometimes across multiple institutions on the same day, ensuring that no single branch records a transaction volume large enough to trigger an automatic alert.

Stage Four: Bank Accounts Aggregate the Deposited Funds

The accounts receiving the cash deposits function as collection points. Once funds are distributed across multiple accounts through multiple mules or transactions, a consolidation phase occurs: funds are transferred between accounts, often to a single account controlled by the operator, before being moved onward for layering.

The bank account is both an instrument and a camouflage; the electronic transfer phase that follows the deposit is structurally indistinguishable from legitimate inter-account transfers unless the deposit-to-transfer timeline and the cash origin of the funds are examined together.

Stage Five: The Transaction Trail and Its Detection Gaps

Cash transactions leave a partial trail that includes teller-recorded deposit receipts, ATM logs, geolocation data from ATM usage, and account activity logs. The detection gap exists because these data sources are often held in separate systems, reviewed at different intervals, and assessed against thresholds calibrated for individual transactions rather than patterns across accounts, branches, or time periods.

For instance, a cash deposit typology that spans fifty transactions, seven accounts, and three branches over ten days will not trigger a single-transaction alert, but will appear clearly in a network-level analysis that correlates deposit timing, amount, and geographic origin.

Real-World Examples of Cash Deposits in Money Laundering

The Commingling Restaurant: Illicit Cash Hidden in Legitimate Revenue

A restaurant operating in a high-footfall commercial district generates, on paper, USD 85,000 in daily cash revenue. The actual cash from legitimate customers amounts to USD 30,000. The remainder is illicit cash introduced by the beneficial owner, a participant in a narcotics distribution network. Both amounts are combined, counted, and deposited each evening as a single consolidated transaction. The bank account records show stable, high-volume daily deposits consistent with a busy food and beverage business.

The scheme begins to unravel when a compliance officer conducting an enhanced due diligence review notices that the restaurant declared seating capacity and known footfall data for its location cannot plausibly generate the recorded daily revenue. The disparity between observable capacity and reported cash income is the detection signal.

The lesson is that cash deposit typologies embedded within cash-intensive businesses are rarely detectable through transaction monitoring alone; they require cross-referencing account data against external benchmarks for the declared business sector.

The Structured Deposit Network: Smurfing Across Multiple Branches

An illicit operator holding AED 2,000,000 in criminal proceeds directs a network of fifteen money mules to deposit amounts between AED 30,000 and AED 45,000 each into their personal accounts over three days.

The deposits are made at different branch locations of the same institution, some via a teller and some via a cash deposit machine. No single account holder deposits more than AED 45,000 in the period, and no single branch records an unusual cash volume.

A network-level review subsequently identifies that all fifteen account holders share a common introducer: a registered mobile number associated with a single individual who opened several of the accounts.

The geographic clustering of the ATM deposits to two specific areas, combined with the temporal clustering of transactions over a 72-hour window, produces a risk score that triggers manual review.

The operational lesson is that structuring typologies are visible only at the network level, not the account level.

The Third-Party Depositor: Concealing the Source Through Proxies

A business account held by a limited liability company receives cash deposits from fifteen different individuals over the course of a month. The account holder cannot provide a credible explanation for why unrelated third parties are depositing cash into the business account. The account holder is a director of a company with minimal declared assets and no identifiable commercial premises.

The frequency of third-party cash deposits, the absence of any documented commercial relationship between the depositors and the company, and the company’s inability to produce invoices or contracts corresponding to the deposited amounts collectively constitute strong indicators of a cash placement scheme using third-party proxies.

The lesson is that third-party cash deposits into business accounts require specific documented justification; where that justification cannot be provided, the institution should apply enhanced due diligence and consider filing a suspicious transaction report.

What Are the Red Flags That Identify Cash Deposits?

| Category | Observation |

| Customer | Customer declared occupation or income source is inconsistent with the volume and frequency of cash deposits observed across a review period. |

| Customer | Customer is unable or unwilling to provide a credible explanation for large or frequent cash deposits during a standard customer due diligence review. |

| Customer | Customer exhibits reluctance when asked about the source of cash deposited, providing vague or contradictory explanations across different staff interactions. |

| Customer | Third-party individuals deposit cash into the same account repeatedly, and the account holder cannot document a commercial or familial relationship. |

| Transaction | Deposits are structured in amounts consistently just below the threshold that triggers a mandatory cash transaction report, occurring repeatedly in a short period. |

| Transaction | Deposit amounts are uniformly round figures or follow a narrow, repetitive pattern with no variation expected from genuine commercial activity. |

| Transaction | A single deposit significantly exceeds the account historical cash deposit levels or the account holder declared annual income. |

| Transaction | Multiple deposits are made across accounts held by the same customer within a short timeframe, with consolidated amounts that would be reportable in a single transaction. |

| Geographic | ATM usage and geolocation data shows cash deposit activity in locations inconsistent with the customer declared place of residence or business. |

| Geographic | Cash deposits are spread across multiple branches in different areas of the city with no operational reason visible in the customer profile. |

| Product | A business bank account receives cash deposits whose volume and frequency are disproportionate to the account holder declared sector, business size, or verified commercial activity. |

| Product | Multiple accounts held at the same institution by the same customer all receive cash deposits without a commercial rationale for using multiple accounts simultaneously. |

| Channel | Deposits made through cash deposit machines rather than branch tellers, avoiding face-to-face identification requirements or teller-level scrutiny. |

| Channel | Deposits followed within 24 to 48 hours by outward transfers in amounts closely corresponding to the deposited sums, indicating transit use of the account. |

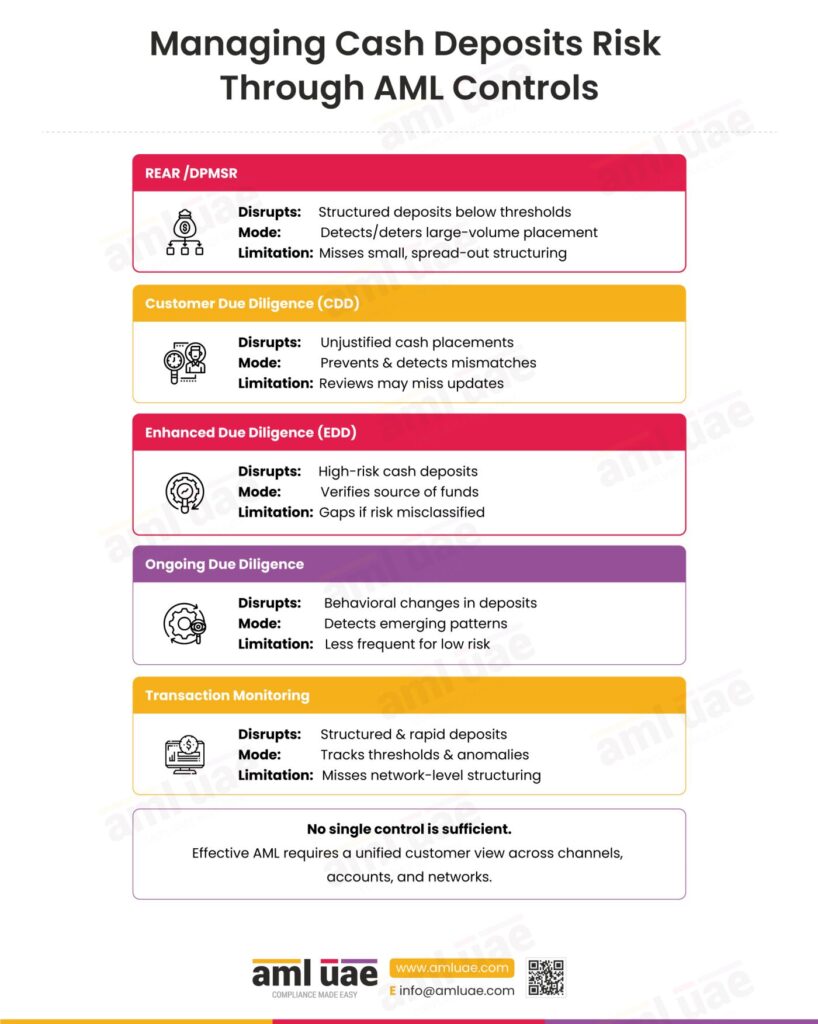

Managing Cash Deposits Risk Through AML Controls

| Control | What It Disrupts | Mode | Specific Limitation |

| REAR/DPMSR | Structured deposits designed to remain below thresholds by making the threshold visible to monitoring systems | Detects / Deters large-volume placement | Does not detect structuring below the threshold; mules calibrate deposits to exploit the threshold boundary spread over different months |

| Customer Due Diligence (CDD) | Placement through accounts where customer profile does not justify the cash volume | Prevents new placement relationships; Detects profile-transaction mismatches | Periodic; changes in deposit behaviour between review cycles may go undetected |

| Enhanced Due Diligence (EDD) | High-risk customer cash placement requiring source of funds verification | Detects unexplained cash in elevated-risk relationships | Applies only to designated risk categories; misclassification creates gaps |

| Ongoing Due Diligence | Changes in cash deposit behaviour after initial CDD | Detects post-onboarding pattern emergence | Review frequency is risk-based; lower-risk customers reviewed less frequently |

| Transaction Monitoring | Pattern-based cash deposit behaviour including structuring and velocity anomalies | Detects threshold-based deposits; structured activity; velocity anomalies | Rule-based monitoring calibrated to individual accounts misses network-level coordinated structuring |

How Do AI and RegTech Automate Detection of Cash Deposits?

Conventional transaction monitoring systems apply rule-based thresholds to individual account transactions. A deposit below the reportable threshold generates no alert, regardless of whether it is one of fifty similar deposits made by a coordinated mule network on the same day. AI-based transaction monitoring addresses this by shifting the unit of analysis from the individual transaction to the behavioural pattern, assessed across accounts, time periods, and geographic data simultaneously.

Graph analytics tools map the network connections between account holders, identifying cases where cash is deposited by unrelated individuals into the same destination account, or where a common introducer appears across multiple independently opened accounts. These tools surface structuring networks that are invisible to account-level monitoring.

Machine learning anomaly detection builds a behavioural baseline for each account and flags deviations that diverge from both the individual account history and peer group benchmarks. ATM geolocation data, when integrated with transaction monitoring, enables the detection of deposit activity inconsistent with the customer’s declared address or regular geographic footprint.

What Data Should Compliance Teams Collect to Detect Cash Deposits?

| Data Point | Source System | What It Reveals |

| ATM Usage and Geolocation Data | ATM network / core banking system | Geographic patterns inconsistent with declared location; clustering of activity around specific ATMs in a compressed time window |

| Account Activity Logs | Core banking / transaction monitoring | Velocity of cash deposits across review period; deposit-to-transfer timing; pattern changes following risk status changes |

| Bank Account Data | Core banking system | Total cash deposit volume relative to account type and declared income; number of accounts held by same customer receiving cash simultaneously |

| KYC and CDD Records | KYC platform / CRM | Declared source of funds and income; discrepancies between declared profile and deposit behaviour; third-party deposit authorisation records |

| Transaction Logs | Transaction monitoring / payment processing | Structuring patterns; round-figure repetition; deposit amounts followed by near-identical outward transfers within 24 to 48 hours |

How Do Cash Deposits Aggravate Channel Risk and Product Risk?

Cash deposit typologies aggravate Channel Risk by depositing physical currency through multiple channels simultaneously, like branch tellers, automated teller machines, cash deposit machines, and payment agents. Each channel applies different levels of identification and scrutiny, and criminal actors deliberately select channels that are easy to exploit.

Where an institution’s transaction monitoring system does not integrate data from all deposit channels into a unified customer view, gaps allow structuring and third-party deposit activity to go undetected across channel boundaries.

Product Risk is aggravated because cash deposits can be placed into a range of account types, including personal checking accounts, business bank accounts, and savings products, each subject to different monitoring parameters and risk classifications. Criminal actors exploit this by routing cash through product types perceived as lower-risk.

The multiplicity of products through which cash can be deposited means that monitoring calibrated to one account type does not automatically capture the same typological behaviour occurring in a different product category.

What Observable Indicators Should Compliance Officers Flag in Cash Deposit Cases?

Compliance officers reviewing accounts for cash deposit indicators should focus on observations, not conclusions. Account activity logs reveal deposits made in amounts consistently clustered below the cash transaction reporting threshold across multiple consecutive transactions.

Customer due diligence records contain a declared annual income that is demonstrably inconsistent with the cash deposit volume recorded over a six-month review period.

Branch records or ATM logs reflect deposits made by individuals other than the account holder into the same account, without any documentation of a business or familial relationship justifying those deposits.

Transaction logs show a pattern of cash deposits followed within 24 to 48 hours by outgoing transfers in amounts that correspond closely to the deposited sums.

KYC records show that a customer holds multiple accounts at the same institution and that cash is being deposited into several of those accounts simultaneously without a commercial rationale.

Sectors at Highest Exposure for Cash Deposits Risk

| Sector | Risk Rating | Specific Reasoning |

| Financial Institutions (Retail Banking) | Critical | Primary channel for cash deposit activity; volume creates monitoring burden criminals exploit; branch-level and ATM-level deposits are the most direct placement mechanism |

| Money Service Businesses (MSBs) | Critical | Process cash-to-electronic conversion; customer base includes elevated-risk cash users; role in transferring large amounts of cash across borders. |

| Cash-Intensive Businesses (Retail, Food and Beverage, Hospitality) | High | Generate legitimate cash revenues making them ideal commingling vehicles; inflated cash declarations structurally difficult to detect without sector-specific benchmarking |

| Dealers in Precious Metals and Precious Stones (DPMS) | High | DNFBP obligations triggered by cash transactions of AED 55,000 or more under CR 134/2025 Art. 3(3); cash placement through DPMS purchases exploits physical-to-asset conversion |

Geographies and Contexts of Concern in the UAE

The UAE 2024 National Risk Assessment identifies cash as a high-risk instrument for money laundering due to its historically significant use across retail and commercial sectors.

The cross-border cash dimension is particularly relevant: cash couriered from high-risk jurisdictions is physically deposited into UAE bank accounts, with couriers often operating as money mules for organised crime networks based outside the UAE.

The UAE Financial Intelligence Unit strategic analysis has identified fund movement through UAE financial institutions as a high-risk typology, with cash placement constituting the entry point for a significant proportion of reported suspicious transaction activity.

Best Practices for Cash Deposits Risk Management

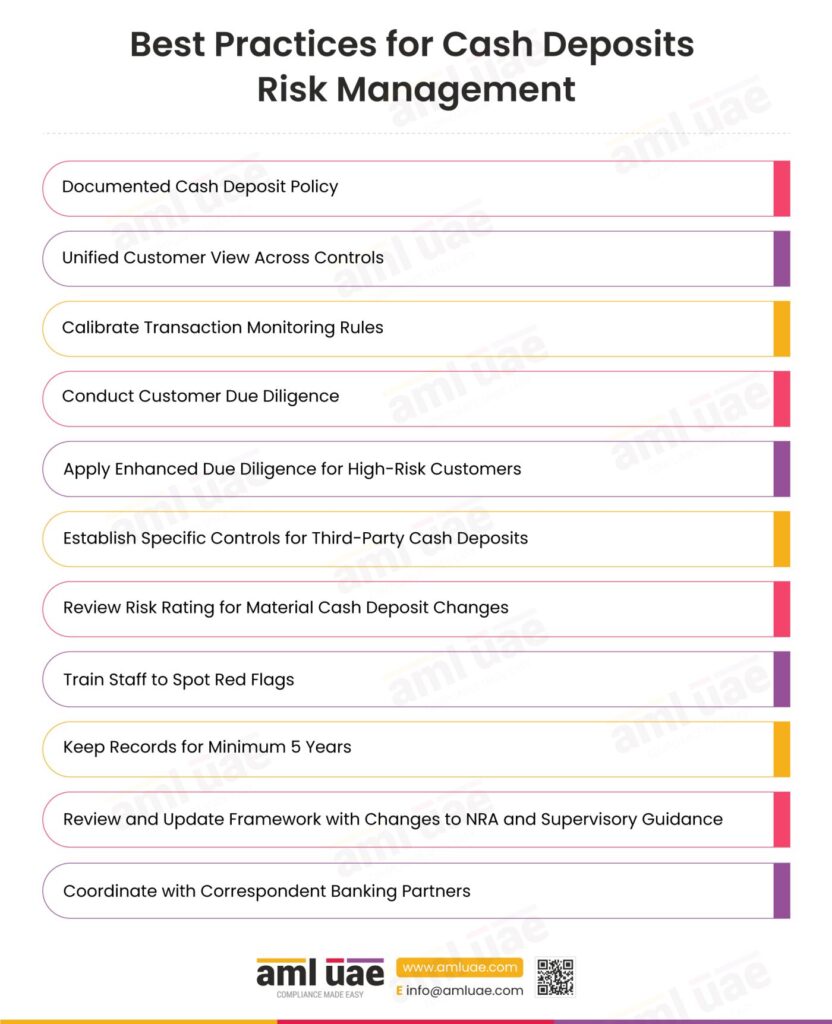

- Establish a documented cash deposit monitoring policy defining the institution’s risk appetite, alert thresholds, and escalation procedures specifically for cash transaction activity. The policy must be approved by senior management, reviewed annually, and updated whenever regulatory guidance changes in line with Cabinet Resolution No. (134) of 2025, Article 21.

- Implement a unified customer view across all deposit channels so that cash deposits made through branch tellers, ATMs, and cash deposit machines are aggregated into a single account-level view before transaction monitoring rules are applied. The unified view must include geolocation data from ATM deposits to enable analysis of geographic inconsistencies.

- Calibrate transaction monitoring rules to detect structuring behaviour specifically, such as repeated deposits in amounts consistently clustered below the cash transaction reporting threshold, made across short time intervals. Structuring detection rules should apply at the account, customer, and network levels, not only to individual transactions.

- Conduct customer due diligence with specific attention to source of funds verification for customers whose account activity includes regular or high-volume cash deposits. Declarations of income or business revenue should be cross-referenced against sector benchmarks and third-party data. For cash-intensive business customers, obtain and review financial accounts and verify declared cash revenues.

- Apply enhanced due diligence to all customer relationships where the cash deposit profile is elevated, such as high cash-to-total-deposit ratios, frequent deposits just below reportable thresholds, or unexplained third-party cash deposits, with senior management approval for continuation of the relationship.

- Establish specific controls for third-party cash deposits by defining the institution’s policy on permitting third parties to deposit cash into customer accounts, requiring documented authorisation from the account holder for any third-party deposit, and applying enhanced monitoring to accounts receiving repeated third-party cash deposits.

- Ensure that the ongoing due diligence process triggers a review of the customer risk rating when cash deposit behaviour changes materially from the established baseline. Automated alerts that flag significant changes in cash deposit velocity or volume relative to account history are an effective trigger for reactive review.

- Train frontline staff, particularly branch tellers and cash handling personnel, to identify and report internal suspicion indicators when processing cash deposits. Staff who interact directly with depositors can observe behavioural indicators that transaction monitoring systems cannot detect.

- File suspicious transaction reports promptly and accurately via the goAML platform immediately upon the formation of reasonable grounds for suspicion, under Federal Decree Law No. (10) of 2025, Article 18. The suspicion trigger is the presence of reasonable grounds for suspicion, not just the crossing of a monetary threshold.

- Maintain comprehensive records of all cash transaction activity for a minimum of five years from the date of the transaction, in accordance with Cabinet Resolution No. (134) of 2025, Article 25. Records should include deposit amounts, dates, channel used, and any customer interaction notes relevant to the transaction.

- Review and update the cash deposit monitoring framework whenever the UAE National Risk Assessment or sector-specific supervisory guidance identifies changes to the cash placement risk landscape.

- Coordinate with correspondent banking partners to share intelligence on cash deposit typologies identified in cross-border transactions. Cash physically couriered into the UAE and deposited into domestic accounts creates a cross-border dimension that domestic monitoring alone cannot address.

These twelve practices only work when they operate as a system, not a checklist. The single biggest lift comes from unifying the customer view across tellers, ATMs, and CDMs; without it, structuring hides in plain sight. Calibrate rules at the network level, not the transaction level, and treat any unexplained third-party deposit as a hard stop, not a soft flag. Frontline observation closes what monitoring misses.

Related Terms and Concepts

| Term | Connection to Cash Deposits | |

| Placement | Cash deposits are the primary mechanism through which the placement stage of the money laundering cycle is executed | |

| Structuring (Smurfing) | The practice of breaking a large cash deposit into smaller amounts to avoid reporting thresholds; the most common sub-typology within the broader cash deposits category | |

| Money Mule | Individuals who physically execute cash deposits on behalf of an illicit operator; the mule account is the vehicle through which the typology operates at the transactional level | |

| Suspicious Transaction Report (STR) | Must be filed when any cash deposit activity creates reasonable grounds for suspicion, regardless of the transaction amount | |

| Customer Due Diligence (CDD) | The process through which an institution verifies the customer identity and assesses the expected cash deposit profile; the foundational control | |

| Enhanced Due Diligence (EDD) | Applies to elevated-risk cash deposit relationships; requires additional verification of source of funds and increased monitoring frequency | |

| Transaction Monitoring | Systems that apply rules and models to identify cash deposit patterns including structuring, velocity, and network-level behaviour | |

| Beneficial Owner | Identifying the beneficial owner of accounts receiving high-volume cash deposits is critical; beneficial ownership opacity is frequently used to conceal the ultimate recipient | |

| Commingling | Mixing illicit cash with legitimate business revenue before deposit; the technique through which cash-intensive businesses obscure the criminal origin of funds | |

| Financial Intelligence Unit (FIU) | The CBUAE FIU receives STRs, DPMSRs, REARs via goAML and generates strategic financial intelligence used to detect and disrupt cash placement operations | |

| Anti-Money Laundering (AML) | The overarching regulatory and operational framework within which cash deposit monitoring, reporting, and CDD obligations are situated

| |

| Cash Intensive Business Deposit | The specific variant where a business with legitimate cash revenues is used as a commingling vehicle for illicit cash deposits | |

| Bulk Cash Smuggling | Physical transportation of large quantities of cash across borders before deposit into the domestic banking system | |

| Currency Deposits | Synonymous with cash deposits in most regulatory contexts | |

What Products and Services Do Criminals Abuse in Cash Deposits Schemes?

Business Bank Accounts are the product most extensively abused in cash deposit schemes because they offer institutional legitimacy for high-volume cash activity.

Criminals establish companies in cash-intensive sectors, open business accounts consistent with that declared activity, and use those accounts to deposit illicit cash alongside whatever genuine revenue the business generates.

The business account expected cash profile provides a normative baseline that the institution’s monitoring system accepts as legitimate, allowing placement to proceed under commercial cover.

Cash Transaction Services at branches and ATMs are abused as the physical interface through which deposits are made.

ATM and cash deposit machine services are exploited precisely because they accept deposits without human review of the depositor’s identity or the stated purpose of the transaction.

Personal Checking Accounts are abused as mule accounts. Accounts opened by individuals who accept payment for allowing their personal accounts to be used as conduits for cash placement.

How AML UAE Helps Businesses to Manage Cash Deposit Risk

AML UAE is a compliance advisory and consulting firm that helps businesses manage cash deposit risk by addressing a key challenge in compliance systems: fragmented data.

Transaction records, KYC information, ATM geolocation data, and branch-level observations often exist in separate systems, making it difficult to identify behavioural patterns such as structuring, unusual cash velocity, or cross-account activity. Our approach focuses on connecting these data points to strengthen risk visibility and improve the effectiveness of controls.

Our financial crime risk assessment service maps cash deposit exposure across customer segments, accounts, and channels, producing a risk-based view of vulnerabilities along with a gap analysis aligned with Federal Decree Law No. (10) of 2025 and Cabinet Resolution No. (134) of 2025. In addition, our AML training programmes equip branch staff, analysts, and senior management with practical skills to effectively identify and manage cash-related financial crime risks.

The most persistent challenge in cash deposit monitoring is not the volume of transactions but the fragmentation of the data. Compliance teams see teller records in one system, ATM logs in another, and KYC files in a third. By the time an analyst pieces together that the same person has deposited cash at seven different branches over ten days, the funds have already been transferred three times. The institutions that detect cash placement early are the ones that have invested in the unified view, not the ones with the most sophisticated alert rules running against siloed data.

Conclusion: Cash Deposits

Cash deposits occupy a unique position in the AML landscape because they represent the point at which criminal proceeds are most physically tangible and most vulnerable to detection.

The transition from physical cash to an electronic ledger entry is irreversible in terms of detection. Once deposited and transferred, funds lose the properties that made them traceable as physical currency. This is why the placement stage, and the cash deposit typologies that execute it, must be the first line of defence in any institution’s financial crime programme.

Regulatory compliance in the UAE context requires institutions to go beyond threshold-based reporting and build a genuine understanding of each customer’s expected cash behaviour. The obligations under Federal Decree Law No. (10) of 2025 and Cabinet Resolution No. (134) of 2025 requires a monitoring capability that detects structuring, commingling, third-party deposit patterns, and velocity anomalies that no single threshold rule will surface. The institutions that meet this standard are those that have invested in integration across their deposit channels, their KYC systems, and their transaction monitoring systems.

The consequence of falling short is not only a regulatory penalty but an active contribution to the criminal economy. Robust cash deposit monitoring is not a regulatory compliance checkbox; it is a structural contribution to the integrity of the financial system.

Frequently Asked Questions

In AML terms, a cash deposit is the act of placing physical currency into a bank account or equivalent financial product. The AML significance lies in its role as the primary placement mechanism in money laundering: the moment when criminal proceeds in physical form enter the formal financial system and assume the appearance of legitimate funds.

Structuring is the deliberate practice of breaking a large cash deposit into multiple smaller deposits to keep the total below the threshold. It is a criminal offence when committed with the intent to evade reporting obligations and is one of the most common sub-typologies within the broader category of cash deposits.

Financial institutions in the UAE must file suspicious transaction reports (STR) for qualifying transactions via goAML immediately upon reasonable grounds for suspicion under Federal Decree Law No. (10) of 2025, Article 18, regardless of transaction amount.

Money mules are often individuals recruited through social media, job advertisements, or personal networks. They are typically identified by modest declared income inconsistent with deposit volumes, accounts opened recently with limited prior transaction history, and repeated cash deposits followed by near-immediate outward transfers.

Commingling is the mixing of illicit cash with legitimate business revenue before deposit. A cash-intensive business commingles criminal proceeds by including them in its daily cash takings. Detection is difficult because the deposit is consistent with the business-declared sector and scale, necessitating cross-referencing against sector benchmarks.

Effective cash deposit monitoring requires integration of five data sets: ATM usage and geolocation data, account activity logs, bank account transactional data, KYC and CDD records, and transaction logs from all deposit channels. Integration into a unified customer view is the technical prerequisite for detecting network-level structuring.

Under Federal Decree Law No. (10) of 2025, Article 28, failure to file an STR carries criminal liability, including imprisonment and fines of up to AED 1,000,000. Administrative penalties under Cabinet Resolution No. (71) of 2024 impose fines of up to AED 500,000 for STR filing failures and up to AED 200,000 for CDD failures.

Yes. Many legitimate businesses receive substantial cash revenues. The AML concern arises when the volume, frequency, or pattern of cash deposits is inconsistent with the account holder’s declared sector, business size, and verified commercial activity. Compliance teams assess cash deposits in context rather than in isolation.

ATM geolocation data enables the identification of deposit activity that is geographically inconsistent with the customer’s declared address or regular behavioural footprint. A customer whose deposits are systematically clustered around ATMs remote from both their home and business address presents a spatial indicator that enhances the evidential picture supporting suspicion.

Cabinet Resolution No. (134) of 2025, Articles 5 and 21, require all regulated entities to implement risk-based AML programmes, including specific controls for cash deposit activity. The 2024 National Risk Assessment has elevated cash as a high-risk instrument, signalling that inadequate cash monitoring is a specific supervisory priority.

Protect Your Institution from Deposit-Related AML Risks

Get tailored support on managing cash deposit monitoring, structuring detection, and reporting thresholds.

Share via :

About the Author

Pathik Shah

FCA, CAMS, CISA, CS, DISA (ICAI), FAFP (ICAI)

Pathik is an ACAMS-certified AML consultant specialising in governance, risk, and compliance for regulated entities in the UAE. He brings over 28 years of experience, with 1,000+ hours of AML training and 200+ advisory engagements across DNFBPs, VASPs, and FIs. He supports businesses in aligning with AML/CFT requirements from the CBUAE, DFSA, MoET, MoJ, VARA, CMA, FSRA, and FATF. Known for translating complex regulations into audit-ready procedures, Pathik enables operational clarity and compliance readiness.

Reach Out to Pathik