AML Regulations for Real Estate Agents and Brokers in UAE

Published On: 04/28/2026

Protect your business with reliable and effective AML strategies with AML UAE.

Last Reviewed On: 07/21/2026 | Last Updated On: 07/21/2026

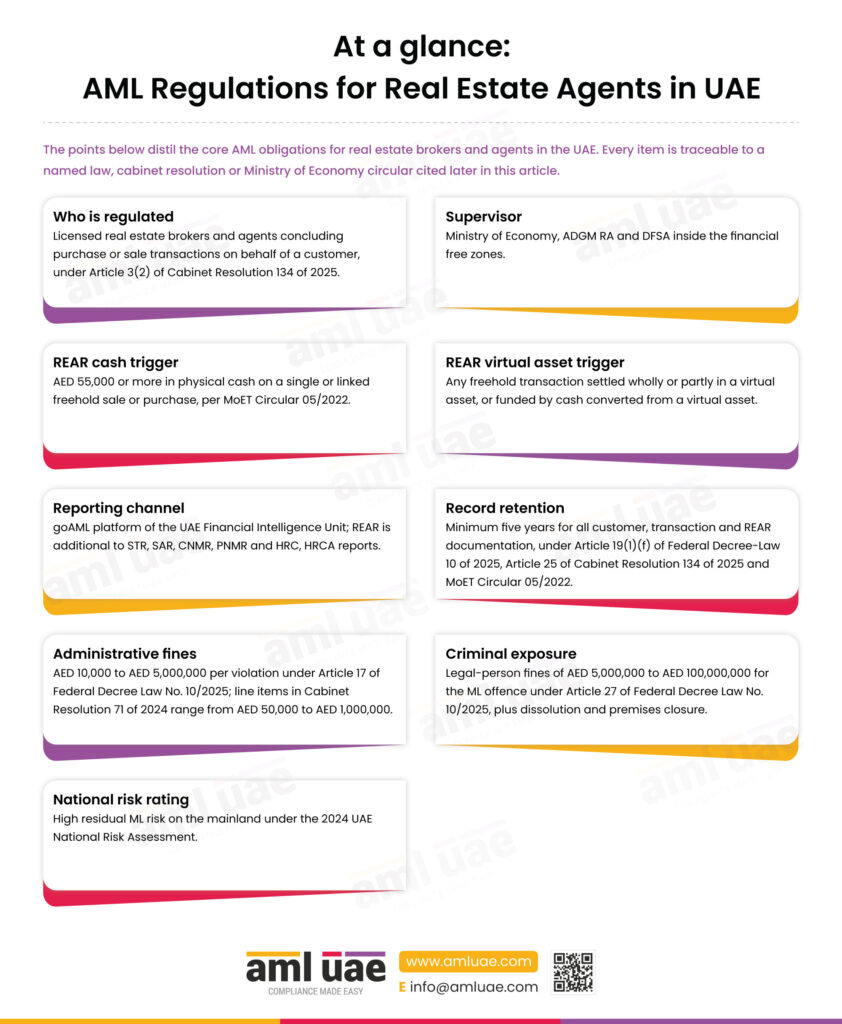

At a glance: AML regulations for real estate agents in UAE

The points below distil the core AML obligations for real estate brokers and agents in the UAE. Every item is traceable to a named law, cabinet resolution or Ministry of Economy circular cited later in this article.

Who is regulated

Licensed real estate brokers and agents concluding purchase or sale transactions on behalf of a customer, under Article 3(2) of Cabinet Resolution 134 of 2025.

Supervisor

Ministry of Economy, ADGM RA and DFSA inside the financial free zones.

REAR cash trigger

AED 55,000 or more in physical cash on a single or linked freehold sale or purchase, per MoET Circular 05/2022.

REAR virtual asset trigger

Any freehold transaction settled wholly or partly in a virtual asset, or funded by cash converted from a virtual asset.

Reporting channel

goAML platform of the UAE Financial Intelligence Unit; REAR is additional to STR, SAR, CNMR, PNMR and HRC, HRCA reports

Record retention

Minimum five years for all customer, transaction and REAR documentation, under Article 19(1)(f) of Federal Decree-Law 10 of 2025, Article 25 of Cabinet Resolution 134 of 2025 and MoET Circular 05/2022.

Administrative fines

AED 10,000 to AED 5,000,000 per violation under Article 17 of Federal Decree Law No. 10/2025; line items in Cabinet Resolution 71 of 2024 range from AED 50,000 to AED 1,000,000.

Criminal exposure

Legal-person fines of AED 5,000,000 to AED 100,000,000 for the ML offence under Article 27 of Federal Decree Law No. 10/2025, plus dissolution and premises closure.

National risk rating

High residual ML risk on the mainland under the 2024 UAE National Risk Assessment.

AML regulations for real estate agents in UAE sit at the intersection of federal AML law, Ministry of Economy sector supervision and the UAE Financial Intelligence Unit reporting regime. Every licensed real estate broker or agent concluding a purchase or sale on behalf of a customer is a Designated Non-Financial Business and Profession (DNFBP) under Article 3(2) of Cabinet Resolution 134 of 2025, and must operate a risk-based AML/CFT/CPF programme anchored in Federal Decree-Law 10 of 2025. This article walks through who qualifies as a regulated real estate broker, who supervises the sector, which specific laws and circulars apply, and which obligations actually bite on a typical freehold transaction.

Real estate is not a low-risk sector in the UAE. The 2024 National Risk Assessment rates mainland real estate brokers and agents at high residual ML risk, driven by cash-intensive transactions, foreign buyers and the use of legal persons to hold residential property. The FIU strategic analysis reviewed 976 Real Estate Activity Reports and 405 suspicious reports from real estate agents and brokers for the period 2020 to 2023, and the dominant typologies and red flags from that analysis are now embedded in the Ministry of Economy supervision.

To see how this page fits the wider AML framework, start with the DNFBPs pillar page and the hub guide to AML laws in UAE. If you operate inside the ADGM or DIFC, the regime is materially different and is covered in our ADGM AML regulations and DIFC AML regulations pages.

AML regulations for real estate agents in UAE

Four pillars of sector compliance walked through in this article, each anchored in specific UAE laws, circulars and guidance.

1. Who counts as a broker or agent

The DNFBP scope test under Article 3(2) of Cabinet Resolution 134 of 2025, plus Ministry of Economy scope statements

2. Who supervises the sector

Ministry of Economy and Tourism (MoET) for mainland and Commercial Free Zones, with distinct regimes for ADGM and DIFC.

3. Applicable laws and guidance

Federal decree-law, executive regulations, EOCN and FIU guidance, NRA, DNFBP circulars and real estate sector guidance.

4. Conclusion and obligations

Practical synthesis of CDD, REAR, STR, UBO and record-keeping duties, plus main red flags and penalties.

Who Counts as a Real Estate Agent or Broker for AML Purposes in the UAE?

For AML purposes in the UAE, a real estate agent or broker is any licensed natural or legal person that concludes a purchase or sale of real estate on behalf of a customer. That scope is set by Article 3(2) of Cabinet Resolution 134 of 2025, which replaced Cabinet Decision 10 of 2019 as the executive regulation of the federal AML decree-law.

Cabinet Resolution 134 of 2025 lists seven categories of Designated Non-Financial Businesses and Professions. Brokers and real estate agents are the second category, defined as DNFBPs when concluding transactions or settlements on behalf of their customers for the purchase or sale of real estate. The trigger is the act of concluding a purchase or sale for a client, not the act of holding a trade licence. Marketing, property management, valuation, and pure leasing work fall outside the statutory DNFBP scope, although the Ministry of Economy’s Supplemental Guidance for the Real Estate Sector notes that brokers should apply similar AML controls to lease transactions when the risk profile is comparable.

The Ministry of Economy reinforces the scope in its foundational Circular No. 1/2021 to real estate brokers and agents and in the September 2025 AML/CFT Guidelines for DNFBPs, both of which confirm that every brokerage concluding a purchase or sale for a customer is a DNFBP and must register on goAML, appoint a compliance officer and operate a full AML/CFT/CPF programme.

Lawyers, notaries and independent legal professionals become DNFBPs when preparing, conducting or executing financial transactions for a client concerning the purchase and sale of real estate (Article 3(4)(a) of Cabinet Resolution 134 of 2025). Company and Trust Service Providers become DNFBPs when acting as agents in the incorporation of legal persons that hold real estate. Dealers in precious metals and stones become DNFBPs at the AED 55,000 single or linked cash transaction threshold. Those adjacent categories are covered in the DNFBPs pillar page and in the specific lawyers and notaries, TCSPs and DPMS pages.

Scale of the regulated population: the UAEFIU 2023 Strategic Analysis Report on Real Estate Money Laundering records 4,446 registered real estate agents and brokers as of September 2023. The 2024 National Risk Assessment notes that approximately 99.8 per cent of real estate agents operate in the mainland and commercial free zones under Ministry of Economy oversight, with only a small minority inside the financial free zones supervised by the DFSA and the ADGM.

Scope test in one sentence

If your firm is licensed as a real estate broker or agent in the UAE and you conclude the purchase or sale of real estate for a customer, you are a DNFBP under Article 3(2) of Cabinet Resolution 134 of 2025 and all obligations in this article apply, regardless of brokerage size, nationality of clients or property value.

Not sure whether you are a regulated DNFBP?

If your brokerage wants a second opinion on DNFBP scope, CDD trigger points or REAR reporting boundaries, the AML UAE team runs scoping assessments for real estate firms of every size.

AML Supervisory Authority for Real Estate Agents and Brokers in UAE

The AML supervisory authority for real estate agents and brokers on the UAE mainland and in commercial free zones is the Ministry of Economy and Tourism (MoET). The MoET was designated as the supervisor of DNFBPs in 2019 under Cabinet Resolutions 28/4/M and 3/1 and continues to hold that role under the regime introduced by Federal Decree-Law 10 of 2025 and Cabinet Resolution 134 of 2025.

The Ministry of Economy and Tourism issues binding sector circulars, publishes implementation guides, runs risk-based on-site and off-site inspections, operates the supervisory grievance system and acts as the gateway for administrative fines under Cabinet Resolution 71 of 2024. Every licensed real estate broker or agent on the mainland or in a commercial free zone registers, communicates and reports to the Ministry of Economy and Tourism.

Inside the two financial free zones, supervision is different. The ADGM Registration Authority (ADGM RA) supervises real estate activity within ADGM. The Dubai Financial Services Authority (DFSA) supervises real estate activity within DIFC. These regimes apply their own AML rulebooks and are not covered by this page.

Two other federal authorities form essential touch points for every broker, even under the Ministry of Economy supervision. The UAE Financial Intelligence Unit receives all REAR, STR, SAR, CNMR, PNMR, and HRC reports through goAML. The Executive Office for Control and Non-Proliferation (EOCN) administers the UAE Targeted Financial Sanctions list and the Automatic Reporting System for sanctions screening outcomes. Ministry of Economy and Tourism circulars require brokers to register with the EOCN Notification Alert System (NAS) and to use the Automatic Reporting System on sanctions matches.

A single brokerage can touch more than one supervisor on a given deal. A mainland broker that introduces a property within DIFC to a client, or uses a DIFC-licensed law firm to conclude the transaction, still carries its own Ministry of Economy obligations in parallel with the DIFC obligations of the legal counterpart. See the DIFC AML regulations page and ADGM AML regulations page for each free-zone regime.

AML Regulations Applicable to Real Estate Agents and Brokers in UAE

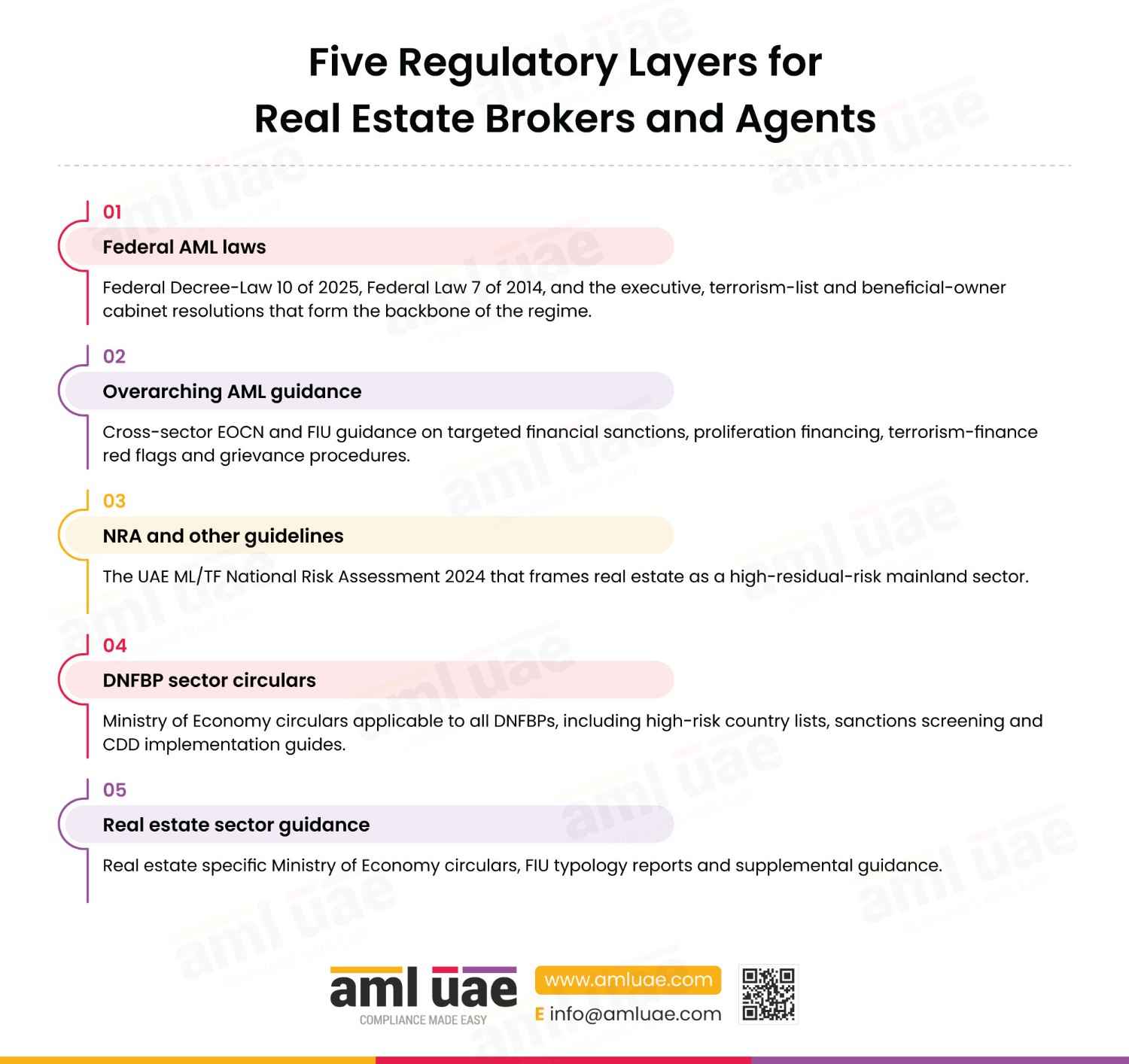

The AML regulations applicable to real estate agents and brokers in UAE sit in five concentric layers: federal laws and executive regulations, overarching EOCN and FIU guidance, the national risk assessment, DNFBP-wide Ministry of Economy and Tourism circulars, and sector-specific real estate guidance. Each layer speaks to a different part of the compliance programme, and a real estate broker is expected to read down through all five.

Five regulatory layers for real estate brokers and agents

1. Federal AML laws

Federal Decree-Law 10 of 2025, Federal Law 7 of 2014, and the executive, terrorism-list and beneficial-owner cabinet resolutions that form the backbone of the regime.

2. Overarching AML guidance

The UAE ML/TF National Risk Assessment 2024 that frames real estate as a high-residual-risk mainland sector.

3. NRA and other guidelines

The UAE ML/TF National Risk Assessment 2024 that frames real estate as a high-residual-risk mainland sector.

4. NRA and other guidelines

Ministry of Economy circulars applicable to all DNFBPs, including high-risk country lists, sanctions screening and CDD implementation guides.

5. Real estate sector guidance

Real estate specific Ministry of Economy circulars, FIU typology reports and supplemental guidance.

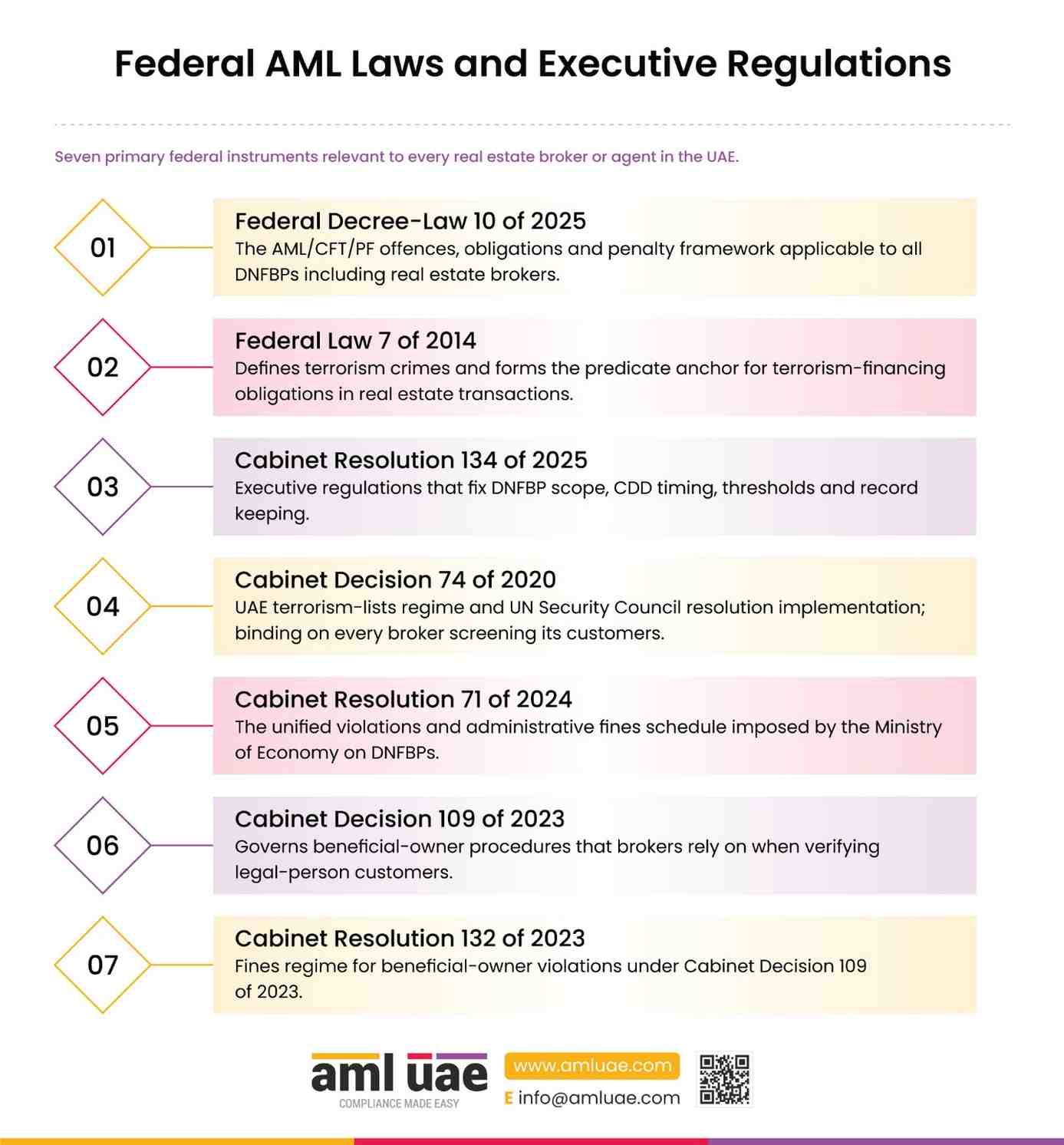

Federal AML Laws and Executive Regulations Applicable to the Real Estate Sector

These seven federal instruments define the offence structure, set the DNFBP scope, regulate beneficial ownership and provide the administrative penalty schedule that the Ministry of Economy applies to real estate brokers. They form the non-negotiable statutory floor for every real estate AML programme.

1. Federal Decree-Law 10 of 2025

The AML/CFT/PF offences, obligations and penalty framework applicable to all DNFBPs including real estate brokers.

2. Federal Law 7 of 2014

Defines terrorism crimes and forms the predicate anchor for terrorism-financing obligations in real estate transactions.

3. Cabinet Resolution 134 of 2025

Executive regulations that fix DNFBP scope, CDD timing, thresholds and record keeping.

4. Cabinet Decision 74 of 2020

UAE terrorism-lists regime and UN Security Council resolution implementation; binding on every broker screening its customers.

5. Cabinet Resolution 71 of 2024

The unified violations and administrative fines schedule imposed by the Ministry of Economy on DNFBPs.

6. Cabinet Decision 109 of 2023

Governs beneficial-owner procedures that brokers rely on when verifying legal-person customers.

7. Cabinet Resolution 132 of 2023

Fines regime for beneficial-owner violations under Cabinet Decision 109 of 2023.

1. Federal Decree-Law No. (10) of 2025 Regarding Anti-Money Laundering, and Combating the Financing of Terrorism and Proliferation Financing

This is the governing AML/CFT/PF statute for every real estate broker in the UAE. Article 2 defines money laundering; Article 3 defines the financing of terrorism and proliferation; Article 18 requires reporting of suspicious transactions through the Financial Intelligence Unit; Article 19(1)(e) imposes targeted financial sanctions duties; Article 24 protects the confidentiality of reports (with tipping-off penalised under Article 29); and Articles 17, 27, 28, 29, 32, 33 and 35 set the administrative and criminal penalty framework. The DNFBP definition that captures real estate brokers sits in the definitions chapter of this decree-law and is fleshed out in its executive regulation, Cabinet Resolution 134 of 2025.

2. Federal Law No. (7) of 2014 Combating Terrorism Crimes

Federal Law 7 of 2014 defines terrorism offences, terrorist organisations and terrorist acts in the UAE. It is the predicate statute that underpins the terrorism-financing obligations imposed on real estate brokers under Federal Decree-Law 10 of 2025, Cabinet Decision 74 of 2020 and the EOCN Targeted Financial Sanctions guidance. Brokers who encounter a customer match on a terrorism sanctions list apply the sanctions regime by reference to this statute.

3. Cabinet Resolution No. (134) of 2025 Concerning the Executive Regulations of Federal Decree-Law No. (10) of 2025 Concerning Combating Money Laundering, Terrorist Financing, and the Financing of the Proliferation of Weapons

Cabinet Resolution 134 of 2025 is the practical rulebook that real estate brokers apply every day. Article 3(2) places brokers and agents within the DNFBP perimeter; Articles 5 to 9 set the risk-based approach and customer due diligence timing; Article 10 addresses beneficial-owner identification; Article 16 governs enhanced due diligence for politically exposed persons; Article 21 fixes internal programme, compliance officer and training requirements; and Article 25 sets the five-year record-keeping duty. This resolution replaces Cabinet Decision 10 of 2019, but circulars issued under the 2019 regulation remain valid unless specifically repealed.

4. Cabinet Decision No. (74) of 2020 Regarding Terrorism Lists Regulation and Implementation of UN Security Council Resolutions on the Suppression and Combating of Terrorism, Terrorist Financing, Countering the Proliferation of Weapons of Mass Destruction and related resolutions

Cabinet Decision 74 of 2020 establishes the UAE Local Terrorism List, governs listing and delisting procedures and implements UN Security Council resolutions 1267, 1373, 1718, 2231 and their successors. Real estate brokers use this instrument, together with the EOCN NAS and Automatic Reporting System, to screen every customer, beneficial owner and counterparty. A confirmed match triggers a freeze, a Confirmed Name Match Report (CNMR) on goAML and immediate notification to the EOCN.

5. Cabinet Resolution No. (71) of 2024 Regulating Violations, Administrative Penalties Imposed on Violators of Measures for Confronting Money Laundering and Combating Financing of Terrorism Subject to the Control of the Ministry of Justice and the Ministry of Economy

Cabinet Resolution 71 of 2024 is the unified penalty schedule that the Ministry of Economy uses against real estate brokers and other DNFBPs. Article 3 empowers the Ministry of Economy to impose the administrative penalties in Article 14 of the previous federal decree-law (now Article 17 of Federal Decree-Law 10 of 2025), the fines in the attached schedule, or both. The schedule includes fines of AED 50,000 to AED 200,000 for CDD failures, AED 100,000 to AED 500,000 for enhanced due diligence failures and AED 50,000 to AED 1,000,000 for failure to act on National Risk Assessment findings, which are the bands real estate brokers see most often.

6. Cabinet Decision No. (109) of 2023 On Regulating the Beneficial Owner Procedures

Cabinet Decision 109 of 2023 governs the UBO regime that real estate brokers rely on when verifying legal-person customers. Article 4 lists the basic data that every legal person must maintain on its beneficial owners, partners and nominee directors; Article 8 sets the duty to keep the UBO register up to date; Article 11 obliges the legal person to disclose UBO information to the registrar, and Article 11(8) fixes a five-year retention duty for UBO records after dissolution or liquidation. MoE Circular 05/2022 requires real estate brokers to collect the UBO register for every legal-person buyer or seller, in addition to the trade licence, articles of association and Emirates ID or passport of each UBO and shareholder.

7. Cabinet Resolution No. (132) of 2023 Concerning the Administrative Penalties against Violators of the Provisions of the Cabinet Resolution No. (109) of 2023 Concerning the Regulation of Beneficial Owner Procedures

Cabinet Resolution 132 of 2023 sets out the specific administrative fines applied to legal persons and their representatives who fail to maintain, update or disclose UBO data under Cabinet Decision 109 of 2023. Real estate brokers do not themselves impose these fines, but they must recognise them when a legal-person customer declines to provide UBO data. A refusal by a counterparty to provide UBO information is itself a CDD red flag and a basis for declining to conclude the transaction.

Want your real estate team trained on AML/CFT compliance obligations?

AML UAE provides practical AML/CFT training tailored to real estate brokerages, helping teams stay informed, inspection-ready, and aligned with the federal law, executive regulation, MoE circular and EOCN guidelines.

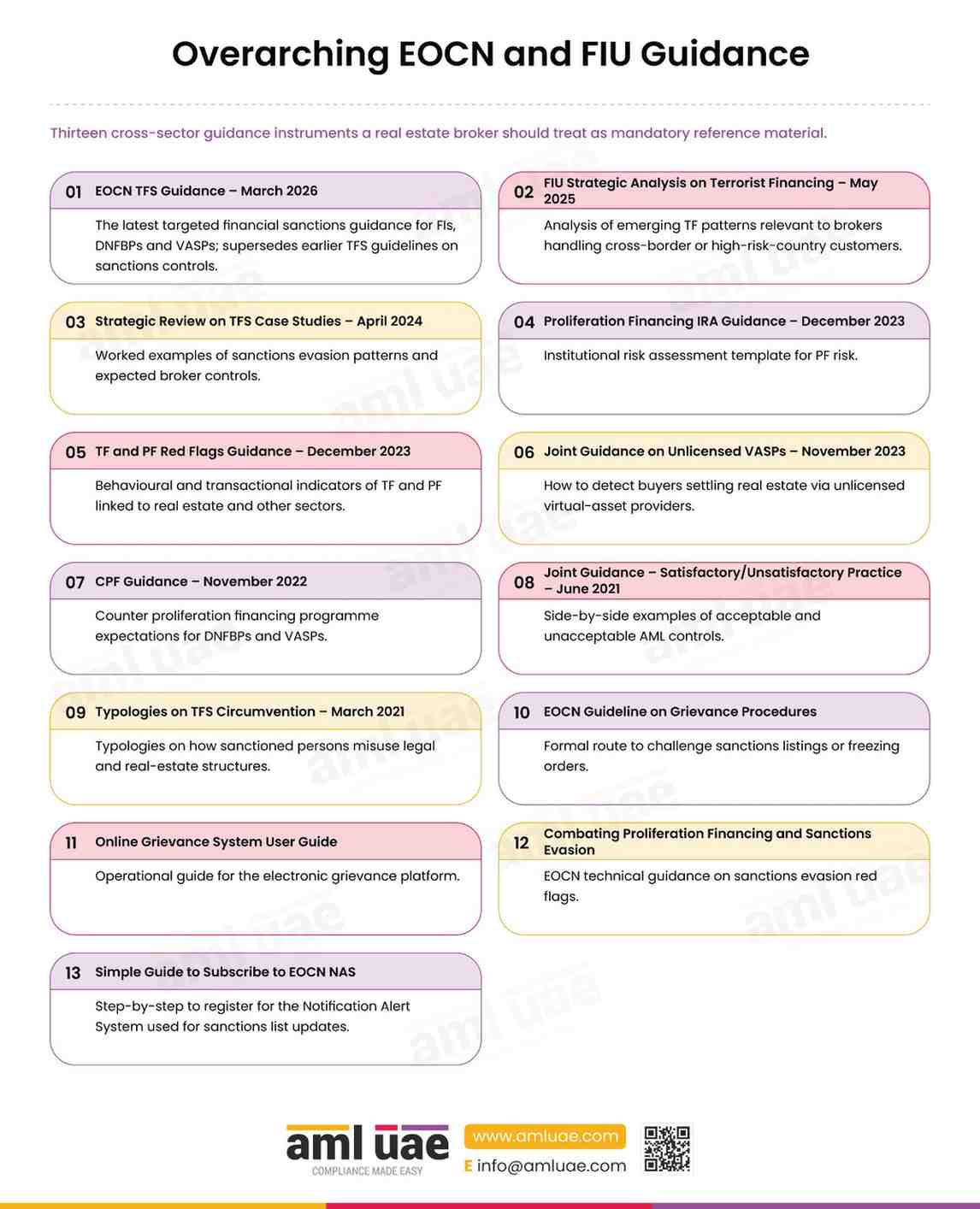

Overarching AML Guidance Applicable to Real Estate Agents and Brokers

The EOCN and the UAE Financial Intelligence Unit publish cross-sector guidance and strategic reports that apply to every DNFBP, including real estate brokers. Together they set expectations on targeted financial sanctions, proliferation financing, terrorism-finance red flags and the use of the Automatic Reporting System and grievance channels.

Thirteen cross-sector guidance instruments a real estate broker should treat as mandatory reference material.

1. EOCN TFS Guidance – March 2026

The latest targeted financial sanctions guidance for FIs, DNFBPs and VASPs; supersedes earlier TFS guidelines on sanctions controls.

2. FIU Strategic Analysis on Terrorist Financing – May 2025

Analysis of emerging TF patterns relevant to brokers handling cross-border or high-risk-country customers

3. Strategic Review on TFS Case Studies – April 2024

Worked examples of sanctions evasion patterns and expected broker controls.

4. Proliferation Financing IRA Guidance – December 2023

Institutional risk assessment template for PF risk.

5. TF and PF Red Flags Guidance – December 2023

Behavioural and transactional indicators of TF and PF linked to real estate and other sectors.

6. Joint Guidance on Unlicensed VASPs – November 2023

How to detect buyers settling real estate via unlicensed virtual-asset providers.

7. CPF Guidance – November 2022

Counter proliferation financing programme expectations for DNFBPs and VASPs.

8. Joint Guidance – Satisfactory/Unsatisfactory Practice – June 2021

Side-by-side examples of acceptable and unacceptable AML controls.

9. Typologies on TFS Circumvention – March 2021

Typologies on how sanctioned persons misuse legal and real-estate structures.

10. EOCN Guideline on Grievance Procedures

Formal route to challenge sanctions listings or freezing orders.

11. Online Grievance System User Guide

Operational guide for the electronic grievance platform.

12. Combating Proliferation Financing and Sanctions Evasion

EOCN technical guidance on sanctions evasion red flags.

13. Simple Guide to Subscribe to EOCN NAS

Step-by-step to register for the Notification Alert System used for sanctions list updates.

1. Guidance on Targeted Financial Sanctions for Financial Institutions, Designated Non-Financial Business and Professions (DNFBPs) and Virtual Asset Service Providers (VASPs) issued by the Executive Office for Control and Non-Proliferation (EOCN) – March 2026

This is the most recent cross-sector TFS guideline from the EOCN. It consolidates screening, listing, delisting, reporting and record-keeping expectations for DNFBPs, including real estate brokers, against UN Security Council resolutions and the UAE Local Terrorism List. The guidance fixes expectations on the use of the Automatic Reporting System for Confirmed Name Match Reports and Partial Name Match Reports, and on the integration of NAS alerts into customer screening workflows.

2. FIU’s Strategic Analysis Report on Terrorist Financing – May 2025

The UAEFIU strategic report identifies TF typologies and emerging patterns seen across STR and SAR filings. For real estate brokers, it matters because freehold purchases by or on behalf of designated persons, or using funds routed through high-risk jurisdictions, are persistent patterns the FIU expects brokers to detect and report via goAML.

3. Strategic Review on Targeted Financial Sanctions Case Studies – April 2024

This review from the EOCN collates anonymised case studies on TFS compliance failures and successes in the UAE. Real estate brokers use the case studies to benchmark their own sanctions screening thresholds, their handling of false-positive alerts and their internal escalation procedures.

4. Proliferation Finance Institutional Risk Assessment Guidance for FIs, DNFBPs, and VASPs – December 2023

This EOCN document provides a template for the PF institutional risk assessment that every DNFBP, including real estate brokers, must produce and keep current. The template covers threat, vulnerability and control assessments, and is the document that the Ministry of Economy expects to see during an on-site inspection of any brokerage.

5. Terrorist and Proliferation Financing Red Flags Guidance – December 2023

This red-flag compendium lists customer, transactional and geographic indicators of TF and PF risk relevant to DNFBPs. Several red flags apply directly to real estate transactions, including payments from or to high-risk jurisdictions, structuring cash deposits and use of complex legal persons with no apparent commercial purpose.

6. Joint Guidance on Combating the Use of Unlicensed Virtual Asset Providers in the UAE – November 2023

Issued jointly by the UAEFIU, SCA, EOCN and other authorities, this guidance explains how unlicensed VASPs are used to move illicit funds into and out of the UAE, and how DNFBPs should detect the pattern. It is highly relevant to real estate brokers because virtual-asset settlements or conversions on freehold transactions trigger REAR filing under MoE Circular 05/2022.

7. Guidance on Counter Proliferation Financing for FIs, DNFBPs, and VASPs – November 2022

This older but still binding CPF guideline sets the minimum controls that a real estate brokerage must apply to proliferation financing risk. It has been supplemented by the 2023 PF institutional risk assessment guidance, but has not been repealed; brokers read both together.

8. Joint Guidance – Satisfactory/Unsatisfactory Practice – June 2021

This cross-supervisor joint guidance shows how the UAE regulators score AML control effectiveness. Several examples cover real estate transactions, especially around beneficial ownership, source of funds and suspicious transaction reporting. It is a useful calibration benchmark when a broker is writing its AML policies.

9. Typologies on the circumvention of Targeted Sanctions against Terrorism and the Proliferation of Weapons of Mass Destruction – March 2021

Typologies published by the EOCN that show how sanctioned persons attempt to use legal persons, family members and intermediaries to move funds or acquire assets, including real estate. Real estate brokers use the typologies to design screening rules and to train front-office staff.

10. EOCN Guideline on Grievance Procedures

The grievance procedure lets a listed person or their representative challenge the listing or a resulting freeze action. Real estate brokers keep a copy of the guidelines to answer customer queries where a freeze on a pending property purchase has been applied.

11. Online Grievance System User Guide

The EOCN publishes an electronic portal for submitting grievances against listings and freezing actions. The user guide is a practical reference for compliance officers needing to navigate the portal on behalf of a customer or counterparty.

12. Combating Proliferation Financing and Sanctions Evasion

This EOCN policy document sets out typologies and controls specifically aimed at proliferation financing and sanctions evasion. Real estate brokers use it to supplement the PF institutional risk assessment with scenario-based control testing, especially around corporate buyers linked to high-risk jurisdictions.

13. Simple Guide to Subscribe to the EOCN Notification Alert System (NAS)

The NAS is the free, opt-in subscription service that delivers every update to the UAE Local Terrorism List and the UNSC Consolidated List directly to subscribed compliance officers. The EOCN expects every DNFBP, including real estate brokers, to subscribe to the relevant compliance officer to NAS.

Need help operationalising EOCN and FIU guidance?

AML UAE maps every EOCN and FIU publication to the controls a real estate brokerage actually has to run, from NAS subscription to PF institutional risk assessment to CNMR filing. .

NRA, SRA, and Other Important Guidelines Applicable to Real Estate Agents and Brokers

The national risk assessment tells real estate brokers how the State itself rates ML and TF risk in the sector. The 2024 exercise is the most recent authoritative assessment and is the reference document that Ministry of Economy supervisors benchmark against.

UAE ML/TF National Risk Assessment – 2024

The 2024 National Risk Assessment classifies mainland real estate brokers and agents as high residual ML risk. The assessment highlights cash-intensive transactions, luxury freehold properties, foreign investment and the use of legal persons to hold residential property as the dominant risk drivers. It records that approximately 96 per cent of the circa 16,000 DNFBP firms fall under Ministry of Economy supervision and that 99.8 per cent of real estate agents sit in the mainland and commercial free zones. Brokers must map their own business-wide risk assessment to the 2024 NRA findings; Ministry of Economy Circular 4 of 2025 explicitly requires DNFBPs to integrate the NRA conclusions into their risk management.

DNFBP Sector-Specific Guidance Applicable to Real Estate Agents and Brokers

Ministry of Economy circulars and DNFBP-wide guidance apply to every regulated real estate broker. They translate the federal decree-law and executive regulations into operational expectations, and are the documents that Ministry of Economy supervisors quote during inspections.

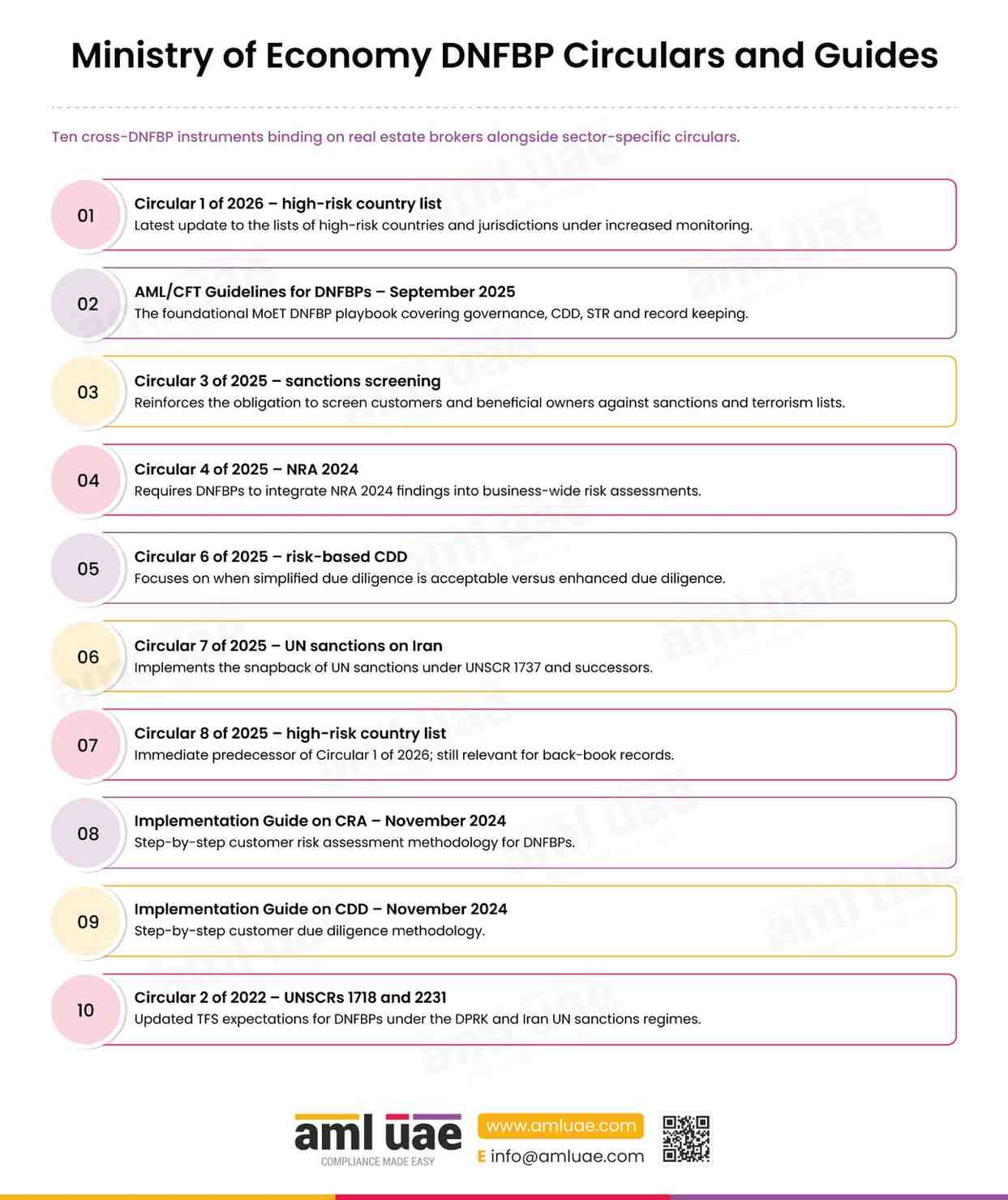

Ministry of Economy DNFBP circulars and guides

Ten cross-DNFBP instruments binding on real estate brokers alongside sector-specific circulars.

1. Circular 1 of 2026 – high-risk country list

Latest update to the lists of high-risk countries and jurisdictions under increased monitoring.

2. AML/CFT Guidelines for DNFBPs – September 2025

The foundational MoET DNFBP playbook covering governance, CDD, STR and record keeping.

3. Circular 3 of 2025 - sanctions screening

Reinforces the obligation to screen customers and beneficial owners against sanctions and terrorism lists.

4. Circular 4 of 2025 – NRA 2024

Requires DNFBPs to integrate NRA 2024 findings into business-wide risk assessments.

5. Circular 6 of 2025 – risk-based CDD

Focuses on when simplified due diligence is acceptable versus enhanced due diligence.

6. Circular 7 of 2025 – UN sanctions on Iran

Implements the snapback of UN sanctions under UNSCR 1737 and successors.

7. Circular 8 of 2025 – high-risk country list

Immediate predecessor of Circular 1 of 2026; still relevant for back-book records.

8. Implementation Guide on CRA – November 2024

Step-by-step customer risk assessment methodology for DNFBPs.

9. Implementation Guide on CDD – November 2024

Step-by-step customer due diligence methodology.

10. Circular 2 of 2022 – UNSCRs 1718 and 2231

Updated TFS expectations for DNFBPs under the DPRK and Iran UN sanctions regimes.

1. Circular No. (1) of 2026 on Updating the Lists of High-Risk Countries, Countries Subject to Increased Monitoring, and Related Measures

Circular 1 of 2026 updates the Ministry of Economy list of high-risk countries and countries subject to increased monitoring, in line with the most recent FATF plenary outcomes. Real estate brokers integrate the list into screening and customer risk assessment, apply enhanced due diligence to customers connected to high-risk jurisdictions, and consider filing a High Risk Country Report or High Risk Country Activity Report on goAML where a transaction has a material link to such a country.

2. AML/CFT Guidelines for Designated Non-Financial Businesses and Professions – September 2025

These are the revised Ministry of Economy guidelines for DNFBPs, signed by the Director of the AML Department in September 2025. The guidelines cover governance, compliance officer duties, business-wide risk assessment, customer risk assessment, CDD and enhanced due diligence, STR and SAR filing, record keeping, and staff training. They explicitly identify real estate agents and brokers as a core DNFBP category and are the single most-cited supervisory document in Ministry of Economy inspections.

3. Circular No. (3) of 2025 emphasizes the importance of screening sanctions and terrorist lists

Circular 3 of 2025 reinforces the screening obligation. It requires every DNFBP, including real estate brokers, to screen customers, beneficial owners and relevant counterparties against the UN, UAE Local Terrorism List and Ministry of Economy notifications at onboarding, at every transaction and whenever the lists are updated. The circular ties the obligation to the Automatic Reporting System for CNMR and PNMR filing.

4. Circular No. (4) of 2025 on Understanding the Importance of the UAE 2024 National Risk Assessment

Circular 4 of 2025 instructs DNFBPs to read the 2024 NRA and to integrate its findings into their business-wide risk assessments, customer risk methodology, staff training and internal policies. For real estate brokers, the integration turns the NRA’s high-risk rating on mainland real estate into a concrete risk factor that must be reflected in each customer’s risk score.

5. Circular No. (6) of 2025 on Emphasizing the Implementation of Risk-Based Customer Due Diligence Measures (with a Focus on Simplified Due Diligence)

Circular 6 of 2025 explains the scope and limits of simplified due diligence and reinforces the primacy of the risk-based approach. For real estate brokers, the circular is material because simplified due diligence is almost never appropriate on freehold purchase or sale transactions above AED 55,000 in cash or settled in virtual assets; those transactions trigger full CDD and REAR obligations.

6. Circular No. (7) of 2025 Regarding the Reimposition of United Nations Sanctions Related to Iran Pursuant to United Nations Security Council Resolution No. 1737 (2006) and Subsequent Resolutions

Circular 7 of 2025 implements the reimposed UN sanctions on Iran. It extends the sanctions perimeter and lists the categories of Iranian persons and entities now subject to asset freezing. Real estate brokers update customer screening and beneficial-owner checks in light of this instrument, particularly when a transaction has any Iran nexus.

7. Circular No. (8) of 2025 on Updating the Lists of High-Risk Countries, Countries Subject to Increased Monitoring, and Related Measures

Circular 8 of 2025 is the immediate predecessor of Circular 1 of 2026. It is no longer the operative list but remains part of a broker’s audit trail for customer risk decisions taken during its period of application.

8. Implementation Guide For DNFBPs on Customer Risk Assessment (CRA) – November 2024

The Implementation Guide on CRA sets out the Ministry of Economy’s recommended methodology for scoring customer ML/TF/PF risk. It gives real estate brokers a concrete template that combines customer, geographic, product and delivery-channel factors, and it specifies the frequency of rescoring. Real estate-specific factors such as freehold versus leasehold, cash versus financed and residential versus commercial properties map cleanly into the CRA template.

9. Implementation Guide For DNFBPs on Customer Due Diligence (CDD) – November 2024

The CDD Implementation Guide describes how to conduct identification, verification, beneficial-ownership investigation, source-of-funds review and ongoing monitoring. The guide sets expectations on acceptable identity documents, verification sources and enhanced measures for PEPs and high-risk countries. Real estate brokers use it alongside MoET Circular 05/2022 and the Supplemental Guidance for the Real Estate Sector to build a sector-specific CDD workflow.

10. Circular No. (2) of 2022 regarding Implementation of Targeted Financial Sanctions (TFS) on UNSCRs 1718 (2006) and 2231 (2015)

Circular 2 of 2022 consolidates earlier TFS obligations on the DPRK (UNSCR 1718) and Iran (UNSCR 2231) programmes. It remains in force as a binding instruction to real estate brokers alongside Circular 7 of 2025 and the EOCN guidance. A broker facing a match on either programme must freeze the assets, submit a CNMR through the Automatic Reporting System and notify the EOCN without delay.

Run a quick maturity check on your AML programme

AML UAE offers a one-day diagnostic that maps a brokerage’s current AML controls against every Ministry of Economy circular and EOCN guideline, producing a prioritised remediation plan.

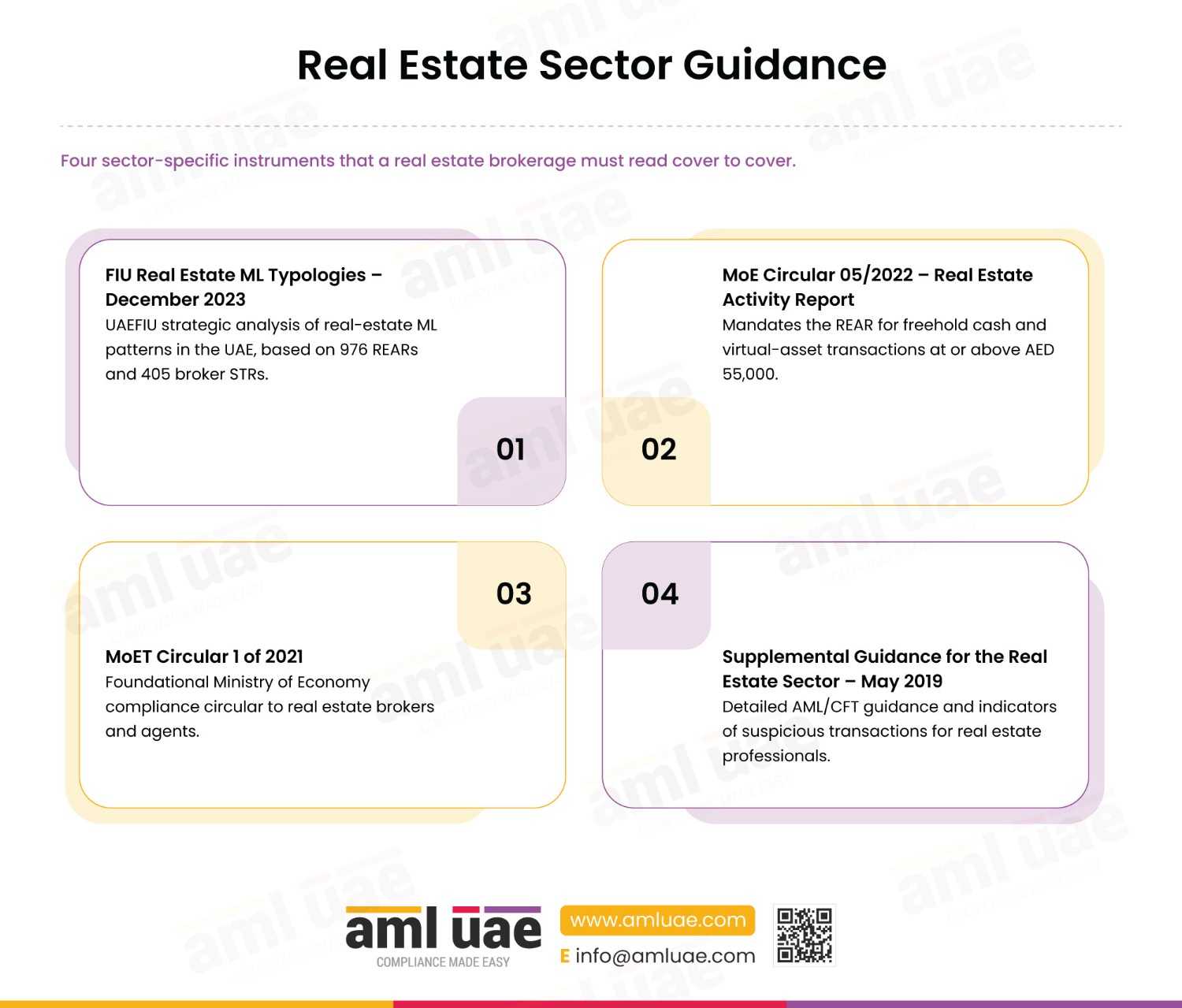

Sector-Specific Guidelines Applicable to Real Estate Agents and Brokers

Four real-estate-specific documents set the sector detail that a broker must master alongside the cross-DNFBP framework. They fix the Real Estate Activity Report trigger points, the typologies the UAEFIU expects brokers to detect, and the baseline compliance programme for the sector.

1. FIU Real Estate ML Typologies – December 2023

UAEFIU strategic analysis of real-estate ML patterns in the UAE, based on 976 REARs and 405 broker STRs.

2. MoE Circular 05/2022 – Real Estate Activity Report

Mandates the REAR for freehold cash and virtual-asset transactions at or above AED 55,000.

3. MoET Circular 1 of 2021

Foundational Ministry of Economy compliance circular to real estate brokers and agents.

4. Supplemental Guidance for the Real Estate Sector – May 2019

Detailed AML/CFT guidance and indicators of suspicious transactions for real estate professionals.

1. FIU’s Strategic Analysis Report on Real Estate Money Laundering Typologies and Patterns – December 2023

The UAEFIU strategic analysis examines 976 Real Estate Activity Reports, 405 suspicious reports from real estate agents and brokers and 612 suspicious reports from other reporting entities between 1 July 2020 and 30 June 2023. The report identifies six dominant typologies for the UAE real estate sector: use of third parties and family members, abuse of legal-person structures and corporate accounts, involvement of DNFBPs and brokers’ own bank accounts, claimed rental income, use of home finance and early settlement and manipulation of the property price. The report also covers unlicensed real estate crowdfunding, hawala and VASP-related patterns. Real estate brokers should map each typology to at least one red flag inside their transaction monitoring rule set. See the full report on the UAEFIU website.

2. Ministry of Economy Circular No. (05/2022) On Real Estate Activity Report

MoE Circular 05/2022, dated 24 June 2022 and effective from 1 July 2022, is the single most operationally important document for real estate brokers. It requires every licensed real estate broker or agent in the UAE to submit a Real Estate Activity Report (REAR) through goAML whenever a freehold purchase or sale transaction involves (a) a single or linked physical cash transaction equal to or exceeding AED 55,000, (b) payment in virtual assets for a portion or the whole of the property value, or (c) funds converted from a virtual asset to cash for a portion or the whole of the property value. The circular mandates the collection of Emirates ID or passport, receipts, contracts and the Purchase and Sale Agreement; for legal-person counterparties, it additionally requires the trade licence, articles of association, UBO register and Emirates ID or passport of every UBO and shareholder. Records must be kept for at least five years. A REAR does not replace STR, SAR, CNMR, PNMR, HRC or HRCA obligations.

3. MoET Circular No. (1) of 2021

MoET Circular 1 of 2021, dated 4 February 2021, is the foundational Ministry of Economy circular to real estate brokers, DPMS, auditors and corporate service providers. It sets the baseline compliance programme: appoint a compliance officer under Article 21 of Cabinet Decision 10 of 2019 (now Article 21 of Cabinet Resolution 134 of 2025), perform customer due diligence, report suspicious transactions via goAML, comply with targeted financial sanctions, and keep records for five years. The circular remains valid because it was issued under the predecessor executive regulation and has not been specifically repealed; it should be read together with the September 2025 DNFBP Guidelines and MoE Circular 05/2022.

4. Supplemental Guidance for the Real Estate Sector – May 2019

The Supplemental Guidance is the detailed sector companion to the DNFBP Guidelines. Section 11.3 covers real estate specifically: scope of DNFBP obligations, sector-specific risk factors, enhanced CDD expectations, ongoing monitoring and an extensive catalogue of typologies and indicators of suspicious transactions. The indicators cover concealment of beneficial ownership, concealment of the illicit source of funds, realisation of value or utility for the perpetrators, and the means of payment. Brokers use the guidance to calibrate their red-flag library and to train transaction-facing staff.

Conclusion: practical AML obligations, REAR, red flags and penalties

This section consolidates the operational duties, the REAR mechanics, the typology-driven red flags and the penalty exposure that a licensed real estate broker must manage in practice.

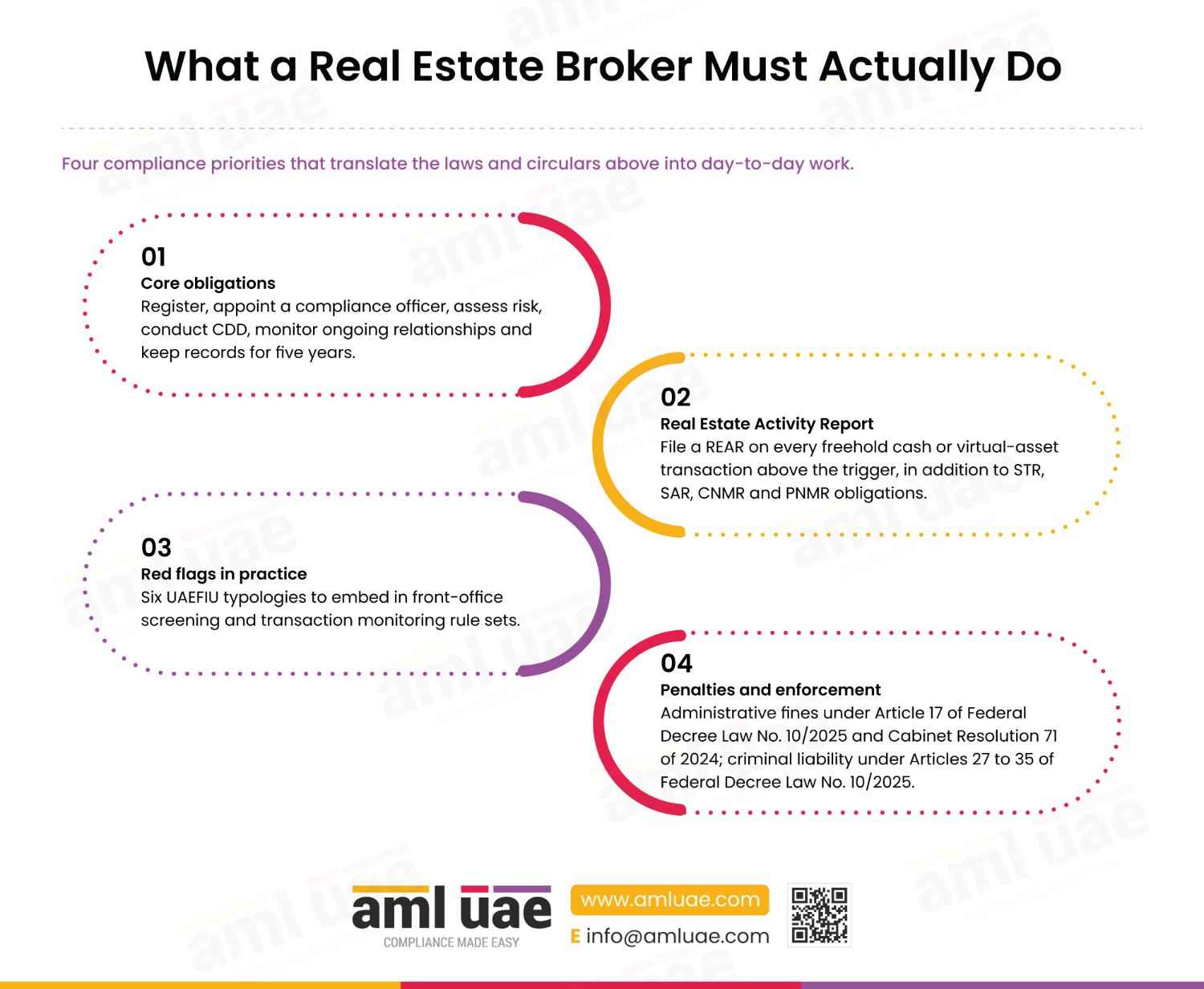

What a real estate broker must actually do

Four compliance priorities that translate the laws and circulars above into day-to-day work.

1. Core obligations

Register, appoint a compliance officer, assess risk, conduct CDD, monitor ongoing relationships and keep records for five years.

2. Real Estate Activity Report

File a REAR on every freehold cash or virtual-asset transaction above the trigger, in addition to STR, SAR, CNMR and PNMR obligations.

3. Red flags in practice

Six UAEFIU typologies to embed in front-office screening and transaction monitoring rule sets.

4. Penalties and enforcement

Administrative fines under Article 17 of Federal Decree Law No. 10/2025 and Cabinet Resolution 71 of 2024; criminal liability under Articles 27 to 35 of Federal Decree Law No. 10/2025.

Core obligations for real estate brokers

- Every licensed real estate broker or agent who concludes a purchase or sale for a customer must:

- Register on goAML and on the EOCN Automatic Reporting System;

- Appoint a compliance officer under Article 21 of Cabinet Resolution 134 of 2025;

- Produce and maintain a business-wide risk assessment integrating the 2024 National Risk Assessment findings;

- Develop AML policies and procedures

- Conduct risk-based customer due diligence under Articles 5 to 9 of Cabinet Resolution 134 of 2025;

- Identify and verify the beneficial owner under Article 10 of Cabinet Resolution 134 of 2025 and Cabinet Decision 109 of 2023;

- Apply enhanced due diligence to politically exposed persons under Article 16 of Cabinet Resolution 134 of 2025 and to high-risk-country customers and complex legal-person structures;

- Screen against UN, UAE Local Terrorism List and Ministry of Economy notifications;

- File STRs, SARs, CNMRs, PNMRs, HRC, and HRCA reports via goAML without tipping-off; and

- Keep all records for at least five years under Article 19(1)(f) of Federal Decree-Law 10 of 2025 and Article 25 of Cabinet Resolution 134 of 2025.

Real Estate Activity Report (REAR) mechanics

MoE Circular 05/2022 mandates a REAR whenever a freehold purchase or sale involves AED 55,000 or more in physical cash (single or linked), or any virtual-asset settlement or cash converted from a virtual asset. The report is submitted on goAML and sits on top of the STR, SAR, CNMR, PNMR, HRC and HRCA regimes; it does not replace them. For a legal person, the broker collects, in addition to the buyer’s or seller’s Emirates ID or passport and the Purchase and Sale Agreement, the trade licence, articles of association, UBO register and identity documents of each UBO and shareholder. Records are kept for at least five years. A broker that fails to submit the REAR, or submits it late or with incomplete data, exposes itself to administrative fines under Cabinet Resolution 71 of 2024 and, where the underlying transaction is linked to an offence, to criminal liability under Federal Decree-Law 10 of 2025.

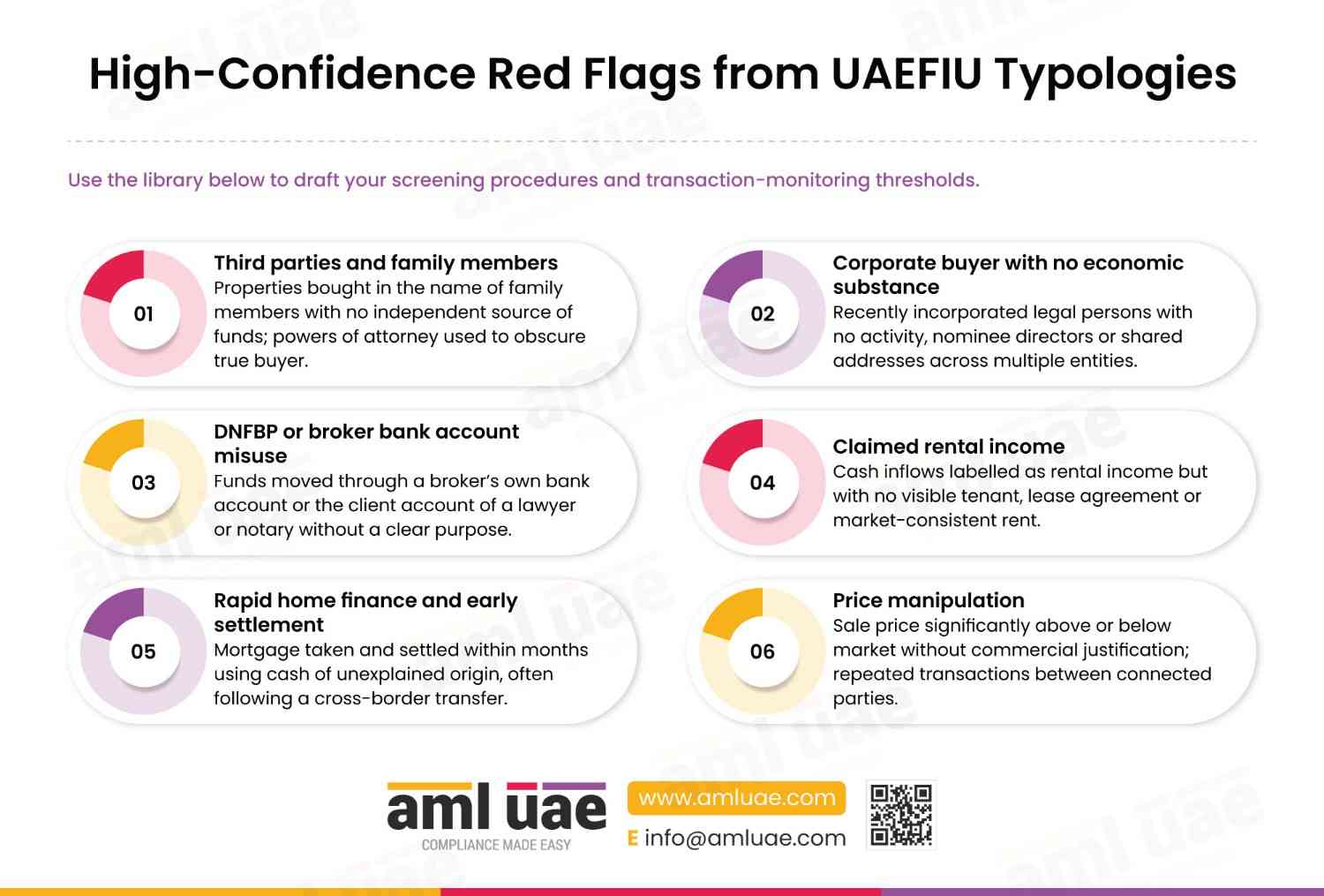

Typology-driven red flags

The UAEFIU 2023 strategic analysis, the 2019 Supplemental Guidance, and the 2023 TF and PF Red Flags Guidance together give real estate brokers a consolidated red-flag library. Six high-confidence red flags stand out:

High-confidence red flags from UAEFIU typologies

Use the library below to draft your screening procedures and transaction-monitoring thresholds.

1. Third parties and family members

Properties bought in the name of family members with no independent source of funds; powers of attorney used to obscure true buyer.

2. Corporate buyer with no economic substance

Recently incorporated legal persons with no activity, nominee directors or shared addresses across multiple entities.

3. DNFBP or broker bank account misuse

Funds moved through a broker’s own bank account or the client account of a lawyer or notary without a clear purpose

4. Claimed rental income

Cash inflows labelled as rental income but with no visible tenant, lease agreement or market-consistent rent.

5. Rapid home finance and early settlement

Mortgage taken and settled within months using cash of unexplained origin, often following a cross-border transfer.

6. Price manipulation

Sale price significantly above or below market without commercial justification; repeated transactions between connected parties

The Supplemental Guidance adds detailed indicators across customer, transaction and means-of-payment dimensions. Among the most common for UAE brokers are: customer reluctance to explain the source of funds, use of legal persons registered in high-risk jurisdictions, use of bearer instruments or cashier’s cheques that conceal the payer, structuring cash deposits to stay under reporting thresholds, and last-minute changes to buyer identity or contract price. Every red flag should trigger enhanced due diligence, a senior-management review and, where suspicion crystallises, a suspicious-transaction report through goAML.

Penalties for non-compliance

Non-compliance exposes a brokerage to three layers of liability.

1. Administrative action:

- Under Article 17 of Federal Decree-Law 10 of 2025, the Ministry of Economy can issue warnings, impose fines from AED 10,000 to AED 5,000,000 per violation, ban violators, suspend managers, restrict or cancel the trade licence and close the premises.

- The unified schedule in Cabinet Resolution 71 of 2024 fixes specific ranges, including AED 100,000 to AED 200,000 for failing to set an AML policy approved by top management, AED 50,000 to AED 500,000 for failing to assess and document crime risks, AED 100,000 to AED 500,000 for failing to apply enhanced due diligence to high-risk customers and AED 50,000 to AED 200,000 for failing to complete CDD before establishing a business relationship. The Ministry may double fines for repeat violations within twelve months.

2. Criminal Liability:

- Criminal liability under Federal Decree-Law 10 of 2025: Article 27 provides that a legal person whose representatives, directors or agents commit an ML, TF or PF offence on its behalf is punished by a fine of AED 5,000,000 to AED 100,000,000, or an amount equal to the value of the criminal property, whichever is greater, and the Court may order dissolution and closure of premises.

- Article 28 imposes imprisonment and a fine of AED 100,000 to AED 1,000,000 for deliberate or grossly negligent failure to report suspicious transactions under Article 18; Article 29 imposes imprisonment and a fine from AED 50,000 for tipping-off and for failing to comply with freezing orders; Article 32 imposes AED 200,000 to AED 10,000,000 for engaging in DNFBP activity without the necessary registration; Article 33 imposes a fine from AED 20,000 for violating EOCN targeted financial sanctions instructions; Article 35 imposes a fine from AED 20,000 for providing false beneficial-owner information. An attempt is punished on the same footing as the completed offence (Article 26(5)).

3. Reputational and licensing consequences:

- The Ministry of Economy publishes enforcement outcomes, the EOCN publishes freezing actions, and supervisors in the ADGM and DIFC cooperate with the Ministry of Economy and UAEFIU on cross-jurisdiction matters.

Build a real estate AML programme that stands up to Ministry of Economy inspection

AML UAE designs, documents and implements end-to-end AML programmes for real estate brokers across the UAE, including goAML registration, REAR workflow automation, NAS and ARS integration, and inspection readiness.

FAQs: AML regulations for real estate agents in UAE

Are real estate brokers and agents subject to AML rules in the UAE?

Yes. Every licensed real estate broker or agent that concludes a purchase or sale of real estate for a customer is a Designated Non-Financial Business and Profession (DNFBP) under Article 3(2) of Cabinet Resolution 134 of 2025, and is subject to the full AML/CFT/PF obligations in Federal Decree-Law 10 of 2025, the Ministry of Economy circulars and the EOCN and FIU guidance. The Ministry of Economy supervises mainland and commercial-free-zone brokerages; ADGM and DIFC brokerages follow their own regimes.

What is the real estate activity report in the UAE?

The Real Estate Activity Report (REAR) is a transaction-level filing on the goAML platform required by MoE Circular 05/2022 since 1 July 2022. Brokers file a REAR on every freehold purchase or sale transaction involving AED 55,000 or more in physical cash (single or linked), or any settlement in virtual assets, or any cash funded by conversion from a virtual asset. A REAR is filed in addition to any STR, SAR, CNMR, PNMR, HRC or HRCA obligations, and records are kept for at least five years.

What AML checks should a real estate broker perform?

At minimum: identify and verify the customer under Article 9 and the beneficial owner under Article 10 of Cabinet Resolution 134 of 2025; screen every party against UN sanctions, the UAE Local Terrorism List and MoE notifications; understand the source of funds and source of wealth for high-value or cash-intensive transactions; apply enhanced due diligence to politically exposed persons under Article 16 and customers linked to high-risk countries; conduct ongoing monitoring for the duration of the relationship; and report suspicions via goAML. The November 2024 Implementation Guides on CRA and CDD provide the detailed methodology.

What are the main money laundering red flags in real estate?

The UAEFIU 2023 strategic analysis identifies six dominant typologies: use of third parties and family members, abuse of legal-person structures and corporate accounts, misuse of DNFBPs and brokers’ bank accounts, claimed rental income with no substance, home finance followed by rapid early settlement and manipulation of the property price. The 2019 Supplemental Guidance lists detailed indicators across the customer, the transaction and the means of payment. Any combination of these factors requires enhanced due diligence and, if suspicion remains, an STR via goAML.

Do real estate businesses in ADGM and DIFC follow different AML rules?

Yes. Real estate activity inside the ADGM is supervised by the ADGM Registration Authority and follows the ADGM AML rulebook. Real estate activity inside the DIFC is supervised by the Dubai Financial Services Authority and follows the DFSA AML rulebook. Both regimes align with Federal Decree-Law 10 of 2025 at the principles level, but the specific rules, thresholds, reporting channels, and penalty schedules are different. Brokers operating across the mainland and a financial free zone must comply with both regimes in parallel.

Found this helpful?

If this guide clarified AML regulations for real estate agents in UAE for your brokerage, a short Google review helps the next compliance officer find it.

Share via :

About the Author

Pathik Shah

FCA, CAMS, CISA, CS, DISA (ICAI), FAFP (ICAI)

Pathik is an ACAMS-certified AML consultant specialising in governance, risk, and compliance for regulated entities in the UAE. He brings over 28 years of experience, with 1,000+ hours of AML training and 200+ advisory engagements across DNFBPs, VASPs, and FIs. He supports businesses in aligning with AML/CFT requirements from the CBUAE, DFSA, MoET, MoJ, VARA, CMA, FSRA, and FATF. Known for translating complex regulations into audit-ready procedures, Pathik enables operational clarity and compliance readiness.

Reach Out to Pathik