Protect your business with reliable and effective AML strategies with AML UAE.

This blog discusses the intricate subject of tipping off in the context of AML Compliance by taking the reader through the topics covering the following:

- What is Tipping Off

- A nuanced analysis of the specific exemption from filing STRs available to professionals like Accountants, Independent Legal Auditors, Lawyers, and Notaries when providing privileged services

- Obligation to file STR by complying with no-tipping-off requirements when performing services or activities coming under the purview of AML/CFT obligations.

- Do’s and Don’ts to avoid tipping off

- Best Practices to avoid tipping off

- Suggestive Checklist to Avoid Tipping- Off Customers While Filing STR With UAE FIU.

What is Tipping Off in AML Compliance?

What Does The Word “Tip-Off” Mean?

The act of informing a person about an upcoming event, information, or any action against them so that they can take precautionary measures or prepare themselves for the consequences of such event, action, or information is known as tipping off.

Tipping Off in the Context of AML Compliance

Before delving into understanding tipping off in the context of AML/CFT and TFS compliance, a rewind or refresh of AML compliance and suspicious transaction reporting (STR) obligations is required. The Federal Decree by Law No. (10) of 2025 on AML/CFT requires the reporting entity (FIs, DFNBPs, or VASPs) to report to the FIU about the suspicious transaction without any delay, while ensuring confidentiality. This confidentiality requirement is two-pronged, requiring reporting entities to ensure confidentiality in two stages:

- Not disclosing the information, contents, and subject matter of the STR to anyone, particularly the customer themselves, except the concerned team members (which include senior management, AML compliance officers, and other compliance team members) or personnel working on the particular case.

- Not disclosing the act of reporting itself, except for the concerned team members, that regulatory reporting measures are being carried out for a particular customer regarding their transaction with the entity.

Any violation of this confidentiality requirement, particularly resulting in the customer being forewarned, informed, or given any hint or disclosure of impending or concluded reporting by the regulated entity to the authorities, is known as tipping off.

In simple words, when a customer is reported to the authorities, the regulated entity must ensure that such customer does not know through any staff member of the regulated entity that they are being or are reported, either intentionally or unintentionally.

Consequences of Tipping Off on Regulated Entities

If the customer gets to know about STR because of a lapse of confidentiality on the part of the regulated entity, then such a lapse would amount to tipping-off (under Article 29(1)). The penalty for this is imprisonment and/or a fine of not less than AED 50,000.

However, if this tipping-off results in the inability of authorities to seize the proceeds, or leads to their destruction or loss of value (the offence falls under Article 29(3)). This triggers a mandatory minimum imprisonment for not less than one year and a fine equal to the value of the proceeds provided that such fine shall not be less than AED 100,000.

Tipping-off compromises the integrity of a regulated entity and can result in reputational damage by raising concerns about the effectiveness of its AML/CFT controls and confidentiality safeguards.

Balancing Act: Navigating Specific Exemption from Regulatory Reporting & STR Confidentiality Obligations For Professionals like Accountants, Independent Legal Auditors, Lawyers, and Notaries

Unlike other DNFBPs, professionals like Accountants, Independent Legal Auditors, Lawyers, and Notaries providing services such as the following:

- Assessment of customer’s legal position

- Defending or representing customers before the court of law or authorities

- Assisting with or providing services such as arbitration or mediation

- Providing legal advice or opinion in the context of legal proceedings

Consulting services for avoiding or commencing legal proceedings or their completion of such services are exempt or waived from the responsibility of reporting and filing an STR with the FIU due to direct invocation of professional secrecy in order to avoid conflict of interest and safeguard the privacy of communications with the client, ensuring that the best interest of the clients is served through the professional services. To put it simply, reporting suspicious transactions is not required if the service rendered by these professionals comes directly under the purview of legal professional privilege.

Nevertheless, activities and services under the scope of AML compliance but outside the purview of direct professional privilege, having any suspicious element (pertaining to ML, TF, and PF) in transactions, must be reported to the UAE FIU without any delay. These activities and services are discussed more at length in further paragraphs. This portion of UAE AML/CFT compliance obligations is drawn in alignment with the Financial Action Task Force (FATF) Recommendation Nos. 20, 21 and 23 for Suspicious Transaction Reporting and Tipping Off.

Caution to be Exercised by Lawyers and Accountants to Prevent Tipping Off While Complying with UAE’s AML/CFT Regulatory Reporting Obligations

By virtue of specific exemption from reporting STRs granted to professionals like Accountants, Independent Legal Auditors, Lawyers, and Notaries, they need not file STR with the UAE FIU, apparently freeing them up from no tipping-off obligations with regard to services impacting the legal standing of the client as described earlier.

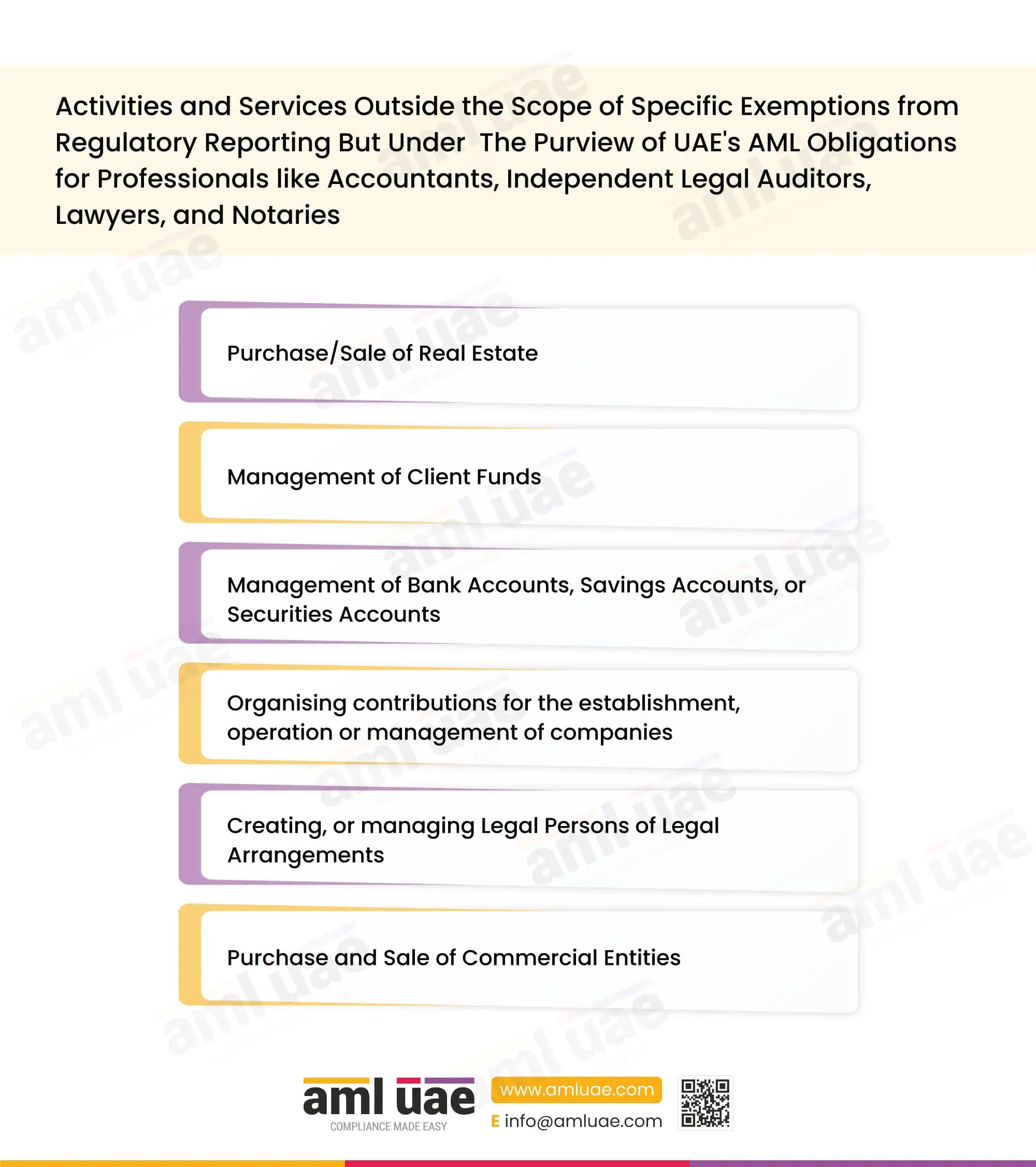

However, the catch exists as professionals like Accountants, Independent Legal Auditors, Lawyers, and Notaries need to file STR if they come across suspicious transactions when their service is outside the scope of the specific exemption, but under the purview of AML obligations. Examples of such services or activities include, but are not limited to, activities and services such as illustrated and enumerated:

- Purchase/Sale of Real Estate

- Management of Client Funds

- Management of Bank Accounts, Savings Accounts, or Securities Accounts

- Organising contributions for the establishment, operation or management of companies

- Creating, or managing Legal Persons of Legal Arrangements

- Purchase and Sale of Commercial Entities

Interestingly, dissuading or advising the client or customers against engaging in any activity or transaction pertaining to ML/TF does not amount to tipping off by professionals like Accountants, Independent Legal Auditors, Lawyers, and Notaries.

Professionals like accountants, independent legal auditors, lawyers, and notaries must exercise caution when formulating AML/CFT policies and procedures. Their AML/CFT Policies and Procedures must be crafted in such a way that the processes for customer due diligence (CDD) for activities within the scope of a specific exemption from reporting and those activities covered under AML/CFT compliance and resultant statutory reporting, such as STR should have distinct workflows, escalations and protocols in place so that there is no under or over-reporting or wrongful or missed reports on part of the accountants, independent legal auditors, lawyers, and notaries. This also helps eliminate the risk of the occurrence of tipping off event as there are distinct services where exempted services do not need reporting and the ones under the scope of AML compliance are reported accurately in the event of suspicious transaction in a timely manner, without the risk of breaching professional secrecy.

How Can All Regulated Entities Prevent Tipping Off

It is important to strike a balance between tipping-off prevention and complying with AML/CFT regulatory reporting obligations. Regulated Entities need to maintain this balance smartly. This section addresses how all Regulated Entities, including professionals like Accountants, Independent Legal Auditors, Lawyers, and Notaries, can prevent tipping off while ensuring compliance with reporting obligations.

The primary recourse available with the regulated entities is to delay the processing or conclusion of the suspicious transaction or the proposed transaction attempted by the subject customer of the SAR/STR.

- Delay Processing of Transaction: Rejecting or terminating the business relationship with the reported customer may tip off the person. Thus, the regulated entities are required to avoid tipping off by delaying the transaction until the entity has received any recommendation, feedback, or additional information request from the Financial Intelligence Unit (FIU).

- Delay Internal Approval Process: The regulated entities can delay the processing of the transaction by informing the customer that it is pending due to the internal approval process, rather than disclosing that the entity is awaiting feedback from FIU or that it is reconsidering the decision to engage with the person on account of observed red flag.

For example, regulated entity may inform the customer that the delay has occurred due to the review of their transaction as part of the internal compliance process, which includes verifying the information and obtaining the necessary internal approval. - Increase Paperwork: The regulated entities can avoid tipping off by informing the customer that the paperwork has been misplaced and needs to be resubmitted. This process may take some time, during which the FIU may respond or provide further guidance around the reported suspicion.

- Demand Additional Information: The regulated entities can ask for additional information or documents like more identification documents or bank documents for verification, thereby delaying the execution of the transaction or trying to create botheration for the customer, which may result in the customer withdrawing from the proposed transaction.

- Any Other Reason: Apart from the above-mentioned reasons, regulated entities can make other excuses, such as the delay being caused by a technical glitch that might take some time to resolve or that the business relationship cannot be continued on account of commercial reasons or that the fees/charges need re-negotiation.

General Do’s and Don’ts to Avoid Tipping-Off

There are certain general Dos and Don’ts that all Regulated Entities can imbibe in their daily operations discussed below:

Do’s to Avoid Tipping Off

- Report Suspicious Transactions Confidentially: Regulated entities are required to report suspicious transactions while maintaining the confidentiality of both the reporting act and the information being reported. This protects the essential purpose STR serves in combating financial crimes.

- Formulation of Proper Protocols and Controls Within AML/CFT Policy and Procedures To Prevent Tipping Off: Regulated entities need to formulate the guiding principles, protocols, and controls regarding the confidentiality of STR within their AML/CFT Policy and Procedures. Moreover, policies should also talk about staff training, which needs to be documented and approved by senior management.

- Training The First Line of Defence to Avoid Tipping Off: The first line of defence are the employees who directly interact with customers. Training them about cases of suspicious transactions, questions they have to ask the customers, and information that should not be disclosed helps minimise the risk of breaching the NO tipping off requirement.

Don’ts to Avoid Tipping Off

- Disclose Customer About Ongoing Investigation: Disclosing information about the ongoing investigation to the customer results in the breach of no tipping-off obligation, resulting in the regulatory fine and/or imprisonment to the employees of the regulated entity and the regulated entity itself. For this, the Company must ensure that customer communication post reporting is handled by the expert compliance team member who understands the tipping-off risk.

- Discuss AML Reports With Anyone: The information about STR should not be discussed with anyone unless such information is necessary for the recipient to discharge their official duties within DNFBPs or its affiliated groups entrusted with the identification and prevention of ML/FT and PF risk.

Join the Fight against Financial Crimes!

Protect your business with reliable and effective

AML strategies with AML UAE.

Best Practices to Avoid Tipping Off a Customer Through Strengthening Internal Controls Within the Regulated Entity

- Establish AML/CFT policies, procedures and controls by identifying the situations that may lead to tipping off and applying the control measures to prevent it.

- Maintain robust security practices, such as an electronic document storage system with strong password protection, to avoid information leakage and access to such confidential information by authorised personnel only.

- Maintain the customer files and documents with digital user verification and password protection to avoid easy access to customer files by unauthorised personnel within the organisation, leaving an audit trail.

- Apply internal controls appropriate for business, such as restricting the sharing of information to only those who have a genuine need to know.

- Balance the obligations of data privacy and protection with the requirement to file STRs involving disclosure of only the necessary information to authorities while ensuring the protection of the customer’s personal data, as discussed in the context of lawyers and accountants.

- When appointing a third party to undertake Customer Due Diligence (CDD) measures, the regulated entity should consider the internal controls deployed by the third party to prevent tipping off.

- Formulate policies that outline the terms and conditions for sharing information with the customers by clearly identifying situations where sharing information could constitute tipping off and specifying the circumstances in which sharing of the specified information is restricted.

- Provide staff training, particularly those in the first line of defence, on how to maintain the confidentiality of STR filings and the necessary steps to avoid tipping off.

- Use legally enforceable agreements when disclosing confidential information to third-party employees.

- Clearly define the penal consequences an employee may face in case of tipping off and communicate the same to all the employees within the organisation.

Suggestions to Avoid Tipping Off

Establishing robust AML compliance procedures requires DNFBPs to have a checklist to avoid tipping off. Any regulated entity’s AML Compliance Officer can refer to the suggestions mentioned below and use them as their checklist to rule out potential breaches of the tipping-off obligations by taking remedial measures.

- Does the person handling the customer communication understand the requirement of “No Tipping Off”?

- Whether any activity, event, or communication took place with the customer, which can be inferred as the AML compliance team has filed or is going to file STR?

- Did any activity, event, or communication take place with the customer informing that the regulated entity received notice from the FIU for additional information?

- Did any activity, event, or communication take place with the customer regarding suspicion of their involvement in ML/FT or PF-related transactions?

- Does the customer-facing team and AML compliance team follow AML/CFT Policies and Procedures in place, having protocols to avoid tipping off?

- Has the transaction processing been delayed with reasonable justification given to the customer or rejected on commercial grounds?

Tipping Off & Robust Regulatory Reporting: A Final Thought

Avoiding tipping off and establishing robust regulatory reporting is essential for complying with the AML/CFT obligations. By establishing clear policies and procedures and conducting proper training, regulated entities can ensure that they meet the regulatory requirements.

We Simplify AML Compliance so You Can

Amplify Your Business

AML UAE provides proactive AML solutions to secure your business from financial crimes

Share via :

About the Author

Pathik Shah

FCA, CAMS, CISA, CS, DISA (ICAI), FAFP (ICAI)

Pathik is an ACAMS-certified AML consultant specialising in governance, risk, and compliance for regulated entities in the UAE. He brings over 28 years of experience, with 1,000+ hours of AML training and 200+ advisory engagements across DNFBPs, VASPs, and FIs. He supports businesses in aligning with AML/CFT requirements from the CBUAE, DFSA, MoET, MoJ, VARA, CMA, FSRA, and FATF. Known for translating complex regulations into audit-ready procedures, Pathik enables operational clarity and compliance readiness.

Reach Out to Pathik