History of AML Regulations in UAE

Last Updated: 05/04/2026

Protect your business with reliable and effective AML strategies with AML UAE.

AT A GLANCE: UAE AML Legislative Timeline

- Current Primary Law: Federal Decree-Law No. 10 of 2025, entered force October 2025 (Article 42)

- Current Executive Regulation: Cabinet Resolution No. 134 of 2025 , replaces Cabinet Resolution No. 10 of 2019

- Counter-Terrorism Law: Federal Law No. 7 of 2014 , remains in force alongside Law 10/2025

- Targeted Financial Sanctions: Cabinet Resolution No. 74 of 2020 , without-delay asset freeze obligation (Article 15); 24-hour standard per Executive Office guidance

- Beneficial Ownership Rules: Cabinet Resolution No. 109 of 2023 , 25% threshold; 60-day register deadline (Art. 8)

- DNFBP Penalty Schedule: Cabinet Resolution No. 71 of 2024 , fines AED 50,000 to AED 1,000,000 (schedule, 41 violations)

- Financial Intelligence Unit: Receives and analyses SAR/STR

- ML Criminal Penalty: 1-10 years + AED 100,000-5,000,000; aggravated AED 1M-10M (Article 26, Law 10/2025)

- FT Criminal Penalty: Life imprisonment or 10+ years + AED 1,000,000-10,000,000 (Article 26, Law 10/2025)

- Legal Person ML/FT/PF Fine: AED 5,000,000-100,000,000 (Article 27, Law 10/2025)

- Predecessor Primary Law: Federal Decree-Law No. 20 of 2018 , repealed by Article 41 of Law 10/2025

What Are UAE AML Regulations?

UAE AML regulations are the body of federal laws, cabinet resolutions, and supervisory guidance that require financial institutions, designated non-financial businesses and professions (DNFBPs), and virtual asset service providers (VASPs) to detect, prevent, and report money laundering and terrorism financing.

History of AML Regulations in UAE

The history of AML regulations in UAE is a story of progressive legal reform, shaped by the country’s position as a global financial hub and by successive rounds of international standard-setting from the Financial Action Task Force (FATF) and the United Nations Security Council. This article traces the principal federal instruments that have defined the UAE’s anti-money laundering and counter-terrorism financing (AML/CFT) framework, examining what each law introduced, what it repealed, and how the regulated population and supervisory architecture evolved over time.

The focus of this page is historical and chronological. For a detailed explanation of current compliance obligations, please see Federal AML Laws and Executive Regulations in the UAE. For guidance on which entities must comply, see Who Must Comply with UAE AML Regulations. Primary legislation is available via the UAE Legislation Portal and the National Anti-Money Laundering Committee website.

Note: Scope of This Page

This page covers the chronological legislative history of UAE AML/CFT regulation. It does not cover: (1) current compliance obligations in detail , see the Federal AML Laws page; (2) which entities must comply , see the Who Must Comply page; or (3) sector-specific requirements , see the relevant sector articles. The boundary between this page and the Federal AML Laws page is historical context versus current obligation.

History of AML Regulations in UAE

1. Why AML Became Important

The UAE’s economic role, FATF pressure, and the shift to preventive compliance

2. How the Framework Evolved

Law-by-law analysis of seven key federal instruments from 2014 to 2025

3. Conclusion

Key themes and what the 2025 reforms signal for practitioners

4. FAQs

Seven frequently asked questions answered from primary legal sources

Why AML Regulations Became Important in the UAE

The UAE’s commitment to combating money laundering and terrorism financing reflects both domestic economic priorities and obligations under international law. Three interlocking factors explain why the country developed one of the most comprehensive AML/CFT legislative frameworks in the region.

Why AML Regulations Became Important in the UAE

1. The UAE as a Global Hub

How the country’s financial and trade position creates AML risk and responsibility

2. The Global Push

UN Security Council resolutions, FATF standards, and international treaty obligations

3. From Crime Control to Prevention

The shift from post-facto criminalisation to risk-based preventive compliance

The UAE's Role as a Global Financial, Trade, and Investment Hub

The UAE is a natural crossroads between East and West. Dubai and Abu Dhabi host major international financial centres, one of the world’s highest-volume trade corridors, and a real estate market that attracts substantial cross-border capital. This economic openness is a strategic asset and a regulatory responsibility. A jurisdiction that processes high volumes of capital, provides financial infrastructure for regional commerce, and attracts significant foreign investment must maintain robust controls to prevent those systems from being exploited for illicit purposes.

Federal Decree-Law No. 10 of 2025 acknowledges this reality in its preamble, stating that the legislation is issued in fulfilment of the State’s international obligations and national commitments to protect the integrity of its financial system. The territorial scope set out in Article 2 of the law, which extends to acts committed outside the country where they affect UAE interests or financial institutions, reflects the need to police cross-border flows as well as domestic ones.

The breadth of the sectors brought within the UAE AML framework further illustrates the point. Cabinet Resolution No. 134 of 2025 identifies fourteen categories of financial institution activity in Article 2, six categories of virtual asset service provider activity in Article 4, and a range of designated non-financial businesses and professions in Article 3, from commercial gaming operators to real estate brokers and trust and company service providers. This comprehensive scope maps directly onto the sectors most commonly exploited for illicit financial flows in a highly internationalised economy.

The Global Push for Stronger Anti-Money Laundering Frameworks

The preamble of Cabinet Resolution No. 74 of 2020, which establishes the UAE’s targeted financial sanctions framework, references five UN Security Council Resolutions explicitly: Resolution 1267 (1999), establishing the Al-Qaeda and Taliban sanctions regime; Resolutions 1988 and 1989 (both 2011), which separated and refined those regimes; Resolution 1718 (2006), addressing North Korea’s weapons programme; and Resolution 2231 (2015), concerning Iran’s nuclear activities. The obligation to implement these resolutions without delay is encoded in Article 15 of Cabinet Resolution No. 74 of 2020, which requires asset freezes to be effected within 24 hours of a designation or notification.

The FATF Recommendations form the overarching international standard to which the UAE’s legislative framework must conform. Cabinet Resolution No. 109 of 2023 references Federal Decree-Law No. 20 of 2018 and Cabinet Resolution No. 10 of 2019. Cabinet Resolution No. 71 of 2024 references Cabinet Resolution No. 16 of 2021 before repealing it. Federal Decree-Law No. 10 of 2025 expressly repeals Law 20 of 2018 in Article 41, completing the most recent reform cycle.

The institutional architecture created by Federal Decree-Law No. 10 of 2025 reflects these international obligations. Article 12 establishes a Supreme Committee for supervising the national AML/CFT strategy. Article 13 establishes the National Committee for Combating Money Laundering and the Financing of Terrorism, charged with coordinating strategy across supervisory authorities. Article 11 embeds the Financial Intelligence Unit within the Central Bank of the UAE, providing the operational infrastructure for the exchange of financial intelligence with foreign counterparts and for the reporting and analysis of suspicious transactions

The Move from Crime Control to Preventive Compliance

A reading of the instruments examined in this article reveals a clear direction of travel: from reactive criminalisation to proactive, risk-based prevention. Federal Law No. 7 of 2014, the oldest instrument discussed here, is principally a criminal statute concerned with terrorism and terrorism financing as offences. Its primary remedies are penal: imprisonment and fines following the commission of a crime, as set out in Articles 29 and 34 of that law.

The instruments from 2020 onwards are primarily preventive. Cabinet Resolution No. 74 of 2020 mandates active screening of customer databases against UN and national sanctions lists and requires institutions to freeze assets before a transaction is completed, an obligation that applies even where no criminal investigation has been opened. Cabinet Resolution No. 109 of 2023 moves further upstream, requiring legal persons to identify and register their real beneficiaries as an ongoing disclosure obligation aimed at eliminating corporate anonymity before any financial transaction is in question.

Federal Decree-Law No. 10 of 2025 and Cabinet Resolution No. 134 of 2025 complete this transition. Article 19 of Law 10/2025 imposes preventive measures obligations on financial institutions, DNFBPs, and VASPs as ongoing compliance requirements, independent of any specific transaction or suspicious activity. Article 17 empowers supervisory authorities to impose administrative penalties of AED 10,000 to AED 5,000,000 for compliance failures alone, meaning that inadequate internal controls, poor record-keeping, or failure to appoint a compliance officer are themselves punishable, whether or not any money laundering has occurred.

Need guidance on current AML obligations?

This article covers legislative history. For an explanation of what the law requires today, read our guide to Federal AML Laws and Executive Regulations in the UAE.

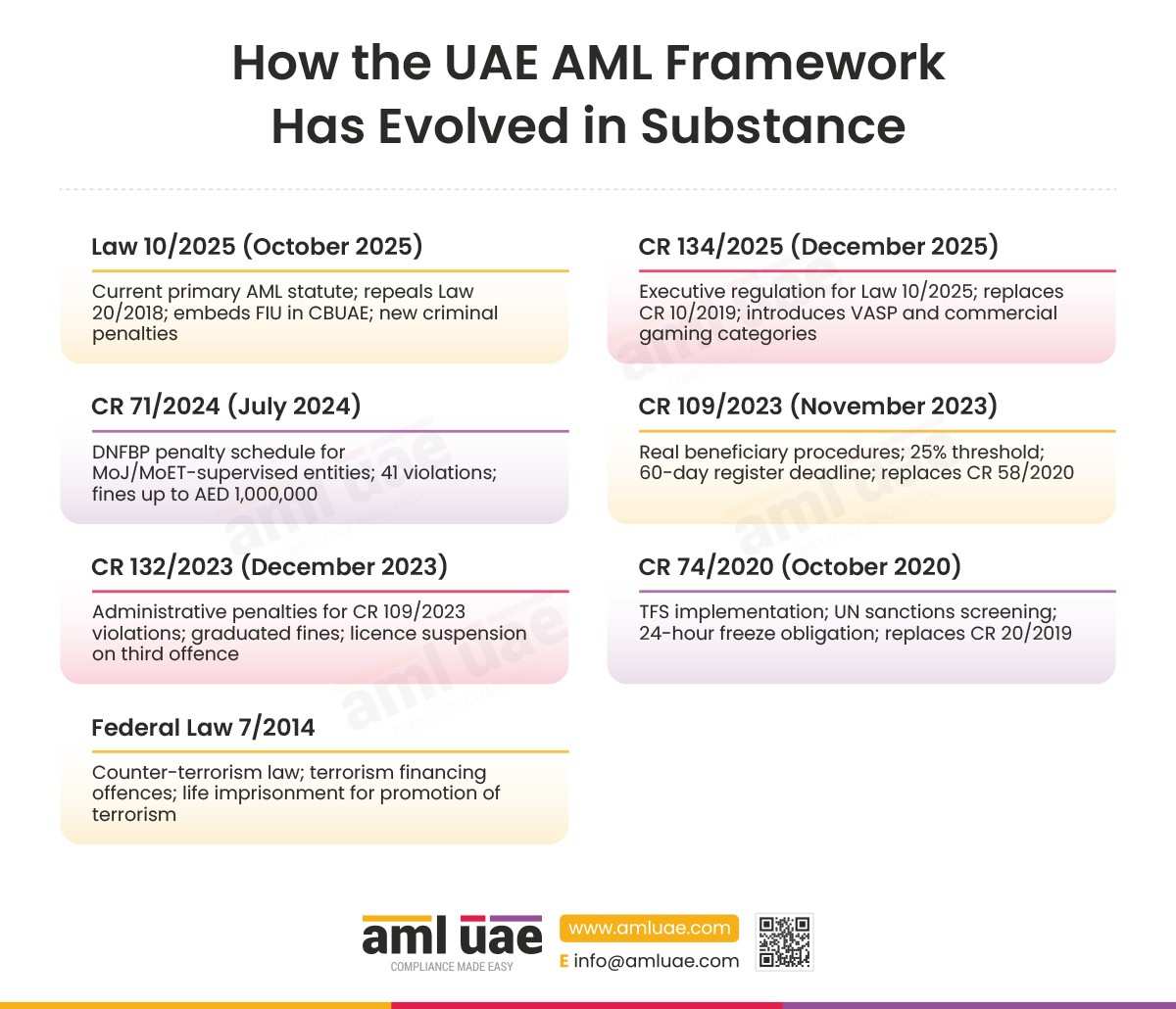

How the UAE AML Framework has evolved in Substance

The following section examines seven federal instruments in order of their issuance date, most recent first. For each instrument, it sets out the date of issue, the primary purpose, the key provisions, and what the instrument repealed or replaced. All article references are to the specific instruments cited and are traceable to the source legislation texts held in the UAE legislation repository.

How the UAE AML Framework has evolved in Substance

1. Law 10/2025 (October 2025)

Current primary AML statute; repeals Law 20/2018; embeds FIU in CBUAE; new criminal penalties

2. CR 134/2025 (December 2025)

Executive regulation for Law 10/2025; replaces CR 10/2019; introduces VASP and commercial gaming categories

3. CR 71/2024 (July 2024)

DNFBP penalty schedule for MoJ/MoET-supervised entities; 41 violations; fines up to AED 1,000,000

4. CR 109/2023 (November 2023)

Real beneficiary procedures; 25% threshold; 60-day register deadline; replaces CR 58/2020

5. CR 132/2023 (December 2023)

Administrative penalties for CR 109/2023 violations; graduated fines; licence suspension on third offence

6. CR 74/2020 (October 2020)

TFS implementation; UN sanctions screening; 24-hour freeze obligation; replaces CR 20/2019

7. Federal Law 7/2014

Counter-terrorism law; terrorism financing offences; life imprisonment for promotion of terrorism

2025

Primary Law

Federal Decree-Law No. 10 of 2025

Repeals Law 20/2018. Embeds FIU in CBUAE. Introduces FIU suspension and freeze powers. Broad criminal and administrative penalty framework.

2025

Exec. Regulation

Cabinet Resolution No. 134 of 2025

Executive regulation for Law 10/2025. Introduces commercial gaming and VASP categories. Sets CDD thresholds. Replaces CR 10/2019.

2024

DNFBP Penalties

Cabinet Resolution No. 71 of 2024

41 violations; fines AED 50,000-1,000,000. Doubling for repeat offences. Replaces CR 16/2021.

2023

Beneficial Owner

Cabinet Resolution No. 109 of 2023

Real beneficiary register; 25% threshold; 60-day deadline. Replaces CR 58/2020.

2023

UBO Penalties

Cabinet Resolution No. 132 of 2023

Administrative penalties for CR 109/2023 violations. Graduated fines; licence suspension on third offence. Replaces CR 53/2021.

2020

Sanctions/TFS

Cabinet Resolution No. 74 of 2020

Implements UN UNSC Res. 1267, 1718, 1988, 1989, 2231. 24-hour freeze obligation. Replaces CR 20/2019.

2014

Counter-Terrorism

Federal Law No. 7 of 2014

Foundational counter-terrorism and TF statute. Life imprisonment for terrorism financing promotion. Remains in force alongside Law 10/2025.

Federal Decree Law No. 10 of 2025, October 2025

Federal Decree-Law No. 10 of 2025 on Combating Money Laundering and the Financing of Terrorism and Illegal Organisations is the UAE’s current primary AML legislation. Issued on 30 September 2025, it entered into force two weeks after publication in the Official Gazette, per Article 42. The law supersedes Federal Decree-Law No. 20 of 2018, which it expressly repeals under Article 41, whilst preserving circulars, resolutions, and supervisory guidance issued under the repealed law where they do not conflict with the new legislation.

Article 2 defines money laundering as the conversion, transfer, deposit, or acquisition of proceeds with the intent to conceal their illicit origin or to assist in evading criminal liability. Article 3 defines terrorism financing. Article 4 extends criminal liability to legal persons alongside natural persons, meaning that companies, institutions, and other corporate entities face prosecution under the law in addition to the individuals acting on their behalf.

The institutional architecture introduced by Law 10/2025 has three principal elements. Article 11 formally embeds and strengthens the Financial Intelligence Unit within the Central Bank of the UAE (CBUAE). The FIU had operated under the previous Law 20/2018, and the 2025 legislation reinforces its mandate and expands its powers. Article 11 grants the FIU authority to receive and analyse suspicious transaction reports and to disseminate intelligence to competent authorities. Article 12 establishes the Supreme Committee for supervising the national AML/CFT strategy. Article 13 establishes the National Committee for Combating Money Laundering and the Financing of Terrorism, charged with coordinating the national strategy and monitoring its implementation across supervisory authorities.

A significant new power introduced by the 2025 law is Article 5, which gives the FIU the authority to order a cessation of any suspicious activity for a period of up to ten working days, and to impose a freeze on related assets for up to thirty days pending referral to the competent authority. This places the FIU in an active protective role rather than a purely analytical one.

Criminal penalties are set out in Article 26. Money laundering carries one to ten years’ imprisonment and a fine of AED 100,000 to AED 5,000,000; aggravated cases attract a fine of AED 1,000,000 to AED 10,000,000. Financing of terrorism carries life imprisonment or not less than ten years, plus a fine of AED 1,000,000 to AED 10,000,000. Legal persons face fines of AED 5,000,000 to AED 100,000,000 under Article 27. Violations of suspicious transaction reporting obligations carry imprisonment and a fine of AED 100,000 to AED 1,000,000 under Article 28. Tipping off, disclosing a report or investigation to the subject, carries a fine of at least AED 50,000 under Article 29. Supervisory authorities are empowered by Article 17 to impose administrative penalties of AED 10,000 to AED 5,000,000 for compliance failures. For the full obligations framework under the current law, see Federal AML Laws and Executive Regulations in the UAE.

Cabinet Resolution No. (134) of 2025, December 2025

Cabinet Resolution No. 134 of 2025 is the executive regulation of Federal Decree-Law No. 10 of 2025. It provides the operational detail required to convert the primary law’s principles into specific procedural requirements and threshold obligations for supervised entities. Cabinet Resolution No. 134 of 2025 replaces Cabinet Resolution No. 10 of 2019, which had served as the executive regulation for the repealed Law 20 of 2018.

Article 1 introduces a number of defined terms not previously present in UAE AML legislation, including Commercial Gaming, Trust Protector, and Nominator, categories that reflect the expanding scope of the framework under international standards. Article 2 sets out fourteen categories of financial institution activity subject to the AML/CFT framework, providing a comprehensive definition of the population of regulated financial entities. Article 4 identifies six categories of virtual asset service provider activity, bringing VASPs comprehensively within the supervised population under this legislative instrument for the first time.

Article 3 defines DNFBP obligations with specific transaction thresholds. Commercial gaming operations trigger CDD obligations at AED 11,000. Dealers in precious metals and precious stones must apply CDD for occasional transactions of AED 55,000 or more. For financial institutions, Article 7 sets CDD trigger thresholds at AED 55,000 for occasional transactions and AED 3,500 for wire transfers; VASPs are subject to the same AED 3,500 wire transfer threshold. Beneficial ownership identification under Article 10 uses a threshold of 25 per cent shareholding or voting rights.

The Resolution also contains detailed provisions on CDD timing under Article 6, risk identification under Article 5, and the conditions under which entities may commence a business relationship before verification is complete under a risk-based approach. Taken together, Cabinet Resolution No. 134 of 2025 and Federal Decree-Law No. 10 of 2025 constitute the complete 2025 legislative architecture governing AML/CFT compliance in the UAE.

Unsure whether your business is in scope?

Our guide to who must comply with UAE AML regulations sets out the complete list of regulated entity categories and the obligations that apply to each.

Cabinet Resolution No. (71) of 2024, July 2024

Cabinet Resolution No. 71 of 2024 was issued on 8 July 2024. It regulates violations and administrative penalties applicable to designated non-financial businesses and professions that fall under the supervisory oversight of the Ministry of Justice and the Ministry of Economy (MoET). The Resolution’s scope of application, defined in Article 2, covers all DNFBPs under Ministry oversight who violate any provision of the AML Decree-Law, the executive regulation, or any implementing resolutions.

Article 3 empowers the Ministry to impose one or more of the administrative penalties available under Article 14 of the Decree-Law, to impose the administrative fines specified in the schedule annexed to the Resolution, or both, upon commission of any violation listed in that schedule. The schedule lists 41 violation categories. Fines range from AED 50,000 to AED 1,000,000. Selected examples from the schedule include: failure to establish policies and internal controls approved by senior management (AED 100,000-200,000, violation 1); failure to undertake required customer due diligence for transactions at or above AED 55,000 (AED 50,000-200,000, violation 9); failure to report suspicious transactions promptly to the Financial Intelligence Unit (AED 100,000-500,000, violation 22); and failure to freeze funds without prior notice upon a sanctions match (AED 500,000-1,000,000, violation 35).

Article 5 of Cabinet Resolution No. 71 of 2024 provides that the Ministry may double the administrative fine where a violation is repeated. Article 5, clause 3, further provides that imposition of a fine does not prevent the Ministry from also applying any other administrative sanction available under Article 14 of the primary Decree-Law. Cabinet Resolution No. 71 of 2024 repeals Cabinet Resolution No. 16 of 2021 under Article 8, updating the DNFBP penalty regime with a more detailed and higher-ceiling structure.

Cabinet Decision No. (109) of 2023, November 2023

Cabinet Resolution No. 109 of 2023, issued on 6 November 2023, establishes a comprehensive framework for identifying, recording, and disclosing the real beneficiaries of legal persons licensed or registered in the UAE. The Resolution aims to eliminate anonymity from corporate ownership structures, which the FATF has consistently identified as a primary vehicle for money laundering and terrorism financing. Cabinet Resolution No. 109 of 2023 repeals Cabinet Resolution No. 58 of 2020, which had established the earlier real beneficiary framework, under Article 22.

Article 5 defines the real beneficiary of a legal person as the natural person who owns or ultimately controls it through direct or indirect shareholding of 25 per cent or more of the capital, through voting rights of 25 per cent or more, or through the exercise of ultimate control by other means, including the right to appoint or remove the majority of board members. The Resolution establishes a cascading determination method: if no qualifying shareholder can be identified, the natural person exercising control through other means is treated as the real beneficiary; if no such person can be identified, the person holding the most senior management position is deemed the real beneficiary (Article 5, clause 6).

The procedural obligations are set out in Articles 8 to 11. Article 8 requires every legal person to establish and maintain a Real Beneficiary Register within 60 days of the Resolution’s implementation (or from the date of licensing, for newly established entities). Updates to the register must be made within 15 days of any change. A separate Partners or Shareholders Register must be maintained under Article 10, with the same update timeline. Article 11 obliges legal persons to submit the data in both registers to the relevant Registrar within the same 60-day period and to take reasonable measures to preserve these records from damage or loss. The Registrar is required under Article 13 to apply a risk-based approach to registered entities to ensure they are not misused for money laundering and terrorism financing.

Article 3 of the Resolution excludes companies wholly owned by the federal or local government, financial free zones, and entities with a government partner from the scope of the beneficial ownership disclosure obligations. This exemption reflects the different transparency and accountability mechanisms applicable to state-owned or government-linked entities.

Cabinet Resolution No. (132) of 2023, December 2023

Cabinet Resolution No. 132 of 2023, issued on 15 December 2023, sets out the administrative penalty regime for violations of Cabinet Resolution No. 109 of 2023. It gives the real beneficiary disclosure framework its enforcement mechanism and repeals Cabinet Resolution No. 53 of 2021 under Article 8. The Resolution applies to legal persons licensed or registered in the UAE, including in non-financial free zones, that violate the provisions of Cabinet Resolution No. 109 of 2023.

The penalty schedule annexed to the Resolution covers 15 categories of violations related to the real beneficiary and shareholder register obligations. The structure is graduated: a written notice requiring correction within a specified period on the first occurrence, escalating to a monetary fine on the second occurrence, and a higher fine on the third occurrence. Article 3, clause 2, grants the Registrar an additional power on the third offence: suspension of the violating entity’s commercial licence and closure of its commercial premises, pending payment of the fine and correction of the violation.

Fines under the schedule range from AED 5,000 (second-time failure to disclose the details of shares issued in the names of board members, per Article 11/6 of Cabinet Resolution No. 109 of 2023) to AED 100,000 (third-time failure to create and maintain a Real Beneficiary Register at all, per Article 8/1 of Cabinet Resolution No. 109 of 2023). Failure by a liquidator to maintain records for five years after dissolution of a legal person carries a flat fine of AED 100,000 on first occurrence (violation 15, citing Article 11/8 of Cabinet Resolution No. 109 of 2023). Article 4 of Cabinet Resolution No. 132 of 2023 reserves to the Cabinet the power to amend the fine amounts by addition, deletion, or amendment.

Cabinet Resolution No. (74) of 2020, October 2020

Cabinet Resolution No. 74 of 2020 establishes the UAE’s framework for implementing targeted financial sanctions (TFS) and administering terrorist designation lists. It gives domestic legal effect to a series of UN Security Council Resolutions: 1267 (1999) and its successors 1988 and 1989 (both 2011), which govern the Al-Qaeda and Taliban sanctions regimes respectively; 1718 (2006), which addresses North Korea’s weapons of mass destruction programme; and 2231 (2015), which concerns Iran’s nuclear activities. Cabinet Resolution No. 74 of 2020 replaces Cabinet Resolution No. 20 of 2019.

Article 3 of the Resolution sets out the functions of the Supreme Council for National Security in relation to local terrorist lists, including the procedures for nomination, addition, amendment, and de-listing of designated persons and entities. Article 15 is the operational core: it requires all financial institutions, DNFBPs, and other obligated entities to freeze, without prior notice or delay, the funds and other assets of any person or entity appearing on the UN Consolidated List or the national terrorist list, as soon as they become aware of a match. The phrase ‘without delay’ in Article 15 does not specify a time period in the Resolution’s text; the 24-hour operational standard for effecting a freeze is set out in guidance published by the Executive Office for Control and Non-Proliferation, which supervises compliance with the targeted financial sanctions regime.

The administrative consequence of failing to comply with the TFS obligations of Cabinet Resolution No. 74 of 2020 is captured in Cabinet Resolution No. 71 of 2024, which lists violations 33 to 41 in its schedule as explicitly referencing the 2020 Resolution. Relevant violations include: failure to register with the Executive Office for Control and Non-Proliferation (AED 50,000-1,000,000, violation 33); failure to screen databases against designated lists on an ongoing basis (AED 50,000-1,000,000, violation 34); failure to freeze matched funds without prior warning (AED 500,000-1,000,000, violation 35); and failure to report promptly to the Executive Office upon determining any match (AED 100,000-1,000,000, violation 38).

Federal Law No. (7) of 2014 Combating Terrorism Crimes

Federal Law No. 7 of 2014 Concerning Combating Terrorism Crimes and their Financing is the foundational counter-terrorism statute in the UAE. It was enacted before the current AML primary law and continues in force alongside Federal Decree-Law No. 10 of 2025, which preserves prior legislation not specifically repealed or contradicted (Article 41 of Law 10/2025). Federal Law No. 7 of 2014 establishes the criminal framework within which terrorism financing is prosecuted, distinct from the AML framework established by Law 10/2025.

The law defines a range of key concepts, including terrorist crimes, terrorist purposes, terrorist consequences, and terrorist organisations. Article 5 addresses the seizure of vehicles and transport used in the commission of terrorist operations, carrying a maximum sentence of life imprisonment. Article 29 addresses the direct and indirect financing of terrorism, providing for life imprisonment or a term of not less than ten years for persons convicted of terrorism financing offences. Article 34 criminalises the promotion of terrorist organisations, activities, and ideology, imposing a penalty of life imprisonment and a fine ranging from AED 2,000,000 to AED 5,000,000.

The practical significance of Federal Law No. 7 of 2014 for financial institutions and DNFBPs is that it defines the predicate criminal conduct against which their AML/CFT controls must be calibrated. The obligation under Article 18 of Federal Decree-Law No. 10 of 2025 to report suspicion of terrorism financing to the Financial Intelligence Unit operates in conjunction with the criminal offences established in Federal Law No. 7 of 2014. A compliance programme that correctly identifies and reports indicators of terrorism financing is, in effect, providing intelligence relevant to enforcement under both instruments simultaneously.

Federal Law No. 7 of 2014 remains the primary legal basis for terrorism-related prosecutions in the UAE alongside Federal Decree-Law No. 10 of 2025. Its persistence in the legislative framework, even as the AML primary law was replaced in its entirety in 2025, reflects the UAE’s commitment to maintaining a stable and comprehensive counter-terrorism legal framework as a foundation for the preventive compliance obligations layered on top of it.

Speak to an AML compliance specialist

AML UAE provides practical compliance guidance and advisory services tailored to the UAE regulatory framework. Whether you are a financial institution, DNFBP, or VASP, our specialists can help you navigate your obligations under the 2025 legislative framework.

Conclusion

The seven instruments examined in this article trace a coherent legislative trajectory. Federal Law No. 7 of 2014 established the criminal framework for terrorism and terrorism financing. Cabinet Resolution No. 74 of 2020 operationalised international sanctions obligations, introducing a real-time screening and freeze regime. Cabinet Resolutions No. 109 and No. 132 of 2023 addressed the transparency gap in corporate ownership by mandating beneficial ownership registers and attaching a penalty framework. Cabinet Resolution No. 71 of 2024 updated the DNFBP administrative penalty schedule, raising fine ceilings and introducing a doubling mechanism for repeat violations. Federal Decree-Law No. 10 of 2025 and Cabinet Resolution No. 134 of 2025 completed the current reform cycle, consolidating and updating the entire framework and bringing virtual assets and commercial gaming fully within the regulated population.

Three themes emerge from this history. First, the shift from crime control to prevention: the framework has moved steadily away from post-facto criminalisation towards ongoing, risk-based obligations that attach before any suspicious activity occurs. Second, the broadening of the regulated population: from banks and financial institutions in the early framework, through DNFBPs and real estate brokers, to virtual asset service providers and commercial gaming operators under the 2025 legislation. Third, the deepening of international alignment: each legislative update has been driven at least in part by FATF standards and UN Security Council obligations, a dynamic that will continue to generate further reform as international standards evolve.

For practitioners, the key starting points are the primary law and its executive regulation: Federal Decree-Law No. 10 of 2025 and Cabinet Resolution No. 134 of 2025. For a guide to current compliance obligations, see Federal AML Laws and Executive Regulations in the UAE. For the full list of regulated entities, see Who Must Comply with UAE AML Regulations. The National Anti-Money Laundering Committee website publishes regulatory guidance and updates as they are issued.

Status of Key Legislative Instruments

The table below sets out the current status of each instrument discussed in this article, whether it remains in force, has been replaced, or has been repealed. Practitioners should confirm the current position against the UAE Legislation Portal before relying on any instrument for compliance purposes.

| Instrument | Status | Notes |

|---|---|---|

| Federal Decree-Law No. 10 of 2025 | In Force | Current primary AML/CFT statute. In force from October 2025 (Article 42). |

| Cabinet Resolution No. 134 of 2025 | In Force | Current executive regulation for Law 10/2025. Replaces CR 10/2019. |

| Cabinet Resolution No. 71 of 2024 | In Force | Current DNFBP administrative penalty schedule. Replaces CR 16/2021. |

| Cabinet Resolution No. 109 of 2023 | In Force | Current real beneficiary framework. Replaces CR 58/2020. |

| Cabinet Resolution No. 132 of 2023 | In Force | Penalty schedule for CR 109/2023 violations. Replaces CR 53/2021. |

| Cabinet Resolution No. 74 of 2020 | In Force | TFS and sanctions framework. Replaces CR 20/2019. Not repealed by 2025 law. |

| Federal Law No. 7 of 2014 | In Force | Counter-terrorism statute. Preserved by Article 41 of Law 10/2025. |

| Federal Decree-Law No. 20 of 2018 | Repealed | Repealed by Article 41 of Federal Decree-Law No. 10 of 2025. |

| Cabinet Resolution No. 10 of 2019 | Replaced | Executive regulation for Law 20/2018. Replaced by CR 134/2025. |

| Cabinet Resolution No. 16 of 2021 | Replaced | Prior DNFBP penalty schedule. Replaced by CR 71/2024 (Article 8). |

| Cabinet Resolution No. 58 of 2020 | Replaced | Prior real beneficiary framework. Replaced by CR 109/2023 (Article 22). |

| Cabinet Resolution No. 53 of 2021 | Replaced | Prior penalty schedule for UBO violations. Replaced by CR 132/2023 (Article 8). |

| Cabinet Resolution No. 20 of 2019 | Replaced | Prior TFS framework. Replaced by CR 74/2020. |

Frequently Asked Questions

When did the UAE first introduce AML regulations?

The UAE has maintained a formal AML legislative framework for more than two decades. The most recent iteration of the primary AML statute, Federal Decree-Law No. 10 of 2025, expressly repeals Federal Decree-Law No. 20 of 2018 under Article 41, which was the immediately preceding primary AML law. The preambles of Cabinet Resolutions 109/2023, 71/2024, and 134/2025 each reference Law 20 of 2018 and its executive regulation, Cabinet Resolution No. 10 of 2019, as the predecessor instruments they build upon or replace. The seven instruments examined in this article cover the period from 2014 to 2025, representing the modern, internationally aligned phase of UAE AML regulation.

What is the relationship between Federal Decree-Law No. 10 of 2025 and earlier AML laws?

Federal Decree-Law No. 10 of 2025 is the current primary AML/CFT legislation. Article 41 repeals Federal Decree-Law No. 20 of 2018 and any provision that contradicts the new law. However, the same article preserves circulars, resolutions, and decisions issued under the 2018 law to the extent they do not conflict with the 2025 statute or its executive regulation, Cabinet Resolution No. 134 of 2025. This means that supervisory guidance, sector-specific circulars, and administrative decisions issued by the CBUAE, CMA, and other supervisory authorities under the old framework generally remain valid, unless a specific conflict exists with the new legislation. Practitioners should review each item of existing guidance against the new law to confirm its continued applicability.

Why has the UAE updated its AML framework so many times?

Frequent legislative updates reflect two primary pressures: evolving international standards and expanding domestic risk categories. The FATF Recommendations are reviewed periodically, and member jurisdictions are expected to align their laws accordingly. The preambles of Cabinet Resolutions 74/2020, 109/2023, 71/2024, and others reference and supersede the instruments that preceded them, illustrating the iterative nature of reform. New risk categories, virtual assets, commercial gaming, trust arrangements, and complex corporate structures require specific legislative responses as they grow in economic significance. The governance architecture of Law 10/2025, including the National Committee under Article 13 and the Supreme Committee under Article 12, is designed to ensure continuous monitoring and timely legislative updating.

Which entities must comply with UAE AML regulations?

The UAE AML framework applies to three broad categories of entities. Financial institutions are defined across fourteen activity types listed in Article 2 of Cabinet Resolution No. 134 of 2025. Designated non-financial businesses and professions (DNFBPs) are defined in Article 3 of the same Resolution and include: commercial gaming operators, real estate brokers, dealers in precious metals and precious stones, lawyers, accountants, notaries, and trust and company service providers. Virtual asset service providers are defined across six activity types in Article 4 of Cabinet Resolution No. 134 of 2025. For a complete breakdown with entity-specific obligations, see Who Must Comply with UAE AML Regulations.

How do the DFSA, FSRA, CBUAE, and CMA differ in their AML oversight roles?

Each authority supervises a distinct population of entities. The Central Bank of the UAE (CBUAE) supervises financial institutions licensed on the UAE mainland, including banks, exchange houses, finance companies, and payment service providers. The Dubai Financial Services Authority (DFSA) supervises financial institutions within the Dubai International Financial Centre (DIFC), a financial free zone that operates under its own legal framework. The Financial Services Regulatory Authority (FSRA) supervises financial institutions within the Abu Dhabi Global Market (ADGM), another financial free zone with a separate regulatory regime. The Capital Markets Authority (CMA) supervises securities and investment businesses. Federal Decree-Law No. 10 of 2025 designates supervisory authorities generically in Article 16 and empowers them to impose administrative penalties of AED 10,000 to AED 5,000,000 per Article 17, with each authority applying these powers within its own supervised population.

What changed for DNFBPs under the 2025 AML law?

The most significant changes for DNFBPs under the 2025 legislative package concern scope, thresholds, and the penalty framework. Cabinet Resolution No. 134 of 2025 introduces commercial gaming as a new DNFBP category under Article 3, with a CDD threshold of AED 11,000 per transaction. The AED 55,000 threshold for precious metals and precious stones dealers is retained. Article 3 also defines the activities of real estate brokers, lawyers, accountants, notaries, and trust and company service providers in updated terms consistent with international standards. The administrative penalty schedule applicable to DNFBPs under Ministry of Justice and MoET oversight was updated by Cabinet Resolution No. 71 of 2024, which replaced the 2021 penalty schedule, raised fine ceilings to AED 1,000,000, and introduced a doubling mechanism for repeated violations under Article 5.

When was the UAE Financial Intelligence Unit (FIU) established?

The Financial Intelligence Unit has operated within the UAE’s AML framework since before the 2025 reforms. It functioned under Federal Decree-Law No. 20 of 2018 and was already embedded within the Central Bank of the UAE. Federal Decree-Law No. 10 of 2025 formally re-embeds and significantly strengthens the FIU under Article 11, reinforcing its mandate and conferring new active powers. Under Law 10/2025, the FIU retains its analytical functions, receiving and disseminating suspicious transaction reports, and gains new protective powers under Article 5: the authority to order the suspension of suspicious transactions for up to ten working days and to freeze related assets for up to thirty days pending referral to the competent authority. The expansion of the FIU’s powers beyond analysis into active intervention is one of the most significant institutional developments in the current reform cycle.

Found this article useful?

If this guide helped you understand the history of UAE AML regulations, a Google review would be appreciated. Your feedback helps other compliance professionals find reliable resources.

Legal Disclaimer: This article is provided for general information and educational purposes only and does not constitute legal advice. The information reflects the legislative position as of April 2026. Laws and regulations may change. For advice specific to your situation, consult a qualified legal or compliance professional.

Share via :

About the Author

Pathik Shah

FCA, CAMS, CISA, CS, DISA (ICAI), FAFP (ICAI)

Pathik is an ACAMS-certified AML consultant specialising in governance, risk, and compliance for regulated entities in the UAE. He brings over 28 years of experience, with 1,000+ hours of AML training and 200+ advisory engagements across DNFBPs, VASPs, and FIs. He supports businesses in aligning with AML/CFT requirements from the CBUAE, DFSA, MoET, MoJ, VARA, CMA, FSRA, and FATF. Known for translating complex regulations into audit-ready procedures, Pathik enables operational clarity and compliance readiness.

Reach Out to Pathik