Annual AML Return For DFSA

Annual AML Return submission is a paramount obligation for businesses operating in Dubai International Financial Centre (DIFC). Here’s the extensive uncovering of deadlines, reporting periods, key inputs to include in submission, adverse effects of not filing it, and a thorough checklist and RACI chart to understand the filing necessities and accountabilities.

What is the Annual AML Return for DIFC Reporting Entities?

Reporting Entities in Dubai International Financial Centre (DIFC) are mandated to submit an annual return with regard to their Anti Money Laundering (AML) program to the Dubai Financial Services Authority (DFSA). The anchor point to the filing of this annual return is to provide the DFSA with a comprehensive overview of the adherence to AML obligations, AML issues, emerging trends and the effectiveness of related controls.

Keeping Pace with Annual AML Return Compliance Requirements

The Annual Report form should be submitted covering all relevant AML-related incidents and compliance matters occurring between 1st August of the preceding year to 31st July of the reporting year, as mandated by the DFSA.

Ensure every report finds its way through DFSA’s designated ePortal platform as a priority.

The DFSA grants a generous timeframe by making the Annual AML Return form available on its ePortal two months prior to the submission deadline, allowing Reporting Entities a cushion of time to submit without rush.

Complete. Consistent. Accurate.

Engage us to prepare and file the Annual AML Return for your business.

Who’s on the AML Annual Return Filing List?

Any Reporting Entities having their business operations under Dubai International Financial Centre (DIFC) are required to submit their AML Annual Return as a yearly ritual. These specific Reporting Entities include:

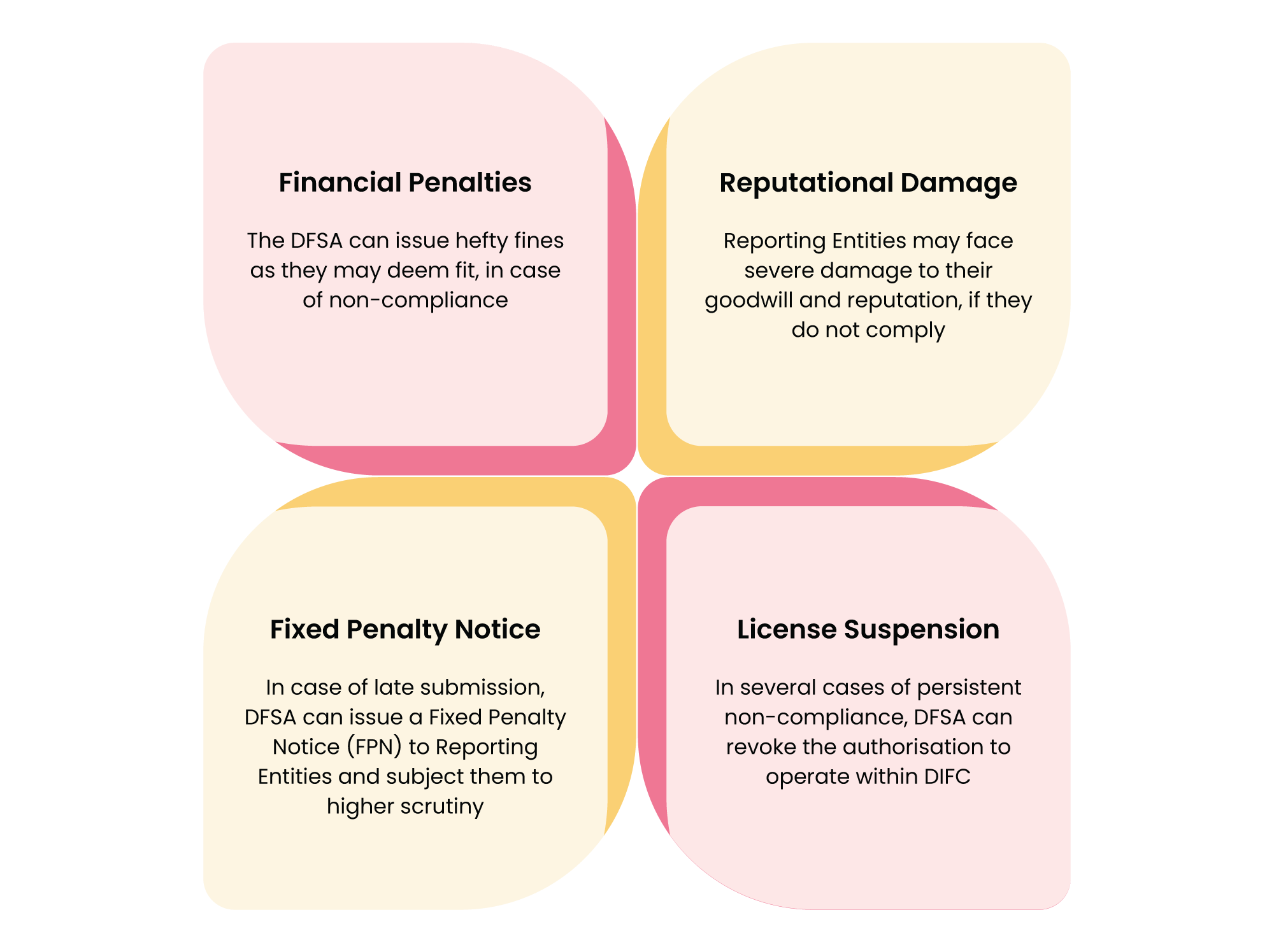

Ripple Effect of Missing the Deadlines: Non-Compliance Consequences

The consequences can be severe for missing the filing deadline of the Annual AML Report.

Get on a call with our AML experts and identify what services you need.

Don’t delay your access to our timely, cost-effective, and quality AML Consultancy services.

Key Inputs for the AML Annual Report

Reporting Entities are required to create a version of information before they file an annual report. This version includes elements like the firm’s profile, business relationships and services, customer information, geographic risk exposure, and AML/CFT policies, procedures, and controls.

Assess Your Preparedness for Filing Annual AML Return: Checklist for Robust Regulatory Compliance

Preparation and Deadlines

- Does the firm qualify as a “Relevant Person” required to submit the annual return as per the DFSA AML Rule 14.5.1?

- Has the Annual AML Return Form from the DFSA ePortal been retrieved and ready for use?

- Has the Money Laundering Reporting Officer (MLRO) received the official notification from DFSA regarding the Annual AML Return submission?

- Is the firm aware of the deadline for submitting the Annual AML Return?

- Are the MLRO’s contact details on the DFSA ePortal current and accurate?

- Is the Firm aware of the “Reporting Period” timeframe for covering the data in the submission?

Yes

No

Firm and Senior Management Details

- Have all senior management and members of the governing body been identified for the reporting period?

- Has the senior management fulfilled its AML responsibilities during the reporting period?

- Has the senior management approved the AML Annual Return prior to the submission to DFSA?

- Has the firm reported the arrangements they have made to deal with the absence of MLRO?

- Has the firm accurately disclosed the responsibilities fulfilled by senior management during the reporting period?

- If the MLRO is outsourced, then is the information related to the outsourced provider and other relevant information correctly reported?

Yes

No

Risk Assessment and Policies

- Has the firm reviewed and confirmed that the Business AML Risk Assessment (BARA) is up to date before reporting?

- Have all the details regarding Customer Risk Assessment been disclosed in relation to the reporting period?

- Have all business relationships with Financial Institutions and DNFBPs during the reporting period been listed?

- Are current Anti-Money Laundering (AML) and Counter Financing Terrorism (CFT) policies and procedures readily available for review before reporting?

- Have any previous updates or amendments been made to AML Policies during the reporting period, and are they ready to be submitted?

- Has the data related to Customer Due Diligence (CDD), Enhanced Due Diligence (EDD) and Ongoing Monitoring conducted during the Reporting Period been easily accessible before reporting?

Yes

No

Suspicious Activity Reporting

- Are the internal systems and controls for detecting Suspicious Activity and Suspicious Transactions clearly documented?

- Are the number of internal SARs and STRs raised during the reporting period accessible for reporting?

- Are the external SARs and STRs submitted to the Financial Intelligence Unit clearly recorded and in place for reporting?

Yes

No

Submission and Documentation

- Have all members of senior management formally acknowledged and signed off before submitting it to DFSA?

- Has the signed declaration been uploaded to the DFSA ePortal as per their mandate?

- Is all information provided in the Annual AML Report complete and accurate?

- Have all the copies of relevant documents been submitted?

- Are the answers submitted precise and to the point?

- Have relevant AML Module terms and references been incorporated while framing answers for the AML Annual Return?

- Has a copy of the submitted Annual AML Return been retained for the record?

Yes

No

Training and Awareness

- Has appropriate training been provided to staff regarding the filing of the Annual AML Return?

- Are the senior management and MLRO well-versed in the DFSA AML Module before submitting the return?

- Have the frequency and methodology of training provided to the employees been accurately reported in the submission?

Yes

No

Complete. Consistent. Accurate.

Engage us to prepare and file the Annual AML Return for your business.

How RACI Matrix Simplifies Annual AML Return Task Delegation and Role Clarity

What is RACI?

RACI framework enables internal governance by providing information on who will be responsible for work, who will be accountable, who will be consulted and who will be informed.

How does the RACI Framework help?

- Clarifies the roles and responsibilities for the AML Annual Return submission activity among the team.

- Enables entities to stay aligned with the regulatory expectations of DFSA.

- Reduces the gaps or duplications of work and improves coordination.

RACI Chart for Filing Annual Return for DFSA

How Does AML UAE Help You With Your AML Annual Return?

AML UAE takes pride in bridging the gaps between your business and robust AML compliance.

| Difficulties Encountered by Reporting Entities | Results that Speak |

| Unsure what to immerse in an AML Annual Return? | We guide you throughout with a clear checklist of required information. |

| Stuck anywhere while filing the AML Annual Returns? | Our expert professionals are ready to help you at points of confusion. |

| Have other priority tasks to complete? | We assist you as a team that makes you feel relaxed from regulatory obligations. |

| Running late? Scared of penalties? | Our clients rely on us to submit the returns on time. |

| Made the AML Annual Return Report not up to the mark. | AML UAE helps you with an accurate and complete structured AML Annual Return to safeguard from non-compliance. |

AML UAE - The Right Fit for Your AML Compliance Needs

AML UAE is your trusted partner that provides extensive support with the AML Annual Return filing requirements. We have a team of experienced professionals who will help you file your AML Annual Return on time to save you from heavy penalties and reputational damage. Our experts are equipped with AML Compliance knowledge to place your essential resources where needed and help you remain ready with the AML Annual Return during submission season.

Say Goodbye to Compliance Worries

AML UAE stand ready to guide and support you with all your compliance needs.

Frequently Asked Questions on Annual AML Return For DFSA

Yes, all the authorised firms operating in the DFSA’s jurisdiction should mandatorily submit the AML annual returns. It’s a regulatory requirement which also applies to any firm that was authorised within the reporting period or has performed very limited or no business to date since its authorisation. All firms must comply with AML Rule 14.5.1 by the due date.

The reporting period for the DFSA AML Return is from 1 August of the previous year to 31 July of the reporting year. For consistency, figures as at 31 July should be used, even though figures may fluctuate during this period.

You can find the AML Return form on the DFSA ePortal.

You are supposed to submit the AML Return via DFSA’s ePortal, where all the responses should be precise, accurate, and limited to the specific questions.

As per AML rule 14.5.1, the submission deadline falls at the end of September of each reporting year, where DFSA generally makes the return available two months prior to this deadline. If there is any delay in releasing the return, the submission date will be adjusted to ensure that all the firms still get the full timeframe to complete the filing and submit it successfully.

Any types of general communications related to the Annual AML Return, including extension-related requests, can be made through the Supervised Firm Contact Form via the DFSA ePortal.

If you fail to submit the return within the specified timeframe (usually 30th September), then, as per Article 91 of the Regulatory Law, the Fixed Penalty Notice process may be initiated.

- When: By the end of September each year (usually 30th September)

- Where: DFSA ePortal.

If DFSA has any queries while reviewing your AML Return, it will contact Firms individually.