Entertainment Venture Fronts

Last Updated: 06/15/2026

Protect your business with reliable and effective AML strategies with AML UAE.

Entertainment Venture fronts - Key takeaways

Fronts operated under an entertainment brand conceal illicit funds by reporting fabricated ticket sales, licensing fees, and sponsorship income as legitimate revenue. Compliance teams that fail to apply enhanced due diligence to these structures risk enabling the integration stage of money laundering. Scrutinise revenue verifiability, beneficial ownership transparency, and cross-border payment flows before establishing any entertainment sector relationship.

What is Entertainment Venture Fronts?

What is an entertainment venture front in AML?

An entertainment venture front is a businaess that presents itself as a legitimate entertainment company but may be used to disguise criminal proceeds as ticket sales, sponsorship income, licensing fees, royalties, or production revenue. The AML risk arises where the reported revenue, ownership structure, counterparties, or payment flows cannot be independently verified.

Are entertainment businesses automatically high risk?

No. Entertainment businesses are legitimate commercial entities. The risk increases where there is opaque beneficial ownership, unverifiable revenue, unusual cash deposits, unexplained offshore royalty flows, inflated production budgets, or counterparties with no genuine commercial presence.

Formally described, an entertainment venture front is a legal entity registered or presenting itself as operating in the entertainment sector, including live events, film production, music publishing, sports promotion, or digital content distribution, that exists primarily or substantially to receive, process, or disguise proceeds of crime through the reporting of fabricated or inflated commercial revenues. The underlying predicate offences that generate the illicit funds range from narcotics trafficking and fraud to corruption and organised crime.

The mechanism places such a structure squarely within the definition of a money laundering vehicle under Federal Decree Law No. (10) of 2025 Concerning Anti-Money Laundering and Combating the Financing of Terrorism and Proliferation Financing (FDL 10/2025). Article 2 of FDL 10/2025 criminalises the acquisition, possession, transfer, exchange, or deposit of funds where the perpetrator knows those funds are the proceeds of a predicate offence and intends to conceal their illicit origin.

Regulatory Reference

Federal Decree Law No. (10) of 2025, Article 2 (Money Laundering Criminalisation) | Cabinet Resolution No. (134) of 2025, Articles 6-9 (Customer Due Diligence Obligations) | Cabinet Resolution No. (109) of 2023, Article 8 (Real Beneficiary Register Obligations)

Regulatory Framework Related to Entertainment Venture Fronts

The primary UAE regulatory instruments applicable to this typology are FDL 10/2025, Cabinet Resolution No. (134) of 2025 Concerning the Implementing Regulations of FDL 10/2025 (CR 134/2025), and Cabinet Resolution No. (109) of 2023 Concerning the Procedures Regulating Real Beneficiaries (CR 109/2023).

FDL 10/2025 Article 19 imposes a comprehensive set of preventive measures on all financial institutions (FIs) and Designated Non-Financial Businesses and Professions (DNFBPs), including the obligation to identify and verify the identity of customers and beneficial owners and to apply enhanced due diligence (EDD) to higher-risk relationships.

CR 134/2025 Article 10 operationalises beneficial ownership (BO) identification, requiring obliged entities to identify and verify any natural person holding, directly or indirectly, 25% or more of the ownership or control of a legal person.

CR 109/2023 Article 8 requires every UAE legal person to maintain a Real Beneficiary Register and update it within 15 days of any material change in ownership.

Administrative penalties for failing to apply adequate customer due diligence are set out in Cabinet Resolution No. (71) of 2024 (CR 71/2024).

Failures in EDD carry a maximum administrative fine of AED 500,000 per CR 71/2024 Violation Serial Numbers 15-17. Failures in ongoing monitoring carry a maximum of AED 500,000 per CR 71/2024 Violation Serial Number 19.

Primary Authority or Supervisory Body

In the UAE, the Central Bank of the UAE (CBUAE) supervises licensed financial institutions, including banks and payment service providers that are most likely to process entertainment sector transactions. The Ministry of Economy and Tourism (MOET) supervises DNFBPs, including accountants, auditors, trust and company service providers (TCSPs), and dealers in precious metals and stones. The Ministry of Justice supervises lawyers, notaries, and other legal professionals. The General Commercial Gaming Regulatory Authority (GCGRA) regulates the commercial gaming operators.

The UAE Financial Intelligence Unit (UAE FIU), established as an independent unit within the CBUAE under FDL 10/2025 Article 11, receives all Suspicious Transaction Reports (STRs) exclusively through the goAML platform. The Executive Office for Control and Non-Proliferation (EOCN) administers the UAE’s targeted financial sanctions (TFS) regime.

Compliance Obligations and Channels of Entertainment Venture Fronts

Any FI or DNFBP that identifies or suspects that an entertainment entity is being used to launder funds must file an STR with the UAE FIU via goAML without delay, per FDL 10/2025 Article 18 and CR 134/2025 Article 18. The obligation to file arises upon forming a reasonable suspicion; a confirmed finding is not required. Tipping off the customer about a pending STR is a criminal offence under FDL 10/2025 Article 29.

Before establishing a business relationship with an entertainment entity, obliged entities must perform CDD under CR 134/2025 Articles 6-9, including obtaining information about the nature and purpose of the relationship, verifying the identity of the legal person, and identifying and verifying beneficial owners to the 25% threshold under CR 134/2025 Article 10. Records of all CDD documentation, transaction data, and business correspondence must be retained for a minimum of five years per CR 134/2025 Article 25.

Recent Developments, Enforcement Actions, or Supervisory Priorities

FDL 10/2025, which came into force on 14 October 2025, repeals Federal Decree Law No. (20) of 2018 and its amendments. Its Executive Regulation, CR 134/2025, came into force on 14 December 2025. The new statute materially strengthens the UAE’s AML/CFT framework, including a broader definition of predicate offences, enhanced FIU powers, and a revised administrative penalty scale under Article 17 that reaches AED 5,000,000 per violation.

The UAEFIU Strategic Analysis Report on TF Typologies and Facilitators (May 2025) identifies corporate structure establishment as a documented method used to move terrorist financing through UAE financial channels. Front companies are specifically cited as operational vehicles. Compliance teams must treat entertainment entities with opaque corporate structures as elevated-risk customers.

What Does Entertainment Venture Fronts Mean?

Picture a restaurant that never actually serves food but always reports full tables and a packed kitchen. The kitchen activity is a fiction; the revenue reports are designed to make illicit money appear to have come from hungry diners. Entertainment venture fronts work on the same principle. The concerts, films, sponsorship deals, and licensing agreements are the empty tables. The documented revenue they generate is the mechanism that converts criminal proceeds into income that can be spent, invested, and explained to any authority that asks.

The entertainment venture front is used in this article as a typology label, not a separate statutory category under UAE AML law. The legal obligations arise from the entity’s status as a customer, FI, DNFBP, VASP, or legal person, and from the underlying facts that create ML, TF, or PF risk or suspicion.

Why Entertainment Venture Fronts Matter

Entertainment businesses handle large, variable, and frequently cash-inclusive revenue streams that are inherently difficult to verify against objective benchmarks. Ticket sales, sponsorship agreements, licensing royalties, and production budgets do not carry market-standard prices that a compliance officer can validate simply by consulting a public tariff. This structural opacity is what makes the entertainment sector attractive for the integration stage of money laundering, the point at which illicit funds enter the legitimate economy in a form that survives scrutiny.

The UAEFIU Strategic Analysis Report on TF Typologies and Facilitators (May 2025) confirms that corporate structure establishment, including the use of front and shell companies presenting as legitimate businesses, is a documented method for moving funds through UAE financial channels.

International AML typology materials similarly recognise front companies in cash-intensive, high-revenue-variability sectors as a known integration-stage vehicle, given the structural difficulty of benchmarking reported revenues against verifiable commercial data.

For regulated entities in the UAE, the practical consequence is direct. A bank that maintains an account for an entertainment venture front and processes its fabricated revenues without filing an STR is exposed to criminal liability under FDL 10/2025 Article 28 and administrative penalties of up to AED 500,000 for STR filing failures per CR 71/2024. An accountant who audits the same entity’s accounts without applying the CDD and reporting obligations faces administrative penalties of up to AED 500,000 and potential criminal liability.

Fabricated revenue, inflated costs, and inflated losses in an entertainment vehicle can also create tax and accounting exposure for the entity and its advisers. This article does not provide tax advice; entities should assess any such exposure with a qualified tax or accounting professional.

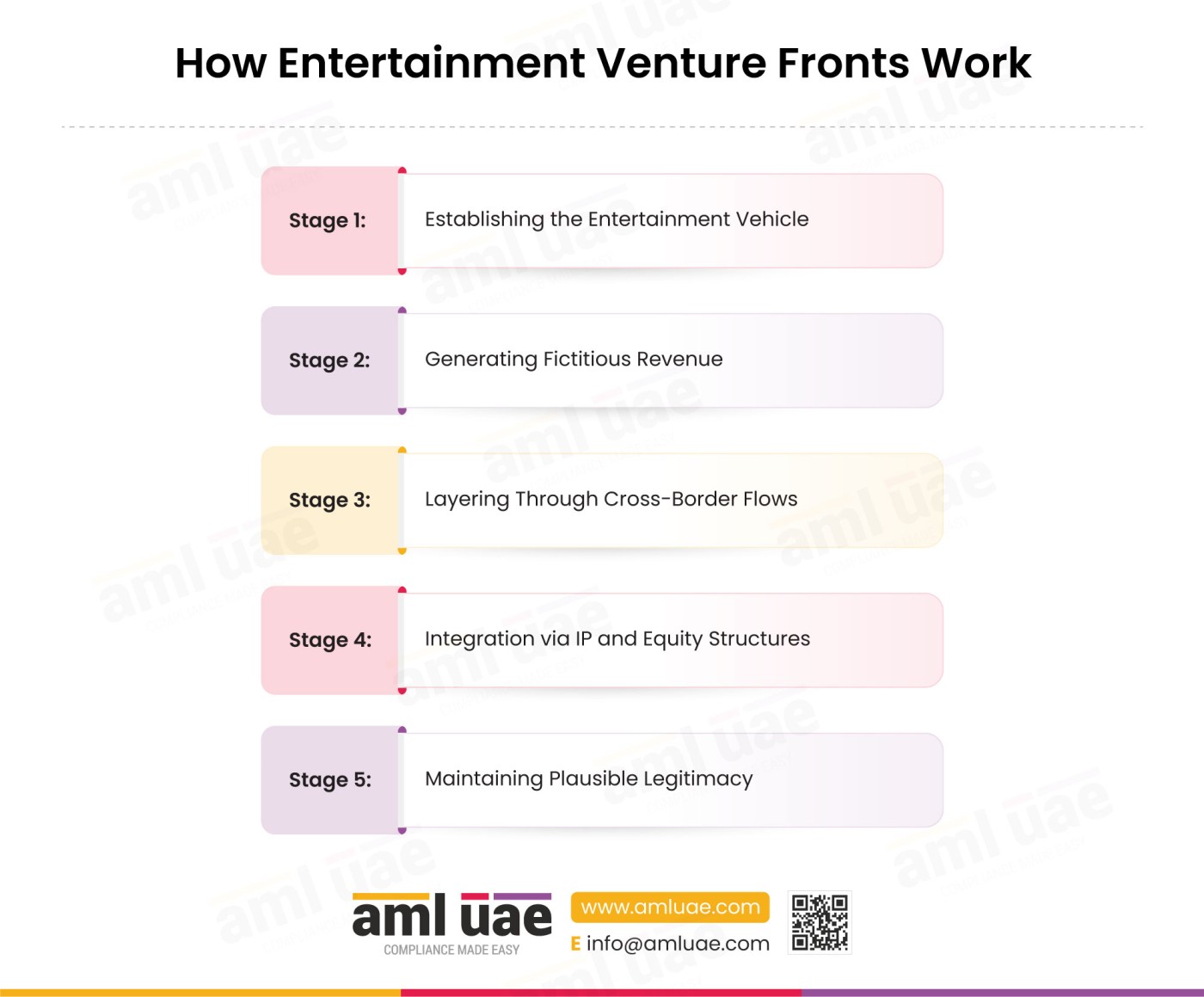

How Entertainment Venture Fronts Work

Stage 1: Establishing the Entertainment Vehicle

The illicit operator, or a professional intermediary acting on their behalf, incorporates a legal entity presenting as an entertainment business. The entity typically acquires a trade name with credible market associations: a concert promotion firm, a film production house, a sports talent management company, or a music publishing label.

Offshore company incorporation services are engaged to create a holding structure that separates the presenting entity from the beneficial owner. Trust and corporate service providers in secrecy jurisdictions are used to install nominee directors and shareholders, obscuring any direct link between the illicit operator and the registered entity.

Stage 2: Generating Fictitious Revenue

With the corporate vehicle in place, the illicit operator begins recording fabricated commercial transactions. Cash generated from criminal activity is introduced as ticket sales, merchandise revenue, or production advances. Alternatively, inflated invoices are raised against affiliated entities. The payer is an entity controlled by the same beneficial owner, and the transaction creates an apparent commercial obligation with no genuine underlying service.

Accounts receivable instruments are produced to document each transaction, creating a paper trail that appears consistent with legitimate commercial practice.

Stage 3: Layering Through Cross-Border Flows

Funds are then moved across jurisdictions through cross-border payment services and correspondent banking channels.

Royalty payments are directed to IP rights-holding entities registered in low-disclosure jurisdictions. Licensing fees are paid to unverifiable intermediaries.

Production cost advances are transferred to offshore accounts and returned through ostensibly different payment channels. Each transaction adds a layer of distance between the illicit source and the settled funds, exploiting the natural complexity of international entertainment supply chains.

Stage 4: Integration via IP and Equity Structures

At the integration stage, the illicit operator converts accumulated funds into legitimate assets. Equity interests in entertainment entities are sold or transferred, generating capital gains that are entirely legitimate in form.

Intellectual property rights to music catalogues, film libraries, or sports broadcasting licences are transferred between affiliated entities at valuations that bear no relationship to independent market assessments.

Criminal proceeds appear as investment returns from a credible sector, documented by a chain of corporate transactions.

Stage 5: Maintaining Plausible Legitimacy

The operator sustains the fiction through selective engagement with real commercial activity. Occasional genuine events are produced, genuine artists or talent are engaged, and real audiences are generated. The ratio of real to fabricated revenue is managed to ensure that the overall financial profile does not trigger automated detection.

Business bank accounts are maintained across multiple institutions to fragment the transaction record, making pattern detection across accounts more difficult for any single compliance team.

Real-World Examples of Entertainment Venture Fronts

The Concert Promoter and the Phantom Ticket Sales

A concert promotion company is incorporated by an illicit operator who controls a narcotics distribution network. The company announces a series of large-scale music events, issues tickets through a payment processing intermediary it controls, and records substantial ticket sale revenues. Attendance at the events is genuine but modest; the reported revenues are four times the actual income. The company’s bank processes the deposits as commercial revenue, applying standard CDD and noting only that the client operates in the entertainment sector.

The scheme is only identified when adverse media links one of the company’s directors to a criminal investigation in a third country.

The operational lesson: revenue verification for entertainment clients must go beyond face-value assessment of deposits and must include independent confirmation of event scale, ticket sales data, and venue capacity.

The Music Label with Offshore Royalty Chains

A music label registers five catalogue-holding entities across three low-disclosure jurisdictions. The label pays royalties to these entities for the use of music rights in streaming and licensing deals. The royalty rates paid are fifteen times the market standard for catalogue music of comparable commercial value. Financial statements show substantial royalty expenses and a corresponding reduction in taxable income. The beneficial owner of all five offshore entities is the same person who controls the label, obscured through nominee shareholders.

The scheme is detected during an EDD review triggered by a large cross-border payment to an entity in a jurisdiction on the FATF grey list. OSINT reveals that the catalogue entity has no identifiable employees, offices, or prior commercial activity. The operational lesson: royalty payment analysis must include an independent assessment of the applicable market rate, and any payment to an entity that cannot demonstrate genuine IP ownership warrants an STR review.

The Film Production House and the Inflated Budget

A film production company raises investment capital through equity interests sold to investors whose ultimate beneficial owners are not disclosed to the company’s bank. The company produces a film with a stated production budget of USD 8 million. Actual production costs are USD 2.5 million; the remaining USD 5.5 million is disbursed through service provider invoices to entities that are subsequently wound up or become uncontactable. The film generates negligible revenue. The investors record a capital loss that is used to offset gains elsewhere in their portfolio.

A forensic review of the invoicing structure reveals that multiple service providers shared beneficial ownership with the investors. The operational lesson: investment structures in the entertainment sector must be subject to source-of-funds analysis, and service provider invoices must be verified against independently confirmed deliverables.

Classification Specific Deep-Dive

What Are the Red Flags That Identify Entertainment Venture Fronts?

The following indicators are presented as observable conditions, not conclusions.

| Category | Red Flag |

| Customer | Multiple affiliated entities linked to the same entertainment business, with inconsistencies in director and shareholder details across different corporate jurisdictions |

| Customer | A newly incorporated entertainment entity seeking high-value transactions immediately after incorporation, with no verifiable trading history, event history, or identifiable industry footprint |

| Customer | Sponsorship commitments documented as income from entities that cannot provide audited financial statements, identifiable beneficial owners, or verifiable operating history commensurate with the stated sponsorship value |

| Customer | Beneficial ownership records that are contradictory or incomplete across multiple corporate vehicles connected to the same entertainment group |

| Transaction | Ticket sale deposits or advertising payments in amounts inconsistent with independently verifiable venue capacity, attendance data, or market rates for comparable events |

| Transaction | Production budget payments made against invoices where the stated scope of work is not supported by verifiable contracts, deliverables, or evidence of the service provider’s capacity |

| Transaction | Cash deposits that are large and frequent relative to the scale of the entertainment business, including the known revenue model of comparable entities in the sector |

| Transaction | Licensing fees paid to entities that cannot be traced to any original creator, rights registry, or verifiable IP ownership chain |

| Transaction | Royalty or licensing payments routed through multi-jurisdictional intermediaries with no commercial explanation for the involvement of each intermediate entity |

| Transaction | Funds received from foreign box office or distribution markets where no verifiable distribution agreement, audience data, or counterparty entity can be independently confirmed |

| Geographic | Repeated payment flows directed to or received from jurisdictions included on FATF lists of countries subject to increased monitoring |

| Geographic | Cross-border payment flows involving jurisdictions with low corporate disclosure requirements, where BO of the counterparty entity cannot be independently confirmed |

| Product | IP rights transferred between affiliated entities at valuations that a licensed valuation professional would be unable to reconcile with independent market comparables |

| Product | Accounts receivable invoices raised for entertainment services where the stated counterparty has no identifiable commercial presence outside the transaction documentation |

| Channel | Use of multiple business bank accounts across different institutions to process entertainment revenue in a manner that fragments the transaction record |

Distinguishing a Legitimate Entertainment Business from a Front

Entertainment businesses are legitimate commercial entities, and the typology described here applies only to a minority that are misused. The distinction turns on whether revenue, ownership, and royalty flows can be independently verified.

Where an entertainment business operates through a ticketing or payment platform, further red flags arise where the platform is controlled by the same beneficial owner as the entity, where refunds or chargebacks are abnormally high, where ticket purchases are concentrated in unusual patterns, where repeated card payments originate from related cards or geographies, or where high-value ticket purchases are inconsistent with the event profile.

Payment and Ticketing Red Flags

Legitimate Entertainment Business | Possible Entertainment Front |

Revenue aligns with venue capacity, ticketing data, and contracts. | Revenue cannot be reconciled with attendance, platform data, or market rates. |

Beneficial ownership is transparent and commercially justified. | Ownership is opaque, layered, or nominee-driven. |

Royalties are linked to verified IP rights. | Royalties are paid to entities with no verifiable IP ownership. |

Cash activity is event-driven. | Cash deposits are regular, mechanical, or inconsistent with events. |

Which Controls Counter Entertainment Venture Fronts?

| Control | What It Disrupts | Type | Limitation |

| Enhanced Due Diligence (EDD) | Obscured BO; unverifiable corporate history; inflated revenue claims | Detects | Depends on document quality; sophisticated operators produce professionally prepared false documentation |

| OSINT and External Source Verification | Fabricated event revenues; phantom box office proceeds; unverifiable sponsorship origins | Detects | Public data on private events and non-public entertainment contracts is often limited |

| Trade Monitoring | Invoice manipulation; IP licensing abuse; service provider invoice fraud | Detects / Prevents | Requires staff with sector-specific knowledge to assess whether entertainment contract terms are commercially plausible |

| Transaction Monitoring | Cash structuring; cross-border layering; account fragmentation | Detects | Standard rule sets may not account for the legitimate revenue variability of entertainment businesses |

How Do AI and RegTech Automate Detection of Entertainment Venture Fronts?

Transaction monitoring platforms that apply machine learning anomaly detection identify revenue patterns inconsistent with the declared business model. Where an entertainment entity records deposits that consistently exceed the revenue ceiling implied by its declared operational scale, an anomaly detection model trained on sector benchmarks will surface those patterns for human review, rather than applying static threshold-based rules that an operator can calibrate around.

Network analytics and graph-based relationship detection tools map corporate structures and identify hidden connections between entities that share directors, registered addresses, or payment counterparties. A graph analytics engine that visualises all entities connected to a single beneficial owner across multiple jurisdictions will surface the circular ownership and payment structures that manual review of individual accounts would miss.

Natural language processing (NLP) applied to adverse media databases and court filings identifies negative signals linked to entertainment entity directors, shareholders, and associated persons that do not yet appear on formal sanctions lists. Intelligent document review tools apply automated analysis to financial statements, invoices, and contracts submitted during CDD, flagging internal inconsistencies such as invoices that reference tax registration numbers belonging to dissolved entities.

AI-driven peer comparison engines benchmark an entertainment client’s financial profile against anonymised sector peers at comparable revenue scale. Persistent deviations from sector norms, such as unusually high cash ratios, anomalous royalty payment frequencies, or revenue concentration in a single counterparty, are surfaced as prioritised alerts.

What Data Should Compliance Teams Collect to Detect Entertainment Venture Fronts?

| Data Point | Source System | What It Reveals |

| Corporate registration and director history | Company and BO registries; offshore registry searches | Identifies nominee structures, recently incorporated entities, and discrepancies between declared and actual controllers |

| BO declarations vs. registry data | KYC platform cross-referenced against national and offshore BO registries | Reveals whether the 25% BO threshold disclosure under CR 134/2025 Art. 10 is consistent with independent registry data |

| Revenue documentation: ticket sales, licensing agreements, production contracts | Contractual and invoice data submitted during CDD or EDD | Allows comparison of declared revenues against independently verifiable data |

| Cross-border transaction records: volume, frequency, counterparty jurisdiction | Correspondent and cross-border transaction data; core banking systems | Identifies routing to high-risk jurisdictions; reveals payment fragmentation across accounts |

| Cash deposit patterns relative to sector benchmarks | Transaction logs; transaction monitoring system | Reveals structuring behaviour inconsistent with an event-driven revenue model |

| Adverse media and court filing data linked to entity personnel | Adverse media database; court filing searches | Surfaces criminal associations, ongoing investigations, or prior convictions |

| Tax filings and financial statements | Financial, business, and tax records | Identifies mismatches between declared revenue, reported expenses, and independently verifiable commercial activity |

| Jurisdictional risk profile of counterparty entities | Geographical and jurisdictional risk data; FATF lists | Assigns risk weighting to cross-border payment flows based on the AML/CFT framework strength of the counterparty jurisdiction |

Open-source intelligence, adverse-media screening, registry searches, and multi-language searches should be conducted within the entity’s data protection and privacy framework, and personal data gathered for AML purposes should be handled in accordance with applicable UAE data protection requirements.

Who Is Affected

How Entertainment Venture Fronts Aggravate Customer Risk and Jurisdictional Risk

Entertainment venture fronts directly aggravate customer risk by making it structurally difficult to establish the true beneficial owner of the entity presenting for a business relationship.

The corporate vehicles used to operate entertainment fronts are typically multi-layered, combining domestic operating entities with offshore holding structures that deliberately obscure the line of ownership.

A compliance team applying standard CDD to the operating entity alone will identify only the nominee directors and registered shareholders, not the illicit operator who controls the structure.

Jurisdictional risk is aggravated because the layering mechanism depends on cross-border flows routed through jurisdictions chosen for their limited disclosure requirements. Each payment to or from a low-disclosure jurisdiction compounds the difficulty of mapping the true transaction counterparty and introduces the risk of inadvertent interaction with sanctioned entities whose names are obscured by the corporate structure.

What Observable Patterns Signal Entertainment Venture Fronts to a Compliance Officer?

A compliance officer reviewing CDD files or transaction records for an entertainment sector client would find the following observable patterns consistent with this typology.

Financial documentation submitted to support revenue claims shows internal inconsistencies: invoice dates that do not align with event dates, venue hire agreements issued by entities that cannot be traced to any identifiable operator, or ticket sale confirmation records that do not bear the digital signatures of established ticketing platforms.

Transaction records show cash deposits at intervals and values that suggest a mechanical introduction of funds rather than organic commercial income; the pattern is regular rather than event driven. Cross-border payments are directed to multiple counterparties in different jurisdictions, none of which can be identified as having a genuine role in the entertainment supply chain.

Corporate documentation reveals that the entertainment entity shares a registered address, a corporate secretary, or a formation agent with other entities that have no visible connection to the entertainment sector.

Sectors at Highest Exposure

| Sector | Risk Rating | Reasoning |

| Banking, corporate and commercial | Critical | Processes primary account activity including cash deposits, cross-border payments, and invoice-based transactions |

| Accounting, auditing, and bookkeeping | Critical | Prepares or certifies financial statements that form the evidentiary basis for legitimising fabricated revenues; MOET-supervised DNFBP |

| Trust and corporate service providers | High | Incorporates offshore holding structures and installs nominee arrangements that conceal the BO; MOET-supervised DNFBP |

| Payment processing services | High | Processes ticket sales and event revenue, creating the transaction records that support the fictitious income narrative |

| Legal professionals | High | Advises on corporate structuring, IP rights transfers, and investment arrangements; MOET/MoJ-supervised DNFBP |

| Cross-border payment providers | Moderate | Facilitates offshore layering of entertainment revenues; exposure depends on the jurisdictions and counterparties involved |

Geographies and Contexts of Concern

In the UAE context, the entertainment sector has expanded materially since 2020, with Dubai and Abu Dhabi hosting a growing volume of international concerts, sports events, film productions, and digital content operations. This genuine commercial growth creates a plausible context for entertainment front operators, who can reference the sector’s genuine growth to explain the scale of their declared revenues.

The UAE’s 2024 National Risk Assessment identifies the integration stage of money laundering as a key national risk and notes the use of complex corporate structures as a documented method for obscuring beneficial ownership.

Cross-border flows from UAE entertainment entities to jurisdictions on FATF increased-monitoring lists, jurisdictions subject to FATF countermeasures, or jurisdictions with limited beneficial ownership transparency should be assessed against the full EDD framework under CR 134/2025 Article 23.

Best Practices for Entertainment Venture Fronts Risk Management

- Before establishing any relationship with an entertainment entity, request a comprehensive ownership structure chart that maps every entity in the corporate group to its natural person beneficial owners. Verify the stated 25% ownership threshold against the UAE commercial register, MOET business registry, and any available offshore registry data for non-UAE incorporated entities. Where a corporate entity rather than a natural person satisfies the threshold, apply a look-through analysis until a natural person is identified, per CR 134/2025 Article 10.

- Obtain and independently verify the entertainment entity’s trading history. Confirm verifiable prior events, productions, or commercial outputs against publicly available sources: venue booking records, industry databases, streaming platform catalogues, sports event regulatory filings, or equivalent. An entity that cannot produce independently verifiable evidence of prior commercial activity presents a materially elevated risk that warrants EDD or declination.

- Apply OSINT to all directors, shareholders, and declared beneficial owners of the entertainment entity before and during the relationship. Include adverse media searches in multiple languages relevant to the jurisdictions where the entity operates. Cross-reference against PEP databases, court filing archives, and insolvency registers.

- Scrutinise income documentation for internal consistency. Ticket sales records should align with venue capacity at the declared ticket price across the declared number of events. Licensing income should be reconcilable with the stated IP catalogue and applicable market royalty rates. Production budgets should be supported by contracts with identified, verifiable service providers.

- Apply trade monitoring to all invoices and contractual documentation provided by entertainment sector clients. Identify invoices raised against entities that share beneficial ownership with the client, that are recently incorporated, or that cannot be reached through independent channels. Flag circular payment flows where funds paid out as expenses return through a different channel as income.

- Set enhanced transaction monitoring rules for entertainment sector accounts that account for the legitimate revenue variability of the sector while identifying patterns inconsistent with the declared business model. Rules should flag cash deposits that are regular rather than event-driven, and cross-border payments to jurisdictions with no apparent role in the client’s declared supply chain.

- Apply EDD and senior management approval requirements to any entertainment entity that uses offshore holding structures, nominee arrangements, or multiple affiliated entities before establishing or renewing the relationship. The EDD review must include source-of-funds and source-of-wealth analysis for the declared beneficial owner.

- File an STR via goAML without delay whenever the review of a new or existing entertainment sector relationship generates reasonable suspicion that the entity is a vehicle for money laundering, even if the suspicion cannot be confirmed through available documentation. The obligation to file arises on suspicion, not on certainty, per FDL 10/2025 Article 18.

- Train front-line relationship managers and onboarding teams in the specific behavioural and documentary red flags associated with entertainment fronts. Sector-specific training that walks through the revenue verification process for ticket sales, royalties, production budgets, and sponsorship agreements equips first-line staff to escalate effectively.

- Maintain a five-year retention record of all CDD documentation, transaction records, and correspondence related to entertainment sector relationships, as required by CR 134/2025 Article 25. Where a relationship is exited or declined due to AML concerns, retain the file with a documented record of the reasons for the decision.

In the entertainment files I have reviewed, the schemes that clear onboarding are the ones whose documentation looks complete on its face. The practices above work because they force verification outside the file: ownership charts checked against the registry, ticket revenues reconciled to venue capacity, royalties tied to a verifiable catalogue and rate. Treat trading-history checks, look-through BO analysis, and trade-document scrutiny as non-negotiable first-line controls, and reserve EDD and senior-management sign-off for the structural red flags where face-value review will not surface the risk. Where suspicion remains unresolved, the goAML filing obligation is triggered on suspicion, not on certainty.

Related Terms and Concepts

How Entertainment Venture Fronts and Front Companies Are Related

An entertainment venture front is a specific variant of the broader typology of front companies. A front company is any legal entity that presents itself as engaged in legitimate commercial activity while its primary function is to receive or process proceeds of crime. The distinction is the sector-specific mechanism: the inherent difficulty of verifying entertainment revenues against objective benchmarks, and the availability of complex, cross-jurisdictional IP and licensing structures that provide a plausible commercial explanation for large cross-border flows.

Where a generic front company might use any business type as its cover, an entertainment venture front specifically exploits the compliance challenge of assessing whether ticket sales figures, royalty payment rates, and production budgets are commercially plausible. Detection requires sector-specific expertise that generic front company controls do not always deliver.

| Term | Connection |

| Front Company | Parent typology; entertainment venture fronts are a sector-specific variant of the front company mechanism |

| Shell Companies | Corporate vehicles used within the ownership structure of entertainment fronts to obscure beneficial ownership |

| Shelf Companies | Pre-incorporated entities sometimes acquired to give entertainment fronts the appearance of established trading history |

| Fictitious Consulting Firm | Sibling typology; same fictitious revenue mechanism applied to the consulting sector |

| Fictitious Jewellery Business | Sibling typology; same integration-stage mechanism applied to the jewellery and precious metals sector |

| Invoice Manipulation | Core technique used by entertainment fronts to document fabricated revenues through structured invoice chains |

| Intellectual Property (IP) Rights | Key instrument in entertainment front layering; royalty and licensing payment flows are a primary channel for cross-border fund movement |

| Multi-Jurisdiction Corporate Structures | Structural enabler; entertainment fronts typically rely on multi-layer cross-border ownership to obscure the beneficial owner |

| Offshore Company Incorporation | Service exploited to create holding entities that separate the entertainment operating entity from the illicit operator |

| Beneficial Ownership Transparency | Core control that entertainment fronts are designed to defeat; BO verification is the primary detection gate |

Variants, Synonyms, and Instruments

What Financial Instruments Do Criminals Use in Entertainment Venture Fronts and Schemes?

Bank accounts are the primary instrument through which fabricated entertainment revenues are received and processed. The illicit operator maintains multiple business bank accounts across different institutions, using each to receive a portion of the fictitious income. This fragmentation is deliberate. It prevents any single institution from constructing a complete picture of the entity’s total financial flows and reduces the probability that transaction monitoring at any one bank will breach the alert thresholds the operator has assessed.

Cash plays a central role, particularly in the initial phase when criminal proceeds are introduced as ticket sale revenues, venue entrance fees, or event-day merchandise income. Cash receipts are inherently difficult to verify against independent data, and the entertainment sector’s legitimate cash handling creates a plausible commercial context for large cash deposits.

Accounts receivable, in the form of structured invoice chains, provide the documentary evidence that makes fabricated revenues appear commercially grounded. Each invoice is a legal instrument that, if professionally prepared and supported by a corresponding contract, will satisfy standard document-based CDD. The weakness in this instrument is that invoice authenticity can be challenged through trade monitoring and OSINT if the stated counterparty is subjected to independent investigation.

Equity interests in entertainment entities serve the integration function. Once illicit funds have been introduced as commercial revenue and appear in audited financial statements, the operator sells equity in the entity. The sale price reflects the capitalised value of the revenue stream, converting criminal proceeds into investment returns that are formally legitimate.

Intellectual property rights are the most sophisticated instrument in the entertainment front’s toolkit. IP rights held by offshore entities can be assigned, licensed, sub-licensed, and revalued with very limited external visibility. A royalty payment from a UAE entertainment operating entity to an offshore IP rights holder requires a demonstrably legitimate commercial agreement, an IP valuation, and an understanding of the market rate.

| Variant Term | Context or Jurisdiction | Distinction from Entertainment Venture Fronts |

| Entertainment shell company | General / multi-jurisdictional | Emphasises the shell company structure; may lack active event or production activity |

| Front company (entertainment sector) | General AML terminology | Broader label; entertainment venture fronts is the taxonomy-specific sub-term |

| Music label front | Specific to music sector | Limited to music publishing, distribution, and recording |

| Film production front | Specific to film and media | Limited to film and television production; exploits budget inflation and distribution market obscurity |

| Nightclub or venue front | Specific to hospitality/live venue sector | Exploits cash-intensive venue operations; lower complexity but high cash volume |

Virtual Asset and Digital-Content Exposure

Entertainment businesses increasingly receive value through virtual assets, streaming platforms, online fan communities, non-fungible tokens, and tokenised rights. Where payments are received or made in virtual assets, the entity or its service provider may fall within the VASP obligations of CR 134/2025, and the same source-of-funds, ownership, and counterparty checks should be applied to digital-asset flows as to fiat flows.

Products, Services, and Jurisdictional View

What Products and Services Do Criminals Abuse in Entertainment Venture Fronts Schemes?

Accounting, auditing, and bookkeeping services are abused when a professional engaged by the entertainment front prepares or certifies financial statements that reflect fabricated revenues.

The auditor who certifies accounts without independently verifying the underlying commercial activity provides the entertainment front with the highest-quality legitimising credential available. DNFBPs providing these services in the UAE are subject to the full CDD and STR framework under CR 134/2025 and supervised by MOET.

Business bank accounts are the operational backbone of the scheme. Each account receives a portion of the fabricated revenue stream, and the combined picture across accounts presents a financial institution with what appears to be a commercially active entertainment entity generating income consistent with its sector profile.

Cross-border payment services are used to route the layering phase of the scheme. Licensing payments, royalty flows, and production cost advances are transmitted to offshore entities through cross-border payment service providers, exploiting the natural complexity of international entertainment supply chains.

Offshore company incorporation services are used to create the corporate vehicles that hold IP rights, receive royalties, and own equity in the operating entities. Jurisdictions chosen for incorporation are typically those with minimal public disclosure requirements for beneficial ownership.

Payment processing services, including card payment platforms and online ticketing intermediaries, are used to create transaction records that support the ticket sales narrative. Trust and corporate service providers register entities, appoint nominees, and maintain registered offices in multiple jurisdictions, creating and maintaining the corporate vehicles without which the cross-border layering mechanism cannot operate.

UAE Jurisdictional View

The UAE’s entertainment sector has expanded substantially over the 2020-2026 period, driven by the legacy of Expo 2020, increased investment in live events, film production, and sports tournaments, and the development of Dubai and Abu Dhabi as regional hubs for music, culture, and media. This genuine commercial growth creates a fertile environment for entertainment venture fronts.

The UAE legal framework applicable to this typology is comprehensive. FDL 10/2025, effective 14 October 2025, provides the ML criminalisation basis. CR 134/2025, effective 14 December 2025, provides the operative CDD, EDD, STR, and record-keeping obligations for all FIs and DNFBPs. CR 109/2023 requires all UAE-incorporated legal persons to maintain a BO register that must identify natural person beneficial owners to the 25% threshold and update it within 15 days of any change.

DNFBPs engaged by entertainment entities, including accountants, lawyers, TCSPs, and dealers in precious metals and stones, must apply the same risk-based CDD framework that applies to all their client relationships. Where the entertainment entity presents with indicators consistent with this typology, EDD applies, and a relationship that cannot be satisfactorily clarified through EDD must be declined, with an STR filed where suspicion has arisen.

How AML UAE Helps

The compliance challenge posed by entertainment venture fronts is not one that general AML guidance resolves on its own. The sector-specific nature of the revenue verification problem, whether a declared ticket sale figure is commercially plausible for the stated event, whether a royalty rate is consistent with the applicable market, and whether a production budget is reconcilable with the entity’s operational capacity, requires advisory support from practitioners who understand both the regulatory framework and the commercial mechanics of the entertainment sector.

AML UAE provides UAE-registered FIs and DNFBPs with the advisory resources, compliance tools, and training programmes needed to build entertainment sector risk assessment into existing CDD and EDD frameworks. For institutions that are expanding their entertainment sector client portfolios or that have identified potential exposure through existing relationships, AML UAE’s team brings the practical sector knowledge required to assess whether specific indicators warrant escalation, declination, or STR filing.

The goAML registration and filing process, which governs all STR obligations under FDL 10/2025 Article 18, is one of the most operationally critical elements of any compliance programme. AML UAE provides dedicated guidance on goAML registration, form completion, and filing protocols to ensure that institutions can meet their reporting obligations without procedural delay.

Frequently Asked Questions

An entertainment venture front is a legal entity that presents itself as operating in the entertainment sector, including live events, music, film, or sports, while its primary or substantial purpose is to receive and process proceeds of crime as fabricated commercial revenues. The entity uses the inherent difficulty of verifying entertainment income to conceal the illicit origin of the funds it processes. Under FDL 10/2025 Article 2, processing funds known to be criminal proceeds constitutes money laundering.

Illicit operators introduce criminal proceeds as ticket sales, sponsorship income, licensing fees, or production advances, then record these amounts as commercial revenues in financial statements. The funds are then layered through cross-border payments to offshore IP rights holders or affiliated entities, before being integrated into the legitimate economy through equity sales, property acquisition, or reinvestment. Each stage uses genuine commercial instruments to make the flow appear legitimate.

The most operationally significant red flags are: reported revenues that cannot be reconciled with independently verifiable data on event scale or market rates; sponsorship or licensing income from entities that have no identifiable operating history; multiple affiliated corporate vehicles with opaque beneficial ownership; cash deposits that are regular rather than event-driven; and cross-border payments to jurisdictions with no apparent role in the declared entertainment supply chain.

Under CR 134/2025 Articles 6-10, obliged entities must verify the identity of the entertainment entity, identify and verify all natural person beneficial owners to the 25% threshold, understand the nature and purpose of the relationship, and perform ongoing monitoring throughout the relationship. Where the entity presents higher-risk indicators, obliged entities should apply enhanced measures proportionate to the risk under CR 134/2025 Article 5, including source-of-funds, source-of-wealth, ownership, counterparty, and transaction-purpose checks. Where PEP exposure is present, CR 134/2025 Article 16 applies, including senior management approval.

IP rights, including music publishing rights, film distribution licences, and sports broadcasting rights, can be transferred between affiliated entities at values with no relationship to independent market assessments. Royalty payments made under IP licensing agreements create apparently legitimate cross-border flows. Because IP valuation is inherently subjective and market rates for specific catalogues are not publicly disclosed, the mechanism is difficult to challenge through standard document-based CDD.

A legitimate entertainment business generates revenues from genuine commercial activity that can be independently verified against public data, event records, audience attendance, and market benchmarks. An entertainment venture front reports revenues that significantly exceed what any independent verification would support, uses corporate structures that prevent identification of the true beneficial owner, and relies on counterparties that cannot be independently confirmed as genuine commercial operators.

There is no single sector-specific AML regulator for the entertainment industry in the UAE. FIs providing banking and payment services to entertainment entities are supervised by the CBUAE. DNFBPs, including accountants, lawyers, and TCSPs engaged by entertainment entities, are supervised by MOET for those operating under mainland licences, and by the MoJ for legal professionals.

Transaction monitoring rules for entertainment sector accounts should account for the event-driven nature of legitimate revenue, which means peaks around announced events rather than regular periodic deposits. Rules should flag regular cash deposits inconsistent with an event-driven model; cross-border payments to jurisdictions with no documented role in the client’s supply chain; and payment frequencies or amounts to IP rights holders that exceed commercially plausible royalty benchmarks.

Yes. Under FDL 10/2025 Articles 11 and 18, all STRs must be filed with the UAE FIU exclusively through the goAML platform, regardless of the sector or transaction type that generated the suspicion. This obligation applies to all FIs and DNFBPs subject to the UAE AML/CFT framework. Filing must occur without delay from the point at which suspicion arises.

Closing Summary

Entertainment venture fronts represent one of the more sophisticated typologies in the integration stage of the money laundering cycle. Their effectiveness depends not on technological complexity but on the structural difficulty of verifying entertainment revenues against objective benchmarks. A compliance team that applies standard CDD processes to an entertainment entity without incorporating sector-specific revenue verification will, in a significant proportion of cases, fail to identify the indicators that make the structure a laundering vehicle rather than a commercial business.

The UAE’s updated AML/CFT framework under FDL 10/2025 and CR 134/2025 provides a clear and enforceable legal foundation for the enhanced scrutiny that entertainment sector relationships require. The obligations to identify beneficial owners to the 25% threshold, to apply EDD for higher-risk relationships, and to file STRs without delay are not optional elements of a compliance programme; they are statutory requirements with material criminal and administrative consequences for entities that fail to meet them.

If your institution has entertainment sector client relationships that have not been reviewed under the current FDL 10/2025 and CR 134/2025 framework, or if your CDD and transaction monitoring processes do not include sector-specific calibrations for the entertainment industry, the time to address those gaps is now. AML UAE is available to support the assessment, remediation, and ongoing monitoring processes your institution needs to manage this risk within the law.

Need Help Reviewing Entertainment Sector Clients?

Strengthen your CDD and EDD processes to identify hidden beneficial owners and suspicious entertainment-sector transactions.

Share via :

About the Author

Pathik Shah

FCA, CAMS, CISA, CS, DISA (ICAI), FAFP (ICAI)

Pathik is an ACAMS-certified AML consultant specialising in governance, risk, and compliance for regulated entities in the UAE. He brings over 28 years of experience, with 1,000+ hours of AML training and 200+ advisory engagements across DNFBPs, VASPs, and FIs. He supports businesses in aligning with AML/CFT requirements from the CBUAE, DFSA, MoET, MoJ, VARA, CMA, FSRA, and FATF. Known for translating complex regulations into audit-ready procedures, Pathik enables operational clarity and compliance readiness.

Reach Out to Pathik