Offshore Transfers

Last Updated: 05/18/2026

Protect your business with reliable and effective AML strategies with AML UAE.

Offshore Transfers: At a Glance

- Moving funds through offshore accounts in secrecy jurisdictions is among the most effective tools criminals use to layer illicit proceeds and obscure their origin.

- Compliance teams that miss these transfer patterns expose their institution to regulatory sanction and criminal liability.

- Enhanced due diligence, transaction monitoring, and country risk assessment are the three non-negotiable controls.

What are Offshore Transfers?

The term “offshore transfers” describes the movement of funds from accounts or entities domiciled in one jurisdiction to accounts or entities held in a foreign jurisdiction, specifically to exploit the regulatory, disclosure, or oversight disparities between those jurisdictions. In the context of anti-money laundering, offshore transfers become a typology when the choice of destination is motivated by banking secrecy, limited beneficial ownership transparency, or a weaker supervisory framework rather than by any legitimate commercial or operational purpose.

The Financial Action Task Force (FATF) identifies cross-border wire transfers routed through multiple jurisdictions to obscure the origin of funds as a core layering mechanism. The UAE’s own 2024 National Risk Assessment identifies fund movement through UAE-based financial institutions as a high-risk typology, particularly when involving offshore or secrecy-friendly jurisdictions as transit or destination points.

Regulatory Framework Related to Offshore Transfers

Federal Decree Law No. (10) of 2025 on Anti-Money Laundering, Combating the Financing of Terrorism, and Proliferation Financing (FDL 10/2025) is the UAE’s primary AML/CFT/CPF statute. Article 19 requires all financial institutions and DNFBPs to identify, assess, and manage ML/TF risks; apply CDD; maintain records; and implement targeted financial sanctions forthwith. Article 2 criminalises money laundering, including concealing or disguising the illicit origin of funds through any financial transaction.

Cabinet Resolution No. (134) of 2025 (CR 134/2025) is the operative executive regulation implementing FDL 10/2025. Article 5 requires covered entities to conduct an enterprise-wide risk assessment applying a risk-based approach, including explicit assessment of geographic and jurisdictional risk.

Article 6 requires standard CDD, including identification and verification of the customer, beneficial owner, and purpose of the business relationship.

Article 16 requires enhanced due diligence (EDD) for high-risk customers, including those whose transaction profiles involve high-risk or offshore jurisdictions.

Articles 17 and 18 of CR 134/2025 require regulated entities to file a suspicious transaction report (STR) without delay via goAML to the UAEFIU when there is reasonable suspicion that a transaction involves money laundering or terrorism financing proceeds. The obligation arises from reasonable suspicion alone; certainty is not required.

Supervisory Authorities in UAE

The Central Bank of the UAE (CBUAE) supervises banks, exchange houses, and payment service providers. The Ministry of Economy and Tourism (MoET) and the Ministry of Justice (MoJ) supervise DNFBPs under their respective remits. The UAEFIU, established as an independent unit within the CBUAE under FDL 10/2025 Article 11, receives all STR filings through the goAML platform.

Reporting or Compliance Obligations and Channels of Offshore Transfers

Any regulated entity that identifies or suspects that a transfer has been structured to exploit offshore jurisdictions for money laundering purposes must file an STR without delay via the goAML platform. There is no minimum transaction value; reasonable suspicion is the sole trigger.

Under FDL 10/2025 Article 29, the entity must not tip off the customer that an STR has been filed.

CR 134/2025 Article 25 requires all transaction records and CDD documentation to be retained for a minimum of five years from the end of the business relationship or transaction date.

Recent Developments, Enforcement Actions, or Supervisory Priorities

The UAEFIU Strategic Analysis Report on TF Typologies and Facilitators (May 2025) identified high-risk jurisdiction routing and financial institution layering as active ML and TF methods observed in UAE-based data from January 2021 to December 2024. The NAMLCFTC Joint Guidance on Satisfactory and Unsatisfactory Practice (2021) identified deficient source of wealth identification and weak beneficial ownership understanding for corporate customers as the leading DNFBP weaknesses, both of which are directly implicated in offshore transfer schemes.

Geographies and Contexts of Concern

The UAE NRA 2024 rates fund movement through UAE financial institutions as a high-risk typology. The UAEFIU Strategic Analysis Report (May 2025) identified high-risk jurisdiction routing and financial institution layering as active ML and TF techniques observed in UAE-based data from 2021 to 2024.

Jurisdictions with banking secrecy legislation, FATF grey and black list designations, and known offshore financial centre activity with limited supervisory oversight all represent elevated geographic risk indicators for offshore transfers involving the UAE.

The UAE’s role as a correspondent banking hub for the MENA region amplifies its structural exposure to offshore transfer routing risks.

What Does Offshore Transfers Mean?

Think of it as sending cash through a maze of locked boxes, each placed in a different country. The criminal places money into the first box in Country A and passes the key to someone in Country B, who transfers it to a box in Country C, where no public registry records who opened it. By the time the funds reach their destination, the original owner is invisible. Each jurisdictional hop adds another locked door between the investigator and the beneficial owner.

Why Offshore Transfers Matter

Offshore transfers sit at the core of the layering stage of money laundering, the point at which detection is hardest and the paper trail is deliberately severed. Institutions that process wire transfers without calibrated country-risk controls do not merely face regulatory sanctions; they become unwitting enablers of criminal networks that use UAE correspondent relationships as transit points.

The administrative penalty regime under Cabinet Resolution No. (71) of 2024 imposes fines of up to AED 500,000 for failures in EDD and ongoing monitoring. Under UAE Federal Decree-Law No. 10 of 2025, Article 26 imposes fines of up to AED 5,000,000 on natural persons for money laundering offences, while Article 27 provides fines of up to AED 100,000,000 for legal persons. The supervisory priority placed on cross-border payment risk means institutions processing offshore transfers without documented risk assessments, calibrated monitoring, and EDD records face examination findings and potential enforcement action.

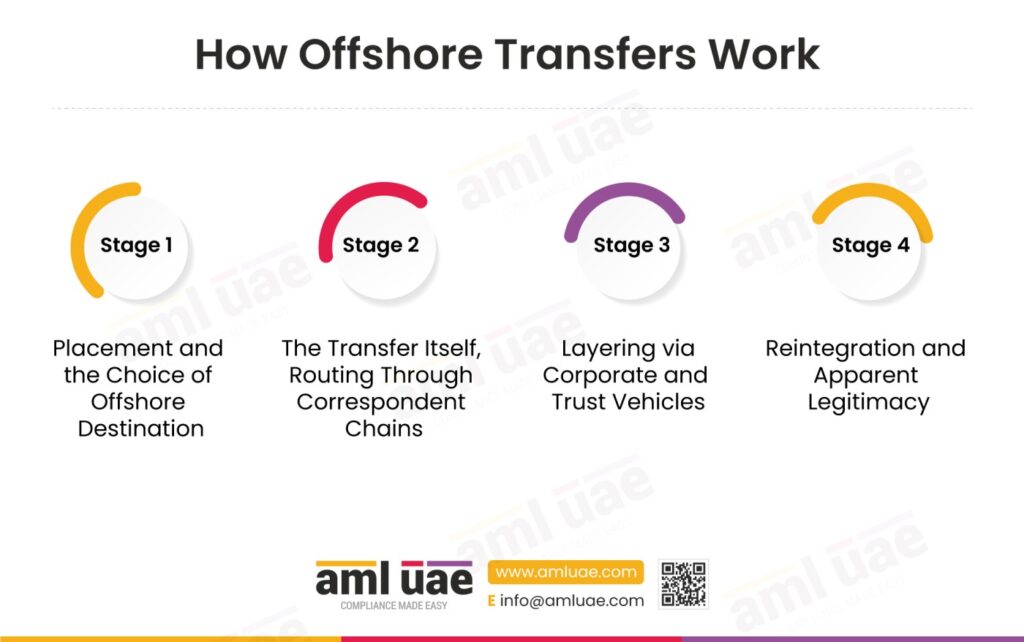

How Offshore Transfers Work

Cross-border fund transfers become a laundering mechanism through a structured sequence of decisions by the criminal actor. Each stage is designed to widen the gap between the funds’ origin and their apparent source, exploiting the procedural friction of international correspondent banking and the opacity of offshore corporate structures.

Stage One: Placement and the Choice of Offshore Destination

The criminal’s first decision concerns jurisdiction selection. Offshore financial institutions operating in jurisdictions with banking secrecy legislation, nominee director frameworks, or minimal beneficial ownership reporting requirements are preferred because they create structural barriers to information requests from regulators in the originating country.

Correspondent banks facilitate this by opening channels between onshore and offshore banking systems, without always conducting the same level of CDD on respondent institution customers.

Stage Two: The Transfer Itself, Routing Through Correspondent Chains

The actual transfer is typically routed through a chain of one to three correspondent banking relationships spanning different jurisdictions. Each link in the chain applies its own CDD standards, which vary widely across jurisdictions.

A transfer originating from a high-risk jurisdiction that passes through a mid-tier financial centre before arriving at a UAE institution may appear to originate from the mid-tier centre. Transfer routes involving multiple intermediary banks without a clear economic rationale represent a structural indicator of deliberate routing.

Stage Three: Layering via Corporate and Trust Vehicles

Corporate entities with no apparent operational activity receive and re-transmit offshore transfers. Nominees hold the shares or directorship of those entities, ensuring the beneficial owner’s name does not appear on any registry. Trust beneficial interests and bearer shares are similarly used.

Each transfer between these vehicles appears at the bank account level as a legitimate business-to-business payment, because the corporate wrapper provides a facially plausible explanation for the movement.

Stage Four: Reintegration and Apparent Legitimacy

The final stage sees the layered funds re-enter the legitimate economy, often as a “loan repayment,” “dividend,” or “consulting fee” flowing back from the offshore vehicle to the original beneficial owner or to a business they control. The transaction is documented as a commercial arrangement.

At this point, the funds carry the appearance of legitimacy derived from the offshore corporate structure, and the connection to the original predicate offence has been broken across multiple jurisdictions and corporate layers.

Real-World Examples of Offshore Transfers

The Correspondent Chain Scenario

A professional money laundering network operating across three jurisdictions uses a general trading company registered in a secrecy jurisdiction to receive wire transfers from multiple counterparties.

The trading company holds an account at a local offshore financial institution with limited AML controls, which is a respondent bank to a mid-tier financial centre bank, which holds a correspondent relationship with a domestic country institution.

When the funds arrive at the domestic country institution, the originator of record is the mid-tier bank, not the opaque trading company. The compliance officer reviewing the credit does not see the offshore entity; only the correspondent’s SWIFT message is visible.

The operational lesson is direct: correspondent banking relationships require ongoing due diligence on the respondent bank’s AML framework. A respondent institution’s limited compliance track record is itself a red flag, independent of any specific transaction.

The Nominee and Shell Structure Scenario

A nominee director nominally controls an offshore entity in a jurisdiction that does not publish beneficial ownership registers. The entity receives transfers described as “investment proceeds” and transmits those funds onward to a resident individual described as “loan repayment.”

The resident account holder’s transaction history shows only inward remittances and local expenditure.

The offshore entity appears in neither the customer’s declaration nor the account’s stated source of funds. The inconsistency between the stated business profile and the incoming transfer volumes represents the observable signal.

The Trust Vehicle Scenario

A trust administered by a TCSP in an offshore jurisdiction holds beneficial interests on behalf of an undisclosed ultimate beneficiary. Funds move between trust accounts in a cyclical pattern, returning to the same institutions under different transaction descriptions, before a large-value transfer is directed to a domestic financial institution for a property acquisition.

The compliance team identifies the beneficiary as the TCSP acting in its trustee capacity, but cannot identify the ultimate beneficial owner behind the trust structure. This is the point at which enhanced scrutiny is mandatory.

What Are the Red Flags That Identify Offshore Transfers?

| Category | Red Flag Observation |

| Customer | The customer’s declared business profile does not explain the volume or frequency of cross-border wire transfers initiated or received. |

| Customer | Corporate counterparties have no verifiable operational activity, commercial registry listing, or web presence beyond their jurisdiction of incorporation. |

| Customer | Nominees or trustees are named parties to transfers without a commercial rationale documented in the account file. |

| Customer | The customer is unable or unwilling to provide documentation explaining the purpose of recurring offshore transfers. |

| Transaction | Transfer amounts are markedly inconsistent with the account holder’s historic transaction patterns and cannot be explained by declared business activity. |

| Transaction | Multiple transfers are executed in close succession across different foreign jurisdictions with minimal intervals between movements. |

| Transaction | Cyclical flows of funds return to the same account across offshore jurisdictions, each leg carrying a different transaction reference or stated purpose. |

| Transaction | Transfer documentation is absent, incomplete, or internally inconsistent regarding stated purpose and beneficiary details. |

| Geographic | Funds are directed to or received from financial institutions in jurisdictions with banking secrecy legislation, limited AML supervisory frameworks, or FATF grey or black list designations. |

| Geographic | The destination jurisdiction is materially weaker in regulatory terms than the customer’s own jurisdiction of business or residence. |

| Geographic | Transfer routes pass through multiple intermediary banks without a commercial explanation for the indirect routing. |

| Channel | The correspondent or respondent institution processing the transfer has a documented history of limited AML controls or beneficial ownership transparency failures. |

| Channel | Transfers involve financial institutions subject to regulatory enforcement actions or peer institution derisking decisions. |

| Product | Transfers are linked to corporate entities holding bearer shares or trust beneficial interests, making BO verification structurally unavailable. |

| Product | Equity interests in legal entities are transferred simultaneously with cash movements without clear commercial purpose. |

Which AML Controls Counter Offshore Transfers?

| Control | What It Disrupts | Detect / Prevent / Deter | Specific Limitation |

| Country Risk Assessment | Routes through rated-high-risk jurisdictions | Detects | Does not prevent initiation; alerts are only as current as the risk matrix update cycle. |

| Enhanced Due Diligence (EDD) | Obscured BO structures and nominee arrangements | Detects | EDD quality depends on information provided; offshore structures can limit availability. |

| Transaction Monitoring | Patterns inconsistent with declared profiles, cyclical flows | Detects | Rules must be calibrated specifically for offshore transfer patterns. |

| Ongoing Due Diligence | Profile divergence over time as transfer volumes shift | Detects | Periodic review cycles may miss intra-period anomalies. |

| Third-Party Risk Management | Respondent bank CDD quality failures | Prevents | Depends on information made available by respondent institutions. |

| OSINT and External Verification | Nominee and offshore entity opacity | Detects | Jurisdictions without public BO registers limit available intelligence. |

| Service Restriction | Continued exposure to high-risk offshore routes | Deters | Ends the relationship but does not recover already-transferred funds; STR obligation must be completed first. |

How Do AI and RegTech Automate Detection of Offshore Transfers?

Transaction monitoring platforms calibrated for offshore transfer patterns apply rule-based alert logic to flag jurisdiction-specific routing risks. This includes country-of-origin and country-of-destination scoring using FATF grey and black list designations, correspondent banking network mapping, and amount-frequency deviation alerts benchmarked against historic customer baselines. When a transfer pattern produces multiple simultaneous rule hits, the combined score triggers an elevated-priority alert.

Graph analytics tools map the full network of accounts, correspondent relationships, and beneficial ownership connections across a transfer chain. When an offshore transfer passes through two or more intermediary institutions, network analytics can visualise the routing path and identify structural patterns invisible from individual transaction records: cyclical return flows, fan-out structures, and reappearing counterparty identifiers. Natural Language Processing (NLP) applied to payment messaging extracts inconsistencies in stated transaction purposes and beneficiary details, flagging messages for manual review without requiring an analyst to read every wire instruction.

Machine learning anomaly detection, trained on peer group patterns for the customer’s industry and business profile, identifies transfer amounts and frequencies falling outside the statistically expected range. These models are effective for detecting the gradual escalation of offshore transfer volumes across extended periods, a pattern characteristic of long-duration ML schemes in which the criminal deliberately keeps early transfers below alert thresholds before scaling.

What Data Should Compliance Teams Collect to Detect Offshore Transfers?

| Data Point | Source System | What It Reveals About Offshore Transfers |

| Beneficial ownership records | KYC platform | Identifies whether disclosed corporate structure matches the business purpose; reveals nominees and ownership layers. |

| Correspondent and cross-border transaction data | Core banking / payment platform | Maps the full routing path of offshore transfers, including intermediary institutions and jurisdictions. |

| Geographical and jurisdictional risk scores | Transaction monitoring / risk engine | Rates each jurisdiction in the transfer chain against AML framework standards and FATF designations. |

| Geographic transaction history | Core banking | Establishes the customer’s historic cross-border transfer pattern; reveals deviations in destination, frequency, and amount. |

| KYC and CDD records | KYC platform | Provides the declared business profile against which observed transfer patterns are assessed. |

| Transaction logs | Core banking / payment platform | Documents the sequence, timing, and value of each transfer leg; identifies close-succession patterns and cyclical flows. |

| Trust information and accounts | KYC platform / trust register | Identifies whether a trust vehicle is interposed and whether the beneficial owner behind the trust is verifiable. |

How Do Offshore Transfers Aggravate Customer Risk and Jurisdictional Risk?

Offshore transfers aggravate customer risk by structurally concealing the identity of the beneficial owner behind the transfer chain. When a nominee holds the account or a shell entity is interposed, the compliance officer’s visibility into who is ultimately sending or receiving funds is deliberately impaired.

Standard CDD procedures that rely on customer-provided documentation are insufficient because the nominee framework is specifically designed to pass those checks. This elevates the residual customer risk rating regardless of the declared purpose of the transfer.

Jurisdictional risk is aggravated because offshore transfers exploit differentials in regulatory quality between sending and receiving jurisdictions. When funds transit through a jurisdiction with banking secrecy legislation or limited AML supervisory capacity, the information available to subsequent institutions in the chain is truncated at source.

The UAE’s country risk assessment framework under CR 134/2025 Article 5 requires each institution to rate the jurisdictions it is exposed to; transfers from or to jurisdictions rated as high risk automatically elevate the transaction risk rating and trigger EDD obligations.

What Behavioural Patterns Signal Offshore Transfer Activity?

A compliance officer conducting a periodic file review would observe that the customer’s declared business activity does not generate the observed volume of cross-border wire transfers.

Transfers are directed to financial institutions in jurisdictions the customer has no stated business connection to, and transaction references are generic, repetitive, or inconsistent across a series of transfers sharing the same economic counterparty. Corporate entities named as counterparties cannot be verified through commercial registries or open-source searches.

A review of correspondent banking credits and debits would also reveal that inward transfers originate from institutions in multiple jurisdictions within a compressed time window, suggesting fund aggregation from dispersed sources prior to onward transmission. The transaction narrative may show amounts clustering near round-number thresholds or escalating progressively across successive review periods.

Sectors at Highest Exposure

| Sector | Risk Rating | Specific Reasoning |

| Banks and financial institutions | Critical | Direct processors of wire transfers; correspondent banking is the primary infrastructure through which offshore transfer routing occurs. |

| Correspondent banking intermediaries | Critical | Respondent bank CDD failures pass directly through the correspondent chain; payable-through account risks are structurally embedded. |

| Trust and Company Service Providers (TCSPs) | High | Administer the offshore trust structures and corporate vehicles that provide the ownership layer between beneficial owners and the transfer chain. |

| Offshore company incorporation services | High | Create the corporate shells and nominee arrangements that make beneficial ownership opaque to institutions processing the transfers. |

| Real estate (financed via offshore transfers) | High | Property acquisitions funded through offshore vehicle structures represent a documented reintegration mechanism. |

| Legal professionals (as settlement agents) | Moderate | Involvement in cross-border property or business acquisitions creates exposure to funds layered through offshore structures. |

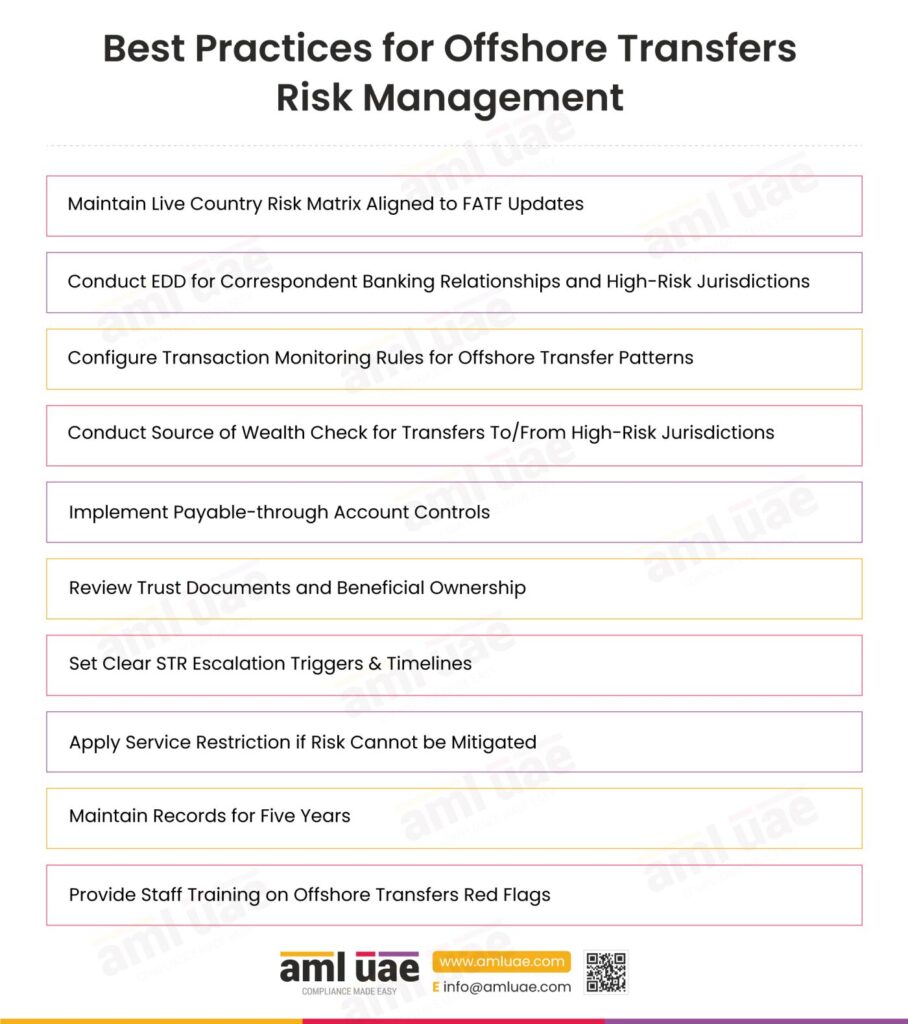

Best Practices for Offshore Transfers Risk Management

- Maintain a live country risk matrix calibrated to FATF designations and updated at every plenary cycle. Apply enhanced monitoring automatically to all transactions involving the grey list, the black list, or banking secrecy jurisdictions. The matrix must be reviewed within 30 days of a jurisdiction reclassification.

- Apply EDD to all correspondent banking relationships, not only to newly onboarded respondents. Review the AML framework and beneficial ownership transparency practices of all respondent institutions on an annual basis. Request correspondent bank due diligence questionnaires and document the outcome.

- Configure transaction monitoring rules specifically for offshore transfer patterns. Effective rules must include jurisdiction-pair scoring, amount deviation against customer-specific baselines, close-succession timing detection, and correspondent chain depth alerts. Review rule effectiveness quarterly using back-testing against known typologies.

- Conduct source of wealth (SoW) verification for all customers whose account patterns include offshore transfers to or from high-risk jurisdictions. SoW documentation must be verified independently. Where SoW cannot be corroborated, escalate to senior management approval before continuing the relationship.

- Implement payable-through account controls on all correspondent banking credits. For accounts that receive credits from respondent institutions on behalf of the respondent’s own customers, apply the same CDD standards to those underlying customers as would apply to direct customers.

- Review trust documentation and beneficial ownership declarations whenever an offshore transfer involves a trust vehicle. CR 134/2025 Article 10 requires identification and verification of the beneficial owner. When a trustee is the nominal account holder, identify the settlor, trustee, protector, beneficiaries, and any other person exercising control.

- Set clear escalation triggers and timelines for STR filing when offshore transfer patterns cannot be explained. FDL 10/2025 Article 18 requires reporting without delay. Document the decision timeline for every transaction reviewed and not reported.

- Apply service restriction decisively when EDD is inconclusive, and the risk cannot be adequately mitigated. The STR obligation must be completed before or simultaneously with the decision to restrict or exit.

- Ensure record retention covers the full offshore transfer chain documentation for a minimum of five years. CR 134/2025 Article 25 sets the retention minimum. This includes SWIFT message content, stated transfer purpose, correspondent bank details, beneficial ownership documentation, and all EDD actions taken.

- Train front-line and compliance staff on offshore transfer red flags as a distinct training module. The indicators specific to offshore transfers, including nominee involvement, secrecy jurisdiction destinations, correspondent chain opacity, and transfer pattern inconsistency, require specific training that generic AML awareness does not supply.

In my experience advising UAE institutions, the firms that stay ahead of offshore transfer risk are the ones that treat best practices as a live discipline, not a checklist. A risk-based EDD programme, a country-risk methodology refreshed against the latest FATF and CMA guidance, and front-line staff trained to spot a nominee structure before it clears, that combination is what separates a compliance function that detects from one that merely documents. Deploying these controls consistently, and revisiting them as typologies evolve, is how institutions counter the layering and concealment that offshore transfers are designed to achieve.

How Offshore Transfers and Offshore or Secrecy Exploitation Are Related

Offshore transfers are a specific sub-technique of the broader typology known as Offshore or Secrecy Exploitation. The parent technique describes the full range of methods through which criminals exploit jurisdictional opacity, banking secrecy, and weak regulatory frameworks to conceal the ownership and movement of funds.

Offshore transfers are the execution mechanism within that framework: the specific act of moving funds across jurisdictions to exploit those disparities.

The distinction matters for detection because the observable indicators of offshore transfers operate at the transaction and account level, whereas the indicators of Offshore or Secrecy Exploitation as a broader pattern span corporate structures, nominee arrangements, and multi-jurisdictional regulatory gaps.

A compliance officer who identifies an offshore transfer pattern has found one evidence strand. Understanding the parent technique equips them to recognise that the same customer may also exhibit structural indicators that belong to the same broader scheme.

What Financial Instruments Do Criminals Use in Offshore Transfer Schemes?

Bank accounts held at offshore financial institutions are the foundational instrument in offshore transfer schemes. The account’s jurisdiction of domicile determines the level of disclosure the institution owes to information requests from regulators in other countries.

Bearer shares are exploited when the criminal requires the ownership of the corporate entity receiving the offshore transfer to remain invisible, because bearer shares pass ownership through physical possession rather than a public registry entry.

Equity interests in legal entities are used to provide an apparent commercial rationale for offshore fund movements.

Trust beneficial interests provide a layer of structural opacity beyond the corporate layer. When a trust holds the ultimate economic interest in an offshore entity that initiates or receives transfers, the chain of ownership leads to the trust rather than to a named individual. Unless the trust deed is examined and the beneficial owner identified, the transfer appears to originate from a legitimate trust vehicle.

What Products and Services Do Criminals Abuse in Offshore Transfer Schemes?

Correspondent banking services are the infrastructure through which offshore transfers operate at scale. A correspondent relationship between a UAE bank and an offshore financial institution provides a channel for the offshore institution’s customers to transact in UAE dirhams or US dollars without holding an account directly with the UAE institution.

This infrastructure is commercially essential; it becomes a money laundering vulnerability when the respondent institution’s CDD standards are inadequate, and the correspondent does not apply payable-through account controls.

Cross-border payment services are abused when used to route transfers through jurisdictions selected for their regulatory opacity rather than commercial relevance.

Offshore banking services in jurisdictions with banking secrecy legislation are the direct enabler of the account layer in offshore transfer schemes.

Offshore company incorporation services create the corporate vehicles, including shell companies, nominee-held entities, and special purpose vehicles, that hold the offshore accounts through which transfers are made.

Trust and corporate services administered by TCSPs interpose a further layer between the beneficial owner and the offshore transfer chain. A TCSP acting as trustee holds the account or shares in the offshore entity, meaning that from the processing institution’s perspective, the customer is the TCSP rather than the ultimate economic owner. This is the primary opacity mechanism that renders standard CDD insufficient without specific trust documentation review.

How AML UAE Helps in Managing Offshore Transfers Risk

Addressing the compliance gaps due to offshore transfers risk requires technical capability to monitor cross-border transaction patterns, jurisdictional knowledge to distinguish commercially legitimate offshore activity from structurally suspicious routing, and documented procedures that will survive supervisory examination.

AML UAE provides regulated entities with the tools and advisory support to build and operationalise offshore transfer risk management frameworks that meet the requirements of FDL 10/2025 and CR 134/2025. This includes enterprise-wide risk assessment methodology that explicitly incorporates geographic and jurisdictional risk scoring, transaction monitoring calibration for offshore transfer typologies, and EDD procedures for correspondent banking relationships and TCSP-related accounts.

Firms that have received examination findings on cross-border payment risk can use AML UAE’s remediation support to rebuild their country risk assessment framework, recalibrate their monitoring rule sets, and establish the documentation standards that regulators expect. Training programmes designed specifically for offshore transfer red flags are available for compliance teams whose generic AML training does not address the jurisdictional and structural indicators that characterise this typology.

Closing Summary: Offshore Transfers

Offshore transfers occupy a central position in the money laundering lifecycle because they exploit the procedural gaps between jurisdictions that differ in regulatory quality, banking secrecy, and beneficial ownership transparency. They are difficult to detect at the individual transaction level precisely because each leg of the transfer chain is constructed to appear commercially legitimate.

The legal framework is unambiguous. FDL 10/2025 and CR 134/2025 impose specific obligations on CDD, EDD, STR filing, geographic risk assessment, and record retention, all of which are directly implicated when offshore transfers appear in an institution’s transaction profile. Non-compliance carries administrative penalties of up to AED 500,000 for EDD failures, and criminal penalties of up to AED 100,000,000 for legal persons convicted of facilitating money laundering.

The practical response is not to restrict cross-border payments indiscriminately but to build a risk management framework calibrated specifically to offshore transfer typologies: a live country risk matrix, transaction monitoring rules designed for layering patterns, payable-through account controls on correspondent relationships, and EDD procedures capable of reaching through nominee and trust layers to the beneficial owner. Institutions that build these capabilities will detect offshore transfer schemes earlier, document their decisions more effectively, and be better placed to defend their compliance programmes during supervisory examination.

Offshore transfers are often not a single suspicious transaction but a series of individually explicable payments that only reveal their laundering function when viewed as a network. The compliance team that sees one wire transfer to a secrecy jurisdiction may see nothing alarming. The compliance team that maps the full correspondent chain, the beneficial ownership structure at each node, and the pattern across twelve months will see a very different picture. Transaction monitoring without network analytics is a structural detection gap for this typology.

Frequently Asked Questions on Offshore Transfers

In the AML context, offshore transfers are wire transfers or fund movements directed to or received from accounts in foreign jurisdictions where the destination is selected for regulatory opacity, banking secrecy, or limited beneficial ownership disclosure rather than a genuine commercial purpose. They function as a layering mechanism by replacing origination information with jurisdictional opacity at each transfer leg.

No. Legitimate international business generates substantial volumes of cross-border payments, and the majority are commercially motivated. An offshore transfer becomes suspicious when the destination jurisdiction is selected for its secrecy or regulatory weakness, the beneficial ownership behind the transfer chain cannot be identified, the transfer pattern is inconsistent with the customer’s declared business, or the transaction documentation is absent or internally inconsistent.

FDL 10/2025 Article 19 requires all regulated entities to identify, assess, and manage ML/TF risks and apply CDD. CR 134/2025 Article 5 requires geographic risk assessment covering jurisdictional exposure from cross-border activity. CR 134/2025 Articles 17 and 18 require STR filing without delay when offshore transfers generate reasonable suspicion of money laundering or terrorism financing.

STRs must be filed with the UAEFIU through the goAML platform. There is no minimum transaction value; reasonable suspicion is the trigger. Under FDL 10/2025 Article 29, tipping off the customer that an STR has been filed is a criminal offence carrying imprisonment and a fine of at least AED 50,000.

Correspondent banking provides the interbank infrastructure through which offshore transfers are routed. A UAE institution that holds a correspondent relationship with an offshore financial institution may receive credits on behalf of that institution’s own customers, including customers whose identities are not known to the UAE institution. This payable-through account risk is one of the primary mechanisms through which offshore transfers enter UAE financial institutions without triggering the CDD that would otherwise apply.

CR 134/2025 Article 16 requires EDD for high-risk customers. A customer whose account includes offshore transfers to or from high-risk jurisdictions, whose beneficial ownership structure involves nominees or trusts, or whose transfer pattern is inconsistent with their declared business triggers EDD obligations. EDD must include an enhanced source of funds and source of wealth verification, senior management approval, and more frequent account reviews.

CR 134/2025 Article 25 requires all CDD records and transaction documentation to be retained for a minimum of five years from the end of the business relationship or transaction date. For offshore transfers, this includes the SWIFT message content, stated transfer purpose, correspondent bank details, beneficial ownership documentation, and all EDD and monitoring actions taken.

Yes. CR 134/2025 Article 14 permits regulated entities to exit a relationship where risk cannot be adequately managed through available controls. When ongoing offshore transfer activity cannot be explained, the source of funds cannot be verified, or beneficial ownership cannot be established after a reasonable EDD process, service restriction is a proportionate response. Any STR obligation must be completed before or simultaneously with the exit decision.

Country risk assessment assigns risk ratings to jurisdictions based on FATF designation, banking secrecy legislation, and AML supervisory quality. When a customer’s transfer pattern involves high-risk jurisdictions, the risk assessment framework triggers EDD obligations and enhanced monitoring. A live, regularly updated country risk matrix is the foundational control for offshore transfer risk calibration.

Under FDL 10/2025 Article 26, standard money laundering penalties for natural persons are one to ten years imprisonment and a fine of AED 100,000 to AED 5,000,000. Aggravated money laundering carries temporary imprisonment and a fine of AED 1,000,000 to AED 10,000,000. Legal persons face fines of AED 5,000,000 to AED 100,000,000. Administrative penalties under CR 71/2024 for EDD and monitoring failures reach AED 500,000 per violation.

Protect Your Institution from Offshore AML Threats

Learn the key indicators and enhanced due diligence practices needed to monitor cross-border transfers to high-risk jurisdictions.

Share via :

About the Author

Pathik Shah

FCA, CAMS, CISA, CS, DISA (ICAI), FAFP (ICAI)

Pathik is an ACAMS-certified AML consultant specialising in governance, risk, and compliance for regulated entities in the UAE. He brings over 28 years of experience, with 1,000+ hours of AML training and 200+ advisory engagements across DNFBPs, VASPs, and FIs. He supports businesses in aligning with AML/CFT requirements from the CBUAE, DFSA, MoET, MoJ, VARA, CMA, FSRA, and FATF. Known for translating complex regulations into audit-ready procedures, Pathik enables operational clarity and compliance readiness.

Reach Out to Pathik