Public WiFi Networks

Published On: 05/21/2026

Protect your business with reliable and effective AML strategies with AML UAE.

Last Reviewed On: 07/27/2026 | Last Updated On: 07/27/2026

Public WiFi Networks - Key Takeaways

Public WiFi networks give criminals a shared, transient IP that cannot be attributed to any individual user, defeating IP-based identity controls without any additional tools. Illicit operators use public hotspots to register accounts, initiate high-value transactions, and coordinate multi-account operations. Where financial institutions and VASPs treat shared-network access as a relevant delivery-channel risk in their own risk assessments, hotspot classification and cross-account session analysis are among the controls that can be calibrated to counter ML/TF/PF risk through this channel.

What are Public WiFi Networks?

Public WiFi Networks refers to the use of shared, unsecured, or semi-secured internet access points in public locations, including airports, hotels, coffee shops, libraries, and shopping centres, to conduct financial transactions or access financial accounts in a manner that defeats individual-level IP attribution.

When a user connects to a public WiFi network, all devices sharing that network present the same IP address to external systems, including the login and session infrastructure of financial institutions and virtual asset service providers.

In an AML context, this shared IP characteristic is deliberately exploited. An illicit operator who initiates a financial transaction, creates a new account, or conducts cryptocurrency trading from a public WiFi hotspot presents an IP address that could belong to dozens or hundreds of concurrent users at the same location. No individual attribution can be made on the basis of the IP alone. This is not a technical evasion tool requiring specialist knowledge; it is an operational technique available to any person with a mobile device and physical access to a public location.

Regulatory Framework Related to Public WiFi Networks

Federal Decree Law No. (10) of 2025 on Anti-Money Laundering, Combating the Financing of Terrorism and Proliferation Financing and its executive regulations under Cabinet Decision No. (134) of 2025 set the AML, CFT and proliferation financing framework that applies to financial institutions, DNFBPs and VASPs in the UAE. Neither instrument addresses public WiFi networks specifically; the framework is technology-neutral, and public hotspot access is treated here as one example of a delivery-channel risk that a regulated entity may bring into its risk assessment.

Three general duties under that framework are particularly relevant when assessing access-channel risk. Article 5 of Cabinet Decision No. (134) of 2025 requires regulated entities to identify and assess the money laundering, terrorism financing and proliferation financing risks they face, including risks arising from delivery channels, and to incorporate those risks into an enterprise-wide risk assessment. Articles 6 to 10 set out the risk-based approach to customer due diligence and require CDD measures calibrated to the actual risk profile of the customer. Article 19 of Federal Decree-Law No. (10) of 2025 makes continuous monitoring a distinct obligation, requiring regulated entities to maintain active, ongoing oversight of customer relationships and risk profiles.

A regulated entity that has identified mobile-first or shared-network access as a material delivery channel for its customer base may reasonably bring consistent public hotspot access into its EWRA, calibrate CDD to that channel, and monitor for the access patterns this typology describes, calibrated to the entity’s own risk profile.

Primary Authority or Supervisory Body

The Central Bank of the UAE (CBUAE) supervises licensed financial institutions, payment service providers, mobile banking operators, and digital banking platforms.

The Virtual Assets Regulatory Authority (VARA), the Financial Services Regulatory Authority (FSRA), and the Dubai Financial Services Authority (DFSA) supervise VASPs in their respective jurisdictions.

The UAE Financial Intelligence Unit (UAE FIU), established under Article 11 of Federal Decree-Law No. (10) of 2025 within the CBUAE, receives all STRs and SARs via the goAML platform.

Reporting or Compliance Obligations and Channels

Article 18 of Federal Decree-Law No. (10) of 2025 requires regulated entities to report suspicious transactions to the UAE FIU without delay through goAML, on the basis of suspicion or reasonable grounds to suspect, and without a minimum transaction value. The statutory suspicion test is fact-based and channel-neutral. Where a regulated entity has identified shared-network access as a relevant delivery channel in its own risk assessment, hotspot-related facts, such as a mismatch between the hotspot location and the customer’s registered address, multiple new account creations from the same hotspot, or high-value transactions from unsecured public networks, are examples of indicators a compliance officer may weigh alongside other information when assessing whether the threshold is met.

The tipping-off prohibition under Article 29 of Federal Decree Law No. (10) of 2025 applies in all circumstances. A compliance officer who escalates a hotspot-access-based suspicion must not disclose to the customer that their access patterns are under review.

Article 25 of Cabinet Decision No. (134) of 2025 sets a general five-year record-keeping duty across customer, transaction and supporting records. The provision does not prescribe particular data fields. Where a regulated entity has incorporated digital access channels into its risk framework, access-related metadata, such as IP logs, device fingerprints, session metadata, and geographic transaction data, may form part of the records retained to evidence ongoing monitoring. Separately, as an operational matter, the ability to cross-reference a hotspot IP against public hotspot location databases is useful for public WiFi investigations.

Recent Developments, Enforcement Actions, or Supervisory Priorities

The growth of mobile-first financial services in the UAE, particularly mobile banking platforms, peer-to-peer payment systems, and virtual asset exchanges with mobile applications, has expanded the surface area for public WiFi exploitation. Customers who access these platforms predominantly on mobile devices are more likely to be on shared networks, such as public WiFi, than desktop users with fixed IP addresses.

The NAMLCFTC Joint Guidance on Satisfactory/Unsatisfactory Practices, issued June 2021, identifies the failure to apply adequate CDD when a customer’s behaviour is inconsistent with their declared profile as an example of unsatisfactory practice. A customer whose account access consistently originates from public hotspots in locations inconsistent with their registered address and stated occupation presents exactly this type of inconsistency.

What Do Public WiFi Networks Mean?

Imagine a room with thirty people in it, all of whom have their letters delivered to the same building address. If one of those people sends a suspicious letter, the postal authority can see it came from that building, but cannot determine which of the thirty people sent it. Public WiFi works the same way. The hotspot at a coffee shop has one IP address; every customer using it presents that same IP to any online service. A bank or exchange that sees a transaction from that IP cannot tell which customer was responsible based on the IP alone. The criminal uses this shared address as a shield against individual attribution.

Why Public WiFi Networks Matter

Public WiFi exploitation matters in an AML context because it requires no technical capability whatsoever. Every other sub-technique in the anonymous networking category, VPNs, Tor, proxy servers, requires at a minimum the installation and configuration of a tool. Using public WiFi requires only a mobile device and the decision to sit in a coffee shop. This accessibility means the technique is available to the full population of potential illicit operators rather than to a technically capable subset.

The scale of public WiFi infrastructure in the UAE, including international airports with extremely high transaction volumes, hotel networks, and commercial district hotspots, creates a large attack surface. Any financial platform that processes transactions from these IPs without cross-referencing the hotspot geography against the customer’s stated profile is accepting an attribution gap at every such transaction. The volume of legitimate transactions from public networks means that flagging all public WiFi access is not operationally practical; the detection challenge is identifying the risk-relevant subset through contextual analysis.

How Public WiFi Networks Work

Public WiFi exploitation in financial crime follows consistent operational patterns, each of which exploits a different aspect of the shared IP attribution problem.

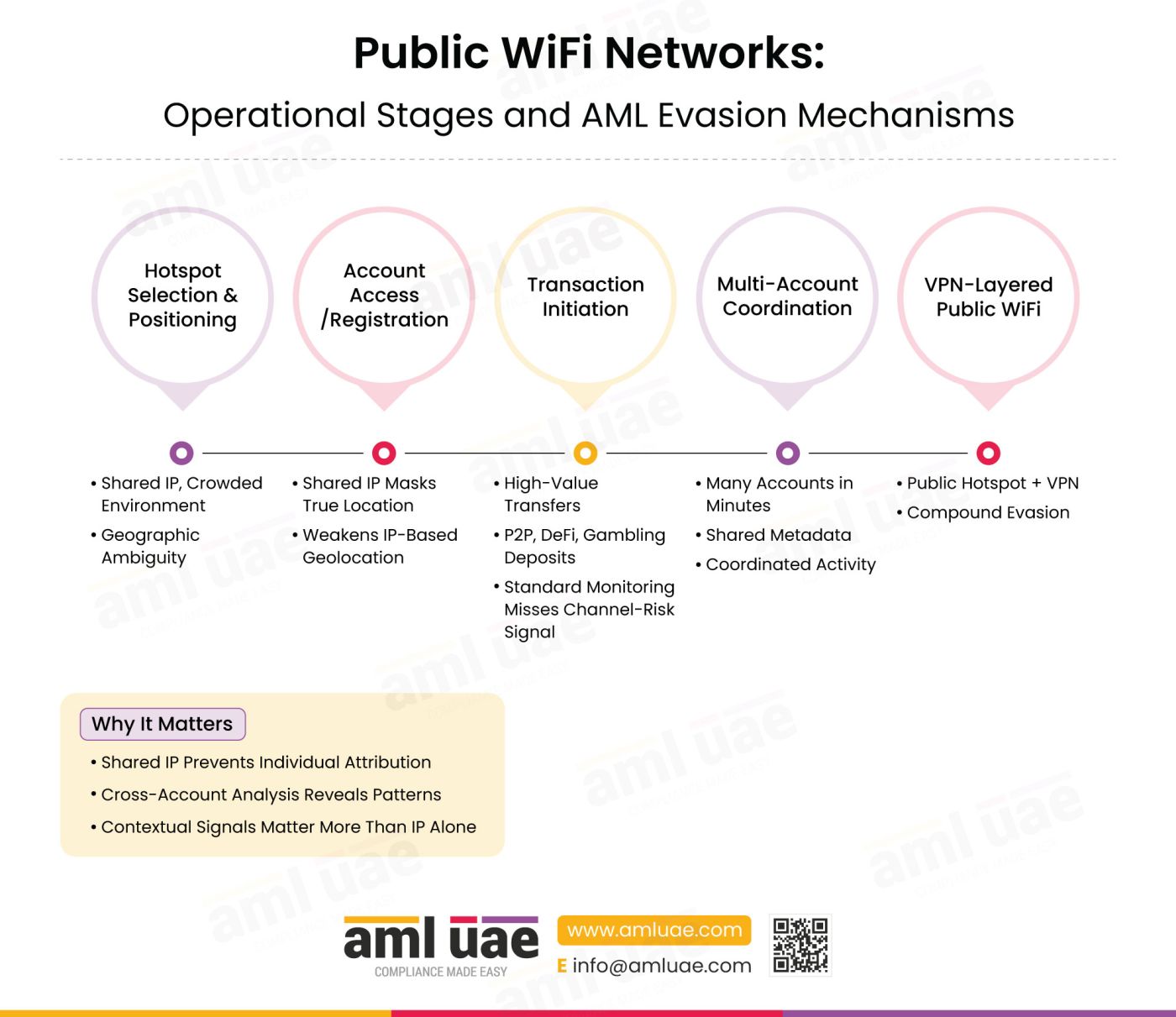

Stage One: Hotspot Selection and Positioning

The illicit operator selects a public WiFi location based on the intended financial activity. Account registration requires a location with a high volume of concurrent users, maximising the number of legitimate users sharing the IP and minimising the operational significance of any single device. High-value transaction initiation may favour a location with known geographic ambiguity, such as an international airport, where the hotspot IP is associated with multiple possible jurisdictions of origin.

Locations with minimal CCTV coverage or crowded environments where device identification is practically impossible provide the additional operational security of physical anonymity alongside the digital IP-sharing advantage. The operator may rotate between multiple hotspot locations within a single session or across multiple sessions to prevent any individual hotspot IP from accumulating suspicious activity volume.

Stage Two: Account Access or Registration from Shared IP

The operator accesses an existing financial account or registers a new one from the hotspot connection. For account registration, the hotspot IP prevents the platform from geolocating the registration to a specific address or jurisdiction. If the platform’s risk assessment assigns risk based partly on the registration IP geography, the hotspot IP, which may be associated with a commercial district or transportation hub rather than a residential address, may trigger a lower risk rating than the operator’s true location would generate.

For existing account access, the hotspot IP creates a geolocation mismatch against the customer’s registered address that may not individually trigger an alert if the customer is a frequent traveller or the platform does not apply geographic consistency checks across sessions.

Stage Three: Transaction Initiation from Public Network

Transactions are initiated through the hotspot-masked session. These include high-value transfers, cryptocurrency purchases through virtual asset exchanges, DeFi platform interactions, peer-to-peer payments, and online gambling deposits. The transaction records show the hotspot IP as the origin. Standard transaction monitoring calibrated only to transaction value and counterparty geography does not flag the access channel as a risk covariate.

Multiple transactions across multiple accounts may be initiated in rapid sequence from the same hotspot within a short window. Because each account sees the transaction as initiated from a plausible commercial district IP, none individually raises an alert. Only cross-account analysis that identifies the shared hotspot IP across all accounts reveals the pattern.

Stage Four: Multi-Account Coordination via Hotspot

The most significant use of public WiFi in financial crime is the coordinated creation or access of multiple accounts from the same hotspot within a short timeframe. A single hotspot session can be used to open multiple new accounts at different financial platforms, submit account registration documents that include false or inconsistent personal information, and initiate the first transactions on each account before the standard onboarding monitoring has identified the pattern.

Multiple accounts created from the same hotspot IP within minutes of each other, particularly when the accounts use different identity documents but share session metadata such as device type or browser configuration, provide a detectable pattern that individual account onboarding does not identify.

Stage Five: VPN-Layered Public WiFi for Compound Evasion

The most sophisticated variant combines public WiFi access with VPN use. The operator connects to a public hotspot, then routes their traffic through a VPN. The platform sees a VPN server IP, not the hotspot IP. If the VPN is also on a residential IP list, the connection appears entirely legitimate in terms of IP geography. The public WiFi access provides the physical location ambiguity; the VPN provides the IP substitution.

This layered approach, specifically identified in this typology’s indicators as a red flag, creates a compound evasion stack that is visible only in the network access logs of the institution, where the combination of hotspot network characteristics and VPN routing can be identified through deep packet inspection or network access metadata analysis.

Real-World Examples of Public WiFi Networks

The Airport Hotspot Account Opening Operation

An international airport WiFi network was identified as the registration IP for eleven new accounts opened at a cryptocurrency exchange over a four-hour window during a single business day. Each account used different identity documentation; the documentation submitted showed some signs of inconsistency, with similar photo backgrounds across four of the accounts. The shared hotspot IP was the initial alert trigger, identified when the exchange’s onboarding system flagged multiple new accounts from the same IP within a defined time window. An EDD review of the eleven accounts identified the documentation inconsistencies. STRs were filed.

The operational lesson is that a maximum account creation rate per IP address is an effective first-line control for public hotspot onboarding fraud, but must be calibrated to distinguish between legitimate multi-device household use and coordinated new-account operations.

The Coffee Shop Multi-Account Structuring Scheme

A peer-to-peer payment platform identified that a set of sending accounts had collectively transferred amounts just below the platform’s standard monitoring threshold to the same receiving accounts over a two-week period. Network access log analysis revealed that the majority of the sending account sessions had originated from the same commercial-district hotspot IP at a café adjacent to the receiving accounts’ registered address. The sessions from the café hotspot occurred consistently in the late afternoon, outside the business hours declared by the account holders’ stated occupations. The combination of hotspot-shared IP, consistent session timing, inconsistent with stated occupation, and sub-threshold structuring across multiple accounts provided a robust suspicion basis for coordinated STR filing.

The lesson is that hotspot access combined with temporal session patterns and structuring behaviour creates a composite indicator set stronger than any single signal.

The Hotel WiFi Combined VPN Operation

A digital banking platform identified a customer whose account access consistently originated from hotel WiFi IP addresses across three different cities over a six-week period. Each hotel session was further masked by a VPN, with the VPN exit nodes rotating between different commercial IP providers. The customer’s stated occupation and registered address suggested a local professional with no documented travel requirement. The combination of hotel hotspot IP origins, rotating VPN routing, and a profile inconsistent with the observed travel pattern triggered an EDD review. The EDD identified that the customer’s account had received multiple peer-to-peer payments from accounts also originating from hotel WiFi networks in the same cities on overlapping dates.

The lesson is that hotel WiFi access is not inherently suspicious but becomes a red flag when combined with VPN layering and a profile that does not explain the travel pattern.

How do Public WiFi Networks Facilitate Money Laundering?

Public WiFi networks facilitate money laundering through operational evasion, specifically by providing geographic and individual attribution ambiguity without requiring any technical tool installation. A criminal using a public hotspot does not hide their IP address; they share it with dozens of other users, making individual attribution from the IP alone practically impossible and legally insufficient.

This shared attribution property is exploited at two stages. At the placement stage, account registrations and initial deposits from public hotspot IPs prevent platforms from accurately geolocating the true origin of the funds and the identity of the person opening the account. At the layering stage, transactions initiated from public hotspot IPs, particularly when combined with rapid account switching and sub-threshold structuring, create a transaction pattern that appears distributed across multiple apparently unrelated users of the same hotspot.

How Do Criminals Exploit Public WiFi Networks?

Illicit operators deploying public WiFi for financial crime fall into two broad operational profiles. The first is the individual actor who uses public hotspots as a matter of routine operational security, accessing financial accounts from locations where physical presence cannot be individually attributed. This actor does not use any additional technical tool; the public IP is sufficient for their evasion objective, which is to prevent their home or office IP from appearing in access logs that could later connect them to a specific transaction.

The second profile is the more operationally significant one: the coordinated actor who uses public hotspots specifically for mass account opening operations, coordinated structuring across multiple accounts, and the physical evasion advantage of crowded public spaces. This actor may use multiple devices simultaneously from the same hotspot, registering accounts at different financial platforms within a single session, relying on the shared IP to prevent cross-platform correlation.

What Are the Red Flags That Identify Public WiFi Networks?

| Customer | Account registrations or modifications initiated from public WiFi IPs, accompanied by false or inconsistent personal information submitted at the same session |

| Customer | Customer profile (stated occupation, location) is inconsistent with the geographic pattern of public hotspot access sessions observed over time |

| Customer | Multiple accounts at the same institution or across platforms registered from the same public hotspot IP within a short timeframe |

| Access Pattern | Discrepancies between the geolocation data of the transaction origin (public hotspot) and the customer’s registered or declared address |

| Access Pattern | Frequent switching between geographically disparate public WiFi locations within a short time span, inconsistent with the customer’s stated lifestyle or business travel pattern |

| Access Pattern | Multiple session logs from distinct public WiFi networks accessing various customer accounts in a condensed timeframe, suggesting coordinated access from multiple locations |

| Access Pattern | Use of VPN in conjunction with public WiFi access, identified by layered IP proxy patterns in network logs, indicating compound evasion intent |

| Device | Rapid changes in device fingerprints during sessions from public hotspots, reflecting possible device switching or emulation within the same session |

| Transaction | High-value or rapid repeated fund transfers executed from unsecured public WiFi connections that deviate from the customer’s normal access pattern |

| Transaction | Multiple transactions initiated from IP addresses associated with known public WiFi hotspots, such as airports, hotels, libraries, and coffee shops |

| Transaction | Sub-threshold structured transactions are consistently initiated from different public hotspot locations across a compressed time period |

Controls to Mitigate Risks from Public WiFi Networks

| Control | What It Disrupts | Detect / Prevent / Deter | Specific Limitation |

| Access Authentication and Monitoring | Unattributed account access from shared hotspot IPs | Detects | Requires integration of public hotspot IP classification into session authentication; standard username-password authentication does not check IP type |

| Public Hotspot IP Classification | Known commercial hotspot IPs (airports, hotels, major café chains) | Detects and deters | Maintains databases of known public hotspot IP ranges; less effective against unclassified local hotspots |

| Geolocation Cross-Reference | Mismatch between the hotspot location and the customer’s stated address | Detects | Requires that KYC records include a reliable registered location that can be compared against the session hotspot geography |

| Device Fingerprint Consistency Monitoring | Session fingerprint variance at hotspot locations | Detects | Effective when combined with hotspot IP classification; less reliable alone, as device changes are common legitimate behaviour |

| Multi-Account New Registration Rate Limit per IP | Coordinated mass account opening from a shared hotspot | Prevents | Requires calibration to distinguish between household multi-device use and coordinated network operations |

| Risk-Based Customer Profiling and Segmentation | Inconsistent access patterns relative to the declared customer profile | Detects | Dependent on the institution having a reliable baseline for expected access behaviour per customer segment |

| Transaction Monitoring | High-value transactions and structuring patterns from hotspot sessions | Detects | Standard value-based rules do not capture access-channel as a covariate; hotspot-specific rules are required |

| Staff AML Training and Awareness | Failure to recognise and escalate hotspot access patterns during customer interactions | Deters | Front-line staff who understand the specific red flags for public WiFi abuse are better equipped to escalate concerns at the EDD review stage |

| Service Restriction | New high-value transactions or account registrations from classified high-risk public hotspots | Prevents | Blanket restriction on all public hotspot access creates access barriers; a risk-based approach, restricting only specific high-risk activity types from hotspot sessions, is more proportionate |

| Ongoing Due Diligence | Evolving access patterns that emerge after onboarding and only become concerning over time | Detects | Requires periodic review of access metadata, not only onboarding-time checks |

How Do AI and RegTech Automate Detection of Public WiFi Networks?

The detection signatures of public WiFi exploitation, particularly the combination of shared hotspot IPs, geolocation mismatches against customer profiles, and coordinated multi-account session patterns, are well-suited to automated detection systems that operate at the intersection of access-layer and transaction-layer data.

Public WiFi and hotspot IP classification databases are maintained by commercial threat intelligence providers and include the IP ranges associated with airport WiFi networks, major hotel chains, café franchise hotspot systems, and municipal free WiFi infrastructure. When integrated into the session authentication and monitoring system, these databases classify incoming connections in real time as public hotspot access. This classification enables hotspot-specific risk rules to be applied at the transaction and onboarding layers.

Geolocation enrichment of session data overlays each session’s hotspot IP with the physical location of the hotspot. When the hotspot location is correlated against the customer’s KYC-registered address, frequent discrepancies are automatically flagged for compliance review.

Multi-account new registration detection applies per-IP session analysis to identify when the same hotspot IP has been used to register multiple new accounts at the same institution within a defined time window. Machine learning models trained on the normal distribution of new account registrations per IP can flag outlier events that suggest coordinated account opening operations.

Behavioural baseline models identify individual customer session patterns and flag deviations. A customer who has consistently accessed their account from a residential IP and begins accessing from a series of public hotspot IPs represents a session discontinuity that, when combined with a transaction behaviour change, generates a composite risk alert for compliance review.

Combined VPN and hotspot detection identifies the specific compound evasion pattern in which a public WiFi connection is used as the network entry point and a VPN is then applied to substitute a clean residential or commercial IP. Deep packet inspection or network access metadata analysis that identifies the public WiFi network characteristics at the connection layer, even when the IP presented to the application layer is the VPN server’s IP, provides the most complete detection coverage for the layered evasion variant.

What Data Should Compliance Teams Collect to Detect Public WiFi Networks?

| Data Point | Source System | What It Reveals |

| IP address per session with hotspot classification (public WiFi, residential, commercial) | System and network access logs / IP intelligence feed | Whether the connecting IP is a known public hotspot, and the specific location of that hotspot |

| Geographic location of the hotspot vs the KYC-registered customer address | Geographical transaction data / KYC records | Whether a persistent gap exists between the customer’s stated location and the actual session geography |

| Session timing patterns per account | Digital banking and cybersecurity event data | Whether session timing is consistent with the customer’s stated lifestyle and occupation, or suggests public location access at unusual hours |

| Per-IP new account registration count within rolling time windows | KYC records/system access logs | Whether the same hotspot IP has been used to register multiple new accounts indicating potential coordinated account opening |

| Device fingerprint per session at hotspot IPs | Digital banking and cybersecurity event data | Whether device fingerprints are consistent with normal single-user behaviour or show rapid device variation suggesting multi-device coordination |

| Transaction initiation method per session | Transaction logs | Whether high-value or structured transactions are consistently initiated from public hotspot sessions rather than normal access sessions |

| Network layer connection metadata (for VPN-layered hotspot detection) | System and network access logs | Whether the connection exhibits the combination of public network entry and VPN IP presentation characteristic of layered evasion |

How Do Public WiFi Networks Aggravate Channel Risk?

Channel Risk is increased by public WiFi use because the shared IP characteristic fundamentally degrades the individual attribution component of the digital channel’s identity verification function. Every other channel risk factor, geographic risk rating, sanctions jurisdiction screening, and EDD trigger based on access geography operate on the assumption that the connecting IP can be attributed to a specific individual or, at a minimum, to a specific physical location used by a specific person. The shared hotspot IP completely breaks this assumption.

The specific channel risk impact on the financial sector, which has large-volume public hotspot environments, including the International Airport, which processes some of the world’s highest annual passenger volumes, and the city’s substantial business hotel and conference infrastructure, provides legitimate high-traffic contexts in which individual-level attribution from IP is practically impossible. Criminals who understand this volume effect specifically select these high-traffic locations to maximise the attribution difficulty.

For financial institutions and VASPs operating mobile-first platforms, where a significant proportion of legitimate customer transactions occur from mobile devices on shared networks, the channel risk calibration challenge is particularly acute. The institution must identify the risk-relevant subset of hotspot transactions without applying controls that impede the legitimate mobile access behaviour that defines the product’s value proposition.

How Do Compliance Officers Identify Public WiFi Network Patterns?

Compliance officers encounter public WiFi exploitation most frequently through four observable patterns.

The first is the account registration cluster. Multiple new accounts at the same institution appearing in the onboarding queue within a short window, all with the same registration IP in a known commercial hotspot area.

The second is the profile-geography mismatch. A customer whose stated occupation and residential address are inconsistent with a pattern of access from airport and hotel hotspot IPs across multiple cities.

The third is the combined hotspot-VPN pattern. A sessions where the application-layer IP is a VPN server, but the network access logs reveal a public network entry point.

The fourth is the structuring-from-hotspot pattern. Multiple sub-threshold transactions initiated from different public hotspot locations within a compressed time period, with no other contextual explanation.

Sectors at Highest Exposure

| Sector | Risk Rating | Specific Reasoning |

| Mobile Banking Services | Critical | Mobile banking is accessed predominantly through mobile devices on mixed networks, including public WiFi; the platform design creates structural exposure to this typology |

| Virtual Asset Exchanges | Critical | VASPs with mobile applications are used for cryptocurrency purchases and account opening operations that can be initiated from public hotspot sessions without triggering standard transaction-value monitoring |

| Peer-to-Peer Payment Platforms | High | P2P payment systems on mobile devices are used for structured payment operations that can be coordinated from shared public network IPs |

| DeFi and Online Brokerage Platforms | High | Account registrations and transaction initiations on DeFi platforms and online brokerage accounts can be coordinated across multiple platform accounts from a single hotspot session |

| Digital Wallets and Online Payment Platforms | Moderate | Digital wallets used for P2P and merchant payments may be loaded from public hotspot sessions; the transaction value range is typically lower, but the volume of accounts at risk is higher |

Best Practices for Public WiFi Networks Risk Management

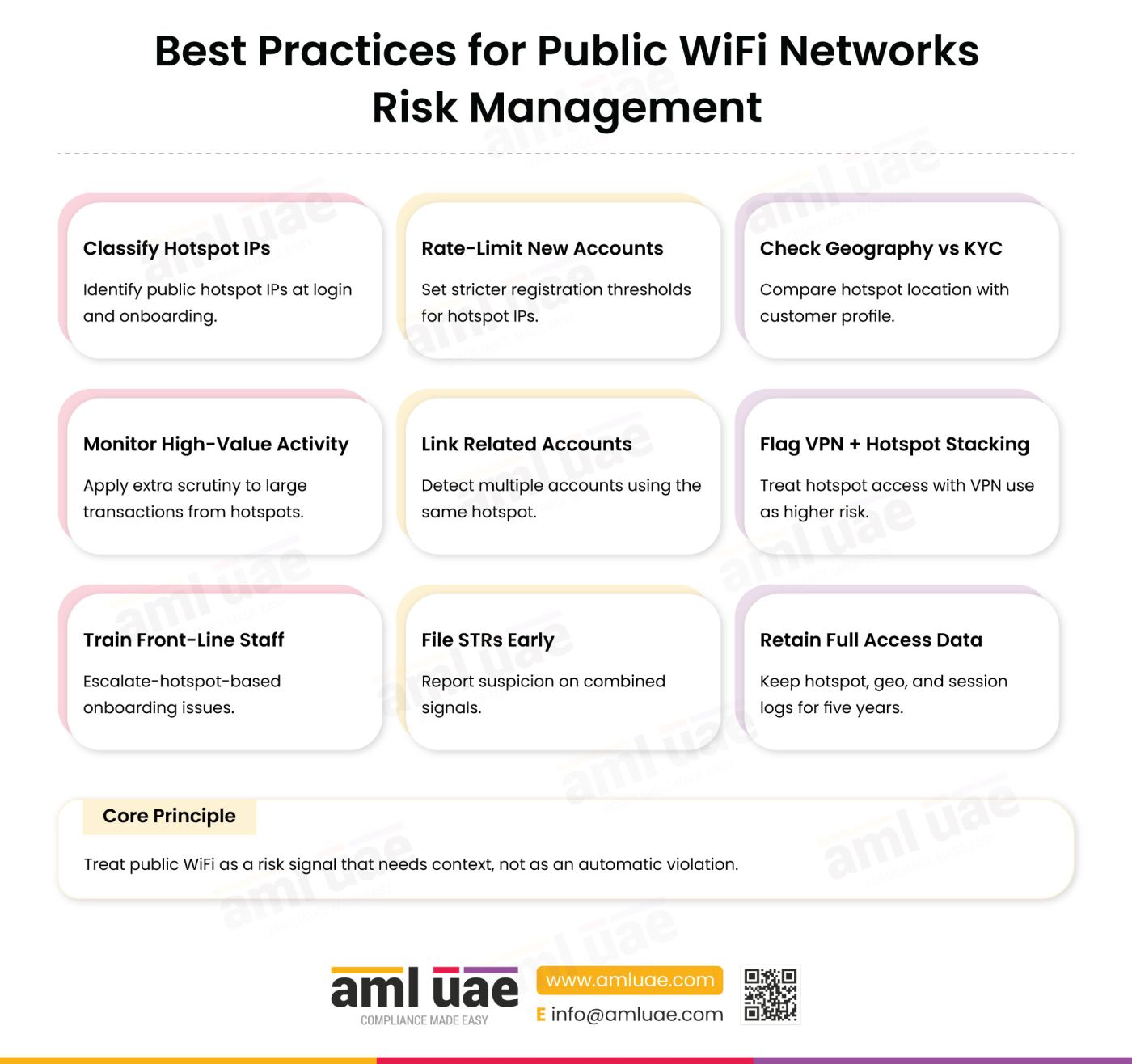

- Integrate public hotspot IP classification into the session authentication and onboarding risk assessment. Maintain a subscription to a commercial hotspot IP database that includes airport networks, hotel chains, café franchise systems, and municipal public WiFi. Apply hotspot classification at login and at account registration initiation. Treat hotspot-origin sessions as a distinct access channel with a separate risk covariate in the monitoring framework.

- Apply a maximum new account registration rate per IP address, calibrated by IP type. A residential IP generating three new accounts per month is within normal multi-person household use. A public hotspot IP generating ten new accounts per hour is not. Implement a rate limit for new account registrations from classified hotspot IPs, with an automatic hold and EDD escalation when the threshold is exceeded. Calibrate the threshold to the expected normal rate for the hotspot type, not a blanket IP-level cap.

- Cross-reference hotspot session geography against the customer’s KYC-registered address and stated profile. When a session originates from a public hotspot in a different city or country from the customer’s registered address, flag the geographic mismatch for compliance review. A single instance is of low significance; a consistent pattern of hotspot access from geographies inconsistent with the stated profile requires a specific explanation during the next periodic review.

- Configure transaction monitoring to apply elevated scrutiny to high-value transactions initiated from public hotspot sessions. Transactions above a defined value initiated from a public hotspot IP, particularly where the customer’s normal access pattern does not include public hotspot use, should trigger a specific alert. This is not a restriction on all hotspot transactions, but rather a contextual rule that combines the access channel with the transaction value and the deviation from baseline.

- Identify and investigate multi-account coordinated patterns from shared hotspot IPs. Run cross-account analysis on the hotspot IP access logs to identify cases where multiple accounts, either at the same institution or shared with intelligence from the UAEFIU, have been accessed or registered from the same hotspot IP within a defined time window. The presence of multiple accounts from the same hotspot IP, particularly with consistent session timing, provides the primary signal for coordinated account operations.

- Detect and flag the VPN-layered public WiFi compound evasion pattern. When network access metadata indicates that the application-layer connection presents a VPN IP while the network entry point is a public hotspot, apply the detection rules for both the VPN and public WiFi typologies simultaneously. This compound pattern indicates a higher level of deliberate intent to evade than either signal alone.

- Train front-line staff to escalate account registrations from public hotspot IPs when combined with documentation inconsistencies. Staff who conduct customer identity verification at onboarding should understand that documents submitted during a session originating from a public hotspot, particularly when combined with photo background similarities across multiple accounts or other documentation inconsistencies, represent a specific red flag requiring an immediate compliance escalation. Staff AML training for this typology must cover the multi-account hotspot registration pattern specifically.

- File STRs based on combined hotspot access and profile inconsistency evidence, without waiting for a transaction threshold. Article 18 of Federal Decree Law No. (10) of 2025 triggers on suspicion without a minimum value, and the suspicion test is channel-neutral. By way of example, a new account registration from a public hotspot IP, combined with documentation inconsistencies and a customer profile that does not explain the hotspot access pattern, may form part of the facts on which a compliance officer concludes that the threshold is met, even if no individual transaction has yet occurred. Early STR filing on the account opening event itself is appropriate where the evidence supports it.

- Retain granular geographic transaction data and session access metadata for the full five-year period. Article 25 of Cabinet Decision No. (134) of 2025 sets a general five-year minimum retention period. The provision does not prescribe particular data fields. As an operational matter, where a regulated entity treats shared-network access as a relevant channel risk, geographic transaction data that links the hotspot IP to a specific location database record, and session-level timing data that supports cross-account pattern analysis, are useful records to retain at the granularity required for forensic investigation. Records that capture only the transaction without the access layer metadata do not support effective investigation of this typology.

How Public WiFi Networks and Anonymous Networking Are Related

Public WiFi Networks are a sub-technique of the Anonymous Networking typology. Anonymous networking encompasses all techniques that sever the reliable attribution of a digital financial activity to a specific individual. Public WiFi achieves this through the shared IP property of public network infrastructure rather than through technical IP substitution.

The critical distinction that makes public WiFi a unique sub-technique rather than a variation on VPN or proxy use is the absence of any additional technical tool requirement. VPN and proxy use require installation and configuration; public WiFi use requires only physical presence in a public location.

This accessibility means that the population of potential users of this technique is the full population of mobile device owners, not only technically capable actors. The detection methodology also differs: public WiFi detection depends on hotspot IP classification databases and geographic session pattern analysis, not on the behavioural anomaly detection required for residential proxy identification.

The compound evasion variant, in which public WiFi is used alongside a VPN, combines the IP substitution capability of the VPN sub-technique with the physical location ambiguity of the public WiFi sub-technique. Compliance programmes that address VPN detection without extending their analysis to the underlying network access characteristics will miss the compound variant entirely.

Related Terms and Concepts

Related Terms

| Term | Connection |

| Anonymous Networking | Parent typology: public WiFi is one specific implementation within the anonymous networking detection evasion category |

| Virtual Private Network | Sibling sub-technique: VPN replaces the IP address; public WiFi provides a shared IP that cannot be individually attributed; the two are frequently combined |

| Proxy Servers | Sibling sub-technique: proxies route traffic through intermediary infrastructure; public WiFi provides the shared network entry point that may precede proxy or VPN routing |

| Micro-Structuring | Sub-threshold transaction technique is frequently deployed from public hotspot sessions to defeat both access-layer and transaction-layer monitoring simultaneously |

| Privacy Coins | Financial instrument acquired through virtual asset exchange accounts accessed from public hotspot sessions; combines access-layer and financial record-layer anonymisation |

| Account Takeover and Fraud | Fraud typology for which public WiFi access provides the unattributed access point for the initial fraudulent account access or creation event |

Related Processes

| Process | Connection |

| Public Hotspot IP Classification | The primary access-layer detection procedure for identifying public WiFi access in real time |

| Cross-Account Session Correlation | The analytical procedure that identifies coordinated multi-account operations from shared hotspot IPs |

| Geographic Session Cross-Reference | The compliance procedure that compares hotspot session geography against KYC profile data |

Related Controls

| Control | Connection |

| New Account Registration Rate Limiting | The specific preventive control that addresses the coordinated mass account opening vulnerability |

| Device Fingerprint Monitoring | An access signal that detects multi-device coordination during hotspot sessions |

| Transaction Monitoring with Access Covariates | Requires extension beyond value and counterparty to include the access channel type |

What Financial Instruments Do Criminals Use in Public WiFi Networks Schemes?

Bank accounts are both created and accessed from public hotspot sessions. New account opening from a public WiFi IP provides a registration record that cannot be geographically attributed to the criminal’s true location. Existing account access from public hotspots, combined with immediate high-value transactions, provides a transaction event whose initiation cannot be traced to a specific physical address.

Cryptocurrency wallets are accessed from public hotspot sessions for cryptocurrency purchase, transfer, and conversion. Virtual asset exchange accounts created from public hotspot IPs, combined with subsequent conversion to privacy coins, create a financial record that connects only to the hotspot IP at the account opening stage.

Online gambling accounts are used as an integration channel. Funds deposited through gambling accounts accessed from public hotspot sessions are described as gambling activity with no fixed geographic origin. The gambling platform’s own geographic risk controls are defeated by the hotspot IP.

Prepaid and stored-value payment instruments are funded through public hotspot sessions, removing the geographic attribution of the funding event. Loaded balances can then be transferred or spent without reference to the hotspot session from which they were funded.

Privacy coins are acquired through virtual asset exchange accounts accessed from public hotspot sessions. The combination of hotspot IP at account access and privacy coin at the transaction level creates compound evasion at both the access layer and the financial record layer.

Variants and Synonyms

| Term | Context or Jurisdiction | Distinction from Primary Term |

| Public hotspot exploitation | Technical and compliance contexts | A general term for any use of public WiFi infrastructure for financial evasion purposes |

| Free WiFi exploitation | Consumer and fraud analytics | Emphasises the free access characteristic that makes this technique universally accessible |

| Airport WiFi fraud | Law enforcement and onboarding fraud contexts | Specific application of the technique in high-volume airport hotspot environments |

| Nomadic account fraud | Account opening fraud analytics | Describes the pattern of creating multiple accounts from different transient public network locations |

What Products and Services Do Criminals Abuse in Public WiFi Networks Schemes?

Digital banking services are abused through mobile application access from public hotspot sessions. Banks with mobile-first product designs experience the highest exposure to this typology because their customers are structurally more likely to access the platform from mobile devices on shared networks. A digital bank that does not apply hotspot IP classification at the access layer is processing a proportion of its mobile transactions without reliable geographic attribution.

Mobile banking applications are the primary attack surface for this typology. A mobile banking application accessed from a public hotspot provides the combined advantages of a small screen that prevents easy shoulder surveillance, a shared IP that prevents network attribution, and a mobile payment capability that enables immediate fund movement after account access.

Peer-to-peer payment systems are used for structured payment operations initiated from public hotspot sessions. The recipient attribution in P2P payments is typically verified at the beneficiary’s end; the sender’s geographic origin at the time of payment initiation is captured only in the session log.

Online payment platforms and payment processing services are abused for payments whose geographic origin is recorded as the hotspot IP rather than the operator’s true location. Merchants receiving payments processed through hotspot sessions cannot readily identify that the payment was initiated from a non-residential access point.

Decentralised finance services are accessed from public hotspot sessions for interactions with DeFi protocols that have no centralised onboarding or IP monitoring capability. A compliance obligation exists at the regulated access points to these services, such as centralised exchanges or payment on-ramps, not at the DeFi protocol level itself.

Peer-to-peer cryptocurrency trading platforms are used for cryptocurrency acquisition from public hotspot sessions, exploiting the lighter onboarding controls typical of P2P platforms to create accounts and initiate trades without reliable geographic attribution.

How AML UAE Helps Manage Public WiFi Network Risks

The public WiFi typology presents a compliance challenge that sits at the intersection of access-channel risk management and mobile platform design. Financial institutions and VASPs with mobile-first products face this typology at scale, because the proportion of legitimate transactions from public networks is significant and blanket restrictions are not operationally viable.

AML UAE provides practical guidance on configuring transaction-monitoring covariates for access channel type and on staff training requirements for recognising the multi-account hotspot registration pattern at the onboarding stage.

For institutions building or reviewing their VASP and mobile banking compliance frameworks, AML UAE supports the development of AML/CFT programme, KYC/CDD procedures, training, and health check services.

Conclusion: Public WiFi Networks

Public WiFi networks represent the most accessible sub-technique within the anonymous networking typology, requiring no tool installation and no technical capability beyond physical presence in a public location. The shared IP characteristic creates an attribution problem that affects the geographic dimension of every compliance control applied at the access layer.

The detection investment is proportionate. Hotspot IP classification databases are commercially available, cross-account session analysis is a logical extension of existing monitoring infrastructure, and the specific red flags for coordinated account opening operations are well-defined.

The compliance programme that addresses this typology effectively treats public hotspot access as a contextual risk signal rather than as either an inherently suspicious event or an ignored channel characteristic. The context, specifically the combination of hotspot access with profile inconsistency, documentation anomalies, transaction pattern deviations, and multi-account timing, is what converts a normal mobile session into a compliance event requiring escalation and, where the evidence warrants, immediate STR filing.

Public WiFi is the compliance challenge that requires no technical expertise from the criminal and no database gap from the institution. The hotspot IP is not a VPN IP. It is not in any blacklist. It is a legitimate commercial network entry point. The only reason it creates an attribution problem is that it is shared. The compliance answer is not to block public WiFi transactions; it is to treat hotspot access as a signal that additional contextual evidence is needed before risk is assessed. Profile, timing, transaction value, and multi-account coordination, those are the covariates that turn a hotspot session into a compliance event.

Frequently Asked Questions

Public WiFi networks provide shared, transient IP addresses that cannot be attributed to any individual user. Criminals use public hotspots to access financial accounts, register new accounts, and initiate transactions in a manner that prevents IP-based individual attribution, without requiring any additional technical tool such as a VPN or proxy.

VPNs substitute the user’s real IP with a different IP. Public WiFi shares the same IP across all concurrent users of the hotspot, making individual attribution from the IP impossible rather than merely difficult. The two techniques are frequently combined: the criminal uses public WiFi as the network entry point and adds a VPN for additional IP substitution.

Mobile banking platforms are accessed primarily from mobile devices that frequently connect to shared networks, including public WiFi. The platform receives a shared hotspot IP that cannot be attributed to an individual, defeating IP-based geographic risk controls. The high volume of legitimate mobile banking transactions from public networks makes blanket restriction impractical and requires risk-based detection instead.

Multiple new account registrations from the same public hotspot IP within a short timeframe are the most operationally significant red flag, as it directly indicates coordinated account opening operations. This pattern, combined with documentation inconsistencies, provides a robust basis for both STR filing and regulatory referral.

Primary detection methods include: classifying known public hotspot IPs using commercial hotspot databases; cross-referencing session hotspot geography against the customer’s KYC profile; applying elevated risk rules to high-value transactions from hotspot sessions; and running cross-account analysis to identify shared hotspot IP patterns across multiple accounts.

Article 18 of Federal Decree-Law No. (10) of 2025 requires reporting to the UAE FIU on the basis of suspicion or reasonable grounds to suspect, without a minimum transaction value. The suspicion test is channel-neutral and fact-based. Where a regulated entity treats shared-network access as a relevant channel risk, hotspot access combined with profile inconsistency, documentation anomalies, or coordinated multi-account patterns is an example of facts a compliance officer may weigh in assessing whether the threshold is met, including before any individual transaction reaches a standard monitoring threshold.

Standard VPN use involves routing traffic through a VPN server from any network. The layered variant specifically uses a public hotspot as the network entry point and then adds VPN routing. This provides both physical location ambiguity (the operator is at a public location) and IP substitution (the VPN server’s IP is what the platform sees), creating compound evasion that requires both hotspot classification and VPN detection to identify.

Article 25 of Cabinet Decision No. (134) of 2025 sets a general five-year minimum retention duty across customer, transaction and supporting records. The provision does not prescribe particular data fields. As an operational matter, where a regulated entity has treated digital access channels as part of its risk framework, useful records to support public WiFi investigations include IP access logs with hotspot classification, geographic transaction data linking the IP to the hotspot’s physical location, device fingerprint data per session, and the results of cross-account IP correlation analysis.

No. A significant proportion of legitimate banking transactions are conducted from mobile devices on shared networks including public WiFi. The compliance assessment focuses on context. Whether the hotspot access is combined with other risk indicators, such as profile inconsistency, documentation anomalies, high-value transaction initiation, or cross-account coordination. Hotspot access alone, without additional indicators, is a risk-elevated access channel signal, not an inherently suspicious event.

Identify Public WiFi Risk in Your AML Controls

See how shared hotspot IPs can weaken attribution, create access-channel risk, and trigger the need for stronger monitoring in mobile-first environments.

Share via :

About the Author

Pathik Shah

FCA, CAMS, CISA, CS, DISA (ICAI), FAFP (ICAI)

Pathik is an ACAMS-certified AML consultant specialising in governance, risk, and compliance for regulated entities in the UAE. He brings over 28 years of experience, with 1,000+ hours of AML training and 200+ advisory engagements across DNFBPs, VASPs, and FIs. He supports businesses in aligning with AML/CFT requirements from the CBUAE, DFSA, MoET, MoJ, VARA, CMA, FSRA, and FATF. Known for translating complex regulations into audit-ready procedures, Pathik enables operational clarity and compliance readiness.

Reach Out to Pathik