Micro-Structuring

Last Updated: 05/29/2026

Protect your business with reliable and effective AML strategies with AML UAE.

Micro-Structuring - Key Highlights

Micro-structuring fragments criminal funds into very small transactions, each individually unremarkable, to defeat monitoring systems calibrated to larger thresholds.

Money mules, organised crime groups, and virtual asset users operate across ATMs, digital wallets, and P2P platforms, often using micro-structuring techniques.

Compliance teams require to apply aggregate transaction monitoring to detect cumulative placement patterns such as micro-structuring invisible at the individual transaction level.

What is Micro-Structuring?

Micro-structuring is a variant of the structuring typology in which criminal proceeds are fragmented into extremely small individual transactions, each individually designed to remain not merely below standard reporting thresholds but well below the level at which any individual transaction would attract compliance review. Where standard structuring keeps individual transactions just below reporting thresholds, micro-structuring operates in amounts so small that each transaction is entirely consistent with ordinary low-value retail activity or casual personal payments.

The technique exploits the design of transaction monitoring systems that flag individual transactions above defined value limits. A compliance system that generates alerts for transactions approaching AED 55,000 for a DPMS operator, or that monitors individual cash deposits above defined thresholds, will not generate any alert for a series of deposits of AED 200, AED 150, or AED 500. The criminal activity is not in any single transaction; it is in the pattern of transactions aggregated over time.

Regulatory Framework Related to Micro-Structuring

Federal Decree Law No. (10) of 2025 on Anti-Money Laundering, Combating the Financing of Terrorism and Illegal Organisations governs this typology. Article 2 criminalises money laundering where a person knows or has sufficient indication that funds are proceeds of a predicate offence, covering conversion, transfer, concealment, acquisition, possession and use of such proceeds, and confirms that money laundering is an independent offence.

Article 8 of Cabinet Resolution No. (134) of 2025 requires ongoing monitoring of the business relationship, including scrutiny of transactions to ensure consistency with the customer profile, activity and risk. This is the direct obligation that aggregate transaction monitoring programmes for micro-structuring must satisfy.

A transaction monitoring system calibrated only to individual transaction values, without aggregate pattern analysis, may fall short of the ongoing monitoring obligations contemplated under Article 19 of Federal Decree-Law No. (10) of 2025.

Article 17 of Cabinet Resolution No. (134) of 2025 requires Financial Institutions, DNFBPs and VASPs to establish and continuously update indicators for identifying suspicious transactions when assessing whether to file a STR report, including unusual transaction patterns or activity inconsistent with a customer’s profile.

Supervisory Authorities in UAE

The Ministry of Economy and Tourism (MOET) supervises DNFBPs such as real estate agents, DPMS, TCSPs, and accountants, which may be exploited by criminals through micro-structuring activities to convert illicit proceeds into legitimate funds. Further, the General Commercial Gaming Regulatory Authority (GCGRA) supervises commercial gaming operators, the Capital Markets Authority (CMA) supervises capital markets and securities, and the VARA supervises the VASPs. Cabinet Resolution No. (134) of 2025, Article 4 defines virtual asset activities subject to AML obligations, including exchange between virtual assets and fiat currencies, virtual asset transfers, safekeeping or administration, and related financial services. Moreover, the Central Bank of the UAE (CBUAE) supervises licensed financial institutions, including banks, exchange houses, insurance, payment services and money transfer, all of which are primary channels for micro-structuring. The UAEFIU, established under CBUAE, receives all STRs via goAML and analyses aggregate pattern intelligence.

Reporting or Compliance Obligations and Channels

The STR obligation under Article 18 of Federal Decree Law No. (10) of 2025 applies immediately upon suspicion, without any minimum transaction value. A compliance officer who identifies an aggregate pattern of sub-threshold micro-transactions inconsistent with the customer’s profile has grounds for suspicion requiring STR filing via goAML. The obligation is not triggered by any individual micro-transaction; it is triggered by the pattern that the aggregate reveals.

Article 25 of Cabinet Resolution No. (134) of 2025 requires all CDD, transaction, and access records to be retained for five years. For micro-structuring investigations, transaction-level data across a rolling window of months or years is often required to reconstruct the full pattern. Systems that retain only recent transaction data, or that aggregate historical transactions rather than retaining individual records, limit the investigative capability that the retention obligation is designed to support.

Recent Developments, Enforcement Actions, or Supervisory Priorities

The 2021 NAMLCFTC joint guidance highlights the need for effective transaction monitoring systems, indicators, complete monitoring records and prompt suspicious activity reporting. A compliance programme that detects individual large transactions but has no mechanism for identifying cumulative small-transaction patterns is exhibiting the type of passive compliance the guidance identifies as insufficient.

The FATF has consistently identified micro-structuring as a primary placement-stage technique associated with both traditional cash-based money laundering and with digital asset and P2P platform exploitation. The expansion of digital payment infrastructure in the UAE has created new channels for micro-structuring operations that traditional ATM and bank-deposit-focused monitoring does not fully address.

What Does Micro-Structuring Mean?

Think of it this way. A suspicious large cash deposit of AED 50,000 generates an alert. Fifty deposits of AED 1,000 over two weeks generate no individual alert, but move the same total amount. Now imagine a hundred different accounts, each receiving ten deposits of AED 500 over a month. The same AED 50,000 has moved. No individual transaction exceeded AED 1,000. The crime is invisible at the transaction level, but obvious at the aggregate level, if anyone is looking across all the accounts and all the time periods simultaneously.

Why Micro-Structuring Matters

Micro-structuring matters because it is the placement technique specifically designed to defeat the most common form of transaction monitoring: the threshold-based alert. Most financial institutions configure monitoring rules to flag transactions above defined values or approaching reporting thresholds. Micro-structuring operates deliberately below these values, relying on the monitoring system’s inability to aggregate dispersed sub-threshold activity into a coherent picture.

The UAE’s digital payment infrastructure amplifies the exposure. P2P payment systems, digital wallets, online payment platforms, and peer-to-peer cryptocurrency platforms all enable high-frequency low-value transactions at scale, with minimal friction. An organised crime group that deploys a network of money mules, each processing dozens of micro-transactions per day across multiple platforms, can move substantial criminal proceeds through the formal financial system without any individual transaction generating an alert.

The internal risk dimension of this typology is also significant. Financial institution staff who facilitate micro-structuring, whether wittingly or through systematic failure to apply aggregate monitoring, create compliance exposure for the institution. For DNFBPs subject to MoET supervision, Cabinet Resolution No. (71) of 2024 provides an administrative penalty of AED 100,000 to AED 500,000 for failure to promptly submit suspicious transaction reports or related information to the FIU. For institutions supervised by the CBUAE, equivalent penalty frameworks apply.

How Criminals Use Micro-Structuring to Evade Detection

Micro-structuring is an operational process that requires advanced planning, network coordination, and awareness of the specific monitoring thresholds of target institutions.

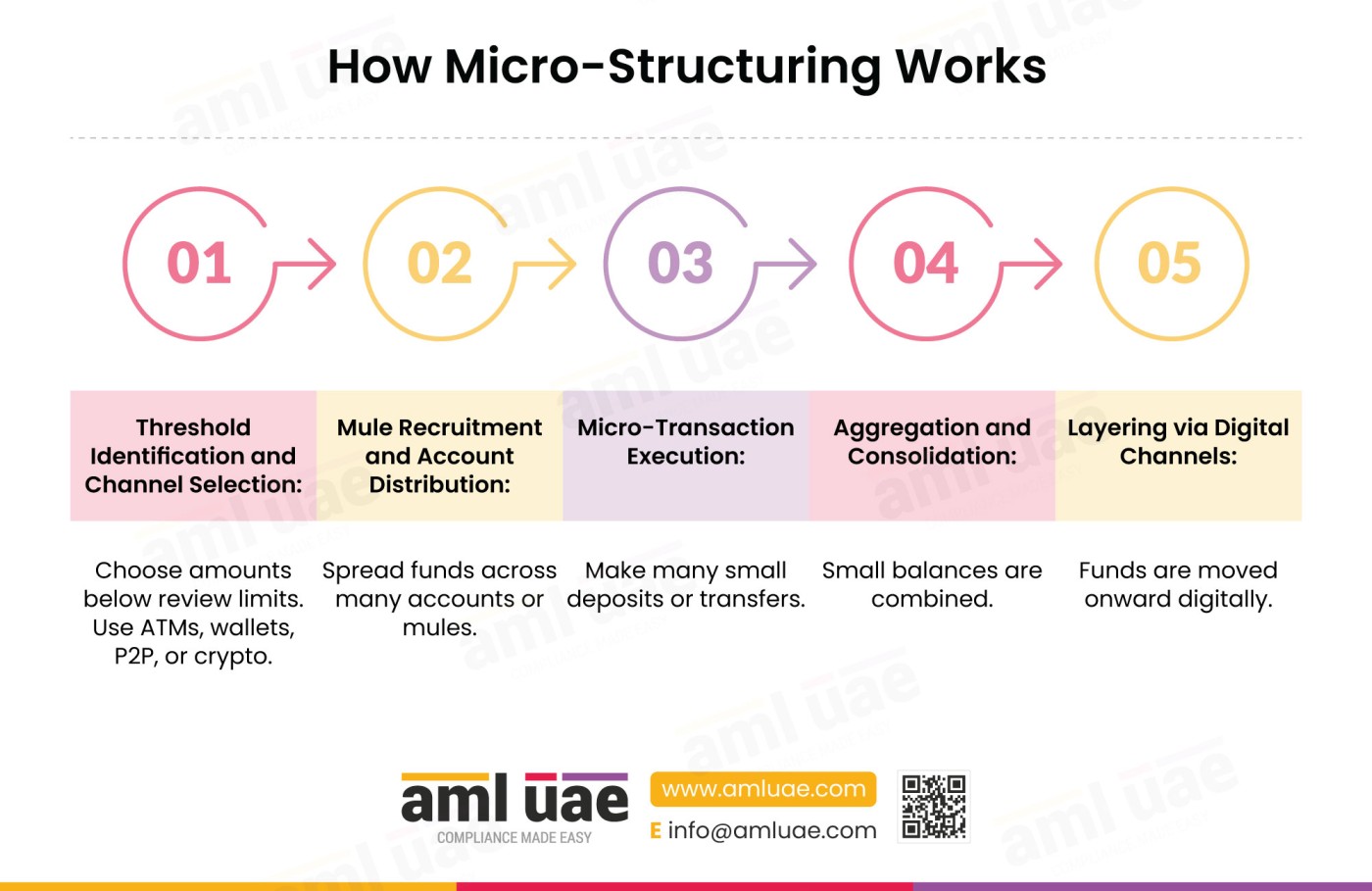

Stage One: Threshold Identification and Channel Selection

The organiser, typically a money mule herder or organised crime group, identifies the monitoring thresholds applied by the target financial institutions. This knowledge may be acquired through operational testing, through intelligence from complicit staff, or simply by observing which transactions generate compliance contact. The organiser selects a micro-amount sufficiently below the lowest relevant threshold to ensure no individual transaction attracts review.

Target channels are selected based on their ability to process high-frequency small-value transactions with minimal friction. ATMs that accept cash deposits without a human teller provide operational anonymity. Digital wallets and P2P payment systems process micro-amounts instantly and remotely. Cryptocurrency P2P platforms allow micro-purchases across multiple counterparties without centralised monitoring.

Stage Two: Mule Recruitment and Account Distribution

The money mule herder recruits a network of money mules, each of whom provides access to bank accounts, digital wallets, or cryptocurrency exchanges. Mules are recruited through employment fraud, social engineering, or direct criminal involvement. Each mule is assigned a specific set of accounts and instructions for the amount and frequency of transactions.

The distribution of transactions across multiple mules and multiple accounts is the operational feature that defeats per-account monitoring. An account receiving fifty deposits of AED 500 over thirty days is showing a pattern. The same total, spread across ten accounts each receiving five deposits, may not trigger an alert on any individual account.

Stage Three: Micro-Transaction Execution

The criminal funds are introduced into the financial system through the mule network. Cash is deposited at ATMs or branch counters in micro-amounts. Digital wallet loads are made using prepaid cards or bank transfers in micro-amounts. Cryptocurrency is purchased in small denominations across multiple P2P counterparties.

Each individual micro-transaction is recorded in the institution’s transaction log. The transaction log contains evidence of the scheme; the failure is the absence of aggregate analysis across the log’s full data set.

Stage Four: Aggregation and Consolidation

After the micro-transactions have accumulated in the mule accounts, the organiser instructs the mules to consolidate the funds. Small balances are transferred to intermediate accounts before being forwarded to the organiser’s destination. The individual transfer from a mule account may itself be small, or may represent a consolidation of accumulated micro-deposits that now represent a single transaction of note.

Stage Five: Layering via Digital Channels

The consolidated funds are moved through additional layering transactions. Cryptocurrency purchased through micro-transactions across P2P platforms is converted to privacy coins or transferred to multiple wallets. Digital wallet balances are transferred to money service businesses for onward remittance. The placement is complete; the layering and integration stages follow.

Real-World Examples of Micro-Structuring

The ATM Distribution Network

An organised crime group recruited a network of 28 money mules and distributed criminal proceeds among them as cash. Each mule was instructed to make daily cash deposits at ATMs in amounts between AED 400 and AED 800 across two different banks.

Over six weeks, the network deposited a total of approximately AED 2.3 million in 4,100 individual transactions, none of which individually exceeded AED 1,000. The scheme was identified when a bank’s quarterly transaction aggregation review flagged multiple accounts with an unusual frequency of sub-threshold cash deposits from ATM channels.

Cross-account analysis identified the pattern of shared ATM usage locations. The operational lesson is that ATM deposit frequency analysis, applied across all accounts using the same ATM infrastructure, reveals network-level micro-structuring patterns invisible at the individual account level.

The Digital Wallet Micro-Deposit Scheme

A money service business in a high-traffic commercial area was identified as the source of thousands of digital wallet load transactions, each between AED 100 and AED 500, across 47 different customer accounts. The loads occurred in rapid succession over several-hour windows, typically in the early evening.

Each individual account showed a plausible pattern of low-value wallet activity when reviewed in isolation. An automated aggregate analysis of loads from the same MSB within tight time windows identified that the aggregate daily loading volume was significantly inconsistent with the MSB’s declared customer base and transaction profile.

An STR was filed. The lesson is that point-of-entry aggregate monitoring, applied at the MSB level rather than the individual account level, is the detection layer that identifies coordinated micro-loading operations.

The Money Mule Multi-Account P2P Operation

A peer-to-peer cryptocurrency trading platform identified a pattern through its VASP reporting obligations: sixteen different user accounts had each conducted between 30 and 60 small cryptocurrency purchases over a three-week period, with each purchase below the platform’s standard monitoring threshold.

The accounts were registered in different names but shared common device fingerprints and IP access patterns. Cross-account analysis identified that the aggregate purchases across the sixteen accounts had totalled the equivalent of AED 1.8 million in cryptocurrency. Each account individually appeared to be a normal, low-volume retail cryptocurrency buyer. The shared device and IP evidence confirmed coordinated control.

The lesson is that cross-account device and IP correlation, applied as a standing monitoring procedure, identifies money mule network micro-structuring on cryptocurrency platforms that per-account value monitoring cannot detect.

What Are the Red Flags That Identify Micro-Structuring?

| Category | Red Flag |

| Customer | Customer profile, stated income, and transaction history are inconsistent with the frequency and aggregate volume of micro-transactions observed over the monitoring window |

| Customer | Multiple depositors or payors from diverse locations repeatedly sending micro-amounts into a single account within a short period |

| Customer | Newly established account immediately exhibiting high-frequency micro-transaction activity inconsistent with the onboarding profile |

| Transaction | High frequency of micro-transactions that, when aggregated over a short period, reveal substantial fund movements despite remaining individually unremarkable |

| Transaction | Pattern of regularly recurring deposits, transfers, or withdrawals in micro-amounts that each individually remain below monitoring thresholds |

| Transaction | Sudden or unusual surge in small, frequent transactions that deviates significantly from the customer’s typical activity baseline |

| Transaction | Frequent micro-transactions channelled through multiple digital wallets or platforms, collectively moving amounts inconsistent with the customer’s stated financial profile |

| Transaction | Repeated micro-transactions lacking a verifiable business or personal justification, inconsistent with the account’s stated purpose |

| ATM | Frequent small ATM withdrawals or deposits across multiple institutions or foreign ATMs over a short period, consistent with layering after micro-placement |

| Crypto | High frequency of micro-cryptocurrency purchases across multiple P2P counterparties below the platform’s standard monitoring threshold |

| Internal | Staff member consistently processing high volumes of small transactions without applying aggregate pattern review or escalating anomalies |

Which AML Controls Counter Micro-Structuring?

Article 21 of Cabinet Resolution No. (134) of 2025 requires Senior Management-approved internal AML/CFT policies, controls and procedures; designation of a compliance officer; staff training on AML/CFT obligations; screening of officers and employees; and an independent audit function to assess programme effectiveness. Each of the controls described below should be embedded in documented internal policies and procedures that satisfy this obligation.

| Control | What It Disrupts | Detect / Prevent / Deter | Specific Limitation |

| Transaction Monitoring with Aggregate Rules | Cumulative micro-transaction patterns invisible at individual transaction level | Detects | Requires purpose-built aggregate rules that sum transaction volumes across defined time windows; standard value-threshold rules alone are insufficient |

| Velocity Monitoring | High-frequency transaction patterns across short time periods | Detects | Must be calibrated to normal customer transaction frequency; poorly calibrated velocity rules generate excessive false positives |

| Cross-Account Aggregation Analysis | Mule network distribution across multiple accounts at the same institution | Detects | Requires compliance systems to correlate transactions across accounts linked by common beneficial owner, device, or IP; per-account monitoring alone misses this |

| Staff AML Training | Teller and front-line staff failure to recognise micro-structuring patterns at the deposit counter or digital channel | Deters | Requires specific micro-structuring awareness training; generic AML training is insufficient |

| Service Restriction | Channels repeatedly exploited for micro-structuring at identified customer accounts | Prevents | Must be applied based on pattern evidence, not individual transactions; premature restriction generates false positive barriers |

| Ongoing Due Diligence | Evolving micro-structuring patterns that emerge over months of account activity | Detects | Requires periodic review of transaction patterns against customer profile baseline; reactive monitoring misses slow-build schemes |

| Risk-Based Customer Profiling | Accounts whose aggregate transaction patterns are inconsistent with their stated profile | Detects | Effectiveness depends on the accuracy of the original profile and the regularity of baseline updates |

| Blockchain Monitoring | Micro-cryptocurrency purchase patterns on VASP platforms and P2P exchanges | Detects | Requires VASP data integration; effective only where on-chain and off-chain data are combined |

| STR Filing on Pattern Suspicion | Detected micro-structuring patterns before funds complete placement | Detects | FDL 10/2025 Art. 18 triggers on aggregate pattern suspicion without minimum value threshold |

How Do AI and RegTech Automate Detection of Micro-Structuring?

The defining characteristic of micro-structuring, the deliberate fragmentation of activity into individually unremarkable units that only become significant in aggregate, is precisely the type of pattern that machine learning detection systems identify most effectively.

Velocity and aggregation analytics are the foundational automated detection layer. Machine learning models applied to transaction logs compute rolling window sums across defined periods, specifically AED aggregations over 24 hours, 7 days, and 30 days, for each customer. When the rolling aggregate for a customer whose profile would not support that level of activity crosses a statistically anomalous threshold, the model generates an alert. This is operationally distinct from standard threshold monitoring because the alert is triggered by the aggregate, not by any individual transaction.

Network graph analytics identify the mule network structure by mapping the connections between accounts sharing common funding sources, device fingerprints, or IP access patterns. A graph analysis that identifies 16 accounts receiving micro-funds from the same source, or 28 accounts using the same ATM infrastructure, reveals the coordinated network at a scale that per-account analysis cannot achieve.

Behavioural baseline deviation models track each customer’s normal transaction frequency and average transaction size over a historical period. When a customer begins exhibiting a micro-structuring pattern, the deviation from their established baseline generates a specific alert that requires compliance review. These models are effective at identifying the transition from normal account behaviour to mule network activity.

Cross-institution intelligence platforms, where regulatory frameworks permit, allow the UAEFIU and participating institutions to share intelligence about micro-structuring networks identified at one institution that may be operating across multiple institutions simultaneously. The full network pattern is often visible only in aggregate across institutions; individual institution monitoring sees only a fraction of the complete scheme.

What Data Should Compliance Teams Collect to Detect Micro-Structuring?

| Data Point | Source System | What It Reveals |

| Rolling aggregate transaction volume per account over 24-hour, 7-day, and 30-day windows | Transaction logs / account activity logs | Whether cumulative low-value transactions are aggregating to amounts inconsistent with the customer’s profile |

| Transaction frequency per account per time period | Transaction logs | Whether transaction frequency spikes in a pattern inconsistent with normal account behaviour |

| ATM usage data including machine ID and geographic location per deposit | ATM usage and geolocation data | Whether the same customer or group of customers is using the same ATM network in a pattern consistent with organised cash placement |

| Device fingerprint and IP access per transaction initiation event | Online and digital payment platform data | Whether multiple accounts are being accessed from the same device or IP, indicating coordinated mule network operations |

| Cryptocurrency micro-purchase history and on-chain destination wallet data | Blockchain and cryptocurrency data / VASP data | Whether micro-purchases are being consolidated at destination wallets, revealing the aggregation step following placement |

| KYC profile versus observed transaction aggregate | KYC records / transaction logs | Whether the customer’s declared income, occupation, and stated account purpose can explain the observed aggregate transaction volume |

| P2P payment counterparty distribution | P2P cryptocurrency and payment platform data | Whether the same counterparties are being used across a network of accounts in a pattern suggesting coordinated micro-structuring |

| Geographical transaction data for dispersed multi-location activity | Geographical transaction data | Whether transactions are being distributed across multiple geographic locations in a pattern consistent with organised mule network deployment |

How Does Micro-Structuring Aggravate Channel Risk and Internal Risk?

Channel Risk is elevated by micro-structuring because the high-frequency, low-value nature of the transactions exploits channels specifically designed for legitimate low-value payment activity. ATMs are designed for convenient small-value cash access; their design creates no friction for small cash deposits. Digital wallets and P2P platforms are designed for fast, low-cost micro-payments. Each channel’s design features that make it valuable for legitimate users are precisely the features that make it useful for micro-structuring. The channel risk assessment must account for the aggregate volume capacity of these channels, not only their individual transaction risk profile.

Internal Risk is elevated because micro-structuring schemes, particularly those involving cash deposits at branch counters, require repeated in-person interactions with financial institution staff. A teller who processes the same customer’s small cash deposits repeatedly without flagging the pattern, or who has been approached by a mule herder and accepts payments for ignoring the pattern, represents the internal risk dimension of this typology.

How Do Compliance Officers Identify Micro-Structuring Patterns?

Compliance officers identify micro-structuring through three detection pathways. The first is the aggregate anomaly: a transaction aggregate report that flags customers whose total transaction volume over a 7-day or 30-day window is inconsistent with their profile, even though no individual transaction approached a threshold. The second is the frequency spike: a velocity monitoring alert for a customer whose transaction frequency has increased sharply in a pattern inconsistent with stated business or personal activity. The third is the cross-account network signal: a graph analytics report identifying accounts sharing common characteristics, such as the same ATM, device, or funding source, suggesting coordinated mule network operation.

Sectors at Highest Exposure

| Sector | Risk Rating | Specific Reasoning |

| Money Transfer and Remittance Services | Critical | Remittance operators process high volumes of small-value transactions structurally suited to micro-structuring; ATM and digital channel access enables rapid high-frequency micro-deposits |

| Banking (ATM and Digital Channels) | Critical | ATMs provide anonymous, friction-free cash deposit capacity; digital banking enables high-frequency small-value transactions at scale |

| P2P Cryptocurrency Platforms | High | P2P platforms enable micro-cryptocurrency purchases without centralised aggregation monitoring; distributed counterparty structure makes network analysis particularly challenging |

| Digital Wallet and Payment Processors | High | Digital wallets accept repeated micro-loads from multiple funding sources; payment processors handle high volumes of small-value transactions that may mask micro-structuring flows |

| Prepaid and Stored-Value Platforms | Moderate | Prepaid cards accept micro-loads from cash and digital sources; the stored value is then usable for further layering without connection to the original micro-load events |

Geographies and Contexts of Concern

The UAE’s high number of money service businesses, ATMs and remittance operators in busy commercial areas creates a system where many small-value transactions can be processed quickly. Areas with large migrant populations and high cash usage naturally see a large flow of small, frequent transactions across these services.

Best Practices for Micro-Structuring Risk Management

- Deploy aggregate transaction monitoring rules across rolling time windows, not only individual transaction thresholds. Configure transaction monitoring to compute rolling 24-hour, 7-day, and 30-day aggregate transaction volumes per customer and compare them against profile-based expected ranges. An aggregate alert threshold for a retail customer should reflect their stated income and account purpose; a spike in aggregate volume that exceeds this baseline requires compliance review regardless of individual transaction values.

- Apply velocity monitoring calibrated to normal customer transaction frequency, not only value. High transaction frequency in small amounts is the defining signature of micro-structuring. Configure velocity rules that flag accounts where transaction frequency in a defined window exceeds the statistically expected rate for the customer’s profile type. Calibrate the frequency threshold against peer-group benchmarks to minimise false positives while ensuring genuine anomalies are detected.

- Conduct cross-account aggregation analysis identifying accounts sharing common funding sources, devices, or ATM usage. Run periodic cross-account analysis that identifies clusters of accounts linked by shared characteristics. A cluster of accounts all receiving micro-amounts from the same source, all using the same ATM, or all accessed from the same device within a short window, provides the network-level evidence of coordinated micro-structuring that per-account monitoring cannot generate.

- Train front-line staff specifically on micro-structuring red flags and aggregation awareness. Tellers and front-line digital channel staff must understand that a customer making daily small cash deposits is not inherently suspicious, but that a pattern of daily small cash deposits from the same customer over three weeks, or from the same set of customers in the same location over three weeks, requires escalation to the compliance officer for aggregate review. Staff training must specifically address the aggregation dimension of this typology.

- File STRs based on aggregate pattern evidence rather than waiting for individual transactions to reach the threshold. Article 18 of Federal Decree Law No. (10) of 2025 requires the detection and reporting of suspicious transactions. An aggregate pattern that is inconsistent with the customer’s profile provides grounds for suspicion even if every individual transaction is a modest amount. The STR filing decision should be based on the pattern, documented with the aggregate data that revealed it.

- Apply blockchain analytics aggregate monitoring to VASP accounts showing micro-purchase patterns. For virtual asset service providers, configure blockchain analytics tools to flag VASP accounts where the aggregate of micro-purchases over defined windows exceeds expected profile values, and where the on-chain destination of aggregated funds is concentrated at a small number of wallet addresses, suggesting consolidation after placement.

- Retain granular transaction-level records for the full five-year period, with full timestamp precision. Article 25 of Cabinet Resolution No. (134) of 2025 requires retention of transaction records, CDD records, ongoing monitoring records, STRs and analysis results for at least five years, and specifies that records must permit reconstruction of individual transactions and data analysis. For micro-structuring investigations, transaction-level records with full timestamp precision should be retained at that granularity. Aggregated or compressed historical data cannot reconstruct the individual transaction pattern required to document the scheme or support an investigation.

- Include aggregate monitoring capability as a specific requirement in the enterprise-wide risk assessment. Cabinet Resolution No. (134) of 2025, Article 5, requires regulated entities to identify, understand, manage and assess crime risks, considering customer, country, product, service, transaction and delivery channel risks. Micro-structuring is a transaction and delivery channel risk that must appear explicitly in the EWRA. An institution that has identified micro-structuring as a risk in its EWRA but has not implemented aggregate transaction monitoring is not meeting its own risk assessment commitments. The EWRA should reference the specific aggregate monitoring capability as the required mitigation and confirm its operational status.

How Micro-Structuring and Structuring Are Related

Micro-structuring is a sub-technique of the Structuring typology. All structuring schemes share the defining characteristic: the deliberate fragmentation of transactions to defeat reporting obligations or monitoring thresholds. Micro-structuring narrows this concept to the smallest available denomination, operating at transaction values so low that the aggregation problem becomes the primary detection challenge rather than the threshold proximity that characterises standard structuring.

The detection methodology differs significantly between the two. Standard structuring monitoring looks for transactions approaching but not exceeding reporting thresholds, a relatively targeted detection problem. Micro-structuring detection requires aggregate pattern analysis across full transaction histories, comparing cumulative volumes against profile-based baselines. An institution that has deployed effective structuring detection for near-threshold transactions may still have a material gap for micro-structuring if its monitoring does not include aggregate analysis across extended time windows.

Related Terms and Concepts

Related Terms

| Term | Connection |

| Structuring | Parent typology: micro-structuring is the extreme low-denomination variant of the structuring technique family |

| Smurfing | Closely related technique: smurfing uses multiple individuals to make sub-threshold deposits; micro-structuring may or may not involve multiple actors |

| Money Mule (actor) | Primary delivery mechanism for coordinated micro-structuring operations using mule networks |

| Placement | The money laundering stage at which micro-structuring operates: introducing criminal proceeds into the financial system |

| Cryptocurrency Mixing | Blockchain-layer technique often deployed after micro-cryptocurrency purchase aggregation to obscure the consolidated on-chain funds |

| Anonymous Networking | Access-layer technique sometimes combined with digital micro-structuring to prevent attribution of the micro-transaction sessions |

Related Processes

| Process | Connection |

| Aggregate Transaction Monitoring | The primary compliance control required to detect micro-structuring; standard threshold-based monitoring is insufficient |

| Velocity Monitoring | Transaction frequency analysis that identifies the high-frequency low-value pattern characteristic of micro-structuring |

| Cross-Account Analysis | The network-level detection procedure required to identify coordinated mule network micro-structuring |

Related Controls

| Control | Connection |

| Transaction Monitoring | Must include aggregate rules to be effective against this typology |

| Staff AML Training | Specific micro-structuring awareness training required for front-line staff at cash and digital channel points |

| Record Retention (5 Years) | Granular transaction-level records required for retrospective aggregate pattern analysis |

What Financial Instruments Do Criminals Use in Micro-Structuring Schemes?

Bank accounts are the primary receiving vehicle for cash-based micro-structuring. Multiple mule accounts at the same institution or across multiple institutions receive the micro-deposits. The individual account balance growth is unremarkable; the aggregated growth across the network is the criminal activity.

Cash is the primary funding instrument for micro-structuring at the ATM and branch counter level. Criminal proceeds in cash are divided into micro-amounts for deposit. The cash source is not attributable to any specific transaction because the micro-denomination disguises its origin in the transaction record.

Cryptocurrencies are used for digital micro-structuring on P2P platforms and VASP accounts. Micro-purchases of public ledger cryptocurrencies across multiple counterparties place criminal value into the blockchain ecosystem in amounts that individually pass standard monitoring thresholds. The consolidated on-chain value is then available for further layering.

Prepaid and stored-value payment instruments are loaded with micro-amounts and used as an intermediate holding vehicle. Micro-loads to prepaid cards from multiple sources, followed by consolidation at a single point of use, replicate the deposit-and-consolidate pattern of cash micro-structuring within the digital stored-value ecosystem.

Variants and Synonyms

| Term | Context or Jurisdiction | Distinction from Primary Term |

| Sub-threshold structuring | Compliance and legal contexts | General term for any transaction structuring below reporting thresholds; micro-structuring emphasises the very small denomination specifically |

| Micro-smurfing | Informal and media contexts | Combines micro-structuring with the smurfing multiple-actor model; not a formal regulatory designation |

| Chip and pin structuring | Digital payment contexts | Informal term for micro-structuring through stored-value and contactless payment systems |

| Digital micro-placement | Academic and FATF contexts | Academic term for digital channel micro-structuring; emphasises the placement stage context |

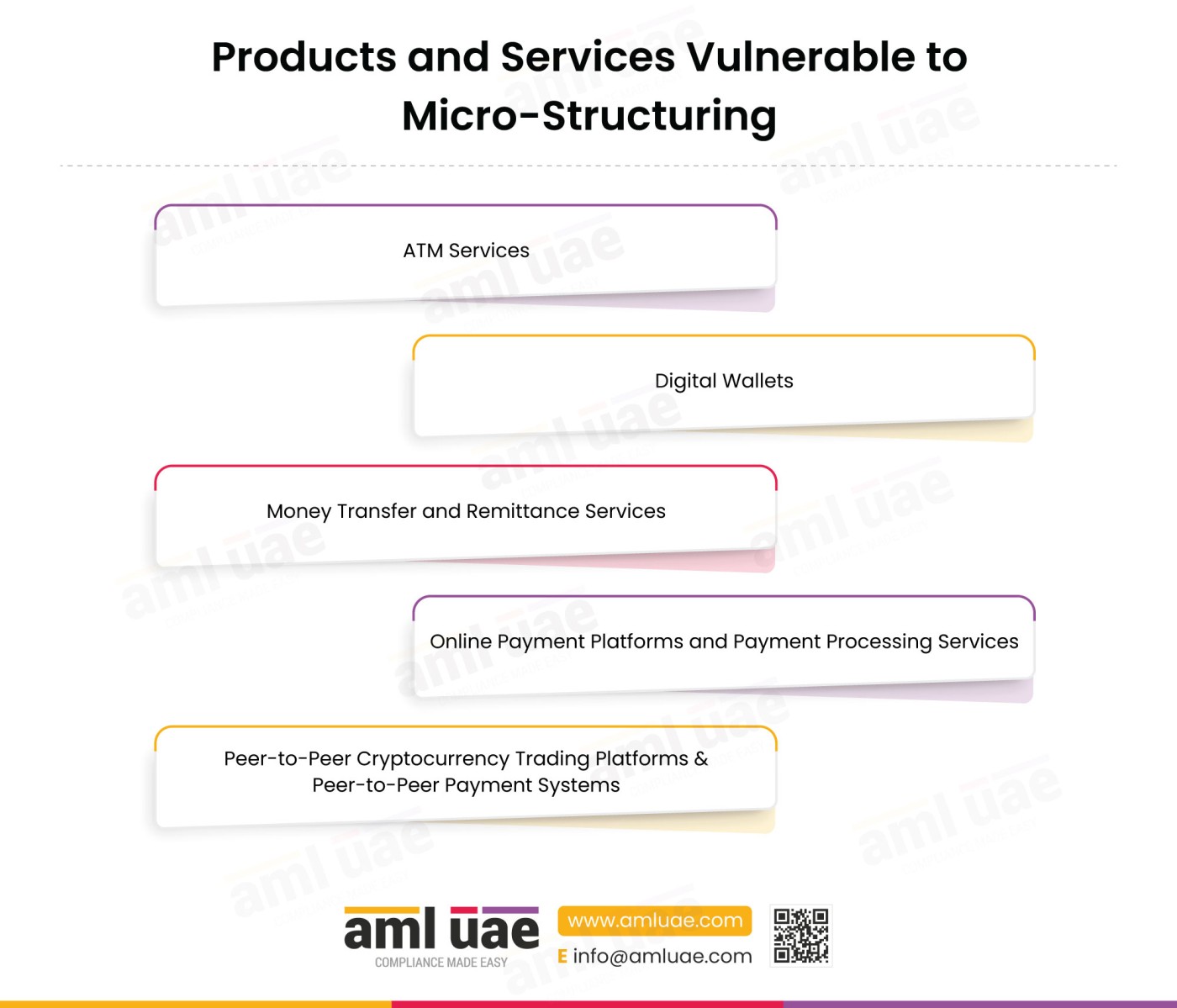

What Products and Services Do Criminals Abuse in Micro-Structuring Schemes?

ATM services are abused as the primary cash placement channel for micro-structuring. Automated teller machines that accept cash deposits, including deposit-enabled ATMs operated by multiple institutions, provide a friction-free, geographically distributed infrastructure for micro-cash placement. A mule network can deploy individuals across multiple ATMs simultaneously, making the aggregate pattern visible only to institutions with cross-ATM network analytics.

Digital wallets are abused as the digital equivalent of mule bank accounts. Micro-loads to digital wallets from multiple funding sources, including cash ATM top-ups, bank transfers, and P2P payments, accumulate criminal proceeds in a form that is portable and immediately usable for further layering. The load event is the micro-structuring placement; the wallet balance is the aggregated proceeds.

Money transfer and remittance services are abused both as funding sources for micro-deposits and as destination channels for consolidated funds. A remittance operator that processes many small-value incoming transfers to a single beneficiary, or that sends many small-value outgoing remittances from a network of customers in rapid succession, may be operating as a micro-structuring channel without adequate aggregate monitoring.

Online payment platforms and payment processing services are abused for digital micro-payments between mule accounts and consolidation points. The combination of high transaction volume capacity, low per-transaction friction, and limited real-time aggregate monitoring makes digital payment platforms structurally suited to micro-structuring operations at scale.

Peer-to-peer cryptocurrency trading platforms and peer-to-peer payment systems are abused for micro-purchase and micro-transfer operations in both fiat and digital asset formats. The distributed counterparty model of P2P platforms means that the aggregate of a mule network’s activity is distributed across many counterparties and may not be visible to any single counterparty or to the platform operator without network-level analytics.

How AML UAE Helps Manage Micro-Structuring Risks

The micro-structuring typology presents a compliance challenge that is fundamentally an analytics problem: detecting patterns that are invisible at the individual transaction level but clear at the aggregate level. Financial institutions and payment service providers in the UAE that have effective per-transaction monitoring but have not deployed aggregate rolling-window analysis have a material detection gap that micro-structuring schemes specifically exploit.

AML UAE provides compliance guidance calibrated to the specific aggregate monitoring requirement of micro-structuring detection, including the configuration of rolling-window aggregate rules, velocity monitoring thresholds, and cross-account network analysis procedures. AML UAE further supports the fulfilment of staff training requirements specific to front-line micro-structuring recognition and the STR assessment process for aggregate pattern suspicion.

For institutions building or reviewing their transaction monitoring frameworks, AML UAE supports the development of EWRA entries for micro-structuring that confirm aggregate monitoring capability deployment, and the five-year granular transaction record retention protocols required under Article 25 of Cabinet Resolution No. (134) of 2025.

Closing Summary: Micro-Structuring

Micro-structuring exploits the most common limitation in transaction monitoring infrastructure: the calibration of alert rules to individual transaction values rather than to aggregate patterns. Every regulated entity that processes small-value transactions in volume, and in the UAE’s digital economy, which includes virtually every financial institution, payment processor, remittance operator, and VASP, is structurally exposed to micro-structuring unless it has specifically deployed aggregate rolling-window monitoring.

The regulatory framework under Federal Decree Law No. (10) of 2025 and Cabinet Resolution No. (134) of 2025 provides clear obligations: ongoing monitoring that identifies unusual patterns, including sub-threshold aggregation, STR filing upon suspicion from aggregate evidence without any minimum value, and five-year retention of granular transaction records. The detection gap is not a regulatory uncertainty; it is an implementation question about whether the monitoring infrastructure includes the aggregate analytics layer that the regulations imply.

Institutions that close this gap move from a compliance posture that detects only the unsophisticated structuring schemes to one that can identify the coordinated mule network operations that represent the highest-volume micro-structuring threat.

Micro-structuring is the typology that tests whether an institution actually has aggregate monitoring or just thinks it does. You can have a perfectly tuned threshold alert for anything approaching AED 50,000 and miss a network moving AED 2 million through two hundred accounts in AED 1,000 increments. The question the compliance team needs to answer is not which individual transactions are large, but which customers are accumulating at a rate inconsistent with who they say they are. That is an aggregation question, not a threshold question.

Frequently Asked Questions

Micro-structuring is a placement-stage money laundering technique that fragments criminal proceeds into extremely small individual transactions, each well below monitoring thresholds and individually consistent with normal low-value activity. The criminal activity is not visible at the individual transaction level; it is visible only when transactions are aggregated across time and accounts.

Standard structuring keeps individual transactions just below reporting thresholds, targeting the threshold margin. Micro-structuring operates at denominations so small that individual transactions are entirely unremarkable in any retail context. The detection challenge is different: standard structuring requires threshold-proximity monitoring; micro-structuring requires aggregate rolling-window analysis.

The most reliable red flags are aggregate anomalies: a customer whose cumulative transaction volume over a 7 or 30-day window is inconsistent with their declared profile, or whose transaction frequency has spiked sharply beyond their historical baseline. Cross-account signals, such as multiple accounts receiving micro-amounts from the same source, are a secondary detection layer that identifies coordinated mule network operations.

Primary detection methods include rolling-window aggregate transaction monitoring, comparing cumulative volumes against profile baselines, velocity monitoring flagging unusual transaction frequency, and cross-account analysis identifying shared funding sources, devices, or ATM infrastructure across accounts. Blockchain analytics aggregate monitoring is applied to VASP accounts showing micro-purchase patterns.

Federal Decree Law No. (10) of 2025, Article 2, criminalises the concealment and disguise of the illicit origin of proceeds, treating such conduct as an independent ML offence. Article 18 triggers an STR filing upon suspicion based on aggregate patterns, without a minimum value. Cabinet Resolution No. (134) of 2025, Article 8 requires ongoing monitoring that includes aggregate pattern analysis. Article 25 requires five-year retention of granular transaction records.

Money mules provide the account access and physical presence required for distributed micro-transactions. Mule herders distribute cash or digital value among mules and instruct their transaction execution. The distribution across multiple mules and accounts is the operational feature that defeats per-account monitoring, requiring cross-account analysis to identify the full network.

A 7-day rolling window typically provides the best balance between detection sensitivity and false-positive rate for cash-based micro-structuring. A 30-day window is more appropriate for detecting slower-build schemes. Both windows should be applied simultaneously, with different alert thresholds calibrated to the customer profile type. For cryptocurrency micro-structuring, a 24-hour window is also valuable given the higher transaction velocity of digital platforms.

Build Smarter AML Controls for Micro-Transactions

Get expert guidance on detecting smurfing, structuring, and other transaction-splitting techniques used in money laundering schemes.

Share via :

About the Author

Pathik Shah

FCA, CAMS, CISA, CS, DISA (ICAI), FAFP (ICAI)

Pathik is an ACAMS-certified AML consultant specialising in governance, risk, and compliance for regulated entities in the UAE. He brings over 28 years of experience, with 1,000+ hours of AML training and 200+ advisory engagements across DNFBPs, VASPs, and FIs. He supports businesses in aligning with AML/CFT requirements from the CBUAE, DFSA, MoET, MoJ, VARA, CMA, FSRA, and FATF. Known for translating complex regulations into audit-ready procedures, Pathik enables operational clarity and compliance readiness.

Reach Out to Pathik