International Real Estate

Last Updated: 06/24/2026

Protect your business with reliable and effective AML strategies with AML UAE.

Key Highlights: International Real Estate

Cross-border property acquisition is a significant money laundering risk because it combines high transaction values, long-term asset holding, offshore ownership structures and multi-jurisdictional opacity.

In the UAE, Federal Decree-Law No. (10) of 2025 and Cabinet Resolution No. (134) of 2025 impose AML/CFT obligations on UAE-regulated real estate brokers and agents when they conclude transactions or settlements on behalf of customers in relation to the purchase or sale of real estate. The supervisory authorities expect beneficial ownership identification through multi-jurisdictional corporate chains to the natural person.

Every compliance team processing a property transaction involving a foreign buyer, foreign property, offshore structure, or cross-border funding source should conduct a heightened risk assessment and apply enhanced due diligence where the customer, jurisdiction, structure, PEP exposure, source of funds, or transaction pattern warrants it.

What is International Real Estate?

Criminals can use international real estate for money laundering, which involves the cross-border acquisition, ownership, and disposal of property to integrate illicit proceeds across jurisdictions. The technique exploits the structural mismatch between AML/CFT supervision, which is national in scope, and property ownership, which is international in practice: for instance, a UAE-based illicit operator can purchase property in London, Dubai, Singapore, or Miami through a chain of offshore companies, and no single supervisory authority possesses a complete view of the transaction. Each jurisdiction sees only the portion within its own borders, with the corporate structure, the source of funds, and the beneficial owner remaining invisible unless multiple regulatory bodies cooperate and share intelligence.

Under Federal Decree-Law No. (10) of 2025 (FDL 10/2025) Article 1, money laundering extends to any act that conceals the illicit origin of proceeds, including the acquisition of property in any jurisdiction when funded by criminal proceeds with a UAE nexus.

Cabinet Resolution No. (134) of 2025 (CR 134/2025) Article 3(2) designates real estate brokers and agents as DNFBPs for all purchase and sale transactions on behalf of their customers.

The DNFBP designation is not framed around a monetary threshold for real estate brokerage activity. Where a UAE real estate broker or agent is involved in the purchase, sale, brokerage, conclusion, or settlement of a real estate transaction, its DNFBP obligations apply to that regulated activity.

Where a UAE bank or financial institution processes the payment, its AML/CFT obligations apply to the payment relationship, customer relationship, and transaction monitoring.

Regulatory Framework Related to International Real Estate

Federal Decree-Law No. (10) of 2025 (FDL 10/2025) is the primary AML/CFT statute. Article 1 defines money laundering as any act of concealment applied to funds derived from a predicate offence, regardless of the jurisdiction in which the property asset is located.

Article 18 requires all DNFBPs to file STRs without delay via goAML when suspicion arises, including when the suspicion derives from cross-border funding patterns, multi-jurisdictional corporate structures, or a beneficial owner residing in a high-risk jurisdiction.

Article 19 mandates CDD, prohibits anonymous accounts, and requires policies covering all customer types, including legal persons with international ownership structures.

Article 26 criminalises money laundering, with penalties of one to ten years’ imprisonment and fines of AED 100,000 to AED 5,000,000 for natural persons; under Article 27, a legal person whose representative, director, or agent commits money laundering in its name or on its account faces fines of AED 5,000,000 to AED 100,000,000.

Article 28 imposes imprisonment and fines of AED 100,000 to AED 1,000,000 for the deliberate or grossly negligent breach of the Article 18 suspicious transaction reporting obligation. CDD failures are addressed separately as administrative breaches under Cabinet Resolution No. (71) of 2024, and may carry wider criminal risk only where linked to laundering conduct.

Cabinet Resolution No. (134) of 2025 (CR 134/2025) provides the operative regulatory framework. Article 3(2) confirms the DNFBP designation for real estate brokers and agents. Article 5 requires an enterprise-wide risk assessment that must include cross-border transaction risks and jurisdictional exposure. Article 10 requires the identification of the beneficial owner of all legal-person customers meeting the 25% threshold. Article 16 requires EDD for all politically exposed persons and their associates, a critical provision given the prevalence of PEP involvement in high-value international property acquisitions. Article 25 requires retention of all CDD records and transaction documentation for a minimum of five years.

Cabinet Resolution No. (109) of 2023 (CR 109/2023) establishes the UAE corporate beneficial ownership register framework. Subject to the statutory exclusions under CR 109/2023, Articles 5, 6 and 8 require UAE-registered legal persons to determine and maintain a Real Beneficiary Register identifying every natural person holding or controlling 25% or more of the company: Article 5 sets the 25% ownership or control threshold, Article 6 requires reasonable measures to keep beneficial ownership information accurate and up to date, and Article 8 mandates the Real Beneficiary Register itself. For international real estate structures that use UAE-incorporated holding companies for foreign property assets, CR 109/2023 creates a domestic transparency obligation on the UAE-domiciled layer of the structure.

Cabinet Decision No. (74) of 2020 (CD 74/2020) governs targeted financial sanctions. Article 21(2) requires all real estate agents and financial institutions to screen all parties against the UAE Local Lists and UN Consolidated List, including foreign buyers and the beneficial owners of foreign corporate purchasers. Under Article 15, an international property transaction involving a sanctioned person or entity requires the funds to be frozen without delay and without prior notice to the listed person, with the match and the freezing action reported through the applicable UAE sanctions reporting mechanism and supervisory channel. For targeted financial sanctions, regulated entities should not limit their analysis to the ordinary 25% beneficial ownership threshold. They should consider whether a listed person or entity owns, controls, benefits from, or acts through any party to the transaction, directly or indirectly.

MoET Circular No. 5 of 2022 (MoET-Cir-5-2022) introduced the Real Estate Activity Report (REAR) filing requirement for specified freehold purchase and sale transactions. A REAR must be filed via goAML where a freehold real estate transaction is settled in physical cash at or above AED 55,000 (whether a single payment or aggregated payments), where the payment is made using a virtual asset, or where the funds are converted from a virtual asset. For international buyers funding UAE property purchases through accounts in multiple jurisdictions, the REAR obligation and source-of-funds verification are concurrent and independent requirements.

UAE Obligations at a Glance

| Obligation | What it requires | Legal basis |

| Risk assessment | Maintain an enterprise-wide risk assessment covering cross-border and jurisdictional exposure. | CR 134/2025 Art. 5 |

| Customer due diligence | Identify and verify the customer and, for legal persons, the beneficial owner at the 25% threshold. | CR 134/2025 Art. 10; FDL 10/2025 Art. 19 |

| Enhanced due diligence | Apply EDD to PEPs and higher-risk customers and countries, proportionate to the assessed risk. | CR 134/2025 Arts. 16, 23 |

| Sanctions screening | Screen all parties against the UN Consolidated and UAE Local Lists; freeze without delay on a match. | CD 74/2020 |

| Suspicious transaction reporting | File an STR via goAML without delay where suspicion arises. | FDL 10/2025 Art. 18 |

| Real estate transaction reporting | File a REAR via goAML for freehold cash transactions at or above AED 55,000 or virtual-asset funding. | MoET Circular No. 5 of 2022 |

| Record keeping | Retain CDD and transaction records for at least five years. | CR 134/2025 Art. 25 |

Primary Authority or Supervisory Body

The Ministry of Economy and Tourism (MoET) supervises real estate brokers and agents as DNFBPs and conducts risk-based inspections covering international transactions.

The Financial Intelligence Unit (FIU), operating within the CBUAE under FDL 10/2025 Article 11, receives all goAML reports, including those filed in connection with cross-border real estate transactions and shares financial intelligence with domestic law enforcement and, through Egmont Group membership, with foreign FIUs.

The CBUAE supervises banks and financial institutions that process cross-border property payments, correspondent banking flows, and international wire transfers connected to real estate acquisitions.

The UAE implements FATF standards through its national AML/CFT framework, its membership of MENAFATF, and its participation through the GCC, which is a full FATF member. The FATF’s 2022 Risk-Based Approach Guidance for the Real Estate Sector directly informs the supervisory priorities applied to international transactions in the UAE.

Reporting or Compliance Obligations and Channels of International Real Estate

Real estate agents and brokers handling cross-border transactions face a heightened CDD standard. Where the buyer is a foreign national, a non-resident, or a corporate entity with international ownership, the broker must identify the beneficial owner to the 25% threshold under CR 134/2025 Article 10, regardless of the purchasing entity’s jurisdiction of incorporation. This obligation is not discharged by accepting the first layer of corporate documentation; it requires penetrating the ownership chain through every intermediate entity, regardless of jurisdiction, to the ultimate natural person.

The STR obligation under FDL 10/2025 Article 18 applies without threshold to any suspicion arising from an international transaction, including suspicion arising from: the jurisdiction of origin of the purchase funds; the complexity of the ownership structure; the involvement of nominee directors or officers; the absence of a credible commercial rationale for the cross-border acquisition; or the customer’s reluctance to provide source of funds documentation that explains the cross-border movement of the acquisition funds.

The REAR obligation under MoET-Cir-5-2022 applies to qualifying cash or crypto transactions, regardless of the buyer’s nationality or residence. An international buyer who pays cash or crypto of at least AED 55,000 for a UAE freehold property triggers the REAR obligation independently of any STR filing.

Banks and financial institutions processing cross-border property payments are required to apply correspondent banking controls under CR 134/2025 for transactions routed through correspondent relationships and to apply transaction monitoring calibrated to cross-border real estate typologies.

Recent Developments, Enforcement Actions, or Supervisory Priorities

The UAE NRA 2024 identifies the real estate sector as vulnerable to money laundering, particularly due to its attractiveness to domestic and foreign investors and the cross-border nature of many transactions.

It notes that the primary ML methods include the use of unknown sources of funds, complex legal structures, and nominees and family members to obscure beneficial ownership, all of which are characteristic of international real estate ML.

FATF’s February 2024 Plenary highlighted the importance of effective beneficial ownership transparency and of identifying individuals who hide illicit funds through complex corporate structures and legal arrangements.

What does International Real Estate Mean?

Picture two countries, each with its own land registry and its own AML supervisor. A person in Country A has cash they cannot explain. They establish a company in Country B, which in turn establishes a company in Country C, which buys a flat in Country D. The flat is registered in the name of Country C’s company. Country D’s land registry shows a foreign company as the owner. Country D’s real estate agent processed the sale without identifying who controls Country C’s company. Country B and Country C do not share ownership information with Country D unless a formal request is made. The person in Country A is invisible in all four countries simultaneously. International real estate works because property is local, but ownership is global, and AML supervision has not fully closed that gap.

Why International Real Estate Matters

Cross-border property acquisition can provide a durable form of ML integration because it spreads the risk of compliance failure across multiple jurisdictions.

In the UAE context, the intersection of a high-volume international property market, a large non-resident investor population, active use of free zone companies with reduced public disclosure requirements, and significant cross-border fund flows creates an environment in which international real estate ML is both common and difficult to detect without specialist CDD capabilities.

The jurisdictional dimension compounds the compliance challenge for every institution in the transaction chain. A UAE real estate agent handling a purchase by an offshore holding company cannot rely on the CDD performed by the bank in the offshore jurisdiction, because a different regulatory framework defines that bank’s obligations.

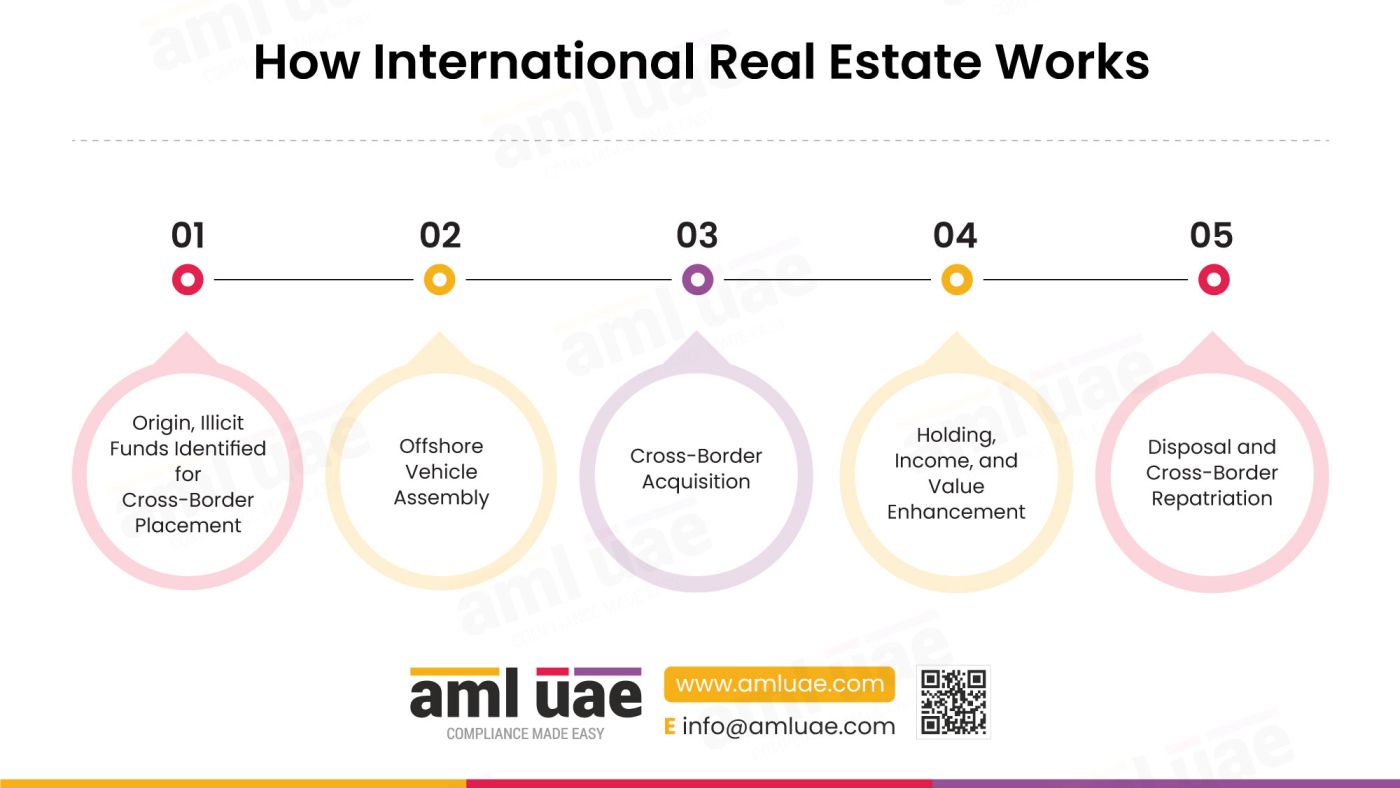

How International Real Estate Works

Stage One: Origin: Illicit Funds Identified for Cross-Border Placement

The scheme begins with illicit funds in a source jurisdiction, typically generated through corruption, fraud, drug trafficking, or tax evasion. The illicit operator identifies a target acquisition jurisdiction, selected for a combination of factors: high property values that absorb large sums without generating individual-transaction scrutiny; a real estate market open to foreign buyers; limited CDD requirements for international purchasers; limited information-sharing with the source jurisdiction; and a stable legal system that protects property rights and makes the asset difficult to seize once acquired. Dubai, London, Singapore, and Miami are among the most frequently cited destination markets in international property ML cases documented by FATF and Transparency International. For UAE-originating proceeds, the destination market selection often reflects personal or business connections in the target jurisdiction.

Stage Two: Offshore Vehicle Assembly

Before the acquisition, the illicit operator assembles the corporate structure through which the property will be purchased. A TCSP in a secrecy jurisdiction, such as the British Virgin Islands, the Cayman Islands, or the Seychelles, incorporates a holding company with nominee directors and, where available, bearer shares. The holding company may itself be owned by a second offshore entity, adding a second corporate layer. The UAE-based illicit operator’s connection to the offshore company is documented only in the TCSP’s internal files, which are not publicly accessible and may not be subject to international information-sharing requests from the destination jurisdiction’s supervisor. The TCSP that incorporates the structure and provides nominees does not apply adequate CDD on the ultimate beneficial owner, or accepts a corporate intermediary as the customer rather than the natural person behind it.

Stage Three: Cross-Border Acquisition

The offshore holding company instructs a bank or international payments provider to wire the acquisition funds to the destination jurisdiction. The funds pass through one or more correspondent banking relationships. At each correspondent node, the payment appears as a normal commercial wire transfer from a corporate entity; without direct enquiry into the sending company’s beneficial ownership, the correspondent bank sees a routine cross-border payment. The real estate agent in the destination jurisdiction processes the transaction with the offshore company as the purchaser. Source of funds documentation is not requested, or the offshore company’s bank statement is provided, showing the transfer, without any investigation of the origin of the funds in that account. The property is registered in the name of the offshore company.

Stage Four: Holding, Income, and Value Enhancement

Once the property is acquired, the holding period generates a stream of commercially explainable income. Rental income paid by tenants is credited to the offshore company’s account. The property appreciates over time. The offshore company may make additional improvements to the property funded by further illicit proceeds, record them as capital expenditure, and add them to the asset’s value. Throughout this stage, the property appears on the land registry as a legitimately acquired foreign investment. The illicit operator’s identity is separated from the asset by the corporate structure; the beneficial owner, if any, is visible on the company’s documents and is the nominee.

Stage Five: Disposal and Cross-Border Repatriation

The scheme concludes when the property is sold. The sale proceeds, representing the original illicit funds plus the holding period appreciation, are paid to the offshore company. The offshore company distributes the funds as a dividend, a shareholder loan repayment, or a management fee to another entity in the chain. By the time the funds reach the illicit operator’s personal account or are reinvested into a new asset, they have passed through a property transaction in a foreign jurisdiction, a corporate distribution, and at least two international wire transfers. The funds are indistinguishable from legitimate foreign investment returns. The integration is complete and durable.

Real-World Examples of International Real Estate

The Cross-Border PEP Portfolio

A senior government official in a high-risk jurisdiction accumulates proceeds of corruption over several years. Through a TCSP, the official establishes three offshore holding companies, each with a different nominee director, and two domestic corporate entities that hold minority interests in the offshore structures.

The offshore companies purchase high-value residential properties in multiple international property markets. Each property purchase is processed by a local real estate agent, who verifies the nominee director’s identity and does not trace ownership further. In one transaction, the reporting entity submits the required regulatory report for a high-value cash transaction but does not file a suspicious transaction report because the nominee director presents apparently legitimate corporate documentation.

Over five years, the three properties appreciate, generate rental income, and are refinanced against their increased value, producing additional proceeds that are returned to the offshore structure.

A competent authority eventually identifies the PEP connection through a cross-border intelligence-sharing request. Still, by then, two of the three properties have been sold, and the proceeds have been further layered.

The compliance failure was the failure to apply enhanced due diligence (EDD) measures despite the PEP-connected beneficial ownership of the purchasing structure, resulting in the concealment and integration of illicit proceeds through the real estate sector.

The Correspondent Banking Property Purchase

A financial institution receives a wire transfer instruction from a corporate account held at a foreign bank in a high-risk jurisdiction. The remitting entity is described as a property investment company, and the funds are intended for the purchase of real estate.

The receiving institution processes the wire through its correspondent banking relationship without triggering enhanced scrutiny because the transaction value is within the normal range for that relationship with the remitting bank. The funds are deposited into a real estate agent’s client account.

The agent verifies the purchasing entity’s corporate registration but does not identify the beneficial owner beyond the first layer. No source-of-funds inquiry is conducted because the agent treats the correspondent bank wire as a proxy for source-of-funds verification. The property is purchased and registered.

The purchasing entity is subsequently identified in a foreign law enforcement request as a front company involved in serious predicate offences. The receiving bank’s transaction monitoring failed to flag the combination of a high-risk-jurisdiction origin, a single large payment, and a real estate destination, indicating insufficient CDD.

The Multi-Jurisdictional Property Flip

An illicit operator uses a network of ten shelf companies incorporated across three jurisdictions, connected through nominee shareholding relationships, to execute a series of property transactions across two countries over three years.

Company A, incorporated in jurisdiction 1, purchases a commercial property in jurisdiction 2 for USD 2.5 million below market value from a connected seller. Company B, incorporated in jurisdiction 3 and nominally owned by Company A, sells the property to Company C six months later at market value, generating a paper profit of USD 2.5 million. Company C holds the property for 18 months, undertakes nominal renovations funded by additional illicit proceeds, and sells to an independent third-party buyer at a further premium.

The USD 5 million net gain across the series is distributed as management fees and shareholder dividends through the nominee structure. No single real estate agent or bank involved in any of the individual transactions has a view of the full series. Each institution processed one transaction with an offshore company whose beneficial ownership it did not penetrate.

The scheme is identified only when a cross-border tax investigation in jurisdiction 1 reconstructs the full transaction chain from land registry records in jurisdiction 2.

How Does International Real Estate Facilitate Money Laundering?

International real estate schemes serve the Integration tactic in the money laundering cycle, but their defining characteristic is their exploitation of jurisdictional fragmentation to neutralise national-level CDD. Unlike domestic real estate ML, which can, in principle, be detected by a single supervisory authority with access to all relevant transaction records, international real estate schemes distribute observable transactions across multiple regulatory perimeters.

The placement stage may occur in the source jurisdiction through an initial wire transfer or corporate distribution. The layering stage is completed through the multi-jurisdictional corporate structure that interposes offshore holding entities between the illicit operator and the property. Integration is achieved through the property asset, which appears on the land registry of the destination jurisdiction as a legitimate foreign investment.

The Jurisdictional Risk dimension makes international real estate uniquely durable as an integration vehicle. Once property has been acquired in a foreign jurisdiction through an offshore corporate chain, and the real estate agent’s CDD has been inadequate, the beneficial owner’s connection to the asset is legally obscured in a way that is very difficult to unwind without a coordinated multi-jurisdictional investigation. This durability is what distinguishes international real estate from financial product ML, where the instrument matures or closes, creating a retrospective audit opportunity that property held in a nominee company over decades does not provide.

How Do Criminals Exploit International Real Estate?

The illicit operator is the architect and ultimate beneficiary. This actor selects the destination jurisdiction based on its combination of a strong real estate market, limited CDD requirements for international purchasers, and a history of receptiveness to cross-border investment. The illicit operator directs the TCSP to establish the corporate structure, instructs the bank on the funding route, and selects the property through a real estate professional who may or may not be witting. In cases involving government officials, the illicit operator may have diplomatic connections in the destination jurisdiction that further reduce the scrutiny applied to them.

The nominee provides the identity layer that substitutes for the illicit operator across all documents. A nominee director of the offshore purchasing entity appears on the corporate records presented to the destination jurisdiction’s real estate agent and land registry. A nominee shareholder holds the equity in the offshore company, preventing any public disclosure of the beneficial owner. The nominee is typically a professional service provider in the TCSP’s network, whose identity is entirely legitimate but who has no genuine connection to the property or the funds.

The real estate professional in the destination jurisdiction is the primary gatekeeper. A real estate agent who processes the transaction without identifying the beneficial owner of the offshore purchasing entity, without requesting source-of-funds documentation, and without filing an STR when suspicion arises has enabled the integration.

The shell or front company is the acquisition vehicle and the legal registration holder. The offshore holding company’s name on the land register is the most visible indicator of international real estate ML, as it places the property’s registered title at the maximum distance from the beneficial owner. Front companies that maintain a nominal level of commercial activity, such as a website or a registered trade licence, provide a further layer of apparent legitimacy during basic verification by real estate agents.

TCSPs provide the infrastructure of the entire scheme. A TCSP that incorporates the offshore holding company, provides nominee directors and shareholders, administers the company’s accounts, and routes the acquisition funds without applying the required CDD on the ultimate beneficial owner is the enabling professional whose failure makes every other actor’s concealment possible. In jurisdictions with strong TCSP AML obligations, including the UAE under CR 134/2025, a TCSP that performs these functions without identifying the beneficial owner breaches its own DNFBP obligations.

What Are the Red Flags That Identify International Real Estate?

| Category | Redflags |

| Customer | A customer persistently delays or refuses to provide beneficial ownership documentation for offshore entities used to purchase foreign property, despite multiple requests and clear legal obligations to provide it. |

| Customer | The purchasing entity is an offshore company with no documented commercial activity other than property holding, incorporated in a jurisdiction with limited disclosure requirements, presenting a nominee director as its sole officer. |

| Customer | A foreign buyer’s declared income, profession, or business profile is materially inconsistent with the acquisition value of the property being purchased, without a credible source of funds explanation for the discrepancy. |

| Customer | Multiple foreign real estate holdings are formally registered under different shell companies but are administered by the same individual, the same TCSP, or the same professional address across jurisdictions. |

| Customer | Overlapping control persons, contact information, or corporate service providers appear across multiple offshore corporations collectively used in cross-border real estate acquisitions. |

| Transaction | Frequent property transactions completed within short timeframes show large valuation discrepancies between the acquisition price and independent market assessments, without a documented commercial or structural explanation. |

| Transaction | Large international wire transfers arrive from multiple offshore entities into an account used exclusively for purchasing foreign real estate, without a single identifiable beneficial owner who can be verified. |

| Transaction | A property acquisition in a high-value range is funded through a series of smaller transfers from multiple foreign jurisdictions, structured in amounts and timing that suggest deliberate fragmentation of a single larger sum. |

| Transaction | Property transactions involve simultaneous or closely sequenced purchases and disposals between connected offshore entities, at prices that generate a documented capital gain with no independent market justification. |

| Geographic | Frequent real estate acquisitions are concentrated in jurisdictions characterised by minimal disclosure requirements, limited information sharing with the UAE, or high scores on international corruption indices. |

| Geographic | The corporate ownership chain of the purchasing entity spans three or more jurisdictions, none of which is the jurisdiction of residence of any of the beneficial owners identified through CDD. |

| Geographic | Purchase funds originate from or route through jurisdictions on the FATF grey or black list, or through correspondent banking relationships with banks in those jurisdictions. |

| Product | Property transactions in high-value ranges exceed the customer’s stated income or business revenues without documented source of wealth that explains the accumulation of the acquisition sum. |

| Channel | The transaction is introduced by a third-party intermediary based in a different jurisdiction, who is unable to identify the ultimate principal behind the purchasing entity or provide documentation on the source of acquisition funds. |

| Channel | The buyer declines to use escrow services or structured settlement procedures that would require independent source of funds verification, requesting instead a direct transfer to the seller’s account. |

Which AML Controls Counter International Real Estate?

| Control | What It Disrupts | Detects / Prevents / Deters | Limitation |

| Country Risk Assessment | Identifies high-risk jurisdictions associated with cross-border property ML, enabling risk-proportionate CDD calibration | Prevents | Requires regular updating against FATF, EOCN, and bilateral risk ratings. A static country risk framework does not respond to jurisdictions that deteriorate or improve. |

| Customer Due Diligence (CDD) | Forces source of funds and beneficial ownership identification at the point of the transaction, regardless of the jurisdiction of the purchasing entity | Detects and prevents | Effective only when source of funds is actively pursued through the full corporate chain. Accepting first-layer corporate documents without penetrating to the natural person is the most common CDD failure in international real estate. |

| Enhanced Due Diligence (EDD) | Requires deeper source of wealth inquiry, Senior Management approval, and ongoing scrutiny for high-risk international customers including PEPs and entities in secrecy jurisdictions | Prevents | Depends on correct risk classification. A corporate purchaser with a BVI holding structure may indicate higher risk and should be assessed under the relevant country, ownership, and structure risk factors, with enhanced due diligence applied where the assessment warrants it. |

| OSINT and External Source Verification | Cross-references customer identity and declared background against adverse media, PEP lists, sanctions databases, and corporate intelligence across multiple jurisdictions | Detects | International adverse media and corporate intelligence varies significantly in quality and completeness by jurisdiction. OSINT is supplementary to, not a substitute for, formal CDD documentation. |

| Sanctions and Watchlist Screening | Screens all parties to the transaction, including foreign beneficial owners and offshore entities, against the UAE Local Lists and UN Consolidated List | Prevents | Must cover the beneficial owner, not only the presenting corporate entity. A sanctioned person holding a 25% interest through a nominee does not appear in a screening of the company name alone. |

| Service Restriction | Declines to process transactions where adequate beneficial ownership documentation cannot be obtained, preventing the integration from completing | Deters | Creates business relationship friction. Requires senior management commitment and a documented policy that supports declining high-risk transactions without adequate CDD. |

| Transaction Monitoring | Identifies anomalous cross-border payment patterns including rapid layering, multiple-jurisdiction fund sourcing, and structured transfers below reporting thresholds | Detects | Most effective for financial institutions. Real estate agents do not typically operate transaction monitoring systems. Calibration must include cross-border real estate typology rules. |

How Do AI and RegTech Automate Detection of International Real Estate?

Cross-border corporate ownership graph analytics are the primary technological application for international real estate ML detection. A compliance platform that integrates corporate registry data from multiple jurisdictions can automatically trace the ownership chain of an offshore purchasing entity through intermediate holding companies to the natural person, across dozens of jurisdictions and tens of thousands of corporate records. Graph analytics applied to this data can identify clusters of offshore entities sharing nominee directors, registered addresses, or corporate service providers, revealing coordinated multi-jurisdictional structures that appear unconnected when viewed individually.

Network analytics applied to correspondent banking payment flows can identify patterns characteristic of cross-border real estate ML, including aggregation of funds from multiple foreign accounts into a single acquisition account, rapid layering through multiple correspondent nodes, and routing through jurisdictions on FATF high-risk lists. Where the payment origination jurisdiction, the corporate registration jurisdiction, and the property destination jurisdiction are all different, and none coincides with the beneficial owner’s documented residence, the combination is a structural indicator that automated systems can flag without human intervention.

Machine learning models trained on confirmed international real estate ML cases, using features such as jurisdiction combinations, corporate structure depth, fund flow patterns, and property values relative to declared customer wealth, can assign transaction-level risk scores to incoming cross-border acquisitions. Models of this type can direct the highest-risk transactions to enhanced review queues, concentrating compliance resources on the transactions most statistically similar to confirmed ML cases.

International PEP database integration is particularly valuable for international real estate because PEP involvement is a significant risk factor in cross-border government-official property acquisitions. Automated PEP screening that extends to the beneficial owners of all offshore corporate purchasers and is continuously updated as PEP lists change, provides a second line of detection for the category of international real estate ML that standard CDD most commonly fails to identify.

What Data Should Compliance Teams Collect to Detect International Real Estate?

| Data Point | Source System | What It Reveals About International Real Estate |

| Full beneficial ownership chain across all jurisdictions to the natural person | Company and Beneficial Ownership Registries | Whether the cross-border corporate structure has been penetrated to the ultimate beneficial owner in every jurisdiction through which the chain passes |

| Correspondent and cross-border transaction records for acquisition funding | Correspondent and Cross-Border Transaction Data | Whether the funds used to acquire the property were aggregated from multiple foreign accounts, routed through high-risk jurisdictions, or structured to avoid individual-transaction scrutiny |

| Source of funds and source of wealth documentation | KYC and CDD Records | Whether the cross-border funds can be traced to a legitimate commercial activity consistent with the customer’s declared profile and financial standing |

| Property ownership and transaction history in destination jurisdictions | Real Estate and High-Value Asset Ownership Records | Whether the property has been subject to rapid resales among connected entities, or whether the acquisition price is inconsistent with independently verified market values |

| Corporate registry extracts and director/shareholder records from all jurisdictions in chain | Company and Beneficial Ownership Registries; Individual, Entity and Public Records Databases | Whether offshore entities in the ownership chain have nominee directors, no commercial activity, recent incorporation, or shared characteristics across multiple properties |

| Financial, business, and tax records for the declared beneficial owner | Financial, Business and Tax Records | Whether the beneficial owner’s declared financial profile supports the accumulation of the acquisition funds through legitimate commercial activity |

| Geographical and jurisdictional risk data for all countries in the transaction chain | Geographical and Jurisdictional Risk Data | Whether the jurisdictions involved in the corporate structure, the funding route, or the property location are associated with elevated ML risk per FATF, EOCN, or UAE country risk ratings |

| Trust information and accounts for trust-held property structures | Trust Information and Accounts | Whether property held through a trust structure has been subjected to the required identification of settlor, trustee, protector, beneficiary class, and controlling person. |

How Does International Real Estate Aggravate Jurisdictional Risk and Product Risk?

International real estate schemes elevate both Jurisdictional Risk and Product Risk to levels higher than any other real estate ML sub-typology, because the cross-border dimension compounds each risk independently, and their interaction creates a compounding effect.

Jurisdictional Risk is inherently maximised in international real estate ML because the scheme is specifically designed to exploit the gap between the jurisdictional scope of AML supervision and the geographic reach of property ownership.

An offshore corporate chain that spans three jurisdictions before arriving at a UAE property asset creates three separate layers of jurisdictional risk, each of which reduces the probability that the UAE supervisor can obtain the beneficial ownership information needed to assess the transaction.

Where one or more of the intermediate jurisdictions are secrecy jurisdictions with limited information-sharing obligations, or grey-listed jurisdictions with inadequate AML supervision, the risk compounds further.

The UAE’s CR 134/2025 Article 10 imposes the beneficial ownership tracing obligation on the UAE-licensed real estate agent.

This should be regardless of the jurisdictions through which the ownership chain passes, but the practical difficulty of executing that obligation across non-cooperative jurisdictions remains a significant residual risk.

Product Risk is elevated because international property transactions combine the high-value, long-duration characteristics of all real estate transactions with the additional opacity of cross-border funding and offshore ownership.

A single international property acquisition can absorb tens of millions of dirhams in a single transaction, produce a registered title that persists for decades, and generate rental income and capital appreciation that appear entirely legitimate to any subsequent reviewer who lacks access to the source-of-funds documentation.

The product’s durability means that a CDD failure at the point of the initial cross-border acquisition creates an AML exposure that remains embedded in the institution’s records indefinitely, compounded by each subsequent transaction the same customer completes.

What Cross-Border Patterns Signal International Real Estate to a Compliance Officer?

During CDD review or at the point of transaction processing, a compliance officer reviewing an international property transaction may encounter the following patterns that warrant escalation:

A foreign buyer presenting an offshore corporate entity as the purchaser, whose directors are professional nominees with no documented connection to the property sector or the acquisition rationale. An acquisition funded by a wire transfer from a jurisdiction on the FATF grey list, described in the payment instruction as an ‘investment transfer’ without supporting commercial documentation.

A series of transactions involving the same offshore company across multiple jurisdictions over a short period, each at prices that generate a documented capital gain without an independent market explanation.

A customer whose declared occupation is in a public sector role in a high-risk jurisdiction, purchasing property at a value materially inconsistent with that role’s remuneration.

A corporate ownership chain that cannot be penetrated beyond the second layer because the intermediate company is registered in a jurisdiction that does not respond to information requests.

Sectors at Highest Exposure

These ratings are AML UAE’s operational exposure assessment for compliance risk management. They are not official UAE sector risk ratings.

| Sector | Practical Exposure Rating | Reasoning |

| Real Estate Brokers and Agents | Critical | Process the property transaction in the destination jurisdiction. CDD obligations are not dependent on the AED 55,000 REAR threshold; they arise from the regulated activity and customer relationship. REAR and STR obligations are independent and concurrent. Most commonly identified for CDD failures in MoET enforcement actions. |

| Banks and Financial Institutions | Critical | Process all cross-border wire transfers used to fund international acquisitions. Are the primary checkpoint for correspondent banking flows and cross-border fund structuring. Must apply country risk assessment to all international transactions. |

| Trust and Company Service Providers (TCSPs) | High | Establish and maintain the offshore corporate structures used to hold international property. Carry DNFBP CDD obligations. Failure to identify the ultimate beneficial owner is the central enabler of international real estate ML. |

| Lawyers, Notaries, and Legal Professionals | High | Draft the corporate structures, trust arrangements, and property transfer documentation used in international acquisitions. Carry DNFBP obligations when carrying out specified activities under CR 134/2025. |

| Real Estate Investment Advisors | Moderate | Provide investment structuring advice to international buyers. May introduce offshore holding structures and cross-border financing arrangements that create the conditions for ML without being aware of the ultimate beneficial owner. |

Best Practices for International Real Estate Risk Management

- Penetrate the full ownership chain of every offshore purchasing entity to the natural person beneficial owner, regardless of how many jurisdictions the chain traverses. The obligation is not discharged by accepting first-layer corporate documentation; every intermediate entity in the ownership chain must be documented, and every layer must be traced to a natural person whose identity has been independently verified.

- Apply country risk assessment to all jurisdictions in the transaction chain, including the jurisdiction of incorporation of the purchasing entity, the jurisdiction of origin of the acquisition funds, and any intermediate jurisdictions through which the funds have passed. CR 134/2025 Article 5 requires an enterprise-wide risk assessment that explicitly addresses jurisdictional exposure. Transactions involving high-risk jurisdictions should trigger enhanced due diligence or a documented enhanced review, proportionate to the assessed risk.

- Require source of funds documentation that traces the acquisition funds from the beneficial owner’s confirmed income or business activity to the account from which they were transferred, not merely a bank statement showing the balance in the offshore company’s account at the time of transfer. The offshore company’s account may hold laundered funds transferred from multiple sources; the source-of-funds obligation requires tracing through the offshore account to the ultimate origin.

- Apply EDD to all customers identified as PEPs, PEP-connected, or resident in high-risk jurisdictions, regardless of the declared value of the acquisition. CR 134/2025 Article 16 requires EDD for PEPs and their associates.

- Conduct sanctions screening that covers the beneficial owner identified through the corporate chain, not only the presenting entity. Regulated entities should screen all parties against the UAE Local Lists and the UN Consolidated List. A sanctioned natural person who holds a 25% interest in an offshore purchasing entity through a nominee does not appear in a screening of the company name; only screening of the identified beneficial owner will reveal the sanctions connection.

- File STRs where cross-border transaction circumstances generate suspicion, independently of whether a REAR has been or will be filed. FDL 10/2025 Article 18 requires an STR on suspicion regardless of transaction value. A cross-border property transaction involving a grey-list jurisdiction of origin, an offshore purchasing entity, and a source-of-funds narrative that cannot be independently verified provides multiple concurrent grounds for suspicion requiring STR consideration.

- Apply Service Restriction where adequate beneficial ownership documentation cannot be obtained for an offshore purchasing entity. CR 134/2025 does not require a real estate agent to proceed with a transaction when CDD cannot be satisfactorily completed. Where the beneficial owner cannot be identified through reasonable CDD procedures, the obligation is to decline the transaction and, where suspicion has arisen, to file an STR via goAML.

- Maintain a documented record of all CDD steps taken in cross-border transactions, including the sources consulted, the documents obtained, the jurisdictions covered, and the rationale for any risk classification decisions. CR 134/2025 Article 25 requires retention of all CDD records for a minimum of five years. For international transactions, this record must include the full ownership chain documentation, the source of funds file, and any EDD materials, organised to allow complete reconstruction of the CDD process if required by MoET inspection.

- Establish a dedicated escalation pathway for transactions involving offshore purchasing entities in secrecy jurisdictions, correspondent banking fund flows, or beneficial owners with connections to high-risk jurisdictions. Routine CDD procedures calibrated to domestic transactions are not adequate for international structures. The escalation pathway should include notification to Senior Management for transactions exceeding a value threshold or for any transaction where the full ownership chain cannot be verified within a defined period.

- Train compliance staff on the specific cross-border indicators. Staff who can recognise the combination of an offshore purchaser, a grey-list funding jurisdiction, and a nominal source of funds narrative as a structural indicator for EDD, rather than as routine transaction characteristics, are substantially more effective than those applying generic AML training to cross-border transactions.

How International Real Estate and Real Estate-based Methods Are Related

International real estate is a specific sub-typology of real estate-based methods. Real estate-based methods are a broader category that covers all techniques by which illicit proceeds are integrated into property assets, including domestic acquisition, price manipulation, rental income abuse, and construction project schemes.

International real estate applies the same integration objective in the narrower operational context of a cross-border transaction, exploiting the jurisdictional gap between AML supervision and property ownership to reduce the probability that any single authority will detect the beneficial owner’s connection to the illicit funds.

The distinction is practically significant because international real estate introduces a specific set of compliance obligations, including country risk assessment, correspondent banking controls, and multi-jurisdictional beneficial ownership tracing, that do not apply to purely domestic real estate transactions.

A compliance programme calibrated to domestic real estate CDD will not detect the specific indicators that characterise cross-border property ML.

Related Terms

| Term | Connection |

| Real Estate-based Methods | Parent typology; international real estate applies the integration objective of real estate ML in the cross-border context, exploiting jurisdictional fragmentation as the primary concealment mechanism. |

| Asset Cloaking | The nominee and offshore corporate structures used to conceal beneficial ownership in international property transactions are the operational implementation of asset cloaking applied to cross-border real estate. |

| Shell Companies | Offshore shell companies are the primary acquisition vehicle in international real estate ML, providing legal title to the property without disclosing the beneficial owner in the destination jurisdiction. |

| Multi-Jurisdiction Corporate Structures | International real estate ML is built on multi-jurisdictional corporate chains; the sub-typology and the instrument are inseparable in practice. |

| Construction Project Schemes | A sibling sub-typology of real estate-based methods; construction project schemes exploit the cost structure of a development project, while international real estate exploits the jurisdictional gap in supervision of cross-border acquisition. |

| High-Cash Flow Real Estate | A sibling sub-typology of real estate-based methods; high-cash-flow real estate exploits rental income as the integration mechanism, while international real estate exploits the cross-border dimension of acquisition and ownership. |

| Bribery | PEP-connected property ML, where corruption proceeds are integrated through international real estate, is the most prevalent and most value-significant intersection between bribery and the international real estate typology. |

| Intermediary-Facilitated Transfers | Third-party intermediaries who introduce offshore buyers to real estate agents, or who route acquisition funds through correspondent accounts on behalf of the ultimate beneficial owner, are the channel facilitators in international real estate ML. |

Related Processes and Typologies

| Process or Typology | Connection |

| Source of Funds Verification | The CDD measure most commonly deficient in international real estate cases; tracing cross-border acquisition funds from the beneficial owner’s confirmed income through the offshore account to the acquisition payment is the specific investigative challenge. |

| Correspondent Banking Controls | The transaction monitoring and CDD framework applied to cross-border wire transfers; international real estate acquisition funds invariably pass through correspondent banking relationships that are the primary payment detection point. |

| Beneficial Ownership Tracing | The CDD process of penetrating multi-jurisdictional corporate structures to the natural person; the central challenge in international real estate ML and the most frequently failed control. |

| International Information Exchange | The legal frameworks through which UAE supervisory authorities and law enforcement can obtain beneficial ownership information from foreign jurisdictions; a critical but frequently slow tool for international real estate investigations. |

What Financial Instruments Do Criminals Use in International Real Estate Schemes?

Bank accounts are the primary payment channel for all international real estate acquisitions. Illicit operators maintain bank accounts across multiple jurisdictions, routing acquisition funds through multiple correspondent relationships to obscure their origin. Accounts held in the names of offshore entities ensure that the transaction record in the destination jurisdiction’s bank shows the corporate entity as the sending party, not the beneficial owner. Where the bank in the source jurisdiction has not applied adequate CDD on the account holder, the payment originated from a point of compliance failure that the destination jurisdiction cannot independently detect.

Nominee shareholding, non-public ownership records, layered corporate ownership, and historically bearer shares have been used to conceal beneficial ownership in offshore property structures. Where any ownership instrument or arrangement allows control to be transferred without transparent public disclosure, the AML risk increases materially. The UAE prohibition on bearer shares in domestic legal persons under CR 109/2023 closes this gap for UAE-registered entities. However, offshore companies in non-prohibitive jurisdictions can still hold UAE property-owning entities through such structures.

Equity interests in offshore legal entities are the standard instrument through which beneficial ownership of international property is separated from the land registry record. A natural person’s beneficial interest in foreign property is expressed as an equity interest in the offshore holding company, rather than as a direct ownership right, thereby preventing the land registry from disclosing the beneficial owner even when the registry is publicly accessible.

Real estate itself is the integration asset. Unlike financial instruments that are liquid and volatile, international property provides a stable, appreciating asset that is physically located in the destination jurisdiction and legally registered in the name of the offshore entity. The property’s immobility makes it a permanent component of the ML integration portfolio, generating income and value while remaining outside the direct reach of the source jurisdiction’s enforcement authorities unless a formal asset-tracing and recovery process is initiated.

Trust beneficial interests are exploited where the property is held through a trust structure administered by a TCSP in a secrecy jurisdiction. The beneficial interest in the trust is defined by the trust deed, which is a private document not accessible to the destination jurisdiction’s land registry or real estate agent. CR 134/2025 Article 10 requires DNFBPs such as real estate agents and banks to identify the settlor, trustee, protector, beneficiary class, and controlling person of any trust that appears in the ownership chain of a purchasing entity. This makes trust-held property subject to the same beneficial ownership tracing obligation as corporate-held property.

What Products and Services Do Criminals Abuse in International Real Estate Schemes?

Offshore banking services are the primary channel through which international acquisition funds are moved and stored. An offshore bank account held in the name of the purchasing entity receives funds from multiple sources, aggregates them, and wires the acquisition price to the destination jurisdiction. The offshore bank, subject to a different regulatory framework from the destination jurisdiction, may not apply CDD standards equivalent to those required in the UAE, creating a gap in the compliance chain that the destination jurisdiction’s real estate agent cannot fill.

Offshore company incorporation services provide the corporate holding vehicles that are the structural foundation of every international real estate ML scheme. A TCSP that incorporates an offshore holding company with nominee directors and shareholders, without identifying the ultimate beneficial owner, has created the concealment infrastructure on which the entire scheme depends. Under CR 134/2025, TCSPs operating in the UAE that provide company incorporation services are subject to DNFBP CDD obligations when performing those specified activities.

Real estate investment services, including cross-border investment advisory and portfolio structuring, are leveraged to provide a commercially credible rationale for large international property acquisitions. An investment advisory mandate covering a portfolio of international properties provides documentation supporting each acquisition as a professional investment decision, reducing the apparent anomaly of large purchases by entities with no prior real estate track record.

Real estate services, broadly, including brokerage and agency services in the destination jurisdiction, are the primary entry point for illicit funds into the international property market. A real estate agent who facilitates the transaction without completing adequate CDD on the offshore purchasing entity and without requesting source-of-funds documentation is the compliance failure that allows the integration to proceed.

Real estate transaction services, including legal conveyancing, notarial services, and title transfer in the destination jurisdiction, are secondary access points. A legal professional processing the transfer of title to an offshore company without independently verifying that company’s beneficial ownership or source of funds provides the legal instrument of integration without detecting it.

Trust and corporate services provide the complete structural package for international real estate ML. A TCSP that incorporates the offshore company, provides nominees, administers the trust overlay, maintains the account, and routes the acquisition funds, all without identifying the ultimate beneficial owner, has constructed an integrated concealment system that operates across jurisdictions simultaneously.

How AML UAE Helps Manage International Real Estate Risks

The compliance challenge in international real estate is not principally a legal uncertainty. The obligations are established and specific. Beneficial ownership must be traced to the natural person regardless of the jurisdictions traversed by the corporate chain; source of funds must be verified at origin, not at the offshore company; EDD must be applied to PEPs and high-risk customers; STRs must be filed on suspicion without a threshold.

The challenge is operational. Cross-border beneficial ownership tracing requires access to multiple corporate registries across multiple jurisdictions, familiarity with each jurisdiction’s disclosure standards, and the analytical capability to assemble a complete ownership picture from fragments of information held in different systems.

AML UAE works with real estate agents, financial institutions, and corporate service providers engaged in cross-border property transactions to build the operational capabilities required by international CDD. The compliance advisory service helps institutions design CDD frameworks for cross-border real estate transactions, including beneficial ownership tracing procedures for multi-jurisdictional corporate structures, country risk matrices, and EDD protocols for PEP-connected international buyers. The risk assessment service helps institutions build the cross-border real estate scenario into their enterprise-wide risk assessment. The AML training service equips compliance staff with the cross-border detection skills needed to identify the specific indicators that distinguish international real estate ML from legitimate cross-border investment.

Frequently Asked Questions

International real estate money laundering uses cross-border property acquisition, through offshore corporate structures, to integrate illicit proceeds across jurisdictions. The technique exploits the gap between AML supervision, which is national, and property ownership, which is global, ensuring that no single authority has a complete view of the transaction, the funding source, and the beneficial owner simultaneously.

Under CR 134/2025 Article 3(2), real estate agents and brokers are considered DNFBPs for the purchase and sale of real estate on behalf of their customers. This triggers the full CDD obligation mandated for DNFBPs, without any monetary threshold, regardless of the buyer’s nationality or residence. For an international buyer purchasing through an offshore corporate entity, the agent must identify the beneficial owner of that entity to the 25% threshold under Article 10, penetrating the ownership chain through every intermediate entity to the natural person, regardless of the jurisdictions traversed.

Yes. The REAR obligation applies to all freehold purchase and sale transactions in cash at or above AED 55,000, and to all transactions where any part of the consideration is funded by virtual asset conversion, regardless of the nationality or residence of the buyer. An international buyer paying cash above the threshold triggers the REAR obligation independently of any STR that may also be required.

The most commonly identified failure is the acceptance of first-layer corporate documentation without tracing the ownership chain to the natural person beneficial owner. Real estate agents who complete CDD on the presenting offshore entity, obtaining the company’s certificate of incorporation and the nominee director’s passport, without penetrating to the ultimate beneficial owner, satisfy the form of the obligation while leaving the beneficial owner entirely invisible.

A PEP identified through the beneficial ownership tracing of a foreign corporate purchaser triggers the full EDD requirement under CR 134/2025 Article 16. EDD requires source-of-wealth verification for the PEP, Senior Management approval for the transaction, and enhanced ongoing monitoring for the duration of the business relationship. The EDD obligation applies regardless of the jurisdiction in which the PEP holds public office, the value of the transaction, or the apparent commercial legitimacy of the acquisition structure.

Real estate round-tripping describes a specific variant of international real estate ML in which proceeds leave the UAE, are integrated into foreign property assets, and are then repatriated to the UAE as foreign investment returns. The technique exploits the fact that inbound investment from foreign jurisdictions may receive different scrutiny than CDD applied to UAE-origin funds, allowing illicit proceeds to re-enter the UAE economy with a foreign-investment provenance that obscures their domestic criminal origin.

Conclusion: International Real Estate

International real estate exploits the fundamental mismatch between the national scope of AML supervision and the global nature of property ownership, giving illicit operators a concealment mechanism that no single regulatory authority can fully close without cross-border cooperation. The offshore corporate structure, the nominee director, the correspondent-banking wire transfer, and the destination-jurisdiction real estate agent who accepts first-layer documentation are the four components of a scheme.

The UAE’s regulatory response is explicit and demanding. CR 134/2025 imposes CDD obligations on UAE-regulated real estate brokers and agents concluding purchase or sale transactions on behalf of customers, regardless of the buyer’s nationality or the complexity of the corporate structure.

The beneficial ownership tracing requirement under Article 10 should apply to every offshore entity in the ownership chain, without any jurisdictional limitation.

EDD under Article 16 is mandatory for every PEP-connected purchaser, regardless of the jurisdiction in which the PEP holds office. And the STR obligation under FDL 10/2025 Article 18 requires filing on suspicion wherever the cross-border circumstances of a transaction give grounds for concern, regardless of whether a REAR has been filed or whether the beneficial ownership has been satisfactorily established.

The implementation challenge is operational, not legal. Cross-border beneficial ownership tracing requires access to corporate registry data across multiple jurisdictions, the analytical capability to assemble a complete ownership picture from partial information, and the procedural infrastructure to promptly escalate when the chain cannot be fully traced. Institutions that have built this capability are fulfilling the substance of the obligation. Institutions that perform identity verification on the presenting entity without penetrating to the beneficial owner are fulfilling their form. In international real estate, the gap between form and substance is precisely where the illicit proceeds are hidden.

Investing in International Real Estate?

Understand the AML risks and due diligence requirements for cross-border property transactions.

Share via :

About the Author

Pathik Shah

FCA, CAMS, CISA, CS, DISA (ICAI), FAFP (ICAI)

Pathik is an ACAMS-certified AML consultant specialising in governance, risk, and compliance for regulated entities in the UAE. He brings over 28 years of experience, with 1,000+ hours of AML training and 200+ advisory engagements across DNFBPs, VASPs, and FIs. He supports businesses in aligning with AML/CFT requirements from the CBUAE, DFSA, MoET, MoJ, VARA, CMA, FSRA, and FATF. Known for translating complex regulations into audit-ready procedures, Pathik enables operational clarity and compliance readiness.

Reach Out to Pathik